Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

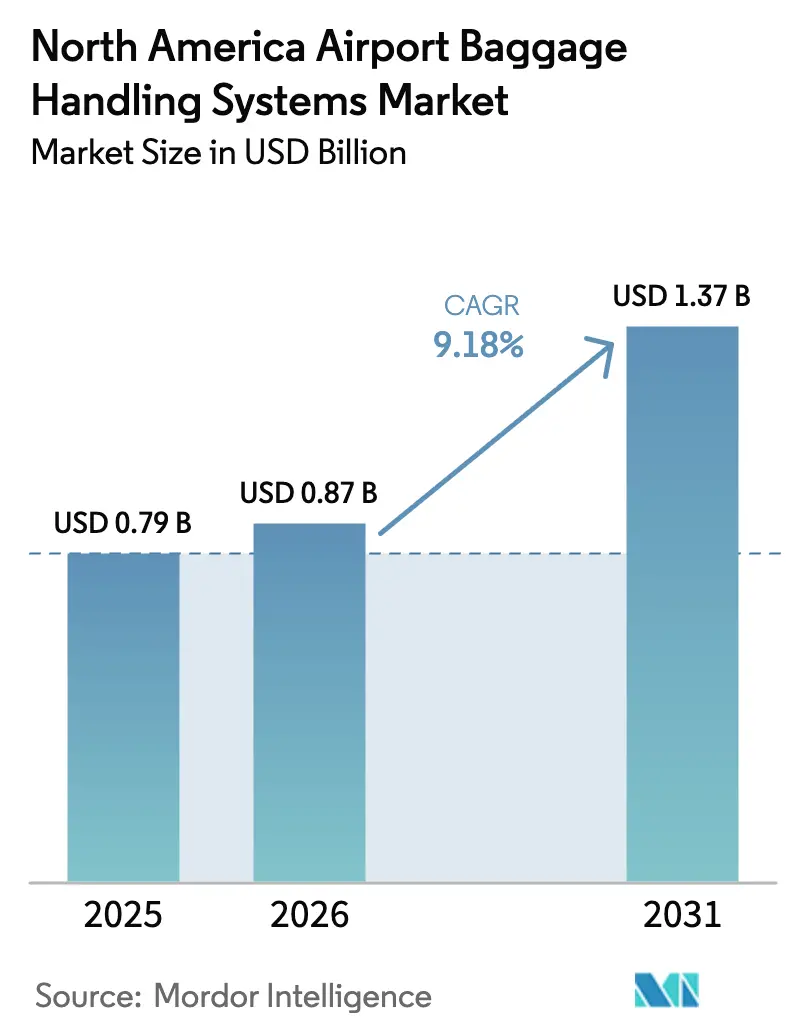

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.37 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

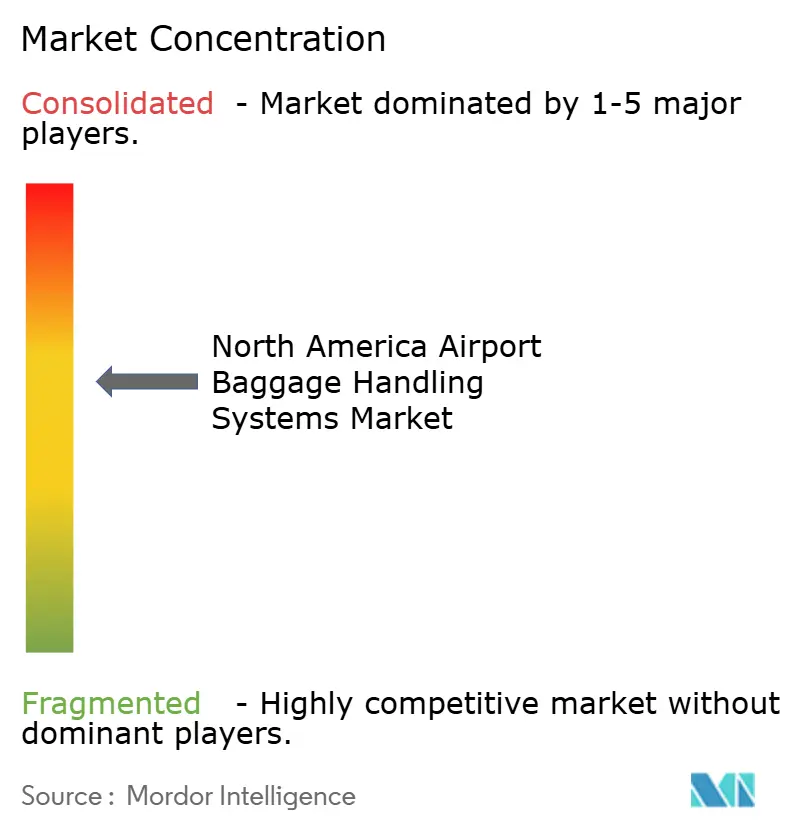

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Airport Baggage Handling Systems Market Analysis by Mordor Intelligence

The North America airport baggage handling systems market size is expected to grow from USD 0.79 billion in 2025 to USD 0.87 billion in 2026 and is forecasted to reach USD 1.37 billion by 2031 at 9.51% CAGR over 2026-2031. Capacity expansion projects, regulatory mandates such as IATA Resolution 753, and TSA-driven upgrades to computed tomography explosives detection scanners are accelerating replacement cycles and sparking new installations across all hub tiers. Operators are implementing radio-frequency identification (RFID), machine-learning (ML) routing software, and tote-based architectures to reduce mishandled-baggage penalties and minimize unplanned downtime, which can cost upwards of USD 100,000 per hour at major hubs. Vendor consolidation, exemplified by Vanderlande’s acquisition of Siemens Logistics, has increased the bargaining power of large systems integrators, prompting smaller firms to differentiate themselves through niche automation offerings. Meanwhile, climate-resilient designs, cyber-secure networks, and tariff-hedged supply chains have become baseline requirements as airports aim to future-proof critical baggage infrastructure.

Key Report Takeaways

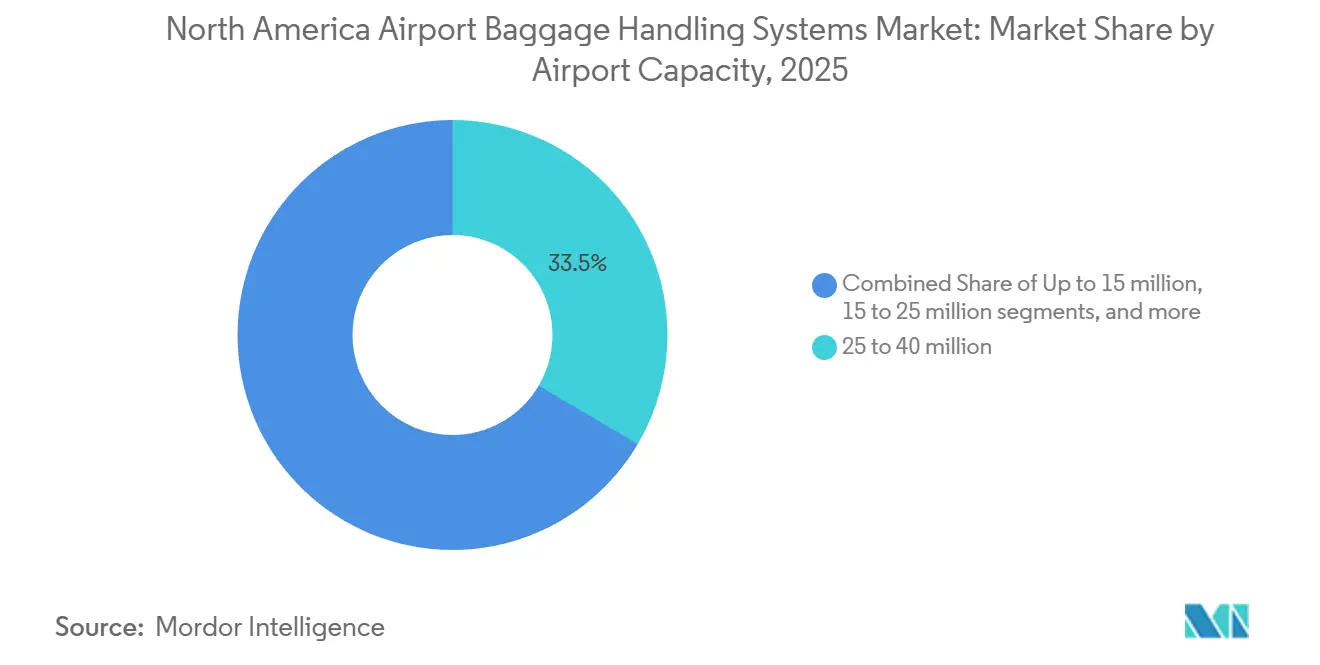

- By airport capacity, the 25 to 40 million passenger segment accounted for 33.47% of the North America airport baggage handling systems market share in 2025 and is forecasted to expand at a 9.75% CAGR to 2031.

- By solution, conveying and sorting platforms captured 37.86% of the North America airport baggage handling systems market in 2025, while tracking subsystems are projected to grow at a 10.65% CAGR through 2031.

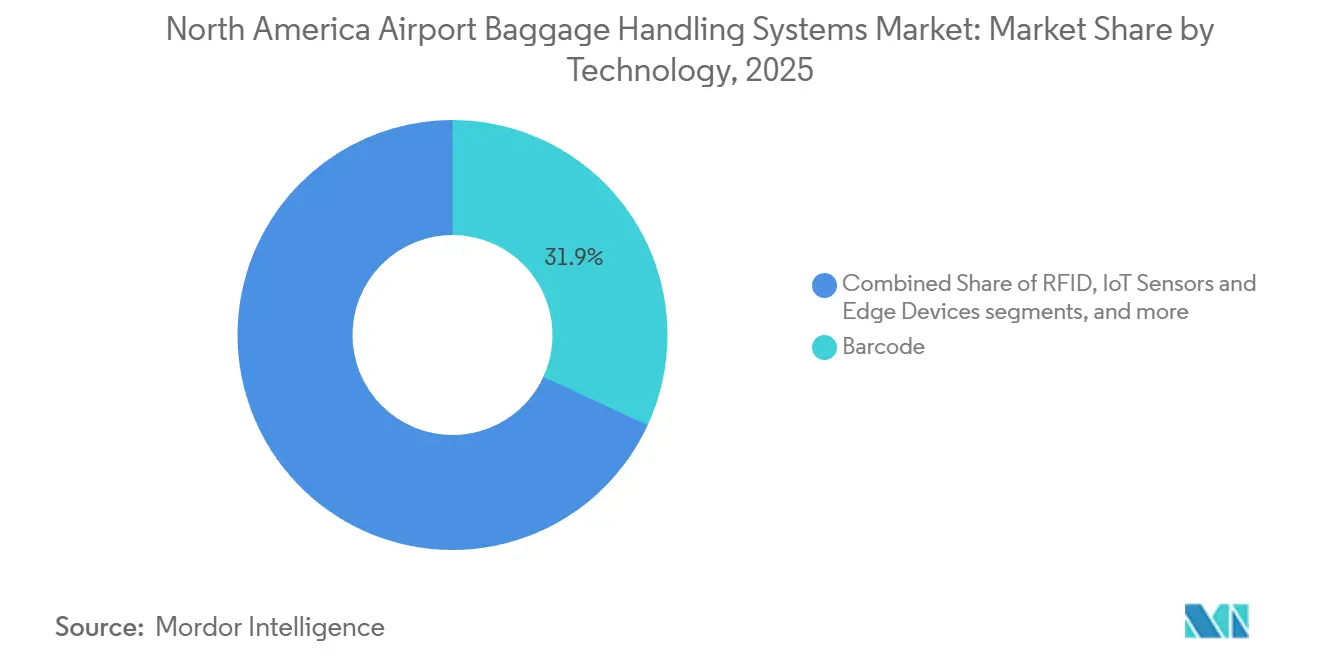

- By technology, barcode systems retained a 31.88% share of the North America airport baggage handling systems market in 2025, whereas AI/ML software is forecast to expand at a 12.87% CAGR through 2031.

- By system type, conveyor belts dominated the North America airport baggage handling systems market with a 49.98% share in 2025; tote-based and individual carrier systems are projected to grow at a 11.60% CAGR through 2031.

- By geography, the United States accounted for 78.56% of the North America airport baggage handling systems market size in 2025, while Mexico is the fastest-growing country, with a 10.21% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Airport Baggage Handling Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery in air passenger traffic driving higher baggage throughput demand | +2.3% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Acceleration of airport modernization and capacity expansion programs | +2.1% | US hub airports, Toronto Pearson, Mexico City | Medium term (2-4 years) |

| Regulatory compliance with IATA Resolution driving RFID-based tracking adoption | +1.8% | Region-wide, with early US adoption | Medium term (2-4 years) |

| Increasing use of automation and AI to reduce mishandled baggage rates | +1.6% | Major US and Canadian hubs | Long term (≥ 4 years) |

| TSA mandates for CT-EDS integration driving baggage system upgrades | +1.4% | United States | Medium term (2-4 years) |

| Rising emphasis on climate-resilient baggage handling system design | +0.9% | US coastal and hurricane-exposed airports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovery in Air Passenger Traffic Driving Higher Baggage Throughput Demand

North American total passenger traffic continued to grow in 2024 with a 4.5% increase over 2023 levels, pushing legacy conveyors to 95% of their rated capacity. Peak-season surges cause jam rates to double, which forces hubs to install higher-speed sorters and early-bag storage that absorbs up to six hours of dwell time. International recovery trails domestic demand, yet bag-transfer complexity at gateway hubs now adds 10 to 15 minutes per connection, prompting deployment of destination-coded vehicles that reroute bags without manual intervention. As these systems come online, operators report throughput gains that offset incremental labor cost inflation.

Acceleration of Airport Modernization and Capacity Expansion Programs

The Federal Aviation Administration granted a total of USD 465 million in 2024 to finance baggage upgrades at 25 airports, including Denver, Miami, and Seattle. Phased commissioning strategies avoid terminal shutdowns, applying lessons from Denver’s 2008 overrun. Toronto Pearson’s “Baggage 2025” program is installing a tote-based line sized for 80 million passengers annually, targeting mishandling below 0.5%. Similar projects across Austin-Bergstrom and Phoenix Sky Harbor demonstrate that mid-tier hubs can support USD 180 million-plus retrofits when passenger growth outpaces gate capacity.

Regulatory Compliance with IATA Resolution 753 Driving RFID Adoption

IATA reports 75% airport readiness and 44% airline implementation for Resolution 753 as of 2025, which has led to RFID read rates increasing to 99% compared to 90% for barcodes in high-speed sorters. Delta Air Lines’ RFID rollout across 344 airports achieved 99.9% accuracy and a 37% reduction in mishandled cases.[1]Delta Air Lines, “Delta Expands Industry-Leading RFID Baggage Tracking,” delta.com Newark Liberty validated cost-effective passive tags priced at USD 0.08 each, strengthening ROI for large-scale deployments.

Increasing Use of Automation and AI to Reduce Mishandled Baggage Rates

The mishandled-bag frequency globally fell to 6.3 per 1,000 passengers in 2024, following the adoption of ML routing and automated reconciliation tools by airports. SITA WorldTracer Auto Reflight matches bags to passengers in under two minutes, halving resolution time and saving airlines nearly USD 400 million annually. Cincinnati/Northern Kentucky’s autonomous Aurrigo tugs remove driver shifts that previously caused up to 12% of misconnections. These deployments generate granular data that reveals micro-bottlenecks, enabling low-cost fixes that extend asset life without capital overhauls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment requirements for large-scale baggage system retrofits | −1.2% | US regional and smaller Canadian airports | Medium term (2-4 years) |

| Integration complexity with legacy baggage handling infrastructure | −0.9% | Pre-2010 US facilities, Toronto Pearson | Short term (≤ 2 years) |

| Cybersecurity risks associated with connected and IoT-enabled baggage systems | −0.7% | Major US hubs, Canadian internationals | Long term (≥ 4 years) |

| Component cost volatility linked to tariffs and import dependencies | −0.8% | Region-wide supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements for Large-Scale Retrofits

Complete baggage overhauls at large hubs cost USD 100 million to USD 250 million, with Austin-Bergstrom’s USD 241.5 million and Denver’s USD 124 million projects illustrating scale. Regional airports incur per-bag capital costs that can exceed USD 40, double those at mega-hubs. However, FAA grants cover up to 75% of eligible spending, matching-fund rules, and multi-year appropriations delay groundbreaking by up to three budget cycles. Opportunity costs also disfavor baggage vs gate additions that yield higher returns, leading many regionals to adopt piecemeal upgrades that extend payback periods beyond 10 years.

Cybersecurity Risks Associated with Connected Baggage Systems

Seattle-Tacoma’s August 2024 Rhysida ransomware shut down automated sorters, forcing manual processing of 7,000 bags and exposing a USD 6 million ransom demand. DHS auditors later identified 6,331 critical vulnerabilities and lingering access for 60 separated employees across TSA high-value assets.[2]Department of Homeland Security Office of Inspector General, “TSA High-Value Asset Cybersecurity Audit,” oig.dhs.gov Collins Aerospace’s MUSE software incidents at Heathrow, Brussels, and Berlin in 2025 showed how vendor platforms can create cross-airport vulnerabilities. Airports incur additional costs on segmentation firewalls and continuous monitoring, a burden that smaller hubs struggle to absorb within their capital programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Airport Capacity: Mid-Tier Hubs Drive Modernization Spending

Airports processing 25 to 40 million passengers captured 33.47% of the North America airport baggage handling systems market in 2025, mirroring the overall 9.75% CAGR to 2031 as facilities like Austin-Bergstrom and Phoenix Sky Harbor tackle decade-old bottlenecks. Passenger growth of 12-15% between 2019 and 2024 outpaced that of mega-hubs, yet legacy conveyors were sized for far lower volumes. Projects now emphasize tote-based or destination-coded vehicle architectures, which can increase throughput per conveyor foot by up to 40%.

Grand Rapids’ Gerald R. Ford International proved tote systems viable for sub-10-million-passenger airports, achieving 99.5% tracking accuracy and saving USD 800,000 annually in mishandling compensation.[3]BEUMER Group, “Gerald R. Ford International Airport Individual Carrier System Installation,” beumergroup.com The success is spurring peers in the 5 to 15 million passengers segment to consider modular upgrades rather than full belt replacements, though funding gaps continue to prolong the decision-making cycle.

By Solution: Tracking Systems Outpace Core Conveyance

Tracking and tracing modules are advancing at a 10.65% CAGR, the swiftest among solutions, as carriers aim to replicate Delta’s 99.9% RFID accuracy benchmark and cut penalty payouts. Conveying and sorting platforms remain the revenue anchor in the North America airport baggage handling systems market, with a 37.86% share in 2025, but grow at a slower rate of 9.2% as airports overlay sensors onto existing belts.

Security screening systems follow at 9.8%, buoyed by CT-EDS mandates worth USD 1.3 billion in 2024. Early-bag storage modules and reclaim automation are experiencing significant growth. Yet bundled contracts, such as Austin-Bergstrom’s integrated scope, demonstrate that airports are increasingly seeking one-stop packages to mitigate risk.

By Technology: AI Software Leads Amid Barcode Dominance

AI engines expand at 12.87%, the fastest among technology buckets, leveraging predictive analytics to minimize downtime and speed reconciliations. Barcode labeling still commands 31.88% share in 2025, yet growth lags at 7.2% as airports migrate toward RFID’s superior read rates for IATA 753 compliance.

IoT sensors feed data lakes that expose latent choke points, such as a 4-minute merge delay uncovered at one central hub. Robotics and autonomous vehicles, though niche, post double-digit gains driven by showcase pilots at Cincinnati/Northern Kentucky and Heathrow, signalling longer-term labor-savings potential.

By System Type: Tote-Based Systems Gain Amid Conveyor Maturity

Conveyor belts dominate the North America airport baggage handling systems market with a 49.98% share in 2025, but register only an 8.9% growth outlook, reflecting technological maturity and space inefficiencies. Tote-based and individual carrier systems expand at an annual rate of 11.60%, cited for achieving 30-40% floor-space savings and 99.5% tracking accuracy in deployments at Los Angeles International and Toronto Pearson.

Cross-belt and tilt-tray sorters maintain relevance with mid-single-digit growth, especially where brownfield constraints lend themselves to incremental sorter swaps, such as Southwest Airlines’ 8,400-bag-per-hour unit at Denver.

Geography Analysis

The United States dominated 78.56% of the North America airport baggage handling systems market in 2025, driven by TSA CT-EDS procurements exceeding USD 1.3 billion and a five-year FAA infrastructure program valued at USD 2.6 billion. Domestic throughput reached 1.037 billion passengers in 2024, generating an average of 2.5 million daily screenings and putting pressure on hubs to fast-track conveyor replacements at Austin-Bergstrom, Denver, Miami, and Seattle-Tacoma. Climate resilience adds another layer of investment, with elevated systems and surge barriers reducing projected flood losses by USD 10-15 million per airport annually.

Mexico is the fastest riser, with a 10.21% CAGR from 2026 to 2031, as passenger counts were projected to reach 110 million in 2024, driven by nearshoring and business travel.[4]Mexican Ministry of Communications and Transportation, “Airport Infrastructure Investment Program 2024–2026,” sct.gob.mx Capacity expansions at Mexico City, Cancún, and Monterrey channel approximately USD 2.5 billion into terminals; however, baggage-hall bottlenecks persist, resulting in claim times of up to 22 minutes during peak periods.

Competitive Landscape

Consolidation is reshaping vendor dynamics in the North America airport baggage handling systems market. Vanderlande’s 2025 takeover of Siemens Logistics created a portfolio that commands more than 30% of large-hub contracts, enabling turnkey design, build, and operate offerings. Penalty-backed service-level agreements stipulate 99.5% tracking accuracy and 99.9% uptime, raising entry barriers for mid-tier integrators.

Software-centric models are emerging as growth engines. SITA’s WorldTracer generates recurring revenue across 2,800 airports, prompting hardware incumbents to launch digital-twin analytics to lock in service margins. Smaller challengers, such as Pteris Global and Glidepath, pursue regional airports with 20-30% lower list prices; however, limited maintenance footprints and elongated commissioning periods temper their competitiveness. Post-attack procurement criteria emphasize cybersecurity hardening, with the 2024 breach in Seattle-Tacoma catalyzing the implementation of mandatory network segmentation, multi-factor authentication, and 72-hour recovery guarantees.

North America Airport Baggage Handling Systems Industry Leaders

Vanderlande Industries B.V.

BEUMER Group GmbH & Co. KG

Daifuku Co., Ltd.

Smiths Group plc

Rapiscan Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Leonardo bolstered its presence in US airport operations by clinching two significant contracts for baggage handling system solutions. These contracts, valued at over USD 120 million, are for Houston Hobby Airport (HOU) and Melbourne Orlando International Airport (MLB). With these initiatives, Leonardo aims to modernize and optimize baggage operations, ensuring seamless integration with the airports' daily functions. This upgrade is poised to address the anticipated surge in traffic demand by 2026.

- June 2024: Toronto City Airport tapped Alstef Group to enhance its baggage handling system. This upgrade aligns with the airport's initiative to integrate US Customs and Border Protection (CBP) preclearance processing. The revamped outbound conveyor system will feature a new transfer line, sortation conveyors, a manual encode station, an inline screening system, a bag recall vertical lift, and a make-up carousel, all specifically for US CBP bags. Beyond these conveyor enhancements, Alstef Group is set to install and activate the Baggage Imaging and Weight Identification System (BIWIS) to aid US CBP officers.

North America Airport Baggage Handling Systems Market Report Scope

The North America airport baggage handling systems market encompasses automated equipment, software platforms, and integrated solutions for passenger baggage processing from check-in through reclaim, including conveying systems, sortation technologies, security screening integration, tracking solutions, and lifecycle services, while excluding manual handling equipment and cargo-specific systems, with market evolution toward AI-powered automation and biometric integration.

The North America airport baggage handling systems market is segmented by airport capacity, solution, technology, system type, and geography. By airport capacity, the market is segmented into up to 15 million, 15 to 25 million, 25 to 40 million, and above 40 million. By solution, the market is segmented into check-in and ticketing systems, security screening systems, conveying and sorting systems, early baggage storage, baggage reclaim/unloading, and tracking and tracing. By technology, the market is segmented into barcode, RFID, IoT sensors and edge devices, robotics and autonomous vehicles, and AI/ML software. By system type, the market is segmented into conveyor belt systems, tilt-tray and cross-belt sorters, destination-coded vehicles, tote-based/individual carrier systems, and hybrid and other emerging systems. The report also offers market sizes and forecasts for three countries across the region. For each segment, the market sizes and forecasts have been done based on value (USD).

By Airport Capacity

| Up to 15 million |

| 15 to 25 million |

| 25 to 40 million |

| Above 40 million |

By Solution

| Check-In and Ticketing Systems |

| Security Screening Systems |

| Conveying and Sorting Systems |

| Early Baggage Storage |

| Baggage Reclaim/Unloading |

| Tracking and Tracing |

By Technology

| Barcode |

| RFID |

| IoT Sensors and Edge Devices |

| Robotics and Autonomous Vehicles |

| AI/ML Software |

By System Type

| Conveyor Belt Systems |

| Tilt-Tray and Cross-Belt Sorters |

| Destination-Coded Vehicle (DCV) |

| Tote-based/Individual Carrier Systems |

| Hybrid and Other Emerging Systems |

By Geography

| United States |

| Canada |

| Mexico |

| By Airport Capacity | Up to 15 million |

| 15 to 25 million | |

| 25 to 40 million | |

| Above 40 million | |

| By Solution | Check-In and Ticketing Systems |

| Security Screening Systems | |

| Conveying and Sorting Systems | |

| Early Baggage Storage | |

| Baggage Reclaim/Unloading | |

| Tracking and Tracing | |

| By Technology | Barcode |

| RFID | |

| IoT Sensors and Edge Devices | |

| Robotics and Autonomous Vehicles | |

| AI/ML Software | |

| By System Type | Conveyor Belt Systems |

| Tilt-Tray and Cross-Belt Sorters | |

| Destination-Coded Vehicle (DCV) | |

| Tote-based/Individual Carrier Systems | |

| Hybrid and Other Emerging Systems | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America airport baggage handling systems market?

The North America airport baggage handling systems market is valued at USD 0.87 billion in 2026 and is projected to reach USD 1.37 billion by 2031, expanding at a 9.18% CAGR.

Which airport capacity segment contributes the most spending on baggage systems?

Facilities handling 25 to 40 million passengers account for 33.47% of 2025 revenue and are expanding in line with overall growth.

How fast are tote-based baggage handling systems growing in North America?

Tote-based and individual carrier architectures are advancing at an 11.60% CAGR to 2031 due to superior tracking accuracy and space efficiency.

Why are RFID solutions gaining traction in baggage handling?

IATA Resolution 753 compliance and demonstrated 99.9% read accuracy at airlines such as Delta are driving airports to replace barcode-only tracking.

What role does artificial intelligence play in reducing mishandled baggage?

AI-enabled modules like SITA WorldTracer Auto Reflight match bags to itineraries in under two minutes, cutting compensation costs and improving passenger satisfaction.

Which country in North America shows the fastest market growth?

Mexico leads with a 10.21% CAGR to 2031, fueled by nearshoring-related passenger expansion and ongoing terminal upgrades.

Page last updated on: