Offshore Helicopter Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.82 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Helicopter Services Market Analysis by Mordor Intelligence

The Offshore Helicopter Services Market size is expected to increase from USD 3.68 billion in 2025 to USD 3.82 billion in 2026 and reach USD 4.64 billion by 2031, growing at a CAGR of 3.97% over 2026-2031. Fleet renewal toward super-medium twins, rapid offshore wind build-out, and stricter digital-safety rules are reshaping operator economics. Super-medium helicopters already displace legacy heavy twins on routes up to 200 nautical miles because they cut fuel burn by 20% to 30% while preserving 14-to-16-passenger capacity.[1]Airbus, “2025 Helicopter Orders,” airbus.com Offshore wind’s 9.0% CAGR through 2031 cushions revenue swings in oil and gas, but service providers must invest in hoist-capable aircraft and sustainable aviation-fuel (SAF) logistics to win premium contracts.[2]Orrick, “Global Offshore Wind Report 2025,” orrick.com Meanwhile, deep-water E&P budgets exceeding USD 7 billion from Chevron alone in 2026 keep long-range crew-change demand resilient.[3]Chevron, “Offshore Capital Expenditure 2026,” chevron.com Consolidation around power-by-the-hour maintenance, SAF adoption, and data-driven compliance is creating entry barriers that favor scale operators with diversified multi-OEM fleets.[4]Bristow, “Leonardo 10-Year Support Deal,” bristowgroup.com

Key Report Takeaways

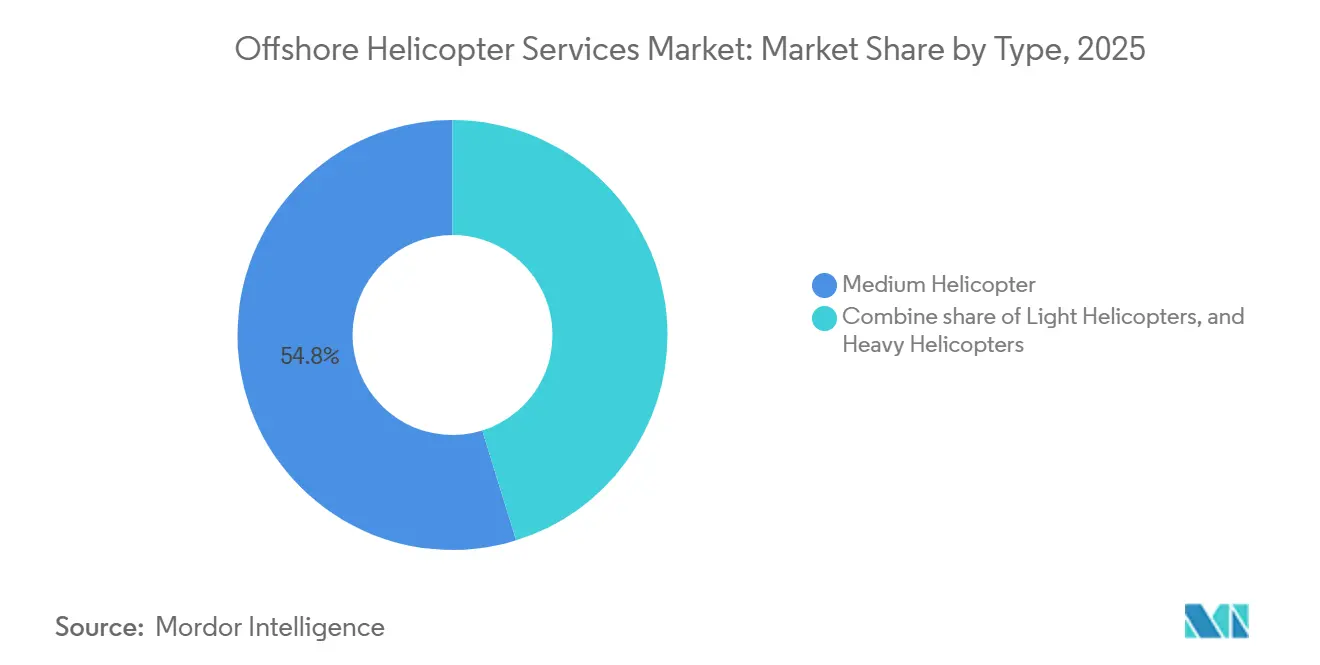

- By type, medium helicopters led with 53.7% of offshore helicopter services market share in 2025, while light helicopters are forecast to grow fastest at 6.3% CAGR through 2031.

- By application, crew transport accounted for 45.1% of offshore helicopter services market size in 2025 and inspection, monitoring, and surveying is set to expand at a 7.1% CAGR to 2031.

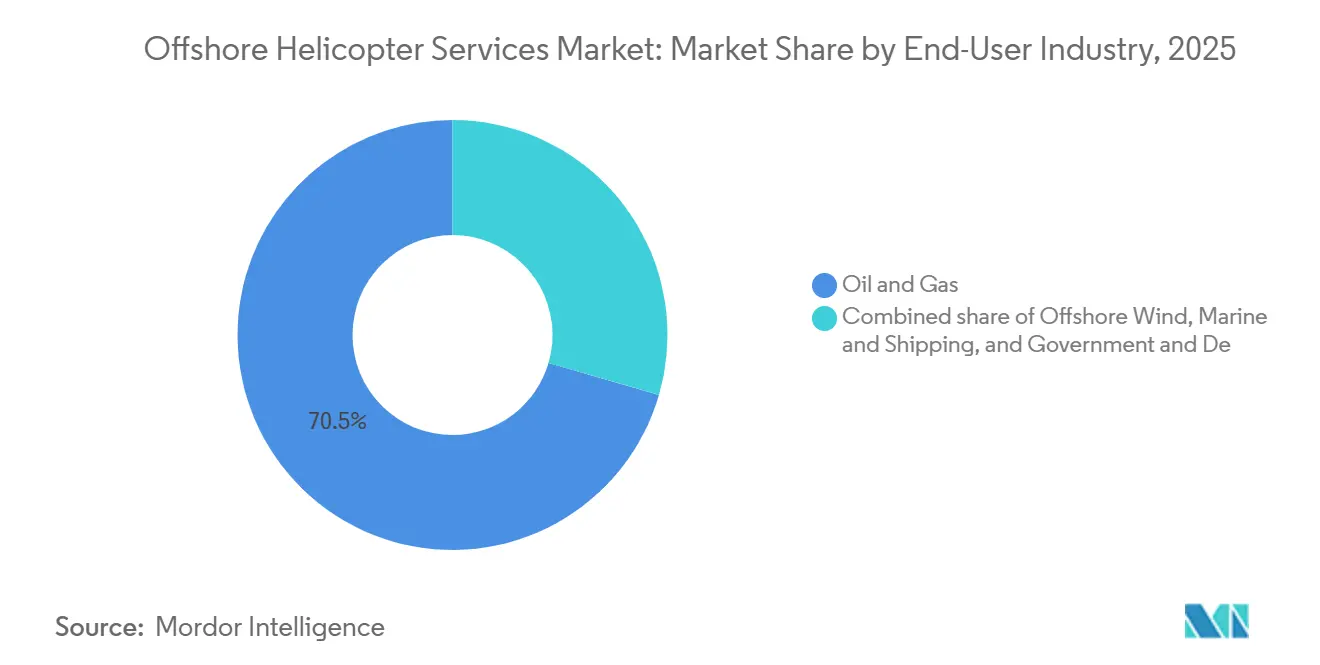

- By end-user industry, oil and gas accounted for 70.5% of offshore helicopter services market size in 2025 and offshore wind is set to expand at a 9% CAGR to 2031.

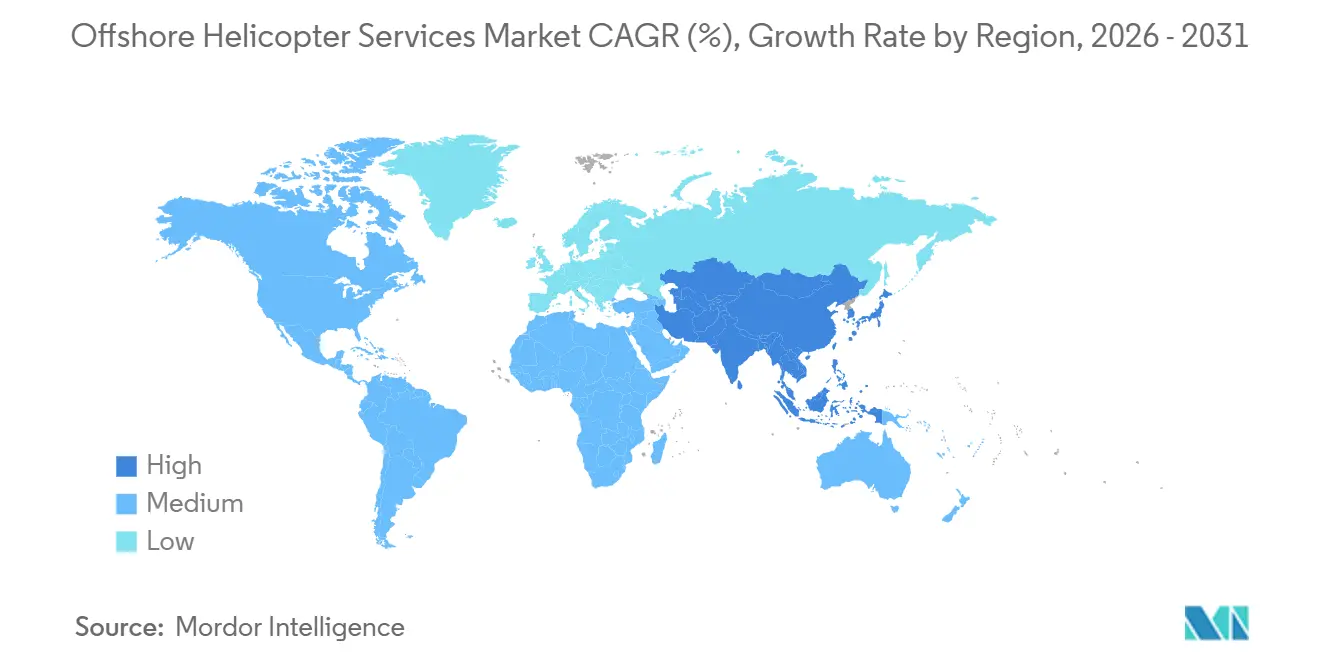

- By geography, North America dominated with 31.9% share in 2025 whereas Asia-Pacific is projected to post the highest 6.8% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Offshore Helicopter Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Deep- and Ultra-Deep-Water E&P Spending | +1.20% | South America, North America, West Africa | Medium term (2-4 years) |

| Accelerating Build-Out of Offshore Wind Farms | +1.50% | Europe, Asia-Pacific, North America | Long term (≥ 4 years) |

| Fleet Modernization Toward Medium-Heavy Twins | +0.80% | Global | Short term (≤ 2 years) |

| Digitalised Safety Mandates | +0.30% | Europe, North America | Short term (≤ 2 years) |

| Growth of Hybrid-/E-Fuel Retrofit Programs | +0.40% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Deep- and Ultra-Deep-Water E&P Spending

Investment momentum continues as operators chase high-margin barrels in ultra-deep basins where helicopters remain the only viable crew-change option. Chevron allocated USD 7 billion to offshore CAPEX in 2026, prioritizing Gulf of Mexico tie-backs that demand super-medium range. Guyana’s output reached 918,000 barrels per day in 2026 and will climb when ExxonMobil’s Uaru FPSO adds 250,000 barrels per day more than 190 kilometers offshore. Petrobras committed over USD 12 billion to SEAP I/II pre-salt projects in waters deeper than 2,000 meters, locking in helicopter utilization for decades. Subsea7’s USD 1.25 billion Búzios 9 contract underlines the subsea infrastructure that will require aerial inspection and emergency cover. Combined, these programs are expected to keep offshore helicopter fleet utilization above 70% through 2031.

Accelerating Build-Out of Offshore Wind Farms

Global installed offshore wind capacity hit 89.2 GW in 2025 and continues to rise on projections of 9.0% CAGR to 2031. China alone added 6 GW in 2025, while Europe advanced megaprojects such as Hornsea 3 at 2.9 GW. Vietnam cleared targets that could reach 17 GW by 2035, creating new hoist-mission demand beyond 80 nautical miles. NHV logs up to 100 flight-hours per month on H175s for Vestas at Baltic Power, showing how super-medium platforms can complement crew-transfer vessels on distant wind zones. Although drones cut routine inspection sorties, emergency blade repair and medical evacuation keep helicopters integral to wind-farm O&M cycles.

Fleet Modernization Toward Medium-Heavy Twins

Operators retire costly heavy S-92s in favor of AW189s and H175s that match payload with lower fuel burn. Bristow’s firm order for 10 AW189s, scheduled for delivery through 2028, cements the type as its primary offshore workhorse. PHI inked an H175 framework accord and incremental AW189 purchases to diversify away from gearbox-challenged S-92s. Airbus booked 544 helicopter orders in 2025 super-mediums represented the bulk thanks to performance and IOGP-compliant avionics. Leonardo’s AW189 run-dry main transmission and satellite HUMS reduce unscheduled downtime by up to 20%, supporting power-by-the-hour maintenance economics. As support packages cap residual-value risk, the offshore helicopter services market pivots decisively toward super-medium fleets.

Growth of Hybrid-/E-Fuel Retrofit Programs

Europe’s emissions-trading deadlines spur SAF uptake and hybrid demonstrators. NHV and Vestas operate H175s on 40% SAF, yielding 32% lifecycle carbon cuts without engine change. HeliService flies AW139s and AW169s on identical blends at Baltic Eagle, proving drop-in fuels match offshore mission demands. Airbus PioneerLab targets 30% fuel-efficiency gains with a hybrid H145 testbed slated for 2027. Sikorsky’s HEX tilt-wing couples a GE CT7 to a 1.2-MW generator to exceed 500 nautical-mile range in 2027 trials. Contracts in European wind farms already stipulate minimum 30% SAF blends from 2028, separating compliant fleets from legacy operators.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Crew-Transfer Vessels | -0.60% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| Oil-Price Volatility Curbing Drilling Budgets | -0.90% | Global | Medium term (2-4 years) |

| Global Shortage of Certified Offshore-Rated Pilots | -0.40% | Global | Long term (≥ 4 years) |

| Prolonged S-92 Gearbox Bottlenecks | -0.50% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Crew-Transfer Vessels

Crew-transfer vessels move crews at under half the cost of helicopters on routes below 50 nautical miles and emit 60% less carbon per passenger-kilometer. Wind-farm operators accept higher injury risk to meet ESG budgets, so helicopters now focus on long-range, hoist, and medevac sorties. NHV’s H175s at Baltic Power demonstrate the unique capability to move multiple teams and conduct stretcher hoists in one flight, which CTVs cannot match. The most acute substitution threat lies in shallow European and Chinese wind zones where CTVs could absorb up to 70% of short-haul volume by 2028.

Oil-Price Volatility Curbing Drilling Budgets

Wood Mackenzie expects Brent to average USD 60 per barrel in 2026 amid a 2.3 million-barrel-per-day surplus, prompting operators to delay deep-water sanctioning. Transocean’s backlog declined as clients shifted to short-cycle shale, cutting helicopter hours on floating rigs. Rystad recorded a 12% drop in deep-water FIDs during 2025, reinforcing the link between commodity cycles and flight demand. Bristow mitigated exposure through a USD 196 million Barents SAR contract that guarantees utilization regardless of oil price. Diversification into wind and government SAR is becoming standard practice to buffer cyclical drilling cuts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Super-Mediums Displace Legacy Heavies

Medium helicopters dominated with 53.7% offshore helicopter services market share in 2025 thanks to AW189 and H175 fleets that deliver 14-to-16-seat capacity at 20% lower fuel burn than heavy twins. The offshore helicopter services market size tied to light types will accelerate at 6.3% CAGR through 2031 as marginal-field crew changes and wind inspection reward agility.

Operators increasingly tailor fleet mix to route length instead of defaulting to heavy platforms. Light AW139s cover sub-100-nautical-mile hops, super-mediums handle 150-plus-nautical-mile missions with hoist, and heavies stay on ultra-long routes above 300 nautical miles or Arctic duty. Abu Dhabi Aviation’s fresh order for six AW139s shows Middle East carriers modernizing regional fleets under new IOGP rules. By 2031, super-mediums are forecast to exceed 60% of total fleet, while heavies drop below 15% as S-92s retire.

By Application: Inspection Growth Outpaces Crew Transport

Crew transport represented 45.1% of offshore helicopter services market size in 2025, yet inspection, monitoring, and surveying will post a 7.1% CAGR to 2031.

Hybrid human-drone workflows are reshaping demand. Ørsted cuts routine sorties 7.5-fold with tethered drones, but still calls helicopters for emergency blade repair and medevac. Shell’s Turritella used an ROV to finish the first class-approved no-entry FPSO inspection, saving 40% of cost but retaining helicopter standby for confined-space rescue. Decommissioning support emerges as a premium niche because lifting teams and equipment during platform dismantling needs vertical access in tight windows. The application mix will skew toward higher-margin, lower-volume missions that value technical skill over seat-mile price.

By End-User Industry: Offshore Wind Disrupts Oil-Gas Dominance

Oil and gas retained 70.5% share of the offshore helicopter services market in 2025, yet offshore wind will expand at 9.0% CAGR and capture up to 25% share by 2031.

Deep-water oil projects such as Petrobras SEAP I/II and ExxonMobil’s Guyana expansions still need long-range helicopters through 2035. Wind developers increasingly award long-term hoist contracts: CHC supports Hornsea 3 with H175s, and NHV logs 100 monthly flight hours for Vestas at Baltic Power. Marine and shipping, plus government and defense, offer counter-cyclical demand at 10%-15% share through search-and-rescue or pilot-transfer missions. A more balanced revenue mix will shield operators from oil-price swings.

Geography Analysis

North America accounted for 31.9% of offshore helicopter services market share in 2025, anchored by Gulf of Mexico deep-water fields and Arctic Barents contracts. Bristow’s NOK 1.9 billion Barents agreement deploys two S-92 transports and one SAR variant, servicing up to 3,400 passengers per month. CHC and Lufttransport together landed a NOK 4.3 billion Bergen contract to fly three S-92s and two AW189s to Troll, Gullfaks, and Oseberg starting May 2026. Although shallow-water Gulf routes see CTV encroachment, ultra-deep-water hubs and harsh-weather Arctic missions keep helicopter demand robust.

Europe remains the historical nucleus of the offshore helicopter services market. NHV introduced Airbus H160s financed by GD Helicopter Finance for North Sea and Baltic wind work beginning May 2026. Avincis entered offshore wind through the KN Helicopters buyout, adding H135s and H145s in Denmark. Mandatory helideck monitoring and HUMS upgrades under UK CAA and EASA rules raise compliance costs but also solidify barriers to entry.

Asia-Pacific is the fastest-growing region at 6.8% CAGR to 2031. Jadestone’s Nam Du and U Minh gas project approval and ONGC’s extended Vietnam Block 06.1 license will add long-range crew changes above 100 nautical miles. China added 6 GW of offshore wind capacity in 2025 yet remains CTV-centric, providing a white-space for super-medium helicopter entrants. Global Vectra supports ONGC and Reliance from Mumbai bases with over 25 helicopters, illustrating domestic fleet capability growth. South America accelerates on Guyana’s march toward 1 million bpd and Brazil’s pre-salt programs, while Middle East-Africa posts steady demand from Mozambique LNG and Angola’s USD 7.8 billion Agogo development.

Competitive Landscape

The top five operators Bristow, CHC, PHI, Era, and Abu Dhabi Aviation controls significant share of global capacity, indicating moderate concentration. Bristow wrapped a 10-year global service pact with Leonardo bundling inventory, HUMS, and simulators, stabilizing maintenance cash flows. CHC secured more than USD 1 billion in multi-year contracts during 2025, including a NOK 4.3 billion Equinor deal, proving that scale plus OEM alliances steer tender wins.

Technology diffusion shapes competition. NHV’s Helionix-equipped H175s achieve reduced-visibility minima, giving an operational edge in winter North Sea conditions. Leonardo’s satellite-linked AW189 predictive maintenance cuts downtime by 20%, enhancing bid competitiveness. Lessors are consolidating: SMFL Helicopters emerged from LCI and Macquarie Rotorcraft’s merger with 290 aircraft, offering operators capital-light access to new models.

Strategic moves expand footprints. The Helicopter Company bought 76% of Heliconia to target West African offshore contracts. GD Helicopter Finance is acquiring NHV, keeping the brand independent but infusing fleet-expansion capital. SAF capability and hybrid-retrofit roadmaps increasingly sway procurement, positioning early adopters for 2027 EU emissions trading thresholds.

Offshore Helicopter Services Industry Leaders

Bristow Group Inc.

CHC Group Ltd.

PHI Inc.

Abu Dhabi Aviation PJSC

NHV Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NHV Group introduced two Airbus H160s financed by GDHF, entering North Sea service in May 2026.

- March 2026: SMFL Helicopters launched after SMFL merged LCI and Macquarie Rotorcraft, creating a 290-aircraft lessor.

- March 2026: CHC do Brazil won an Equinor Bacalhau crew-change deal using an S-92A from early Feb 2026.

- February 2026: Equinor and Vår Energi awarded Bristow a NOK 1.9 billion Barents Sea transport and SAR contract effective Sept 2026.

Global Offshore Helicopter Services Market Report Scope

Offshore helicopter services provide specialized aerial transportation, facilitating the movement of personnel, equipment, and cargo between onshore bases and offshore locations such as oil rigs, production platforms, ships, and wind farms. These services play a vital role in energy sector logistics, supporting crew transfers and emergency operations in challenging and remote environments.

The Offshore Helicopter Services Market is segmented into type, application, end-user industry, and geography. By type, the market is segmented into light helicopters, medium helicopters, and heavy helicopters. By application, the market is segmented into crew transport, cargo transport, inspection/monitoring/surveying, relocation/decommissioning support, and other applications. By end-user industry, the market is segmented into oil and gas, offshore wind, marine and shipping, and government and defence. The report also covers the market size and forecasts for the offshore helicopter services market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Light Helicopters |

| Medium Helicopters |

| Heavy Helicopters |

| Crew Transport |

| Cargo Transport |

| Inspection, Monitoring, and Surveying |

| Relocation and Decommissioning Support |

| Other Applications |

| Oil and Gas |

| Offshore Wind |

| Marine and Shipping |

| Government and Defence |

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle East and Africa |

| By Type | Light Helicopters |

| Medium Helicopters | |

| Heavy Helicopters | |

| By Application | Crew Transport |

| Cargo Transport | |

| Inspection, Monitoring, and Surveying | |

| Relocation and Decommissioning Support | |

| Other Applications | |

| By End-user Industry | Oil and Gas |

| Offshore Wind | |

| Marine and Shipping | |

| Government and Defence | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the offshore helicopter services market today and where is it heading by 2031?

The offshore helicopter services market size stands at USD 3.82 billion in 2026 and is projected to reach USD 4.64 billion by 2031, growing at a 3.97% CAGR.

Which helicopter segment is expanding the fastest?

Light helicopters are forecast to post a 6.3% CAGR through 2031 due to rising demand for wind-farm inspection and marginal-field crew changes.

What share does offshore wind hold and how fast is it growing?

Offshore wind represents about 20% of end-user demand in 2026 and is advancing at a 9.0% CAGR, potentially reaching 25% share by 2031.

Which region will contribute most to incremental growth?

Asia-Pacific is set to register the highest 6.8% CAGR to 2031, propelled by Vietnam gas projects and Chinas expanding offshore wind fleet.

How are operators addressing sustainability mandates?

Leading carriers are flying 40% SAF blends and ordering super-medium helicopters with predictive-maintenance suites, while OEMs target hybrid-electric demonstrators for post-2027 deployment.

What is the main competitive edge for large operators?

Scale enables multi-OEM fleets, power-by-the-hour maintenance deals, and the capital required to meet digital safety and emissions regulations that smaller rivals struggle to finance.

Page last updated on: