Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

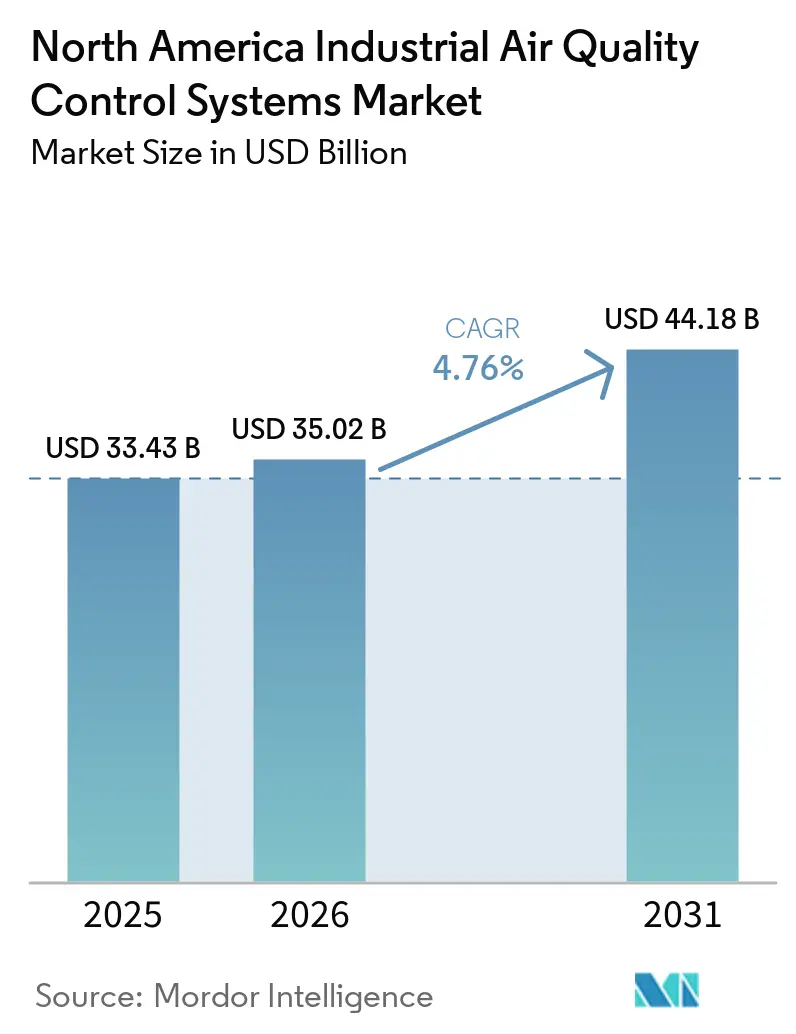

| Base Year Market Size (2025) | USD 33.43 Billion |

| Market Size (2026) | USD 35.02 Billion |

| Market Size (2031) | USD 44.18 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

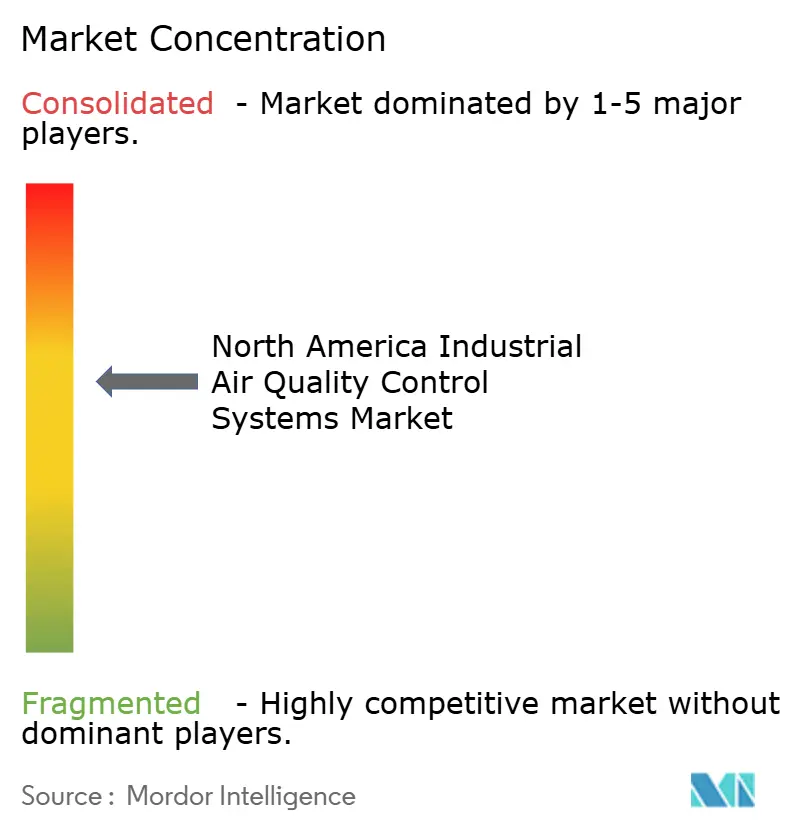

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Industrial Air Quality Control Systems Market Analysis by Mordor Intelligence

The North America Industrial Air Quality Control Systems Market size is expected to grow from USD 33.43 billion in 2025 to USD 35.02 billion in 2026 and is forecast to reach USD 44.18 billion by 2031 at 4.76% CAGR over 2026-2031. Growth is being led by tighter air quality compliance requirements, especially after the U.S. Environmental Protection Agency revised the primary annual PM2.5 standard to 9.0 µg/m³ in February 2024, which raised the pressure on industrial sites to upgrade emission control equipment.[1]Environmental Protection Agency, “Clean Air Act Reclassification of the San Antonio, Dallas-Fort Worth, and Houston-Galveston-Brazoria Ozone Nonattainment Areas, TX,” Federal Register, federalregister.gov New industrial investment tied to nearshoring, refinery activity, and data center related power demand is also increasing permitting pressure across major U.S. corridors, which is lifting demand for scrubbers, filters, and integrated control systems. The North America air quality control systems market is also benefiting from carbon capture related retrofit plans in cement, steel, and power, because these projects need cleaner flue gas before capture systems can operate reliably.[2]Government of Canada, “Canada Partners With Heidelberg Materials to Drive Cement Industry Decarbonization,” Innovation, Science and Economic Development Canada, canada.ca Vendor strategy is shifting toward larger bundled contracts that combine hardware, controls, and performance services, which favors suppliers with strong engineering depth and execution capacity. At the same time, fabrication limits, catalyst availability, and skilled labor shortages are slowing project conversion and keeping the North America air quality control systems market on a steady rather than a rapid growth path.

Key Report Takeaways

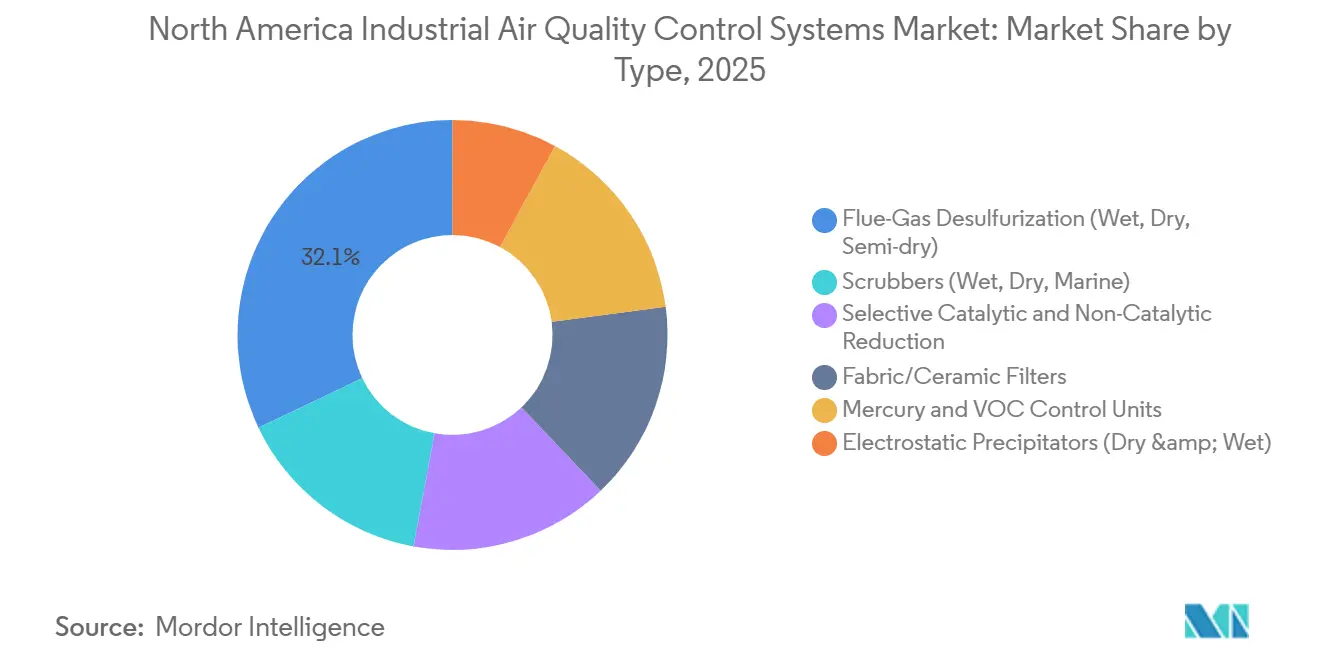

- By type, flue-gas desulfurization held 32.1% of the North America air quality control systems market share in 2025, while fabric and ceramic filters are projected to grow at a 5.3% CAGR through 2031.

- By pollutant controlled, particulate matter accounted for 34.7% of the North America air quality control systems market size in 2025, while VOC control is forecast to expand at a 5.5% CAGR through 2031.

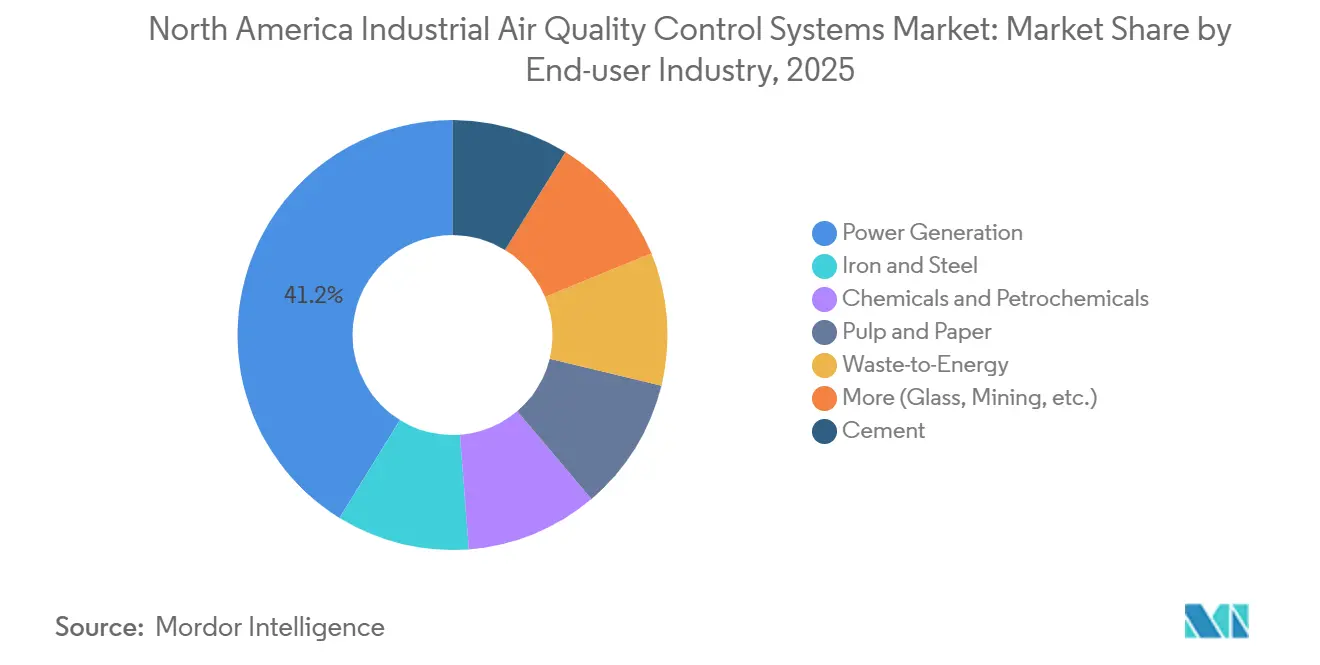

- By end-user industry, power generation captured 41.2% of demand in 2025, while chemicals and petrochemicals is expected to record the highest CAGR at 6.3% through 2031.

- By geography, the United States held 78.6% share in 2025, while Mexico is expected to post the fastest growth at a 6.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Industrial Air Quality Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter PM2.5 And Ozone Compliance | +1.2% | U.S. nationwide, with stronger effect in California, the Ohio Valley, the Mid-Atlantic, and other nonattainment counties | Short term (≤ 2 years) |

| Oil And Gas Methane And Sulfur Control Upgrades | +0.8% | U.S. Gulf Coast, Permian Basin, Alberta, and British Columbia | Medium term (2-4 years) |

| CCUS-Ready Cement And Steel Retrofit Wave | +0.9% | Indiana, Missouri, Texas, and Alberta | Long term (≥ 4 years) |

| AI-Enabled Optimization And Predictive Maintenance | +0.5% | Early adoption in U.S. refining, power, and chemical clusters | Medium term (2-4 years) |

| Tighter Permit Headroom From Lower PM2.5 Thresholds | +0.4% | U.S. attainment and near-nonattainment industrial corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter PM2.5 and Ozone Compliance Reshapes Permitting Economics

The U.S. Environmental Protection Agency lowered the primary annual PM2.5 standard to 9.0 µg/m³ in February 2024, which immediately tightened the compliance context for large industrial sources.[3]Environmental Protection Agency, “Standards of Performance for New, Reconstructed, and Modified Sources, Oil and Natural Gas Sector Climate Review,” GovInfo, govinfo.gov This change reduced the operating cushion that many facilities had relied on when planning plant expansions or permit renewals. Projects that could once move forward with limited control upgrades now face a stronger need to prove lower emissions performance under stricter air quality review. The pressure increased further when Dallas-Fort Worth, Houston-Galveston-Brazoria, and San Antonio were reclassified from Moderate to Serious ozone nonattainment, effective in July 2024.[4]Environmental Protection Agency, “Clean Air Act Reclassification of the San Antonio, Dallas-Fort Worth, and Houston-Galveston-Brazoria Ozone Nonattainment Areas, TX,” Federal Register, federalregister.gov That change lowered major source thresholds to 50 tons per year and pushed RACT obligations toward 2026 implementation windows. In the North America air quality control systems market, these combined rules are moving filter, scrubber, and NOx-control spending into current capital planning cycles.

Oil and Gas Methane and Sulfur Control Upgrades Expand Multi-Pollutant Demand

The EPA finalized a major package of methane and VOC controls for the oil and natural gas sector in March 2024, making this one of the most important compliance shifts affecting heavy industrial emissions equipment. The rule covers 28% of U.S. anthropogenic methane emissions and 23% of anthropogenic VOC emissions from the sector. It requires zero-emissions pneumatic controllers, quarterly optical gas imaging at multi-well sites, and 99.9% SO2 reduction from certain sweetening units. This is changing purchase behavior because gas processing and refining sites are increasingly evaluating sulfur scrubbing, vapor recovery, NOx reduction, and continuous monitoring as part of one investment cycle rather than as separate projects. Canada is also tightening industrial emissions policy for large emitters, which supports a broader regional procurement base for air quality control equipment. As a result, the North America air quality control systems market is seeing stronger multi-pollutant demand across the Gulf Coast, the Permian Basin, Alberta, and British Columbia.

CCUS-Ready Cement and Steel Retrofit Wave Creates Pre-Treatment Hardware Demand

Carbon capture projects in cement and steel do not begin with the capture unit alone, because they also require cleaner and more stable flue gas upstream of the absorber. That requirement is creating parallel demand for wet electrostatic precipitators, gas coolers, and advanced desulfurization systems that protect capture equipment from sulfur, moisture, and particulate contamination. The Government of Canada committed up to CAD 275 million (~USD 198 million) to support Heidelberg Materials’ Edmonton cement project, which targets 1 million metric tonnes of annual CO2 capture and expects operations to begin in late 2026. In the United States, Heidelberg Materials’ Mitchell, Indiana, plant was selected for up to USD 500 million in funding to capture 2 million tonnes of CO2 annually. Cemex’s Knoxville plant was also selected in January 2025 for a USD 101 million carbon capture, removal, and conversion test center. In the North America air quality control systems market, this means CCUS spending is also creating a second stream of demand for pretreatment emission-control hardware before the capture train is installed.

AI-Enabled Optimization and Predictive Maintenance Shifts the Value Proposition

AI-based optimization is changing how operators evaluate emission control systems, because it moves the discussion from basic compliance toward efficiency and uptime. Yokogawa and Aramco commissioned multiple autonomous AI control agents at the Fadhili Gas Plant in October 2025. The project cut amine and steam consumption by 10% to 15% and reduced power use by 5% in acid gas removal operations. JFE Steel also reported in June 2024 that a digital twin-optimized burner design reduced NOx emissions by 30% and cut energy use by 3%. These results support the case for more sensor-rich equipment, remote diagnostics, and software-led performance management. Across the North America air quality control systems market, new installations increasingly need stronger control architecture and data integration as part of the base system scope rather than as an optional add-on.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coal Retirements Reduce Legacy Retrofit Demand | -0.9% | U.S. Midwest, Appalachia, Southeast, and Alberta | Medium term (2-4 years) |

| High Retrofit Capex And Outage Complexity | -0.7% | U.S. nationwide, Ontario, and Alberta | Medium term (2-4 years) |

| Skilled Labor And Catalyst Lead-Time Bottlenecks | -0.5% | U.S. and Canada heavy industrial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Coal Retirements Reduce Legacy Retrofit Demand, but the Pace Is Uneven

Coal retirements are reducing one of the oldest recurring revenue pools for scrubbers, SCR systems, and particulate control retrofits. Coal-fired plants historically required frequent compliance upgrades, which made them a dependable source of aftermarket and replacement demand. As older units leave the grid, the installed base becomes smaller across the Midwest, Appalachia, the Southeast, and parts of Canada. The decline is still uneven because reliability concerns and fuel-price shifts have kept some aging units online longer than earlier assumptions suggested. That uneven retirement pattern preserves catalyst replacement, baghouse maintenance, and scrubber service work as part of the fleet even as total coal exposure falls. For the North America air quality control systems market, the effect is a gradual mix shift toward gas, waste-to-energy, and CCUS-related pretreatment rather than a sudden collapse in power-sector demand.

High Retrofit Capex and Outage Complexity Constrain Project Conversion Rates

Retrofit projects remain difficult to approve because many heavy industrial plants cannot easily stop operations for long installation windows. In cement, adding new emission controls alongside carbon capture can raise production costs by up to 40%, which makes the full retrofit package hard to justify in one step. Operators therefore tend to phase their investment plans, moving first on lower-cost scrubber or filter upgrades and delaying larger integrated packages. This slows near-term order conversion even when compliance needs and decarbonization plans are already clear. Skilled labor shortages and catalyst lead times add another layer of delay in major industrial clusters across the United States and Canada. Vendors with modular designs, outage planning support, and financing flexibility are therefore better positioned to convert pipeline into revenue in the North America air quality control systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fabric and ceramic filters gain ground in high-temperature applications

Flue-gas desulfurization held 32.1% of the North America air quality control systems market share in 2025, which kept it as the leading technology group across regulated heavy industrial sites. Its position reflects the continued need for sulfur control in power generation, refining, and sour-gas processing, where wet, dry, and semi-dry systems each serve different operating conditions. Wet FGD remains the preferred route in large-capacity power and refinery settings where sulfur loads are high and removal efficiency requirements are strict. Semi-dry systems are gaining ground in industrial boilers and similar sites where water handling and wastewater disposal are harder to manage. This leaves FGD with a broad installed base and strong replacement demand even as the technology mix evolves within the North America air quality control systems market.

Fabric and ceramic filters are the fastest-growing type, and the North America air quality control systems market size for this segment is expected to rise at a 5.3% CAGR through 2031. Demand is strongest in cement kilns, waste-to-energy plants, and steel facilities that need finer particulate capture than older electrostatic precipitators can consistently deliver under tighter PM limits. Pulse-jet fabric filters remain attractive because they can achieve very high collection efficiency while keeping pressure drop manageable in many high-temperature settings. SCR and SNCR systems also remain important for facilities managing NOx obligations, especially where ozone compliance is tightening in nearby air basins. Electrostatic precipitators still provide stable maintenance revenue, but growth is slower because more retrofit decisions are shifting toward filters, scrubbers, and integrated multi-pollutant platforms in the North America air quality control systems industry.

By Pollutant Controlled: VOC control gains speed as chemical compliance deepens

VOC control is the fastest-growing pollutant category, and the North America air quality control systems market size for this segment is projected to expand at a 5.5% CAGR through 2031. The main driver is the EPA’s 2024 Hazardous Organic NESHAP amendments, which cover synthetic organic chemical manufacturing and polymers and resins facilities across the United States. The rule requires fenceline monitoring for 6 hazardous air pollutants, including ethylene oxide and chloroprene, with many compliance deadlines tied to July 2026. It also supports capital investment in thermal oxidizers, vapor recovery units, and closed-vent systems, with estimated spending across covered facilities reaching USD 522 million. Regenerative thermal oxidizers are especially well placed in high-volume chemical streams because they combine strong destruction efficiency with lower operating cost when VOC concentrations support autothermal operation.

Particulate matter remained the largest pollutant-controlled segment with a 34.7% share in 2025, reflecting the broad reach of PM2.5 regulation across almost every major industrial end user. This segment stays large because particulate control is required not only in power and cement, but also in metals, mining, grain handling, and waste processing applications. SOx and NOx categories are also stable and sizable, supported by scrubber upkeep, catalyst replacement, and recurring permit-driven maintenance. Mercury and air toxics remain smaller in revenue terms, but they still matter because compliance needs tend to reappear even when short-term exemptions or delays are granted. Across the North America air quality control systems industry, buyer preference is moving toward multi-pollutant packages that address PM, SOx, NOx, and toxics together under one performance guarantee.

By End-user Industry: Chemicals and petrochemicals lead growth while power remains the largest base

Within the North America air quality control systems industry, power generation held 41.2% of demand in 2025, while chemicals and petrochemicals are expected to grow at a 6.3% CAGR through 2031. Power remained the largest base because aging coal and gas units still need scrubber maintenance, SCR catalyst replacement, and baghouse retrofits under continuing air quality obligations. Chemicals and petrochemicals, however, are moving faster because MACT tightening, hazardous air pollutant monitoring, and nearshoring-led capacity additions are increasing control requirements across the Gulf Coast and in Mexico. The 2024 Hazardous Organic NESHAP amendments added another layer of urgency by pushing chemical producers toward fenceline monitoring and tighter vent control systems. This is giving the North America air quality control systems market a stronger growth engine in process industries than in legacy utility retrofit cycles alone.

Cement, iron, and steel plants are entering a more complex investment phase because new control systems now need to fit future CCUS readiness as well as current compliance needs. That pushes demand toward pretreatment equipment that can deliver cleaner, cooler, and more stable flue gas before a capture train is added. Waste-to-energy facilities also remain responsive because tighter standards for acid gases, particulates, and dioxin-related emissions support steady project flow in specialized filtration and scrubbing systems. Pulp and paper, glass, mining, and other industrial applications continue to form the long tail of demand, with spending driven more by permit renewals, asset age, and plant-specific upgrades than by one regulatory event. Over time, this broadening end-user mix should make the North America air quality control systems market less dependent on a single customer group, even though power generation remains the largest revenue contributor today.

Geography Analysis

The United States held 78.6% of the North America air quality control systems market size in 2025, supported by the scale of its industrial base, the depth of its enforcement structure, and the large installed base of regulated assets. Demand is concentrated in the Gulf Coast, the Midwest, and the Mid-Atlantic, where refining, petrochemicals, power generation, cement, and metals all require continuing emissions control investment. The July 2024 ozone reclassification of Dallas-Fort Worth, Houston-Galveston-Brazoria, and San Antonio added another near-term compliance trigger in Texas, which remains one of the region’s most important industrial corridors. Donaldson’s North America Industrial Filtration Solutions business reported 7.8% year-over-year sales growth in the fourth quarter of fiscal 2025, with management pointing to strong demand for new dust collection equipment in the U.S. market. Taken together, these signals show that the North America air quality control systems market remains anchored by U.S. retrofit and replacement cycles.

Canada contributes a smaller but structurally important share of the North America air quality control systems market because policy support for industrial decarbonization is creating a visible project pipeline. The federal commitment of up to CAD 275 million (~USD 198 million) to Heidelberg Materials’ Edmonton project gives Canada one of the clearest full-scale cement carbon capture reference points in the region. Oil sands, LNG, and other heavy industrial activity in Alberta and British Columbia also support recurring demand for vapor recovery, VOC abatement, sulfur control, and pretreatment systems. This makes Canada a smaller market in absolute terms, but a relevant one for suppliers targeting CCUS-linked upgrades and energy-sector emission controls.

Mexico is the fastest-growing geography, with the North America air quality control systems market size for the country expected to expand at a 6.1% CAGR through 2031. Growth is being driven by nearshoring-related investment in steel, cement, chemicals, and automotive production, especially in Nuevo León, Coahuila, and Sinaloa. Industrial operators are also moving toward more active monitoring and emissions management, as shown by Ternium’s deployment of 24 continuous perimeter air-quality monitoring stations across its Las Encinas and Guerrero steel plants in Monterrey in 2025. Mexico’s tightening regulatory alignment with cross-border manufacturing expectations is encouraging earlier investment in compliance equipment than in prior industrial cycles. This gives the North America air quality control systems market a second growth center beyond the United States, even though the country still starts from a smaller installed base.

Competitive Landscape

The North America air quality control systems market is moderately consolidated at the integrated-system level, but it remains more fragmented across filters, fans, catalysts, monitors, and other specialized sub-components. Babcock & Wilcox, CECO Environmental, GE Vernova, Mitsubishi Power, and FLSmidth are among the most visible participants in large utility and heavy-industrial projects because buyers value engineering depth, bankable guarantees, and the ability to manage complex installation scopes. Competition is increasingly centered on multi-pollutant system design rather than on a single device class, which is making project execution and lifecycle support more important than simple equipment pricing. This shift favors vendors that can combine sulfur control, particulate capture, NOx reduction, monitoring, and digital controls in one offering. In the North America air quality control systems market, that is raising barriers for smaller suppliers that only compete in one narrow technology category.

Strategic positioning is also changing because carbon capture readiness is opening a new layer of competition around pretreatment equipment and flue-gas conditioning. Valmet’s first commercial order for an integrated carbon capture pretreatment solution in June 2025 shows how suppliers are trying to build a position in this underserved niche before it becomes crowded. GE Vernova’s October 2024 DOE-funded study on exhaust gas recirculation also shows how process design and proprietary integration can be used to lower capture costs and differentiate platform performance. Babcock & Wilcox’s December 2025 contract for advanced wet gas scrubbing technology at a Canadian petroleum refinery is another example of suppliers winning larger pollution-control scopes where sulfur removal and refinery integration matter more than standalone equipment supply. These moves show that the North America air quality control systems market is rewarding vendors that can align conventional compliance hardware with newer decarbonization and optimization needs. They also explain why installed-base relationships and technical credibility remain strong competitive advantages.

A second white space is emerging in Mexico, where locally assembled and locally serviced industrial emission control platforms remain less developed than in the United States. Another open area is AI-native optimization software that can sit on top of existing continuous emissions monitoring and process-control infrastructure and create recurring service revenue. Suppliers that pair hardware with remote diagnostics, predictive maintenance, and guaranteed operating outcomes should be better placed to defend margins as procurement teams become more performance-focused. Overall, the North America air quality control systems market remains competitive, but the strongest positions are still concentrated among vendors that can fund, engineer, install, and service large multi-technology systems over long project cycles.

North America Industrial Air Quality Control Systems Industry Leaders

General Electric Company

Babcock & Wilcox Enterprises Ltd

Ducon Technologies Inc

CECO Environmental Corporation

ANDRITZ AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Angeleno Group, a Los Angeles-based investment firm, has invested in NESTEC, a provider of industrial air pollution control systems. The investment supports NESTEC's expansion into new markets, including renewable fuels and semiconductors, while enabling geographic growth and product development advancements across its portfolio of clean energy and climate solutions.

- October 2025: Yokogawa and Aramco commissioned multiple autonomous AI control agents at the Fadhili Gas Plant, achieving 10% to 15% reduction in amine and steam use and 5% power savings in acid gas removal, validating AI-driven optimization for emission control processes at a commercial scale.

- August 2025: Donaldson Company reported record fiscal 2025 full-year results with Industrial Filtration Solutions sales of USD 914.2 million, North America IFS growing 7.8% in the fourth quarter, driven by new dust collection equipment demand, and management guided mid-single-digit IFS growth for fiscal 2026.

- June 2025: Valmet launched its first commercial order for an integrated carbon capture pre-treatment solution combining a condensing flue gas scrubber and wet electrostatic precipitator, for cleaner flue-gas conditioning ahead of CO2 absorbers.

North America Industrial Air Quality Control Systems Market Report Scope

Air Quality Control Systems (AQCS) include control systems that reduce the proportion of pollutants from flue gases emitted from exhausts of power plants and other industries, mainly fuelled by fossil fuels.

The North America Industrial Air Quality Control Systems Market is segmented into type, pollutant controlled, end-user industry, and geography. By type, the market is segmented into electrostatic precipitators, flue-gas desulfurization systems, scrubbers, SCR/SNCR systems, fabric/ceramic filters, and mercury and VOC units. By pollutant controlled, the market is segmented into PM, SOx, NOx, VOC, mercury, and air toxics. By end-user industry, the market is segmented into power generation, cement, iron and steel, chemicals and petrochemicals, pulp and paper, waste-to-energy, and other industries. The report also covers the market size and forecasts for the industrial air quality control systems market across key countries in North America, including the United States, Canada, and Mexico. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Type

| Electrostatic Precipitators (Dry & Wet) |

| Flue-Gas Desulfurization (Wet, Dry, Semi-dry) |

| Scrubbers (Wet, Dry, Marine) |

| Selective Catalytic and Non-Catalytic Reduction |

| Fabric/Ceramic Filters |

| Mercury and VOC Control Units |

By Pollutant Controlled

| Particulate Matter (PM) |

| SOx |

| NOx |

| Volatile Organic Compounds (VOC) |

| Mercury and Air Toxics |

By End-user Industry

| Power Generation |

| Cement |

| Iron and Steel |

| Chemicals and Petrochemicals |

| Pulp and Paper |

| Waste-to-Energy |

| Others (Glass, Mining, etc.) |

By Geography

| United States |

| Canada |

| Mexico |

| By Type | Electrostatic Precipitators (Dry & Wet) |

| Flue-Gas Desulfurization (Wet, Dry, Semi-dry) | |

| Scrubbers (Wet, Dry, Marine) | |

| Selective Catalytic and Non-Catalytic Reduction | |

| Fabric/Ceramic Filters | |

| Mercury and VOC Control Units | |

| By Pollutant Controlled | Particulate Matter (PM) |

| SOx | |

| NOx | |

| Volatile Organic Compounds (VOC) | |

| Mercury and Air Toxics | |

| By End-user Industry | Power Generation |

| Cement | |

| Iron and Steel | |

| Chemicals and Petrochemicals | |

| Pulp and Paper | |

| Waste-to-Energy | |

| Others (Glass, Mining, etc.) | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the North America Industrial Air Quality Control Systems Market Size?

The North America Industrial Air Quality Control Systems Market size is expected to grow from USD 33.43 billion in 2025 to USD 35.02 billion in 2026 and is forecast to reach USD 44.18 billion by 2031 at 4.76% CAGR over 2026-2031.

Which technology segment leads demand in this space?

Flue-gas desulfurization leads with 32.1% share in 2025 because sulfur control remains essential in power, refining, and sour-gas processing applications.

Which pollutant category is growing the fastest?

VOC control is the fastest-growing pollutant category, with a 5.5% CAGR through 2031, supported by EPA hazardous air pollutant rules affecting chemical manufacturing facilities.

Which end-user segment offers the best growth outlook?

Chemicals and petrochemicals has the strongest growth outlook at a 6.3% CAGR through 2031, while power generation remains the largest end-user base at 41.2% share in 2025.

Which country has the largest role in regional demand?

The United States leads with 78.6% share in 2025 because of its larger regulated industrial base, broader enforcement framework, and heavier retrofit pipeline.

Why is Mexico becoming more important for suppliers?

Mexico is the fastest-growing geography at a 6.1% CAGR through 2031, supported by nearshoring-led expansion in steel, cement, chemicals, and automotive manufacturing.

Page last updated on: