Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

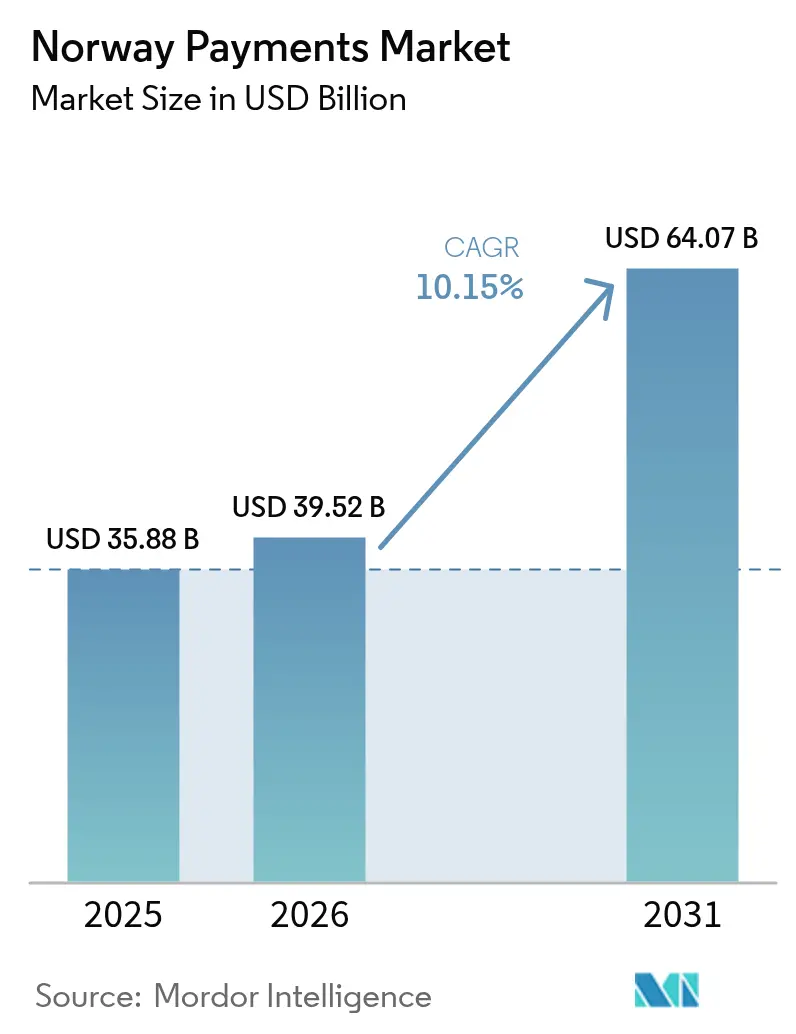

| Base Year Market Size (2025) | USD 35.88 Billion |

| Market Size (2026) | USD 39.52 Billion |

| Market Size (2031) | USD 64.07 Billion |

| Growth Rate (2026 - 2031) | 10.15% CAGR |

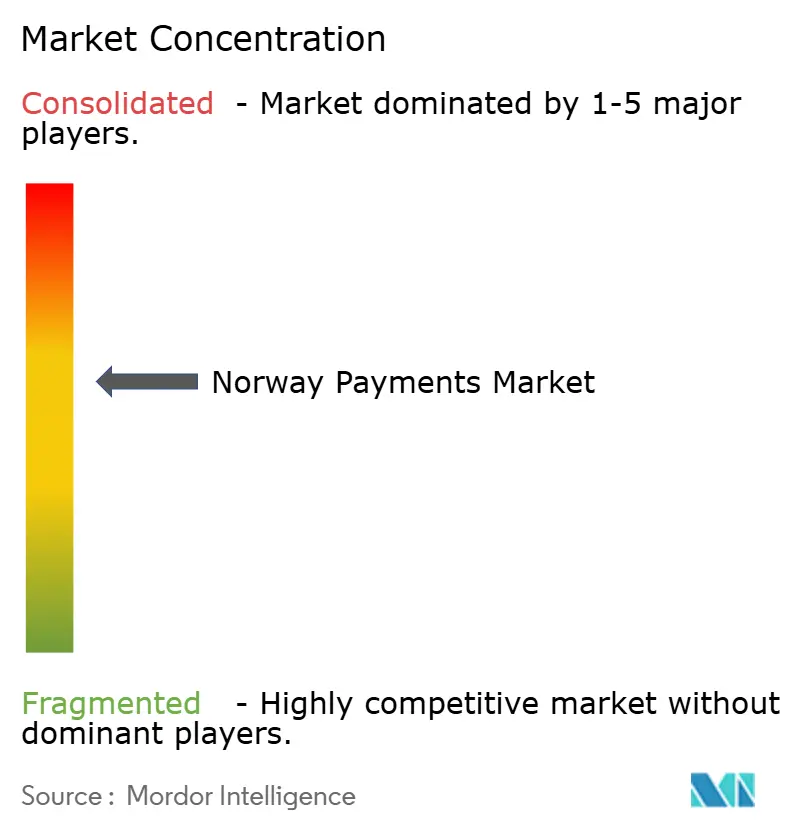

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Payments Market Analysis by Mordor Intelligence

The Norway payments market size is expected to grow from USD 35.88 billion in 2025 to USD 39.52 billion in 2026 and is forecast to reach USD 64.07 billion by 2031 at 10.15% CAGR over 2026-2031. Digital wallet penetration, mandatory contact-less terminals and advanced open-banking rules have positioned the country as Europe’s most cash-averse society, with cash now used for only 3% of consumer transactions.[1]Norges Bank, “Web Report Financial Infrastructure 2025,” norges-bank.no Payments innovation is further propelled by the National Digitalisation Strategy 2024-2030, which directs EUR 90 million (USD 97 million) in annual funding to modernise real-time rails.[2]Norwegian Ministry of Digitalisation, “The Digital Norway of the Future: National Digitalisation Strategy 2024–2030,” regjeringen.no Rapid uptake of NFC services, widespread 5G coverage and a surge in fintech investments are expanding addressable volumes in the Norway payments market, while tighter cyber-fraud mandates and new cash-acceptance rules temper near-term margins. Consolidation around Vipps MobilePay and BankAxept underscores the duopolistic character of the Norway payments market, although interoperability requirements through 2027 preserve access for third-party acquirers.

Key Report Takeaways

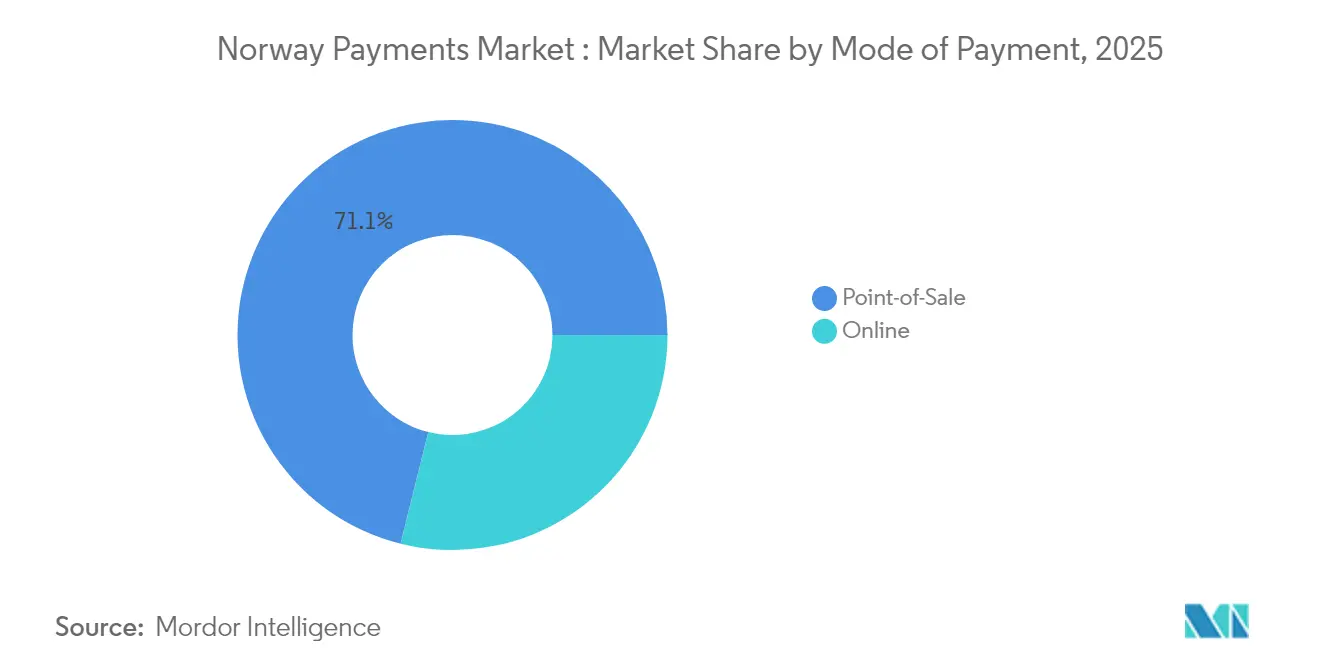

- By mode of payment, point-of-sale led with 71.12% of Norway payments market share in 2025; digital wallets are projected to grow at 13.45% CAGR to 2031.

- By interaction channel, point-of-sale retained 71.02% revenue share in 2025, while e-commerce and m-commerce channels advance at 12.05% CAGR through 2031.

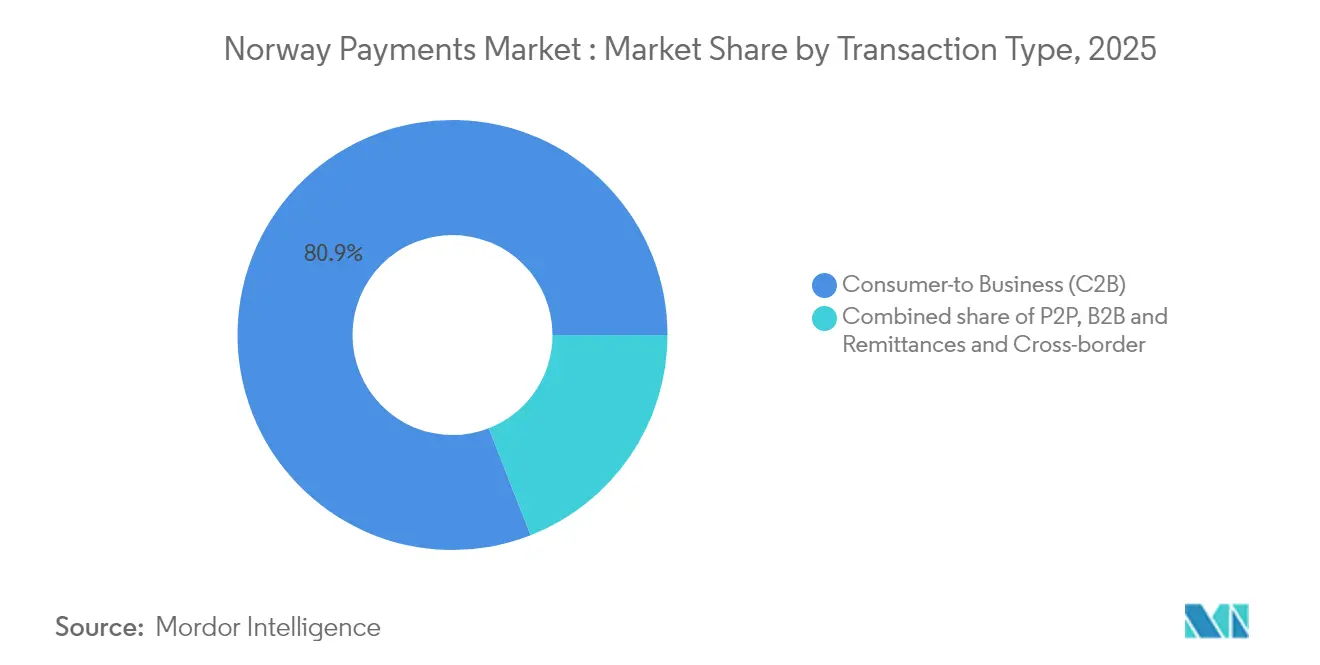

- By transaction type, consumer-to-business flows held 80.92% of the Norway payments market size in 2025; person-to-person payments expand fastest, at 10.85% CAGR to 2031.

- By end-user industry, retail accounted for 45.62% share of the Norway payments market size in 2025, whereas healthcare is set to grow at 13.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Norway Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push toward cashless & real-time payments | +2.8% | National, with early adoption in Oslo, Bergen, Trondheim | Short term (≤ 2 years) |

| Widespread smartphone & internet penetration | +2.1% | National, with rural areas catching up through 5G rollout | Medium term (2-4 years) |

| Mandated rollout of NFC/contactless terminals | +1.9% | National, with retail and hospitality sectors leading | Short term (≤ 2 years) |

| Open-banking regulation spurring fintech apps | +1.7% | National, with spillover effects to Nordic region | Medium term (2-4 years) |

| Consolidation of domestic wallets (Vipps merger effects) | +1.4% | Nordic region, with strongest impact in Norway, Denmark, Finland | Long term (≥ 4 years) |

| Gig-economy demand for instant salary payouts | +1.2% | Urban centers, expanding to suburban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Push Toward Cashless & Real-Time Payments

Annual public funding of EUR 90 million (USD 97 million) accelerates real-time rails, while Norway’s forthcoming entry into TARGET Instant Payment Settlement in 2028 will permit krone-euro instant clearing and reduce cross-border friction.[3]European Central Bank, “Norway Joins TIPS,” ecb.europa.eu Norges Bank is in parallel testing wholesale CBDC use cases, signalling readiness for post-cash settlement models. Mandatory access to cash up to NOK 20,000 mitigates resilience concerns, thereby sustaining consumer trust even as cash use plummets. Together these measures underpin the long-term expansion of the Norway payments market.

Widespread Smartphone & Internet Penetration

Universal broadband and 5G have unlocked biometric and offline payment features that widen digital acceptance in rural areas. Visa finds mobile-wallet usage at 94%, Europe’s highest.[4]Visa, “Decoding the European Mobile Wallet Evolution,” visa.co.uk Offline-first payment design, pioneered by Nordic operators, ensures continuity during outages and mitigates systemic risk, boosting the versatility of the Norway payments market.

Mandated Rollout of NFC/Contactless Terminals

EU Digital Markets Act forced Apple to unlock iPhone NFC, enabling Vipps MobilePay to launch “Tap with Vipps,” the world’s first native iOS alternative to Apple Pay. Hospitality chains such as King Foods and Frich’s cut queue times and labour costs by pairing contactless kiosks with unified POS stacks. Network effects from terminal upgrades speed wallet adoption and lift transaction velocity across the Norway payments market.

Open-Banking Regulation Spurring Fintech Apps

PSD2 opened account-to-account data but bank API pricing has triggered competition complaints from Neonomics. PSD3, effective 2026, will hard-wire dedicated fraud-mitigation APIs, creating fresh parity for third-party apps. As data portability improves, differentiated user journeys will attract new cohorts, bolstering volumes in the Norway payments market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cyber-fraud mitigation costs | -1.8% | National, with higher impact on smaller financial institutions | Short term (≤ 2 years) |

| High interchange & acquiring fees for SMEs | -1.2% | National, with disproportionate effects on rural and small businesses | Medium term (2-4 years) |

| Margin compression from intense PSP competition | -0.9% | National, with spillover effects to Nordic region | Medium term (2-4 years) |

| Data-privacy & localisation concerns | -0.7% | National, with EU regulatory compliance requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Fraud Mitigation Costs

DNB blocked NOK 2.1 billion (USD 190 million) of fraud in 2024, diverting capital toward defensive tooling that might otherwise fund product innovation. Finans Norge’s Cyber Threat Support Unit now coordinates shared intelligence, but Digital Operational Resilience Act compliance imposes fresh cost lines, denting smaller PSP margins and slowing new-service launches within the Norway payments market.

High Interchange & Acquiring Fees for SMEs

International scheme fees remain high for low-volume merchants, while mandatory cash-acceptance rules add parallel cost structures. These dual burdens deter SMEs from upgrading to premium payment functionality, keeping a portion of potential volumes out of the Norway payments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Disrupt Card Dominance

Point-of-sale held 71.12% Norway payments market share in 2025. Yet digital wallets and direct account transfers are rising at 13.45% CAGR, enabled by ISO 20022 migration that delivers richer data for consent-based analytics. The Norway payments market size attached to digital-first rails is forecast to eclipse USD 22.46 billion by 2031, reshaping acquirer economics.

Card issuers respond with value-added perks and tokenised credentials to defend spend levels, but “Tap with Vipps” on iOS cracks closed ecosystems and compresses issuer lock-in. Cash slides below 3% of volume as consumer trust migrates to biometrically-authenticated wallets. Integration of loyalty, BNPL and P2P in single super-apps deepens engagement and magnifies lifetime value within the Norway payments market.

By Interaction Channel: E-commerce Momentum Challenges Physical Dominance

The Norway payments market size transacted through e-commerce and m-commerce grows at 12.05% CAGR, chipping away at physical-only channels that keep 71.02% share today. Logistics-first retailers like Oda already service 70% of online grocery demand, demonstrating scalability of cold-chain automation in Norway’s dispersed geography.In-store merchants counter with omnichannel check-out, click-and-collect and self-checkout kiosks that tether inventory to cloud POS. The Norway payments market dovetails with civic digitisation, as tax, toll and health portals adopt the same rails consumers use for shopping. Mobile commerce further blurs lines, embedding purchase and payment links inside social feeds, live streams and gaming environments.

By Transaction Type: P2P Payments Accelerate Beyond C2B Foundation

Consumer-to-business flows deliver 80.92% of Norway payments market size, underpinned by high per-capita retail spend and universal card ownership. Person-to-person transfers, however, climb 10.85% yearly as cultural shifts orient money exchange around chat-like experiences. Instant salary schemes for gig workers accelerate demand, creating overlap between payroll, remittance and social-transfer use cases.

Business-to-business corridors move slower due to compliance workflows, but TARGET Instant Payment Settlement will shave cross-border latency, unlocking fresh liquidity benefits for SMEs by 2028. Regulatory commitments to non-discriminatory access keep P2P rails open, allowing new overlay services such as group gifting and escrow inside the Norway payments market.

By End-user Industry: Healthcare Innovation Outpaces Retail Maturity

Retail still contributes 45.62% Norway payments market share, reflecting mature POS coverage and omnichannel expansion. Yet healthcare leads growth at 13.2% CAGR, fuelled by USD 47 billion in national health spending, extensive telemedicine adoption and e-prescription roll-outs.

Hospitals now integrate payment APIs into patient portals for co-pays and teleconsult fees, while pharmacies pilot automatic recurring billing for chronic medications. Government utilities digitise billing, adding stable throughput. Entertainment, gaming and streaming subscriptions surge as well, embedding micro-transactions and fractional usage models that lift ARPU across the Norway payments market.Geography Analysis

Norway’s domestic arena remains the epicentre of the Norway payments market, boasting a 94% mobile-wallet adoption rate, the world’s highest. Oslo, Bergen and Trondheim spearhead pilot programmes for CBDC retail testing, while remote northern counties benefit from 5G-enabled offline settlement to assure network resilience. The Nordic region offers spill-over potential through the consolidated Vipps MobilePay user base, yet P27’s uncertain licence status pauses broader cross-border clearing ambitions.

EEA alignment forces Norway to adopt EU payment directives. The Digital Markets Act has already reshaped NFC competition dynamics; PSD3 will layer tougher AML and liability provisions, pushing banks to upgrade fraud orchestration engines ahead of continental peers. TARGET Instant Payment Settlement integration links Norwegian kroner with euro real-time rails by 2028, positioning exporters for faster receivables and drawing foreign PSPs into the Norway payments market.

Outside Europe, Norwegian PSPs explore selective expansion where digital infrastructure readiness mirrors domestic standards—namely Singapore, Australia and the Gulf. Nordic diaspora and shared SEPA SCT Inst adherence ease corridor testing. Currency volatility risk remains elevated due to the krone’s float, but advanced hedging tools embedded in corporate accounts moderate exposure for mid-tier exporters within the Norway payments market.

Competitive Landscape

Vipps MobilePay and BankAxept dominate domestic acceptance rails, while Visa and Mastercard control international scheme routing. Extended merger undertakings oblige Vipps to offer transparent pricing and open APIs, sustaining contestability through 2027. DNB leverages scale to run 392 million daily payment instructions, monetising data-rich ISO 20022 messages for treasury analytics.

Fintech challengers pursue niche penetration; Neonomics offers single-API account aggregation and wages regulatory warfare to dismantle gatekeeping. Sokin gains foothold through its Settle acquisition, targeting remittances and SME multicurrency accounts. International processors such as Worldline pair with incumbents on instant-payment front-ends, securing relevance as the Norway payments market shifts to real-time settlement.

Security posture now differentiates leaders: Thales supplies HCE tokenisation and biometric authentication, enabling Vipps’ iOS NFC breakthrough that reached 1 million users in five months. Shared cyber-intelligence via Finans Norge counters sophisticated attack vectors, though smaller acquirers struggle to fund zero-day response capabilities. Overall, the Norway payments market rewards scale, trust and innovation cadence.

Norway Payments Industry Leaders

Vipps AS

Bank Norwegian

Klarna Bank AB

PayPal Holdings Inc.

Nets A/S (Nexi Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Thales and Vipps launched NFC payments on iOS, reaching 1 million users and establishing the first viable alternative to Apple Pay on iPhone devices through advanced encryption technology and seamless BankAxept integration.

- February 2025: Worldline and DNB partnered to add Swift Instant Connectivity to TARGET Instant Payment Settlement, enhancing real-time B2B and treasury flows.

- December 2024: Vipps MobilePay launched “Tap with Vipps” as the world’s first Apple Pay alternative on iPhone.

- December 2024: Sokin completed acquisition of fintech Settle, strengthening multi-currency wallet capabilities in Norway.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers the Norwegian payments market as all domestic payment transactions, card present and card not present, across point of sale, e-commerce, and account to account rails, recorded in value terms (USD) at the moment of settlement. In practice, this covers consumer to business, peer to peer, business to business, and cross-border flows that clear through licensed banks or authorized payment institutions.

Scope exclusion: we purposely omit crypto asset transfers and interbank wholesale settlement balances as they follow very different risk and regulatory profiles.

Segmentation Overview

- By Mode of Payment

- Point-of-Sale

- Card (Debit, Credit, Pre-paid)

- Digital Wallets (Apple Pay, Google Pay, Interac Flash)

- Cash

- Other POS (Gift-cards, QR, Wearables)

- Online

- Card (Card-Not-Present)

- Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal)

- Other Online (COD, BNPL, Bank Transfer)

- Point-of-Sale

- By Interaction Channel

- Point-of-Sale

- E-commerce/M-commerce

- By Transaction Type

- Person-to-Person (P2P)

- Consumer-to-Business (C2B)

- Business-to-Business (B2B)

- Remittances and Cross-border

- By End-user Industry

- Retail

- Entertainment and Digital Content

- Healthcare

- Hospitality and Travel

- Government and Utilities

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed issuing banks, payment gateway product heads, and merchant side finance managers across Oslo, Bergen, and Trondheim. Conversations verified interchange pass-through rates, take-rate trends on Vipps MobilePay, and typical buy now pay later ticket sizes, allowing us to reconcile desk estimates with on-ground realities.

Desk Research

We began by extracting headline transaction volumes, interchange caps, and terminal penetration from Statistics Norway, Norges Bank, and the European Central Bank's Payment Statistics. Macroeconomic inputs, GDP, household disposable income, retail sales, and tourism receipts, were mapped from World Bank and Eurostat series. Regulatory touchpoints such as PSD2 implementation notes and the Financial Contracts Act were reviewed on the European Payments Council and Norwegian Ministry of Finance portals. Financial disclosures from leading acquirers, network scheme data, and news archived in Dow Jones Factiva enriched our understanding of pricing shifts and merger activity. D&B Hoovers provided directional company revenues that helped approximate share for key processors. This list is illustrative; dozens of additional open and subscription sources were consulted during validation.

Market-Sizing & Forecasting

A top down reconstruction starts with Norges Bank annual transaction values, split by instrument, which are then adjusted for cash displacement, cross-border leakage, and forecast GDP. Selective bottom up checks, sampled acquiring volume multiplied by average merchant service fee, e-commerce basket size multiplied by digital wallet penetration, and card scheme reported net revenue anchor key segments before figures are rolled into the master model. Critical drivers in our forecast include contactless card share, smartphone penetration, real-time payment adoption, EV charging POS mandates, and tourism comeback pacing. Multivariate regression with lagged GDP and retail sales variables underpins the base scenario; scenario analysis tests higher cyber fraud loss or slower BNPL uptake. Gaps in bottom up inputs, for example, private interchange rebates, are bridged using peer ranges obtained during expert calls.

Data Validation & Update Cycle

Outputs pass a three layer review, analyst, senior domain lead, and automated variance scan against macro indicators. Any deviation greater than 5% versus external transaction series triggers a re-check call with sources. Reports refresh once a year, with interim patches when material events, regulatory or macro, emerge.

Why Mordor's Norway Payments Baseline Commands Reliability

Estimates from different publishers seldom align because each chooses its own service scope, exchange rate base, and update cadence.

Key gap drivers include whether cash and domestic giro transfers are counted, the treatment of one-off government disbursements, and how aggressively online wallet average selling prices are inflated when projecting five years out. Mordor's model states assumptions transparently and is refreshed every twelve months, whereas others often lock forecasts for up to three years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 35.88 bn (2025) | Mordor Intelligence | - |

| USD 8.10 bn (2024) | Regional Consultancy A | Counts only card payments at physical POS, excludes online and A2A flows |

| USD 33.89 mn (2025) | Industry Newsletter B | Focuses solely on cross-border remittances, ignores domestic transactions and excludes corporate payments |

The comparison shows that wider scope choices and a disciplined refresh cycle enable Mordor Intelligence to deliver a balanced, transparent baseline that planners can replicate and stress test with confidence.

Key Questions Answered in the Report

How large is the Norway payments market today and what is its growth outlook?

The market stands at USD 39.52 billion in 2026 and is forecast to expand to USD 64.07 billion by 2031, reflecting a 10.15% CAGR.

What portion of everyday transactions in Norway are still made with cash?

Cash now represents just 3% of all payment volumes, confirming Norway’s position as Europe’s most cash-averse economy.

Which payment channel is growing fastest in Norway?

Digital wallets and account-to-account transfers are expanding at a 13.45% CAGR through 2031, eroding the historical dominance of point-of-sale cards.

What government policies are driving rapid payment digitalisation?

The National Digitalisation Strategy 2024-2030 directs EUR 90 million (USD 97 million) in annual funding toward real-time rails and mandates instant settlement for public-sector payments.

How did Norway become the first country with an Apple Pay alternative on iPhone?

The EU Digital Markets Act forced Apple to open iPhone NFC technology, enabling Vipps MobilePay to launch “Tap with Vipps” in December 2024.

Who controls the core payment infrastructure in Norway?

Domestic providers Vipps MobilePay and BankAxept manage essential rails, while Visa and Mastercard dominate cross-border scheme routing; open-access conditions remain in force until 2027.

Page last updated on: