Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

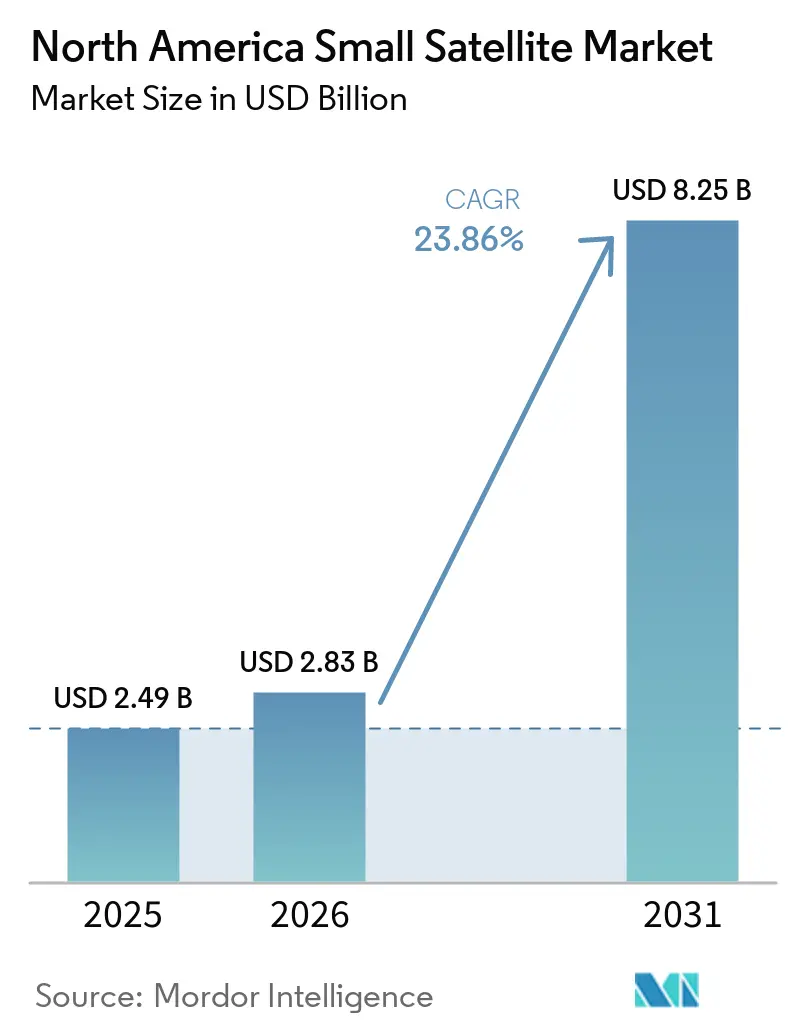

| Base Year Market Size (2025) | USD 2.49 Billion |

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 8.25 Billion |

| Growth Rate (2026 - 2031) | 23.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Small Satellite Market Analysis by Mordor Intelligence

The North America small satellite market size is projected to expand from USD 2.49 billion in 2025 and USD 2.83 billion in 2026 to USD 8.25 billion by 2031, registering a 23.86% CAGR between 2026 and 2031. Venture funding, reusable launch economics, and national-security procurements continue to reshape the competitive landscape. Constellation operators now treat LEO deployments as a recurring capital expense, while the US Department of Defense (DoD) pivots toward proliferated architectures that distribute sensing and communications across hundreds of nodes. SpaceX’s February 2026 price adjustment of USD 350,000 for the first 50 kilograms on Transporter rideshares still undercuts dedicated small-launch vehicles by several multiples, sustaining demand despite the increase. Commercial buyers are also shifting toward analytics-as-a-service contracts that fuse optical, synthetic-aperture radar (SAR), and hyperspectral data, accelerating recurring revenue streams for Earth observation providers.

Key Report Takeaways

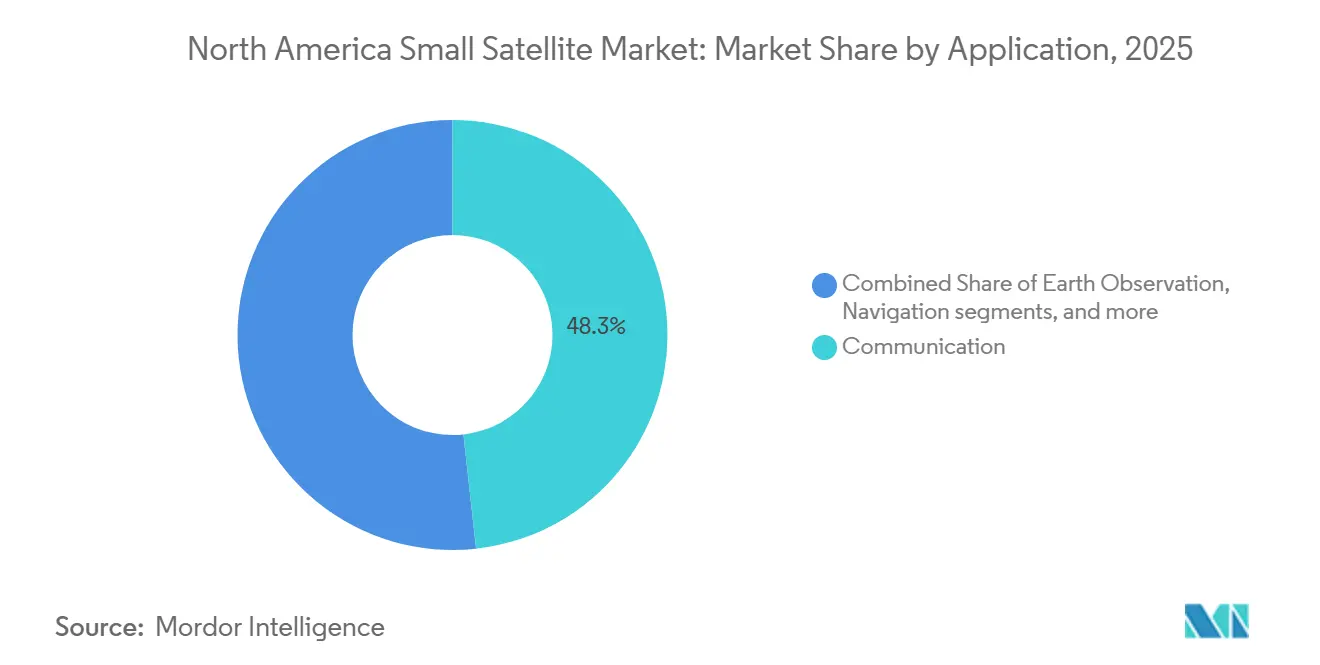

- By application, communication commanded 48.25% of the North America small satellite market share in 2025, while Earth observation is forecast to grow at a 24.78% CAGR through 2031.

- By orbit, LEO satellites accounted for 45.75% of the North America small satellite market in 2025, while MEO satellites are forecast to expand at a 24.83% CAGR over 2026-2031.

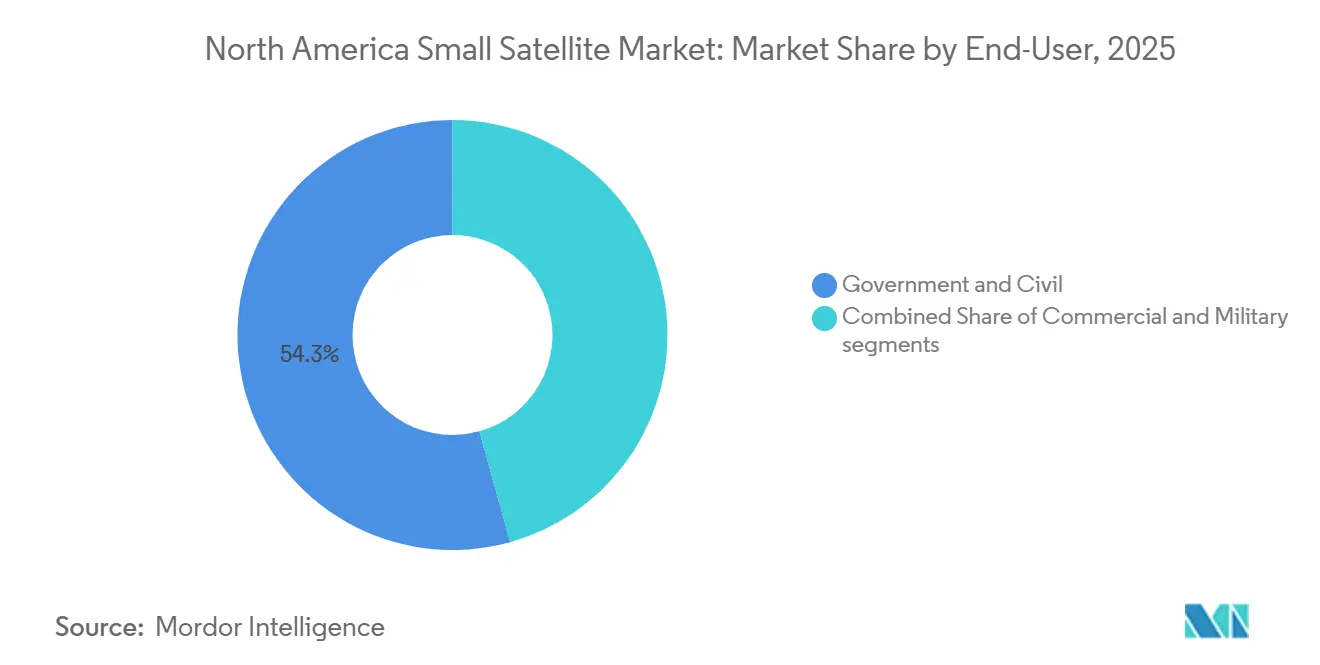

- By end user, government and civil entities accounted for 54.32% of the North America small satellite market in 2025, while the commercial segment is projected to grow at a 25.95% CAGR through 2031.

- By mass, minisatellites led the North America small satellite market with a 46.69% share in 2025; microsatellites are forecast to grow at a 25.58% CAGR through 2031.

- By geography, the United States accounted for 85.77% of the revenue share in 2025 and is forecast to grow at a 25.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Small Satellite Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining launch costs driven by reusable rockets | +6.2% | North America-wide, concentrated in US spaceports | Short term (≤ 2 years) |

| Rising private investment in large small-sat constellations | +5.8% | United States dominates; Canada emerging | Medium term (2-4 years) |

| Growing demand for high-resolution Earth-observation imagery | +4.5% | United States, Canada; spillover to Mexico | Medium term (2-4 years) |

| Government spending on national-security small-sat programs | +4.3% | United States, Canada | Long term (≥ 4 years) |

| Shift toward software-defined payloads | +2.8% | United States, Canada | Medium term (2-4 years) |

| Emergence of on-orbit servicing contracts | +1.5% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Resolution Earth-Observation Imagery

The growing demand for high-resolution Earth imagery is driven by its applications in agriculture, urban development, security, and disaster relief. Satellites belonging to Maxar Technologies’ WorldView Legion series provide highly detailed imagery (30 cm class) and improved revisit frequency, enabling faster responses to time-sensitive incidents such as natural disasters.[1]Maxar Editorial Team, “WorldView Legion Constellation Overview,” Maxar, maxar.com The upcoming Pelican series from Planet Labs features satellites with onboard computing, enabling efficient data processing and reduced latency. In addition, ICEYE continues to build its SAR constellation to deliver highly detailed (25 cm-class) all-weather imagery.[2]ICEYE Awarded EUR 1.7 Billion Contract by the Netherlands,” ICEYE, iceye.com All of these developments are contributing to the move toward subscription-based Earth observation services. Companies like Planet Labs and Maxar Technologies have enabled real-time analysis of high-resolution images in North America.

Declining Launch Costs Driven by Reusable Rockets

Reusable launch systems are significantly altering cost structures by not only reducing prices but also enhancing launch frequency and reliability. SpaceX has achieved over 300 booster landings with Falcon 9 rockets, making them reusable and more cost-effective than other rockets, thereby increasing the competitiveness of its rideshare missions, despite challenges such as rigid schedules and the prioritization of the primary mission. Nevertheless, satellite operators often prefer these missions as they provide better cost efficiency. Simultaneously, new launches by companies such as Rocket Lab, Firefly Aerospace, and Relativity Space have enhanced the capabilities of small launchers. The rapid turnaround of boosters enables small satellite operators to plan flexible, on-demand deployments, reducing capital risks and enhancing the scalability of satellite constellations.

Rising Private Investment in Large Small-Sat Constellations

Investors are increasingly focusing on the vertical integration of satellite constellations to generate revenue from data and related services. Xona Space Systems secured over USD 150 million in funding to develop its Pulsar LEO constellation, which aims to deliver positioning accuracy from centimeter to meter levels for commercial and defense applications.[3]Xona Space Systems, “Raises USD 170 Million Series B,” xonaspace.com Additionally, Tomorrow.io raised approximately USD 175 million in Series E funding to advance its weather satellite constellation, enabling the collection of high-frequency atmospheric data for industries such as aviation, energy, and logistics. Furthermore, CesiumAstro obtained more than USD 250 million to expand the production of software-defined phased-array antennas.

Government Spending on National-Security Small-Sat Programs

Increased emphasis on defense in North America is driving substantial government investment in small satellites for security applications. The Space Development Agency is allocating billions of dollars to its Tracking Layer Tranche 3 satellites, which feature infrared sensors for hypersonic missile detection and optical intersatellite communications for rapid data transfer. Similarly, Canada is supporting the development of Telesat's Lightspeed LEO constellation to enhance domain awareness and maritime surveillance in the Arctic region. This focus is encouraging greater participation from subsystem manufacturers and software providers in the defense sector, thereby supporting the growth of the small satellite market in North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Orbital-debris congestion and stricter licensing rules | -2.5% | United States, Canada | Short term (≤ 2 years) |

| RF-spectrum crowding for small-sat communications | -2.2% | North America-wide | Medium term (2-4 years) |

| Limited launch-slot availability during peak windows | -1.8% | United States launch ranges | Short term (≤ 2 years) |

| Insurance-premium hikes for multi-sat rideshare launches | -1.3% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Orbital-Debris Congestion and Stricter Licensing Rules

The growing congestion issue has led to stricter regulations for spacecraft operators, particularly in the US, where licensing requirements for small satellites are becoming more stringent. The Federal Communications Commission (FCC) now requires that low Earth orbit satellites be deorbited within 5 years of completing their missions.[4]Federal Communications Commission, “Proposes to Modernize Satellite Licensing Rules,” fcc.gov This regulation requires operators to implement mitigation measures such as propulsion systems or drag augmentation technology. Additionally, debris mitigation regulations are being updated to ensure adherence to these standards. Satellite operators have recognized benefits, such as faster compliance licensing processes. However, compliance is becoming more expensive due to the growing size of constellations, which adds complexity to design and operations.

Limited Launch-Slot Availability During Peak Windows

The limited availability of launch slots within specific timeframes for placing satellites into orbit has emerged as a significant operational challenge in small satellite launches. The SpaceX Rideshare Program primarily targets sun-synchronous orbits, which are well-suited for Earth observation satellite missions, and operates on a fixed schedule. Missing a scheduled launch slot can lead to delays of up to six months, impacting revenue generation and competitive positioning. While dedicated satellite launches offer greater scheduling flexibility, they are considerably more expensive compared to rideshare programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Analytics Platforms Outpace Raw Imagery Sales

Communication remained the largest slice of the North America small satellite market in 2025, accounting for 48.25% of revenue, chiefly because Starlink surpassed 6,000 active satellites and expanded direct-to-cell coverage. Yet Earth observation is growing faster, at a 24.78% CAGR, as enterprise customers migrate to subscription-based analytics. Planet’s EUR 240 million (USD 281.35 million) German capacity deal and Tanager-1’s detection of 5,500 methane events illustrate how value shifts from raw pixels to decision-ready insights. Navigation and hybrid PNT payloads such as Xona’s centimeter-level Pulsar constellation add diversification, while space-observation missions use commercial buses like Satellogic’s to prototype new sensors. A second-order effect is cross-fertilization: hybrid satellites combine broadband radios with optical imagers, maximizing revenue per kilogram. Regulatory hurdles diverge; communication operators benefit from streamlined FCC procedures, whereas Earth-observation missions still navigate export-control reviews that extend lead times. Analytics providers, therefore, push for policy harmonization to accelerate customer onboarding, a trend that should enlarge the North America small satellite market over the forecast period.

By Orbit: MEO Economics Challenge LEO Dominance in Niche Segments

LEO captured 45.75% of the revenue share in 2025 because its 500-600 kilometer sweet spot balances revisit rates, launch costs, and link budgets. MEO is now growing at a 24.83% CAGR, led by Xona’s planned 258-satellite Pulsar network offering 5-centimeter accuracy and anti-jam resilience. The North America small satellite market for MEO services is poised to grow as agriculture and autonomous-vehicle customers pay premiums for guaranteed integrity and redundancy. GEO missions remain sparsely populated because propulsion budgets push small spacecraft into higher mass classes. Still, Northrop Grumman’s Mission Extension Pods show that even sub-500-kilogram craft can make GEO financially viable when electric propulsion is combined with life-extension services. Orbit-specific regulation also shapes demand: the FCC’s five-year rule hits LEO hardest, whereas GEO operators focus on longitudinal slot coordination.

By End-User: Commercial Growth Outstrips Government Despite Smaller Base

Government and civil users accounted for 54.32% of the North America small satellite market share in 2025, bolstered by SDA and NRO contracts that guarantee multi-year budgets. Commercial demand, however, is running ahead with a 25.95% CAGR as insurers, logistics firms, and commodity traders bake satellite data into daily workflows. Tomorrow.io’s weather constellation pre-sells forecasts to airlines and event organizers, converting a historically public-sector service into a recurring revenue engine. Dual-use strategies dominate: Planet holds contracts with both the National Reconnaissance Office and European governments while selling subscriptions to agribusiness and infrastructure clients. That diversification buffers market cyclicality and spreads regulatory risk, reinforcing growth prospects for the North America small satellite market.

By Satellite Mass: Microsatellites Gain Share Through Component Miniaturization

Minisatellites accounted for 46.69% of 2025 revenue, valued for their payload volume that accommodates phased-array antennas and high-power radars. Microsatellites are nevertheless the fastest risers, with a 25.58% CAGR, thanks to CMOS imagers and software-defined radios that squeeze enterprise-grade performance into lighter buses. Planet’s 40-kilogram Pelican satellites deliver 50-centimeter resolution with on-board AI, showing how microsats can match or exceed legacy minisat quality metrics. Blue Canyon’s reaction-wheel factory expansion from 650 to 2,400 units per year illustrates how supply chain adjustments follow mass-market shifts. Regulatory costs do not yet scale by mass, but disposal-reliability thresholds may push operators toward fewer, larger satellites over time if compliance becomes too onerous.

Geography Analysis

Regional dynamics in North America highlight the dominance of the US, alongside the growing contributions of Canada and Mexico. The US is projected to account for 85.77% of the North America small satellite market in 2025 and is expected to grow at a CAGR of 25.85% through 2031, according to analyst estimates. This growth is attributed to modifications in FCC licensing aimed at expediting authorization processes and increased funding from venture capital firms for space technology. Furthermore, SpaceX's Starlink, in collaboration with T-Mobile, has introduced direct-to-cell connectivity, enhancing coverage in rural areas and enabling opportunities for IoT services. Additionally, the Space Development Agency's Tracking Layer projects strengthen domestic supply chains by driving demand toward satellite manufacturing and subsystem companies within the US.

Canada is leveraging its Arctic geographic advantage and a public-private financing model to develop a distinct competitive position. Telesat's Lightspeed satellite system, with an estimated capacity of nearly 200 satellites, aims to provide high-capacity connectivity, particularly for underserved polar regions. Additionally, MDA Corporation is consistently enhancing its sovereign synthetic aperture radar systems, supporting both defense objectives and international information service needs.

Mexico remains a relatively new participant in the regional ecosystem. CubeSat development through universities supports disaster monitoring applications, while collaborations with American companies facilitate technology transfers and manufacturing processes. The Instituto Federal de Telecomunicaciones is working to establish effective licensing regulations for small satellites to attract international investments. However, limited financing and challenges in infrastructure development may impede progress.

Competitive Landscape

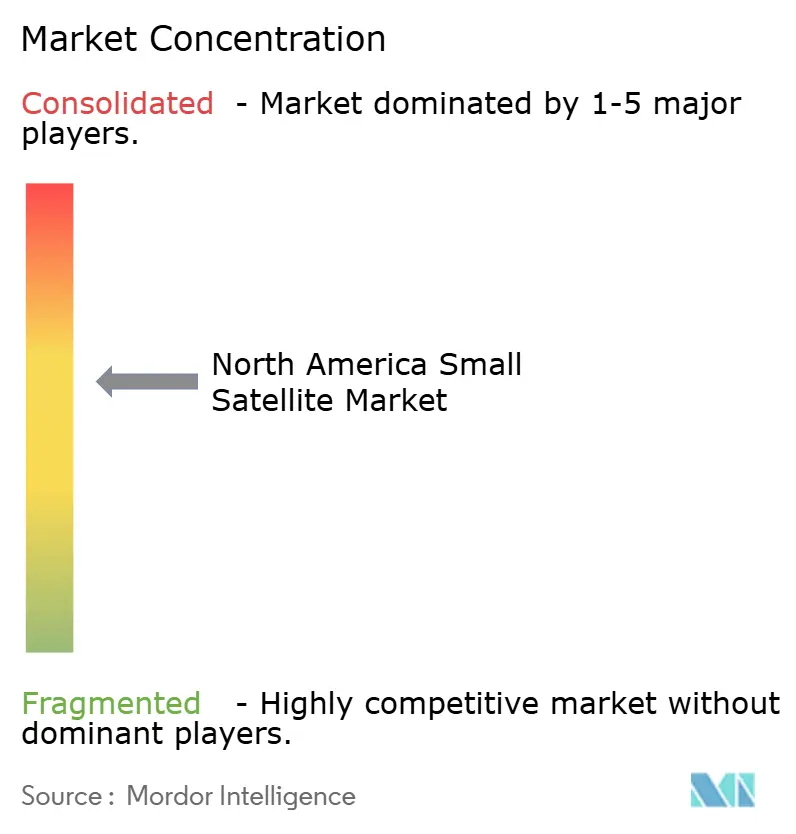

The North America small satellite market exhibits moderate concentration, encompassing both integrated prime contractors and specialized component manufacturers operating across various stages of the supply chain. Established players such as The Boeing Company, SpaceX, and Planet Labs leverage economies of scale, vertical integration, and comprehensive service offerings to maintain their competitive edge.

Meanwhile, subsystem providers such as Blue Canyon Technologies, L3Harris Technologies, and CesiumAstro play a key role in driving innovation, particularly in attitude control, communication payloads, and software-defined satellite architectures. The competitive landscape is shaped by advancements in technology, with software-defined payloads, data processing capabilities, and rapid re-tasking functionalities attracting significant attention and investment.

Emerging technologies, including phased-array antennas and in-orbit servicing solutions, have been introduced by companies such as Northrop Grumman and L3Harris Technologies to secure future revenue streams. Regulatory frameworks significantly impact competition, as changes in Federal Communications Commission requirements have increased compliance costs, favoring larger, well-funded firms and contributing to a growing trend of mergers and acquisitions among smaller operators. However, opportunities persist for innovative entrants to the market.

North America Small Satellite Industry Leaders

L3Harris Technologies, Inc.

Northrop Grumman Corporation

The Boeing Company

Space Exploration Technologies Corp.

Blue Canyon Technologies, LLC (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Amazon acquired Globalstar for USD 11.5 billion to enhance its LEO satellite communications capabilities, positioning it as a direct competitor to Starlink. This move highlighted the increasing competition in device-based communication and the development of satellite constellations.

- March 2026: SpaceX began offering rideshare services at a competitive rate of approximately USD 350,000 per kg of payload for a 50 kg payload. This pricing strategy provides SpaceX with a competitive advantage and positions ridesharing as a cost-effective option.

- January 2026: The Blue Canyon Technologies Saturn-200 minisatellite bus was employed for NASA's Pandora Mission. The mission's primary objective is to study the atmospheres of exoplanets, highlighting the growing use of small satellite buses in scientific missions.

- January 2026: Starfish Space secured a contract valued at approximately USD 52 million with the US Space Force to provide satellite end-of-life disposal services for LEO constellations. This agreement is among the early examples of commercial contracts for in-orbit servicing, reflecting growing interest in sustainable practices within satellite constellations.

North America Small Satellite Market Report Scope

Small satellites are those satellites weighing under 500 kg. The small satellite market report excludes sounding rockets, high-altitude balloon platforms, and purely experimental payloads.

The North America small satellite market is segmented by application, orbit, end-user, satellite mass, and geography. By application, the market is segmented into communication, Earth observation, navigation, space observation, and others. By orbit, the market is segmented into low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary orbit (GEO). By end-user, the market is segmented into commercial, government and civil, and military. By satellite mass, the market is segmented into femtosatellites, picosatellites, nanosatellites, microsatellites, and minisatellites. The report also covers the market sizes and forecasts for the small satellite market in three countries across the region. For each segment, the market size is provided in terms of value (USD).

By Application

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

By Orbit

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

By End-User

| Commercial |

| Government and Civil |

| Military |

By Satellite Mass

| Femtosatellites |

| Picosatellites |

| Nanosatellites |

| Microsatellites |

| Minisatellites |

By Geography

| United States |

| Canada |

| Mexico |

| By Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| By Orbit | Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) | |

| Geostationary Orbit (GEO) | |

| By End-User | Commercial |

| Government and Civil | |

| Military | |

| By Satellite Mass | Femtosatellites |

| Picosatellites | |

| Nanosatellites | |

| Microsatellites | |

| Minisatellites | |

| By Geography | United States |

| Canada | |

| Mexico |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.