Outdoor Solar LED Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

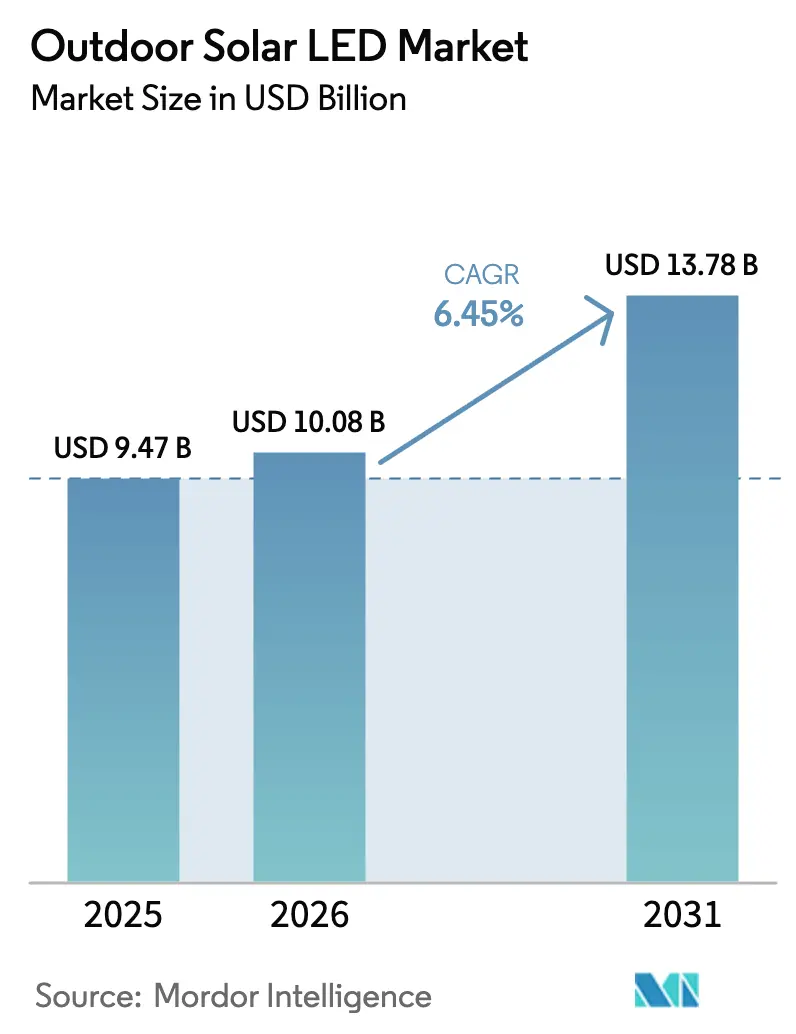

| Market Size (2026) | USD 10.08 Billion |

| Market Size (2031) | USD 13.78 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

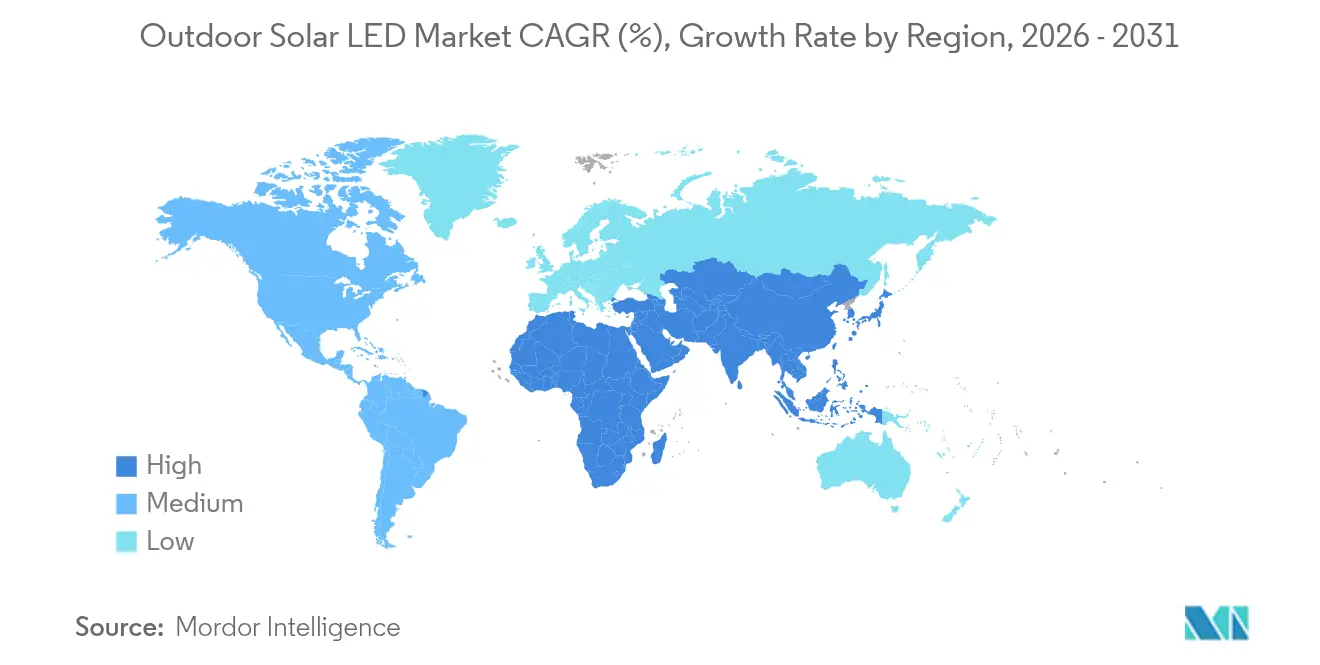

| Fastest Growing Market | Africa |

| Largest Market | Asia |

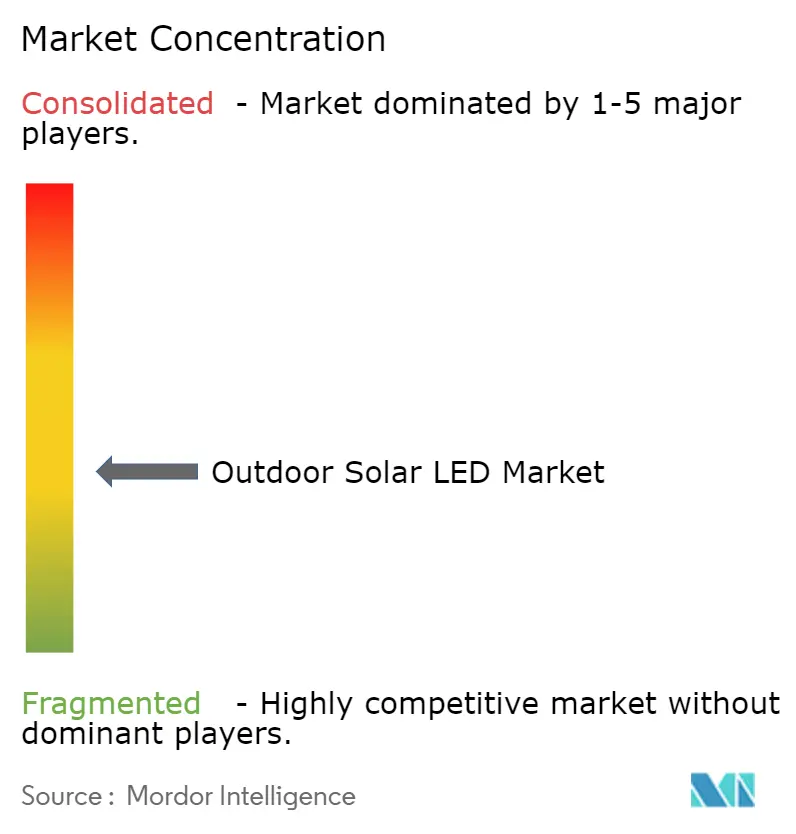

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outdoor Solar LED Market Analysis by Mordor Intelligence

Outdoor solar LED market size in 2026 is estimated at USD 10.08 billion, growing from 2025 value of USD 9.47 billion with 2031 projections showing USD 13.78 billion, growing at 6.45% CAGR over 2026-2031. Regulators are tightening light-pollution rules, battery prices are falling, and governments are funding rural electrification, all of which reinforce a shift from grid-tied to autonomous lighting. Asia commands demand through large-scale public projects, while Africa supplies the strongest growth momentum as multilateral lenders back distributed solar. High-wattage fixtures are now viable in colder climates because lithium iron phosphate (LiFePO₄) pack costs keep dropping and hybrid charging reduces winter downtime. Established suppliers respond by localizing assembly and embedding smart controls, whereas regional specialists exploit local-content rules. Against these drivers stand battery theft, thermal-management limits above 150 W, and financing gaps for mid-sized commercial campuses, challenges that could slow adoption in specific use cases.

Key Report Takeaways

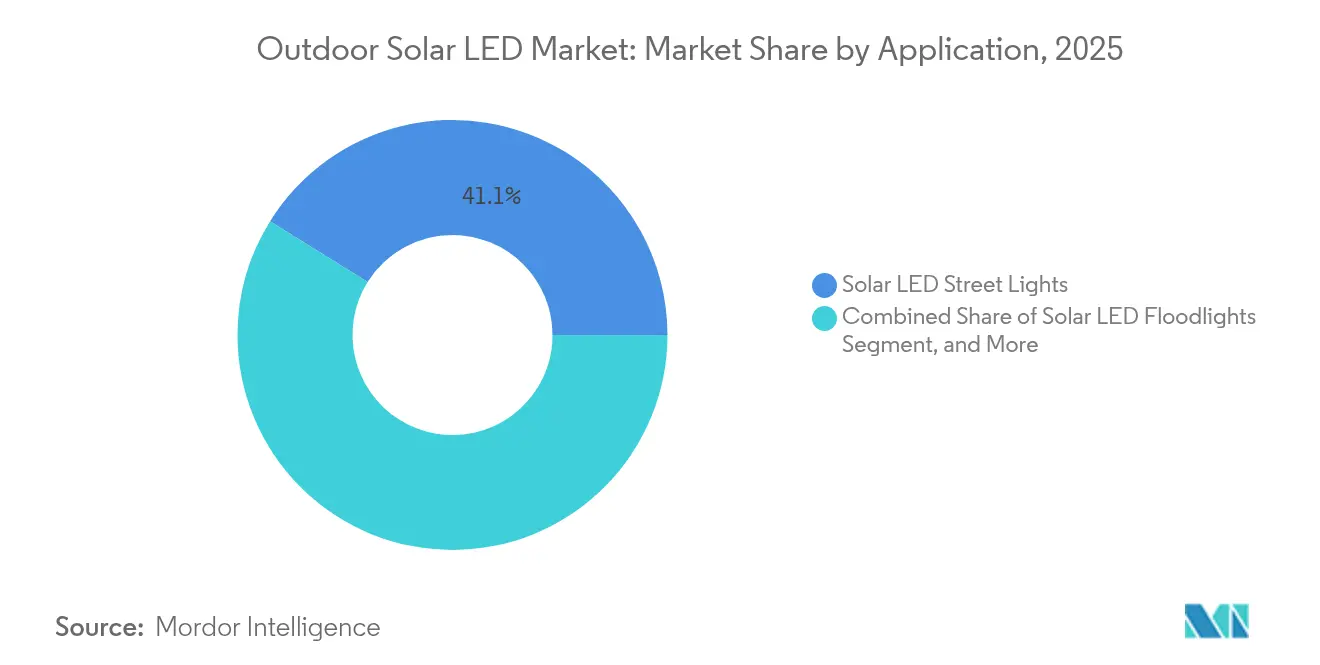

- By application, street lights held 41.12% Outdoor solar LED market share in 2025; floodlights are projected to advance at an 8.32% CAGR to 2031.

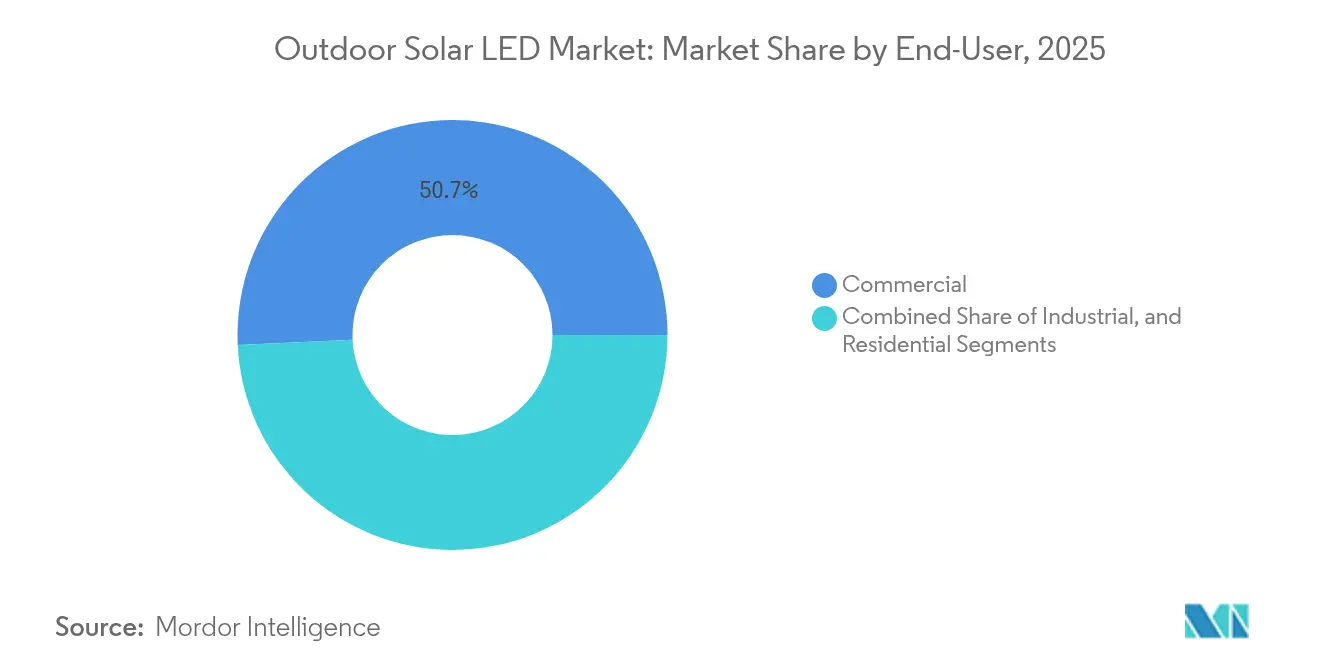

- By end-user, commercial installations accounted for 50.74% of the Outdoor solar LED market size in 2025, while industrial sites are set to grow at 6.94% CAGR through 2031.

- By wattage, 40 W-149 W fixtures captured 46.05% Outdoor solar LED market share in 2025; ≥150 W units are expected to expand at a 7.55% CAGR to 2031.

- By component, luminaires led with 34.22% of the Outdoor solar LED market size in 2025; battery packs exhibit the fastest 8.14% CAGR to 2031.

- By geography, Asia commanded 44.75% Outdoor solar LED market share in 2025, whereas Africa is forecast to grow at 7.2% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outdoor Solar LED Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solar-LED road-illumination mandates | +1.2% | Sub-Saharan Africa, spill-over to MENA | Medium term (2-4 years) |

| Dark-sky retrofit regulations | +0.8% | Europe & North America | Short term (≤2 years) |

| Hybrid telecom-tower upgrades | +0.9% | South Asia, Southeast Asia | Medium term (2-4 years) |

| Rural electrification programs | +1.4% | India, Kenya, Nigeria | Long term (≥4 years) |

| Rapid LiFePO₄ price decline | +1.1% | Global | Short term (≤2 years) |

| Smart-city procurement incentives | +0.6% | Europe, East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Solar-LED Road-Illumination Mandates in Sub-Saharan Africa

Governments confronting energy poverty now specify solar LEDs in road contracts, creating predictable demand that encourages local assembly plants. The World Bank’s USD 35 billion electrification drive recognizes solar as faster and cheaper than extending grids, while private suppliers in Niger already sell quality modules below USD 75, confirming affordability thresholds.[1]“A $35 Billion Loan Project, Led by World Bank, Aims to Expand Electricity in Africa,” The New York Times, nytimes.com

Dark-Sky Regulations Fueling Municipal Retrofits in Europe and North America

Statutes such as Maine’s LD 1934 cap brightness and color temperature, forcing municipalities to swap high-pressure sodium units for compliant solar LEDs that natively meet downward-facing and lumen limits. Early adopters like Groveland, Florida, budget six-figure sums for phased retrofits, anchoring a replacement cycle that favors off-grid systems with built-in controls.[2]“City looks to the stars for lighting policy,” Congress for the New Urbanism, cnu.org

Hybrid Telecom-Tower Upgrades Adopting Solar LEDs in South Asia

Tower owners reduce diesel costs and improve perimeter security by bundling lighting with renewable micro-grids. India’s village-level 8 kW systems run flawlessly through outages, proving technical viability, while policy schemes such as PM-KUSUM unlock capex for rural operations.

Rural Electrification Programs Accelerating Off-Grid Street Lighting

Community solar now reaches three times more people than in 2010, as subsidies absorb upfront costs and monthly tariffs fund maintenance. India’s Aspirational Districts and Kenya’s county schemes favor solar LED street lights that deliver immediate, reliable illumination when grid build-out would take decades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery theft and vandalism | -0.7% | Sub-Saharan Africa, Latin America, South Asia | Short term (≤2 years) |

| High O&M costs in low-irradiance cities | -0.5% | Northern Europe, Canada, Alaska | Medium term (2-4 years) |

| Limited campus-scale financing | -0.4% | Global emerging markets | Long term (≥4 years) |

| Thermal challenges above 150 W | -0.3% | Hot-climate regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Battery Theft and Vandalism Risk in Developing Regions

Municipalities that adopted solar to stop copper wire theft now face new risks as thieves target Li-ion packs. Los Angeles spends USD 20 million yearly on cable repairs, prompting a 900-unit solar rollout, yet tamper-proof housings and alarms raise capex for off-grid systems, particularly in Sub-Saharan Africa where resale incentives remain high.[3]“Residents Are Fed Up With Copper Theft Shutting Off Street Lights,” LAist, laist.com

High O&M Costs in High-Latitude, Low-Irradiance Cities

Seasonal darkness cuts energy harvest, forcing larger batteries and frequent maintenance. Canada’s CAD 300 million Arctic program underscores cost pressures, while bifacial panels and vertical mounts improve yield yet add engineering complexity that stretches payback periods north of 60° latitude.[4]“Potentiality of solar energy in the Arctic,” University of Oulu, oulu.fi

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Street Lights Anchor Municipal Adoption

Street lights contributed USD 3.89 billion to the Outdoor solar LED market size in 2025 and retained 41.12% share as cities favored proven procurement templates. Municipal buyers cite 3-year payback periods and improved citizen safety, illustrated by Seville’s 20 SunStay units delivering 3,000 lumens at 175 lm/W. Solar LED floodlights gained traction in industrial yards and stadiums, growing at 8.32% CAGR as insurers demand better night-time surveillance.

Evolving priorities trigger convergence across lighting forms. Fonroche’s 67,000-unit Senegal project guarantees 365-night autonomy, validating reliability for large public rolls-outs. Campus managers now blend street, area, and garden fixtures inside a single control platform that dims during low-traffic hours, widening use cases without ballooning O&M costs. As dark-sky rules proliferate, downward-directed floodlights gain an edge, and policy-driven retrofits sustain volume while adding smart features.

By Wattage: Mid-Range Dominates, High-Power Accelerates

Fixtures rated 40 W-149 W represented USD 4.36 billion and 46.05% Outdoor solar LED market share in 2025, balancing brightness with panel size and battery depth. They light most collector roads and retail lots, and standardization keeps installation costs predictable. Units exceeding 150 W are forecast to climb 7.55% CAGR as LiFePO₄ packs hit cost thresholds that bring high-mast ports and freight yards into scope.

Cree’s XFL10K diode provides 20,000 lumens with longer throw distance, cutting pole counts and civil works. Heat-sink advances and graphite composites alleviate thermal stress, especially in Gulf Coast and equatorial sites. Sub-39 W devices stay niche in decorative landscapes because limited lumen output restricts commercial uptake, yet smart-home ecosystems could unlock incremental demand as prices fall.

By End-User: Commercial Leadership, Industrial Momentum

Commercial establishments generated USD 4.81 billion, or 50.74% of the Outdoor solar LED market size in 2025, owing to parking-lot retrofits, wayfinding upgrades, and tenant-driven ESG targets. Financing tools such as power-purchase agreements match lease lengths, easing capex hurdles for malls and universities. Industrial users embrace solar to avoid downtime; manufacturing sites post a 6.94% CAGR outlook through 2031 as they secure perimeter zones and loading docks during grid failures.

Developers weave lighting into amenity packages. D.R. Horton integrates solar poles in new communities, raising property values and meeting municipal sustainability codes. Industrial complexes pursue micro-grid resilience strategies that pair rooftop PV with yard lighting, shrinking diesel backup use and trimming scope-2 emissions.

By Component: Luminaires Lead, Batteries Accelerate

Luminaires accounted for 34.22% revenue in 2025 as optics, color rendering, and housing design define end-user perception. On-chip solar cells now exceed 25.79% conversion on test wafers, hinting at future integration that could shrink panel footprints.

Battery packs grow 8.14% CAGR, reflecting scale economies in LiFePO₄ and rising demand for multi-day autonomy. AI-driven controllers dynamically trim output, extending life cycles while supporting IoT sensors that feed asset-management dashboards. Panels, poles, and mounting systems follow price-curve declines, yet innovations such as tilt-adjustable brackets and integrated 5G antennas enrich value propositions beyond mere illumination.

Geography Analysis

Asia delivered 44.75% of global revenue in 2025 due to deep supply chains, government subsidies, and massive grid-extension gaps still best solved through off-grid lighting. China anchors module exports, while India’s National Solar Mission sponsors village micro-grids that combine telecom, household, and street-light loads into single service packages. Japan’s 20 GW perovskite roadmap signals regional R&D leadership that could lower panel weight and broaden rooftop sites. Southeast Asian tower retrofits amplify orders for hybrid lighting kits that share battery strings with radio equipment, improving logistics efficiency.

Africa stands out with a projected 7.2% CAGR through 2031, underpinned by the World Bank loan program and private leasing models targeting 600 million people still without evening light. Niger’s retail boom in sub-USD 100 panels proves that affordability has crossed consumer thresholds, while Senegal’s record-scale street-light rollout shows how national mandates translate to immediate orders. Emerging assembly plants in Egypt and Kenya add local-content advantages that speed tenders.

The Middle East tripled solar generation in five years as oil exporters diversify. Saudi Arabia targets 58 GW of PV by 2030, and regional LED factories now top 3 GW yearly output, lowering landed costs and shortening lead times. Harsh summer temperatures spur demand for high-thermal-tolerance luminaires and smart cooling. North America and Europe focus on replacement rather than greenfield installations, yet dark-sky ordinances, copper-theft countermeasures, and tax-credit transfers keep budgets flowing, sustaining steady mid-single-digit growth.

Competitive Landscape

Incumbents such as Signify, Hubbell, and Cree retain leadership by combining optical engineering, grid-hybrid firmware, and multi-country service networks. Signify’s hybrid charging expands viability in Scandinavia and Alaska, while its 60%-owned Egyptian joint venture satisfies local-content clauses in public bids across MENA. Hubbell reports that 65% of 2024 sales link to renewable applications, signalling a pivot toward full-solution energy resilience packages.

Regional specialists differentiate through financing and climate-specific engineering. Ambient Photonics supplies ultra-low-light indoor cells that can power motion sensors inside covered transit hubs, unlocking cross-selling with outdoor luminaires for unified platforms. Fonroche and Sunna Design scale rapidly in francophone Africa thanks to concessional export guarantees. Chinese OEMs leverage vertical integration to undercut prices yet now face tariffs in North America and stricter quality audits in Europe.

The financing landscape is changing as tax-credit marketplaces enable real-estate investment trusts to monetize solar attributes without direct ownership. Black Bear Energy’s 2025 deal transfers investment credits to institutional buyers, injecting liquidity into campus-scale lighting retrofits. Technology roadmaps emphasise AI-augmented control nodes, battery health monitoring, and edge-based occupancy sensing, features that raise switching barriers and tie customers into long-term service contracts.

Outdoor Solar LED Industry Leaders

CREE Lighting

Gamasonic

Hubbell Outdoor

Ligman Lighting

Sokoyo Solar Lighting Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Niger’s government unveiled 19 MW and 200 MW solar projects to boost in-country generation.

- March 2025: Middle East Solar Industry Association disclosed that regional module output exceeded 3 GW by end-2024.

- March 2025: Los Angeles expanded its pilot from 104 to 900 solar street lights to mitigate USD 20 million yearly copper-theft losses.

- January 2025: Signify formed a joint venture with Gila Al Tawakol Electric to build LED manufacturing capability in Egypt, retaining 60% equity.

- January 2025: The World Bank launched a USD 35 billion electricity-access initiative prioritizing distributed solar.

Global Outdoor Solar LED Market Report Scope

Solar lights are outdoor LED lights that are powered by photovoltaic panels. These panels recharge a battery that supplies enough power for outdoor LED lights. As the global residential and commercial sectors experience increasing popularity and rapid expansion, there is a rising demand for solar outdoor LED lights. Solar LED lights are robust and can withstand harsh weather, temperatures, and UV rays.

Furthermore, the Outdoor Solar LED Market is segmented into Applications (Solar LED Street Lights, Solar Garden LED Lights, Solar LED Floodlights, Solar LED Area Lights, and Solar LED Spot Lights), Wattages (Less than 39W, 40W to 149W, and More than 150W), End User Industries (Residential, Commercial, and Industrial), and Geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Solar LED Street Lights |

| Solar Garden LED Lights |

| Solar LED Floodlights |

| Solar LED Area Lights |

| Solar LED Spot Lights |

| Less than 39 W |

| 40 W - 149 W |

| Above 150 W |

| Residential |

| Commercial |

| Industrial |

| Luminaire (LED Module) | |

| Solar Panel | Monocrystalline |

| Polycrystalline | |

| Thin-Film | |

| Battery Pack | Li-ion |

| LiFePO? | |

| Lead-acid | |

| Charge Controller and Smart Sensor Unit | |

| Pole and Mounting Structure |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Solar LED Street Lights | ||

| Solar Garden LED Lights | |||

| Solar LED Floodlights | |||

| Solar LED Area Lights | |||

| Solar LED Spot Lights | |||

| By Wattage | Less than 39 W | ||

| 40 W - 149 W | |||

| Above 150 W | |||

| By End-User Industry | Residential | ||

| Commercial | |||

| Industrial | |||

| By Component | Luminaire (LED Module) | ||

| Solar Panel | Monocrystalline | ||

| Polycrystalline | |||

| Thin-Film | |||

| Battery Pack | Li-ion | ||

| LiFePO? | |||

| Lead-acid | |||

| Charge Controller and Smart Sensor Unit | |||

| Pole and Mounting Structure | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Outdoor solar LED market?

The market stands at USD 10.08 billion in 2026 and is projected to reach USD 13.78 billion by 2031.

Which application contributes the largest revenue?

Solar LED street lights dominate with 41.12% market share in 2025 because municipalities favor their proven return-on-investment models.

Why is Africa considered the fastest-growing region?

Multilateral loans and government mandates addressing electricity access for 600 million people drive a 7.2% CAGR forecast for 2026-2031.

How are falling LiFePO₄ battery prices influencing adoption?

Lower battery costs now make ≥150 W fixtures economical, extending solar lighting to industrial yards and high-latitude cities.

What are the main obstacles to wider deployment?

Battery theft, high maintenance costs in low-irradiance zones, limited financing for mid-sized campuses, and thermal constraints above 150 W remain key restraints.

How competitive is the supplier landscape?

The top five vendors control just over 60% of global revenue, with regional specialists gaining share through local-content rules and financing innovation.

Page last updated on: