Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

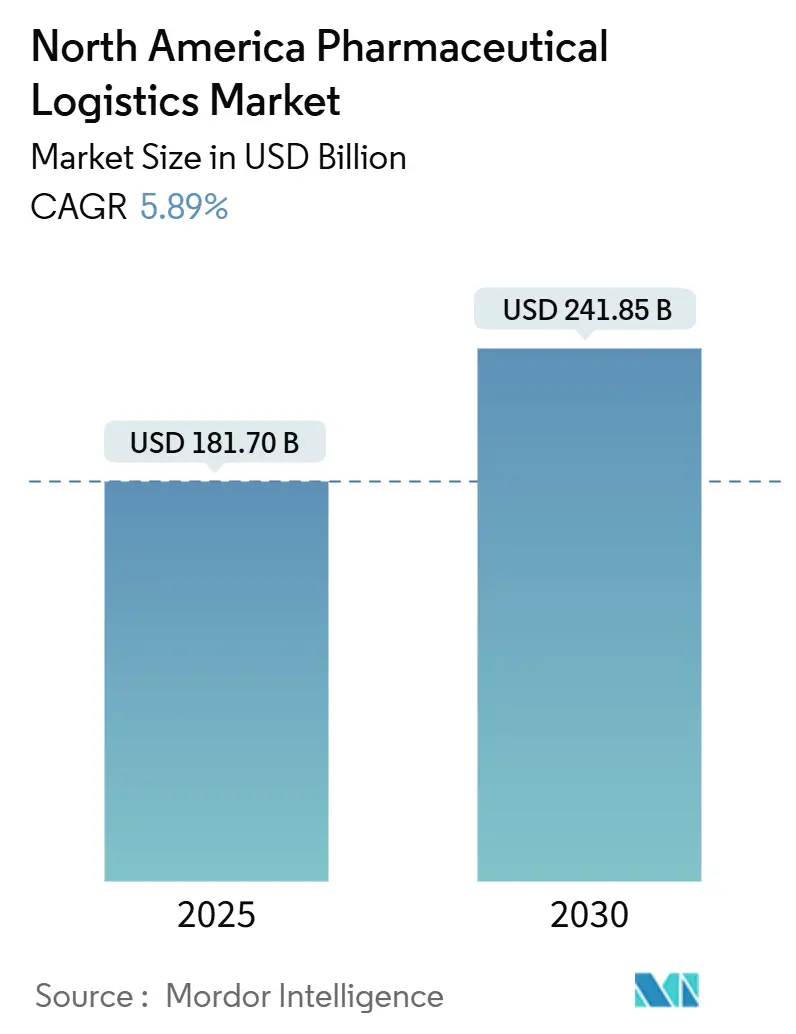

| Market Size (2025) | USD 181.70 Billion |

| Market Size (2030) | USD 241.85 Billion |

| Growth Rate (2025 - 2030) | 5.89% CAGR |

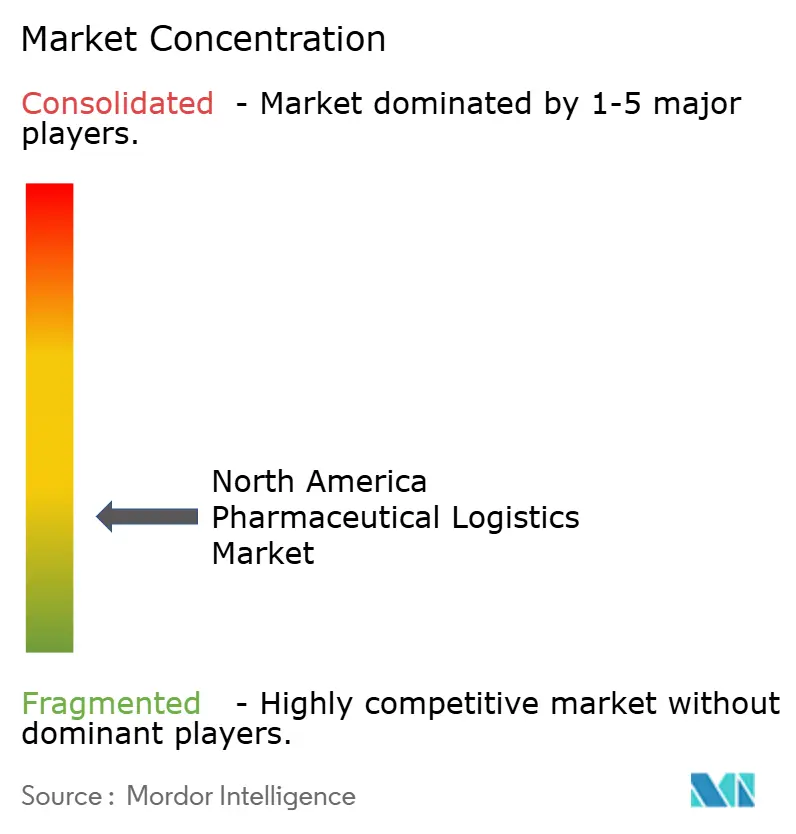

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The North America Pharmaceutical Logistics Market size is estimated at USD 181.70 billion in 2025, and is expected to reach USD 241.85 billion by 2030, at a CAGR of 5.89% during the forecast period (2025-2030).

Growth is anchored in the region’s large drug manufacturing base, strict compliance environment and rapid adoption of digital supply-chain technologies, all of which demand reliable temperature-controlled transport and granular traceability. Momentum is further reinforced by a surge in cell and gene therapy trials that require ultra-cold networks, rising direct-to-patient distribution in the specialty pharmacy channel and near-shoring of fill-finish capacity to Mexico. Capital expenditure remains strong, with DHL alone committing USD 2.2 billion to healthcare logistics through 2030, half of it in North America, to scale purpose-built hubs, vehicle fleets and control-tower systems[1]DHL Group, “DHL to Invest EUR 2 Billion in Global Healthcare Logistics,” dhl.com. Competitive intensity is escalating as integrators, specialist 3PLs and IoT-enabled start-ups vie for opportunities in biologics, last-mile and cross-border corridors, keeping market concentration moderate.

Key Report Takeaways

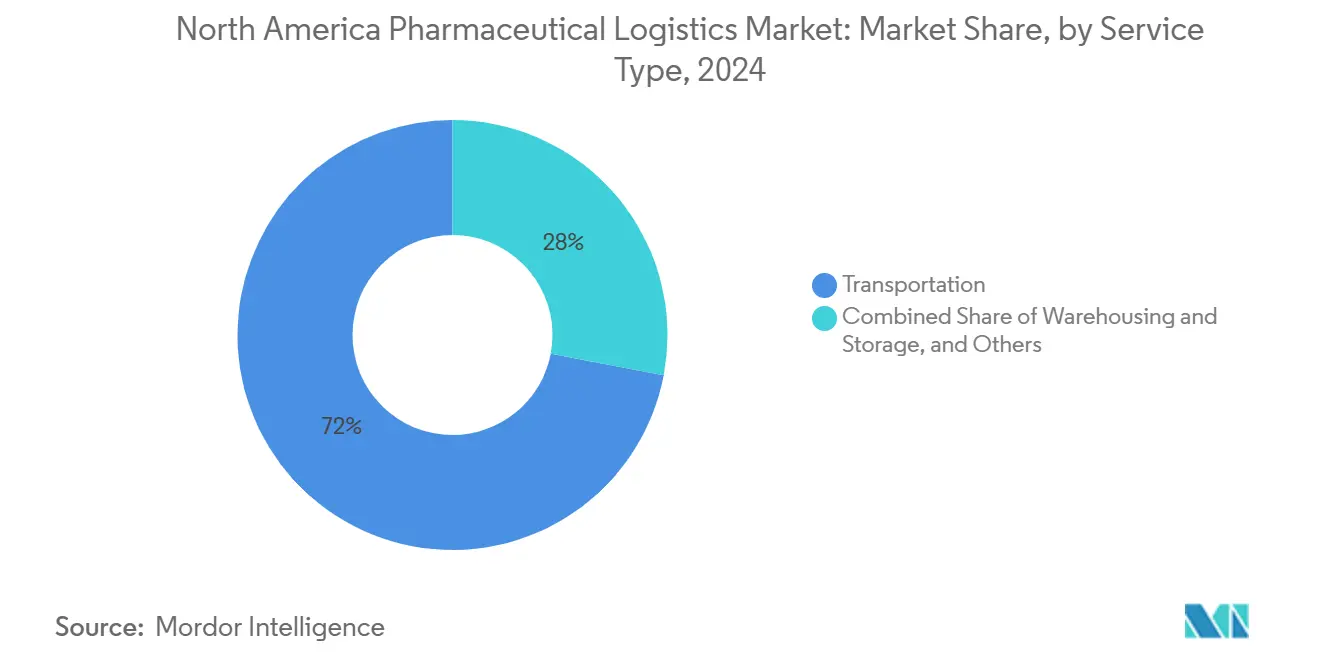

- By service type, transportation captured 72% of the North America pharmaceutical logistics market share in 2024, whereas warehousing and storage is projected to log the fastest 6.5% CAGR through 2030.

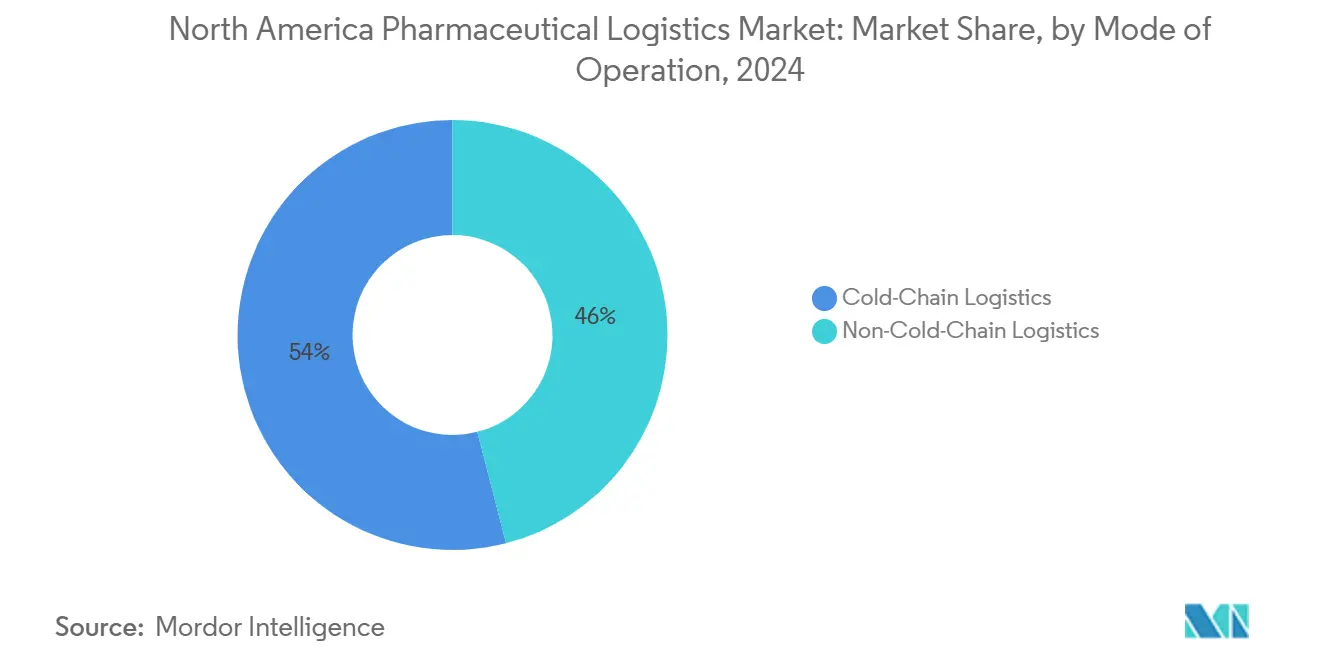

- By mode of operation, non-cold-chain services accounted for a 54% share, while cold-chain services are set to expand at 7.2% CAGR to 2030.

- By product type, prescription drugs led with 38.2% revenue share in 2024; cell and gene therapies are forecast to rise at an 11.6% CAGR through 2030.

- By geography, the United States held an 82% share of the North America pharmaceutical logistics market size in 2024, while Mexico is poised for the fastest 8.1% CAGR to 2030.

North America Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cell & gene therapy clinical trials requiring ultra-cold distribution infrastructure | +1.8% | United States & Canada with spill-over to Mexico | Medium term (2-4 years) |

| Rise of direct-to-patient models in U.S. specialty pharmacy channel | +1.2% | United States, expanding to Canada | Short term (≤ 2 years) |

| Expansion of U.S.–Mexico near-shore fill-finish facilities creating cross-border cold-chain flows | +0.9% | U.S.–Mexico border regions, extending to Canada | Long term (≥ 4 years) |

| Canada’s biologics manufacturing incentives boosting demand for GMP warehousing | +0.7% | Canada, with U.S. cross-border implications | Medium term (2-4 years) |

| Growing adoption of real-time IoT temperature monitoring mandated by U.S. DSCSA 2024 milestone | +0.6% | North America-wide, led by United States | Short term (≤ 2 years) |

| Sustainability push for re-usable passive shippers to slash air-freight carbon footprint | +0.4% | Global, with North America leading | Long term (≥ 4 years) |

Source: Mordor Intelligence

Surge in Cell & Gene Therapy Clinical Trials Requiring Ultra-Cold Distribution Infrastructure

Advanced therapy trials are scaling rapidly, prompting investment in storage solutions that keep cellular material stable at temperatures as low as -196 °C. OmniaBio’s 120,000 square-foot facility in Hamilton, Ontario, now the largest of its kind in Canada, signals growing regional capacity for these therapies. The U.S. FDA’s new Platform Technology Designation for CRISPR-based products simplifies validation steps and shortens review cycles, thus raising shipment volumes that must meet stringent chain-of-custody rules. Logistics providers able to offer validated cryogenic fleets, redundant power back-ups and real-time excursion alerts are well placed to win contracts. Partnerships between manufacturers and 3PLs are also expanding to embed capacity in multi-tenant campuses near research clusters. These dynamics elevate the North America pharmaceutical logistics market as a critical enabler of precision medicine scale-up.

Rise of Direct-to-Patient Models in U.S. Specialty Pharmacy Channel

Manufacturers are building proprietary portals that send high-value drugs directly to patient homes, trimming intermediaries and improving adherence. The direct-to-patient healthcare logistics segment is growing alongside telehealth, which handled over 18% of U.S. outpatient visits in 2024. Last-mile couriers equipped with temperature-verified packaging extend reach to rural areas while blockchain audit trails document custody events for DSCSA compliance. Retail chains are retrofitting clinics to support decentralized clinical trials that rely on just-in-time drug delivery. Automated micro-fulfilment centers near metropolitan zones shorten lead times further. As these practices mature they contribute to recurring revenue streams within the North America pharmaceutical logistics market.

Expansion of U.S.–Mexico Near-Shore Fill-Finish Facilities Creating Cross-Border Cold-Chain Flows

Life-science companies are diversifying supply risk by moving sterile fill-finish lines to northern Mexico. The country’s 14 free-trade agreements and new tax rules that allow 89% deductibility on research machinery lower capital barriers. Cross-border truck volumes of temperature-sensitive goods are rising, though congested ports of entry and fragmented Mexican cold-chain regulations can delay hand-offs. The Wilson Center urges stronger regulatory alignment to safeguard product efficacy and patient safety. Demand for bilingual control-tower services and GPS-tagged passive shippers is therefore escalating. Providers that master customs brokerage, redundant route planning and harmonised data standards are likely to capture incremental share in the North America pharmaceutical logistics market.

Canada’s Biologics Manufacturing Incentives Boosting Demand for GMP Warehousing

Federal and provincial programs are subsidising new biomanufacturing campuses, accelerating the need for certified storage and distribution nodes. Canada’s diverse electronic health-record ecosystem improves real-world evidence capture, attracting multinational trials that require qualified logistics partners. Ottawa’s national pharmacare proposal envisions a single agency to negotiate drug prices and coordinate distribution, which may centralise requirements for temperature-controlled depots. Cross-border flows of biologics into U.S. clinical networks also benefit from the USMCA framework. These initiatives raise warehouse utilisation rates and spur robotics adoption, reinforcing growth prospects for the North America pharmaceutical logistics market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic driver shortages limiting domestic road capacity for time-critical shipments | -1.4% | North America, most acute in United States | Medium term (2-4 years) |

| High cost of dry-ice & liquid-nitrogen compliance for ≤-70 °C modalities | -0.8% | Global, concentrated in North America | Long term (≥ 4 years) |

| Fragmented Mexican Cold-Chain Regulations Elevating In-Transit Risk | -0.6% | U.S.-Mexico border regions, extending to Canada | Medium term (2-4 years) |

| Border Congestion Impacting On-Time Performance of Cross-Border Truckloads | -0.5% | U.S.-Mexico and U.S.-Canada border crossings | Short term (≤ 2 years) |

Source: Mordor Intelligence

Chronic Driver Shortages Limiting Domestic Road Capacity for Time-Critical Shipments

The American Trucking Associations estimate the shortfall could reach 160,000 drivers by 2030, straining time-definite lanes for healthcare cargo. Manufacturing plants already cite labour gaps at 20.6%, and higher transportation prices in December 2024 marked the steepest rise since April 2022. Driver turnover erodes on-time performance, pushing shippers to use premium air options or build buffer inventories. Potential immigration restrictions could tighten labour pools further. These pressures inflate operating costs and temper the otherwise strong outlook for the North America pharmaceutical logistics market.

High Cost of Dry-Ice & Liquid-Nitrogen Compliance for ≤-70 °C Modalities

Complex handling protocols for ultra-cold cargo raise insurance, packaging and training expenses. Failures across the global cold chain already cost industry USD 35 billion each year, highlighting financial risk. Maersk estimates that cold-chain medicines comprised 35% of total pharmaceutical volumes in 2022, and the share is climbing with next-generation biologics. Dry-ice sublimation plus limits on aircraft cargo mass can force split shipments, doubling freight bills. While IoT telemetry curbs excursion loss, it cannot fully offset high material costs, moderating the growth rate of modalities that rely on extreme temperatures within the North America pharmaceutical logistics market.

Segment Analysis

By Service Type: Transportation Dominates Despite Warehousing Acceleration

Transportation captured 72% of the North America pharmaceutical logistics market share in 2024, reflecting the centrality of air, road and multimodal services for timely deliveries across a vast region. Domestic truck routes connect more than USD 1.6 trillion in U.S.-Canada-Mexico trade, while Boeing forecasts 4.1% annual expansion in air-cargo traffic driven by e-commerce and high-value goods, including medicines[2]U.S. Bureau of Transportation Statistics, “U.S. International Freight Flows 2024,” bts.gov.

Warehousing and storage, though smaller, is set to grow at.5 6% CAGR as manufacturers create inventory buffers for critical drugs and as advanced therapies demand controlled environments. Robotic picking systems and automated cold rooms shorten order cycles and raise accuracy, while ISO-certified clean rooms support secondary packaging and kitting. Labour scarcity accelerates capital investment in automation, and value-added services such as late-stage customisation and regulatory support differentiate providers within the North America pharmaceutical logistics industry.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Operation: Cold-Chain Logistics Outpaces Traditional Models

Non-cold-chain services remain the larger category at 54% of the North America pharmaceutical logistics market size in 2024, serving most oral solids and medical devices. Cold-chain services are forecasted to expand 7.2% annually through 2030 as biologics, vaccines and advanced therapies proliferate.

Lineage Logistics and Americold operate 71% of regional cold-storage facilities, yet new entrants armed with sensor-enabled containers are challenging incumbents. Real-time monitoring improves successful deliveries to above 99% while reducing CO₂ output, enhancing competitiveness. Software that predicts lane-specific risk allows shippers to choose optimal modes, strengthening resilience in the North America pharmaceutical logistics market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Cell & Gene Therapies Drive Specialized Logistics Demand

Prescription medicines led with a 38.2% share of the North America pharmaceutical logistics market size in 2024. Over-the-counter products, biosimilars and vaccines follow as mature revenue sources that require strict yet standardised handling.

Cell and gene therapies, although nascent, are projected to post a 11.6% CAGR through 2030. Cryogenic storage at -196 °C, specialised courier escorts and point-of-care delivery models set this class apart. Regulatory agencies are piloting decentralised manufacturing to cut transit time, which could shift logistics from central hubs to regional nodes. Top animal-health firms such as Zoetis, Merck Animal Health and Boehringer Ingelheim also rely on livestock vaccine chains that mirror human vaccine requirements, adding diversity to the North America pharmaceutical logistics market.

Geography Analysis

The United States commanded 82% of North America pharmaceutical logistics market revenue in 2024, supported by large-scale drug manufacturing clusters, world-class compliance standards and heavy infrastructure spending. Multi-billion-dollar expansions by Eli Lilly, Johnson & Johnson and Amgen in North Carolina illustrate how new production hubs create parallel demand for validated storage and time-critical transportation. DSCSA milestones continue to catalyse technology adoption, with serialization and data-exchange solutions rolling out across wholesalers, dispensers and 3PLs.

Canada contributes a smaller but strategically important slice of the North America pharmaceutical logistics market. Government incentives for biologics plants, a rich real-world evidence ecosystem and the proposed national pharmacare program are harmonising demand for GMP-compliant depots[3]Health Canada, “Pharmacare at a Glance,” canada.ca . Cross-border exchanges under USMCA facilitate two-way flows of APIs and finished dose forms. Continued investment in cold-chain corridors through Ontario and Quebec will lift usage of specialised trucking lanes and air-freight charters.

Mexico is the fastest-growing geography, expected to rise 8.1% on a CAGR basis through 2030. Tax breaks on research and manufacturing equipment and proximity to U.S. buyers make near-shoring attractive. Yet power reliability, water scarcity and cargo security remain hurdles. Strengthened customs coordination and the 2026 USMCA review could further streamline trade, positioning Mexico as a vital node in the broader North America pharmaceutical logistics market.

Competitive Landscape

Market structure is moderately fragmented. Global integrators like DHL, UPS and FedEx scale dedicated healthcare units, while specialists such as CryoPDP and Marken focus on clinical and ultra-cold lanes. DHL’s USD 1.1 billion North American outlay covers new pharmaceutical hubs, temperature-controlled vehicles and digital control towers. UPS targets USD 20 billion in healthcare revenue by 2026 via purpose-built campuses and drone-enabled last-mile pilots.

Strategic M&A reshapes capabilities. DHL acquired CryoPDP to lock in end-to-end cell-and-gene coverage, while Novo Holdings’ USD 16.5 billion purchase of Catalent increases integrated supply options though it raised antitrust scrutiny. Technology is becoming a key differentiator. Warehouse robotics, AI-powered demand sensing and blockchain traceability improve visibility and cut errors, helping providers win DSCSA-driven bids.

White-space opportunities are visible in cross-border cold-chain routes, direct-to-patient fulfilment and sustainability-oriented packaging. Emerging players leverage IoT telemetry to promise excursion-free performance and lower carbon footprints, challenging incumbents and expanding service quality across the North America pharmaceutical logistics market.

North America Pharmaceutical Logistics Industry Leaders

-

DHL Supply Chain & Global Forwarding

-

UPS Healthcare

-

Kuehne + Nagel International AG

-

C.H. Robinson

-

FedEx Logistics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Eli Lilly announced a USD 27 billion plan to build four new U.S. production sites, creating 3,000 jobs and boosting injectable capacity.

- Feb 2025: U.S. administration imposed tariffs of 25% on most Mexican and Canadian imports and 10% on Chinese goods, increasing logistics costs in regional supply chains.

- January 2025: DHL Supply Chain agreed to acquire Inmar Supply Chain Solutions to widen pharmaceutical fulfilment capabilities.

- December 2024: Amgen confirmed a USD 1 billion addition to its North Carolina site, bringing total investment to USD 1.5 billion.

North America Pharmaceutical Logistics Market Report Scope

Pharmaceutical logistics entails the procedures and actions of the product acquisition, storage, inventory control, and transportation while ensuring consistency in medicine quality throughout inventory control and delivery.

The North American Pharmaceutical Logistics market is segmented by Product (Generic Drugs and Branded Drugs), Mode of Operation (Cold Chain Transport and Non-Cold Chain Transport), Application (Bio Pharma, Chemical Pharma, and Specialized Pharma), Mode of Transport (Air Shipping, Rail Shipping, Road Shipping, and Sea Shipping), and Geography (United States, Canada, and Mexico). The report offers the market size and forecasts in value (USD billion) for all the above segments.

| By Service Type | Transportation | Road Freight |

| Air Freight | ||

| Sea Freight | ||

| Rail Freight | ||

| Warehousing & Storage | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics & Biosimilars | ||

| Vaccines & Blood Products | ||

| Clinical Trail Materials | ||

| Cell & Gene Therapies | ||

| Medical Devices & Diagnostics | ||

| Veterinary Medicine | ||

| Others | ||

| By Country | United States | |

| Canada | ||

| Mexico |

By Service Type

| Transportation | Road Freight |

| Air Freight | |

| Sea Freight | |

| Rail Freight | |

| Warehousing & Storage | |

| Value-added Services and Others |

By Mode of Operation

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

By Product Type

| Prescription Drugs |

| OTC Drugs |

| Biologics & Biosimilars |

| Vaccines & Blood Products |

| Clinical Trail Materials |

| Cell & Gene Therapies |

| Medical Devices & Diagnostics |

| Veterinary Medicine |

| Others |

By Country

| United States |

| Canada |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the North America pharmaceutical logistics market?

The market is valued at USD 181.70 billion in 2025 and is projected to reach USD 241.85 billion by 2030.

Which service segment holds the largest share of the market?

Transportation services dominate with 72% of revenue in 2024, reflecting the need for rapid, compliant movement of medicines.

Why is cold-chain logistics growing faster than non-cold-chain services?

The rise of biologics, vaccines and cell-and-gene therapies demands strict temperature control, driving an 7.2% CAGR for cold-chain operations through 2030.

Which country is growing the fastest within the region?

Mexico is forecast to post a 8.1% CAGR as companies near-shore fill-finish capacity to take advantage of new tax incentives.

What are the main constraints on market growth?

Chronic driver shortages that limit road capacity and high compliance costs for ultra-cold shipments exert downward pressure on growth despite strong demand.

How are companies addressing sustainability in pharmaceutical logistics?

Carriers are adopting re-usable passive shippers, IoT monitoring and route optimisation to cut carbon emissions while safeguarding product integrity.

Page last updated on: July 1, 2025