Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

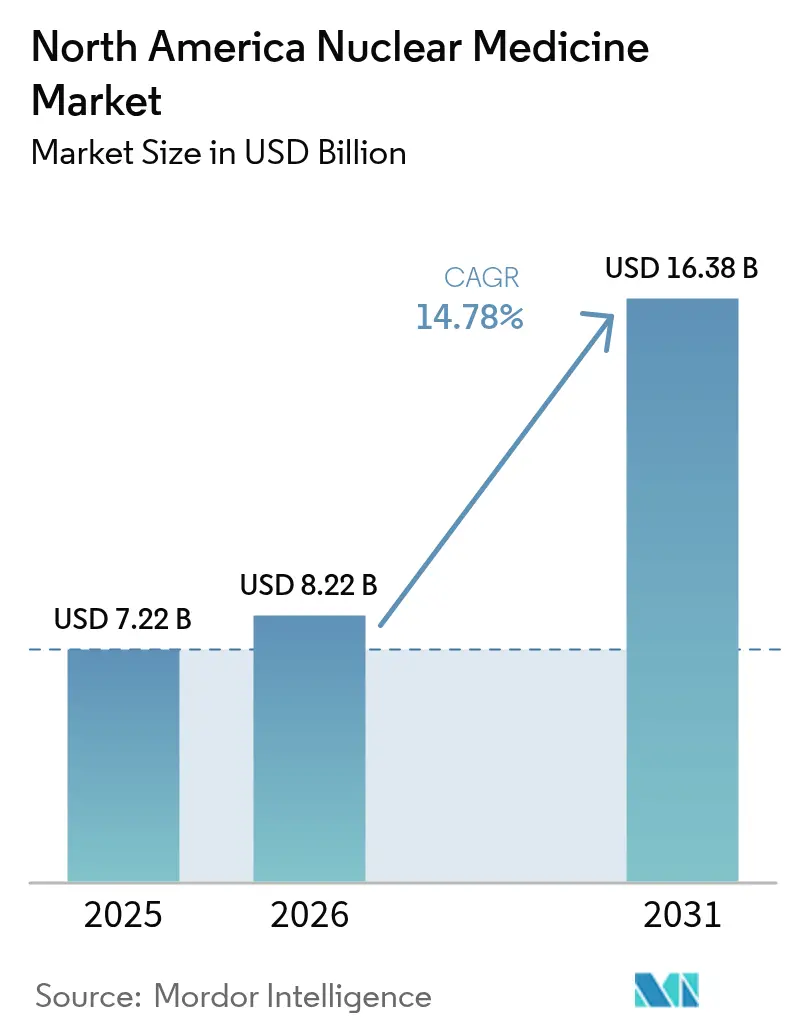

| Base Year Market Size (2025) | USD 7.22 Billion |

| Market Size (2026) | USD 8.22 Billion |

| Market Size (2031) | USD 16.38 Billion |

| Growth Rate (2026 - 2031) | 14.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Nuclear Medicine Market Analysis by Mordor Intelligence

The North America nuclear medicine market size is expected to grow from USD 7.22 billion in 2025 to USD 8.22 billion in 2026 and is forecast to reach USD 16.38 billion by 2031 at a 14.78% CAGR over 2026-2031. This expansion underscores the segment’s pivotal role in precision diagnostics and targeted therapy across oncology, cardiology, and neurology. Sustained investment in radiotheranostics, broader clinical indications, and supportive reimbursement policies continue to lift procedure volumes despite macro-economic pressures. Supply chain localization, particularly for molybdenum-99 and actinium-225, further reduces procurement risk and strengthens value-chain resilience. Intensifying competition among incumbents and new entrants accelerates innovation while patent litigation shapes strategic positioning.

Key Report Takeaways

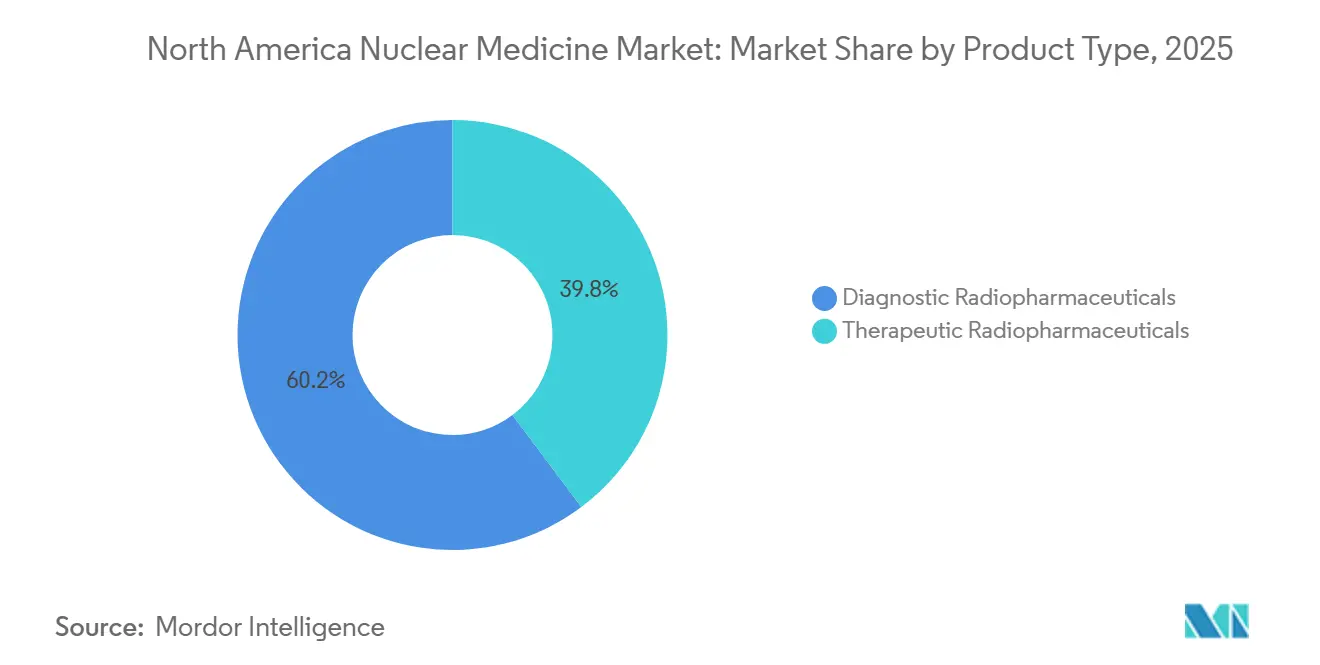

- By product type, diagnostic radiopharmaceuticals held 60.23% of the North America nuclear medicine market share in 2025. Therapeutic radiopharmaceuticals are advancing at an 15.62% CAGR through 2031.

- By application, oncology accounted for a 53.51% share of the North America nuclear medicine market size in 2025, Neurology is projected to expand at an 14.69% CAGR to 2031.

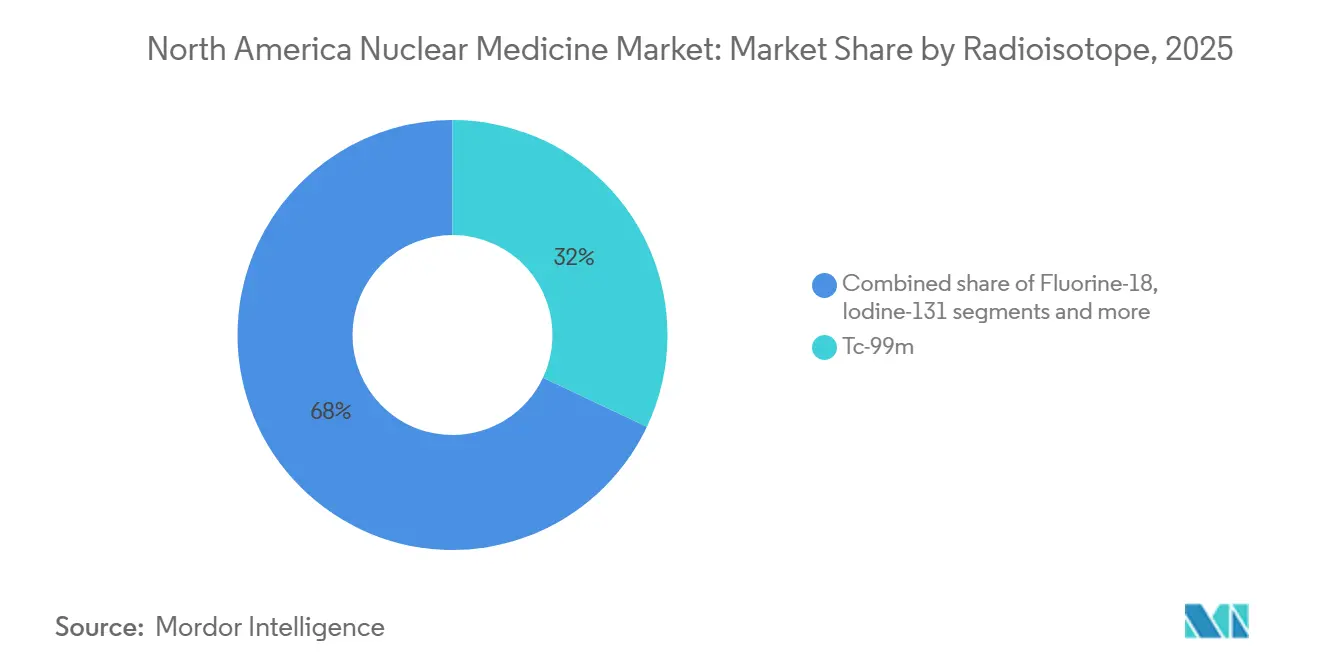

- By radioisotope, technetium-99m commanded 32.01% share of the North America nuclear medicine market size in 2025, Yttrium-90 is growing at a 16.68% CAGR through 2031.

- By end user, hospitals led with 65.11% revenue share in 2025, diagnostic imaging centers record the highest projected CAGR at 15.71% through 2031.

- By geography, the United States commanded 84.40% share of the North America nuclear medicine market in 2025, the country is projected to grow at an 14.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Nuclear Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of cancer & CVD | +2.8% | Aging U.S. population and major Canadian provinces | Long term (≥ 4 years) |

| Hybrid imaging adoption surge | +2.1% | United States and Canada | Medium term (2-4 years) |

| Domestic Mo-99 supply build-out | +1.9% | United States with spillover to Canada | Medium term (2-4 years) |

| FDA fast-tracks novel radiotheranostics | +1.7% | U.S. regulatory leadership | Short term (≤ 2 years) |

| Alpha-emitter pipeline expansion | +1.5% | Major North American cancer centers | Long term (≥ 4 years) |

| AI-enabled dose reduction and workflow gains | +1.3% | Technology-advanced U.S. and Canadian health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising burden of cancer & CVD

Cancer incidence continues to climb across North America, with cardiovascular disease remaining the leading cause of mortality, sustaining demand for accurate diagnostic and therapeutic nuclear medicine procedures. Demographic aging amplifies this need as prostate, breast, and lung cancer prevalence rises sharply beyond age 60. Pediatric indications now grow following FDA approval of lutetium Lu 177 dotatate for patients aged 12 and above, opening new addressable populations[1]Source: U.S. Food and Drug Administration, “FDA approves lutetium Lu 177 dotatate for pediatric patients,” fda.gov . While traditional SPECT cardiac volumes ebb, PET myocardial perfusion imaging gains favor for its higher specificity. The convergence of oncology and cardiology applications enables providers to streamline care pathways and cross-sell services, anchoring multi-specialty revenue streams.

Hybrid imaging (SPECT/CT, PET/CT) adoption surge

North American healthcare systems increasingly adopt these technologies, with cardiac PET imaging gaining significant traction among US cardiologists as demonstrated by expanding clinical adoption and improved reimbursement frameworks under Centers for Medicare & Medicaid Services reforms in 2025 that provide separate payment pathways for advanced diagnostic radiopharmaceuticals. GE HealthCare’s Flyrcado tracer, with a 109-minute half-life, broadens stress testing feasibility and attracts outpatient cardiology centers. Detector advances such as cadmium zinc telluride improve resolution while trimming radiation dose, addressing clinician and patient safety. Artificial intelligence algorithms automate lesion quantification, reducing interpretation variability and accelerating report turnaround.

Domestic Mo-99 supply build-out (NorthStar, etc.)

The U.S. Department of Energy funds multiple initiatives that target 75% self-sufficiency in molybdenum-99 production. SHINE Technologies and NorthStar advance facilities designed to replace historically imported supply, shielding providers from international reactor outages. Canada complements regional resilience through cobalt-60 production at Darlington, diversifying isotope availability. These projects shorten logistics chains, stabilize pricing, and improve predictability for high-volume imaging centers.

Accelerated pathways support agents such as 225Ac-FL-020 and 64Cu-SAR-bisPSMA, cutting development timelines and de-risking capital allocation. The agency’s approval of Flyrcado for coronary artery disease illustrates readiness to endorse tracers with clear clinical benefit. Health Canada mirrors these processes, enabling synchronized launches and larger first-year revenue bases for manufacturers. Regulatory momentum draws venture funding and catalyzes M&A activity around pipeline assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short half-life logistics bottlenecks | -1.8% | Rural United States and remote Canadian regions | Short term (≤ 2 years) |

| High CAPEX & regulatory hurdles for cyclotrons | -1.6% | United States and Canada | Medium term (2-4 years) |

| Mo-99 HEU-to-LEU transition delays | -1.2% | U.S. domestic production initiatives | Long term (≥ 4 years) |

| Radiopharmacist talent shortage | -1.1% | United States with spillover to Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short half-life logistics bottlenecks

Many diagnostic isotopes decay within hours, demanding just-in-time distribution. Fluorine-18’s 6-hour half-life restricts shipment zones to roughly 200 miles. In 2024, unexpected European reactor downtime created 50-100% shortages in technetium-99m across multiple U.S. states, delaying elective scans[2]Source: Society of Nuclear Medicine and Molecular Imaging, “Imminent Mo-99/Tc-99m Shortage,” snmmi.org . Cold-chain compliance adds cost, and rural sites often cannot meet delivery windows, limiting service availability. Longer-lived copper-64 offers partial relief, though widespread clinical adoption hinges on additional infrastructure and trial data.

High CAPEX & regulatory hurdles for cyclotrons

Installing a 70 MeV cyclotron costs USD 17 million, while annual operating expenses can top USD 1.9 million. Dual oversight by FDA and NRC necessitates exhaustive documentation and multi-year licensing, discouraging smaller providers. Jubilant Radiopharma’s USD 50 million deal for five KIUBE 180 units underscores the financial barrier to entry. These constraints concentrate production among large academic centers and commercial radiopharmacies, perpetuating geographic disparities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutics Reshape Market Dynamics

Diagnostic radiopharmaceuticals retained 60.23% share of the North America nuclear medicine market in 2025, supported by entrenched reimbursement and entrenched clinician familiarity. Therapeutic agents, however, are growing much faster at an 15.62% CAGR as radioligands like lutetium-177 PSMA address advanced metastatic disease with favorable safety profiles. The North America nuclear medicine market size for therapeutics is set to surpass USD billion by 2031, reflecting accelerating adoption among oncologists. SPECT remains dominant in routine bone scans, while PET’s superior resolution wins neurology and oncology referrals. Artificial intelligence-driven dosimetry improves treatment precision, reinforcing payer confidence in premium reimbursement tiers.

A reinforcing loop exists between diagnostic and therapeutic revenues: positive imaging experiences facilitate patient enrollment in companion therapeutics. Novartis’s Pluvicto reached USD 1 billion in U.S. sales during the first nine months of 2024, validating commercial appetite for high-value radiotheranostics. CMS payment reform in 2025 created a separate APC for diagnostic tracers above USD 630, improving hospital margins and encouraging inventory expansion. The North America nuclear medicine industry now positions therapeutic innovation as a primary differentiator among manufacturers that once concentrated on diagnostic agents.

By Application: Neurology Gains Momentum Beyond Oncology Dominance

Oncology represented 53.81% of the North America nuclear medicine market in 2025, reflecting its central role in tumor staging and therapy monitoring. The North America nuclear medicine market size for oncology applications is forecast to cross USD 8.97 billion in 2031 at an 14.69% CAGR. Neurology is the fastest-growing application, expanding 11.42% annually as amyloid and tau PET increase Alzheimer’s diagnostic accuracy. CMS travel policy updates in 2025 lowered out-of-pocket costs for Medicare beneficiaries, further encouraging scan uptake.

Neuroimaging demand spurs supply chain adjustments for fluorine-18 tracers like Neuraceq, recently added through Lantheus’s USD 750 million acquisition of Life Molecular Imaging. Advanced AI algorithms shorten interpretation time from 12 minutes to 4 minutes per scan, addressing neuroradiologist shortages. Cardiology maintains relevance through PET perfusion imaging, which grew 6% year-over-year in 2024 despite SPECT declines. Endocrinology remains steady, with thyroid uptake studies and iodine-131 therapy stable across major U.S. academic centers.

By Radioisotope: Actinium-225 Disrupts Technetium Dominance

Technetium-99m delivered 55.70% of procedure volume in 2025, underpinning core cardiology and bone applications. The North America nuclear medicine market share of technetium-based diagnostics is expected to contract to 47.20% by 2031 as alternative tracers gain ground. Actinium-225 is surging at 10.98% CAGR, supported by new domestic production capacity in Wisconsin and Missouri. The North America nuclear medicine market size for actinium-225 therapeutics could reach USD 1.18 billion by 2031, pending successful late-phase trials.

Lutetium-177 benefits from approved products like Pluvicto and Lutathera, while gallium-68 generators broaden access for community sites lacking cyclotrons. Fluorine-18 diversifies beyond FDG into cardiac perfusion and neuroreceptor imaging, increasing throughput at PET-CT sites. NorthStar’s 52,000-square-foot CDMO facility accelerates actinium-225 and lutetium-177 supply, giving smaller biotechs a rapid path to clinical lot manufacturing.

By End User: Imaging Centers Challenge Hospital Dominance

Hospitals captured 65.11% of revenue in 2025, anchored by integrated service lines and established inpatient referrals. Diagnostic imaging centers, however, lead growth at an 15.71% CAGR through 2031 as payers redirect routine scans to lower-cost settings. The North America nuclear medicine market size attributable to imaging centers is projected to reach USD 4.23 billion by 2031. Academic institutes contribute high complexity research and early adopter volumes, while pharmaceutical companies invest in captive facilities to secure trial supply continuity.

IMV survey data show total nuclear medicine procedure volumes falling 5.7% between 2021 and 2023, but non-hospital sites increased 2.5%, foreshadowing sustained outpatient migration. CMS Condition of Participation 42 CFR 482.53 sets uniform quality benchmarks, allowing independent centers to compete on equal footing with hospital departments [ECFR.GOV]. Theranostics capability penetration reached 14% of North American sites in 2024, predominantly within specialty outpatient centers due to streamlined approval pathways and shorter patient stays.

Geography Analysis

The United States accounted for 88.90% of the North America nuclear medicine market in 2025 and is advancing at an 11.10% CAGR, reaffirming its dominance in clinical trial activity, isotope manufacturing, and reimbursement leadership. Medicare’s 2025 payment separation for high-cost tracers enhances provider profitability and supports nationwide adoption of advanced agents. Central Indiana’s cluster effect attracts global manufacturers, offering same-day distribution to two-thirds of the U.S. population, enhancing supply reliability.

Canada holds a smaller but strategically significant share. Health Canada’s alignment with FDA’s accelerated pathways facilitated approvals for Illuccix and NETVision, opening high-growth neurology and neuroendocrine segments. Domestic cobalt-60 production at Darlington strengthens isotope sovereignty, while PET-CT scanner density remains below OECD average, indicating expansion potential. Provincial funding initiatives in Ontario and British Columbia earmark capital for new cyclotrons and radiopharmacy upgrades.

Mexico remains an emerging participant. Regulatory reforms under COFEPRIS align medical device quality standards with international benchmarks, improving market access for imaging equipment vendors. Rising middle-class healthcare spending and public-private partnerships support pilot PET-CT centers in Mexico City and Monterrey. While current procedure volume is modest, double-digit growth trajectories position Mexico as a future outperformer once infrastructure and trained personnel scale.

Overall, geographic concentration in the United States accelerates innovation but introduces risk exposure to U.S. policy shifts. Canada and Mexico offer diversification pathways and incremental volume growth that moderate regional cyclicality

Competitive Landscape

Moderate market concentration characterizes the North America nuclear medicine market as top players combine imaging systems, radiopharmaceutical portfolios, and service contracts to defend share. Novartis, GE HealthCare, Siemens Healthineers, Lantheus, and Curium command roughly 64% of total revenue. Novartis reinforces lead through aggressive patent litigation against Eli Lilly, safeguarding Pluvicto and Lutathera exclusivity. Lantheus accelerated inorganic growth via the USD 750 million Life Molecular Imaging acquisition and Evergreen Theragnostics buyout, expanding neurology and oncology offerings.

Horizontal integration shapes supply security: NorthStar’s CDMO model supplies isotopes to smaller drug developers, challenging vertically integrated manufacturers. Siemens Healthineers bolstered U.S. PET operations by acquiring Novartis’s imaging business for USD 223 million, reducing time-to-market for novel tracers. Strategic alliances, such as the seven-year imaging partnership between GE HealthCare and Sutter Health, illustrate demand for turnkey AI-enabled solutions that mitigate staffing shortfalls.

White-space opportunities persist in rural delivery, alpha-emitter therapeutics, and AI-driven workflow software. Barriers include high CAPEX, complex regulations, and specialized workforce requirements, which collectively moderate new-entrant threat and sustain incumbent pricing power.

North America Nuclear Medicine Industry Leaders

Cardinal Health

GE Healthcare

Novartis AG

Lantheus Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lantheus Holdings completed the acquisition of Life Molecular Imaging for up to USD 750 million, gaining access to Neuraceq F-18 PET imaging agent for Alzheimer’s detection.

- January 2025: GE HealthCare announced a strategic partnership with Sutter Health covering 7 years and 3.5 million patients across California, deploying AI-powered imaging technologies including PET/CT and SPECT/CT.

North America Nuclear Medicine Market Report Scope

As per the scope of the report, nuclear medicine falls under the field of molecular imaging, which involves the use of a very small amount of radioactive material (radiopharmaceuticals) to diagnose and treat diseases. In nuclear medicine imaging, radioisotopes are detected by special types of cameras attached to the computer, which provide precise pictures of the area of the body examined. The North America Nuclear Medicine Market is Segmented by Product Type (Diagnostics (Single Photon Emission Computed Tomography (SPECT) and Photon Emission Tomography (PET)) and Therapeutics (Alpha Emitters, Beta Emitters, and Brachytherapy)), Applications (Cardiology, Neurology, Oncology, and Other Applications), and Geography (United States, Canada, and Mexico). The report offers the value (USD million) for the above segments.

By Product Type

| Diagnostic Radiopharmaceuticals | SPECT |

| PET | |

| Therapeutic Radiopharmaceuticals | Targeted Beta Therapy |

| Targeted Alpha Therapy | |

| Brachytherapy |

By Application

| Oncology |

| Cardiology |

| Neurology |

| Endocrinology |

| Other Applications |

By Radioisotope

| Technetium-99m |

| Fluorine-18 |

| Iodine-131 |

| Lutetium-177 |

| Yttrium-90 |

| Gallium-68 |

| Others |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Academic & Research Institutes |

North America

| United States |

| Canada |

| Mexico |

| By Product Type | Diagnostic Radiopharmaceuticals | SPECT |

| PET | ||

| Therapeutic Radiopharmaceuticals | Targeted Beta Therapy | |

| Targeted Alpha Therapy | ||

| Brachytherapy | ||

| By Application | Oncology | |

| Cardiology | ||

| Neurology | ||

| Endocrinology | ||

| Other Applications | ||

| By Radioisotope | Technetium-99m | |

| Fluorine-18 | ||

| Iodine-131 | ||

| Lutetium-177 | ||

| Yttrium-90 | ||

| Gallium-68 | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Academic & Research Institutes | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America nuclear medicine market in 2026?

It is valued at USD 8.90 billion, with an 11.02% CAGR projected through 2031.

Which product category is growing fastest?

Therapeutic radiopharmaceuticals are expanding at 11.12% annually due to rising adoption of radioligand therapies.

What share do hospitals hold in procedure revenue?

Hospitals account for 68.20% of revenue, though outpatient imaging centers are gaining ground.

Which radioisotope leads diagnostic use?

Technetium-99m maintains 55.70% share, supported by entrenched cardiac and bone scan protocols.

Why is actinium-225 gaining attention?

Alpha-emitter actinium-225 therapies show high tumor-cell kill and are growing at an 10.98% CAGR as domestic production scales.

How are regulators supporting innovation?

FDA and Health Canada deploy fast-track and accelerated approval pathways, shortening development cycles for novel radiotheranostics.

Page last updated on: