Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

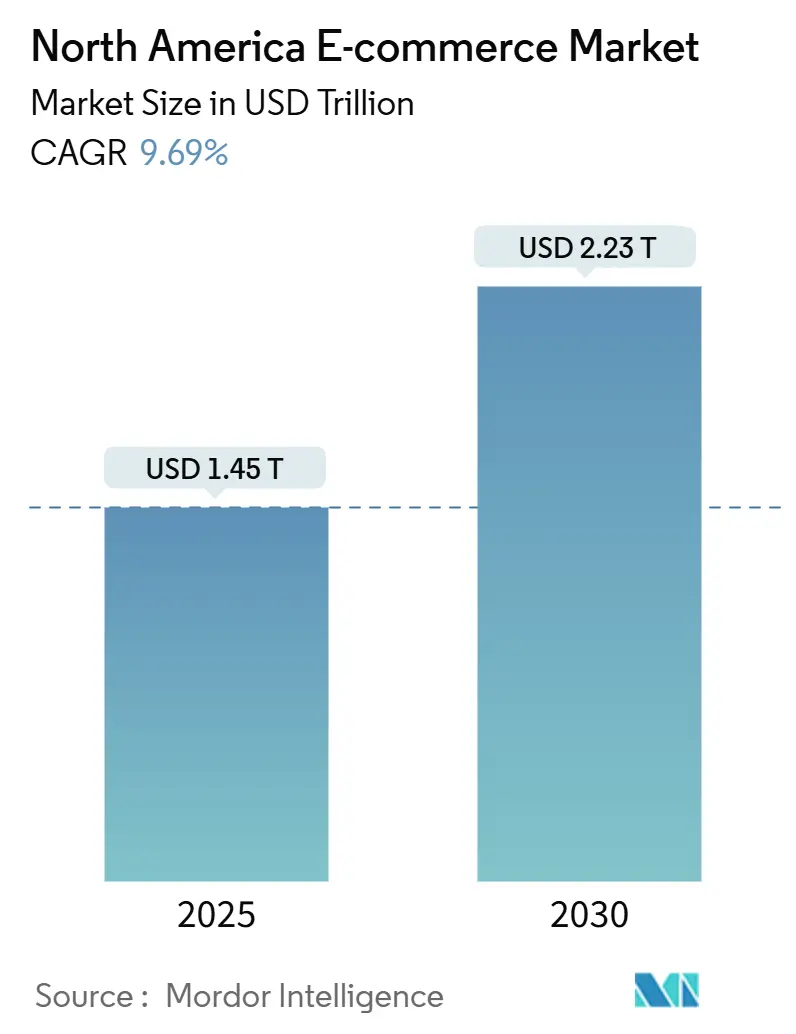

| Market Size (2025) | USD 1.45 Trillion |

| Market Size (2030) | USD 2.23 Trillion |

| Growth Rate (2025 - 2030) | 9.69% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America E-commerce Market Analysis by Mordor Intelligence

The North America e-commerce market stands at USD 1.45 trillion in 2025 and is projected to reach USD 2.23 trillion by 2030 after advancing at a 9.69% CAGR during 2025-2030. Consumers are shifting large portions of their retail budgets online because the region’s digital infrastructure supports friction-free purchase journeys, rapid fulfillment, and sophisticated data-driven personalization. Competitive pressure has intensified as retailers synchronize in-store inventory with online catalogs, turning omnichannel convenience into the baseline expectation. Investments in last-mile automation, micro-fulfillment nodes, and embedded finance are lowering operational bottlenecks that previously constrained growth. Meanwhile, regulatory change and data-privacy mandates are forcing companies to rebuild consent frameworks so that personalization remains effective without violating emerging rules.

Key Report Takeaways

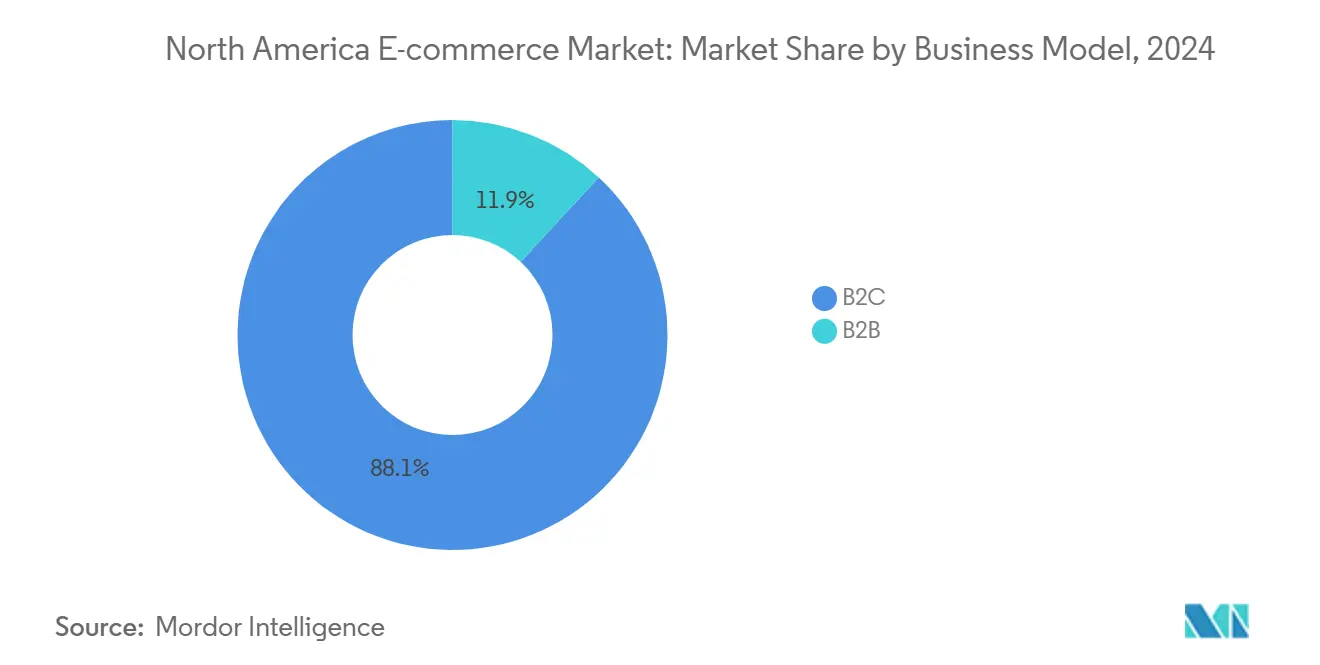

- By business model, the B2C segment held 88.09% of the North America e-commerce market share in 2024, while B2B is projected to register the highest CAGR at 12.1% through 2030.

- By device type, mobile commerce accounted for 72.01% of transactions in 2024 and is advancing at a 10.3% CAGR to 2030.

- By payment method, digital wallets captured 45.21% share of the North America e-commerce market size in 2024; Buy Now, Pay Later is set to grow at 16.2% CAGR through 2030.

- By B2C product category, consumer electronics led with 34.06% revenue share in 2024; food and beverages is forecast to expand at a 16.2% CAGR to 2030.

- By geography, the United States dominated with 87.12% share of the North America e-commerce market size in 2024, while Mexico is the fastest-growing territory at a 13.4% CAGR between 2025-2030.

North America E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-commerce apps with same-day fulfillment | +2.5% | United States major metros; Canadian spillover | Short term (≤ 2 years) |

| Gen-Z BNPL surge | +2.1% | Canada primary; United States secondary | Medium term (2-4 years) |

| USMCA-enabled customs simplification | +1.8% | United States, Canada, Mexico | Medium term (2-4 years) |

| Retail-media networks lifting D2C conversion | +1.7% | United States primary; Canada secondary | Short term (≤ 2 years) |

Source: Mordor Intelligence

Mobile-commerce apps with same-day fulfillment in U.S. urban centers

Mobile transactions already generate 60% of online sales, and retailers that connect smartphone checkouts to dense micro-fulfillment hubs now deliver thousands of SKUs within hours.[1]Pine Labs Research Team, “Mobile Commerce Share Of E-Commerce Sales In North America,” Pine Labs, pinelabs.com Same-day service neutralizes the immediacy advantage of physical stores, trims last-mile expenses by up to 30%, and locks in loyalty among convenience-driven shoppers. The North America e-commerce market is therefore seeing a rush of investment into city-center warehouses, routing algorithms, and gig-driver pools. Brands that fail to replicate these service levels risk losing urban millennials who exhibit low brand stickiness when delivery speed disappoints. Over the next two years, the resulting uplift could add 2.5 percentage points to the overall growth rate of the North America e-commerce market.

Surge of Buy Now, Pay Later adoption among Gen-Z in Canada

BNPL volume is forecast to hit USD 175 billion in North America during 2025, with Canadian Gen-Z consumers accounting for a disproportionate share. Orders financed through BNPL checkouts record 33% higher average ticket sizes and 40% lower cart abandonment than card-only flows. Canadian merchants are weaving BNPL offers into influencer campaigns and loyalty programs, turning payment choice into an acquisition lever rather than a back-office function. Heightened regulatory oversight and rising account-takeover fraud add complexity, yet sustained youth engagement keeps the medium-term impact positive for the North America e-commerce market.[2]Alan Kaplinsky, “Buy Now, Pay Later Services: Regulatory Landscape And Consumer Protection Concerns,” Ballard Spahr, ballardspahr.com

Expansion of cross-border e-commerce via USMCA-enabled customs simplification

Higher de minimis thresholds and harmonized forms under USMCA have encouraged SMEs to ship directly across borders, slashing brokerage fees and transit times. Mexican shoppers now access niche U.S. brands without third-party reshippers, while Canadian artisans tap U.S. demand without building inventory south of the border. Cross-border package volumes are rising fastest on lightweight categories such as beauty and specialty foods, creating a 1.8 percentage-point lift to the regional CAGR. Long-term success hinges on merchants’ ability to manage still-divergent data-privacy and product-labeling standards.

Retail-media networks boosting D2C conversion on large marketplaces

Three-quarters of North American marketers expect retail-media networks to take a larger slice of their budgets, and initial test campaigns show conversion rates running 3-5 times above conventional display ads.[3]Rebecca Stewart, “North American Marketers Survey: Retail Media Networks Integration In Omnichannel Strategies,” The Drum, thedrum.com These networks marry first-party traffic data with closed-loop attribution, allowing brand owners to bid aggressively because sales outcomes are measurable in hours. Expansion into in-store digital displays and off-site programmatic inventory is blurring boundaries between physical and digital promotion, elevating the importance of unified reporting dashboards. Elevated conversion efficiency is expected to sustain a 1.7 percentage-point addition to the North America e-commerce market CAGR in the near term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Last-Mile Delivery Costs from Labour Shortages | -1.2% | United States (primary), Canada (secondary) | Medium term (2-4 years) |

| State-Level Data-Privacy Laws (e.g., CPRA) Elevating Compliance Costs | -1.0% | United States (state-specific) | Medium term (2-4 years) |

| High Return Rates & Reverse-Logistics Complexity in Apparel | -0.9% | North America (region-wide) | Long term (≥ 4 years) |

| Cyber-Fraud Targeting BNPL Checkout Flows | -0.8% | North America (region-wide) | Short term (≤ 2 years) |

Source: Mordor Intelligence

Rising last-mile delivery costs from labor shortages

Transportation payrolls expanded 47% from 2013-2023, yet demand still exceeds driver availability, pushing wages 30% higher since 2020 and eroding retailer margins. Aging couriers and high turnover magnify the challenge. Retailers in the North America e-commerce market are piloting route-optimization software, parcel lockers, and autonomous vehicles, but broad deployment remains years away. Until then, companies must absorb costs or raise delivery fees, a trade-off that could dampen volume growth among price-sensitive shoppers.

State-level data-privacy laws elevating compliance costs

Twenty-one U.S. states now enforce unique privacy statutes, forcing merchants that serve nationwide audiences to re-engineer consent strings, cookie banners, and data-sharing contracts. Compliance spending consumes 2-4% of annual revenue for many mid-size players. Fragmentation undermines the economies of scale that underpin data-driven personalization, limiting the ability of the North America e-commerce market to fully exploit AI-powered recommendation engines. If harmonization stalls, smaller firms may slow expansion into additional states to contain legal exposure.

Segment Analysis

By Business Model: B2B platforms outpace the consumer segment

The segment generated 12.1% CAGR prospects between 2025-2030, outstripping consumer growth even though B2C commands 88.09% of current revenue within the North America e-commerce market. Digitized procurement replicates consumer-grade ease, replacing fax orders with AI-guided catalogs that suggest replenishment and dynamic pricing. Enterprise buyers value real-time inventory visibility and integration with ERP systems, attributes that widen barriers to entry for late adopters. Vertical marketplaces serving healthcare, construction, and industrial supplies embed compliance certificates and financing tools, lifting switching costs.

B2B platforms are importing consumer playbooks such as one-click re-order and mobile-native interfaces, reducing friction for field technicians who now place orders from job sites. The North America e-commerce market size for B2B is also expanding as export-oriented SMEs leverage cross-border APIs that quote duties and fees immediately. Collaboration between suppliers and fintech firms accelerates embedded credit, enabling instant approval and automated net-90 payment schedules. As a result, the segment is forecast to reach USD 3 trillion in U.S. value alone by 2027.

By Device Type: Smartphone commerce dictates experience design

Mobile wallets, voice search, and biometric log-ins collectively pushed smartphones to 72.01% transaction share in 2024, and that figure will climb through a 10.3% CAGR by 2030. Desktop retains a role for high-consideration items, yet shoppers frequently start discovery on handheld screens before closing deals elsewhere. Retailers that optimize image weight, 3D product views, and thumb-friendly navigation win higher dwell time, lifting the North America e-commerce market size attached to mobile checkouts.

Emergent channels such as smart TVs and in-car dashboards add new shopper touchpoints. Voice commerce already logs purchases from 27% of consumers. Interoperable session IDs now allow a cart to travel from phone to laptop to kiosk without re-authentication, reinforcing omnichannel continuity. As 5G coverage strengthens rural areas, latency-free rich media will reach previously underserved shoppers, cementing mobile devices as the growth core of the North America e-commerce market.

By Payment Method: Digital wallets widen their lead while BNPL matures

Digital wallets owned 45.21% of payments in 2024 and will account for more than half of transaction value by 2027. BNPL’s 16.2% CAGR shows sustained momentum, yet provider consolidation is underway as compliance costs rise. Merchants deploy payment-orchestration layers that automatically route transactions to the lowest-cost, highest-conversion rail, an approach that lowers fraud while protecting interchange economics.

Account-to-account rails such as FedNow open fresh paths that bypass legacy card schemes, offering instant settlement and lower fees for high-value goods. Crypto remains a niche option due to volatility, but stablecoins are finding niches in cross-border business purchases. Data from these varied rails fuel personalized offers post-purchase, turning the payment layer into a marketing channel that elevates lifetime value across the North America e-commerce market.

Note: Segment shares of all individual segments available upon report purchase

By B2C Product Category: Online grocery spearheads future gains

Consumer electronics held 34.06% revenue share in 2024 thanks to standardized SKUs and high ticket values, yet food and beverages is the breakout performer with 16.2% CAGR through 2030. Dark-store micro-fulfillment centers now locate groceries within five miles of densest customer clusters, bringing picking accuracy above 98% and cutting delivery windows to under an hour. These hubs are expected to fulfill 8% of total U.S. online grocery orders by 2025. As they scale, the North America e-commerce market size allocated to perishables grows quickly.

Fashion grapples with return costs yet mitigates risk via virtual try-on and size analytics, lifting conversion while trimming reverse-logistics waste. Beauty and personal care brands embrace social commerce and subscription replenishment, capturing routine spend from digital natives. Furniture vendors deploy augmented reality allowing shoppers to place 3D couches in living rooms before purchase, reducing return ratios. Each of these shifts expands the long-tail product mix that collectively invigorates the North America e-commerce market.

Geography Analysis

The United States commands 87.12% of current revenue within the North America e-commerce market and remains the testing ground for innovations such as retail-media networks that merge on-site and in-store data. State privacy laws complicate nationwide campaigns, but large players adapt with modular consent tools that preserve personalization. Same-day delivery expectations in dense metro areas keep capital flowing into robotics, EV delivery fleets, and AI inventory placement.

Canada contributes robust growth anchored in progressive payment habits. Digital wallet penetration nears mainstream levels, and Gen-Z preference for BNPL forces merchants to support multi-rail checkout orchestration. Cross-border shopping is routine; Canadians often tap U.S. catalogs to access broader assortments. Rural fulfillment remains costly, yet investments in regional parcel hubs and expanded pick-up lockers promise to compress delivery times.

Mexico is the fastest-growing component of the North America e-commerce market, rising at a 13.4% CAGR. Smartphone-first access dominates because handsets represent the main internet device for many households. Platforms such as Mercado Libre and Amazon localize seller onboarding, logistics, and language support, facilitating cross-border flow under simplified USMCA rules. Logistics investment in intermodal corridors and last-mile parcel shops reduces historical barriers linked to post-purchase reliability.

Competitive Landscape

Market structure resembles a barbell. Amazon anchors one end with a 37.6% U.S. share and continues to widen its moat through Prime perks, proprietary logistics assets, and voice-activated storefronts. Walmart represents the largest omnichannel challenger, leveraging 4,600 stores as forward fulfillment nodes and turning USD 53.4 billion in online revenue into flywheel data for its rapidly growing retail-media network.

Between those giants and a long tail of niche specialists lies a cohort of digitally native vertical brands that exploit category depth to sidestep price wars. These operators focus on controlled assortments, proprietary IP, and community-driven engagement to defend margins. Competitive intensity now centers on data science capabilities: leading retailers build in-house AI teams to refine search relevance, pricing elasticity, and supply-chain forecasting. This technology push aligns with broader investment trends as the region’s big-data and analytics spending heads toward USD 169.91 billion by 2028.

Strategic activity remains brisk. Logistics providers such as DHL scale returns solutions while software vendors blend composable commerce stacks with immersive 3D front-ends, closing experiential gaps between physical and digital shopping. Private-equity investors chase roll-ups of Shopify storefronts, wagering that operational synergies in marketing and fulfillment can unlock profit in the fragmented mid-tier of the North America e-commerce market.

North America E-commerce Industry Leaders

-

Walmart Inc.

-

Amazon.com, Inc.

-

SHEIN Group Ltd.

-

Coppel, S.A. de C.V.

-

Costco Wholesale Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Stord acquired Ware2Go, adding 21 fulfillment centers and 1.3 million sq ft of space, broadening scalable solutions for direct-to-consumer and B2B clients.

- May 2025: DHL Supply Chain bought IDS Fulfillment, expanding its U.S. footprint and solidifying leadership in returns processing.

- May 2025: TRUBAR Inc. recorded a 593% jump in DTC revenue, with online sales reaching USD 2.9 million and entering Target stores nationwide.

- March 2025: Xebra Brands partnered with BSK Holdings to distribute Elements CBD products in Mexico through e-commerce channels.

North America E-commerce Market Report Scope

E-commerce refers to any type of online business transaction. Online shopping, defined as buying and selling items over the internet on any device, is the most well-known example of E-commerce. On the other hand, E-commerce can encompass a wide range of activities, including online auctions, payment gateways, online ticketing, and internet banking.

North America E-commerce Market is segmented by B2C E-commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverage, Furniture and Home), B2B E-commerce, and Countries.

| By Business Model | B2C |

| B2B | |

| C2C | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories | |

| By Country | United States |

| Canada | |

| Mexico |

By Business Model

| B2C |

| B2B |

| C2C |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

By Country

| United States |

| Canada |

| Mexico |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the North America e-commerce market by 2030?

The market is forecast to reach USD 2.23 trillion by 2030, growing at a 9.69% CAGR during 2025-2030.

Which country will grow the fastest in the region?

Mexico is expected to post a 13.4% CAGR, making it the fastest-growing geography within the North America e-commerce market.

How large is mobile commerce today?

Smartphones facilitated 72.01% of North American online transactions in 2024, and that share is expanding at a 10.3% CAGR.

Why is BNPL important for merchants?

Buy Now, Pay Later lifts average order value by 33% and cuts cart abandonment by up to 40%, especially with Gen-Z shoppers.

Which product category will add the most incremental revenue through 2030?

Food and beverages will grow at 16.2% CAGR thanks to dark-store micro-fulfillment, outpacing all other categories.

How are privacy laws influencing e-commerce strategy?

Fragmented state-level regulations drive compliance spending equal to 2-4% of revenue, prompting companies to adopt modular data-governance frameworks before entering new states.

Page last updated on: July 7, 2025