North America Sugar Free Energy Drinks Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

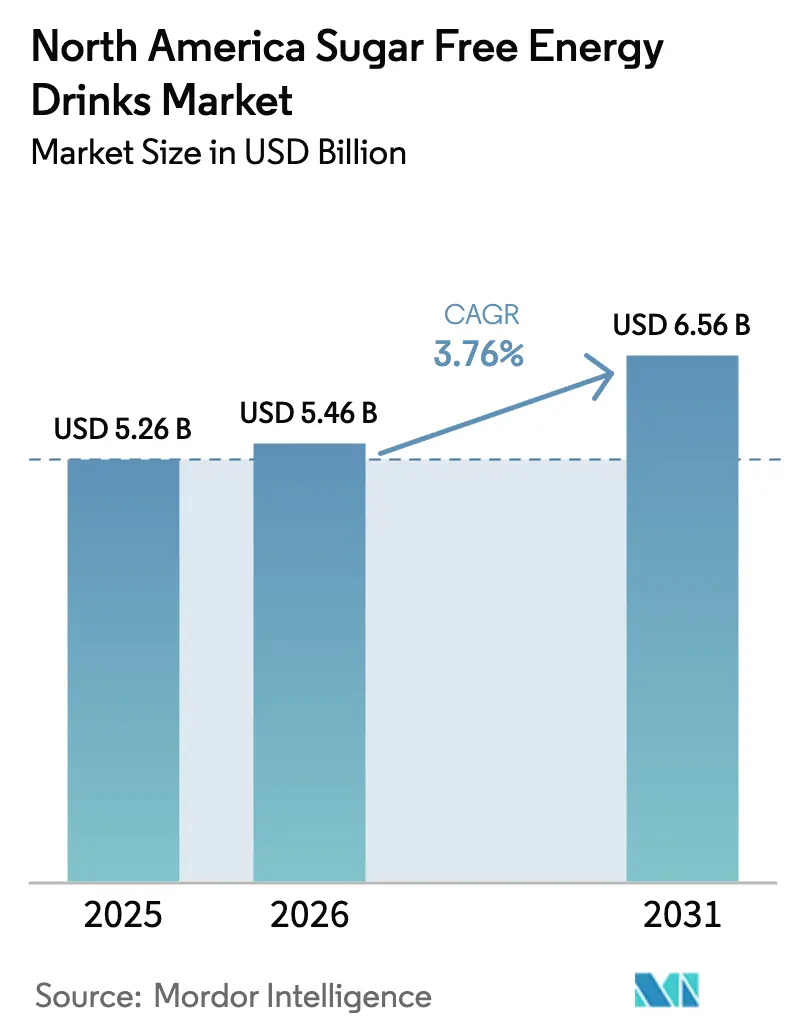

| Base Year Market Size (2025) | USD 5.26 Billion |

| Market Size (2026) | USD 5.46 Billion |

| Market Size (2031) | USD 6.56 Billion |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

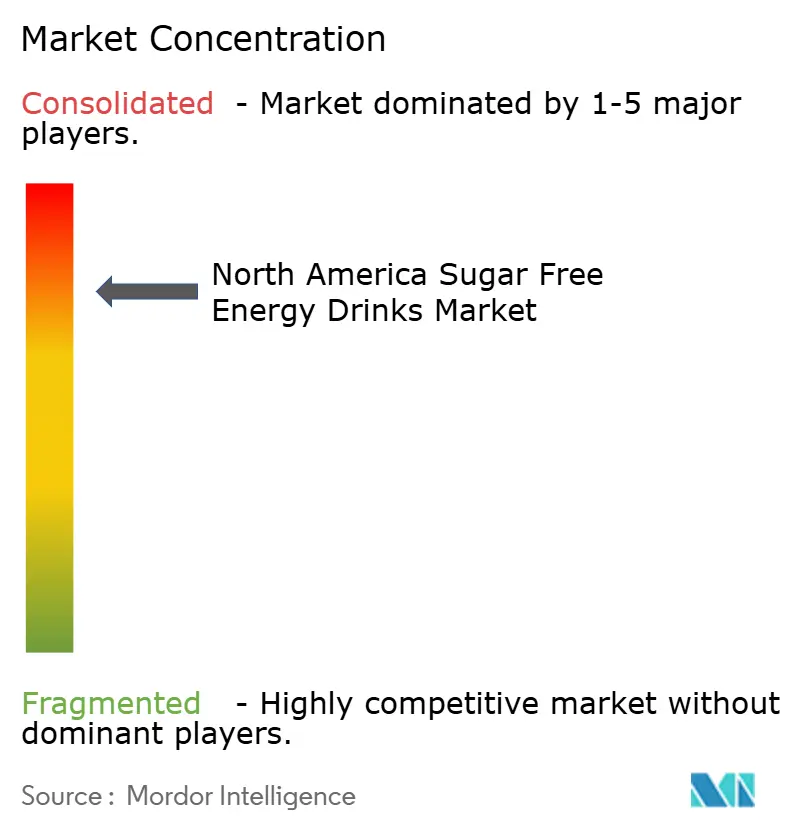

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Sugar Free Energy Drinks Market Analysis by Mordor Intelligence

The North America sugar free energy drinks market size is expected to grow from USD 5.26 billion in 2025 to USD 5.46 billion in 2026 and is forecast to reach USD 6.56 billion by 2031 at 3.76% CAGR over 2026-2031. This growth trajectory indicates a market that, while past its breakout phase, continues to thrive through strategies like premiumization, sugar-free reformulations, and targeted functional extensions. The market's evolution showcases a balancing act: the segment's traditional emphasis on immediate energy boosts now contends with rising wellness expectations. In response, mainstream brands are curating diverse portfolios that blend energy efficacy with cleaner labels. Meanwhile, emerging brands are carving out niches, focusing on performance nutrition, esports, and socially-driven launches. However, challenges loom, rising costs, particularly for aluminium, and stricter caffeine regulations complicate operations. Yet, these challenges favor firms with scale advantages, nimble sourcing, and robust in-house formulation capabilities. While convenience retail remains a cornerstone for the North American energy drinks market, the most rapid sales growth is seen in direct-to-consumer subscriptions, resonating with the habits of a digital-savvy audience.

Key Report Takeaways

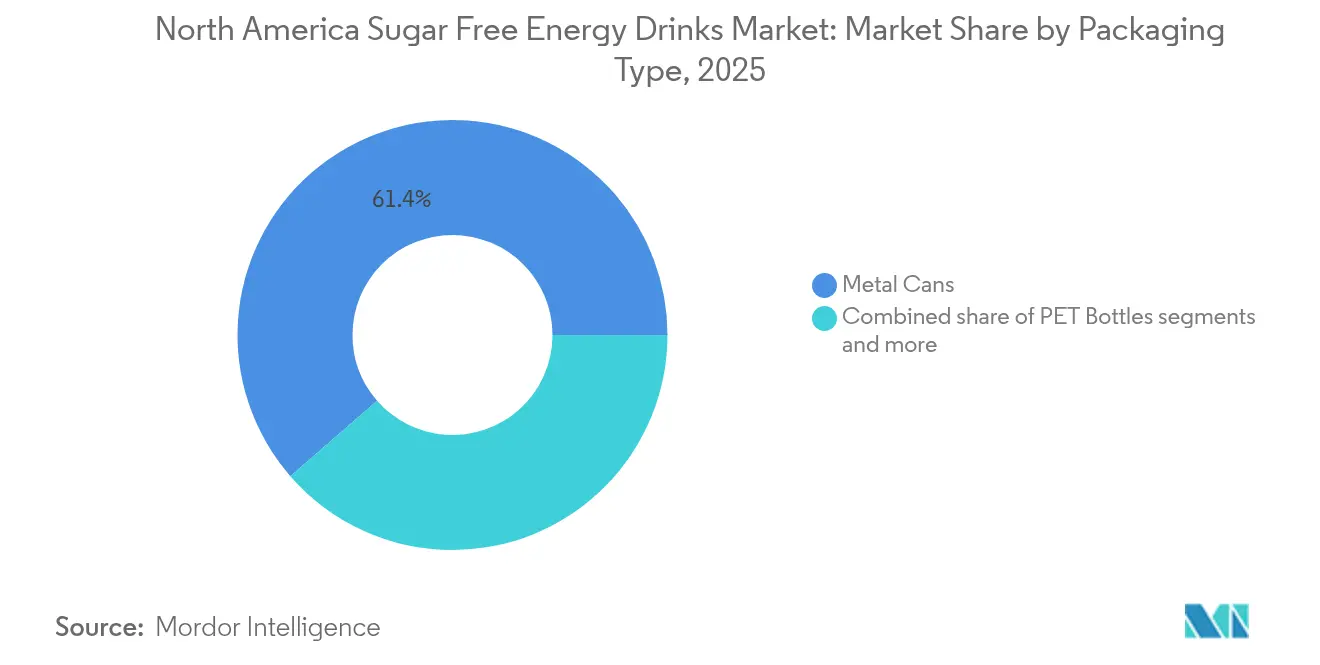

- By packaging type, metal cans led with 61.40% of the North America sugar free energy drinks market share in 2025; glass bottles are forecast to expand at a 4.02% CAGR through 2031.

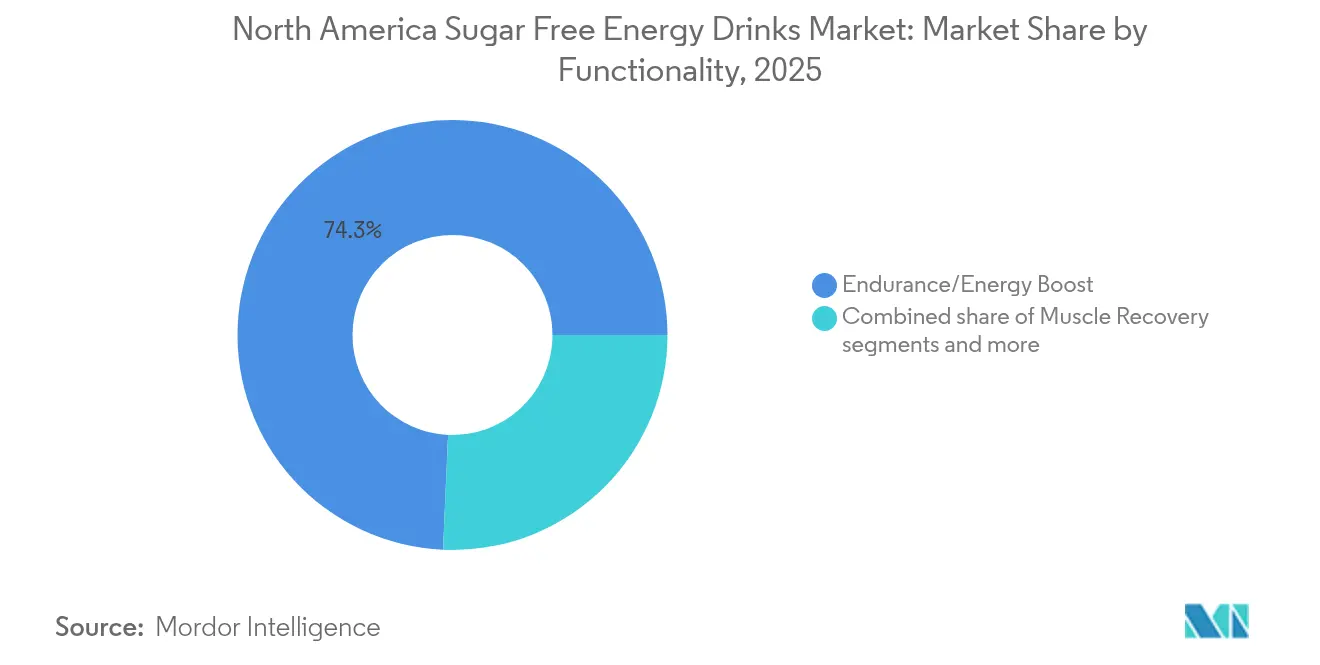

- By functionality, endurance and energy boost accounted for 74.30% share of the North America sugar free energy drinks market size in 2025, while muscle recovery records the highest projected CAGR at 3.95% to 2031.

- By distribution channel, supermarkets and hypermarkets held 93.40% revenue share in 2025, whereas online retail is projected to grow at a 4.32% CAGR through 2031.

- By geography, the United States commanded a 89.30% share of the North America sugar free energy drinks market size in 2025, yet Canada is set to post the fastest regional CAGR at 5.72% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Sugar Free Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Health-driven sugar reduction trend | +0.8% | North America-wide, strongest in United States urban markets | Medium term (2-4 years) |

| Natural and non-nutritive sweetener innovations | +0.6% | United States and Canada | Long term (≥ 4 years) |

| C-store dominance in energy-drink sales | +0.5% | United States convenience channel, expanding to Canada | Short term (≤ 2 years) |

| E-commerce and DTC subscription surge | +0.4% | North America digital-native demographics | Medium term (2-4 years) |

| GLP-1 medication uptake shaping demand | +0.3% | United States primarily, emerging Canadian adoption | Long term (≥ 4 years) |

| Growing college-athletics sponsorship spend | +0.2% | United States collegiate markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health-driven sugar reduction trend

As consumer wellness takes center stage, the industry witnesses a fundamental shift, with sugar-free products gaining both shelf space and consumer favor. According to the Centers for Disease Control and Prevention, around 38 million Americans were grappling with diabetes in 2024 [1]Source: Centers for Disease Control and Prevention, "A Report Card: Diabetes in the United States Infographic", cdc.gov. In the United States, a notable portion of the populace is turning to GLP-1 medications, leading to reduced calorie intake. This shift poses challenges for sugar-laden beverages, simultaneously boosting the appeal of zero-calorie options. Notably, the trend isn't confined to just those on the medication; it's reshaping dietary habits, signaling a broader societal embrace of weight management. Recognizing this shift, Monster Beverage is steering its focus towards sugar-free options, while Red Bull broadens its Zero Sugar lineup. This underscores a collective industry acknowledgment: the traditional high-sugar energy drink model is on a downward trajectory. Brands adept at balancing taste, texture, and functionality in their sugar-reduction efforts stand to gain, while those clinging to older formulations may find themselves at a disadvantage.

Natural and non-nutritive sweetener innovations

Manufacturers leverage advanced sweetener technologies to cater to consumer demands for clean labels, all while ensuring sensory acceptance and functional performance. For instance, sugar cane extracts like Modulex™ can reduce sugar content by 20-30%. They achieve this reduction while enhancing the drink's body and masking any metallic off-notes. This is done through sophisticated sensory mechanisms, such as modulating T1R2/T1R3 receptors and activating calcium-sensing receptors. Steviol glycosides, especially the high-purity Rebaudioside M and D variants, boast taste profiles that surpass earlier stevia generations. This advancement allows formulators to replicate sugar-like sweetness without the typical bitter aftertaste. The innovation landscape also includes positive allosteric modulators. These enhancers boost sweet receptor activity without overshadowing desired flavors, marking a significant technological advancement over mere sweetener substitution. Such innovations tackle the core challenge of ensuring energy drink palatability, all while aligning with regulatory and consumer pushes for reduced sugar content.

C-store dominance in energy-drink sales

Convenience stores have become the focal point in the battle for energy drink market share. As of 2025, the NACS/NIQ TDLinx report indicates that the United States is home to 152,255 convenience stores, up from 150,174 in 2023 [2]Source: National Association of Convenience Stores, "U.S. Convenience Store Count", convenience.org. Brands that master convenience retail strategies like tailored package sizing, effective promotions, and eye-catching point-of-sale displays stand to gain significantly. Beyond mere distribution, convenience stores play a pivotal role in shaping demand. The allure of impulse buys and the need for immediate consumption are propelling category growth. Recognizing the potential, retailers now see energy drinks not just as a means to draw in customers, but also as significant contributors to their profit margins. This has led to a more nuanced approach in managing the category, favoring brands that consistently demonstrate strong sales velocity and consumer loyalty.

E-commerce and DTC subscription surge

Energy drink purchasing patterns are undergoing a transformation, driven by the rise of digital commerce. Online retail is witnessing a robust growth, fueled by the increasing adoption of subscription models and direct-to-consumer strategies. As per the Census Bureau under the Department of Commerce, United States retail e-commerce sales reached an estimated USD 1,865.4 billion in Q2 2025, marking a 0.4 percent (±0.4%) uptick from Q1 2025 [3]Source: Census Bureau of the Department of Commerce, "Quarterly Retail E-Commerce Sales", census.gov. This shift in channel dynamics allows brands to not only capture higher profit margins but also cultivate direct relationships with consumers. Moreover, brands can now offer customization options that were previously unavailable in traditional retail settings. Subscription models have found particular favor among regular consumers, who value the convenience and predictability in pricing. Meanwhile, e-commerce platforms are becoming the go-to for specialty formulations and limited-edition variants, enhancing brand engagement. Furthermore, digital channels are proving invaluable for data collection and gleaning consumer insights. These insights play a pivotal role in shaping product development and marketing strategies, granting brands a competitive edge, especially when they adeptly merge online and offline interactions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Caffeine-safety regulatory scrutiny | -0.4% | North America-wide, intensifying in Canada | Short term (≤ 2 years) |

| Aluminum price volatility inflating packaging cost | -0.3% | North America manufacturing and import channels | Medium term (2-4 years) |

| After-taste issues of natural sweeteners | -0.2% | North America, more pronounced in health-conscious markets | Short term (≤ 2 years) |

| Limited can-line capacity for slim formats | -0.3% | North America manufacturing hubs and co-packing facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Caffeine-safety regulatory scrutiny

Regulatory authorities are tightening their grip on caffeine content and marketing practices, leading to increased compliance costs and potential restrictions on market access. Starting January 2026, Health Canada will enforce new labeling requirements for supplemented foods. These mandates include cautionary statements and detailed nutritional info for products with over 180mg of caffeine per serving. Meanwhile, Mexico is pushing forward with legislation that bans the sale of energy drinks to consumers under 18. The FDA's shifting approach to energy drink regulations, especially concerning marketing to young adults and the disclosure of caffeine content, introduces uncertainty for manufacturers eyeing product launches and marketing strategies. These regulatory shifts exacerbate existing challenges related to age-appropriate marketing and product positioning. As a result, brands are compelled to bolster their compliance infrastructure, which may restrict their access to certain market segments. Notably, these regulatory changes weigh heavily on smaller brands, which often lack the resources to navigate the complexities of legal and regulatory affairs.

Aluminum price volatility inflating packaging cost

Energy drink manufacturers face margin pressures and supply chain uncertainties due to fluctuating aluminum prices, especially since metal cans constitute a significant portion of their packaging. For canned beverages, packaging costs account for 15-25% of the total product cost. This makes aluminum price volatility a crucial factor influencing profitability, pricing strategies, and promotional activities. Major can suppliers, like Ball Corporation, employ pricing mechanisms that transfer these commodity cost fluctuations directly to beverage manufacturers. This results in quarterly margin variabilities, complicating financial planning and guidance for investors. Smaller brands, lacking the purchasing power to negotiate favorable supply agreements or hedge against commodity exposure, feel this constraint acutely. In contrast, large-scale manufacturers, equipped with sophisticated procurement capabilities, enjoy a competitive edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Sustainability Drives Innovation

Glass bottles are projected to grow at a 4.02% CAGR through 2031, outpacing the overall market. This growth comes even as metal cans command a dominant 61.40% market share in 2025. Factors such as premium positioning and heightened environmental awareness are reshaping packaging preferences. Consumers associate the glass segment with product purity and recyclability. This perception allows brands to adopt premium positioning strategies, commanding higher price points. Meanwhile, metal cans retain their market leadership due to superior barrier properties, cost efficiency, and a well-established supply chain. However, manufacturers are increasingly spotlighting sustainability credentials to address growing environmental concerns. PET bottles cater to specific niches, including larger formats and cost-sensitive segments. In contrast, aseptic packages are witnessing growth in shelf-stable and extended shelf-life applications.

Ball Corporation spearheads aluminum can sustainability with next-gen closures and packaging solutions. These innovations reduce material usage without compromising structural integrity. While disposable cups constitute the smallest segment, they play a pivotal role in foodservice and event marketing. Here, brand visibility and the need for immediate consumption are paramount. The evolving packaging landscape mirrors broader consumer trends: a tilt towards sustainability, a quest for convenience, and an appetite for premium experiences. Successful brands are fine-tuning their format portfolios, catering to varied consumption occasions and price points, all while navigating the complexities of supply chains and cost structures.

By Functionality: Performance Specialization Accelerates

Muscle recovery functionality is emerging as the fastest-growing segment, boasting a 3.95% CAGR, and is challenging the traditional endurance and energy boost category, which commands a dominant 74.30% market share in 2025. This surge underscores the category's shift towards specialized performance nutrition. Consumers, particularly those focused on fitness, are gravitating towards protein-enhanced formulations and post-workout recovery options, seeking benefits that extend beyond mere caffeine stimulation. The muscle recovery segment is uniquely positioned, drawing appeal from both energy drinks and sports nutrition. This crossover not only allows brands to command higher price points but also fosters consumer loyalty through precise efficacy claims.

Endurance and energy boost functionalities continue to anchor the market. Their foundation is bolstered by demands for workplace productivity and lifestyle energy needs, which often extend beyond athletic pursuits. Meanwhile, the "Other" functionality category is making waves, encompassing innovations like cognitive enhancement, immune support, and mood regulation. These areas signal potential growth as consumers broaden their wellness priorities beyond conventional energy needs. Brands that once adopted a one-size-fits-all approach are now pivoting. They're crafting functionality-specific formulations, allowing for targeted marketing, premium pricing, and the cultivation of both category expertise and consumer trust.

By Distribution Channel: Digital Transformation Reshapes Access

Online retail is outpacing the broader market with a robust 4.32% CAGR growth rate. This surge is fueled by the rise of subscription models, direct-to-consumer approaches, and the expansion of e-commerce platforms, all of which are reshaping traditional distribution methods. As a result of this digital shift, brands are not only securing higher profit margins but also forging direct relationships with consumers. They're now able to offer tailored options, such as flavor variety packs and personalized nutrition advice, which were previously absent in conventional retail. While supermarkets and hypermarkets command a dominant 93.40% share of distribution, thanks to their established supply chains and consumer habits, they're under increasing pressure to adopt digital tools and provide a seamless omnichannel experience.

Bars, restaurants, and entertainment venues play a pivotal role in brand-building and trial generation for the on-trade segment. Here, the allure of immediate consumption and the sway of social influence help shape category awareness and preferences. Meanwhile, off-trade channels like convenience stores, drug stores, and club retailers cater to varied consumer needs and buying behaviors. Successful brands are those that fine-tune their assortments, pricing, and promotional tactics to each channel. The evolving distribution landscape increasingly favors brands that can adeptly navigate multiple touchpoints while ensuring a consistent brand experience and pricing strategy.

Geography Analysis

In 2025, the United States commands a dominant 89.30% share of North America's energy drink market, buoyed by deep-rooted consumer acceptance, widespread retail distribution, and a competitive brand landscape fostering innovation. The United States market showcases a mature competitive intensity, where stalwarts like Monster Beverage and Red Bull grapple with challenges from swiftly rising disruptors such as Celsius and the portfolio of Congo Brands. This dynamic creates pivotal moments that distinguish market frontrunners from those in decline. Convenience stores play a pivotal role in the United States energy drink landscape, with retailers increasingly dedicating shelf space to the category. Brands are intensifying their focus on college athletics sponsorships which underscore the significance of young adults and sports marketing in shaping brand visibility and preference.

Canada stands out as the region with the most rapid growth, projected at a 5.72% CAGR through 2031. This surge is attributed to well-structured regulatory frameworks and a consumer base receptive to innovations in functional beverages. These conditions favor both established names and newcomers. Starting January 2026, Health Canada's updated labeling mandates for supplemented foods will require cautionary statements and comprehensive nutritional details for products exceeding 180mg of caffeine per serving. This move not only prioritizes consumer safety but also offers brands a clear regulatory landscape for long-term strategic planning. The Canadian market's inclination towards premium pricing and clean-label products allows brands to experiment with novel ingredients and marketing strategies before a wider North American launch. United States manufacturers are capitalizing on these Canadian opportunities, utilizing their established supply chain and marketing prowess for cross-border brand expansions.

While Mexico's energy drink consumption is on the rise, the market presents a dual-edged sword: ample opportunities shadowed by intricate regulatory challenges. Mexico's youthful demographic, urbanization trends, and a burgeoning middle class with disposable income fuel the energy drink expansion. However, the prevailing regulatory ambiguities pose hurdles for international brands eyeing entry or expansion. Meanwhile, the broader North American landscape, including Central American markets, holds promise for the future. As these regions witness economic growth and retail infrastructure advancements, conditions are ripe for energy drink development. Yet, the political and economic fluctuations necessitate a judicious approach, balancing the allure of growth with the imperative of safeguarding investments.

Competitive Landscape

In North America, the sugar free energy drinks market is becoming increasingly concentrated. Major players like Monster Beverage and Red Bull are now contending with nimble challenger brands. These challengers, such as Celsius and Alani Nu from Congo Brands, are carving out their niches by emphasizing wellness and harnessing digital marketing. This shift in the competitive landscape underscores a broader change in consumer preferences, moving towards functional benefits and clean-label formulations. Such changes not only challenge the traditional energy drink narrative but also open doors for brands adept at adapting to these market evolutions.

Major acquisitions, like Keurig Dr Pepper's takeover of Ghost Beverages, highlight a strategic consolidation trend. These moves signal that established players recognize the limitations of organic growth in tapping into new consumer segments and distribution avenues. Furthermore, brands are leveraging technology for a competitive edge, employing advanced sweetener systems, innovative packaging, and direct-to-consumer strategies. With consumer demand outpacing product availability, there's a golden opportunity for innovative brands to introduce tailored formulations and marketing tactics. Success in this competitive arena increasingly hinges on a brand's ability to navigate omnichannel strategies, adhere to regulations, engage consumers, and maintain operational efficiency, all while grappling with rising input costs and heightened promotional pressures.

Marketing alliances are broadening brand horizons. Take Nutrabolt's C4 Ultimate Energy, for instance. It recently clinched the title of WWE's inaugural official energy drink partner, seamlessly weaving its product into live events and digital narratives. In response, established players are ramping up their sponsorship budgets, zeroing in on extreme sports, gaming, and college athletics, all in a bid to stay culturally pertinent. Consequently, the focus has transitioned from mere distribution dominance to the realms of brand storytelling, community involvement, and the agility of limited-edition releases.

North America Sugar Free Energy Drinks Industry Leaders

-

PepsiCo, Inc.

-

Red Bull GmbH

-

The Coca-Cola Company

-

Monster Beverage Corporation

-

Celsius Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Liquid I.V. unveiled its Energy Multiplier Sugar-Free, targeting a new generation of consumers with heightened expectations from energy drinks. Prioritizing hydration, this innovative drink combines natural caffeine for balanced energy and clinically tested hydration-focused ingredients, all without sugar or artificial sweeteners.

- March 2025: Caribou Coffee rolled out its Sugar-Free Energy drinks, debuting two flavors: Sugar-Free Salted Watermelon and Sugar-Free Passionfruit Yuzu. Both drinks promise a refreshing, zero-sugar option with calorie counts under 30, depending on the serving size.

- November 2024: Red Bull introduced Red Bull Zero, a zero-sugar, zero-calorie counterpart to its classic Original energy drink, touting an identical taste. With Red Bull Zero, the brand seeks to bolster its growth trajectory, diversifying its portfolio with more options, including sugar-free variants. The product is available in single cans of 250ml, 335ml, and 474ml, alongside multipack offerings.

- September 2024: GURU launched its sugar-free energy drinks in the United States, asserting that the new product is free from artificial sweeteners, specifically sucralose and aspartame.

North America Sugar Free Energy Drinks Market Report Scope

Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Canada, Mexico, United States are covered as segments by Country.| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic Packages |

| Disposable Cups |

| Endurance/Energy Boost |

| Muscle Recovery |

| Other |

| Off-trade | Convenience Stores |

| Supermarkets/Hypermarkets | |

| Online Retail | |

| Others | |

| On-trade |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic Packages | ||

| Disposable Cups | ||

| By Functionality | Endurance/Energy Boost | |

| Muscle Recovery | ||

| Other | ||

| By Distribution Channel | Off-trade | Convenience Stores |

| Supermarkets/Hypermarkets | ||

| Online Retail | ||

| Others | ||

| On-trade | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms