North America Military Satellite Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 8.96 Billion |

| Market Size (2030) | USD 13.26 Billion |

| Growth Rate (2025 - 2030) | 8.14% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Military Satellite Market Analysis by Mordor Intelligence

The North America Military Satellite Market size is estimated at 8.96 billion USD in 2025, and is expected to reach 13.26 billion USD by 2030, growing at a CAGR of 8.14% during the forecast period (2025-2030).

The North American military satellite industry continues to evolve rapidly, driven by increasing defense requirements and technological advancements. The United States maintains its position as the epicenter of space innovation and research, with government expenditure for space programs reaching a record high of approximately USD 24.8 billion in 2022. This substantial investment reflects the growing recognition of military space-based capabilities as critical components of modern military operations. The industry has witnessed significant technological convergence, with artificial intelligence, machine learning, and advanced electronics being integrated into satellite systems to enhance their capabilities and operational efficiency.

The market landscape is experiencing a transformation through strategic partnerships and technological collaborations between government agencies and private companies. In January 2023, SpaceX announced the launch of Starshield, a new Earth observation military satellite developed specifically for government agencies operating in the national security sector. This satellite incorporates high-assurance cryptographic capabilities to host classified payloads and process data securely, demonstrating the industry's focus on enhanced security features. The US Department of Defense agencies are actively working with military contractors, commercial satellite operators, and technology companies to demonstrate the feasibility of Earth-orbited constellation satellites.

The industry has witnessed substantial progress in satellite deployment and operational capabilities. During 2017-2022, more than 180 satellites manufactured and launched were owned by North American military and government organizations, highlighting the region's commitment to expanding its space-based capabilities. The market is characterized by increasing emphasis on interoperability and multi-mission capabilities, with satellites being designed to support various applications simultaneously. This trend is evident in recent developments where satellites are being equipped with multiple payloads to serve diverse military requirements efficiently.

The sector is experiencing a shift toward more sophisticated communication and surveillance capabilities. In January 2023, Lockheed Martin achieved a significant milestone with the sixth Global Positioning System III satellite entering its operational orbit, contributing to the ongoing modernization of the US Space Force's GPS constellation. The industry is witnessing increased focus on developing advanced missile warning systems and military surveillance satellite capabilities, with companies like Raytheon Intelligence & Space being awarded contracts to develop prototype missile tracking systems. These developments reflect the growing importance of space-based assets in maintaining military superiority and national security.

North America Military Satellite Market Trends and Insights

Growing demand for nano and microsatellites is expected

- The ability of small satellites to perform nearly all of the functions of a traditional satellite at a fraction of the cost of a traditional satellite has increased the viability of building, launching, and operating small satellite constellations. During 2017-2022, various players in the region placed a total of 459 nanosatellites into orbit.

- The demand from North America is primarily driven by the United States, which manufactures the largest number of small satellites annually. Although the launches from the country have decreased over the last three years, the country’s industry holds enormous potential. Ongoing investments in start-ups and nano and microsatellite development projects are expected to boost the revenue growth of the region.

- Currently, NASA is involved in several projects aimed at developing these satellites. NASA is currently using CubeSats for conducting advanced exploration and demonstrating newly emerging technologies for conducting scientific research and educational investigations.

- In March 2020, the Canadian Armed Forces awarded a contract to Elbit Systems to supply satellite communication services to mobile units as part of the Land Command Support System Life Extension program (LCSS LE) program. The deal involves triple-band ELSAT 2100 SATCOM on-the-move (SOTM) systems that aid in real-time broadband communications for mobile military units. The 2100-ELSAT SOTM systems will enable the Canadian Armed Forces to maintain long-range voice and data connectivity between mobile command vehicles, liaison elements, high-priority sensor vehicles, and tactical headquarters or command posts.

,-Number-of-Launches,-North-America,-2017---2022.svg)

Increasing defense spending drives the demand for military satellites in North America

- In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. The US government's spending on its space programs makes the country as a highest spender on the development of satellites across the world. Regarding research and investment grants, the region's governments and the private sector have dedicated funds for research and innovation in the space industry. Agencies spend available budgetary resources by making financial promises called obligations. For instance, till February 2023, the National Aeronautics and Space Administration (NASA) had distributed USD 333 million as research grants.

- In October 2020, the Space Development Agency (SDA) awarded a USD 149 million contract to SpaceX to design, manufacture, and launch a new military satellite capable of tracking and providing early warnings of hypersonic missile launches. A similar contract worth USD 193 million was also awarded to L3Harris during the same timeframe. Eight satellites are scheduled to be manufactured by both companies and are meant to be the first crucial part of the SDA's Tracking Layer Tranche 0, designed to provide missile tracking for the Department of Defense from space using infrared sensors. Apart from the United States, the Canadian space industry adds USD 2.3 billion to the Canadian GDP and employs 10,000 people, according to the Canadian government. The government reports that 90% of Canadian space firms are small- and medium-sized businesses. The Canadian Space Agency's (CSA) budget is modest, and the estimated budgetary spending for 2022-23 was USD 329 million.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The United States is driving the demand in the market

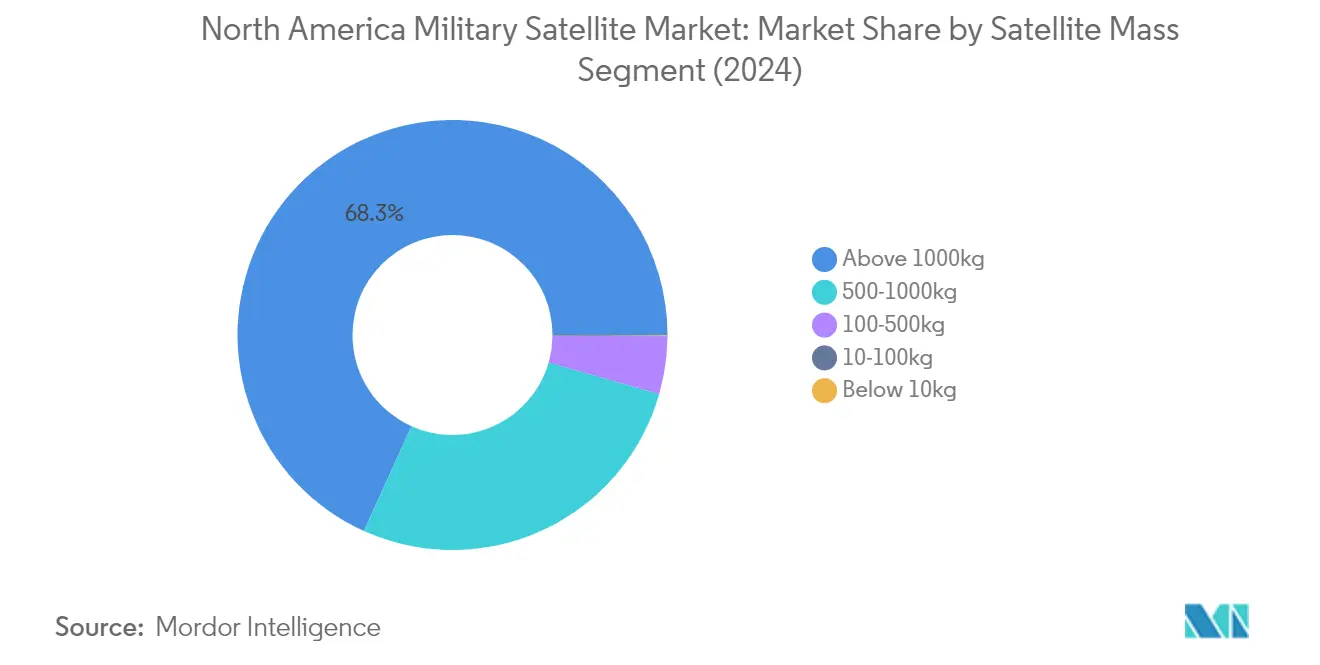

Segment Analysis: Satellite Mass

Above 1000kg Segment in North America Military Satellite Market

The above 1000kg satellite segment dominates the North American military satellite market, commanding approximately 68% market share in 2024. These large satellites are primarily designed for operational purposes with extended lifespans ranging between five and ten years, making them ideal for carrying larger remote sensing payloads and higher numbers of transponders with larger antennas for communication purposes. These operational satellites incorporate redundancy across all major subsystems to support accidental failures and extend their operational life. The satellites in this segment are typically constructed with radiation-hardened space-grade electronics and generate substantial power through larger deployable solar panels to support all subsystems and larger loads. Major defense contractors like Lockheed Martin and Northrop Grumman continue to secure significant contracts for developing and launching these heavy satellites for various military applications, including missile warning systems, secure communications, and surveillance operations.

10-100kg Segment in North America Military Satellite Market

The microsatellite segment (10-100kg) is experiencing the fastest growth trajectory, projected to expand at approximately 27% during 2024-2029. These satellites are designed for medium-duration applications of up to two years and feature redundancy for critical subsystems like bus management units. The growth is primarily driven by their lower manufacturing costs and ability to be mass-produced more efficiently. The flexibility and responsiveness of these smaller missions to new technological opportunities have made them increasingly attractive to military and defense agencies. These satellites can achieve about 80% of program goals at roughly 20% of the cost compared to larger satellite solutions. The US Space Force and other defense organizations are increasingly adopting these microsatellites for various applications, including Earth observation, communications, technology development, and space science missions.

Remaining Segments in Satellite Mass

The remaining segments in the market include satellites ranging from 500-1000kg (medium-sized), 100-500kg (minisatellites), and below 10kg (nanosatellites). Medium-sized satellites offer greater coverage with fewer launches and are particularly valued for surveillance and intelligence gathering. Minisatellites compete with larger satellites in many applications, benefiting from electronic miniaturization and redundant electronics. Nanosatellites, while representing a smaller market share, are gaining traction due to their cost-effectiveness and suitability for constellation deployments. Each of these segments serves specific military requirements and contributes to the overall robustness of North America's space capabilities.

Segment Analysis: Orbit Class

LEO Segment in North America Military Satellite Market

Low Earth Orbit (LEO) dominates the North American military satellite market, commanding approximately 85% market share in 2024. This significant market position is driven by the segment's widespread adoption in modern communication technologies and critical Earth observation applications. The US Department of Defense agencies are actively collaborating with military contractors, commercial satellite operators, and technology companies to demonstrate the feasibility of Earth-orbited constellation satellites. These satellites, operating at altitudes below 1,000 km, are particularly valuable for military reconnaissance satellite operations, espionage, and imaging applications. The reduced signal runtime in LEO results in lower latency, making these satellites ideal for time-sensitive military communications. Major defense contractors like Lockheed Martin and York Space Systems are developing advanced LEO satellites with sophisticated capabilities, including data communications transport and rocket tracking functionalities.

GEO Segment in North America Military Satellite Market

The Geostationary Earth Orbit (GEO) segment is experiencing rapid growth in the North American military satellite market, with projections indicating significant expansion from 2024 to 2029. The segment's growth is primarily driven by increasing demand for GEO satellite services from government and military applications, particularly in communications, navigation, surveillance, remote sensing, weather forecasting, and satellite broadcasting. Military organizations are investing heavily in GEO satellites due to their ability to provide continuous coverage over specific geographic regions. The US Space Force is actively expanding its GEO satellite capabilities through various programs and missions, including advanced communication satellites and space-based infrared systems for missile warning capabilities. These developments are supported by major defense contractors who are incorporating cutting-edge technologies to enhance the capabilities of GEO satellites for military applications.

Remaining Segments in Orbit Class

The Medium Earth Orbit (MEO) segment plays a vital role in the North American military satellite market, particularly in global navigation systems and satellite-based communication systems. MEO satellites, operating at an altitude of around 20,000 km, offer distinct advantages in terms of signal strength and improved communications capabilities compared to other orbital configurations. These satellites are crucial for military applications, providing essential services for navigation, targeting, and intelligence gathering. The US military's increasing focus on MEO satellites is evident in their strategic initiatives to develop new constellation systems for enhanced surveillance and communication capabilities. The segment continues to evolve with technological advancements in areas such as missile tracking and defense systems.

Segment Analysis: Satellite Subsystem

Propulsion Hardware and Propellant Segment in North America Military Satellite Market

The Propulsion Hardware and Propellant segment dominates the North American military satellite market, commanding approximately 79% of the total market share in 2024. This segment's prominence is primarily driven by the increasing launch of mass satellite constellations into space, where propulsion systems play a crucial role in transferring spacecraft to orbit and adjusting their positions. The segment's growth is further bolstered by significant technological advancements in propulsion systems, including the development of both chemical and electric propulsion solutions. The US military's emphasis on developing advanced propulsion technologies, particularly for high-performance defense applications, has led to substantial investments in this segment. Major defense contractors are actively working on innovative propulsion solutions, including nuclear propulsion technologies and alternative fuel options, to enhance the maneuverability and longevity of military surveillance satellite systems in various orbital configurations.

Satellite Bus & Subsystems Segment in North America Military Satellite Market

The Satellite Bus & Subsystems segment is experiencing the most rapid growth in the North American military satellite market, with a projected growth rate of approximately 17% during the forecast period 2024-2029. This remarkable growth is driven by increasing miniaturization of electronic components, enabling the creation of more lightweight and cost-effective satellite buses while maintaining advanced technological capabilities. The segment's expansion is further supported by significant investments from private players in research and development, particularly in developing flexible, multi-mission spacecraft platforms. Recent technological advancements, including the integration of artificial intelligence and machine learning capabilities into satellite buses, are revolutionizing space operations. The US Space Force's increasing focus on adaptable, multi-mission spacecraft platforms has led to the development of innovative satellite bus designs that can support multiple missions, including remote sensing, communications, imaging, radar, and persistent surveillance applications.

Remaining Segments in Satellite Subsystem

The Solar Array & Power Hardware and Structures, Harness & Mechanisms segments play vital complementary roles in the North American military satellite market. The Solar Array & Power Hardware segment is crucial for providing sustainable power solutions for satellites, with manufacturers focusing on developing increasingly efficient and durable solar panel technologies for various orbital applications. The Structures, Harness & Mechanisms segment encompasses critical components such as satellite antennas and structural elements, which are essential for maintaining satellite integrity and ensuring effective communication capabilities. Both segments are experiencing technological advancements, with manufacturers emphasizing the development of lighter, more durable materials and more efficient power management systems to enhance overall satellite performance and longevity.

Segment Analysis: Application

Earth Observation Segment in North America Military Satellite Market

Earth observation satellites dominate the North American military satellite market, commanding approximately 83% market share in 2024. These satellites serve critical functions in military operations, providing essential data for surveillance, intelligence gathering, and monitoring activities. The segment's prominence is driven by increasing investments from defense agencies for applications such as border and maritime security monitoring, forestry and ocean resource tracking, and disaster management capabilities, including drought and flood forecasting. The US National Reconnaissance Office's continued deployment of intelligence-gathering satellites, which supply optical and radar surveillance imagery and data relay support, further strengthens this segment's position. Advanced Earth observation satellites are being equipped with sophisticated sensors and imaging capabilities to enhance military situational awareness and strategic decision-making capabilities.

Navigation Segment in North America Military Satellite Market

The navigation segment is experiencing remarkable growth in the North American military satellite market, projected to expand at approximately 27% annually from 2024 to 2029. This exceptional growth is driven by the increasing integration of GPS capabilities in modern military operations and the rising demand for precise positioning and timing services. The US Space Force's ongoing modernization of GPS satellites, featuring enhanced anti-jamming capabilities and improved accuracy, is contributing significantly to this segment's expansion. Military organizations are increasingly relying on navigation satellites for applications such as precision targeting, surveillance operations, troop movement coordination, and search and rescue missions. The development of next-generation navigation systems with enhanced security features and resilience against interference is further accelerating the segment's growth trajectory.

Remaining Segments in Application

The North American military satellite market encompasses several other vital segments, including communication, space observation, and other specialized applications. The communication segment plays a crucial role in maintaining secure and reliable military communications across various platforms and operational environments. Space observation satellites contribute to space situational awareness and monitoring of potential threats in orbit. The other specialized applications segment includes technology demonstration missions, signal intelligence gathering, and educational initiatives that support military space systems capabilities. These segments collectively enhance the military's space-based capabilities and contribute to maintaining technological superiority in space operations.

Competitive Landscape

Top Companies in North America Military Satellite Market

The North American military satellite market is characterized by continuous product innovation among major players, with companies focusing on developing advanced satellite technologies for enhanced military capabilities. Companies are demonstrating operational agility through the rapid deployment of new satellite constellations and responsive launch capabilities to meet evolving defense requirements. Strategic moves in the industry primarily revolve around partnerships with government agencies, particularly the U.S. Department of Defense and Space Force, while companies are also pursuing collaborative ventures for technology development and payload integration. Market leaders are expanding their manufacturing facilities and research centers, particularly in key aerospace hubs across the United States, to strengthen their production capabilities and maintain technological leadership. These companies are also investing heavily in developing next-generation satellite buses, propulsion systems, and communication payloads while emphasizing the integration of artificial intelligence and machine learning capabilities in their satellite systems.

Consolidated Market Led By Defense Giants

The North American defense satellite market exhibits a highly consolidated structure dominated by established defense and aerospace conglomerates, particularly Lockheed Martin and Northrop Grumman, which possess extensive experience in military satellite manufacturing and deep relationships with defense agencies. These major players leverage their comprehensive capabilities across the entire satellite value chain, from design and manufacturing to launch and operational support services. The market's high barriers to entry, including stringent regulatory requirements, substantial capital investments, and the need for specialized technological expertise, have contributed to maintaining this consolidated structure.

The market has witnessed selective merger and acquisition activities, primarily focused on acquiring specialized technological capabilities and expanding product portfolios. Large defense contractors are particularly interested in acquiring companies with expertise in emerging technologies such as small satellite manufacturing, advanced propulsion systems, and space-based sensors. The trend towards vertical integration is evident as major players seek to control critical components of their supply chain and enhance their ability to deliver complete satellite solutions to military customers.

Innovation and Integration Drive Future Success

For incumbent companies to maintain and expand their market share, they must focus on developing modular and scalable satellite platforms that can accommodate evolving military requirements while reducing production costs and deployment timelines. Success in this market increasingly depends on the ability to integrate commercial space technologies with military space capabilities, particularly in areas such as secure communications, space situational awareness, and missile warning systems. Companies must also strengthen their relationships with key military decision-makers and demonstrate the ability to deliver reliable, long-term satellite solutions that align with evolving defense strategies.

For contenders seeking to gain ground in this market, specialization in niche capabilities such as small satellite technologies, advanced sensors, or specific orbital applications presents opportunities for market entry and growth. The increasing emphasis on space resilience and the proliferation of small satellite constellations creates opportunities for new players to provide innovative solutions. However, success requires navigating complex regulatory requirements, particularly those related to national security and export controls, while building strong relationships with prime contractors and government agencies. The concentration of military end-users and the critical nature of satellite applications in defense operations necessitate maintaining high reliability standards and demonstrating long-term commitment to supporting military space technology capabilities.

North America Military Satellite Industry Leaders

Ball Corporation

Lockheed Martin Corporation

Northrop Grumman Corporation

Raytheon Technologies Corporation

The Boeing Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: Ball Aerospace was selected by the US Air Force’s Space and Missile Systems Center (SMC) to deliver the next-generation operational environmental satellite system, Weather System Follow-on – Microwave (WSF-M), for the Department of Defense (DoD).

- February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the smallsat missions aboard the Transporter-6 launch, which pitched 114 small payloads into polar orbit.

- February 2023: Blue Canyon Technologies LLC, a subsidiary of Raytheon Technologies, provided critical hardware components for several of the SmallSat missions aboard the Transporter-6 launch that pitched 114 small payloads into polar orbit.

North America Military Satellite Market Report Scope

10-100kg, 100-500kg, 500-1000kg, Below 10 Kg, above 1000kg are covered as segments by Satellite Mass. GEO, LEO, MEO are covered as segments by Orbit Class. Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms are covered as segments by Satellite Subsystem. Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application.| 10-100kg |

| 100-500kg |

| 500-1000kg |

| Below 10 Kg |

| above 1000kg |

| GEO |

| LEO |

| MEO |

| Propulsion Hardware and Propellant |

| Satellite Bus & Subsystems |

| Solar Array & Power Hardware |

| Structures, Harness & Mechanisms |

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

| Satellite Mass | 10-100kg |

| 100-500kg | |

| 500-1000kg | |

| Below 10 Kg | |

| above 1000kg | |

| Orbit Class | GEO |

| LEO | |

| MEO | |

| Satellite Subsystem | Propulsion Hardware and Propellant |

| Satellite Bus & Subsystems | |

| Solar Array & Power Hardware | |

| Structures, Harness & Mechanisms | |

| Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.