Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

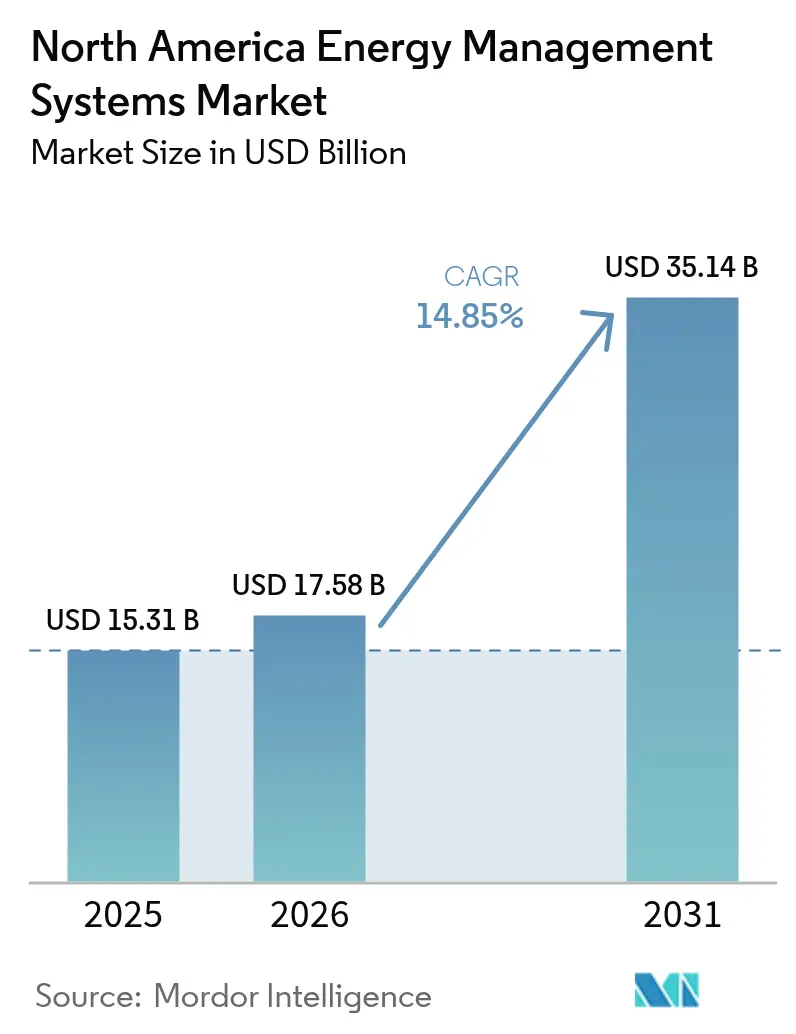

| Base Year Market Size (2025) | USD 15.31 Billion |

| Market Size (2026) | USD 17.58 Billion |

| Market Size (2031) | USD 35.14 Billion |

| Growth Rate (2026 - 2031) | 14.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Energy Management Systems Market Analysis by Mordor Intelligence

North America energy management systems market size in 2026 is estimated at USD 17.58 billion, growing from 2025 value of USD 15.31 billion with 2031 projections showing USD 35.14 billion, growing at 14.85% CAGR over 2026-2031. The doubling of value in just five years underlines the region’s swift shift toward intelligent, software-defined infrastructure that cuts emissions and optimizes power use. Federal incentives, corporate net-zero mandates, and rapid advances in AI-enabled optimization tools are the primary forces behind this rise. US dominance, the cloud pivot, and wireless connectivity all accelerate adoption by shrinking payback periods. At the same time, mid-sized enterprises and public institutions unlock fresh savings through performance-based contracts that transfer risk to service providers. Rising data-center loads, strengthened building codes, and dynamic utility tariffs further widen the addressable pool for the North America energy management systems market.

Key Report Takeaways

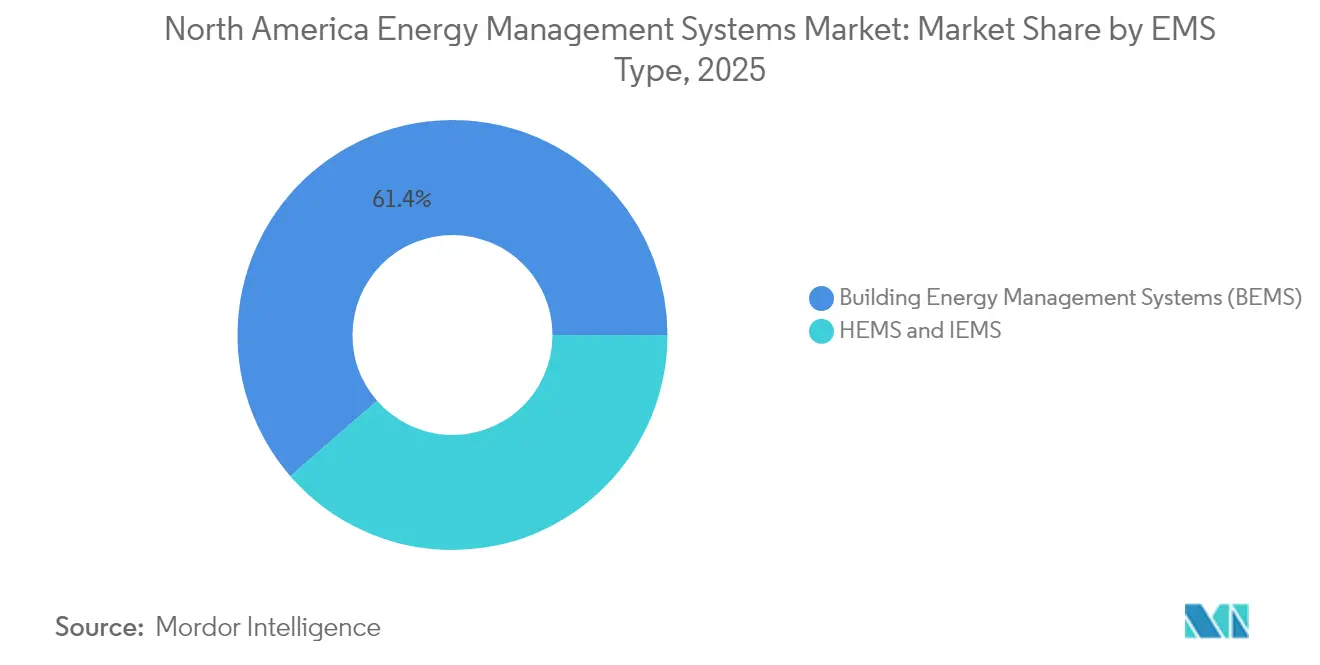

- By EMS type, Building Energy Management Systems led with 61.40% revenue share in 2025, while Home Energy Management Systems are on track for the fastest 16.72% CAGR through 2031.

- By component, services held the largest 42.60% share of the North America energy management systems market size in 2025 and are expanding at a 16.55% CAGR.

- By deployment mode, on-premise solutions accounted for 67.20% share in 2025; cloud models post the strongest 16.30% CAGR to 2031.

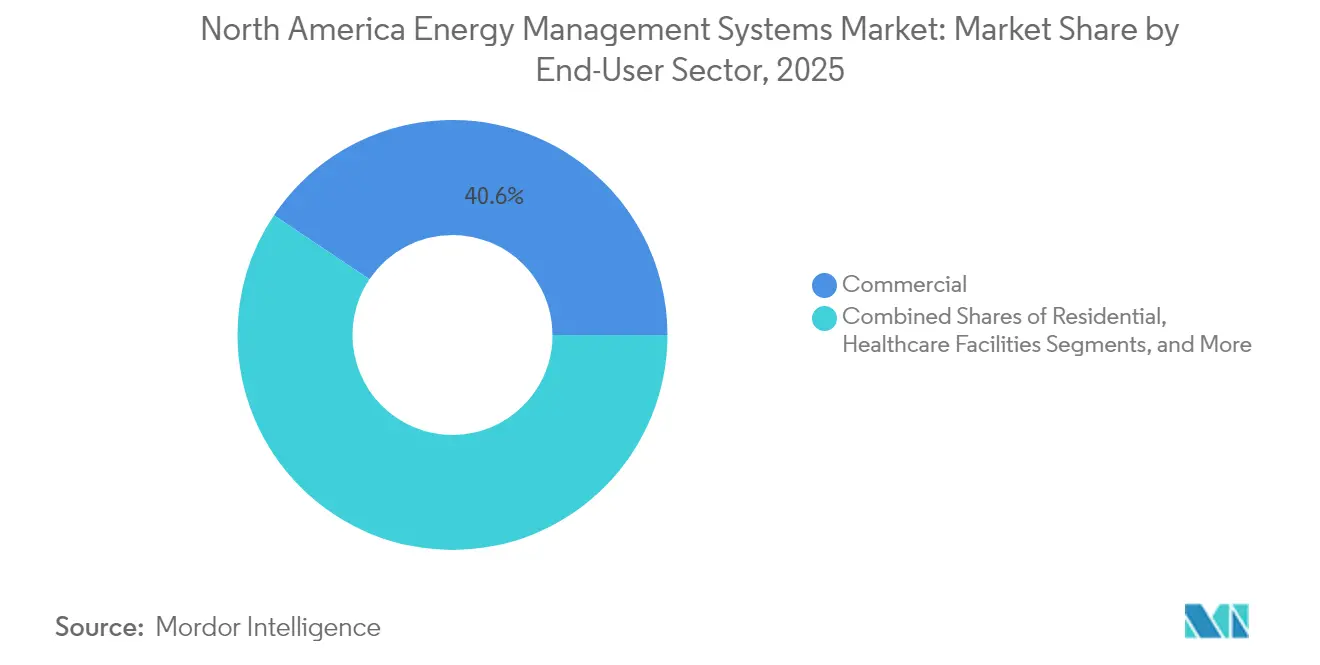

- By end-user sector, commercial facilities commanded 40.60% of the North America energy management systems market share in 2025, whereas the residential segment shows a robust 15.74% CAGR outlook.

- By communication technology, wired protocols retained 56.40% share in 2025; wireless options move ahead at a 15.98% CAGR.

- By country, the United States contributed an 87.50% share in 2025, while Canada is forecast to deliver a 15.92% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Energy Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing electricity prices and sustainability commitments | +2.8% | North America, strongest in California and the Northeast | Medium term (2-4 years) |

| Stringent energy-efficiency regulations and building codes | +2.1% | US federal and state levels; Canadian provincial mandates | Long term (≥ 4 years) |

| Smart-grid roll-outs and AMI penetration | +3.2% | US nationwide; Canadian urban centers; Mexican modernization zones | Medium term (2-4 years) |

| US Inflation Reduction Act retrofit incentives | +4.1% | United States nationwide; spillover in border regions | Short term (≤ 2 years) |

| Corporate VPP and net-zero procurement strategies | +1.9% | North America, concentrated in tech and manufacturing hubs | Medium term (2-4 years) |

| Dynamic real-time utility tariffs | +1.4% | California, Texas, Northeast US, Ontario Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

US Inflation Reduction Act Retrofit Incentives

Generous tax credits and rebates under the USD 370 billion Inflation Reduction Act cut retrofit payback periods and spur immediate procurement of networked controls and analytics platforms. Commercial buildings can now deduct up to USD 5.00 per square foot of qualifying upgrades, while states such as California have secured USD 291 million to deliver whole-home rebates that target 20-35% savings.[1]Internal Revenue Service, “Section 179D Commercial Buildings Energy Efficiency Tax Deduction,” irs.gov Domestic production credits encourage local EMS hardware output and cushion supply chains. As evidence, Johnson Controls reports USD 8.4 billion in customer savings created by performance contracts that ride on federal and state incentive stacks.

Smart-Grid Roll-outs and AMI Penetration

Utilities invested USD 320 billion in grid upgrades during 2023, including USD 50.9 billion for distribution assets that host advanced metering infrastructure.[2]US Energy Information Administration, “Electric Power Annual 2023,” eia.gov AMI data feeds granular load curves into AI engines embedded in modern platforms and enables virtual power plant (VPP) participation. The US Department of Energy projects 80-160 GW of VPP capacity by 2030. Edge analytics shrinks response times by up to 92%, letting buildings monetize flexibility while preserving occupant comfort. Mexico’s USD 23 billion grid program adds cross-border demand for compatible solutions.

Corporate VPP and Net-Zero Procurement Strategies

Enterprises signed 67 GW of clean-energy power-purchase agreements in 2024 worth USD 115 billion. Aggregated DER fleets managed by EMS platforms unlock new revenue and hedge price risk. NYU Langone Health, for example, deploys 20,600 sensors and has saved USD 76 million in energy since 2008 while cutting emissions 16% even as its footprint expanded. Battery-integrated EMS configurations generate yearly savings above USD 900 where time-of-use tariffs prevail.[3]arXiv, “Edge2LoRa Architecture for Industrial Monitoring,” mdpi.com

Dynamic Real-Time Utility Tariffs

Time-varying rates that update every 30 minutes reward automated load shifting. California’s large-power dynamic pricing program highlights the upside as buildings optimize HVAC, lighting, and storage dispatch against live price curves. Complex structures with peak premiums outperform flat tariffs in harvesting renewable value, provided EMS platforms possess sub-minute controls and AI forecasting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and O&M costs | -1.8% | North America, particularly affecting SME adoption | Short term (≤ 2 years) |

| Data-security and privacy concerns | -1.2% | US and Canada, heightened in critical infrastructure | Medium term (2-4 years) |

| Integrator skill-set shortage | -0.9% | North America, acute in rural and secondary markets | Long term (≥ 4 years) |

| Fragmented legacy protocols and interoperability gaps | -0.7% | Legacy building stock; industrial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and O&M Costs

Turnkey systems for mid-sized offices can surpass USD 50,000 before maintenance fees, and life-cycle costs often climb to five times the initial outlay. Residential buyers feel the pinch even more sharply when local incentives are limited. Energy-as-a-service contracts mitigate risk: Cobb County’s USD 7.1 million deal guarantees USD 2 million utility savings over 20 years. Still, semiconductor shortages and the capital demands of cleaner chip fabrication inflate hardware prices in the near term.

Data-Security and Privacy Concerns

Utilities logged over 1,100 cyberattacks a week in 2022, forcing operators to harden defenses. IoT endpoints, cloud gateways, and DER controllers all widen the surface area. Zero-trust architectures, network segmentation, and blockchain-based authentication are becoming standard, yet implementation costs and skills gaps remain hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By EMS Type: Home Platforms Accelerate Residential Savings

Building Energy Management Systems retained a commanding 61.40% share of the North America energy management systems market in 2025, anchored by large commercial portfolios that prize operational transparency and tenant comfort. Yet Home Energy Management Systems are scaling swiftly on the back of smart-speaker ubiquity, utility rebates, and maturing interoperability standards. The segment’s 16.72% CAGR through 2031 makes it the most disruptive pocket of the North America energy management systems market.

Annual data show HEMS installations reducing household consumption by more than 20% once machine-learning algorithms adjust HVAC and appliance schedules. Matter protocol adoption simplifies device pairing and propels mainstream appeal. Industrial EMS offerings occupy a middle niche, providing process-specific analytics and compliance dashboards for heavy manufacturing clients. Collectively, these dynamics keep the North America energy management systems market diversified and resilient.

By Component: Services Anchor Outcome-Based Models

Services captured 42.60% share in 2025 and delivered the highest 16.55% CAGR to 2031, underscoring a decisive tilt away from one-off hardware deals toward continuous optimization agreements. Recurring revenue streams cover monitoring, analytics, and guaranteed-savings contracts that shift performance risk to providers. Hardware is indispensable but increasingly commoditized, while cloud software layers create value through predictive controls.

Service-led engagements often bundle financing, retro-commissioning, and operator training, forming an integrated pathway to energy-as-a-service delivery. Limbach Holdings uses data-driven reviews to uncover hundreds of actionable insights per site, illustrating how analytics skills eclipse pure equipment know-how. These developments sustain the North America energy management systems market momentum even when capital budgets tighten.

By Deployment Mode: Cloud Gains Ground on Legacy On-Premise

On-premise deployments held 67.20% of the North America energy management systems market in 2025 for critical facilities that demand maximum data control. Cloud models grow at 16.30% CAGR as enterprises recognize the scalability and AI horsepower offered by centralized servers. Edge-enabled hybrids combine the best of both worlds, running latency-sensitive loops locally while pushing bulk analytics to the cloud.

Cloud uptake cuts capital outlays and accelerates software upgrades. The PHOENIX pilot cut peak energy by 86% in Greek sites through machine-learning forecasts. Edge nodes, meanwhile, keep response times within operational thresholds even when connectivity falters, maintaining system resilience across the North America energy management systems market.

By End-User Sector: Residential Momentum Challenges Commercial Supremacy

Commercial buildings generated 40.60% of revenue in 2025 owing to large, managed portfolios and tight payback governance. Residential clients, however, register the quickest 15.74% CAGR, buoyed by smart-appliance integration and aggressive demand-response programs. Industrial plants adopt EMS chiefly for process stability and regulatory adherence, whereas healthcare and education carve out niche demand based on constant-operation schedules.

Smart-home predictive models now hit Mean Absolute Percentage Error rates below 5% on energy forecasts, making automation trustworthy for everyday users. Hospitals like Klickitat Valley Health adopt hydrogen backup systems integrated with facility automation to balance resilience and carbon goals. These use cases diversify demand within the North America energy management systems market and buffer it from sector-specific swings.

By Communication Technology: Wireless Jumps Ahead in Retrofits

Wired protocols such as BACnet and Modbus kept a solid 56.40% share in 2025 thanks to proven reliability in mission-critical estates. Still, wireless solutions post a 15.98% CAGR by slashing installation labor and enabling sensor density in retrofits where conduit runs are impractical. LoRaWAN and other LPWAN options extend coverage in warehouses and campuses while sipping power.

Edge2LoRa demonstrations report 91.60% lower bandwidth use and 92% faster local processing versus cloud-only frameworks. As 5G rolls out, ultra-low-latency control loops become feasible, opening pathways for autonomous fault detection across the North America energy management systems market.

Geography Analysis

The United States forms the gravitational center of the North America energy management systems market, commandeering 87.50% of spending in 2025. Early smart-grid outlays, a USD 370 billion federal stimulus for clean energy, and a data-center construction boom supply steady demand. Power-sector capital expenditures hit USD 320 billion in 2023, funneling funds to AMI deployments and grid-interactive building programs. California leads in dynamic pricing, while the Northeast enforces stringent building-performance ordinances that trigger system upgrades. Vertiv alone disclosed USD 5.5 billion in orders tied to data-center efficiency, illustrating how digital-economy expansion sustains EMS growth.

Canada emerges as the quickest climber in the North America energy management systems market, thanks to CAD 92 billion earmarked for generation, transmission, and clean-tech projects. The pipeline spans 223 planned initiatives valued at CAD 294 billion and another 120 under construction worth CAD 180 billion. Provincial programs in Ontario, Alberta, and British Columbia bake EMS requirements into building codes, providing a predictable compliance tailwind. Rising renewable penetration and grid-balancing needs reinforce the call for sophisticated control platforms.

Mexico rounds out the regional picture with reform-driven policy momentum. The 2024-2030 National Strategy allocates USD 23 billion for 51 projects that add 22 GW of capacity and aim for 45% clean energy by 2030. Planned transmission and distribution upgrades worth USD 11 billion demand intelligent controls capable of handling bidirectional flows. Grid Code 2.0 pushes industrial sites to adopt real-time monitoring and power-quality solutions, injecting further volume into the North America energy management systems market.

Regulatory Landscape

In the United States, energy management systems adoption is shaped by federal energy-management requirements for public facilities and grid-modernization authorities administered by the US Department of Energy (DOE), including frameworks originating in the Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007. DOE Office of Electricity published its Strategic Plan on March 31, 2026, reinforcing priorities around grid resilience and modernization that depend on advanced monitoring, automation, and interoperable data exchange between utilities and behind-the-meter assets.

In Canada, the regulatory trajectory is shifting toward updated efficiency rules and clearer incorporation of technical standards into enforceable requirements. Canada has proposed changes such as Amendment 19 to the Energy Efficiency Regulations, 2016 (June 2026 publication cycle), and Bill S-4 in Parliament to amend the Energy Efficiency Act, including provisions that enable regulation of energy-related systems through standards incorporated by reference. This tightens compliance pathways for connected controls and energy management functionality.

Value Chain Analysis

The value chain covers device and controls hardware (sensors, meters, panels, controllers), communications and integration layers (wired building protocols and utility interfaces), EMS software (analytics, optimization, reporting, and dispatch), and service delivery (design, commissioning, cybersecurity hardening, monitoring, and outcome-based performance contracts). Utilities and regulators shape interoperability and data-exchange requirements, and grid modernization programs increase the need for standardized interfaces and coordinated operation across the grid edge.

Recent partnerships show the chain moving toward software-defined, cloud-integrated architectures that connect homes and buildings with utility platforms. SPAN and Landis+Gyr, for example, expanded integration between an intelligent service point and AMI/DERMS platforms (March 2025), while Carrier partnered with Google Cloud to apply AI analytics to home energy management and grid resilience use cases (March 2025). Work around grid-edge visibility and non-wires alternatives, including Itron and Schneider Electric with Microsoft solutions (March 2025), points to tighter extraction of capacity from existing infrastructure, particularly where long lead times for physical equipment slow conventional upgrade cycles.

Competitive Landscape

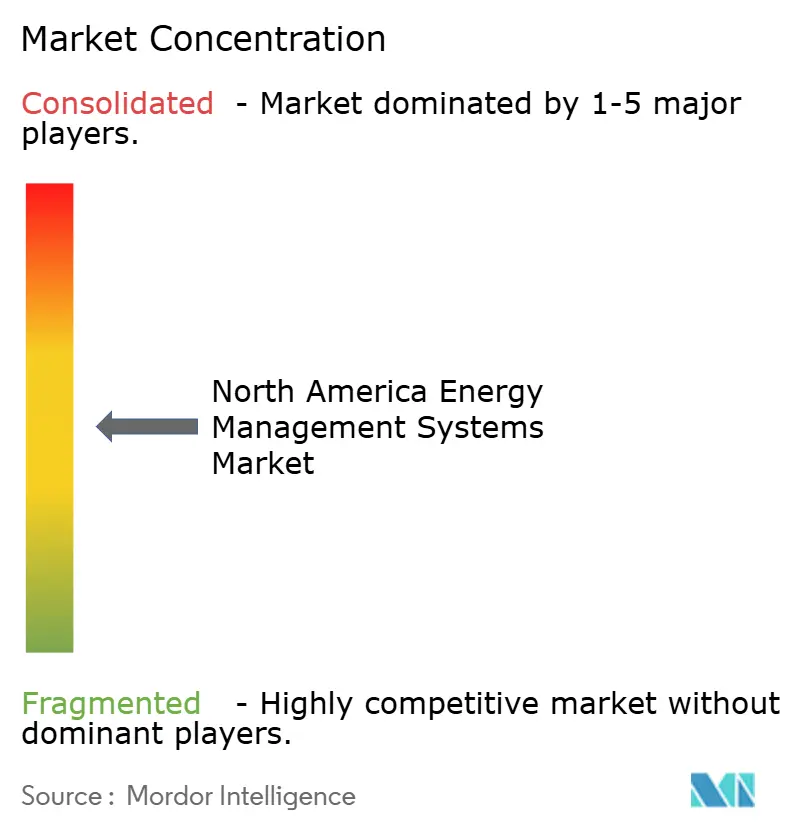

The North America energy management systems market shows moderate concentration, with the largest incumbents leveraging deep service networks while cloud-native entrants chip away on software prowess. Johnson Controls, Honeywell, Siemens, and Schneider Electric anchor the top tier, each coupling extensive installed bases with evolving AI toolkits. Johnson Controls posted 10% organic sales growth in Q1 FY25 and sits on a USD 13.2 billion backlog, proof that outcome-focused contracts resonate with owners.

Schneider Electric is plowing USD 700 million into US manufacturing through 2027 to sharpen its data-center and utility portfolio, adding over 1,000 domestic jobs. Honeywell emphasizes automation and energy transition themes in its latest proxy, signaling continued play in building controls. Siemens invests in edge analytics and open-protocol ecosystems to defend share against nimble SaaS challengers. Patent filings cluster around demand-response algorithms, multi-energy control schemes, and thermal management for ESS, marking innovation hotspots critical to next-generation competitiveness.

Start-ups focus on narrow pain points such as tenant billing accuracy, asset-level analytics, or cyber-secure device onboarding. Partnerships between utilities and software houses multiply as VPP aggregation becomes mainstream. Overall, strategic differentiation tilts toward AI depth, cybersecurity robustness, and the ability to wrap financing around guaranteed savings—traits that decide wins in the North America energy management systems market.

North America Energy Management Systems Industry Leaders

Johnson Control International PLC

Honeywell International Inc.

Siemens AG

Schneider Electric SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Utility and grid-investment cycles are opening concrete whitespace for EMS platforms that can function as grid-edge orchestrators, beyond facility dashboards. In February 2026, Oncor announced an approximately USD 47.5 billion base capital plan for 2026-2030 in Texas. In May 2026, MISO selected a consortium including Ameren Transmission Company of Illinois and GridLiance Heartland to deliver major 765-kV transmission projects in Illinois. Together, these steps highlight the scale of modernization underway and the operational need for demand flexibility, telemetry, and controllability across connected loads.

Canada adds a parallel opportunity set tied to more formal energy-management adoption and standardization in commercial and institutional buildings. NRCan is offering financial assistance from April 2026 to March 2029 for implementing ISO 50001 energy management systems in commercial and institutional facilities, with higher cost-share support for not-for-profit organizations. Programs such as 50001 Ready Canada provide an ISO 50001-aligned pathway without mandatory third-party audits. These initiatives broaden the addressable base for EMS software, measurement and verification services, and integration partners that bundle implementation support with ongoing optimization and reporting.

Recent Industry Developments

- June 2026: Johnson Controls launched Metasys 16.0, updating its building automation platform with integrated, real-time visibility into energy, emissions, and peak load. The release strengthens OpenBlue-aligned workflows that connect monitoring and control to operational reporting, supporting customers managing dynamic tariffs and sustainability metrics.

- September 2025: Honeywell introduced the Ionic Modular All-in-One battery energy storage system for commercial and industrial users, bundling storage hardware with integrated control and energy management software. The launch expands EMS use cases into behind-the-meter storage optimization and demand management by linking facility controls with resilience and cost-reduction objectives.

- May 2024: Honeywell partnered with Enel North America to integrate building automation with demand response programs for commercial and industrial load management. The collaboration connects EMS-driven control at the facility level with grid services, widening monetization pathways for flexible loads and accelerating utility-aligned deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers energy management systems used in North America to measure, monitor, and optimize energy use and related operating performance in buildings, homes, industrial sites, and utility-linked environments, including the supporting software, hardware, and services sold for these systems.

Scope exclusions: We exclude standalone electrical components and general IT infrastructure that do not perform energy monitoring, analytics, or control as a defined EMS offering.

Segmentation Overview

- By EMS Type

- Building Energy Management Systems (BEMS)

- Home Energy Management Systems (HEMS)

- Industrial Energy Management Systems (IEMS)

- By Component

- Hardware

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud-based

- Edge / Hybrid

- By End-User Sector

- Commercial

- Industrial and Manufacturing

- Residential

- Healthcare Facilities

- Education Campuses

- Utilities and Energy Providers

- By Communication Technology

- Wired (BACnet, Modbus, etc.)

- Wireless (Zigbee, Wi-Fi, Bluetooth, Z-Wave)

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map regional demand drivers and to anchor the model with observable indicators that can be checked year over year. We mainly relied on public sources such as US DOE publications, the US Energy Information Administration for energy consumption trends, ENERGY STAR and ASHRAE references for building energy performance guidance, and Statistics Canada for supporting macro indicators where relevant.

To keep the model aligned with commercial reality, we also reviewed company annual reports, investor presentations, product documentation, reputable press releases, and public utility and state-level program updates tied to energy efficiency and grid modernization. In addition, we referenced paid subscriptions we hold for company financials and intelligence, patent databases, and an import and export shipment-level database to cross-check supplier activity and category movement. The desk sources listed here are illustrative only, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with OEM and software-side stakeholders, system integrators, channel partners, and end users that buy and operate EMS across commercial buildings, industrial facilities, and utility-adjacent programs. Because the scope is North America, respondent input was balanced across the United States, Canada, and Mexico so assumptions on adoption pace, pricing, and deployment mix could be checked against local purchasing patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 53% | Functional/Unit leaders: 36% | |

| Smaller Players: 19% | Managers: 50% |

Market-Sizing & Forecasting

Sizing started from a top-down build that reconstructs addressable spend using North America energy consumption and efficiency activity signals, then applies EMS adoption and spending intensity by key use environment. When the logic is laid out, the final number depends on how many sites are likely to deploy EMS, what gets deployed (software, hardware, and services), and the typical replacement and expansion cycle that follows.

To keep the model grounded, we used inputs such as the rate of commercial and industrial energy efficiency program activity, smart meter and grid modernization rollout signals, the share of cloud-based deployments versus on-premise, average contract sizes by facility type, and observed integration needs with building controls and industrial automation. The results were then corroborated with selective bottom-up approximations such as sampled average selling price times estimated project volumes from integrator channel checks, plus revenue reasonableness checks from a set of active suppliers where public reporting allowed it. When bottom-up visibility was incomplete, gaps were handled using proxy ratios (for example, services-to-software mix) that were validated in interviews.

For forecasting, scenario analysis was used, supported by expert consensus on how energy prices, policy support for efficiency, retrofit activity, and digitalization budgets are expected to move. Growth rates were adjusted when leading indicators did not move in the same direction, which helped avoid extending historical curves without adjustment.

Data Validation & Update Cycle

Model outputs were triangulated against independent signals, then reviewed for variance by country (United States, Canada, and Mexico) and by major use environment so any outsized jumps could be explained or corrected. Outliers were flagged, assumptions were revisited, and follow-up calls were triggered when primary inputs conflicted with observable public data.

Before sign-off, the work goes through multi-step analyst checks, including internal peer review of the calculation flow and a final sanity check against known market constraints such as deployment lead times and typical budget cycles. Reports are refreshed annually, with interim updates when material events change demand or pricing assumptions, and a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's North America Energy Management Systems Market Size Compared With Other Published Estimates

Published market sizes for North America energy management systems often do not match because each source draws the boundary of what counts as an EMS offering in its own way, and then selects different years and price assumptions to convert activity into revenue. Differences also show up when one publisher treats services and integration as a large part of the market, while another keeps scope tighter around core systems.

Utility modernization signals, building retrofit activity, and the observed shift toward cloud deployments are the evidence checks that keep Mordor Intelligence's estimate aligned to EMS revenue tied to definable monitoring and control use cases, rather than broader energy management spending. When scope is expanded to include adjacent demand response platforms or wider sustainability management software, the total typically rises, and it can also move when currency timing and base-year selection are not handled consistently across North America.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.31 B (2025) | |

| Global Consultancy A | USD 17.72 B (2024) | Uses an earlier base year and a system definition that more explicitly rolls industrial, building, and home EMS together, which can lift totals when integration-heavy categories are counted at a higher share. |

| Industry Publisher B | USD 35.70 B (2025) | Tracks a wider "energy management" spending pool that can include adjacent platforms and programs beyond EMS, which increases the counted revenue base even if core EMS deployments grow at a similar pace. |

The spread in the table mainly comes from scope and base-year handling, not from a disagreement that EMS demand is growing in North America. By keeping inclusions tied to definable EMS deployments and cross-checking the implied spend against independent activity signals, the estimate stays easier to replicate and explain when clients test assumptions.

Key Questions Answered in the Report

What is the current value of the North America energy management systems market?

The market is valued at USD 17.58 billion in 2026 and is forecast to reach USD 35.14 billion by 2031 at a 14.85% CAGR.

Which EMS segment is expanding the fastest?

Home Energy Management Systems show the quickest 16.72% CAGR through 2031, driven by smart-home device adoption and utility demand-response programs.

Why are services gaining such a large share of spending?

Services capture 42.60% of 2025 revenue because owners favor outcome-based contracts that guarantee savings and include continuous optimization.

How does the Inflation Reduction Act influence EMS uptake?

The Act’s tax credits and rebates cut retrofit costs and enable both residential and commercial buildings to accelerate installations, adding up to +4.1% to forecast CAGR.

Which country is the fastest-growing EMS market in North America?

Canada leads with a 15.92% CAGR outlook, supported by CAD 92 billion in energy investments and a 2035 net-zero grid goal.

What are the primary risks facing EMS deployments today?

High upfront costs, semiconductor supply constraints, and cybersecurity threats are the most significant barriers, each shaving points off the growth trajectory.

Page last updated on: