Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

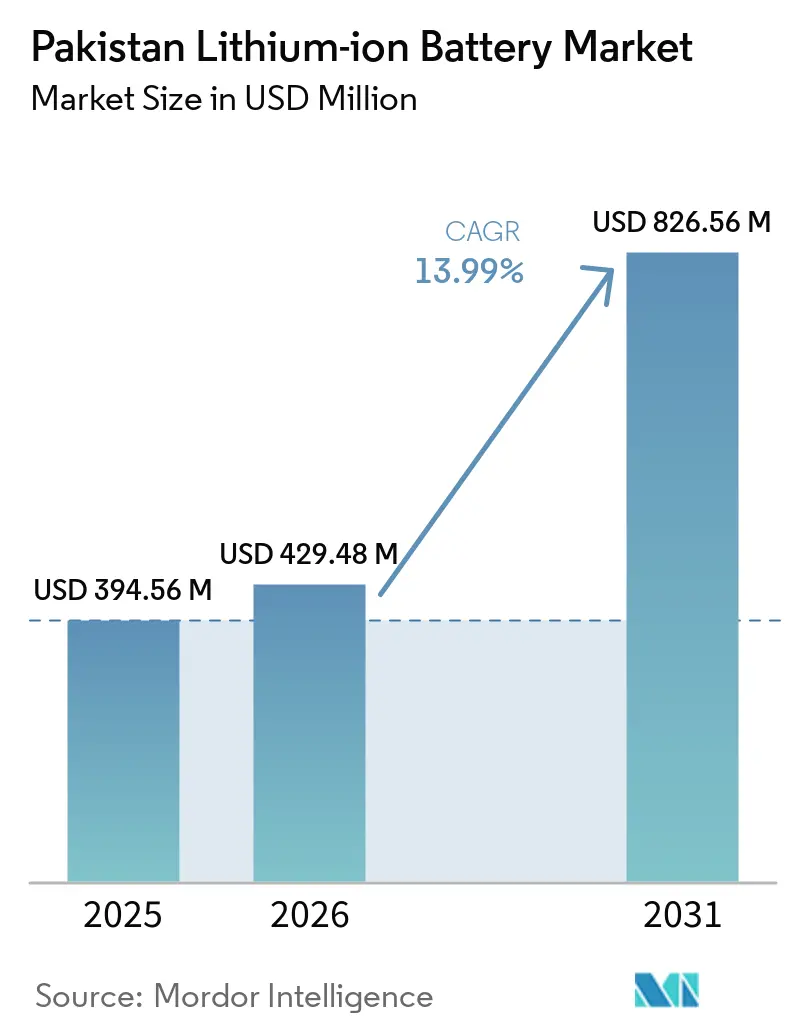

| Base Year Market Size (2025) | USD 394.56 Million |

| Market Size (2026) | USD 429.48 Million |

| Market Size (2031) | USD 826.56 Million |

| Growth Rate (2026 - 2031) | 13.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Lithium-ion Battery Market Analysis by Mordor Intelligence

The Pakistan Lithium-ion Battery Market size is projected to be USD 394.56 million in 2025, USD 429.48 million in 2026, and reach USD 826.56 million by 2031, growing at a CAGR of 13.99% from 2026 to 2031.

Policy certainty around the National Electric Vehicles Policy, sharp reductions in global cell costs, and a rooftop-solar boom are expanding demand across mobility, telecom, and commercial-and-industrial (C&I) segments. A 45% power-tariff cut for public charging announced in January 2025 has lowered the total cost of ownership for fleet operators, while rooftop solar paired with batteries helps businesses hedge against electricity prices that have climbed 155% since 2021. Imports rose to 1.25 GWh in 2024 and are projected to hit 8.75 GWh by 2030, underscoring the momentum behind distributed storage. Local assembly initiatives by Atom Power, Alaska Battery, and Topak Pakistan are beginning to shorten lead times and reduce landed costs despite a 48% import-duty burden. Together, these shifts are reshaping the competitive playbook inside the Pakistan lithium-ion battery market.[1]Pakistan Finance Division, “Monthly Economic Update April 2025,” finance.gov.pk

Key Report Takeaways

- By chemistry, lithium iron phosphate captured 45.9% of 2025 revenue and is projected to expand at a 15.5% CAGR through 2031, making it both the largest and the fastest-growing segment within the Pakistan lithium-ion battery market.

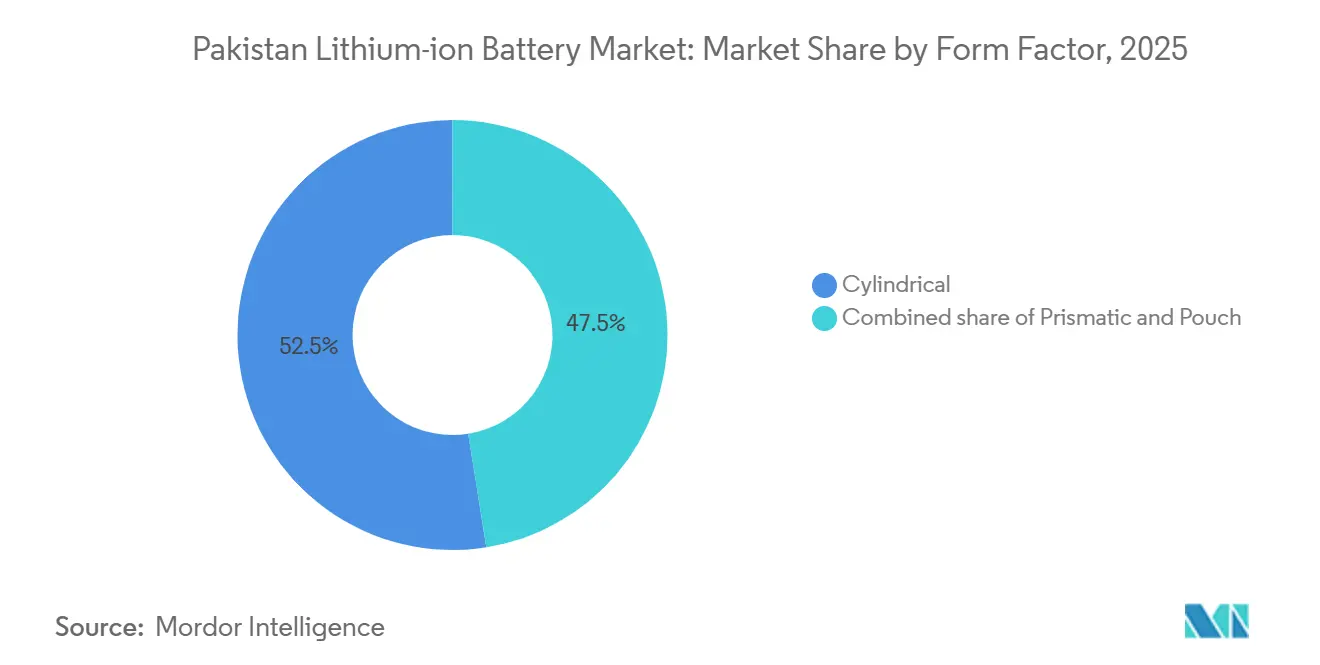

- By form factor, cylindrical cells commanded 52.5% of 2025 sales, whereas pouch cells are on track for a 17.3% CAGR to 2031, the highest growth rate among formats.

- By capacity, the 3,000-10,000 mAh band accounted for 40.2% of the Pakistan lithium-ion battery market share in 2025 and is expected to grow at 15.9% a year to 2031.

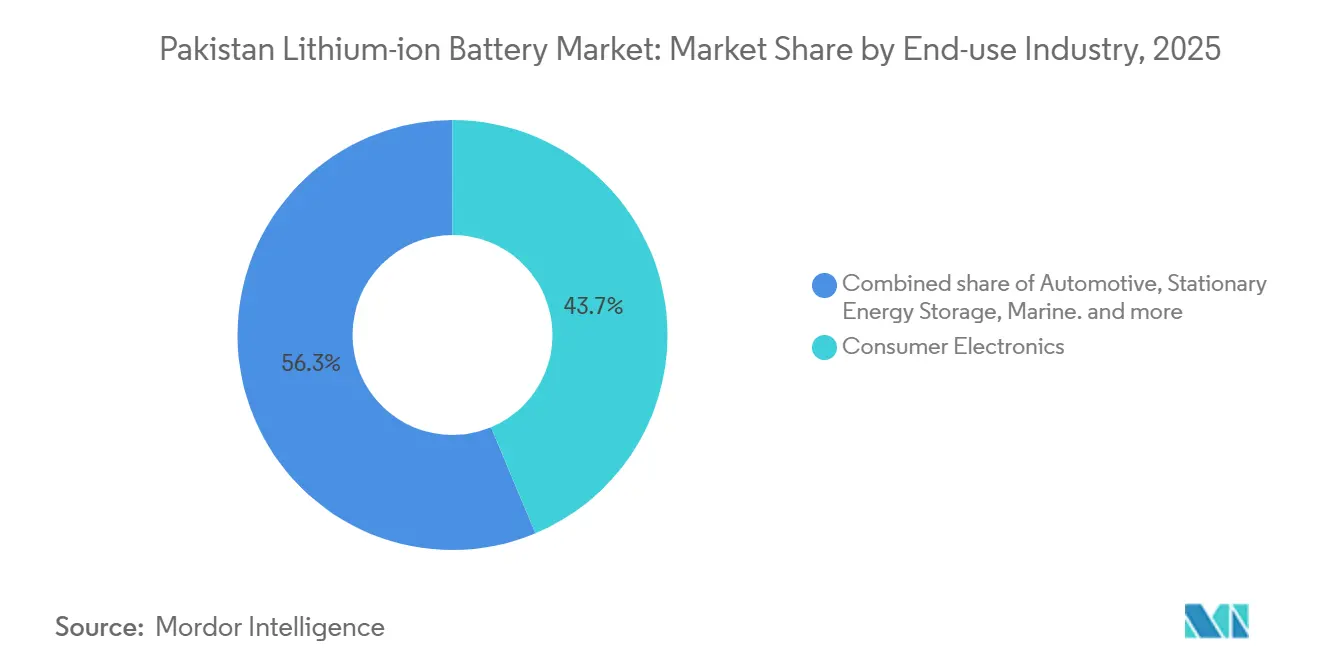

- By end-use industry, consumer electronics led with 43.7% of 2025 revenue; automotive is the fastest-rising application with a 20.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Pakistan Lithium-ion Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National EV policy purchase & tax incentives | +3.2% | Karachi, Lahore, Islamabad | Medium term (2-4 years) |

| Declining global Li-ion pack costs | +2.8% | Nationwide | Short term (≤2 years) |

| Rooftop-solar + BESS boom | +3.5% | Punjab, Sindh industrial hubs | Medium term (2-4 years) |

| Domestic cell/pack assembly initiatives | +1.4% | Karachi, Lahore manufacturing belts | Long term (≥4 years) |

| Telecom base-station shift to LiFePO₄ | +1.6% | Rural KPK and Balochistan tower clusters | Medium term (2-4 years) |

| Cross-border e-commerce surge | +1.0% | Urban centers with dense logistics networks | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

National EV Policy Purchase & Tax Incentives

The revised National Electric Vehicles Policy targets 30% electric penetration by 2030, anchoring demand visibility for automakers and battery suppliers. A 45% reduction in power tariffs for charging stations, effective January 2025, slashed operating costs for fleet managers and ride-hailing operators.[2]Ministry of Energy, “Revised National EV Policy 2025-30,” arabnews.com BYD and Hub Power plan 128 DC fast chargers over three years, with 50 units slated for installation before December 2025, mitigating range anxiety for early adopters. Passenger-vehicle production rebounded 37-87% year-on-year in April 2025, signaling a willing customer base as electric options become price-competitive. Import-duty exemptions on completely-knocked-down kits are accelerating local pack assembly at Port Qasim from mid-2026. However, the absence of a scrappage scheme means 2- and 3-wheelers, over 30 million units, remain largely unaddressed, tempering the policy’s reach.

Declining Global Li-ion Pack Costs

Average pack prices fell to USD 139/kWh in 2024 and are on track to breach the USD 100/kWh mark by 2026, reflecting cathode oversupply and efficiency gains. Pakistan, which imports nearly all of its cells, experiences an almost one-for-one pass-through to local pricing. LG Energy Solution reported a 12% year-on-year drop in cell ASPs during 1H 2024, enabling solar-plus-storage systems to reach sub-4-year payback periods for C&I customers. Imports grew to 1.25 GWh in 2024 and, at the present trajectory, could reach 8.75 GWh by 2030.[3]Institute for Energy Economics and Financial Analysis, “Pakistan Battery Imports Dashboard 2025,” ieefa.org Yet a 48% combined duty and sales tax still pushes a 10 kWh residential system to roughly PKR 1 million, restraining uptake among households.

Rooftop-Solar + BESS Boom in C&I & Residential

C&I users added more than 2 GW of rooftop PV in 2024, with batteries increasingly paired to buffer outages and optimize time-of-use tariffs. A textile mill in Lahore cut monthly bills by 40% after installing a 1 MW PV array plus a 500 kWh lithium iron phosphate pack. Huawei’s LUNA2000 storage platform, introduced in March 2025, scales from 107 kWh to 215 kWh and integrates directly with existing inverters.[4]Huawei Technologies Co., “1,000-Site LiFePO₄ Retrofit Case Study,” huawei.com Growatt’s H-Series all-in-one system, launched in February 2024, offers 5.5-33 kWh modularity and dual MPPT functionality. Rising electricity tariffs, already above PKR 50 per kWh for many commercial users, continue to drive the battery value proposition, although residential adoption is held back by upfront capital requirements that the State Bank of Pakistan is still evaluating for concessional-loan support.

Domestic Cell/Pack Assembly Initiatives

Atom Power rolled out the nation’s first locally assembled lithium-ion batteries in December 2024, with in-house cylindrical-cell production scheduled for Q2 2025. Alaska Battery added a graphite-battery line aimed at industrial UPS and solar applications, while Topak Pakistan expanded LiFePO₄ module output for inverter OEMs. The National Tariff Policy 2025-30 proposes phasing out 20% of duties on key inputs, a move that could bring locally assembled packs within 5-7% of import parity if enacted. BYD’s Port Qasim project will produce 25,000 packs annually from 2026, with export potential to right-hand-drive markets in South Asia and the Gulf. Nevertheless, local value addition is still below 15%, as cathodes, separators, and electrolytes remain fully imported.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import duties & sales taxes | -2.1% | Nationwide | Medium term (2-4 years) |

| Grid-integration & tariff uncertainty for BESS | -1.5% | Punjab, Sindh industrial corridors | Medium term (2-4 years) |

| Limited skills, testing & certification labs | -0.9% | Karachi, Lahore manufacturing clusters | Long term (≥4 years) |

| Geopolitical lithium-supply risks | -0.7% | Gilgit-Baltistan, Balochistan prospects | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Import Duties & Sales Taxes Keep Upfront Costs High

Finished battery packs face a 48% tax burden, 20% customs duty, 8% additional, 3% regulatory, and 17% sales tax, lifting a 10 kWh residential system to PKR 1.2 million (USD 4,200) versus USD 2,800 in peer markets. Although the Tariff Policy 2025-30 recommends trimming extra duties, the Federal Board of Revenue has yet to publish an implementation schedule, clouding price forecasts for distributors. Smaller installers, lacking working-capital buffers, pass the full uplift to end users, stunting residential adoption. Exide Pakistan’s LiFePO₄ modules, listed at PKR 70,000-265,000, illustrate the cost premium relative to neighboring markets. Many households, therefore, continue relying on diesel generators or lead-acid UPS units that demand lower upfront expenditure despite higher lifetime costs.

Grid-Integration & Tariff Uncertainty for BESS

The National Electric Power Regulatory Authority has not finalized net-metering rules for systems above 1 MW, forcing developers to negotiate bespoke agreements that often exclude compensation for grid services. Lucky Cement’s 22.7 MWh system in Pezu, commissioned in July 2025, opted for behind-the-meter operation to bypass regulatory ambiguities, forfeiting ancillary-service revenue that could have improved project ROI. Absence of standardized interconnection protocols delays bankable PPAs and pushes financiers to price in additional risk. Meanwhile, IMF-mandated subsidy withdrawals introduce tariff volatility, narrowing arbitrage windows that underpin storage economics. Lack of capacity-payment or demand-response markets further limits revenue stacking, confining BESS uptake to self-consumption models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemistry: LFP Anchors Stationary and Fleet Demand

The Pakistan lithium-ion battery market size attributed to lithium iron phosphate (LFP) reached USD 181 million in 2025, translating into a dominant 45.9% slice of the overall revenue pie and a 15.5% forecast CAGR through 2031. Cost leadership, benign thermal behavior, and strong cycle life underpin its position in stationary energy storage and commercial-vehicle batteries. Huawei’s LUNA2000, Hithium’s HeroEE, and Topak’s solar-inverter modules all leverage LFP, reinforcing supply security and local pack-assembly skills. The chemistry also aligns with safety codes for telecom towers replacing diesel gensets. Nickel-rich chemistries retain niche status in premium EVs due to higher energy density, while lithium cobalt oxide remains prevalent in imported consumer electronics that seldom see local cell procurement. Limited domestic cathode production keeps input costs coupled to Chinese spot prices, but expected duty relief on raw materials could widen LFP’s cost advantage over nickel-based alternatives inside the Pakistan lithium-ion battery market.

The chemistry mix is unlikely to shift dramatically before 2031. Domestic assemblers prefer cylindrical 21700 LFP cells because they marry performance with low scrap rates. BYD’s prismatic Blade Battery, slated for local EV production starting mid-2026, could marginally lift prismatic share, but the overall headroom for LFP remains substantial. For high-energy-density segments, long-range sedans, premium SUVs, NMC, and NCA chemistries will continue to be imported as complete packs, given Pakistan’s nascent thermal-management ecosystem. Regulatory moves by PSQCA to align fire-safety codes with IEC 62660 are expected to favor LFP for urban delivery fleets, bolstering its already outsized contribution to the Pakistan lithium-ion battery market.

By Form Factor: Pouch Gains in Portables, Cylindrical Holds Industrial Base

Cylindrical cells generated 52.5% of 2025 revenue, anchored by 18650 and 21700 formats that dominate power tools, UPS systems, and light-electric two-wheelers. Their mature supply chain, automated welding, and favorable thermal properties make them a low-risk choice for local assemblers. Conversely, pouch cells, favored by smartphone and wearable OEMs, are registering a rapid 17.3% CAGR and will steadily nibble share through 2031 as local assembly of mobile devices scales up. Prismatic formats sit between the two, benefiting from automotive traction packs and mid-scale C&I storage.

Volume growth in wearables and ultra-thin laptops pushes battery-density requirements that only pouch cells meet, but Pakistan remains largely an importer of finished devices, so most pouch-cell demand is indirect. BYD’s planned Blade Battery integration in locally assembled EVs may elevate prismatic penetration, yet cylindrical formats are expected to sustain a numerical lead through 2031 thanks to telecom-backup retrofits and solar-hybrid inverter packs. The National Energy Efficiency and Conservation Authority has yet to issue form-factor-specific safety protocols, leaving voluntary adherence to IEC standards as the primary compliance pathway for actors in the Pakistan lithium-ion battery market.

By Capacity Band: Mid-Range Cells Dominate Consumer and Light Industrial Use

Cells rated 3,000-10,000 mAh generated 40.2% of 2025 revenue and will sustain a 15.9% CAGR, tightly aligned with demand for power banks, e-bikes, and cordless tools. The sweet-spot capacity marries runtime with form-factor flexibility, enabling ease of integration into modular packs. Sub-3,000 mAh cells remain tied to smartphones and IoT devices whose battery procurement happens offshore, limiting local value capture. In contrast, the 10,000-60,000 mAh tier is expanding on the back of telecom tower retrofits and small commercial UPS units.

Large-format cells above 60,000 mAh flow mainly into grid-scale systems like Lucky Cement’s 22.7 MWh project. However, given regulatory uncertainty and limited EPC capacity, this category’s share will stay modest in the Pakistan lithium-ion battery market. Mid-range packs also benefit from standardized BMS architectures, allowing assemblers such as Topak Pakistan to meet varied OEM requirements without bespoke engineering, thereby compressing lead times and lowering cost overhead.

By End Use: Automotive Surge Challenges Consumer Electronics Lead

Consumer electronics held 43.7% of 2025 sales, fueled by sustained smartphone adoption and a surge in wearables and accessories ordered via cross-border e-commerce. Yet the automotive vertical, starting from a smaller base, is racing ahead with a 20.2% forecast CAGR as BYD-Hub Power, ADEN-Malik, and other ventures bring local EV assembly online. A projected 128 fast chargers by 2025 and 3,000 chargers by 2026 are eroding range anxiety, while duty-exempt CKDs lower sticker prices enough to target mid-income buyers.

C&I stationary storage is the second-fastest expanding segment, driven by rooftop solar arbitrage and outage mitigation. Projects like Lucky Cement’s Pezu facility exemplify the scale at which industrial users are replacing diesel gensets. Telecom upgrades add a steady flow of mid-sized orders, whereas aerospace, marine, and defense remain niche due to limited domestic manufacturing. As charging infrastructure densifies and policy incentives firm up, automotive demand could surpass consumer electronics before 2031, altering the demand mix inside the Pakistan lithium-ion battery market.

Geography Analysis

Provincial demand reflects Pakistan’s industrial map. Punjab and Sindh jointly account for over two-thirds of installations because they host the bulk of textile mills, food processors, and logistics hubs seeking to hedge against grid instability. Karachi alone, with its port and manufacturing estates, concentrates more than 35% of rooftop-solar-plus-storage deployments, aided by preferential financing from local banks. Lahore and Faisalabad follow, driven by textile clusters that require uninterrupted power to avoid fabric wastage. Khyber Pakhtunkhwa’s share is rising due to telecom-tower retrofits in mountainous terrain where diesel logistics are costly; Huawei’s 1,000-site LiFePO₄ rollout exemplifies the strategy. Balochistan records the slowest uptake because of sparse population and limited grid coverage, although planned mining exploration could catalyze future demand for off-grid storage.

Urban centers dominate EV adoption. Karachi, Lahore, and Islamabad are projected to host 75% of the first wave of 128 DC fast chargers, making them focal markets for the Pakistan lithium-ion battery market size tied to mobility. Inter-city corridors, notably the Karachi-Hyderabad-Sukkur motorway, will see clusters of high-power chargers that demand large-format prismatic packs for buffer storage. Rural uptake remains limited by lower purchasing power and long charger-to-vehicle ratios, yet electric two-wheelers could gain traction as duty exemptions trickle down. Grid-tied C&I storage spreads fastest in Punjab’s industrial estates, where tariff differentials create lucrative arbitrage windows; Sindh’s coastal humidity, however, necessitates robust thermal management and conformal coatings, slightly raising system costs.

Government policy diverges by province. Punjab offers a 50% property-tax rebate for buildings installing solar-plus-storage, accelerating the local Pakistan lithium-ion battery market. Sindh’s energy department provides net-metering approvals within 45 days, reducing soft-cost friction. Khyber Pakhtunkhwa channels Universal Service Fund subsidies toward off-grid telecom sites, indirectly boosting battery demand. Balochistan focuses on mini-grids for remote communities, but harsher environmental conditions and security concerns add logistical hurdles. Taken together, geographic disparities inform targeted sales strategies, with OEMs prioritizing Punjab and Sindh for volume and KPK for high-margin, service-oriented contracts.

Competitive Landscape

Global giants continue to supply cells and turnkey modules while local firms scale pack assembly, positioning the Pakistan lithium-ion battery market at a moderate concentration level. CATL delivered Pakistan’s largest industrial BESS at Lucky Cement’s Pezu plant in July 2025, showcasing its capability to integrate 22.7 MWh of prismatic LFP cells into harsh desert climates. BYD, leveraging vertical integration, is setting up 25,000-unit annual EV capacity at Port Qasim from mid-2026. LG Energy Solution and Samsung SDI remain key suppliers to telecom and UPS assemblers, although neither has announced local production.

Domestic players capture downstream value. Atom Power began cell assembly in Karachi and plans on-shoring of graphite purification, while Alaska Battery targets industrial UPS niches with its graphite-enhanced modules. Topak Pakistan supplies OEM inverter companies with 21700-based LiFePO₄ packs and offers in-country maintenance, giving it a service-led advantage. Hithium’s August 2025 distribution deal with Imperial Electric secures up to 1 GWh of residential and C&I systems, extending the Chinese firm’s footprint into Pakistan’s outage-prone grid.

White-space opportunities lie in mid-scale (100-500 kWh) C&I storage, where textile mills and data centers lack turnkey EPC options. Additionally, the Pakistan lithium-ion battery industry faces a skills gap in BMS software and safety testing; companies offering training and certified labs could capture non-hardware revenue streams. Government adoption of IEC standards without establishing local labs elongates certification cycles, creating an opening for joint ventures specializing in compliance services. As more OEMs commit to local EV assembly, the bargaining power of cell suppliers may tighten, pushing domestic firms to pursue partial upstream integration to secure LFP cathode powder and separators.

Pakistan Lithium-ion Battery Industry Leaders

CATL

BYD

LG Energy Solution

Samsung SDI

Topak Pakistan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Lucky Motors partnered with GAC Group to introduce electric vehicles (EVs) in Pakistan, with plans to commence local EV assembly by December 2026. The company also announced that it is evaluating domestic lithium-ion battery manufacturing as part of Pakistan's developing EV ecosystem.

- April 2026: EV Technologies revealed that Pakistan's first lithium-ion battery manufacturing plant, located in Karachi's Korangi Industrial Area, is scheduled to begin production in 2026. The facility will initially produce batteries for e-bikes, e-scooters, EVs, and energy storage applications. This initiative aligns with Pakistan's proposed National Lithium-Ion Battery Manufacturing Policy 2026–31.

- January 2026: Pakistan introduced a new policy framework aimed at localizing lithium-ion battery production. The policy outlines phased localization targets, tariff reforms, recycling guidelines, safety standards, and incentives to attract private investment. The government selected Lithium Iron Phosphate (LFP) chemistry for initial localization due to its safety and cost-effectiveness.

- January 2026: Treet Corporation announced its entry into Pakistan's lithium-ion battery market through partnerships with Chinese manufacturers. The company plans to start with imported battery systems and gradually transition to local assembly and the development of battery management systems (BMS) in Pakistan.

Pakistan Lithium-ion Battery Market Report Scope

Li-ion batteries, rechargeable energy storage devices, generate electrical power by moving lithium ions between a negative anode and a positive cathode through an electrolyte. Renowned for their high energy density, lightweight nature, and longevity, Li-ion batteries efficiently store and release energy, powering most portable electronics, electric vehicles, and other modern devices, with the process reversing during charging.

The Pakistan lithium-ion battery market is segmented by product type, form factor, power capacity, and end-use industry. By product type, the market is segmented into lithium cobalt Oxide, lithium iron phosphate, lithium nickel manganese cobalt, lithium nickel cobalt aluminium, lithium manganese oxide, and lithium titanate. By form factor, the market is segmented into cylindrical, prismatic, and pouch. By power capacity, the market is segmented into up to 3,000 mAh, 3,000-10,000 mAh, 10,000-60,000 mAh, and above 60,000 mAh. By end-use industry, the market is segmented into automotive, consumer electronics, industrial and power tools, stationary energy storage, aerospace and defense, and marine. Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt (NMC) |

| Lithium Nickel Cobalt Aluminium (NCA) |

| Lithium Manganese Oxide (LMO) |

| Lithium Titanate (LTO) |

By Form Factor

| Cylindrical |

| Prismatic |

| Pouch |

By Power Capacity

| Up to 3,000 mAh |

| 3,000 to 10,000 mAh |

| 10,000 to 60,000 mAh |

| Above 60,000 mAh |

By End-use Industry

| Automotive (EV, HEV, PHEV) |

| Consumer Electronics |

| Industrial and Power Tools |

| Stationary Energy Storage |

| Aerospace and Defense |

| Marine |

| By Product Type | Lithium Cobalt Oxide (LCO) |

| Lithium Iron Phosphate (LFP) | |

| Lithium Nickel Manganese Cobalt (NMC) | |

| Lithium Nickel Cobalt Aluminium (NCA) | |

| Lithium Manganese Oxide (LMO) | |

| Lithium Titanate (LTO) | |

| By Form Factor | Cylindrical |

| Prismatic | |

| Pouch | |

| By Power Capacity | Up to 3,000 mAh |

| 3,000 to 10,000 mAh | |

| 10,000 to 60,000 mAh | |

| Above 60,000 mAh | |

| By End-use Industry | Automotive (EV, HEV, PHEV) |

| Consumer Electronics | |

| Industrial and Power Tools | |

| Stationary Energy Storage | |

| Aerospace and Defense | |

| Marine |

Key Questions Answered in the Report

What is the forecast value of the Pakistan lithium-ion battery market by 2031?

It is projected to reach USD 826.56 million, reflecting a 13.99% CAGR from 2026-2031.

Which chemistry leads current sales?

Lithium iron phosphate holds 45.9% of 2025 revenue and is growing at 15.5% a year.

How are import taxes influencing battery prices?

A 48% combined duty and sales tax raises a 10 kWh residential pack to about PKR 1.2 million.

Which end-use segment is growing fastest?

Automotive applications are expanding at a 20.2% CAGR on the back of local EV assembly.

What regional markets show the highest adoption?

Punjab and Sindh dominate installations due to industrial demand and supportive incentives.

Are local firms producing cells or only assembling packs?

Atom Power began cell assembly in Karachi, while others mainly focus on pack integration.

Page last updated on: