North America Offshore Helicopter Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

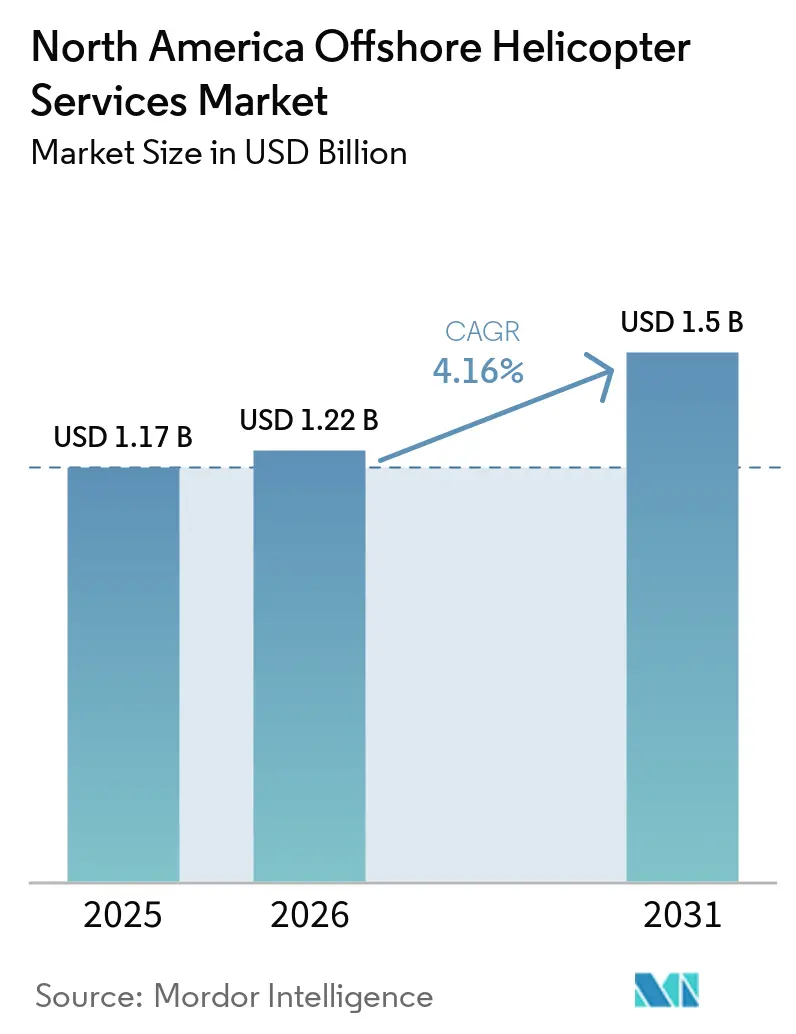

| Base Year Market Size (2025) | USD 1.17 Billion |

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

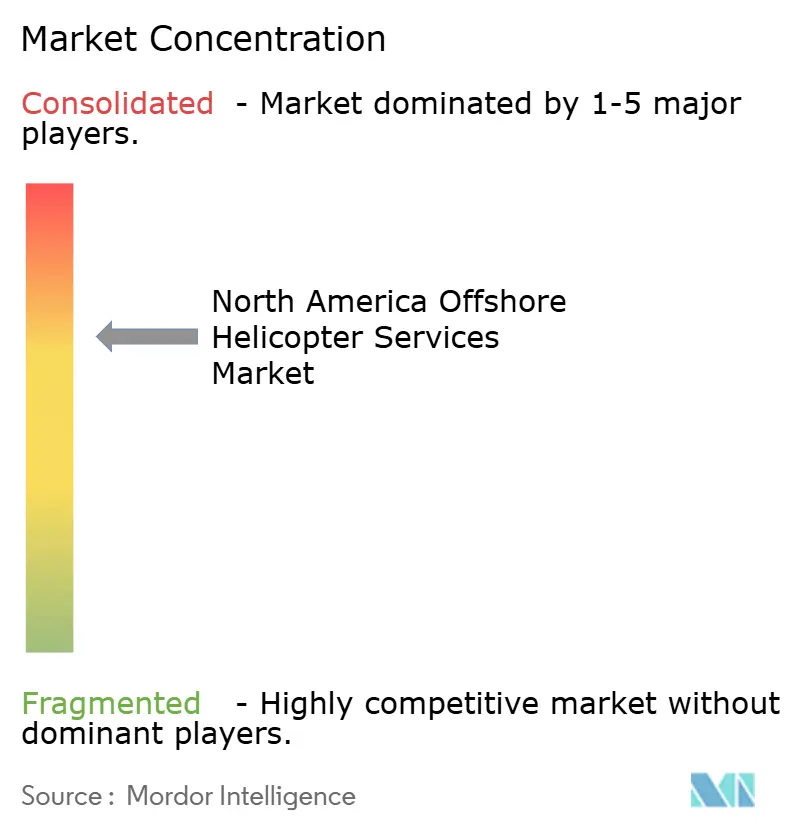

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Offshore Helicopter Services Market Analysis by Mordor Intelligence

The North America Offshore Helicopter Services Market size is expected to grow from USD 1.17 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.5 billion by 2031 at 4.16% CAGR over 2026-2031. Fleet-modernization cycles that favor super-medium platforms, deep-water Gulf of Mexico drilling programs, and the first wave of Atlantic offshore-wind construction are underpinning steady demand even as oil-price volatility recedes as a dominant growth determinant. Operators are reshaping cost structures by phasing out fuel-intensive heavy twins and introducing Leonardo AW189, Airbus H175, and Bell 525 airframes that deliver 20-30% lower fuel burn per passenger-mile, widening margins despite persistent inflationary pressure on spare-parts procurement. Simultaneously, the Bureau of Ocean Energy Management’s (BOEM) lease pipeline for more than 50 gigawatts of wind capacity is opening a second revenue pillar that offsets cyclical downturns in exploration drilling. Medium helicopters kept a 51.7% share in 2025, yet light twins posted the fastest order growth as operators pivot toward inspection, monitoring, and harbor-pilot shuttle missions that do not require the S-92’s lift envelope. On the regulatory front, U.S. Federal Aviation Administration (FAA) Part 135 retrofit mandates effective May 2027 are accelerating fleet consolidation because smaller owners often lack the capital to install flight-data recorders and terrain-awareness systems [1]Federal Aviation Administration, “Part 135 Continuous Operations Safety Mandate,” faa.gov.

Key Report Takeaways

- By type, medium helicopters led with 51.7% of the North America offshore helicopter services market share in 2025, light helicopters are projected to post the fastest growth at a 6.6% CAGR between 2026-2031.

- By application, crew transport dominated with 42.1% revenue share in 2025, while inspection and monitoring is advancing at a 7.3% CAGR to 2031.

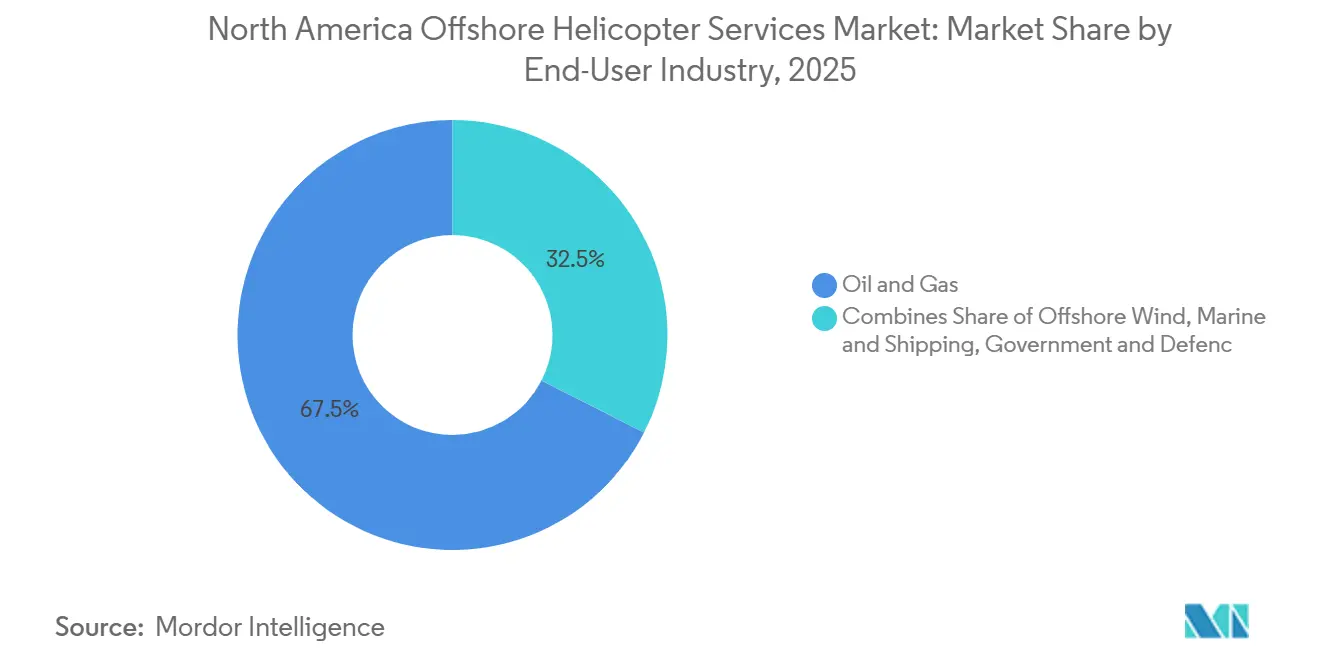

- By end-user, oil and gas accounted for 67.5% of demand in 2025; offshore wind is expanding at 9.5% CAGR through 2031.

- By geography, the United States commanded 79.9% of 2025 revenue; Mexico is the fastest-growing country at 6.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Offshore Helicopter Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deep-water offshore development activity | +1.2% | United States (Gulf of Mexico), Mexico (Trion field) | Medium term (2-4 years) |

| Improved viability of offshore oil & gas projects | +0.9% | United States, Canada (Newfoundland, Nova Scotia) | Long term (≥ 4 years) |

| Expansion of U.S. offshore-wind construction zone | +1.5% | United States (East Coast: New York Bight, Gulf of Maine) | Long term (≥ 4 years) |

| Fleet-modernization cycle (AW139/S-92 replacements) | +0.7% | North America (United States, Canada, Mexico) | Short term (≤ 2 years) |

| U.S. SAF tax-credit incentives lowering fuel costs | +0.3% | United States | Medium term (2-4 years) |

| AI-driven predictive-maintenance savings | +0.5% | North America (operators with advanced HUMS systems) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Deep-Water Offshore Development Activity

Gulf of Mexico Lease Sale 261 in March 2024 awarded 73 tracts covering 395,000 acres and produced USD 382 million in high bids, demonstrating strong operator appetite for acreage in water depths that necessitate 90-minute helicopter transits from Houma and Lafayette shore bases. Shell followed by approving up to four exploration wells for 2025-2026 targeting prospects below 1,500 meters, sustaining call-outs for medium and heavy helicopters certified to Sea State 6 survival requirements. Mexico’s Trion field, 180 kilometers offshore at 2,500 meters, began drilling in 2024 and plans 24 subsea wells that will rely on Tampico-based super-medium aircraft for crew rotations as soon as 2028. Nova Scotia’s 2026 licensing round covering the Sable Island area re-energizes Canada’s Atlantic offshore sector even if near-term well counts stay low [2]Government of Nova Scotia, “Nova Scotia Offshore Area Call for Bids 2026,” novascotia.ca. Deep-water campaigns inherently require larger cabins, auxiliary fuel, and emergency-flotation kits, creating a structural demand floor for the North America offshore helicopter services market.

Improved Viability of Offshore Oil & Gas Projects

Regional breakeven prices for deep-water Gulf of Mexico wells now sit at USD 35-45 per barrel Brent thanks to standardized subsea trees and faster drill-times, encouraging operators to commit to multi-year helicopter capacity blocks despite commodity swings. Gulf production climbed to 1.96 million barrels per day in 2026, above the pre-pandemic level and supporting predictable flight-hour purchasing. Equinor’s Bay du Nord development offshore Newfoundland, expected to sanction in 2027 with first oil in 2031, will need long-range flights of 270 nautical miles from St. John’s, justifying heavy twin-engine capacity retention. West White Rose’s 2026 startup and tie-back projects at Hebron and Hibernia safeguard baseline demand even as Canada targets net-zero by 2050. Stronger project economics therefore decrease the revenue volatility that once typified the North America offshore helicopter services market.

Expansion of U.S. Offshore-Wind Construction Zone

Six lease areas auctioned in the New York Bight will collectively deliver more than 7 gigawatts and require logistic support through at least 2030 helicopters remain the fastest evacuation and engineer-transfer option once sea states exceed 1.5 meters, the operational ceiling for most crew-transfer vessels (CTVs). BOEM’s Gulf of Maine and Central Atlantic auctions enlarged the pipeline beyond 50 gigawatts, distributing projects far enough apart that operators cannot rely on a single coastal base, increasing rotor-craft flying hours. HeliService USA, with five Leonardo AW169s, secured multi-year agreements to shuttle technicians, proving that a dedicated offshore-wind fleet can be profit-viable even when CTVs dominate routine movements. As construction accelerates, emergency medical evacuation and turbine blade exchange tasks sustain high-margin flights despite CTV competition. Consequently, offshore wind bolsters the diversification of the North America offshore helicopter services market without eroding its oil-and-gas core.

Fleet-Modernization Cycle

Sikorsky’s S-92A+ Phase IV gearbox, certified in 2024, introduces auxiliary lubrication that extends inspection intervals by 1,200 flight hours, directly improving aircraft availability for operators pressured by tight crew-change windows. PHI’s framework order for 12 Leonardo AW189s adds super-medium airframes with 50-minute run-dry ratings, allowing flights deeper into the Gulf at lower fuel consumption than legacy S-92s. Bristow’s order for 15 Airbus H135s underlines the dual-fleet strategy: keep heavy-lift capacity while deploying light twins for inspection and wind-farm duties. Delivery lead times of 18-24 months because of gearbox and avionics bottlenecks are encouraging service-life extensions for existing airframes, but the economic case for fuel savings keeps the modernization curve rising. As a result, super-medium helicopters are steadily displacing heavy twins within the North America offshore helicopter services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from crew-transfer vessels (CTV) | -0.8% | United States (East Coast offshore wind zones) | Medium term (2-4 years) |

| High operating & maintenance costs | -0.5% | North America (all operators) | Long term (≥ 4 years) |

| Oil-price volatility reducing drilling programs | -0.6% | United States (Gulf of Mexico), Canada, Mexico | Short term (≤ 2 years) |

| FAA Part-135 retrofit mandates (avionics/safety) | -0.4% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Crew-Transfer Vessels

Jones Act-compliant CTVs operated by WINDEA and Atlantic Wind Transfers price a round trip at USD 150-250 versus USD 800-1,200 for comparable helicopter seats, absorbing roughly 85% of personnel transfers at U.S. wind farms [3]Riviera Maritime Media, “U.S. Crew-Transfer Vessel Market Expands,” rivieramm.com. Motion-compensated gangways now allow safe transfers in 1.5-meter wave heights, conditions that represent most operational days along the New York Bight. Helicopters retain indispensable roles for emergency medical evacuation, senior-executive visits, and winter contingency transport, but those missions account for only 10-15% of offshore-wind labor hours. As wind capacity expands, CTV competition will cap the upside for rotary-wing revenues in that segment of the North America offshore helicopter services market.

High Operating & Maintenance Costs

A Leonardo AW169 flying a 200-nautical-mile sortie consumes nearly 180 liters of Jet A per hour at USD 1.70 per liter, while a CTV amortizes cheaper marine diesel across two dozen seats. Spare-parts inflation averaged 6% year-on-year in 2025-2026, driven by titanium and electronics supply shortages. Large operators combat costs through power-by-the-hour agreements with OEMs, but small fleets struggle, especially once FAA retrofit deadlines add USD 150,000-300,000 per airframe. This cost burden slows fleet renewal in the lower tiers of the North America offshore helicopter services industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Super-Mediums Challenge Heavy-Twin Dominance

Medium helicopters retained 51.7% of 2025 revenue, yet the North America offshore helicopter services market size for light twins is projected to grow at 6.6% CAGR through 2031 as AW169 and H135 aircraft migrate from offshore-wind crew transfer to high-frequency inspection flights. Heavy-lift capacity, still 28% of market revenue, is slowly shrinking as operators retire high-maintenance S-92 and H225 airframes. Super-medium newcomers such as the AW189 and soon-to-be-certified Bell 525 deliver a 20-30% fuel-burn advantage per passenger-mile, explaining why PHI, CHC, and Bristow are placing sizeable orders despite 18-month lead times [4]Leonardo S.p.A., “AW189 Technical Datasheet,” leonardo.com.

Super-medium fleet uptake promotes mission optimization. Operators no longer treat helicopters as one-size-fits-all assets; instead, they tailor capacity to workload, deploying heavy twins for deep-water crew rotations while assigning light twins to turbine-blade inspections and harbor-pilot shuttles. This nuanced fleet mix keeps utilization high and helps the North America offshore helicopter services market defend profitability even under flat topline growth scenarios.

By Application: Inspection Missions Embrace Automation

Crew transport held 42.1% share in 2025, but inspection, monitoring, and surveying flights are set to expand at 7.3% CAGR through 2031 as asset owners adopt AI-enabled remote-inspection regimes. Drones and autonomous underwater vehicles (AUVs) have reduced the headcount that must fly offshore, yet helicopters remain vital for sensor-package deployment and supervisor travel, sustaining baseline flying hours.

Digital-twin analytics allow operators to dispatch helicopters only when risk scores breach thresholds, rather than on fixed monthly timetables. Consequently, flight frequency decreases, but each mission often carries specialized payloads or personnel at premium rates. The North America offshore helicopter services market size attributable to inspection services therefore rises even as total sorties plateau.

By End-User Industry: Offshore Wind Reshapes Demand Mix

Oil and gas generated 67.5% of 2025 revenue, underpinning the largest share of the North America offshore helicopter services market. Offshore wind, expanding at a 9.5% CAGR, is the fastest-growing end-user and will account for a progressively larger revenue slice as 50-plus gigawatts of capacity move from lease to construction. Marine applications such as harbor-pilot transfers occupy 8% of revenue and are climbing as LNG exports surge from Gulf Coast terminals.

Diversification is accelerating but will not unseat oil and gas as the primary revenue generator this decade. High crew headcounts on drilling rigs and floating production units require daily rotations that no other offshore segment matches. Nonetheless, the growth of wind and marine logistics smooths the revenue curve and lowers the beta of the North America offshore helicopter services industry relative to Brent price swings.

Geography Analysis

The United States captured 79.9% of 2025 revenue, anchored by Gulf of Mexico production at 1.96 million barrels per day in 2026 and a 50-gigawatt offshore-wind pipeline. U.S. Coast Guard fleet expansion to 127 MH-60T Jayhawks injects secondary demand for Sikorsky parts and pilot training, indirectly strengthening the commercial supply chain. Niche growth arises from harbor-pilot shuttle programs such as Sabine Bank Pilots, where AW169 helicopters replaced pilot boats during heavy-weather windows.

Canada with four producing fields off Newfoundland and Labrador plus the upcoming West White Rose restart in 2026. Bay du Nord, if sanctioned in 2027, will require long-range heavy-lift support over 500 kilometers of North Atlantic waters, securing future demand even as exploratory drilling remains subdued.

Mexico is the fastest-growing geography at 6.9% CAGR through 2031, propelled by the Trion ultra-deepwater project targeting 100,000 barrels per day by 2028. Although Mexico’s regulatory environment for offshore wind is immature, cross-border service contracts enable U.S. operators to position aircraft in Veracruz or Tampico and extend fleet utilization during seasonal slowdowns north of the border.

Competitive Landscape

North America Offshore Helicopter Services Market is semi-consolidated. Bristow, PHI, and CHC hold major share of the market, leveraging scale in maintenance, spare-parts procurement, and multi-year contracts with Shell, Chevron, and Equinor. Bristow’s NOK 1.9 billion contract for Barents Sea operations underscores how global networks help incumbents secure high-value deals that backstop regional cash flow. CHC’s deployment of AI-based DigitAI predictive maintenance cut unscheduled events by 18%, elevating dispatch reliability and fortifying client retention.

White-space entrants focus on specialty niches. HeliService USA’s AW169 fleet services LNG pilot transfers and offshore-wind emergency response, an area too fragmented for the majors to prioritize. OEM-linked financing is another competitive lever: LCI’s merger with Macquarie into SMFL Helicopters consolidated 290 aircraft under a single lessor, offering flexible lease structures that accelerate uptake of fuel-efficient platforms such as the AW189.

Acquisition activity continues. Gulf Dredging’s purchase of NHV will swell its fleet to more than 60 helicopters once the deal closes in Q1 2026, though immediate North American effects remain limited. Avincis Group’s acquisition of KN Helicopters signals new entrants eyeing offshore-wind logistics, intensifying competitive pressure on incumbents over the medium term.

North America Offshore Helicopter Services Industry Leaders

Bristow Group Inc.

PHI Inc.

CHC Helicopter

Era Helicopters LLC

Cougar Helicopters Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: an offshore rescue conducted by the NYPD Aviation Unit underscored the essential role of helicopters in medical evacuation and safety missions. Safety regulations in offshore operations continue to drive demand for dedicated search and rescue (SAR) helicopter contracts.

- December 2025: Harbour Energy completed a USD 3.2 billion acquisition of LLOG Exploration, expanding its operations in U.S. offshore fields. The increase in production and deployment of new offshore units necessitates regular helicopter shuttle services.

- June 2025: TotalEnergies acquired a 25% stake in 40 offshore exploration blocks operated by Chevron in the Gulf of Mexico. This acquisition significantly heightened offshore exploration activities, directly increasing the demand for crew transport, logistics, and medevac helicopter services.

- March 2025: PHI Aviation commenced offshore crew transport flights for Shell plc in the Gulf of Mexico using the Airbus H160 helicopter. This marked the first global commercial offshore deployment of the H160, reflecting the modernization of offshore fleets with more efficient and safer aircraft.

North America Offshore Helicopter Services Market Report Scope

Offshore helicopter services provide a crucial connection between onshore bases and remote offshore facilities. They facilitate the safe and efficient transportation of personnel, equipment, and emergency support for industries such as oil and gas, as well as offshore wind. These services ensure operational continuity, enable rapid response in critical situations, and comply with stringent safety standards in demanding marine environments.

The North America offshore helicopter services market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into light, medium, and heavy helicopters. By application, the market is segmented into crew transport, cargo transport, inspection, monitoring and surveying, relocation and decommissioning support, and other applications. By end-user industry, the market is segmented into oil and gas, offshore wind, marine and shipping, and government and defence. By geography, the market is segmented into the United States, Canada, and Mexico. The report also covers the market sizes and forecasts for the offshore helicopter services market across these key countries in North America. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Light Helicopters |

| Medium Helicopters |

| Heavy Helicopters |

| Crew Transport |

| Cargo Transport |

| Inspection, Monitoring, and Surveying |

| Relocation and Decommissioning Support |

| Other Applications |

| Oil and Gas |

| Offshore Wind |

| Marine and Shipping |

| Government and Defence |

| United States |

| Canada |

| Mexico |

| By Type | Light Helicopters |

| Medium Helicopters | |

| Heavy Helicopters | |

| By Application | Crew Transport |

| Cargo Transport | |

| Inspection, Monitoring, and Surveying | |

| Relocation and Decommissioning Support | |

| Other Applications | |

| By End-user Industry | Oil and Gas |

| Offshore Wind | |

| Marine and Shipping | |

| Government and Defence | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will the North America offshore helicopter services market be by 2031?

It is projected to reach USD 1.50 billion by 2031, rising from USD 1.22 billion in 2026 at a 4.16% CAGR.

Which helicopter segment is growing fastest?

Light twins such as Airbus H135 and Leonardo AW169 lead growth at a 6.6% CAGR through 2031.

Why are super-medium helicopters displacing heavy twins?

AW189 and Bell 525 models cut fuel burn by up to 30% per passenger-mile while preserving deep-water range, lowering operating costs.

How does offshore wind affect helicopter demand?

Wind projects require fewer routine crew transfers than oil platforms, but emergency response and long-range technician flights still generate a 9.5% CAGR for helicopter services in that segment.

What impact will FAA retrofit rules have on operators?

Mandatory installation of flight-data recorders and terrain-awareness systems by May 2027 will cost USD 150,000-300,000 per airframe and may force smaller fleets to exit or merge.

Page last updated on: