Europe Sugar Free Energy Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

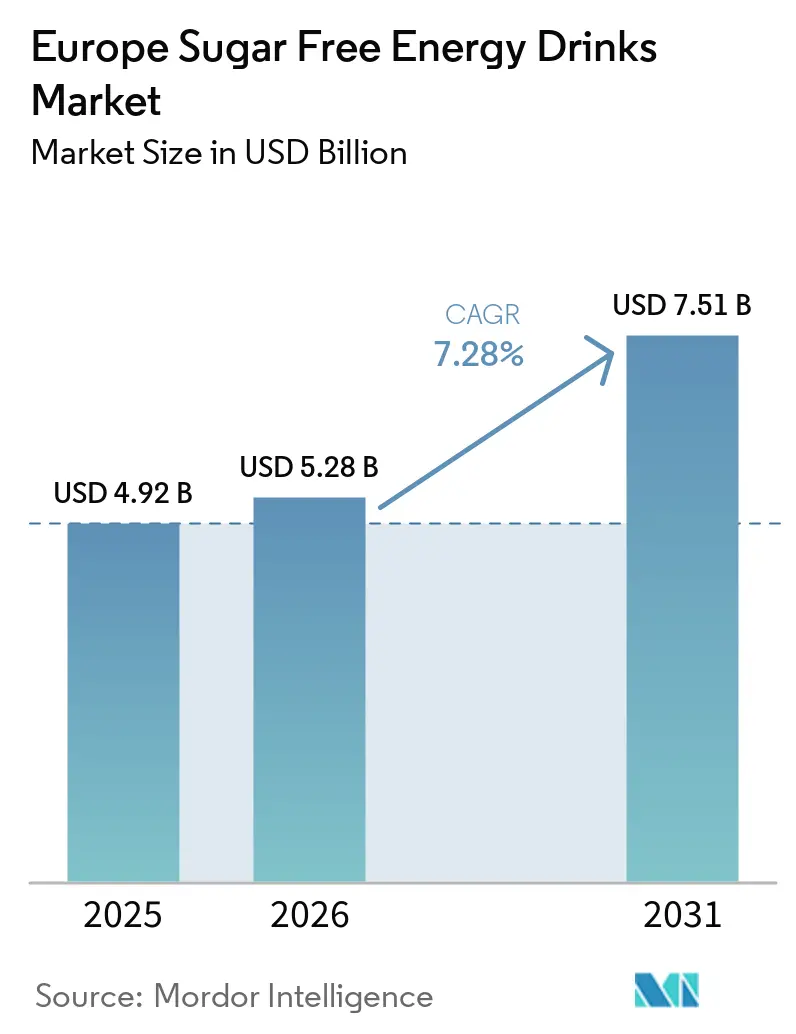

| Base Year Market Size (2025) | USD 4.92 Billion |

| Market Size (2026) | USD 5.28 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

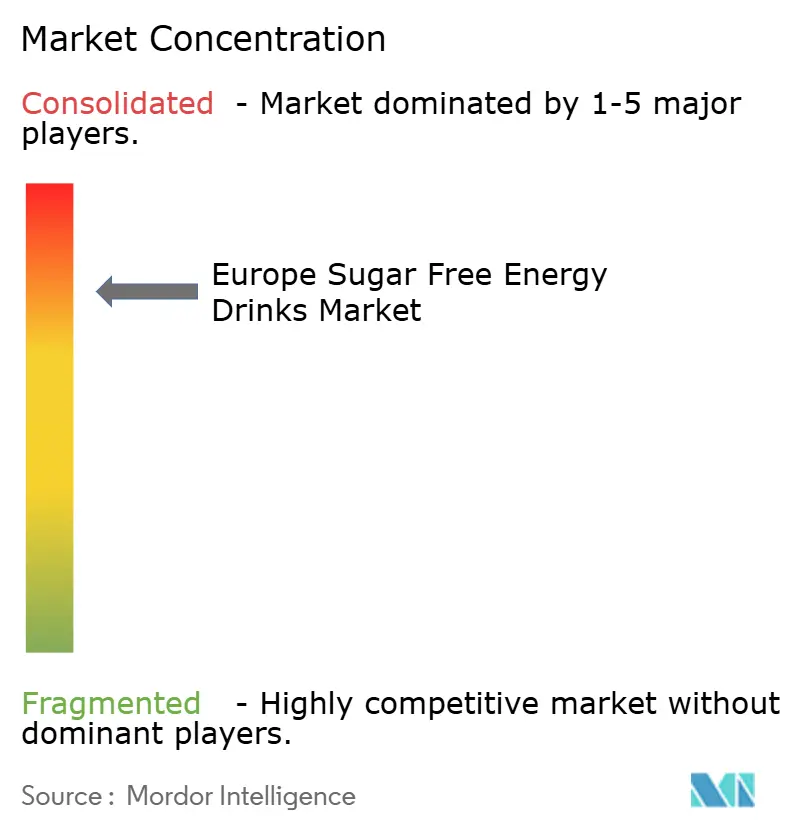

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sugar Free Energy Drinks Market Analysis by Mordor Intelligence

The Europe sugar-free energy drinks market size was valued at USD 4.92 billion in 2025 and estimated to grow from USD 5.28 billion in 2026 to reach USD 7.51 billion by 2031, at a CAGR of 7.28% during the forecast period (2026-2031). This growth is driven by a shift in consumer preferences and regulatory measures favoring lower-sugar formulations, stricter national sugar-levy policies, and the increasing availability of functional zero-calorie products. Metal cans continue to dominate the category due to their convenience and compatibility with chilled supply chains. However, premium glass bottles and slim formats are gaining traction, supported by deposit-return systems and branding strategies that position energy drinks as lifestyle products. Retail data indicates that low- and no-calorie variants are growing three times faster than the overall energy drinks segment, prompting established brands to reformulate flagship products to maintain shelf presence against competition from digitally native brands. The competitive landscape is intensifying as plant-based alternatives leverage direct-to-consumer channels and eSports sponsorships, challenging the market dominance of two leading multinational companies.

Key Report Takeaways

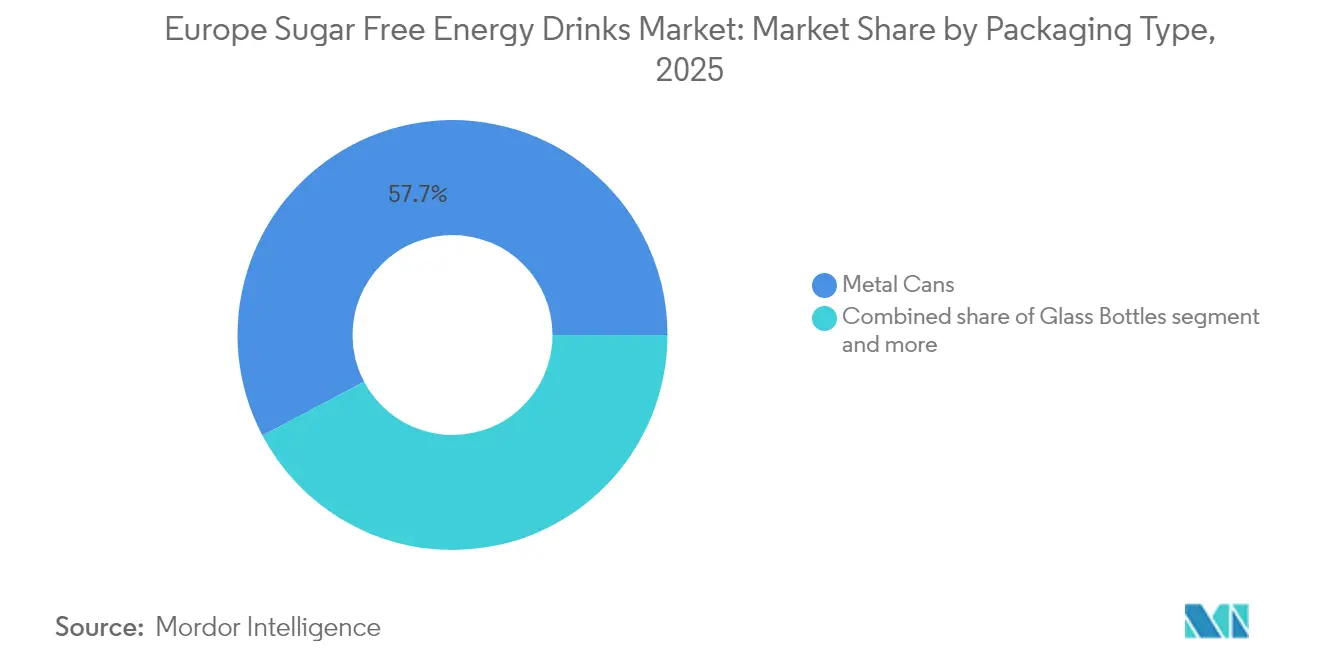

- By packaging type, metal cans accounted for 57.74% of Europe sugar free energy drinks market share in 2025, and glass bottles are forecast to grow at an 8.12% CAGR from 2026 to 2031.

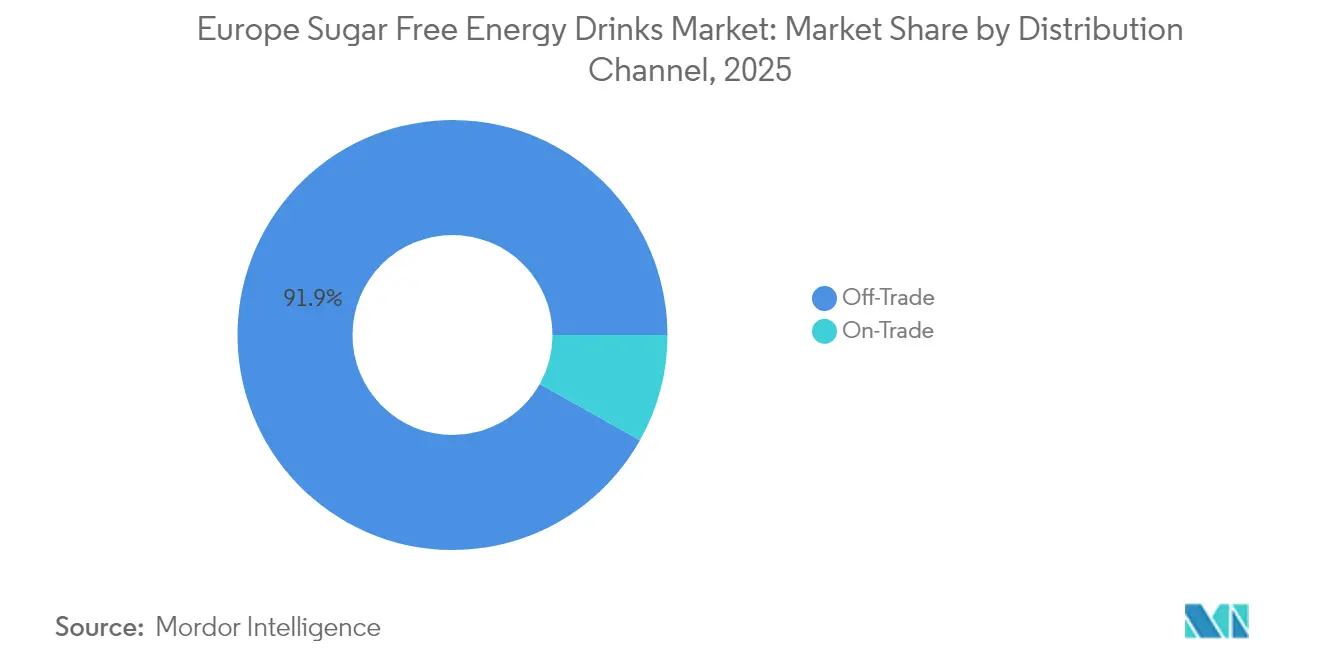

- By distribution channel, off-trade captured 91.86% of 2025 revenues while on-trade venues are projected to rebound at a 7.74% CAGR through 2031.

- By geography, the United Kingdom held 27.86% of regional value in 2025, and Spain is positioned for the fastest upturn with an 8.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sugar Free Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural and non-nutritive sweetener innovations | +1.5% | Global, with early adoption in United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| eSports and gaming-centric demand spike | +1.2% | United Kingdom, Germany, France, Spain, Poland | Short term (≤ 2 years) |

| Natural sweetener breakthroughs (stevia/allulose blends) | +1.3% | European Union-wide, pending novel food approvals in select markets | Long term (≥ 4 years) |

| Health-conscious consumers and European Union sugar taxes | +1.8% | United Kingdom, France, Belgium, Ireland, Spain, Portugal | Medium term (2-4 years) |

| E-commerce and DTC subscription surge | +1.0% | United Kingdom, Germany, Netherlands, Sweden, with spillover to Central Europe | Short term (≤ 2 years) |

| Growing college-athletics sponsorship spend | +0.8% | United Kingdom, Germany, France, Spain, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Natural and non-nutritive sweetener innovations

Innovation in natural and non-nutritive sweeteners is a significant factor driving the growth of sugar-free energy drinks in Europe. Brands are striving to balance health-focused positioning with taste equivalence to full-sugar variants. Consumers increasingly prefer “naturally sweetened” formulations that provide energy and functionality without added calories, sugar spikes, or artificial additives. This trend is encouraging manufacturers to move beyond first-generation high-intensity sweeteners toward advanced sweetening systems that enhance flavor authenticity, mouthfeel, and overall sensory appeal, key elements influencing repeat purchases in the energy drinks market. Regulatory clarity and advancements in ingredient technology are supporting this growth. European Commission Regulation 1131/2011 allows the use of steviol glycosides at levels up to 600 mg/L in energy drinks, providing formulators with flexibility to optimize sweetness intensity and blending strategies[1]Source: European Union, "Document 32011R1131," europa.eu. Additionally, next-generation sweeteners such as Ingredion’s ERYSTA erythritol and Tate & Lyle’s Reb M and Reb D stevia extracts represent significant technical progress [2]Source: Taet & Lyle, "Discover a range of stevia ingredients for your formulation needs.," tl.tateandlyle.com. These innovations enable brands to replicate sugar-like mouthfeel while reducing the bitterness associated with earlier stevia variants. These developments are driving the proliferation of “naturally sweetened” and “no artificial sweeteners” claims on European retail shelves, enhancing consumer trust and enabling sugar-free energy drinks to compete more effectively with full-sugar options and other functional beverages.

eSports and saming-centric demand spike

The growth of eSports, online gaming, and streaming culture across Europe is driving demand for sugar-free energy drinks. Gamers increasingly seek products that provide sustained mental alertness without the calorie intake or sugar crashes associated with traditional energy drinks. Competitive gaming sessions, often lasting several hours, require beverages that support cognitive stimulation, enhance reaction times, and improve focus. Sugar-free energy drinks meet these requirements, positioning themselves as "clean energy" options for gamers focused on performance, endurance, and prolonged consumption. Additionally, increasing health awareness among Gen Z and millennial consumers, who form the majority of the gaming demographic, is shifting preferences toward zero-sugar, naturally sweetened, and functional products. These include formulations with added nootropics, B-vitamins, and plant-based caffeine. Consequently, sugar-free energy drinks are becoming integral not only as beverages but also as performance enhancers within Europe’s expanding gaming economy. This trend is driving volume growth and fostering brand loyalty in a high-frequency consumption market segment.

Health-conscious consumers and European Union sugar taxes

Increasing health consciousness among European consumers, coupled with stricter sugar-reduction policies, is driving the shift toward sugar-free energy drinks. Awareness of the connection between excessive sugar consumption and lifestyle diseases has changed consumer expectations. Energy drinks are now seen not only as performance enhancers but also as products that should support long-term health objectives. Health risks and regulatory measures are further reinforcing this trend. According to the International Diabetes Federation, Portugal had the highest adult diabetes prevalence in Europe at 14.3% in 2024, followed by Croatia at 13.7% [3]Source: International Diabetes Federation, Diabetes Atlas," diabetesatlas.org. This has heightened public awareness of sugar consumption and boosted demand for low- and zero-sugar beverage options. Additionally, EU-wide and country-specific sugar taxes and reformulation targets, such as the UK Soft Drinks Industry Levy and similar measures in Western and Northern Europe, are significantly impacting category economics. These policies penalize high-sugar products while enhancing the price competitiveness of sugar-free alternatives.

E-commerce and DTC subscription surge

The growth of e-commerce and direct-to-consumer (DTC) subscription models is significantly driving the expansion of the Europe sugar-free energy drinks market. These channels are transforming how consumers discover, purchase, and consume products in this category. Digital platforms reduce entry barriers for both multinational and emerging brands, facilitating quicker market penetration without heavy dependence on traditional retail distribution. For sugar-free energy drinks, e-commerce platforms provide an effective medium to highlight functional benefits, ingredient transparency, and health attributes, key factors influencing purchase decisions among health-conscious and digitally savvy consumers. DTC subscription models further support this growth by promoting repeat purchases, increasing customer lifetime value, and fostering brand loyalty. Sugar-free energy drinks are particularly suited to auto-replenishment models due to their frequent consumption by professionals, gamers, fitness enthusiasts, and shift workers. Additionally, online-exclusive offerings, bundle pricing, and flavor-mix packs encourage product trials and cross-SKU purchases. The first-party data collected through DTC channels allows brands to quickly adapt formulations, packaging, and messaging to meet consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Artificial sweetener skepticism and clean-label concerns | -0.9% | United Kingdom, Germany, France, Netherlands, Sweden | Medium term (2-4 years) |

| Stricter caffeine and youth-marketing limits | -1.2% | United Kingdom Norway, Poland, Romania, with European Union-wide spillover risk | Short term (≤ 2 years) |

| Limited can-line capacity for slim formats | -0.6% | European Union-wide, concentrated in Central and Eastern Europe | Medium term (2-4 years) |

| Volatile high-intensity sweetener input costs | -0.7% | Global, with acute exposure in United Kingdom post-Brexit supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Artificial sweetener skepticism and clean-label concerns

Consumer skepticism toward synthetic sweeteners continues despite regulatory approvals. This concern was heightened by the 2023 update to the Nutri-Score algorithm, which reclassified artificially sweetened beverages from a median score of 1.0 to 4.0. As a result, most zero-sugar energy drinks were downgraded from B to C ratings. This policy change aligns with emerging epidemiological studies suggesting a link between non-nutritive sweeteners and metabolic disruption, even without caloric intake. In response, brands are increasingly exploring plant-based alternatives like monk fruit and allulose, which are positioned as "natural" options. However, allulose remains under novel-food review in the European Union and the United Kingdom, delaying its commercial availability. Consequently, manufacturers are relying on stevia-erythritol blends, which some consumers still view as processed.

Stricter caffeine and youth-marketing limits

Age-restriction measures are increasingly being adopted across Northern and Eastern Europe, including within the UK energy drinks market. The United Kingdom's Department of Health and Social Care impact assessment revealed that 4% of pupils aged 11 to 16 consume energy drinks daily, while 11% consume them weekly. Consumption rates are particularly higher in economically disadvantaged areas, where energy drinks are often more accessible and affordable. This has prompted consultations on implementing a statutory ban on sales to individuals under 16, aiming to address health concerns and curb excessive consumption among minors. In 2024, Poland and Romania introduced stricter regulations for energy drinks, enhancing requirements for labeling and distribution. These regulations apply irrespective of sugar content, restricting volume growth even for zero-sugar SKUs. The new rules are designed to ensure greater transparency and limit the availability of energy drinks to younger demographics. Consequently, brands are shifting their marketing strategies toward adult-focused channels, such as workplace vending, premium on-trade venues, and fitness-related partnerships, to mitigate the impact of these restrictions and target a more mature audience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Slim Cans Drive Premiumization

Metal cans accounted for 57.74% of the market share in 2025, driven by their strong presence in convenience stores, supermarkets, and vending machines, where their portability and refrigeration efficiency are prioritized over environmental concerns. PET bottles hold a moderate position, offering resealability and larger serving sizes that attract gym-goers and commuters. However, they face challenges due to single-use plastic bans being implemented in countries such as France, Spain, and Italy. Slim-format cans, typically ranging from 250 to 330 milliliters, are gaining popularity as brands target female and health-conscious consumers who associate smaller servings with moderation. Despite this demand, production capacity for these formats remains limited in Central and Eastern European co-packing facilities, leading to supply constraints during peak summer periods.

Glass bottles are expected to grow at a compound annual growth rate (CAGR) of 8.12% from 2026 to 2031, the highest among packaging formats. This growth is supported by on-trade venues and premium retail channels emphasizing sustainability and enhanced brand perception. PET bottles, while convenient, are under increasing regulatory scrutiny. The European Union's Single-Use Plastics Directive requires bottles to contain at least 25% recycled content by 2025 and 30% by 2030, which is driving up input costs and accelerating the transition toward aluminum and glass packaging alternatives.

By Distribution Channel: Off-Trade Dominance with On-Trade Recovery

Off-trade channels accounted for 91.86% of the market share in 2025, driven by convenience-store impulse purchases and supermarket promotional activities. However, on-trade venues are experiencing a resurgence, with a projected CAGR of 7.74% through 2031, as nightlife, fitness centers, and entertainment complexes increasingly incorporate energy drinks into their beverage offerings. Within the off-trade segment, online retail and direct-to-consumer subscriptions are gaining traction, particularly among gaming-focused brands like Rogue Energy and G FUEL. These brands provide customizable flavor packs and auto-replenishment services, bypassing traditional retail markups and fostering brand loyalty through community engagement.

On-trade growth is primarily concentrated in urban areas, where premium glass-bottle formats and functional positioning align with wellness trends. Gyms and yoga studios are emerging as high-margin distribution points, with sugar-free energy drinks competing directly with protein shakes and electrolyte beverages. The adoption of subscription models is most notable in the United Kingdom, Germany, and the Netherlands, where robust logistics infrastructure enables next-day delivery, and high digital payment penetration facilitates seamless recurring transactions.

Geography Analysis

The United Kingdom accounted for 27.86% of regional revenue in 2025, supported by a well-established retail environment, significant expansions in zero-sugar product portfolios, and a consumer base that has integrated functional beverages into daily consumption habits. The Department of Health and Social Care's consultation on restricting sales to individuals under 16 has introduced some uncertainty. However, brands are proactively shifting their marketing focus to adult-oriented channels, such as workplace vending machines and premium on-trade venues, to safeguard volume growth against potential age-related sales restrictions.

Spain is projected to grow at a compound annual growth rate (CAGR) of 8.21% through 2031, marking the fastest growth among major markets. This growth is driven by a younger demographic with high energy drink consumption and a regulatory framework that emphasizes reformulation rather than outright bans. Germany, France, and Italy collectively account for approximately 35% of regional volume. Germany, in particular, demonstrated double-digit growth in Monster Energy and Coca-Cola Zero Sugar during the second quarter of 2025, fueled by new product launches such as Rio Punch and Strawberry Dreams, which combine tropical flavors with zero-sugar formulations.

Poland, the Netherlands, Belgium, and Sweden are emerging as key growth markets. Poland benefits from increasing disposable incomes and a youthful population with consumption patterns similar to Spain. The Netherlands and Sweden lead in e-commerce penetration and direct-to-consumer sales adoption. Norway, although not part of the European Union, is influencing regional regulatory developments. Its Ministry of Health's proposed ban on sales to individuals under 16 has prompted reformulation efforts and marketing adjustments across Scandinavia. Meanwhile, the Rest of Europe, including Central and Eastern markets, is experiencing rapid growth as retail infrastructure modernizes and multinational brands expand distribution networks beyond major urban centers.

Competitive Landscape

The market is highly concentrated, with several players vying for market share. Private-label manufacturers represent 17% of business-to-business sales, offering retailer-owned brands that compete primarily on price while replicating zero-sugar formulations. This trend places considerable pressure on gross margins, compelling branded players to invest in experiential marketing and emphasize functional differentiation to sustain their competitive position. Branded players are increasingly focusing on creating unique customer experiences, such as interactive campaigns and personalized product offerings, to differentiate themselves in a competitive landscape dominated by price-sensitive alternatives.

New entrants, such as Celsius, Tenzing, and Grenade, are bypassing traditional retail channels by leveraging direct-to-consumer subscriptions, eSports sponsorships, and gym partnerships. These companies focus on ingredient transparency and community engagement, which appeal to younger consumers. By highlighting clean-label ingredients and fostering a sense of community through social media and events, these brands are able to connect with consumers on a deeper level. This strategy enables them to build loyalty among a demographic that increasingly questions the value and authenticity of legacy brands and their products, positioning themselves as modern and relatable alternatives.

Opportunities exist in areas such as functional hydration, plant-based formulations, and on-trade premiumization. In these segments, glass-bottle formats and premium ingredient narratives support higher per-serving margins by appealing to consumers seeking quality and exclusivity. Functional hydration products cater to health-conscious consumers, while plant-based formulations align with the growing demand for sustainable and ethical options. On-trade premiumization focuses on enhancing the consumer experience in hospitality settings, where premium offerings can command higher prices. These approaches also allow brands to differentiate themselves and reduce exposure to the intense price competition commonly observed in convenience stores.

Europe Sugar Free Energy Drinks Industry Leaders

-

Monster Beverage Corporation

-

PepsiCo, Inc.

-

Red Bull GmbH

-

Suntory Holdings Limited

-

Carabao Group Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Celsius is set to expand its presence in the United Kingdom and Ireland with the introduction of four new zero-sugar, fruit-forward energy drink flavors, scheduled for launch in January 2026. The new variants, Sparkling Raspberry Peach, Sparkling Mango Lemonade, Sparkling Kiwi Guava, and Sparkling Strawberry Watermelon, are part of the brand’s core range. This launch aims to address the increasing demand for healthier, sugar-free functional beverages.

- August 2025: Monster Energy has introduced a new grapefruit-flavored variant, Monster Ultra Fantasy Ruby Red, to its zero-sugar Ultra range. Rolling out across the United Kingdom from mid-August, the drink offers a unique grapefruit taste that balances sweetness and tartness with a refreshing citrus profile. It is available in vibrant pink 500 ml cans (both plain and price-marked) as well as in four-can multipacks.

- June 2025: Red Bull has introduced a new sugar-free energy drink in the United Kingdom, Red Bull Sugarfree Lilac Edition. Featuring a grapefruit and blossom flavor, this launch caters to consumer interest in innovative flavors. The product is available in convenience and grocery channels, offered in 250 ml, 335 ml, and 473 ml cans, as well as a 250 ml four-pack.

- January 2025: Maxxx-Energy, a Costa Rican brand owned by FIFCO, has launched a new sugar-free, zero-calorie energy drink line targeting active consumers and fitness enthusiasts. The updated formulations include ElevATP, which supports natural ATP production for sustained energy and endurance, and L-Carnitine, which enhances physical performance and aids in faster muscle recovery. The line is available in Apple-Kiwi and Blackberry Boost flavors, combining refreshing taste with performance-focused ingredients.

Europe Sugar Free Energy Drinks Market Report Scope

Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.| Metal Cans |

| PET Bottles |

| Glass Bottles |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others | |

| On-Trade |

| Germany |

| United Kingdom |

| Italy |

| Spain |

| France |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Packaging Type | Metal Cans | |

| PET Bottles | ||

| Glass Bottles | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| On-Trade | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| Spain | ||

| France | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms