Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

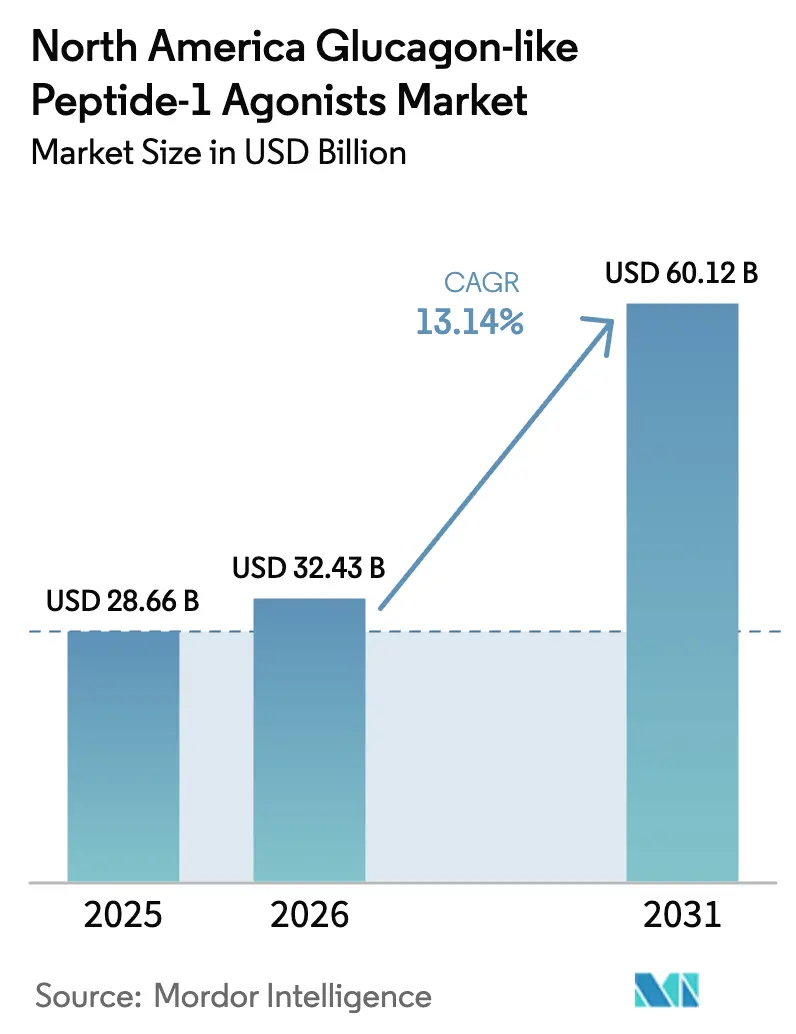

| Base Year Market Size (2025) | USD 28.66 Billion |

| Market Size (2026) | USD 32.43 Billion |

| Market Size (2031) | USD 60.12 Billion |

| Growth Rate (2026 - 2031) | 13.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Glucagon-like Peptide-1 Agonists Market Analysis by Mordor Intelligence

The North America glucagon-like peptide-1 agonists market size is projected to be USD 28.66 billion in 2025, USD 32.43 billion in 2026, and reach USD 60.12 billion by 2031, growing at a CAGR of 13.14% from 2026 to 2031. The trajectory is powered by three converging factors, namely higher type-2 diabetes incidence, escalating obesity prevalence, and cardiometabolic guideline revisions that elevate incretin agents to first-line status. Commercial insurers are widening coverage for weight-management prescriptions, while employer self-insured plans are adopting guaranteed-savings models that accelerate uptake. Manufacturers are spending more than USD 20 billion on capacity expansion through 2026, a response to periodic product shortages that exposed supply-chain bottlenecks. Digital prescribing and direct-to-consumer (DTC) fulfillment have compressed the time from consultation to therapy initiation, further lifting prescription volumes.

Key Report Takeaways

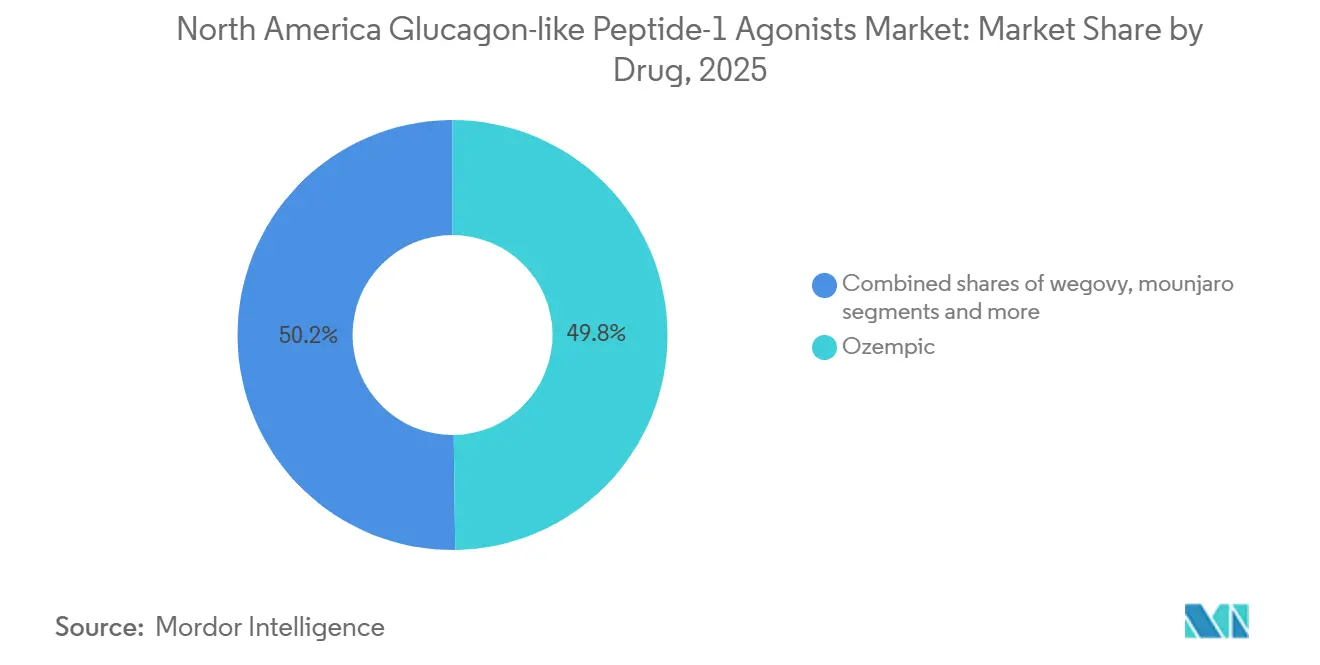

- By drug class, Ozempic led with a 49.8% North America Glucagon-like Peptide-1 agonists market share in 2025, whereas Mounjaro posts the fastest expansion at a 16.87% CAGR through 2031.

- By route, subcutaneous injectables held 85.6% share in 2025; oral formulations carry the highest growth, advancing at a 14.65% CAGR on the back of Rybelsus and orforglipron pipeline momentum.

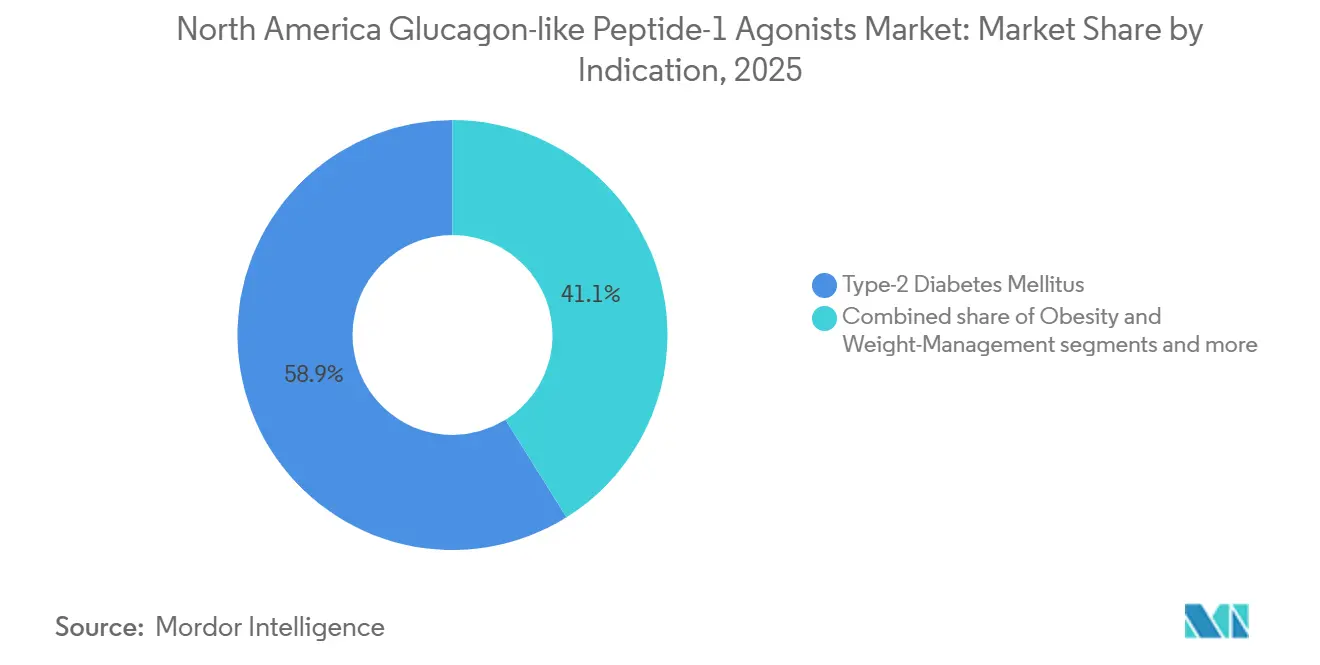

- By indication, Type-2 diabetes mellitus held 58.89% share in 2025, obesity & weight-management advancing at a 13.45% CAGR through 2031.

- By distribution channel, retail and chain pharmacies retained 54.23% share in 2025, while online and DTC platforms accelerate at a 15.82% CAGR through 2031.

- By country, the United States contributed 85.43% of 2025 revenue, whereas Mexico exhibits the strongest trajectory with a 15.10% CAGR as nearshoring expands fill-finish capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Glucagon-like Peptide-1 Agonists Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Type-2 Diabetes Prevalence Escalation | +2.6% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Obesity-Focused Label Expansions and Coverage Gains | +3.0% | United States, Canada | Medium term (2-4 years) |

| Cardiometabolic Outcome-Based Guideline Inclusion | +2.0% | United States, Canada | Medium term (2-4 years) |

| Tele-Prescription and DTC Platforms Accelerate Uptake | +1.8% | United States | Short term (≤ 2 years) |

| Employer-Funded Benefit Designs for Productivity Savings | +1.5% | United States | Medium term (2-4 years) |

| Nearshoring of Fill-Finish Capacity Across Mexico | +1.1% | Mexico, supply benefits to United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Type-2 Diabetes Prevalence Escalation

The Centers for Disease Control and Prevention documented 38.4 million Americans living with diabetes in 2024, of whom up to 95% have type 2 diabetes. Rising adolescent incidence extends lifetime drug utilization horizons, creating multi-decade revenue streams. The American Diabetes Association’s 2025 standards place GLP-1 receptor agonists immediately after metformin for high-risk patients, expanding the eligible pool by roughly 12 million adults [1]American Diabetes Association, “Standards of Care 2025,” diabetes.org. Canada shows a parallel rise, with 11.9 million citizens affected by diabetes or pre-diabetes in 2024. Younger onset increases cardiovascular risk over time, which strengthens the clinical argument for early incretin therapy. Together, these epidemiologic shifts add positive pressure to prescription growth through 2031.

Obesity-Focused Label Expansions and Coverage Gains

The FDA cleared semaglutide for cardiovascular risk reduction in March 2024, which unlocked Medicare Part D coverage because the drug now treats a covered cardiovascular condition rather than obesity alone. In November 2024, the Centers for Medicare & Medicaid Services proposed rules that would extend anti-obesity drug benefits to 7.4 million beneficiaries, opening an untapped payer segment [2]Centers for Medicare & Medicaid Services, “Proposal to Expand Access to Obesity Medications,” cms.gov. Commercial insurers follow a mixed strategy: some demand 12-week lifestyle documentation, whereas others waive step therapy after high-risk scores are confirmed. Employer self-insured plans adopt GLP-1 carve-outs, attracted by modeled 120% returns on investment tied to absenteeism reductions. Expanded benefits sharpen demand visibility and enhance revenue predictability for manufacturers.

Cardiometabolic Outcome-Based Guideline Inclusion

Cardiology, nephrology, and endocrinology societies now unanimously endorse GLP-1 receptor agonists for cardiovascular risk reduction after the SELECT and SOUL trials demonstrated 20% and 14% event reductions, respectively. The World Health Organization added semaglutide to the 2025 essential medicines list, signaling global consensus [3]World Health Organization, “Essential Medicines List 2025,” who.int. In the United States, the American College of Cardiology reclassified semaglutide and tirzepatide as first-line agents for patients with established atherosclerotic disease and obesity in 2025. Health-system formularies responded by raising GLP-1 placement to preferred tiers, giving cardiologists a stronger voice in treatment decisions. Shared decision-making now integrates weight control, glycemic management, and cardiovascular benefit, reinforcing the therapeutic value proposition.

Tele-Prescription and DTC Platforms Accelerate Uptake

Virtual platforms compress the care pathway. Hims & Hers recorded an average 48-hour turnaround from web consultation to medication shipment in 2024. Ro’s asynchronous model enrolled over 100,000 patients by mid-2024, demonstrating scalable clinician capacity. Eli Lilly’s LillyDirect integrates telehealth, independent pharmacies, and home delivery across 49 states, capturing 8% of tirzepatide prescriptions by late 2024. Fast fulfillment appeals to patients facing multi-week waits at traditional clinics. Regulatory scrutiny is tightening; however, the FDA issued warning letters to compounding pharmacies marketing semaglutide despite resolved shortages, a move that may narrow gray-market supply. Balanced oversight will determine whether DTC platforms maintain momentum or revert to conventional dispensing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Drug Cost and Payer Prior-Authorization Hurdles | -2.6% | United States, Canada | Short term (≤ 2 years) |

| Periodic API and Pen-Device Shortages | -1.9% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Tighter Policing of Off-Label Cosmetic Use | -1% | United States | Short term (≤ 2 years) |

| Pipeline Oral Incretin Mimetics Substitute Threat | -1.4% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Drug Cost and Payer Prior-Authorization Hurdles

Wholesale acquisition prices range between USD 935 and USD 1,349 per month in 2026, positioning GLP-1 agonists among the most expensive chronic-care therapies in North America. Pharmacy benefit managers apply layered prior-authorization checks that verify lifestyle modification, body-mass index thresholds, and comorbidity profiles, adding an average 15-day delay to therapy initiation. Prime Therapeutics reported initial denial rates of 42% for GLP-1 requests in 2024, although two-thirds were overturned on appeal with added documentation. High-deductible health plans expose commercially insured patients to USD 150–300 monthly out-of-pocket costs, driving abandonment rates above 30% at first fill. As more outcomes data affirm broader benefits, payers may soften criteria, but cost friction remains the near-term speed limit on market growth.

Periodic API and Pen-Device Shortages

Between 2022 and 2024, the FDA shortage database frequently listed Ozempic, Wegovy, Mounjaro, and Zepbound due to pen-device bottlenecks. Novo Nordisk allocated USD 6 billion to scale its Chartres, France, plant and USD 4.1 billion for a new facility in Clayton, North Carolina, aiming to add 50% more capacity by 2027. Eli Lilly is investing USD 9 billion across four sites to double tirzepatide output by late 2026. While shortages eased in late 2024, recurrent demand spikes could reappear until new lines reach commercial volumes. Interim gaps invite compounded-product alternatives that challenge quality oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug: Mounjaro’s Dual Agonism Redefines Therapeutic Efficacy

The North America Glucagon-like Peptide-1 agonists market size for Mounjaro is poised to expand at a 16.87% CAGR, fueled by 22.5% mean weight reduction in SURMOUNT-1 and superior glycemic control relative to semaglutide. Ozempic kept a 49.8% North America Glucagon-like Peptide-1 agonists market share in 2025 because of its first-mover advantage and positive cardiovascular data from the SELECT trial. Wegovy and Zepbound drew 18% combined revenue in 2025, their growth grounded in fresh cardioprotective labeling and pending Medicare coverage finalization. Rybelsus caters to needle-averse patients, though its fasting rule curbs adherence; orforglipron seeks to remove that barrier when submitted for approval in 2026.

Pipeline candidates are re-shaping competitive contours. Cagrisema, the semaglutide–cagrilintide fixed-ratio mix, reported 27.1% weight loss in REDEFINE-2, while survodutide and retatrutide advance multi-agonist strategies. Trulicity, once a category mainstay, is slipping under patent-expiry shadow as biosimilars queue for 2027. Legacy options such as liraglutide and exenatide are eroding at 6% annually as prescribers pivot to weekly agents with stronger cardiometabolic evidence.

By Route of Administration: Oral Agents Gain Momentum

Subcutaneous injectables command 85.6% of prescriptions due to weekly dosing and well-documented cardiovascular and renal outcomes. Their user-friendly pens, concealed needles, and auto-injector designs help blunt needle aversion. Semaglutide also demonstrated a 24% reduction in kidney disease progression in the FLOW study, reinforcing clinician confidence.

Oral formulations grow at a 14.65% CAGR as patients seek needle-free options. Rybelsus posted USD 1.9 billion global sales in 2024, and its October 2025 cardiovascular indication approval heightened primary-care adoption. The North America Glucagon-like Peptide-1 agonists market size for oral agents is expected to accelerate once orforglipron reaches the market. Patient-preference surveys reveal that 40% of eligible individuals refused injections in favor of tablets when equally effective choices exist. As adherence obstacles, namely, fasting requirements, are ironed out, oral uptake will chip away at injectable dominance.

By Indication: Obesity Applications Outpace Diabetes

Obesity and weight-management prescriptions represent the fastest-moving segment, advancing at a 13.45% CAGR on the heels of expanded labeling and payer adoption. The FDA authorized Wegovy for cardiovascular risk reduction in adults with established cardiovascular disease, allowing Medicare Part D reimbursement, which reshapes the North America Glucagon-like Peptide-1 agonists market size equation for this indication. Commercial insurers layer tiered co-insurance but loosen step therapy once comorbid cardiovascular risk is documented.

Type-2 diabetes still represents 58.89% of revenue in 2025, underpinned by long-standing guideline status and glycemic efficacy. Cardiovascular risk-reduction prescriptions accounted for 12% of 2025 volume yet should reach 22% by 2031, following cardiology guideline alignment. Specialty-level diffusion is visible: cardiologists wrote 8% of GLP-1 scripts in 2024, up from 2% two years earlier. Nephrologists are next in line as FLOW results get embedded into chronic kidney disease management algorithms.

By Distribution Channel: DTC Platforms Disintermediate Traditional Pharmacy Networks

Retail and chain pharmacies held a 54.23% share in 2025; however, DTC platforms climbed at a 15.82% CAGR by promising rapid access and transparent pricing. Hims & Hers enrolled over 40,000 patients in five months, using compounded semaglutide priced 50% below branded injectable alternatives. Eli Lilly’s LillyDirect demonstrates how originators can bypass traditional pharmacy benefit managers while retaining reimbursement acceptance.

Hospital pharmacies dispense 18% of volume, primarily during inpatient stays for hyperglycemia or acute cardiovascular care. They now negotiate value-based contracts linking GLP-1 use to reduced readmission penalties. Retailers combat margin compression by developing virtual consultation arms, yet sustained compounded-product availability hinges on the FDA shortage status. Enforcement actions in late 2024 narrowed compounded supply and may push DTC platforms toward branded sourcing, adding cost pressure but preserving market momentum.

Geography Analysis

The United States leads the region, generating 85.43% of 2025 revenue. Obesity prevalence reached 41.9% among adults during 2017–2020 and is forecast to hit 60.6% by 2050 if trends persist. Employer self-insured plans, covering 64% of workers, model tangible productivity savings, which spur benefit adoption even when PBM rebates remain opaque. If finalized, the 2026 CMS rule will add 7.4 million public beneficiaries, transforming payer mix and volume forecasts. State Medicaid coverage remains fragmented, with unrestricted access in 23 states versus outright exclusions in nine, creating access deserts for low-income populations. FDA approval of oral semaglutide for cardiovascular risk reduction in October 2025 enabled Medicare Advantage plans to list the drug under cardiovascular codes, bypassing obesity exclusions.

Canada exhibits policy heterogeneity due to provincial autonomy. Ontario funds semaglutide and dulaglutide for diabetes under the Ontario Drug Benefit, yet limits Wegovy access to body-mass index above 35 kg/m² with comorbid conditions. Quebec added Wegovy in March 2024, while British Columbia still excludes anti-obesity GLP-1 therapies. CADTH issued positive cost-effectiveness opinions for semaglutide and tirzepatide under diabetes indications, but budget constraints slow uniform uptake. Private insurers cover 78% of employer plans, though step-therapy and prior-authorization add an average 30-day lag before therapy commencement.

Mexico is poised for a 15.10% CAGR through 2031. Nearshoring brings fill-finish plants closer to North American demand, and COFEPRIS utilizes accelerated pathways for biosimilars, as evidenced by Biocon’s liraglutide approval in 2024. Public payers IMSS and ISSSTE reimburse GLP-1 agonists only for diabetes, excluding obesity, yet rising private insurance penetration in the expanding middle class is widening access. Novo Nordisk singled out Mexico as its largest Latin American market in 2024, and Eli Lilly intends to localize manufacturing to bolster regional resilience. Currency fluctuations pose a pricing challenge, but domestic production and biosimilar entry may temper import costs.

Competitive Landscape

Novo Nordisk and Eli Lilly held a majority of shares in 2025. Both companies run aggressive capital-spending programs totaling more than USD 20 billion between 2024 and 2026 to double semaglutide and tirzepatide output. Novo Nordisk’s Clayton, North Carolina, site and Eli Lilly’s Indiana and Ireland plants anchor regional supply chains. Pipeline innovation intensifies rivalry. Amgen’s MariTide achieved 20% weight loss with monthly dosing, aiming to extend intervals even further in Phase 3. Viking Therapeutics’ VK2735 delivered double-digit weight reductions in both injectable and oral forms, signaling future multisource pressure.

Boehringer Ingelheim and Zealand Pharma commenced Phase 3 SYNCHRONIZE trials for survodutide, a dual GLP-1/glucagon agonist, targeting both obesity and metabolic dysfunction-associated steatohepatitis. Roche’s 2023 acquisition of Carmot Therapeutics injected fast-follower oral assets into its pipeline, adding another heavyweight to the fray. Biosimilar developers Biocon, Viatris, and Samsung Bioepis plan dulaglutide and liraglutide offerings as patents expire in 2027, although complex peptide synthesis may limit penetration to 15%–20% of legacy-agent volume.

White-space segments attract strategic bets. Pediatric obesity remains under-served, despite Wegovy adolescent approval in 2022. Non-alcoholic steatohepatitis shows promise following survodutide’s 47% resolution rate in Phase 2, and chronic kidney disease is emerging as a major downstream indication based on FLOW outcomes. As incumbent leaders broaden labels, they also license complementary mechanisms such as amylin analogs and glucagon agonists to reinforce position before biosimilar erosion begins.

North America Glucagon-like Peptide-1 Agonists Industry Leaders

Astrazeneca

Sanofi

Eli Lilly and Company

Pfizer Inc.

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Novo Nordisk released Phase 3 REDEFINE-2 results showing 27.1% mean weight loss with Cagrisema at 68 weeks, and plans regulatory submission in Q2 2026.

- December 2025: The FDA approved the once-daily oral Wegovy pill (semaglutide 25 mg) for long-term weight reduction and cardiovascular risk mitigation.

- December 2025: Eli Lilly announced positive topline data from TRIUMPH-4, where retatrutide improved weight, pain, and function in adults with obesity and knee osteoarthritis.

North America Glucagon-like Peptide-1 Agonists Market Report Scope

As per the scope of the report, Glucagon-like peptide-1 (GLP-1) receptor agonists are a class of medications that mimic the incretin hormone naturally secreted by the intestines in response to food intake. These agents primarily manage blood sugar levels in patients with Type 2 diabetes by stimulating glucose-dependent insulin secretion, suppressing glucagon release, and improving insulin sensitivity. Beyond glycemic control, they are widely utilized for chronic weight management in patients with obesity or overweight and at least one weight-related comorbidity.

The North American glucagon-like peptide-1 agonists market is segmented by drug, route of administration, indication, distribution channel, and geography. By drug, the market is categorized into Ozempic, Wegovy, Mounjaro, Zepbound, Rybelsus, Trulicity, Orforglipron, Cagrisema, Survodutide, and others. By route of administration, the market is categorized into subcutaneous injectable and oral tablet. By indication, the segmentation includes type-2 diabetes mellitus, obesity & weight management, and cardiovascular risk reduction. By distribution channel, the segmentation includes hospital pharmacies, retail & chain pharmacies, and online / direct-to-consumer platforms. Geographically, the market is segmented across the United States, Canada, and Mexico. For each segment, the market size and forecast are provided in terms of value (USD).

By Drug

| Ozempic |

| Wegovy |

| Mounjaro |

| Zepbound |

| Rybelsus |

| Trulicity |

| Orforglipron |

| Cagrisema |

| Survodutide |

| Others |

By Route of Administration

| Sub-cutaneous Injectable |

| Oral Tablet |

By Indication

| Type-2 Diabetes Mellitus |

| Obesity & Weight-Management |

| Cardiovascular Risk Reduction (ASCVD) |

By Distribution Channel

| Hospital Pharmacies |

| Retail & Chain Pharmacies |

| Online / Direct-to-Consumer Platforms |

By Country

| United States |

| Canada |

| Mexico |

| By Drug | Ozempic |

| Wegovy | |

| Mounjaro | |

| Zepbound | |

| Rybelsus | |

| Trulicity | |

| Orforglipron | |

| Cagrisema | |

| Survodutide | |

| Others | |

| By Route of Administration | Sub-cutaneous Injectable |

| Oral Tablet | |

| By Indication | Type-2 Diabetes Mellitus |

| Obesity & Weight-Management | |

| Cardiovascular Risk Reduction (ASCVD) | |

| By Distribution Channel | Hospital Pharmacies |

| Retail & Chain Pharmacies | |

| Online / Direct-to-Consumer Platforms | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will the North America Glucagon-like Peptide-1 agonists market be in 2026?

The North America Glucagon-like Peptide-1 agonists market size is expected to reach USD 32.43 billion in 2026 and is projected to reach USD 60.12 billion by 2031, registering a 13.14% CAGR over the forecast period.

What is driving faster growth in obesity prescriptions?

Cardiovascular outcome data, expanded FDA labeling, and a proposed CMS rule that widens Medicare and Medicaid coverage are accelerating obesity-focused uptake.

Which drug leads current sales?

Ozempic holds the largest share of revenue in 2025, although Mounjaro records the fastest growth through 2031.

How are oral formulations affecting market dynamics?

Oral agents such as Rybelsus are expanding at a 14.65% CAGR and are expected to gain further traction when orforglipron launches.

Why is Mexico the fastest-growing geography?

Nearshoring of fill-finish facilities, COFEPRIS biosimilar approvals, and expanding private insurance are propelling a 15.10% CAGR in Mexico.

Page last updated on: