North America Protein Based Sports Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

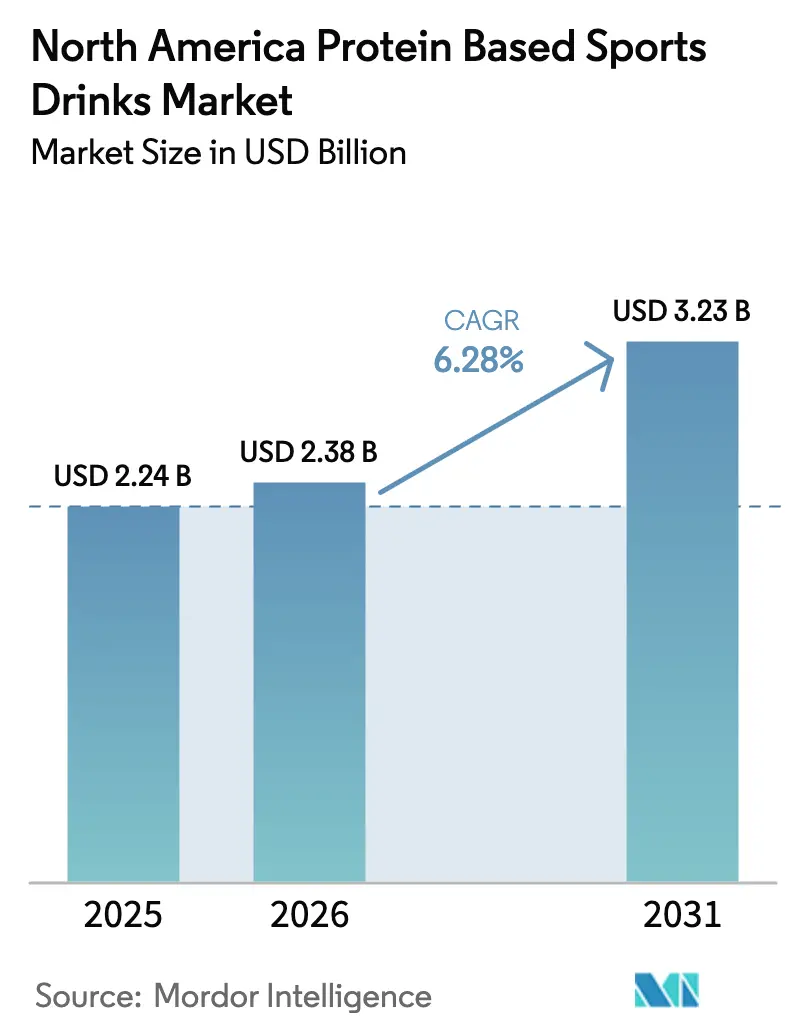

| Base Year Market Size (2025) | USD 2.24 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

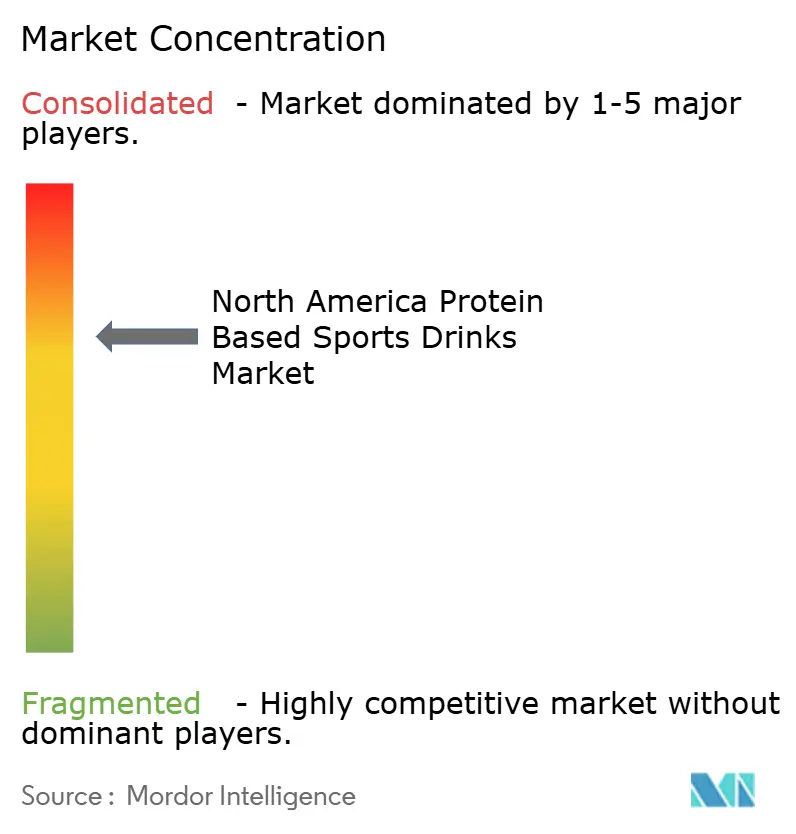

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Protein Based Sports Drinks Market Analysis by Mordor Intelligence

The North America Protein Based Sports Drinks market size in 2026 is estimated at USD 2.38 billion, growing from 2025 value of USD 2.24 billion with 2031 projections showing USD 3.23 billion, growing at 6.28% CAGR over 2026-2031. Momentum comes from consumers who want beverages that hydrate, preserve muscle, and deliver clean functional benefits in one convenient format. An expanding active-aging population, a jump in strength-training participation, and a preference for natural labels are fueling demand for high-protein, low-sugar drinks. Rapid product launches targeting users of GLP-1 weight-management medications, tighter rules on added sugars, and aluminum can adoption for recyclability are reshaping competitive playbooks. Ingredient cost volatility, whey protein isolate spot prices peaked in December 2024, and looming U.S. FDA reforms on artificial colorants pressure margins, prompting suppliers to lock long-term contracts and explore plant or precision-fermented proteins. Companies that balance sustainability claims, protein quality, and transparent labeling stand to secure lasting shelf space in retail and on-premise venues.

Key Report Takeaways

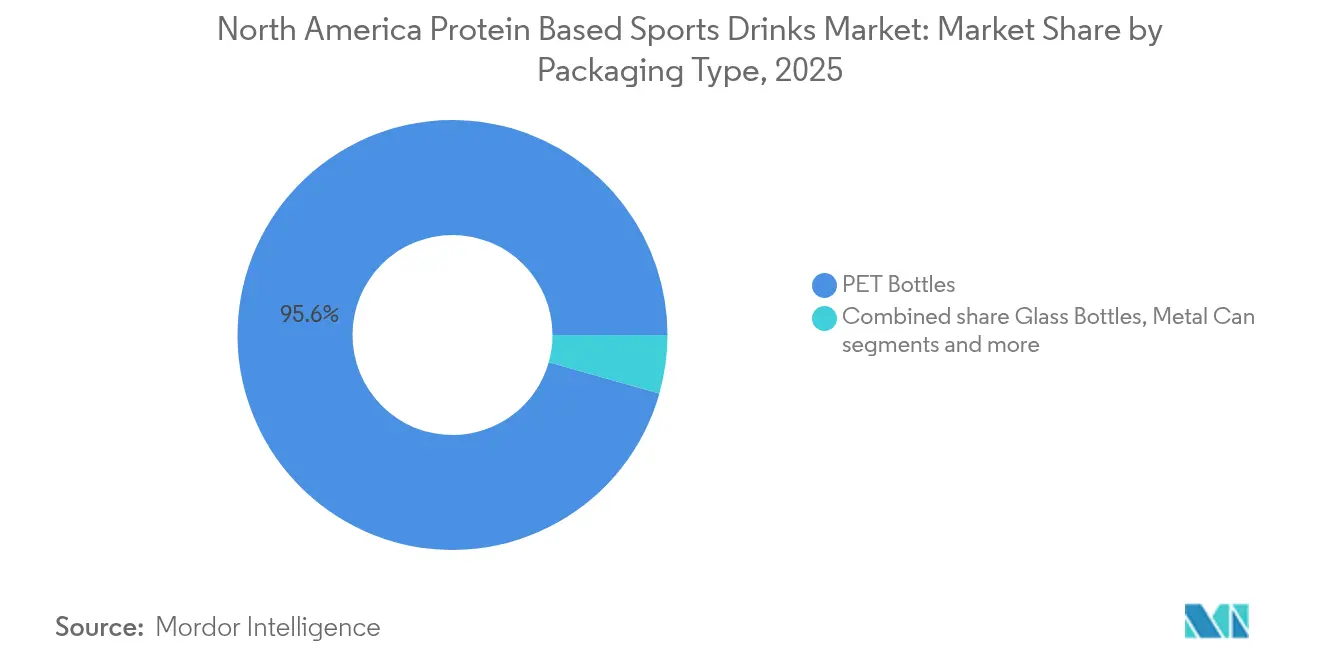

- By packaging type, PET bottles held 95.62% of 2025 revenue, while metal cans are projected to expand at 8.05% CAGR through 2031, the fastest among formats.

- By distribution channel, off-trade accounted for 63.88% of 2025 revenue; on-trade is poised to grow at a 7.62% CAGR to 2031.

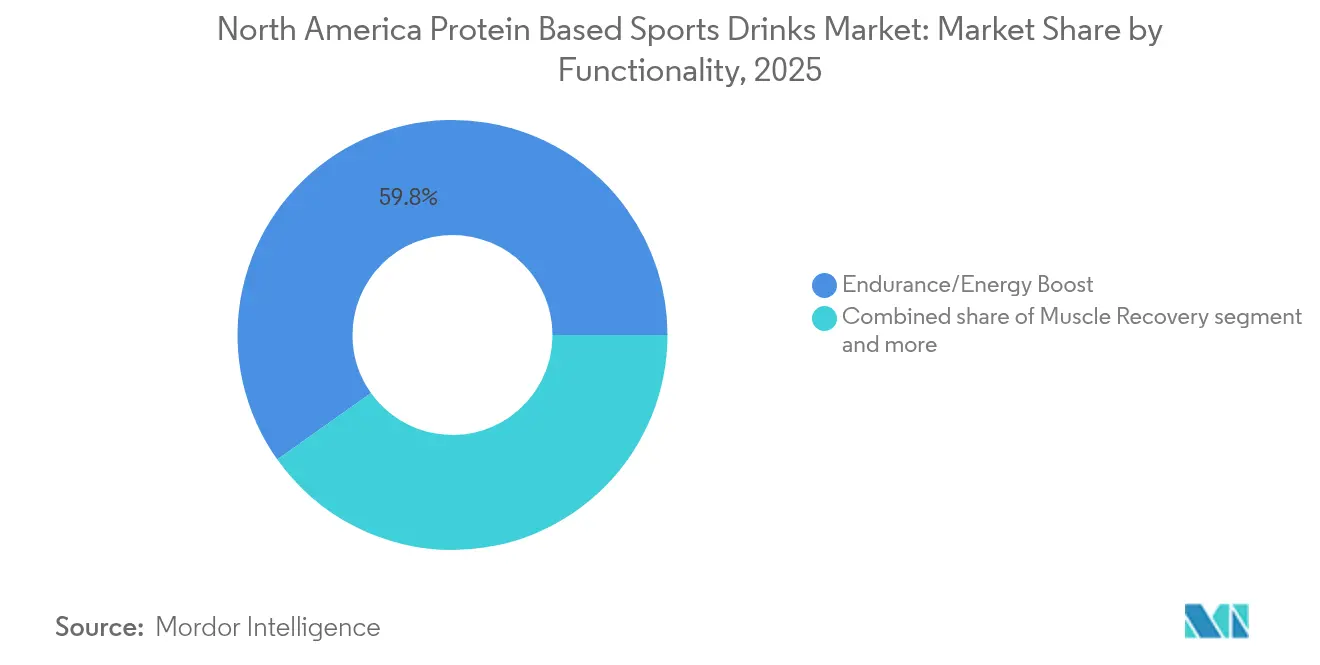

- By functionality, endurance and energy formulations captured 59.84% share of 2025 demand; muscle-recovery drinks are advancing at a 7.33% CAGR through 2031.

- By country, the United States contributed 90.72% of 2025 sales; Canada is forecast to grow at 7.92% CAGR, the fastest in the region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Protein Based Sports Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing health consciousness among consumers | +1.2% | Regional, strongest in United States urban centers | Medium term (2-4 years) |

| Rising participation in fitness activities and sports | +1.0% | North America, led by United States and Canada | Short term (≤ 2 years) |

| Innovation in natural and clean-label product formulations | +0.9% | United States and Canada, spillover to Mexico | Medium term (2-4 years) |

| Expansion of ready-to-drink convenience formats | +0.8% | North America, emphasis on on-trade channels | Short term (≤ 2 years) |

| Strategic partnerships with sports teams and fitness centers | +0.6% | United States major metro areas, Canada emerging | Medium term (2-4 years) |

| Product premiumization with enhanced functional benefits | +0.7% | United States and Canada high-income segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing health consciousness among consumers

Rising health consciousness among consumers is driving demand for protein-based sports drinks, as wellness priorities increasingly focus on convenient, nutrient-rich options that support active lifestyles and nutritional goals. Protein is being prioritized for its benefits in muscle recovery, sustained energy, and overall vitality, aligning with the broader trend of integrating fitness into daily routines. This has heightened the need for post-workout hydration solutions that provide functional benefits beyond electrolytes, such as satiety and performance enhancement. The growing adoption of gym memberships and home fitness, coupled with increased awareness of balanced macronutrients, is encouraging consumers to seek beverages that aid recovery without added sugars, offering a seamless, on-the-go solution to meet dietary needs. Additionally, the preference for clean-label formulations is gaining traction, with transparency in sourcing, such as grass-fed whey or plant-based protein isolates, fostering trust and aligning with values of sustainability and ethical consumption. These factors are contributing to market growth, as evidenced by Cargill’s 2025 Protein Profile, which reports that 61% of American consumers increased their protein intake in 2024, up from 48% in 2019 [1]Source: Cargill, Incorporated, "Consumers are Seeking More Protein for Health and Taste in 2025", cargill.com. This trend underscores the growing importance of protein in health and correlates with the segment's expansion. Sustained protein consumption is driving innovation in ready-to-drink formats designed for diverse activity levels, with demand for versatile serving sizes, such as single-serve bottles and multi-packs, reflecting the adaptability of modern routines. Product formulations are also evolving to include functional ingredients like adaptogens and electrolytes, enhancing recovery and ensuring long-term vitality without compromising on taste or portability.

Rising participation in fitness activities and sports

The increasing engagement in fitness activities and sports is driving the demand for protein-based sports drinks, as individuals prioritize solutions that support muscle repair and efficient rehydration. These beverages cater to the needs of both casual and competitive participants by providing immediate amino acid availability post-workout, facilitating recovery, and accommodating higher training frequencies. This demand is further fueled by the rise in longer workout durations and higher intensity levels across activities such as boutique fitness classes, outdoor running, and team sports. Ready-to-drink options that combine complete protein profiles with electrolytes are gaining traction due to their convenience and effectiveness in combating fatigue and promoting lean muscle retention without the need for mixing powders. Data from the Bureau of Labor Statistics indicates that approximately 21.5% of Americans participated in sports, exercise, and recreational activities daily in 2024, reflecting a growing consumer base seeking functional hydration solutions aligned with their physical output and recovery requirements [2]Source: Bureau of Labor Statistics, "American Time Use Survey - 2023 Results", bls.gov . Additionally, there is a rising preference for great-tasting, low-sugar formulations that encourage consistent consumption across various activities, including morning yoga, lunchtime pickleball, and evening league matches. Brands such as Performance Inspired Nutrition are addressing this demand with products like their Ready 2Go Protein Drink line, offering 16 grams of protein in flavors such as Blueberry Lemonade and Watermelon Blast, appealing to both high-volume athletes and recreational users. The expansion of community-based sports leagues, virtual fitness challenges, and wearable-tracked fitness goals further underscores the role of protein-based sports drinks as essential recovery tools, seamlessly integrating into the routines of an increasingly active population focused on performance enhancement and sustained energy throughout the day.

Innovation in natural and clean-label product formulations

Innovation in natural and clean-label product formulations is driving growth in the protein-based sports drinks market by emphasizing minimally processed ingredients that deliver high-quality protein without artificial additives. This approach addresses consumer demand for transparency and trust in post-workout recovery options while aligning with the increasing preference for plant-based and dairy-derived protein isolates sourced from non-GMO, hormone-free origins. These formulations retain functional benefits, such as rapid absorption, while eliminating synthetic flavors, colors, and preservatives that previously dominated the category. The rising popularity of clean-label claims bridges the gap between performance efficacy and wellness alignment, with brands incorporating natural sweeteners like monk fruit and stevia to support sustained energy with a low glycemic impact, meeting consumer expectations for purity in hydration products. According to Ingredion Incorporated, 38% of all new food and beverage launches in the United States and Canada in 2024 carried clean-label claims, compared to a global figure of 30%, underscoring how this trend is driving mainstream acceptance of protein-based sports drinks among health-conscious consumers [3]Source: Ingredion Incorporated, "Clean Label Ingredients: From Buzzword to Business Driver", ingredion.com . Product advancements also focus on enhancing attributes such as mouthfeel and solubility through natural emulsifiers, ensuring a smooth, clump-free experience that elevates consumption from a functional necessity to an enjoyable routine. Additionally, sustainable sourcing practices, including the use of upcycled proteins and regenerative agriculture, strengthen brand loyalty by aligning product innovation with environmental values, while simplified labeling fosters repeat purchases by appealing to consumers seeking recognizable and pronounceable ingredients. The clean-label movement not only differentiates products in a competitive market but also supports market growth by positioning protein-based sports drinks as versatile, everyday staples that cater to both physical performance and conscious consumption.

Strategic partnerships with sports teams and fitness centers for brand visibility

Strategic partnerships with sports teams and fitness centers are driving significant growth in the protein-based sports drinks market by placing products directly at key recovery points, where immediate post-exercise needs are most pronounced, and peer influence fosters trial and loyalty. These collaborations create authentic connections between brands and athletic performance, turning gym coolers, team sidelines, and locker-room fridges into high-impact sampling locations that position the drink as an essential recovery solution for athletes across all levels. By securing exclusive pouring rights or co-branded recovery stations, companies achieve sustained visibility during peak consumption moments, seamlessly linking the act of refueling with the brand’s identity for gym-goers and competitive players. Additionally, these partnerships enable tailored activations, such as on-site hydration clinics and branded recovery lounges, which deepen consumer engagement while providing partners with premium, athlete-endorsed options that enhance their member or fan experience. This cycle of visibility strengthens as participants consistently choose the familiar product endorsed by trusted coaches, teammates, or favorite teams, transforming initial exposure into habitual preference. For instance, Gatorade has leveraged long-term collaborations with major leagues and university athletic programs through its Gatorade Sports Science Institute, ensuring its protein-recovery products remain the default choice in professional training facilities and collegiate weight rooms. These alliances also amplify social proof through athlete endorsements and event branding, creating a positive association that extends into retail and e-commerce channels, where consumers actively seek the same products used by admired athletes. By embedding themselves into the daily training routines of athletes, brands convert passive awareness into active advocacy, driving trial, repeat purchases, and market share growth in a category where credibility and convenience are critical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus traditional isotonic drinks | -0.8% | United States and Canada price-sensitive segments | Short term (≤ 2 years) |

| Regulatory pressure on sugar and HFSS products | -0.5% | Mexico (COFEPRIS), Canada (Health Canada) | Medium term (2-4 years) |

| Product substitution by alternative protein sources like powders and bars | -0.6% | North America, strongest in fitness enthusiasts | Medium term (2-4 years) |

| Supply chain disruptions impacting ingredient availability | -0.4% | United States and Canada whey protein supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory pressure on sugar and HFSS products

Regulatory scrutiny on sugar and high-fat, salt, and sugar (HFSS) products is exerting significant pressure on manufacturers, requiring them to reduce or eliminate added sugars while maintaining taste profiles that meet consumer expectations, particularly for post-workout consumption. Measures such as front-of-pack warning labels, potential taxation, and stricter marketing restrictions targeting minors challenge traditional formulations that have historically relied on sugar for energy and flavor masking. This has led to complex reformulation processes, increasing research and development costs, and risking consumer dissatisfaction if taste expectations are not met. The demand for lower glycemic impact, closely tied to clean-label trends, further narrows sweetener options to alternatives like allulose or monk fruit, which are more expensive and less effective at masking protein off-notes, thereby raising production costs across the supply chain. Additionally, regulatory differences between the United States and Canada create formulation fragmentation, complicating cross-border product launches and forcing companies to either maintain multiple SKUs or adhere to the strictest common standard, further straining margins in a price-sensitive market. For example, brands like Premier Protein, offering 30g of protein and only 1g of sugar, face ongoing reformulation pressures to comply with evolving guidelines and avoid penalties in retail channels adopting HFSS restrictions. Increased scrutiny on total carbohydrate declarations also limits the inclusion of functional carbohydrates essential for glycogen replenishment, creating a delicate balance between recovery efficacy and regulatory compliance. Smaller companies with limited reformulation budgets struggle to compete, consolidating advantages for larger players while slowing innovation and occasionally causing temporary product shortages. Although these pressures drive the shift toward zero- and low-sugar offerings aligned with consumer health goals, they impose significant operational challenges, tempering short-term growth in an otherwise expanding market.

Product substitution by alternative protein sources like powders and bars

The increasing preference for alternative protein sources, such as powders and bars, presents a significant challenge to the growth of ready-to-drink (RTD) protein-based sports beverages. Many consumers are drawn to these alternatives due to their cost-effectiveness, customizable dosing, and portion control, which often outweigh the convenience offered by RTD options. Protein powders, which provide higher protein content per dollar and the flexibility to mix with preferred liquids or ingredients, are particularly competitive during planned meal preparation routines. Similarly, protein bars offer grab-and-go convenience, directly competing with the on-the-go recovery positioning of bottled shakes. This trend is further amplified when RTD beverages are perceived as overpriced per gram of protein, prompting budget-conscious gym-goers and endurance athletes to reserve liquid formats for immediate post-workout recovery while relying on powders or bars for daily nutritional needs. The rise of home blending, supported by high-powered blenders and personalized nutrition apps, further erodes the market share of pre-mixed drinks by enabling consumers to replicate the taste and texture of RTD beverages at a fraction of the cost. Brands like Optimum Nutrition illustrate this competitive pressure with their Gold Standard whey line and protein bar offerings, which deliver 24–30g protein servings and appeal to travelers, office workers, and students due to their portability and lack of refrigeration requirements. Additionally, the bulk purchasing model associated with powders fosters consumer loyalty through lower unit costs, reducing impulse purchases of single-serve RTD bottles at gyms and convenience stores. Consequently, RTD manufacturers face compressed margins and slower volume growth, necessitating continuous innovation in taste, packaging, and functional differentiation to remain competitive against these economical and versatile alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Metal Cans Capture Sustainability Premium

Although PET bottles hold a commanding 95.62% share of the 2025 market, metal cans are set to grow at the fastest rate among packaging formats, with a projected 8.05% CAGR from 2026 to 2031. This growth reflects a sustainability-driven shift, as aluminum's 90% recycling rate in North America and its lower carbon footprint, especially when powered by renewable energy, appeal to environmentally conscious consumers willing to pay a premium for circular solutions. Ball Corporation's lifecycle assessment, conducted by Sphera, revealed that aluminum cans have the highest recycled content and recycling rates among single-use beverage containers in North America. Brands are leveraging this data in their marketing efforts to justify higher per-unit costs. PET bottles maintain their dominance due to well-established supply chains, lighter weight that reduces shipping costs, and strong consumer familiarity. However, the format faces challenges from extended producer responsibility legislation in states like California, Oregon, and Maine, which impose recycling fees on non-recycled content, thereby narrowing the cost gap with aluminum.

Glass bottles and aseptic packages, including Tetra Pak, cartons, and pouches, occupy niche segments. Glass appeals to premium craft brands seeking shelf differentiation, while aseptic formats enable ambient distribution, cutting cold-chain costs. For example, Flow Beverage's January 2024 manufacturing agreement with BioSteel resulted in the delivery of 12 million zero-sugar Tetra Pak units within four months, showcasing aseptic packaging's ability to secure placements in convenience stores and vending machines without refrigeration. Disposable cups, which account for less than 1% of the packaging market, are gaining traction. Primarily used in on-premise foodservice and automated dispensing machines, their growth is driven by the proliferation of iShaker-style vending machines in gyms and corporate wellness centers. These machines offer over 130 drink combinations from just four 41-kilogram powder containers. Regulatory influence on packaging choices remains minimal beyond recycling mandates, though COFEPRIS in Mexico requires Spanish-language labeling on all formats, adding compliance costs for cross-border distribution.

By Distribution Channel: On-Trade Venues Monetize Fitness Partnerships

On-trade channels, including gyms, sports facilities, corporate cafeterias, and vending machines, are leveraging fitness partnerships to convert captive audiences into loyal repeat purchasers. This approach is driving a projected 7.62% CAGR from 2026 to 2031, surpassing the off-trade segment's dominant 63.88% share in 2025. By embedding products directly into high-engagement environments where recovery needs peak, brands capitalize on post-workout impulses. This strategy allows them to bypass traditional retailer slotting fees and secure premium visibility through co-branded installations tailored to active lifestyles. By integrating into daily training flows, whether through arena coolers for spectators or gym dispensers for members, these venues transform transient visitors into habitual consumers, fostering brand affinity that extends beyond the facility into personal routines. Body Armor's April 2024 NHL partnership exemplifies this monetization, strategically placing branded coolers and bottles across all 32 arenas to span 1,312 regular-season games and generate 60 million viewer impressions, thereby amplifying on-trade reach while associating the protein-infused lineup with elite athletic performance.

This venue-centric approach further evolves with automated solutions like iShaker's countertop units, which streamline protein shake delivery by accepting contactless payments and syncing with fitness memberships to enable seamless, round-the-clock access without operational burdens on facility staff. These dispensers not only mitigate inventory risks for gyms and cafeterias but also generate estimated USD 500 to USD 1,000 per machine monthly in bustling spots, directly tying revenue streams to foot traffic and membership data for personalized upsell opportunities. As such innovations proliferate, they reinforce the on-trade channel's agility in responding to fitness trends, ensuring protein-based sports drinks become indispensable extensions of workout ecosystems rather than mere add-ons. Ultimately, this interconnected monetization model propels category expansion by aligning distribution with consumer proximity, turning every session or event into a branded recovery touchpoint that sustains long-term engagement and volume growth.

By Functionality: Muscle Recovery Formulations Leverage BCAA Science

Muscle recovery formulations are projected to achieve a CAGR of 7.33% from 2026 to 2031, driven by peer-reviewed evidence supporting GLP-1-related muscle preservation. Endurance and energy boost applications accounted for a dominant 59.84% share of the market in 2025. A 2024 study published in Nutrients demonstrated that a BCAA-containing electrolyte beverage with 220 milligrams of BCAAs per 100 milliliters reduced muscle damage markers by 18% and improved hydration status compared to water alone. These findings provide clinical validation for recovery claims, enabling premium pricing. Vita Coco's PWR LIFT protein-infused water combines coconut water electrolytes with BCAAs and zero sugar, strategically positioning the product at the intersection of hydration and recovery. This dual functionality appeals to consumers seeking multi-benefit beverages. Ascent Protein's June 2024 launch of Clean Hydration + Energy, featuring 400 milligrams of electrolytes, 100 milligrams of caffeine, and 2 grams of sugar, targets pre-workout consumption while maintaining Informed Choice Certification, a third-party verification valued by competitive athletes concerned about banned substances.

Endurance and energy boost applications maintain market leadership due to their established positioning in sports nutrition and alignment with fitness trends. According to ACSM's 2025 survey, high-intensity interval training ranked as the sixth most popular fitness activity, driving demand for beverages that support sustained physical effort. The "Others" functionality segment, which includes meal replacement, weight management, and general wellness, is expanding as GLP-1 users increasingly seek protein beverages to prevent muscle loss. Clinical guidelines recommend 1.2 grams of protein per kilogram of body weight to reduce fat-free mass loss by 45%. Regulatory oversight remains focused on claim substantiation. The FDA's December 2024 update to "healthy" nutrient content claims requires foods to deliver meaningful protein content while limiting added sugars, prompting manufacturers to prioritize higher protein density and natural sweeteners in their formulations.

Geography Analysis

In 2025, the United States holds a dominant 90.72% share of the regional protein-based sports drinks market. This leadership is supported by a well-established sports nutrition culture and a robust retail network that ensures ready-to-drink sports protein products are widely available, from major gyms to convenience stores. This market maturity drives a cycle where strong consumer familiarity fosters continuous innovation and dedicated shelf space, solidifying these beverages as everyday essentials rather than niche supplements.

Canada is positioned as the region’s growth leader, with a projected 7.92% CAGR from 2026 to 2031. Growth is driven by clearer regulatory frameworks that promote transparent labeling and a thriving plant-based protein sector. This sector is rapidly advancing, creating hybrid dairy-plant formulations that appeal to flexitarian athletes. Brands such as Protein2o and Performance Inspired Nutrition - Ready 2Go are driving this trend by introducing clean, high-protein ready-to-drink shakes. These brands leverage Canada’s progressive stance on health claims, enabling faster market penetration compared to the more saturated United States market.

Mexico and other parts of the region present long-term growth opportunities, supported by a young, increasingly urban population embracing fitness and wellness trends. However, the premium protein-based sports drinks segment faces significant short-term challenges. Fragmented cold-chain infrastructure limits the reliable distribution of chilled products, restricting availability outside major urban centers. Additionally, lower disposable incomes reduce consumers’ willingness to pay premium prices for imported or specialized high-protein beverages, with traditional, cost-effective hydration options dominating shelves. These challenges hinder market penetration and brand-building efforts, keeping activity concentrated in the mature United States-Canada corridor. Consequently, multinational companies prioritize investments in these established markets, delaying significant expansion in Mexico and smaller regional markets despite their future potential.

Competitive Landscape

The protein-based sports drinks market in North America is moderately concentrated. Industry leaders such as PepsiCo, Nestlé, and Abbott capitalize on their extensive distribution networks and decades of brand equity to secure prime shelf placements across mass retail, convenience, and club channels. Their robust cold-chain infrastructure and long-standing retailer partnerships create significant entry barriers. This competitive edge enables them to rapidly scale new protein-infused product launches and cross-promote within their broader beverage portfolios. Such entrenched operations dominate cooler doors and checkout lanes, making it difficult for smaller competitors to achieve comparable growth without substantial trade investments.

Conversely, emerging players like BioSteel, Protein20, and Vita Coco are gaining traction by leveraging formulation agility and direct-to-consumer strategies that bypass traditional distribution channels. These nimble brands respond swiftly to evolving trends, such as zero-sugar options, hydration-plus-protein blends, or electrolyte-enhanced recovery shakes, often outpacing the slower innovation cycles of larger corporations hindered by bureaucratic processes. By fostering loyal consumer communities through social media, subscription models, and athlete endorsements, they transform early adopters into vocal advocates, amplifying their market presence organically.

This competitive dynamic between established leaders and agile disruptors creates a balanced tension. While the incumbents dominate in volume and visibility, challengers steadily capture premium and functional market segments. This forces brands like Gatorade (PepsiCo), Unwell Hydration (Nestlé), and Ensure Max Protein (Abbott) to continuously innovate their portfolios to retain market share in high-margin, high-growth categories. Ultimately, this competition drives accelerated product development, benefiting consumers while reinforcing the critical role of scale and speed in achieving long-term success in the market.

North America Protein Based Sports Drinks Industry Leaders

-

PepsiCo, Inc.

-

Nestlé S.A.

-

Abbott Laboratories

-

Protein20 Inc.

-

Premier Nutrition Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Unwell Hydration, a functional beverage brand from the United States, announced the launch of its newest product: Unwell Hydration with Protein. This product combined the brand's renowned electrolyte blend with whey isolate protein, positioning itself as a lighter, more refreshing alternative to conventional protein shakes. Each serving of Unwell Hydration with Protein featured 10g of protein, 60kcal, and just 2g of sugar. Additionally, it included 740mg of electrolytes and three vital B vitamins, targeting consumers seeking to refuel after workouts and achieve their protein goals while on the move.

- April 2025: Protein2o, a prominent player in the clear protein drink industry, announced its nationwide retail expansion through 1,400 Target stores, strengthening its position in the ready-to-drink (RTD) protein beverage market. Target carried Protein2o’s recently reformulated line of clear protein drinks, designed to support consumers seeking to boost their daily protein intake while staying hydrated, all without preservatives. Alongside popular flavors such as Strawberry Watermelon and Orange Mango, Target exclusively offered 4-packs of Protein2o’s newest flavor, Lemon-Lime.

- January 2025: Protein2o, a prominent clear protein brand in the United States, announced its first rebrand in eight years, featuring updated packaging and an enhanced formula, which was set to launch in January. To support this initiative, Protein2o introduced a new marketing campaign and website focused on its core positioning around protein and hydration. The redesigned packaging, developed by Safari Sundays, featured a prominent "P" logo, vibrant fruit flavor imagery, and graphics emphasizing hydration and fitness themes.

North America Protein Based Sports Drinks Market Report Scope

The North America Protein Based Sports Drinks Market Report is Segmented by Packaging Type (PET Bottles, Glass Bottles, Metal Can, Aseptic Packages, and Disposable Cups), Distribution Channel (On-Trade, Off-Trade), Functionality (Endurance/Energy Boost, and More), and Geography (United States, Canada, Mexico, and Rest of North America). Market Forecasts are Provided in Terms of Value (USD).

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic Packages (tetra pak, cartons, pouches) |

| Disposable Cups |

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail | |

| Other Distribution Channels |

| Endurance/Energy Boost |

| Muscle Recovery |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic Packages (tetra pak, cartons, pouches) | ||

| Disposable Cups | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Functionality | Endurance/Energy Boost | |

| Muscle Recovery | ||

| Others | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms