Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

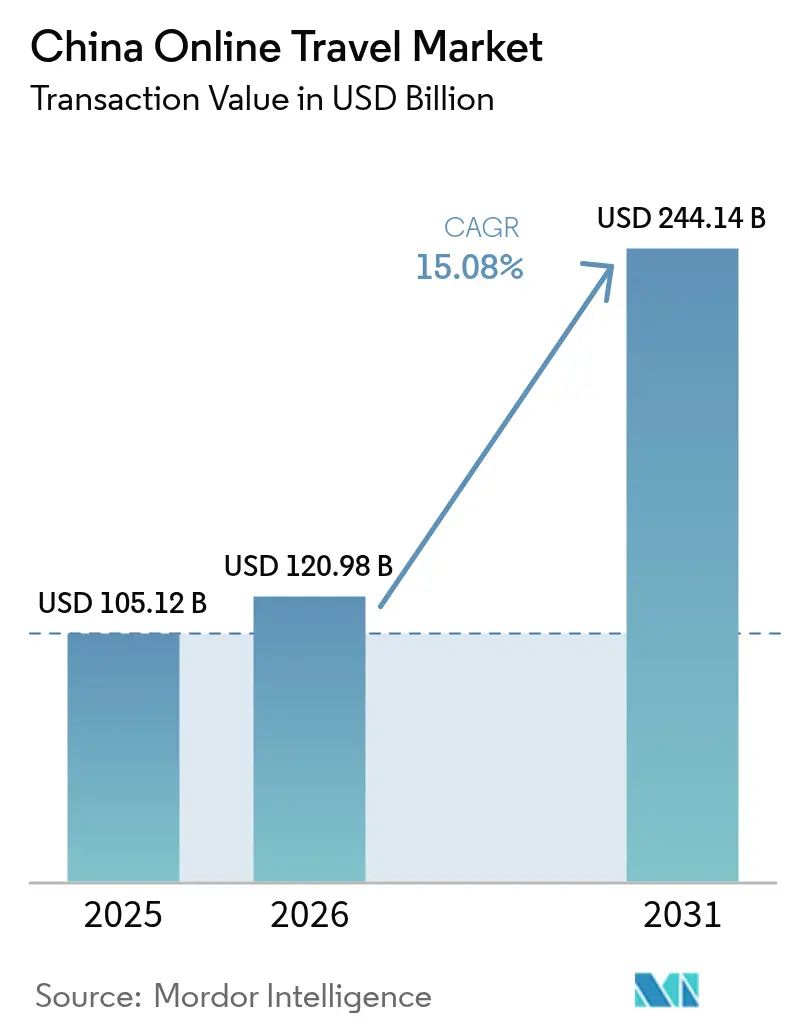

| Base Year Market Size (2025) | USD 105.12 Billion |

| Market Size (2026) | USD 120.98 Billion |

| Market Size (2031) | USD 244.14 Billion |

| Growth Rate (2026 - 2031) | 15.08% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Online Travel Market Analysis by Mordor Intelligence

The China online travel market size was valued at USD 105.12 billion in 2025 and estimated to grow from USD 120.98 billion in 2026 to reach USD 244.14 billion by 2031, at a CAGR of 15.08% during the forecast period (2026-2031). Rising digital literacy, a nationwide pivot toward mobile commerce, and supportive tourism policies collectively keep the growth curve steep. Tier-3 to Tier-5 cities, where first-time travelers now transact almost entirely through super-apps, add a fresh layer of momentum. Established online travel agencies (OTAs) reinforce their positions through AI-powered personalization, dynamic pricing, and bundled lifestyle offerings that raise user stickiness. Relaxed visa regimes and expanded airlift unlock outbound demand, while domestic tourism benefits from high-speed rail connectivity and government-funded destination upgrades.

Key Report Takeaways

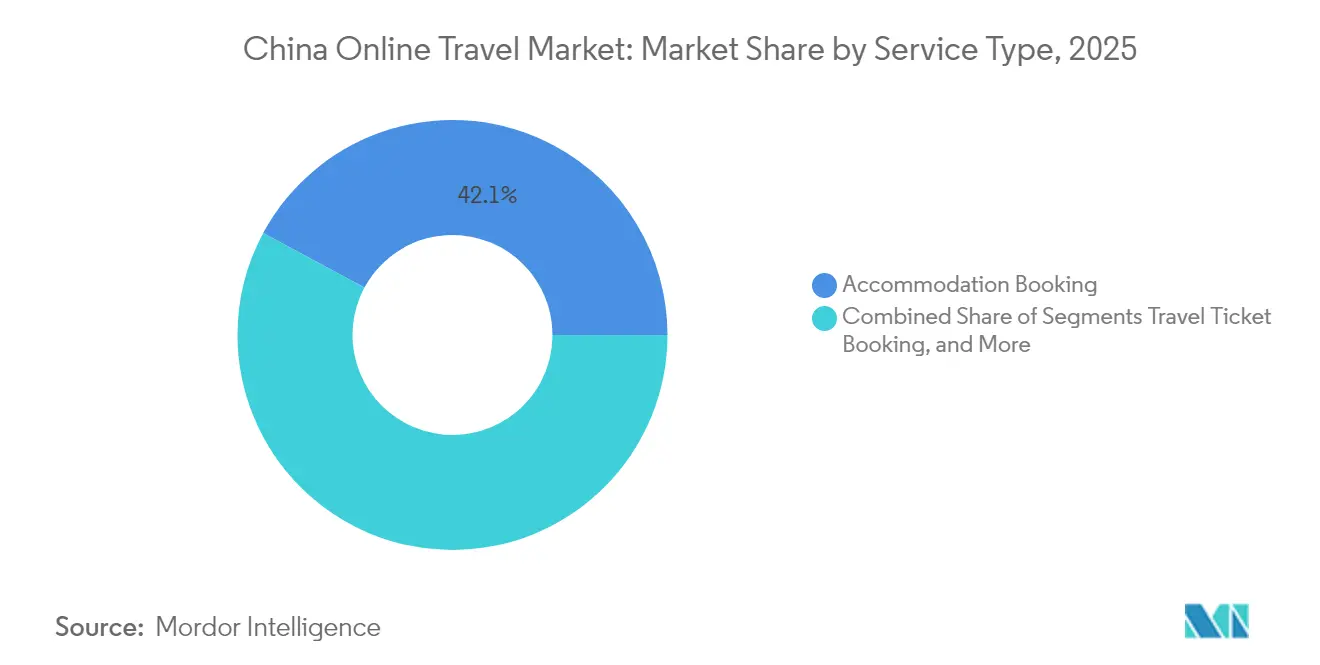

- By service type, accommodation booking led with 42.14% of the China online travel market share in 2025; holiday package booking is forecast to advance at a 16.61% CAGR through 2031.

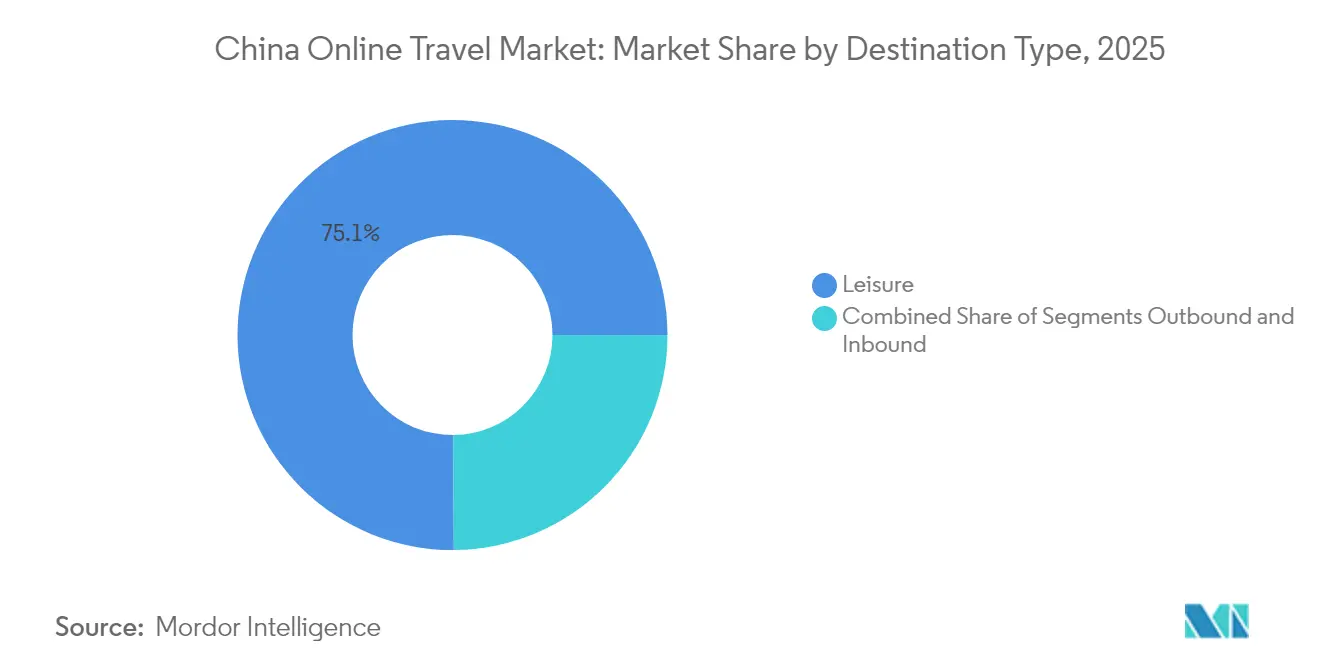

- By traveler type, leisure travelers held 75.10% of the China online travel market in 2025, whereas business travel is set to rise at a 12.41% CAGR.

- By mode of booking, OTAs and travel agents commanded a 68.10% share of the China online travel market in 2025, while supplier direct booking is on track for a 17.32% CAGR.

- By destination type, domestic travel represented 80.05% of the China online travel market size in 2025, and outbound travel is poised to accelerate at a 20.15% CAGR.

- By age group, millennials accounted for 45.52% of the China online travel market in 2025, and Gen Z is projected to expand at an 17.65% CAGR.

- By region, East China holds largest market share around 37.62% and Southwest China are expanding at 7.32% of CAGR to 2031.

- The top five players are Trip.com Group, Meituan-Dianping, Tongcheng-Elong, Qunar.com, and Fliggy which collectively holds significant market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Online Travel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Internet and Smartphone Penetration | +3.2% | National, with stronger impact in Tier 3-5 cities | Short term (≤ 2 years) |

| Government Support for Domestic Tourism | +2.8% | National, with emphasis on cultural and historical destinations | Medium term (2-4 years) |

| Dominance of Super Apps and Travel Platforms | +2.5% | National, with higher adoption in Tier 1-2 cities | Medium term (2-4 years) |

| Growth in Middle-Class and Disposable Income | +2.1% | National, with concentration in eastern coastal regions | Long term (≥ 4 years) |

| Expansion of High-Speed Rail and Domestic Flights | +1.8% | National, connecting previously isolated regions | Medium term (2-4 years) |

| Strong Recovery of Group and Independent Travel | +1.5% | National, with emphasis on popular tourist destinations | Short term (≤ 2 years) |

| AI-Powered Personalization and Dynamic Pricing | +1.2% | National, with higher implementation in Tier 1-2 cities | Medium term (2-4 years) |

| Growth of Tier 2and Tier 3 City Travelers | +0.9% | Central and Western provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Internet and Smartphone Penetration

Smartphone subscriptions now exceed 1.7 billion, and 5G coverage is near-ubiquitous. This connectivity removes physical barriers to booking, especially in smaller cities where brick-and-mortar agencies were scarce. Ubiquitous mobile wallets such as Alipay and WeChat Pay compress checkout times to seconds, even for first-time travelers. Younger cohorts translate that convenience into spontaneous weekend trips, while platforms harvest clickstream data to refine real-time recommendations. The virtuous cycle of wider access, better personalization, and simplified payment keeps the China online travel market on a steep uptake curve.

Government Support for Domestic Tourism

Beijing’s three-year plan for cultural tourism established 19 May as China Tourism Day and bundles tax concessions with bank-subsidized travel coupons to spur local trips. Provincial governments replicate the model with heritage-themed festivals and transport subsidies that lift mid-week hotel occupancy. Policy clarity reduces operator risk, prompting sustained investment in cloud-based reservation systems and data analytics. By directly linking subsidies to digital transactions, authorities funnel incremental traffic toward online platforms, reinforcing the structural shift away from offline channels.

WeChat Mini Programs, Alipay Life Services, and Meituan unify messaging, payments, and reservations in a single user flow. Linking loyalty points to daily coffee purchases and flight seats increases cross-sell potential. Built-in social feeds let travelers crowd-source itineraries, embedding peer validation within the purchase path. For platforms, that ecosystem raises switching costs and shields margins from new entrants. Super-app architecture also underpins voice-activated search and QR-code ticketing, compressing the journey from inspiration to transaction into minutes.

Per-capita disposable income in urban areas reached USD 7,700 in 2025, and nearly 60% of households now fall into the upper-middle-income bracket. This demographic seeks quality upgrades, moving from budget hotels to design-led boutique properties and curated small-group tours. Spending elasticity allows OTAs to bundle insurance, lounge access, and in-destination activities, lifting average order values. The trend is particularly visible along the eastern seaboard, but inland cities such as Chengdu and Xi’an record double-digit increases in premium package bookings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Crackdowns on Tech and Data | -1.9% | National, with emphasis on major tech hubs | Medium term (2-4 years) |

| Economic Uncertainty and Consumer Caution | -1.7% | National, with stronger impact in Tier 1 cities | Short term (≤ 2 years) |

| Competition from Offline and Direct Channels | -1.4% | National, with emphasis on traditional tourist areas | Medium term (2-4 years) |

| Rising Customer Acquisition Costs | -1.2% | National, with higher impact in saturated markets | Medium term (2-4 years) |

| Overdependence on Domestic Tourism | -1.0% | National, particularly affecting international gateway cities | Long term (≥ 4 years) |

| Disruptions from Public Health or Geopolitical Risks | -0.8% | Global, with varying regional impacts | Short term (≤ 2 years) |

| High Platform Commission Fees | -0.7% | National, affecting smaller service providers | Medium term (2-4 years) |

| Fragmentation of User Preferences | -0.5% | National, with stronger impact in younger demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Crackdowns on Tech and Data

The Cross-border Data Flow Provisions require security assessments for outbound data deemed sensitive, compelling OTAs to localize servers and deploy encryption. Compliance outlays erode smaller players’ margins and slow feature roll-outs. Yet clarified guidelines are also reducing gray zones, letting well-capitalized incumbents incorporate privacy-preserving AI models with government-approved safeguards. Long-run effects, therefore, skew toward consolidation rather than outright contraction.

Economic Uncertainty and Consumer Caution

Property-sector volatility and subdued wage growth temper discretionary spending, notably in Tier 1 cities where living costs bite hardest. Travelers pivot toward value-driven “all-in” bundles that cap per-trip expenses. OTAs respond with flexible payment plans and algorithmic discounts. While macro headwinds shave growth in premium categories, pent-up wanderlust in lower-tier markets cushions overall demand, leaving the China online travel market expansion intact though slightly moderated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Platforms Broaden Lodging and Package Portfolios

Accommodation booking steered 42.14% of the China online travel market in 2025, translating to deep commission pools that fund aggressive loyalty campaigns. AI-powered filters parse guest reviews and real-time rate parity to surface room types aligned with individual budgets and amenity priorities. That granular targeting keeps cancellation rates low, boosting hotel-OTA alignment. Holiday package booking, projected to grow at 16.61% CAGR, appeals to new travelers from Tier 3 cities who prefer turnkey itineraries that bundle transport, lodging, and insurance under one QR code.

The accommodation subsector now spills into alternative inventory: homestays, serviced apartments, and pop-up “glamping” pods in lesser-known scenic zones. Major OTAs integrate user-generated micro-videos to preview properties, converting inspiration to booking within the same scroll cycle. Meanwhile, add-on services are airport transfers, local SIM cards, and attraction e-tickets to create ancillary revenue streams that move platforms closer to one-stop lifestyle ecosystems.

By Traveler Type: Leisure Dominates, Business Travel Recovers

Leisure accounted for 75.10% of the China online travel market in 2025, buoyed by social-media storytelling and flash-sale channels that spark impromptu getaways. Short-distance “micro-vacations” drive weekday demand spikes, smoothing seasonality for operators. Business travel, growing at 12.41% CAGR, rebounds as corporations resume in-person deal-making. Digital travel-management dashboards cum expense platforms integrate policy compliance, decision support, and live rebooking, letting finance teams track carbon output and per-diem metrics.

Hybrid “bleisure” itineraries blur segment lines: executives tack a weekend onto a client visit, swelling average stay lengths and cab ride receipts. OTAs curate bundles that align corporate hotel caps with leisure upgrade options, such as spa credits or attraction passes financed through employee wellness budgets.

By Mode of Booking: OTAs Retain Lead as Direct Channels Scale

OTAs and travel agents held 68.10% of bookings in 2025, anchoring the China online travel market through expansive inventory breadth and tiered membership benefits. Machine-learning engines re-rank search results based on loyalty status and price sensitivity, boosting cross-sell from rail to hotels to car rentals. Supplier direct channels, expected to rise at 17.32% CAGR, harness brand apps and mini-programs to reclaim distribution margins.

Hotels lure users with mobile check-in, digital room keys, and breakfast credits unavailable on OTAs, while airlines deploy branded credit cards and tier-match promotions. The tug-of-war stimulates product innovation: OTAs add “best price guarantee” refunds issued instantly to wallet balances, and suppliers partner with fintechs for zero-interest installment plans, ensuring frictionless payment even on big-ticket itineraries.

By Destination Type: Domestic Still Rules, Outbound Takes Flight

Domestic trips represented 80.05% of the China online travel market size in 2025, propelled by high-speed rail lines that place 70% of the population within 3 hours of a coastal city. Provincial subsidies fund museum admissions and rural homestay renovations, further encouraging internal exploration. Outbound travel, forecast to surge at 20.15% CAGR, gains traction as 15-day visa-free entry to Thailand, Malaysia, and Singapore rolls out.

OTAs pre-package international SIM cards and airport lounge passes into one-click “Smart Departure” kits that simplify border crossings. On the inbound side, duty-free expansions in Hainan and Guangdong attract overseas visitors who leverage Chinese e-wallets, creating two-way traffic that strengthens airline route economics.

By Age Group: Gen Z Pushes Digital-First, Millennial Wallets Still Heaviest

Millennials own 45.52% of the China online travel market, combining mid-career incomes with digital familiarity. They respond to sustainability badges and flexible cancellation more than rock-bottom prices. Gen Z, projected to compound at 17.65% CAGR, treats travel as a live-stream moment: 60-second destination reels translate directly into booking clicks. Platforms integrate augmented-reality previews, letting users visualize street-food tours or ski runs before paying, aligning tightly with Gen Z’s immersive expectations.

Gen X prefers family-centric packages with stroller rentals and theme-park fast passes, while boomers show willingness to spend when health-focused perks such as 24-hour tele-consult lines are included. This demographic layering compels OTAs to maintain multi-modal engagement—from customer-service chatbots for Gen Z to phone-hotline concierges for seniors, avoiding one-size-fits-all approaches.

Geography Analysis

The China online travel market geography displays a multi-centered pattern rather than the traditional coastal skew. Tier 1 cities remain revenue leaders but face near-full penetration, prompting OTAs to shift marketing budgets inland. Chengdu, Chongqing, and Wuhan post the fastest booking growth thanks to expanded airport hubs and localized advertising on short-video platforms. Digital wallets backed by local banks lower payment friction, helping first-time users who distrust credit cards.

East China commands the largest regional market share at 37.62% in 2025, establishing itself as the dominant geographic segment in China's tourism and hotel market. This region encompasses major economic powerhouses, including Shanghai, Jiangsu, Zhejiang, Anhui, Fujian, Jiangxi, and Shandong provinces, which collectively represent China's most developed and internationally connected areas.

Southwest China, while representing a smaller current market share, is experiencing rapid expansion at 7.32% CAGR, making it the fastest-growing regional segment. This region includes Sichuan, Yunnan, Guizhou, Chongqing, and Tibet, areas that have benefited from significant government investment in infrastructure development and tourism promotion. The region's growth is driven by its unique combination of natural attractions, ethnic cultural diversity, and emerging urban centers that are attracting increasing numbers of domestic tourists seeking authentic experiences beyond traditional coastal destinations.

Competitive Landscape

The China online travel market concentrates power in a handful of ecosystems. Trip.com Group fuses flights, hotels, rail, and corporate travel onto one backend, cross-selling insurance underwritten by Ping An. Meituan turns dining coupons into travel triggers, sending restaurant customers hotel flash deals within the same app session. Tongcheng-Elong leverages Tencent traffic, while Qunar optimizes metasearch across affiliate partners. Fliggy, backed by Alibaba, embeds travel into Taobao’s live-commerce sessions, letting key opinion leaders showcase hotel rooms via shoppable livestreams.

Strategic skirmishes intensify around content commerce. Xiaohongshu and Douyin convert influencer trip diaries into one-click reservations, forcing incumbents to nurture creator communities via revenue-share programs. AI is the common weapon: recommendation engines analyze not only past bookings but also ride-hailing logs and food-delivery orders to infer taste profiles. White-space innovation surfaces in luxury rail journeys and wellness retreats, segments where middle-aged professionals seek privacy and exclusive add-ons.

China Online Travel Industry Leaders

Trip.com Group Ltd

Meituan-Dianping

Tongcheng-Elong Holdings Ltd

Qunar.com

Fliggy (Alibaba)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Trip.com announced a strategic alliance with ITB China to pilot generative-AI itinerary builders across its domestic platforms, aiming to cut trip-planning time by 40% Trip.com.

- April 2025: Tongcheng-Travel introduced a “First Time, Worry-Free” concierge program for new flyers from Tier 3 cities, providing 24-hour in-app guidance Tongchengtravel.com.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines China's online travel market as the total transaction value generated when residents or inbound visitors book transport, lodging, packaged vacations, or ancillary activities through internet-based interfaces, desktop sites, mobile browsers, super-apps, and OTA apps alike.

Scope exclusion: purchases made entirely offline (walk-in agencies, hotel front desks, rail station counters) fall outside this assessment.

Segmentation Overview

- By Tourism Type

- Domestic Tourism

- Inbound Tourism

- Outbound Tourism

- By Purpose

- Leisure & Adventure & Eco-Tourism

- Business / MICE

- By Traveler Age

- Generation Z (18-24)

- Millennials (25-40)

- Generation X (41-56)

- Baby Boomers (57+)

- By Booking Channel

- Online Travel Agencies (OTAs)

- Direct Hotel Websites & Apps

- Offline Travel Agencies

- By Hotel Category

- Economy / Budget Hotels

- Mid-scale Hotels

- Upscale Hotels

- Luxury Hotels

- Serviced Apartments & Long-Stay

- By Ownership / Branding

- Independent Hotels

- Domestic Chain-Affiliated Hotels

- International Chain-Affiliated Hotels

- By Region

- Central China

- East China

- North China

- Northeast China

- Northwest China

- South China

- Southwest China

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with OTA executives, hotel revenue managers, low-cost airline route planners, and payment-gateway integrators across Beijing, Shanghai, Chengdu, and Guangzhou. These conversations validated segment shares, typical take-rates, and discounting trends that raw desk data could not fully capture.

Desk Research

We began by mapping the sector using freely accessible tier-1 repositories such as the National Bureau of Statistics of China, Ministry of Culture & Tourism visitor flows, UNWTO tourism dashboards, and civil aviation and railway traffic releases. Trade groups like the China Tourism Academy and China Internet Network Information Center supplied traveler sentiment, internet penetration, and mobile payment adoption metrics. Corporate filings, investor decks, and press releases from listed OTAs enriched pricing and margin clues, while D&B Hoovers and Dow Jones Factiva gave us financial sanity checks. This list illustrates, rather than exhausts, the secondary sources screened.

Market-Sizing & Forecasting

We anchor 2025 market size by combining top-down reconstruction of domestic, outbound, and inbound trip volumes with average spending per online booking, which are then corroborated against a bottom-up roll-up of sampled OTA gross bookings and supplier channel checks. Key drivers in the model include smartphone penetration, discretionary income growth, airline seat capacity, high-speed rail mileage, and digital wallet usage. A multivariate regression framework links these drivers to historical online booking values, while scenario analysis adjusts for regulatory or macro shocks. Gaps in bottom-up estimates, common for smaller regional portals, are bridged using regional penetration proxies and verified with interview feedback.

Data Validation & Update Cycle

Outputs undergo variance screening versus independent tourism receipts, foreign exchange data, and publicly reported OTA revenues. Senior reviewers challenge anomalies before sign-off. We refresh numbers annually and reopen the model whenever policy shifts, pandemics, or major M&A events materially alter assumptions.

Why Mordor's Online Travel Market in China Size & Share Analysis Baseline Commands Reliability

Published market figures often differ because firms choose dissimilar service mixes, traveler cohorts, and refresh cadences.

Key gap drivers include whether outbound bookings are counted at point of sale or consumption, how package mark-ups are treated, and the cadence at which average selling prices are refreshed; variables Mordor standardizes through yearly verification with both suppliers and buyers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 105.1 B (2025) | Mordor Intelligence | - |

| USD 91.2 B (2024) | Regional Consultancy A | Excludes ancillary add-ons; older base year skews growth path |

| 110.8 ~ (2024 online share derived from total travel) | Trade Journal B | Uses fixed 73 % online penetration without segment validation |

Taken together, the comparison shows that when scope, timely pricing, and dual-path modeling are aligned, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the China online travel market in 2026?

The market stands at USD 120.98 billion in 2026 and is on a 15.08% CAGR growth path toward USD 244.14 billion by 2031.

Which segment holds the largest China online travel market share?

Accommodation booking leads with 42.14% share, reflecting the essential nature of lodging in any itinerary.

How fast is outbound travel from China expected to grow?

Outbound bookings are projected to accelerate at a 20.15% CAGR between 2026 and 2031, driven by visa-free policies and expanding airlift.

Who are the major players in the China online travel industry?

Trip.com Group, Meituan-Dianping, Tongcheng-Elong, Qunar.com, and Fliggy collectively control 89% of revenue, making the landscape highly concentrated.

What role do super-apps play in China’s travel ecosystem?

Super-apps such as WeChat and Alipay integrate payment, social sharing, and booking functions, raising user convenience and platform stickiness while heightening barriers for standalone newcomers.

Page last updated on: