Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

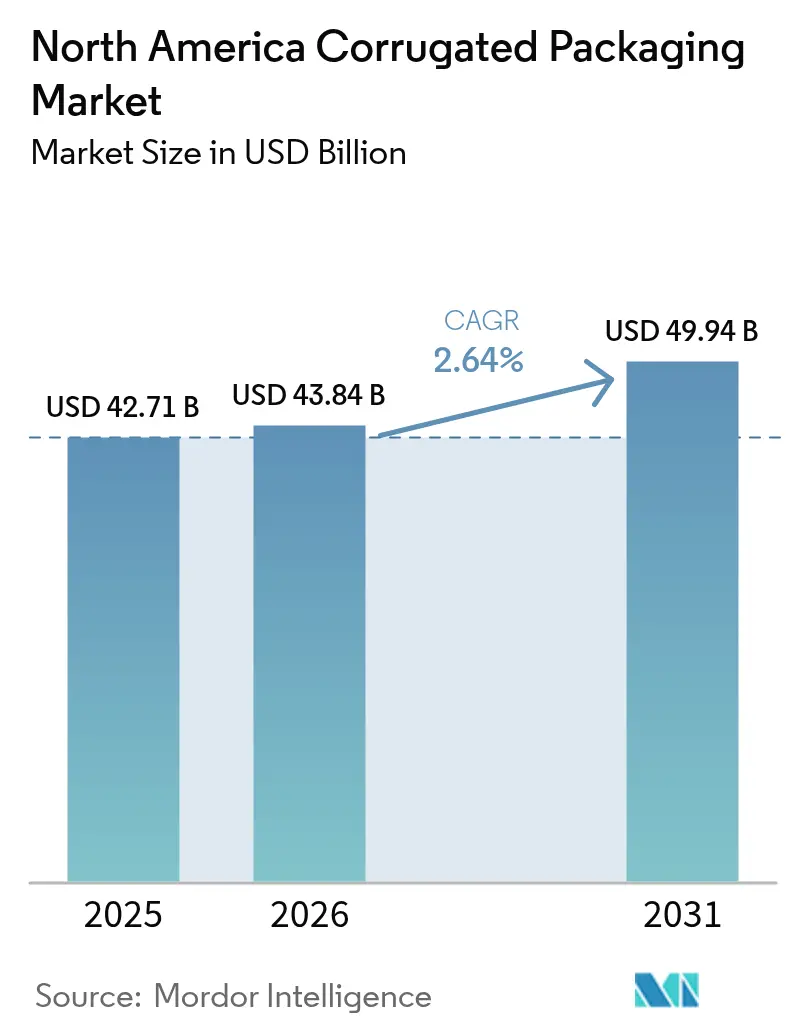

| Base Year Market Size (2025) | USD 42.71 Billion |

| Market Size (2026) | USD 43.84 Billion |

| Market Size (2031) | USD 49.94 Billion |

| Growth Rate (2026 - 2031) | 2.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Corrugated Packaging Market Analysis by Mordor Intelligence

The North America corrugated packaging market size is projected to expand from USD 42.71 billion in 2025 and USD 43.84 billion in 2026 to USD 49.94 billion by 2031, registering a CAGR of 2.64% between 2026 to 2031. Moderate growth hides rapid changes in substrate mix, flute architecture, and end-user priorities that are forcing converters to retool production assets. Recycled containerboard continues to dominate, but premium semi-chemical grades are scaling faster as online beauty brands demand brighter surfaces. Automotive and industrial nearshoring is lifting triple-wall adoption, while microflute formats gain share in parcels as fulfillment centers optimize dimensional weight. At the same time, regulatory pressure on single-use plastics and volatile recovered-fiber prices are reshaping competitive strategies across the North America corrugated packaging market.

Key Report Takeaways

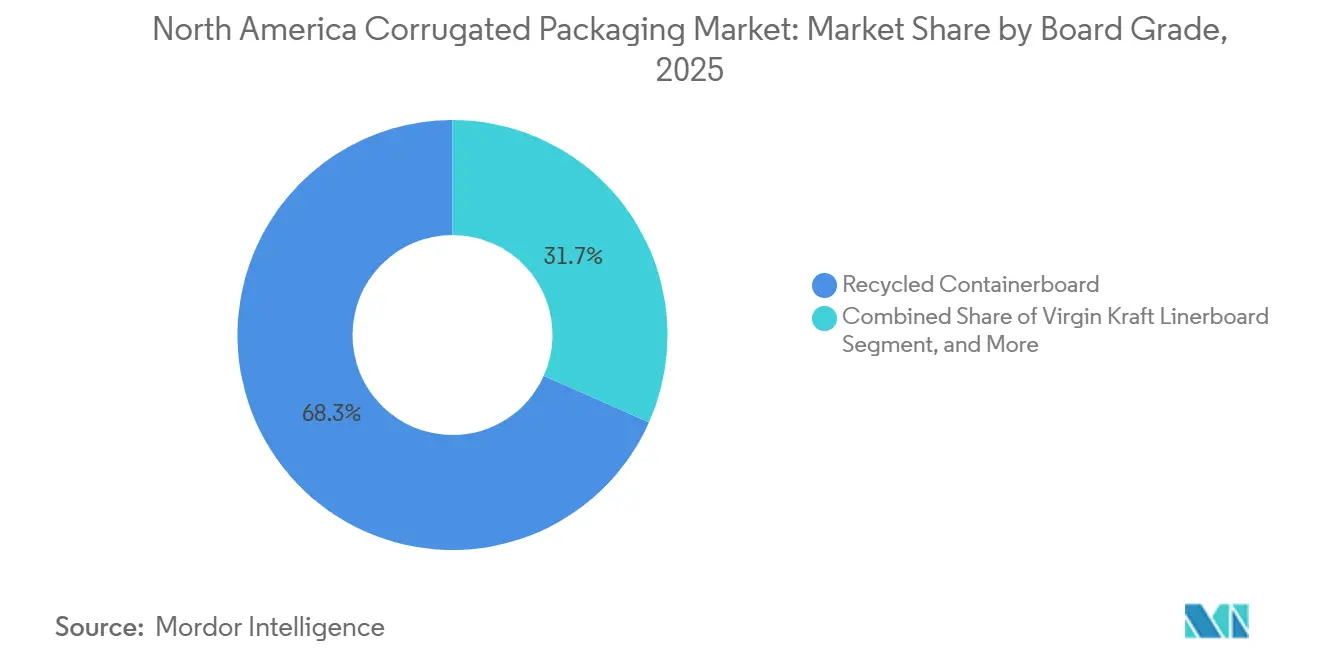

- By board grade, recycled containerboard dominated with 68.34% of the North America corrugated packaging market share in 2025, while semi-chemical and specialty grades are projected to expand at the fastest 3.31% CAGR through 2031.

- By wall type, single-wall formats accounted for 59.76% of regional revenue in 2025, whereas triple-wall configurations are expected to register the highest CAGR of 3.28% over 2026-2031.

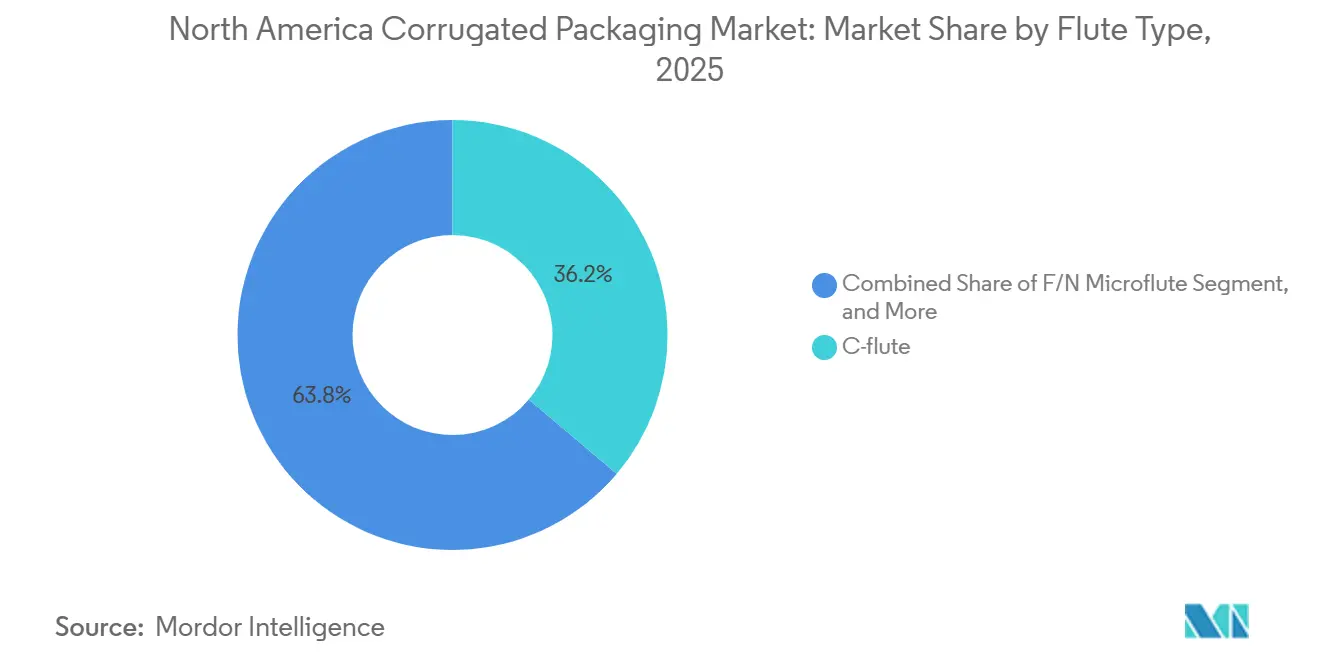

- By flute type, the C-flute held the largest 36.17% of the North America corrugated packaging market share in 2025, yet the F/N microflute is anticipated to deliver the strongest 3.61% CAGR during the forecast period.

- By product type, slotted boxes led with 47.33% of the North America corrugated packaging market share in 2025, while bulk bins and octabins are forecast to grow at a leading 3.69% CAGR to 2031.

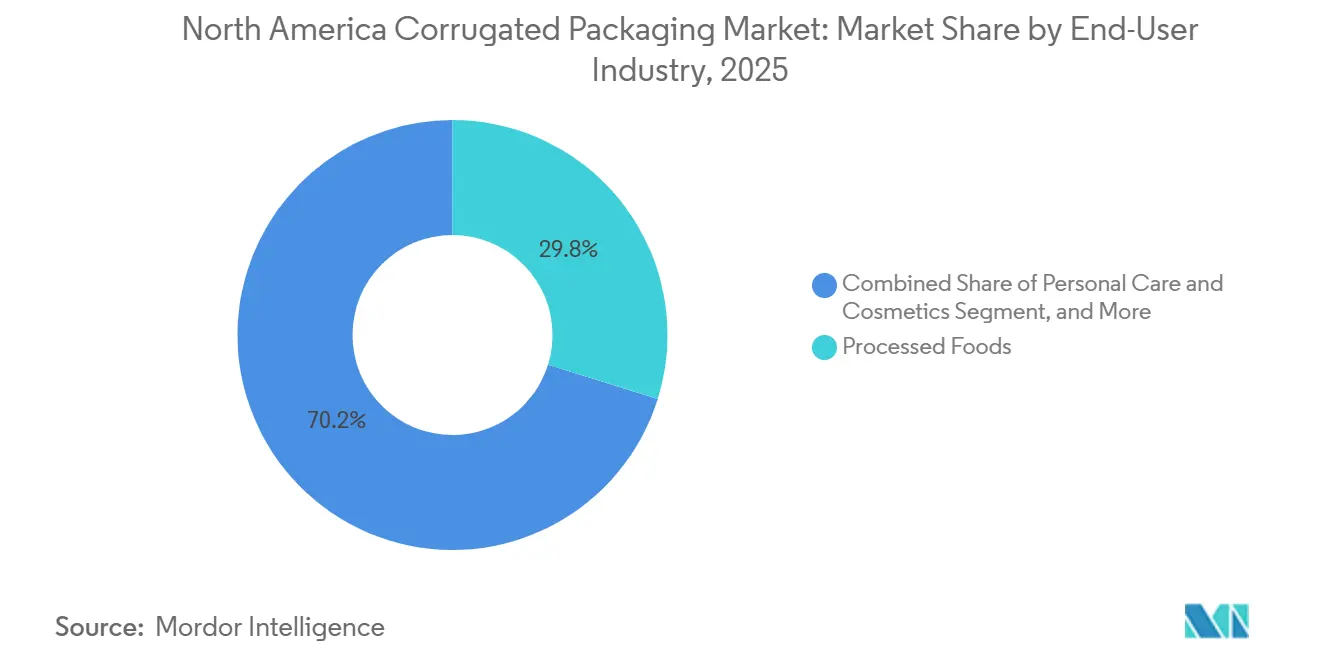

- By end-user industry, processed foods generated 29.82% of 2025 demand, whereas personal care and cosmetics are set to advance at the fastest 4.07% CAGR through 2031.

- By printing technology, flexographic printing captured 63.91% of the North America corrugated packaging market share in 2025, yet digital printing is poised for the highest 3.46% CAGR across 2026-2031.

- By geography, the United States accounted for 79.34% of regional value in 2025, while Mexico is forecast to post the fastest 3.22% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce parcel volumes | +0.9% | United States, Canada, with spillover to Mexico urban centers | Short term (≤ 2 years) |

| Regulatory shift toward recyclable packaging and plastic bans | +0.6% | United States (state-level), Canada (federal), Mexico (municipal pilot programs) | Medium term (2-4 years) |

| Lightweight high-strength micro-flutes and material savings | +0.4% | United States and Canada e-commerce hubs, gradual adoption in Mexico | Medium term (2-4 years) |

| Cold-chain expansion for meal-kit and pharma logistics | +0.3% | United States and Canada metropolitan areas, limited penetration in Mexico | Long term (≥ 4 years) |

| AI-enabled right-sizing and on-demand box production | +0.2% | United States fulfillment centers, pilot deployments in Canada | Medium term (2-4 years) |

| Nearshoring of manufacturing boosting domestic box demand | +0.3% | Mexico manufacturing corridors, southern United States border states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Parcel Volumes

E-commerce shipments in North America topped 20 billion parcels in 2025, and 92% moved in corrugated containers, directly translating into higher box demand.[1]United States Postal Service, “Fiscal Year 2025 First Half Performance Report,” USPS, about.usps.com The United States Postal Service reported a 7.2% year-over-year rise in package volume during the first half of 2025, while private carriers absorbed an additional 12% jump in business-to-consumer deliveries the same year. Amazon installed more than 200 on-demand packaging stations across its regional network by mid-2025, eliminating inventory of 26 fixed box sizes and cutting material waste by 18% per parcel. The National Retail Federation projects online sales will reach 28% of total United States retail by 2027, ensuring sustained corrugated growth even if brick-and-mortar channels stabilize. Fulfillment centers are therefore prioritizing plain kraft slotted containers that run at higher line speeds, reinforcing corrugated’s position as the default transport medium.

Regulatory Shift Toward Recyclable Packaging and Plastic Bans

Canada’s Federal Plastics Registry, effective June 2024, requires producers to report plastic volumes and recycled content, a compliance burden that fiber packaging is exempt from.[2]Environment and Climate Change Canada, “Federal Plastics Registry: Producer Reporting Requirements,” Government of Canada, canada.ca Eight United States states, including California and New York, enacted extended producer responsibility laws during 2024-2025 that levy per-ton fees on non-recyclable formats, but spare corrugated boxes, which have an 89% recovery rate. Mexico City’s 2024 ban on expanded polystyrene foodservice ware redirected an estimated 35,000 short tons of demand to corrugated clamshells and pizza boxes. The Sustainable Packaging Coalition found in 2025 that 73% of North American brand owners now rank recyclability above lightweighting when specifying primary packs. These converging policies collectively lift corrugated’s competitive edge versus plastics and accelerate substrate switching in foodservice, retail carry-out, and direct-to-consumer channels.

Lightweight High-Strength Microflutes and Material Savings

F/N microflute profiles, only 0.5-1.5 millimeters high, cut basis weight up to 20% while matching the 32-ECT strength of C-flute boxes, reducing dimensional-weight charges in parcel networks. EFI’s Nozomi C18000 press can print directly onto these thin substrates at 246 feet per minute, eliminating litho-lamination costs and shortening lead time by up to 5 days. International Paper reported that microflute grades reached 8% of its North American containerboard shipments in 2025, doubling the 2023 figure. Converters leveraging semi-chemical fluting media with higher ring-crush values can now meet heavy-duty requirements without adding caliper, expanding microflute use into consumer electronics and shelf-ready displays. As fulfillment centers penalize excess void space, demand for lighter yet strong microflute boxes is set to climb steadily across the region.

Cold-Chain Expansion for Meal-Kit and Pharma Logistics

Temperature-controlled corrugated packaging grew into a USD 1.2 billion niche by 2025 as meal-kit subscriptions rebounded to 18 million and mail-order pharmacies expanded nationwide. DS Smith’s FDA-compliant TailorTemp system integrates phase-change materials into double-wall constructions, now specified by three of the five largest United States pharmacy fulfillment firms. The American Frozen Food Institute recorded USD 8.3 billion in direct-to-consumer frozen food sales during 2025, a 22% increase over 2024, which relied heavily on corrugated outers paired with gel packs or dry ice. These premium boxes command higher margins because converters must install lamination lines for metallized liners and manage just-in-time inventories of perishable inserts. As regulatory scrutiny on pharmaceutical cold chains tightens, insulated corrugate is becoming indispensable, adding depth and profitability to the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in OCC and virgin pulp prices | -0.5% | United States and Canada integrated mills, Mexico import-dependent converters | Short term (≤ 2 years) |

| Substitution threat from flexible and rigid plastics | -0.3% | United States foodservice and retail, limited impact in Canada and Mexico | Medium term (2-4 years) |

| Labor shortages driving automation capex burden | -0.2% | United States and Canada converting operations, emerging concern in Mexico | Long term (≥ 4 years) |

| Rising energy and transportation costs | -0.2% | United States and Canada freight-intensive routes, Mexico energy-reform impacts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in OCC and Virgin Pulp Prices

Old corrugated container prices fluctuated from USD 50 per short ton in February 2025 to USD 90 in September 2025, an 80% swing that eroded converter margins.[3]Green Markets, “Box Cost Index: Q4 2025 Analysis,” Green Markets, greenmarkets.com China’s reduced appetite for recovered fiber redirected 2.1 million short tons of exports back into North America, flooding the domestic stream and depressing spot values while mills idled 12% of corrugating-medium capacity in early 2025. Virgin Kraft linerboard held near USD 620-650 per ton, creating a wide cost gap that favored integrated producers but punished merchants lacking mill assets. Quarterly price renegotiations have replaced annual contracts, adding uncertainty that can delay capital projects in converting plants. Unless export channels recover or new domestic capacity starts, margin pressure from fiber price volatility will persist.

Substitution Threat from Flexible and Rigid Plastics

Stand-up pouches captured 18% of the United States dry-food volume in 2025, up from 14% in 2023, driven by an 85% weight advantage over equivalent corrugated cartons. The Flexible Packaging Association reported that 67% of consumer-packaged-goods companies were trialing flexible formats on at least one product line in 2025, signaling continued experimentation. Rigid PET clamshells still dominate fresh-produce packs where ventilation and moisture resistance outrank recyclability, keeping corrugated out of some high-growth perimeter aisles. Although Canada’s registry and California’s EPR fees narrow the cost gap, plastics’ resealability and shelf appeal remain persuasive for snack and cereal brands. Corrugated converters are responding with hybrid microflute boxes laminated to barrier films, but these solutions raise costs and blur the fiber’s sustainability advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Board Grade: Recycled Fiber Dominates, Specialty Grades Scale Up

Recycled containerboard captured 68.34% of the North America corrugated packaging market share in 2025, validating the region’s mature recovered-fiber network. The grade’s cost advantage and 89% recovery rate keep it the default choice for grocery, beverage, and e-commerce shippers that prize low total landed cost. Semi-chemical and specialty substrates, however, are forecast to record the fastest 3.31% CAGR through 2031 as cosmetics, meal-kit, and consumer-electronics brands demand brighter print surfaces and grease-resistant coatings. This migration toward premium surfaces is prompting integrated mills to debottleneck specialty machines and secure long-term contracts with converters serving direct-to-consumer channels.

The North America corrugated packaging market for recycled grades will still expand modestly, as volume gains in processed foods outweigh share drift to premium substrates. Virgin Kraft linerboard remains essential for export crates and heavy industrial loads, where stacking strength must offset long transit times, yet its 40% cost premium limits wider use. Recycled grades are also adopting lightweight grammages, notably a switch from 47-pound to 42-pound liner in apparel shipping, widening their appeal. Overall, brand segmentation rather than raw tonnage now guides substrate strategy, and mills that can toggle between brown and white-top grades on the same machine gain scheduling flexibility.

By Wall Type: Single-Wall Prevails, Triple-Wall Gains Strength

Single-wall formats accounted for 59.76% of regional revenue in 2025, as 68% of shipped items weighed under 20 pounds. They remain the workhorse in parcel, retail-ready, and light industrial cases where 32 ECT strength is sufficient and high-speed automation favors thin caliper. Triple-wall constructions are projected to notch the highest 3.28% CAGR over 2026-2031 as nearshored automotive and machinery output demands 275-pound ECT durability for engine blocks and heavy castings. Rising adoption is visible in northern Mexico and southern United States border corridors, where new assembly plants are specifying heavier boxes for ocean and intermodal transit.

Double-wall sits between the extremes, protecting appliances, bulk foods, and cold-chain payloads that are too heavy for single-wall yet do not justify triple-wall cost. Walmart’s 48-ECT pallet mandate has already spurred upgrades from single-wall to double-wall in selected grocery lanes. Meanwhile, microflute innovation is eroding the lower end of single-wall as fulfillment centers trim dimensional weight, indicating share churn even within the dominant class. Producers that can run multiple wall types on the same corrugator window improve asset utilization and meet shifting customer strength specifications without lengthening lead times.

By Flute Type: C-flute Leads, Microflute Accelerates

C-flute retained 36.17% of the 2025 volume, favored for its cushioning and stacking balance, which satisfy general shipping, club-store shippers, and in-store displays. The profile’s mid-range caliper runs reliably on legacy equipment and handles multi-color flexographic graphics without washboarding. F/N microflute is expected to log the fastest 3.61% CAGR as parcel carriers penalize dimensional weight and converters exploit thinner profiles to raise pallet cube by double-digit percentages. Direct digital printing on microflute also eliminates costly litho-lamination, letting beauty and tech brands launch short runs in weeks instead of months.

B-flute continues to win in pizza, bakery, and folding carton applications where print gloss and cut resistance trump cushioning. E-flute Plus High-Definition Flexo targets consumer electronics that require sleek graphics and moderate crush resistance. A flute remains a niche yet irreplaceable option for fragile glass and ceramics, which absorb shocks better due to its 5 millimeter height. As converters retrofit advanced corrugators and tension controls, they can shift flute profile mid-shift, enabling mixed loads and small-batch scheduling that align with the lean requirements of the North America corrugated packaging market.

By Product Type: Slotted Boxes Mainstay, Bulk Bins Expand

Slotted boxes accounted for 47.33% of product-type value in 2025, underscoring their versatility across e-commerce, retail, and light industrial applications. Regular-slotted containers run on high-speed case erectors, accept in-line print, and nest efficiently in fulfillment lines, making them the go-to choice for both mass-merchandise shippers and regional 3PLs. Bulk bins and octabins are forecast to grow at a leading 3.69% CAGR to 2031 as food processors, chemical blenders, and resin suppliers consolidate 50-pound bags into 1-ton corrugated containers that reduce manual handling and freight touches. These extra-heavy boxes lower total pallet movements in high-volume ingredient plants, boosting demand for edge-crush values above 48 ECT.

Rigid two-piece boxes, although smaller in volume, capture premium consumer-electronics and luxury gift sets where unboxing theater justifies a 60% price uplift over slotted forms. Telescope designs serve aftermarket auto parts and industrial tools in closed-loop fleets, yet they face rising competition from returnable plastic totes. Folder boxes appeal to crafters and small businesses ordering fewer than 1,000 units, an online channel that benefits from rapid die-less digital conversion. Product-mix diversification allows converters to mitigate cyclical swings in mass-volume slotted demand, balancing the broader North America corrugated packaging market size.

By End-User Industry: Food Staples Steady, Personal Care Accelerates

Processed foods anchored 29.82% of end-user demand in 2025, leveraging entrenched supply chains for canned goods, cereals, and shelf-stable snacks. These lanes favor recycled single-wall boxes printed flexographically at astonishing speeds, keeping unit cost low. Personal care and cosmetics, on the other hand, are predicted to clock the fastest 4.07% CAGR through 2031 as online subscription beauty kits and influencer-driven brands ship fragile glass jars that need branded, protective corrugate. This segment frequently specifies white-top liner and digital four-color artwork, lifting average selling prices.

Beverage shippers require heavier double-wall trays to bear glass and aluminum loads, while fresh produce alternates between ventilated corrugated crates and reusable plastic containers, depending on retailer preference and route length. Electrical and electronics shipments in Mexico are rising due to nearshoring, spurring demand for anti-static coatings and moisture barriers. Paper and tissue mills order corrugated master cases on a steady cadence but grow slowly, so converters look to higher-margin cosmetic, pharma, and specialty food accounts for upside. End-use diversification provides resilience against isolated sector slowdowns across the North America corrugated packaging market share.

By Printing Technology: Flexography Rules, Digital Finds Niche

Flexographic presses held a 63.91% share in 2025, excelling at long runs above 10,000 impressions, where plate amortization drops below 2 cents each. High-speed gearless lines now approach 2,000 feet per minute, enabling consumer packaged goods to maintain consistent branding across millions of boxes per quarter. Digital inkjet is set to achieve the fastest 3.46% CAGR because direct-to-consumer brands demand micro-batch lots, versioned artwork, and rapid seasonal drops that flexo cannot deliver economically. Recent installations of single-pass inkjet systems capable of 246 feet per minute prove that quality and speed barriers are fading.

Litho-lamination, while shrinking, stays relevant in ultra-high graphics consumer electronics and gift packaging, though direct print on microflute is starting to displace it by trimming costs and lead time. Screen and offset formats are used in specialty point-of-purchase displays and industrial labelling where surface texture or ink laydown requirements differ. The North America corrugated packaging market is increasingly driven by printers’ ability to offer both high-volume commodity flexo and agile digital within the same plant, ensuring they capture the full spectrum of customer artwork and quantity needs.

Geography Analysis

The United States contributed 79.34% of the North America corrugated packaging market share in 2025, reflecting its USD 6.5 trillion consumer economy, 16 billion annual parcel movements, and a network of more than 1,200 converting plants. Fulfillment growth remains strongest in Sun Belt states, where 47 new distribution centers opened during 2025, redirecting box demand away from coastal hubs and lifting regional service expectations. State-level extended producer responsibility laws in California, New York, and Washington are increasing per-ton fees on non-recyclable formats, giving corrugated a cost advantage that sustains capacity utilization near 88%.

Mexico’s corrugated consumption expanded 6.1% in 2025, outpacing the overall North America corrugated packaging market's growth, as nearshored automotive and electronics assembly required heavier triple-wall and bulk bins. Foreign direct investment worth USD 35 billion entered the country across 2024-2025, adding 18 converting plants and 320,000 short tons of incremental capacity along the Monterrey, Guadalajara, and Tijuana corridors. The market is still import-dependent for virgin kraft linerboard, sourcing about 40% of supply from United States mills, which exposes converters to freight volatility and currency swings. Despite limited municipal plastic bans outside Mexico City, structural growth in manufacturing positions the country for a 3.22% CAGR through 2031.

Canada serves a smaller population base yet benefits from the Federal Plastics Registry finalized in 2024, which nudges brand owners toward fiber formats in foodservice and retail carry-out channels. Corrugated usage clusters near Toronto, Montreal, and Vancouver because 68% of Canadians live within 100 miles of the United States border, allowing plants to optimize cross-border freight lanes. Capacity utilization averages 82%, leaving buffer room for e-commerce-driven spikes without the supply tightness seen in the United States. Bulk bins and industrial shippers account for a higher 22% share of Canadian demand versus 14% in the United States, reflecting the country’s concentration in resource extraction and food processing. Together, these geographic patterns create a balanced growth outlook that mitigates localized supply risks across North America.

Competitive Landscape

Market concentration is moderate, with the top five producers now controlling roughly 48% of regional capacity after the Smurfit Westrock merger and Packaging Corporation of America’s Greif mill acquisition. Integrated giants leverage backward links to pulp and paper to shield margins from price swings in old corrugated containers, while merchant converters compete on rapid turnaround and digital-printing flexibility. International Paper plans to separate its pulp assets from its packaging operations, signaling a focus on higher-margin converting operations located close to customers.

Technology adoption is redefining service models. More than 150 United States and Canadian fulfillment centers now run Packsize on-demand systems that eliminate box inventory and favor converters able to deliver blank bundles within hours. EFI installed 14 Nozomi single-pass inkjet presses across the region in 2025, helping mid-tier firms win short-run promotional work that legacy flexographic lines handle inefficiently. Georgia-Pacific committed USD 800 million to increase virgin kraft output, whereas Pratt Industries invested USD 92.5 million in recovered-fiber processing, illustrating divergent feedstock strategies aimed at the same e-commerce opportunity.

Regulatory expertise is emerging as a competitive differentiator because extended producer responsibility rules and Canada’s plastics registry require detailed reporting that small independents struggle to manage. Sustainability credentials also shape bids, with Sonoco executing a 120 megawatt virtual wind power deal to lock in renewable electricity through 2041. Cold-chain and insulated corrugated boxes are another white-space arena, attracting converters that can finance lamination lines and manage phase-change material inventories. Overall, success in the North America corrugated packaging market now hinges on balanced portfolios that blend scale economics, digital agility, and regulatory compliance, rather than raw tonnage alone.

North America Corrugated Packaging Industry Leaders

International Paper Company

Smurfit Westrock plc

Packaging Corporation of America

Georgia-Pacific LLC

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Pratt Industries completed its USD 92.5 million Rock Hill recycling facility, adding 400,000 short tons of recovered-fiber capacity.

- September 2025: Georgia-Pacific announced an USD 800 million expansion of its Brewton, Alabama pulp mill to add 500,000 short tons of virgin kraft by 2027.

- August 2025: Sonoco Products Company signed a 15-year virtual wind-energy agreement covering 120 MW for corrugated operations.

- July 2025: Packaging Corporation of America finalized the USD 1.8 billion acquisition of Greif containerboard mills, securing 1.1 million short tons of recycled capacity.

North America Corrugated Packaging Market Report Scope

The North America Corrugated Packaging Market Report is Segmented by Board Grade (Recycled Containerboard, Virgin Kraft Linerboard, Semi-chemical and Specialty Grades), Wall Type (Single Wall, Double Wall, Triple Wall), Flute Type (A-flute, B-flute, C-flute, E-flute, F/N Microflute), Product Type (Slotted Boxes, Rigid Boxes, Telescope Boxes, Folder Boxes, Bulk Bins and Octabins), End-user Industry (Processed Foods, Fresh Foods, Beverages, Paper Products, Electrical and Electronics, Personal Care and Cosmetics, Other End-user Industries), Printing Technology (Flexographic Printing, Digital Printing, Litho-lamination, Other Printing Technologies), and Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Board Grade

| Recycled Containerboard |

| Virgin Kraft Linerboard |

| Semi-chemical and Specialty Grades |

By Wall Type

| Single Wall |

| Double Wall |

| Triple Wall |

By Flute Type

| A-flute |

| B-flute |

| C-flute |

| E-flute |

| F/N Microflute |

By Product Type

| Slotted Boxes |

| Rigid Boxes |

| Telescope Boxes |

| Folder Boxes |

| Bulk Bins and Octabins |

By End-user Industry

| Processed Foods |

| Fresh Foods |

| Beverages |

| Paper Products |

| Electrical and Electronics |

| Personal Care and Cosmetics |

| Other End-user Industries |

By Printing Technology

| Flexographic Printing |

| Digital Printing |

| Litho-lamination |

| Other Printing Technologies |

By Country

| United States |

| Canada |

| Mexico |

| By Board Grade | Recycled Containerboard |

| Virgin Kraft Linerboard | |

| Semi-chemical and Specialty Grades | |

| By Wall Type | Single Wall |

| Double Wall | |

| Triple Wall | |

| By Flute Type | A-flute |

| B-flute | |

| C-flute | |

| E-flute | |

| F/N Microflute | |

| By Product Type | Slotted Boxes |

| Rigid Boxes | |

| Telescope Boxes | |

| Folder Boxes | |

| Bulk Bins and Octabins | |

| By End-user Industry | Processed Foods |

| Fresh Foods | |

| Beverages | |

| Paper Products | |

| Electrical and Electronics | |

| Personal Care and Cosmetics | |

| Other End-user Industries | |

| By Printing Technology | Flexographic Printing |

| Digital Printing | |

| Litho-lamination | |

| Other Printing Technologies | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America corrugated packaging market in value terms?

It is projected to reach USD 49.94 billion by 2031 after expanding from USD 43.84 billion in 2026 at a 2.64% CAGR.

Which board grade leads regional demand?

Recycled containerboard remains the volume anchor with 68.34% share in 2025 due to the established recovered-fiber collection network.

What is the fastest growing end-use for corrugated boxes?

Personal care and cosmetics are forecast to grow at a 4.07% CAGR, propelled by online beauty sales that rely on protective branded packaging.

Why is triple-wall corrugate gaining traction?

Nearshored automotive and machinery production needs 275-pound ECT strength for heavy components, lifting triple-wall demand at a 3.28% CAGR.

How is technology shaping the competitive landscape?

Investments in digital presses and AI-enabled right-sizing systems allow converters to produce short-run, custom boxes quickly, differentiating service beyond price.

Which country is expected to outpace the regional growth average?

Mexico is projected to grow at a 3.22% CAGR through 2031 as foreign direct investment boosts domestic manufacturing and box consumption.

Page last updated on: