Optical Modulators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

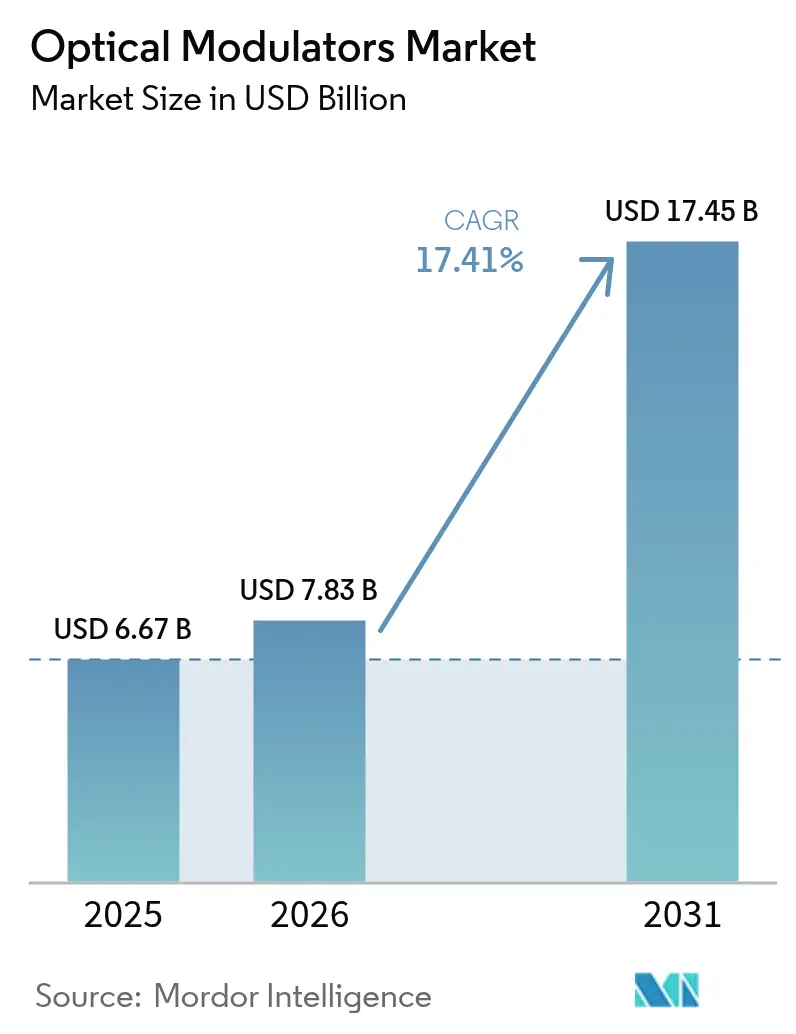

| Market Size (2026) | USD 7.83 Billion |

| Market Size (2031) | USD 17.45 Billion |

| Growth Rate (2026 - 2031) | 17.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Modulators Market Analysis by Mordor Intelligence

The optical modulators market size is expected to grow from USD 6.67 billion in 2025 to USD 7.83 billion in 2026 and is forecast to reach USD 17.45 billion by 2031 at 17.41% CAGR over 2026-2031. This trajectory reflects accelerating bandwidth demand from 800 G and 1.6 T optics, hyperscale data-center rollouts, and early quantum-computing networks that all rely on ever-faster electro-optic components. Vendors are prioritizing phase-stable, low-drive-voltage designs to meet thermal budgets inside co-packaged optics, while material innovation in thin-film lithium niobate and silicon photonics is reshaping cost structures. Integrated modulator chips are moving from niche to mainstream as switch ASIC vendors mandate optical engines optimized for 100 Gbaud and above. Meanwhile, policymakers in emerging economies keep allocating spectrum and subsidies for 5G backhaul and fiber-to-the-home, sustaining large-volume deployments in the 50–100 Gbps class.

Key Report Takeaways

- By product type, phase modulators led with 37.65% revenue share in 2025, whereas integrated modulator chips are on course to expand at an 18.05% CAGR through 2031.

- By material platform, lithium niobate held a 43.55% share in 2025, while silicon photonics is the fastest mover at an 18.25% CAGR.

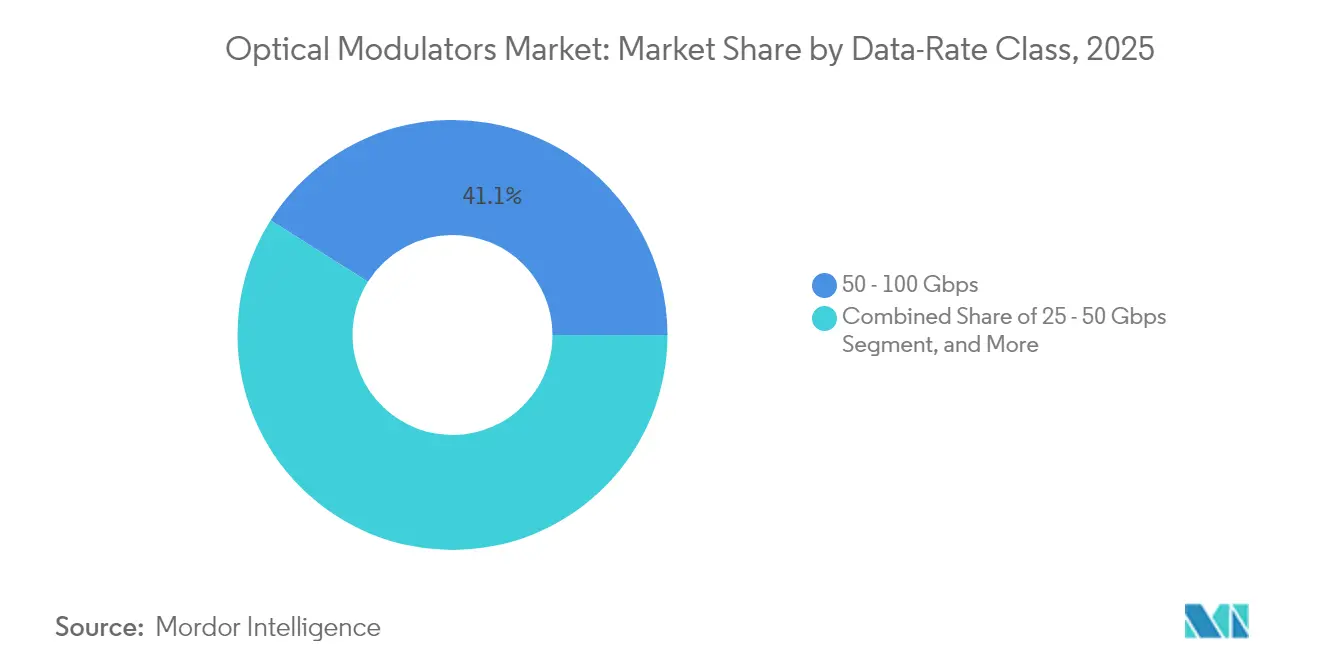

- By data-rate class, 50-100 Gbps captured 41.05% of the optical modulators market share in 2025; the >100 Gbps tier is projected to grow at 19.65% CAGR to 2031.

- By application, optical communication accounted for 56.55% of the optical modulators market size in 2025, yet quantum computing and cryogenic links are projected to surge at a 19.25% CAGR.

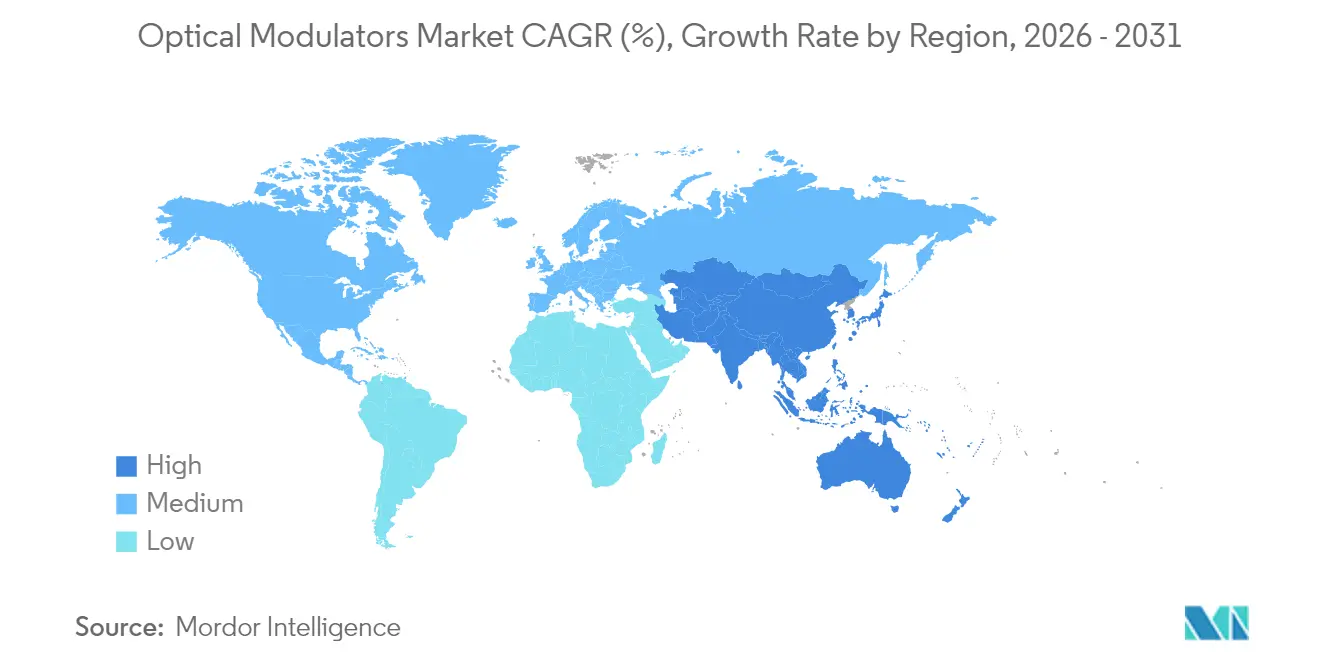

- By geography, Asia-Pacific commanded 38.35% share of the optical modulators market in 2025 and is advancing at a 20.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Optical Modulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising investments in optical-fiber communication infrastructure | +4.20% | Global, with emphasis on Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Hyperscale datacenter expansion and 800G/1.6T optics road-map | +5.10% | North America and Asia-Pacific core, spill-over to EMEA | Short term (≤ 2 years) |

| Accelerated 5G and FTTH rollout in emerging economies | +3.80% | Asia-Pacific, Middle East, and Latin America | Medium term (2-4 years) |

| Move to coherent optics greater than or equal to 400G on metro/long-haul links | +2.90% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Commercialisation of lithium-niobate-on-insulator (LNOI) modulators | +1.70% | Global, concentrated in advanced manufacturing regions | Long term (≥ 4 years) |

| Quantum photonics and cryogenic interconnect demand | +0.80% | North America and Europe, with emerging activity in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising investments in optical-fiber communication infrastructure

Record AI cluster build-outs lifted 800 G transceiver shipments past 20 million units in 2024 as cloud providers chased lower cost-per-bit metrics. The pivot from 400 G to 800 G, and early 1.6 T proof-points such as Ciena’s 1.6 T coherent-lite demo using 224 G SerDes, compel modulators to hit 100 Gbaud symbol rates without breaking power budgets.[1]Steve Alexander, “Ciena Brings Data Center Connectivity Innovations to OFC 2025,” Ciena, Mar 25 2025, ciena.com Linear pluggable optics are doubling from USD 5 billion in 2024 to more than USD 10 billion by 2026, amplifying short-term demand for compact, low-Vπ architectures. Thermal design margins tighten inside co-packaged optics, rewarding integrated suppliers that can co-optimize driver ICs and modulator waveguides on the same substrate. As switch ASIC roadmaps lock in 51 T and 102 T fabrics, optical-engine attach rates accelerate, reinforcing the driver’s positive impact on near-term CAGR.

Accelerated 5G and FTTH rollout in emerging economies

India’s monthly fiber deployment spiked to 101,550 km after 5G launch, six times the pre-5G run-rate, underlining how policy targets such as 70% tower fiberization translate into real optical component pull-through.[2]HP Singh, “Fiber First, 5G Next,” HFCL Blog, Jun 4 2024, hfcl.com Each small cell needs at least one 25 G or 50 G optical fronthaul link, so modulators tuned for cost and temperature resilience see large-volume orders. Chinese cloud operators generated a USD 2–3 billion domestic transceiver market in 2024, reinforcing regional procurement cycles that ripple through modulator fabs. Vendors able to qualify devices under wide environmental ranges win preferred-supplier status in public-telecom tenders, elevating medium-term growth prospects.

Move to coherent optics ≥ 400 G on metro/long-haul links

Ciena’s WaveLogic 5 Extreme exceeded 115,000 unit shipments by 2024, proving operator appetite for 400 G coherent upgrades. Now WaveLogic 6 targets 1.6 Tbps per wavelength, pressuring modulator suppliers to deliver dual-polarization I/Q structures with sub-1 dB insertion loss. IEEE’s open 400 ZR and emerging 800 ZR+ frameworks secure multi-vendor interoperability, opening a long-term pipeline for coherent-class modulators.[3]IEEE Working Group, “400ZR Interoperability Progress,” IEEE Xplore, Jun 9 2024, ieee.org Carriers prefer upgrading spectral efficiency over trenching new fiber, keeping this driver structurally positive through the forecast horizon.

Commercialization of lithium-niobate-on-insulator (LNOI) modulators

Thin-film lithium niobate now supports 3.2 Tbps transmissions while slashing Vπ below 0.5 V, eclipsing bulk-LiNbO₃ benchmarks.[4]SBIR Program Office, “Phase II Award to Critical Frequency Design,” SBIR, Oct 22 2024, sbir.gov HyperLight’s 110 GHz intensity device with Vπ 1.4 V validates readiness for high-frequency datacom and microwave-photonics use cases. Micro-transfer printing onto SiN offers Vπ·L of 2.74 V·cm, marrying lithium-niobate speed with silicon photonics scale economics. As advanced fabs ramp 8-in LNOI wafers, unit cost curves improve, unlocking incremental CAGR uplift in the outer forecast years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Design complexity and thermal-management limits above 100 Gbaud | -2.30% | Global, particularly affecting advanced applications | Short term (≤ 2 years) |

| High BOM cost of InP/LiNbO₃ wafers and poling processes | -1.80% | Global, with higher impact in cost-sensitive markets | Medium term (2-4 years) |

| Skilled-labour shortage in high-speed photonics packaging | -1.20% | North America and Europe primarily | Medium term (2-4 years) |

| Upstream lithium-ore supply-chain concentration risk | -0.90% | Global, with particular exposure in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Design complexity and thermal-management limits above 100 Gbaud

Pushing symbol rates past 100 Gbaud inflates thermal load and challenges velocity matching between microwave and optical signals. MIT Lincoln Laboratory’s inductance-tuned electrodes stretch bandwidth beyond 100 GHz while holding 50-ohm impedance, but packaging such innovations into manufacturable modules remains difficult.[5]Technology Transfer Office, “Inductance-Tuned Electro-Optic Modulators,” MIT Lincoln Laboratory, Jan 1 2025, ll.mit.edu Exotic substrates and liquid-metal thermal vias raise BOM and lengthen qualification cycles, limiting short-term supply diversity and depressing CAGR.

High BOM cost of InP/LiNbO₃ wafers and poling processes

China’s 2024 export curbs on gallium and germanium lifted input prices for InP epitaxy, while LiNbO₃ devices still depend on energy-intensive poling ovens. Yield hits from domain-inversion defects further inflate the cost per good die. These economics deter adoption in price-sensitive metro and access networks, capping medium-term market penetration.[6]Rofea Product Team, “LiNbO₃ Mach-Zehnder Modulator Datasheet,” DirectIndustry, Jan 1 2025, directindustry.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integrated chips reshape value creation

Phase modulators owned 37.65% of the optical modulators market share in 2025 as they remain fundamental for coherent detection. Integrated modulator chips, however, will post the strongest 18.05% CAGR because co-packaged optics depends on single-substrate designs that trim power and latency. The optical modulators market size tied to integrated chips expands as foundries like Tower Semiconductor qualify 400 G-per-lane units.

Established amplitude and polarization devices continue serving direct-detection and sensing. Analog modulators keep niche radio-over-fiber footholds where linearity trumps speed. The shift toward wafer-level test drives ASP reduction, inviting new entrants that master photonic-electronic co-design.

By Material Platform: Silicon photonics closes the gap

Lithium niobate held a 43.55% share thanks to its superior electro-optic coefficient and temperature stability. Yet silicon photonics is accelerating at 18.25% CAGR because CMOS fabs unlock high-volume, low-cost runs. The optical modulators market size attributable to silicon photonics rises as large cloud buyers demand single-supplier photonic ICs end-to-end. Indium phosphide retains a foothold where integrated lasers are mandatory, while electro-optic polymers address >100 GHz microwave photonics, though reliability hurdles persist.

By Data-Rate Class: Greater than 100 Gbps momentum builds

The 50-100 Gbps tier dominated with 41.05% share in 2025, underpinning most 400 G coherent links. However, modules exceeding 100 Gbps symbols will outpace all peers at 19.65% CAGR, reflecting 1.6 T roadmaps. Ciena’s 448 Gb/s PAM4 silicon underscores appetite for fresh modulation formats that place new demands on extinction ratio and chirp. Vendors that master driver-modulator co-packaging will capture an outsized share.

By Application: Quantum computing surges

Optical communication held a 56.55% share as broadband and cloud infra keep scaling. Quantum computing and cryogenic links, despite a small base, will post a 19.25% CAGR as national labs and start-ups fund photonic qubit networks needing ultra-low-loss cryogenic modulators. Fiber-optic sensors, space-defense payloads, and precision test instruments make up stable, specification-heavy niches.

Geography Analysis

Asia-Pacific accounted for 38.35% of the optical modulators market share in 2025, fueled by China’s vertically integrated transceiver ecosystem and India’s sprint to fiberize towers. Regional manufacturing depth keeps BOM low, allowing rapid deployment across 5G and FTTH footprints. Government subsidy programs and local sourcing mandates further anchor production. North America shows mature but innovation-led demand, with hyperscale operators and defense primes adopting cutting-edge thin-film LiNbO₃ and silicon photonics to support AI fabrics and quantum research. Europe maintains steady upgrades in metro networks while automotive LiDAR and industrial sensing open adjacencies for analog and polarization modulators. The optical modulators market size in these mature regions grows via technology refresh, contrasting with volume-driven expansion in emerging economies.

Regulatory Landscape

Optical modulator deployment is shaped by international component standards, laser-safety requirements, and trade and security policy. On the compliance side, DIN EN IEC 62149-3:2024-08 sets performance requirements for electroabsorption-type optical modulators integrated with laser diodes for 40 Gbit/s transmission systems, affecting qualification and documentation for telecom-grade parts. For free-space optics used in mobile backhaul, ITU-T Recommendation G.641 (11/2025) standardizes physical-layer parameters and explicitly references IEC 60825 series laser-safety compliance, which drives design controls and testing for optical transmit/receive subsystems that incorporate modulators.

National policy is increasingly linked to supply-chain provenance for optical components used in sensitive networks and defense programs. In the United States, Section 834 of the National Defense Authorization Act for FY2026 requires the Department of Defense to eliminate reliance on optical glass and systems sourced from covered nations by January 1, 2030, increasing pressure for traceability and alternative sourcing across upstream photonics materials and assemblies. In China, the Ministry of Industry and Information Technology issued AI + Information Communication Innovation Development Implementation Opinions (2026-2028) in June 2026, highlighting co-packaged optics and high-speed optoelectronic chips, which supports domestic sourcing and accelerates local qualification pathways for high-speed modulator platforms.

Competitive Landscape

The market remains moderately fragmented; the five largest suppliers control major market revenue. Incumbents such as Lumentum expand InP wafer output to secure AI-driven demand spikes, whereas silicon photonics specialists gain share through foundry partnerships. M&A continues: Nokia’s 2025 purchase of Infinera folds coherent optics into its routing stack, signaling convergence between photonics and packet layers. Synopsys divested its optical design arm to Keysight to refocus on its EDA core business, illustrating strategic specialization. Start-ups targeting thin-film LiNbO₃ raise venture and DoD grants to close performance gaps at greater than 100 GHz, keeping competitive intensity high.

Optical Modulators Industry Leaders

Lumentum Holdings Inc.

Fujitsu Optical Components Ltd.

Thorlabs Inc.

Gooch and Housego PLC

AA Opto-Electronic SAS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace centers on scaling manufacturable, low-drive-voltage modulation for 800G to 1.6T optical engines while keeping within power and thermal budgets for co-packaged and near-package optics. Recent activity provides support for this focus: Tower Semiconductor and Coherent demonstrated 400 Gbps per-lane transmission on a production-ready silicon photonics Mach-Zehnder modulator platform (March 2026), and imec reported beyond-110 GHz C-band GeSi electro-absorption modulator performance on a 300 mm silicon photonics platform with net 400 Gbps per lane (October 2025). These results point to an opportunity for suppliers that can convert lab-grade bandwidth into high-yield, wafer-level testable designs, including integrated driver-modulator co-optimization for 100 Gbaud and above.

Another opportunity is supply-chain and capacity realignment across InP substrates, EMLs, and high-speed modulator ecosystems as AI interconnect procurement tightens lead times. Multiple investments indicate active capacity building: Coherent disclosed a USD 650 million investment plan for its Sherman, Texas fab to expand footprint and quadruple InP wafer output (June 2026), Source Photonics (Dongshan Precision subsidiary) announced a USD 1.2 billion optical chip and module expansion program (June 2026), and Sumitomo Electric committed JPY 18 billion at Itami Works to lift InP substrate capacity to 3.1x fiscal 2024 levels by fiscal 2028 (July 2026). Together, these moves create room for equipment, materials, packaging, and foundry partners that can meet telecom and datacenter qualification, and for modulator vendors that can secure multi-region manufacturing paths aligned with procurement rules in defense and public-network tenders.

Recent Industry Developments

- May 2026: POET Technologies entered a strategic supply and joint development partnership with Lumilens to advance wafer-level photonic integration aimed at next-generation AI optical networks. The collaboration targets higher-volume, more manufacturable optical-engine building blocks, supporting tighter integration between modulators, packaging, and system-level requirements for data-center interconnect.

- April 2026: Marvell acquired Polariton Technologies to add plasmonics-based, high-speed, low-power optical modulation capabilities to its connectivity portfolio. Bringing modulation IP closer to switch and interconnect silicon strengthens the push toward integrated optical engines and co-packaged optics architectures.

- December 2024: POET Technologies acquired SPX Technologies, adding a 1 million-unit optical-engine line to support scaling of integrated optical engines for high-volume deployments. The added manufacturing capacity and process capability helps shorten the path from design wins to volume shipments in co-packaged optics supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from optical modulators that intentionally change a light signal (such as intensity, phase, polarization, or amplitude) to support fiber communication, sensing, and other photonics use cases.

Scope exclusions: We exclude downstream system revenue (for example, full transceivers, lasers, receivers, and complete network equipment) unless the value is clearly attributable to the modulator itself.

Segmentation Overview

- By Product Type

- Amplitude Modulators

- Polarization Modulators

- Phase Modulators

- Analog Modulators

- Integrated (SiPh/InP/LNOI) Modulator Chips

- By Material Platform

- Lithium Niobate (LiNbO?)

- Indium Phosphide (InP)

- Silicon Photonics (SiPh)

- Electro-optic Polymer

- Others

- By Data-Rate Class

- Less than or Equal to 25 Gbps

- 25 - 50 Gbps

- 50 - 100 Gbps

- Greater than 100 Gbps

- By Application

- Optical Communication

- Datacentre Interconnect

- 5 G Fronthaul / Backhaul

- Sub-sea Cables

- Metro / Long-haul

- Fiber-optic Sensors

- Industrial and Structural Health

- Oil and Gas Monitoring

- Space and Defence

- Test and Measurement Equipment

- Quantum Computing and Cryogenic Links

- Optical Communication

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base and keep assumptions tied to observable demand signals for optical communication and sensing. We reviewed public sources such as the International Telecommunication Union (ITU), the US Federal Communications Commission (FCC), the National Institute of Standards and Technology (NIST), and the World Intellectual Property Organization (WIPO) patent data for photonics activity. Trade references and standards bodies, such as the IEEE and IEC, were also used to understand how modulation performance is usually stated in the industry.

We also used company filings and investor presentations to collect product mix cues, capacity expansion commentary, and regional exposure language, which helped us avoid overcounting demand in smaller end uses. Alongside this, a few paid subscriptions were referenced for company financials and intelligence, news and financials, patent databases, and selective import and export indicators where category mapping was possible. The desk research sources mentioned here are illustrative only, and many other public sources and documents were reviewed for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary discussions were run with a mix of component suppliers, module and subsystem integrators, and buying-side experts from telecom, data center connectivity, sensing, and defense related programs. Respondent inputs were used to validate what is counted as a modulator sale, sanity-check typical price bands, and confirm how demand shifts across regions and applications when network speeds or sensing deployments change.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 29% | EMEA: 36% |

| Smaller Players: 20% | Managers: 59% | Americas: 21% |

Market-Sizing & Forecasting

Market totals were first reconstructed using a top-down approach that links optical communication and sensing build-outs to the attach rate of modulation functions, then translated into value using typical pricing logic. To keep the model realistic, we used selective bottom-up approximations as checks, such as sampling unit volumes from representative supply chains and applying average selling price ranges shared by primary respondents, before adjusting totals.

Key inputs that guided the model included deployment intensity of fiber networks, shifts toward higher-speed links that need tighter modulation performance, the mix of modulator types adopted in telecom and data center interconnect, procurement cycles for sensing and defense programs, and observable patent and standards activity that signals platform transitions. Where direct volume clues were weak, gaps were handled by applying conservative penetration assumptions and then pressure-testing them with interviews and cross-region comparisons.

For forecasting, scenario analysis was used so demand could be flexed based on how quickly high-speed optical links expand and how fast newer modulator platforms get qualified into production. Assumptions for price movement and mix shift were reviewed with experts, then applied consistently across regions to avoid hidden step changes in the forecast.

Data Validation & Update Cycle

Results were validated through triangulation across demand indicators, supply-side commentary, and pacing items such as telecom capex cycles and standards-linked transitions. Outliers are flagged when growth or pricing drifts away from what primary respondents describe as feasible, and the model is then re-checked for unit-to-value consistency and regional allocation logic.

Before sign-off, the work goes through multi-step analyst reviews that focus on variance checks versus prior-year patterns and against independent market signals. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity announcements or sharp changes in telecom spending. Right before delivery, we run a final pass so clients receive the most current view available.

Mordor Intelligence's Optical Modulators Market Size Measured Against Other Published Estimates

Published numbers for optical modulators rarely match perfectly because each study can count a different product set, treat integrated solutions differently, and apply different timing for pricing and currency conversion. Even when the same end uses are discussed, the gap usually comes from how demand is translated into unit volumes and how average selling prices are stepped forward.

Some external estimates lean toward a narrower device-only view or start from shipment-focused baselines with limited cross-checking on where modulators are actually used. In Mordor Intelligence, the value is counted for modulator products tied to optical communication, fiber optic sensing, space and defense, and industrial systems, and adjacent system revenue is kept out unless the modulator share is clearly separable.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.67 B (2025) | |

| Global Consultancy A | USD 4.57 B (2025) | Uses a tighter interpretation of modulator categories and tends to keep only a subset of type definitions, which can undercount demand tied to broader industrial and defense linked deployments. |

| Industry Publisher B | USD 3.99 B (2024) | Anchors on an earlier base year and leans on shipment and revenue framing that can exclude parts of the application set, and it also embeds a much steeper growth path that is sensitive to a few unverified adoption assumptions. |

The comparison shows that scope choices and base-year handling explain most of the spread, and the remaining differences come from how pricing and mix shifts are carried through the forecast. Our approach stays traceable because each step is tied back to visible demand drivers like network build-outs, speed transitions, and application mix, then pressure-tested with primary checks before final totals are set.

Key Questions Answered in the Report

What is the current value of the optical modulators market?

The market reached USD 7.83 billion in 2026 and is forecast to hit USD 17.45 billion by 2031.

Which region generates the highest demand for optical modulators?

Asia-Pacific leads with 38.35% share in 2025 and continues to expand the fastest.

Which product type dominates sales?

Phase modulators held 37.65% share in 2025, driven by coherent system adoption.

Why are integrated modulator chips growing rapidly?

Co-packaged optics and switch ASIC roadmaps require compact, low-power photonic integration, pushing integrated chips at an 18.05% CAGR.

What material platform is gaining momentum against lithium niobate?

Silicon photonics is the fastest-growing platform at an 18.25% CAGR through 2031 due to CMOS fab scalability.

How will quantum computing affect modulator demand?

Quantum computing and cryogenic links are expected to post a 19.25% CAGR, creating a specialized high-growth niche for ultra-low-loss modulators.

Page last updated on: