Pad-Mounted Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.51 Billion |

| Market Size (2031) | USD 9.89 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

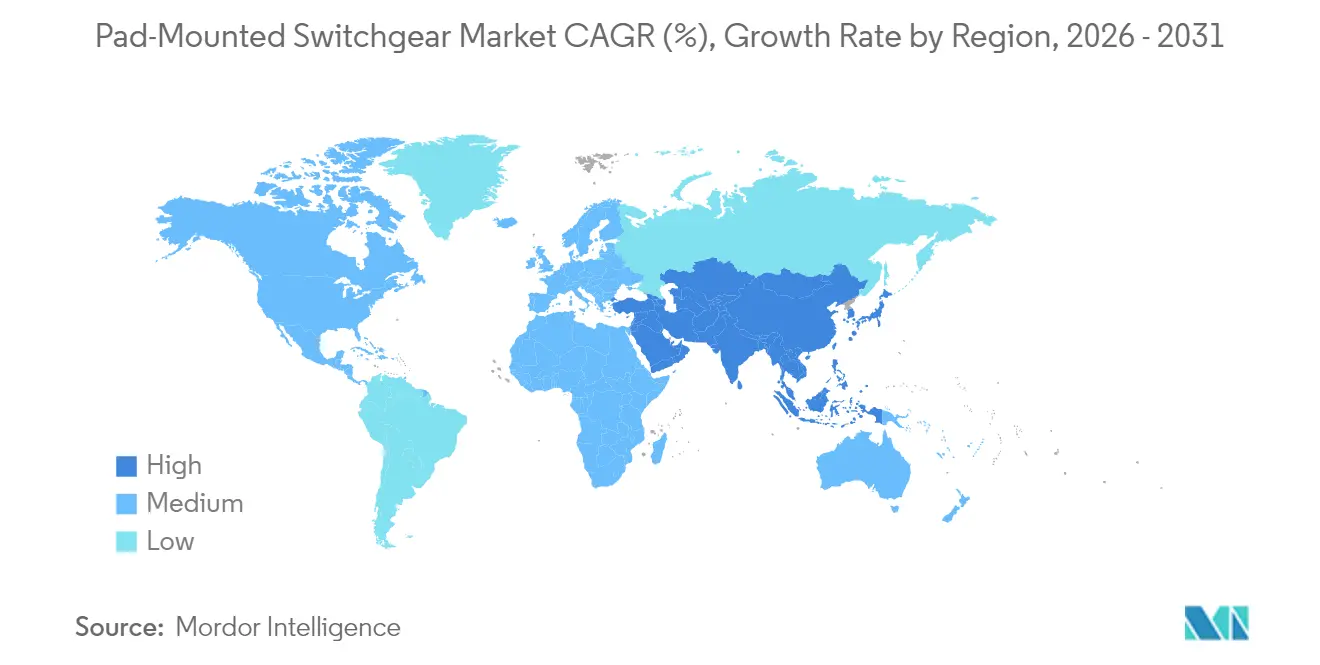

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

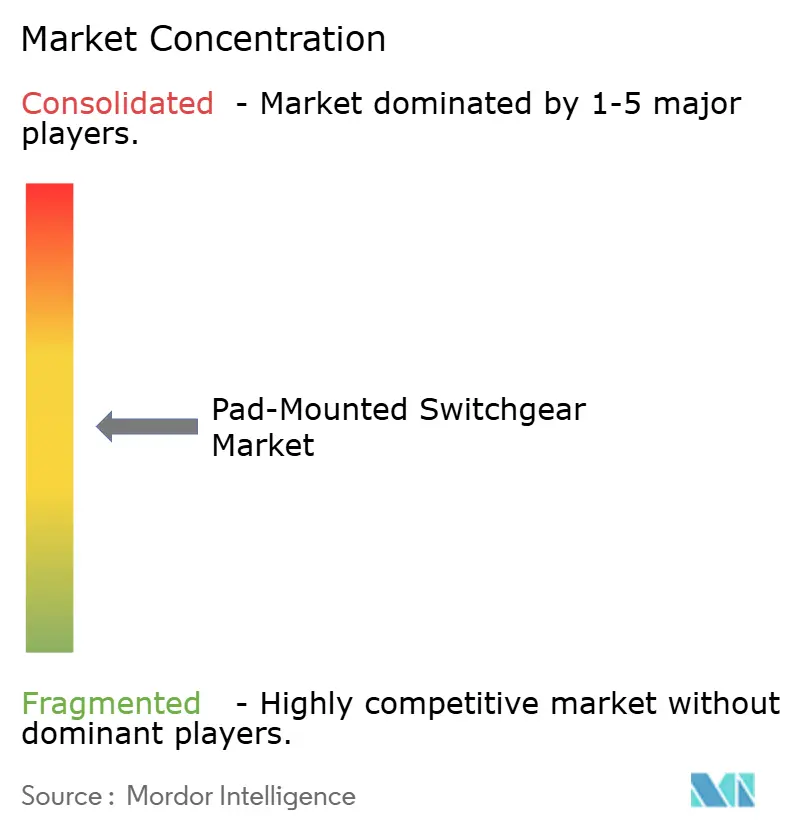

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pad-Mounted Switchgear Market Analysis by Mordor Intelligence

The Pad-Mounted Switchgear Market size was valued at USD 7.10 billion in 2025 and estimated to grow from USD 7.51 billion in 2026 to reach USD 9.89 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031).

Rising underground line deployments, bans on SF₆-filled equipment, and rapid data-center construction underpin this expansion. Utility wildfire-mitigation programs, renewable energy interconnections, and space-constrained urban projects further stimulate demand for the pad-mounted switchgear market, while component lead-time spikes and high capital costs remain near-term headwinds. North America leads in current revenue thanks to grid-hardening mandates, whereas the Asia-Pacific region registers the fastest growth as governments pour record sums into transmission and distribution build-outs. On the technology front, the adoption of solid-dielectric switchgear accelerates as operators seek SF₆-free performance with lower maintenance requirements. Competitive strategies center on vertical integration, capacity expansions, and acquisitions that secure early footholds in the emerging SF₆-free market.

Key Report Takeaways

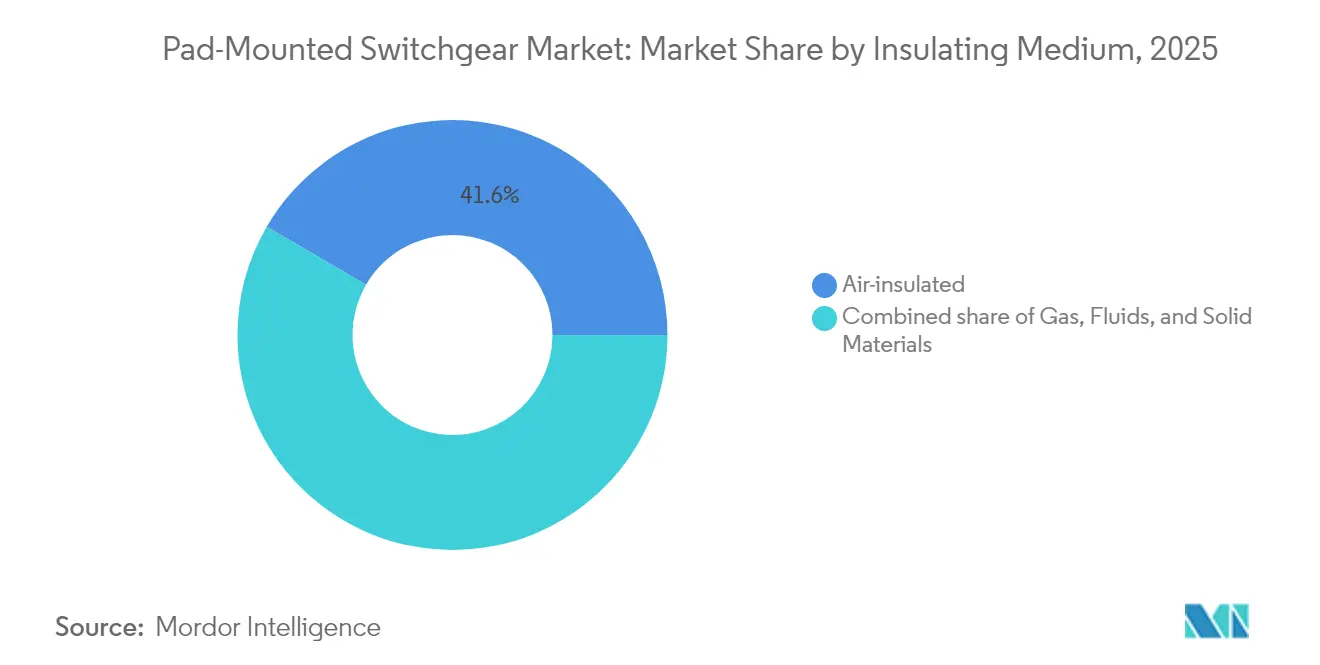

- By insulating medium, air-insulated switchgear is expected to lead with a 41.60% revenue share in 2025; solid-dielectric solutions are projected to expand at a 7.68% CAGR through 2031.

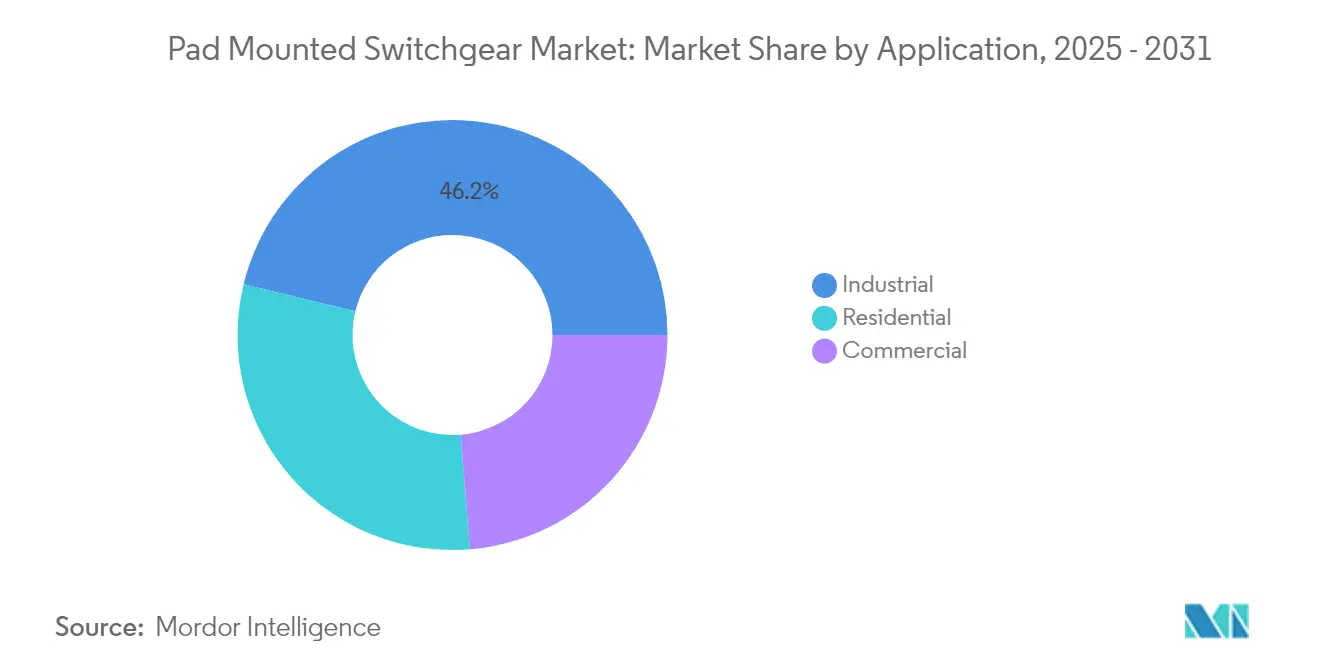

- By application, industrial facilities held 46.20% of the pad-mounted switchgear market share in 2025; commercial installations are forecast to grow at a 7.39% CAGR to 2031.

- By geography, North America accounted for a 36.10% share of the pad-mounted switchgear market size in 2025, and the Asia-Pacific region is projected to advance at a 7.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pad-Mounted Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization undergrounding | +1.8% | North America & EU, with spillover to APAC | Medium term (2-4 years) |

| SF₆-free technology shift | +1.2% | Global, with early adoption in EU & California | Short term (≤ 2 years) |

| Renewable & DER interconnections | +1.0% | APAC core, expanding to North America & EU | Long term (≥ 4 years) |

| Urban space constraints | +0.8% | Global urban centers, concentrated in APAC megacities | Medium term (2-4 years) |

| Microgrid build-outs | +0.6% | North America & EU industrial/commercial sectors | Medium term (2-4 years) |

| Hyperscale data-center demand | +0.5% | North America, EU, and select APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-modernization undergrounding

Underground distribution now commands sizable utility capex as overhead systems struggle to survive extreme weather events. The U.S. Department of Energy allocated USD 34 million to the GOPHURRS program, signifying federal endorsement of below-grade distribution that reduces storm-related outages.[1]U.S. Department of Energy, “GOPHURRS Program Awards,” energy.gov Underground line costs range from USD 1.1 million to USD 62 million per kilometer, creating a substantial addressable market for pad-mounted switchgear. U.S. underground line share rose from 18% in 2009 to roughly 20% in 2023, and Pacific Gas & Electric plans to bury 10,000 miles of circuits, each mile requiring several pad-mounted units for sectionalizing and protection.[2]IEEE Spectrum Staff, “PG&E Commits to Undergrounding,” spectrum.ieee.org These projects translate into multi-year procurement pipelines that insulate the pad-mounted switchgear market from cyclical downturns.

SF₆-free technology shift

Climate policy now bans SF₆ in new medium-voltage gear across the EU from January 2026 and across California by 2033.[3]European Parliament & Council, “Regulation (EU) 2024/789 on SF₆-free Switchgear,” europa.eu Because SF₆ has a 25,200× CO₂ warming potential, utilities must rapidly switch to vacuum, clean-air, or fluoronitrile insulation that lowers emissions up to 99%.[4]GE Vernova, “GRiDEA Portfolio Cuts CO₂e 99%,” ge.com Manufacturers that commercialize SF₆-free pads win early replacement contracts and earn premium margins, while laggards face stranded portfolios. Hitachi Energy shipped the world’s first SF₆-free 550 kV GIS in May 2025, proving the scalability of the alternative technologies. Early adopters in Europe and California shorten testing cycles, accelerating global diffusion and bolstering the pad-mounted switchgear market.

Renewable & DER interconnections

The Asia-Pacific region alone represents USD 1.1 trillion in renewable supply-chain opportunity by 2050, and 60-75% of each project’s cost falls on balance-of-system items such as switchgear. Bidirectional power flows from rooftop solar, batteries, and electric vehicles demand switchgear equipped with intelligent electronic devices and adaptive protection. Pad-mounted units with remote control and automation features now sit at feeder ends, enabling microgrid islanding and voltage regulation without requiring substation intervention. As renewable penetration rises, utilities deploy more sectionalizing points to manage fault currents, directly enhancing demand in the pad-mounted switchgear market.

Urban space constraints

Megacities seek compact, visually unobtrusive networks as surface real estate premiums soar. Pad-mounted switchgear operates underground or in flush-mounted enclosures, freeing sidewalks and satisfying aesthetic codes. The format also permits co-location with water, gas, and telecom ducts, optimizing trench usage in dense corridors. Asia-Pacific metropolitan areas add thousands of kilometers of underground feeders annually, and local zoning now bans new overhead corridors in many central business districts. These planning rules reinforce the steady expansion of the pad-mounted switchgear market in cities from Tokyo to Jakarta.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs | -1.50% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| MV component lead-time spikes | -1.00% | Global, most visible in North America & EU | Medium term (2-4 years) |

| Safety concerns around eco-fluids | -0.60% | EU & North America | Short term (≤ 2 years) |

| Skills gap for solid-dielectric O&M | -0.40% | Global, sharper in developed economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital costs

Underground feeders can cost 3.5 to 8 times more than their overhead equivalents, straining utility budgets and sparking public opposition to rate hikes. In Ontario, developers pay up to USD 12,400 per all-electric home for distribution hookups, an expense that dampens green-field adoption. Municipal utilities with small rate bases often defer undergrounding, postponing pad-mounted switchgear purchases. Consequently, the pad-mounted switchgear market faces adoption gaps in lower-income regions until cost-sharing mechanisms mature.

MV component lead-time spikes

Medium-voltage component deliveries now exceed 92 weeks, forcing utilities to overspecify and over-order equipment to avoid delays. Requiring oversized ratings inflates project budgets and reduces network efficiency. The U.S. National Infrastructure Advisory Council advocates for a “virtual transformer reserve,” underscoring the systemic risk posed by supply constraints. Persistent bottlenecks pressure the pad-mounted switchgear market outlook despite strong order books.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulating Medium: Solid-Dielectric Emerges as Growth Leader

Air-insulated switchgear retained 41.60% of the pad-mounted switchgear market size in 2025, thanks to established supply chains and cost advantages. Solid-dielectric variants, however, are tipped to progress at a 7.68% CAGR through 2031 as SF₆ bans drive technology conversions. Gas-insulated units occupy a middle ground, benefiting from fast installation yet facing environmental scrutiny. Fluid-insulated models-using synthetic esters or natural oils-address niche fire-safe applications in dense cities.

Solid-dielectric platforms eliminate gas leakage concerns and reduce routine maintenance, making them appealing to utilities transitioning large feeder sections below grade. Operators report safer fault clearing and lower lifecycle costs compared to legacy gas units. As SF₆ deadlines approach, training initiatives intensify to equip technicians with new diagnostic protocols. GIS remains attractive where land prices justify compact footprints, cutting site area up to 75% and shaving project schedules by 45%. Overall, the escalating need for environmental compliance propels solid-dielectric technology to the forefront of the pad-mounted switchgear market.

By Application: Commercial Sector Drives Growth Acceleration

Industrial plants dominated the pad-mounted switchgear market with a 46.20% market share in 2025, as petrochemical, mining, and heavy-manufacturing sites require rugged, high-ampacity switching. Data-center and commercial-building demand is the fastest-growing, climbing at a 7.39% CAGR on the back of hyperscale campus build-outs. U.S. data-center power demand could reach 12% of national generation by 2030, and leading operators secure dedicated nuclear and renewable supplies to meet round-the-clock loads.

Each hyperscale campus integrates dozens of pad-mounted switchgear line-ups for dual-feeder redundancy and sectionalizing between power rooms. Vendors such as Siemens have signed 2024 modular-skid agreements with Compass Datacenters, under which switchgear and transformers arrive pre-integrated to reduce site work. Residential electrification, spurred by the Inflation Reduction Act’s USD 8.8 billion rebate fund, opens a nascent frontier. Electric vehicle chargers and heat pumps reduce street-level loads, prompting distribution operators to deploy underground residential distribution networks equipped with compact pads. These developments solidify long-term prospects across every application class within the pad-mounted switchgear market.

Geography Analysis

North America commands the largest revenue share at 36.10% in 2025, driven by expansive grid-hardening programs and wildfire mitigation mandates. Pacific Gas & Electric’s 10,000-mile undergrounding plan, coupled with the DOE’s GOPHURRS grants, sustains high single-digit annual equipment outlays. The United States alone is projected to show a 10.5% CAGR for medium-voltage switchgear through 2030, resulting in more than USD 2 billion in additions to the pad-mounted switchgear market size. Canada estimates USD 1.4 trillion in electricity investments by 2050, with half earmarked for transmission and distribution (T&D), signaling robust medium-term spending.

Asia-Pacific records the quickest advance, posting a 7.08% CAGR from 2026-2031. India plans INR 9.1 lakh crore (USD 109 billion) for transmission and distribution by 2032, a figure that incorporates significant underground feeder deployment. China leads in technology scale-up, as evidenced by State Grid’s first-in-class 550 kV SF₆-free GIS rollout, underscoring its regional leadership in alternative insulation adoption. Japan and South Korea utilize advanced manufacturing to export solid-dielectric units across Southeast Asia, where economic corridors, such as the Eastern Economic Corridor in Thailand, require resilient underground networks. The pad-mounted switchgear market, therefore, enjoys a broad pull in the Asia-Pacific region, rooted in the integration of renewable energy and urban electrification.

Europe experiences steady but regulation-intensive growth. The EU SF₆ prohibition, effective January 2026, requires wide-scale retrofit and replacement budgets that favor domestic OEMs. Norway’s six-year SF₆-free framework with Siemens signals the growing appetite for green switchgear in North Europe. The UK, France, and Germany are mirroring this trend, prioritizing low-carbon equipment in their post-Brexit and post-pandemic recovery plans. In South America, transmission projects for renewable exports drive incremental demand, although financing obstacles temper volumes. The Middle East & Africa benefit from industrial diversification agendas, yet skilled labor gaps and CAPEX hurdles slow project flow. Collectively, these regional patterns reinforce diversification benefits for global suppliers to the pad-mounted switchgear market.

Competitive Landscape

The pad-mounted switchgear market exhibits moderate concentration. Multinationals, including ABB, Siemens, GE Vernova, Hitachi Energy, and Eaton, leverage vertical integration to secure raw materials, design SF₆-free platforms, and maintain lifecycle service contracts. Acquisition activity intensifies: Siemens will absorb Trayer Engineering to deepen North American pad-mount expertise. ABB earmarked USD 120 million in 2025 for additional U.S. manufacturing, expanding production floors in Tennessee and Mississippi. Meanwhile, a USD 40 million Elastimold facility in New Mexico will double accessory output to mitigate lead-time shocks.

Innovation focuses on alternative insulation, digital monitoring, and modular construction. GE Vernova’s 2024 GRiDEA portfolio slashes CO₂e by 99%, aligning with utilities setting Scope 3 emissions targets. Hitachi Energy’s May 2025 SF₆-free 550 kV delivery demonstrates top-end voltage credibility, paving the way for a trickle-down effect to 15-38 kV pad units. Start-ups are leveraging IoT sensors for SF₆ leakage detection, forming partnerships like Planet2050-MasterGrid that capture retrofit budgets as the installed base transitions to greener equipment.

Capacity expansion is a common hedge against supply-chain risk. Mitsubishi Electric directed USD 86 million to a Pennsylvania switchgear plant in late 2024 to localize production for U.S. grid-hardening schemes. ABB, Siemens, and Eaton pursue multi-sourcing of vacuum interrupters and solid-dielectric modules to curtail 92-week lead-time exposures. As demand rises, firms invest in upskilling field crews to service SF₆-free assets, thereby locking clients into long-term service frameworks that elevate switching costs and increase recurring revenue within the pad-mounted switchgear market.

Pad-Mounted Switchgear Industry Leaders

ABB Ltd

S&C Electric Company

Eaton Corporation PLC

G&W Electric Co

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hitachi Energy delivered the world’s first SF₆-free 550 kV gas-insulated switchgear to State Grid’s Central China Branch, proving high-voltage scalability of eco-designs.

- April 2025: ABB opened a USD 40 million plant in Albuquerque to produce Elastimold cable accessories and Fisher-Pierce fault indicators for undergrounding projects.

- March 2025: ABB announced USD 120 million to expand U.S. switchgear manufacturing, adding 250 jobs across Tennessee and Mississippi.

- January 2025: EMCOR Group agreed to purchase Miller Electric Company for USD 865 million, strengthening electrical build capabilities in the data-center and healthcare segments.

Global Pad-Mounted Switchgear Market Report Scope

Switchgear is a broad phrase that encompasses a wide range of switching devices that all have a common purpose: controlling, safeguarding, and isolating electrical systems.

The market is segmented by insulating medium, application, and geography. By insulating medium, the market is segmented into air, gas, fluids, and solid materials. By application, the market is segmented into industrial, commercial, and residential. The report also covers the market size and forecasts for the pad-mounted switchgear market across the major regions (Asia-Pacific, Europe, North America, South America, and Middle-East and Africa). For each segment, the market sizing and forecasts have been done on the revenue (USD Billion).

| Air |

| Gas (SF₆ / SF₆-free) |

| Fluids (E200, FR3) |

| Solid Materials |

| Industrial |

| Commercial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Insulating Medium | Air | |

| Gas (SF₆ / SF₆-free) | ||

| Fluids (E200, FR3) | ||

| Solid Materials | ||

| By Application | Industrial | |

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current pad-mounted switchgear market size?

The pad-mounted switchgear market size is USD 7.51 billion in 2026 and is projected to reach USD 9.89 billion by 2031.

Which region holds the largest share of the pad-mounted switchgear market?

North America leads with 36.10% revenue share due to aggressive grid-hardening and undergrounding initiatives.

What segment is growing fastest within the pad-mounted switchgear market?

Solid-dielectric switchgear records the highest growth at 7.68% CAGR as utilities migrate away from SF₆-filled equipment.

How do SF₆ bans impact the pad-mounted switchgear industry?

EU and California bans effective 2026-2033 force rapid adoption of SF₆-free technologies, driving significant replacement demand.

Why are data centers important for pad-mounted switchgear demand?

Hyperscale campuses require extensive medium-voltage sectionalizing gear, propelling commercial-application growth at 7.39% CAGR.

What are the main challenges for pad-mounted switchgear deployment?

High undergrounding costs, prolonged component lead times, and a skilled-labor gap for solid-dielectric maintenance hinder rapid rollout.

Page last updated on: