North America Agricultural Chemical Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

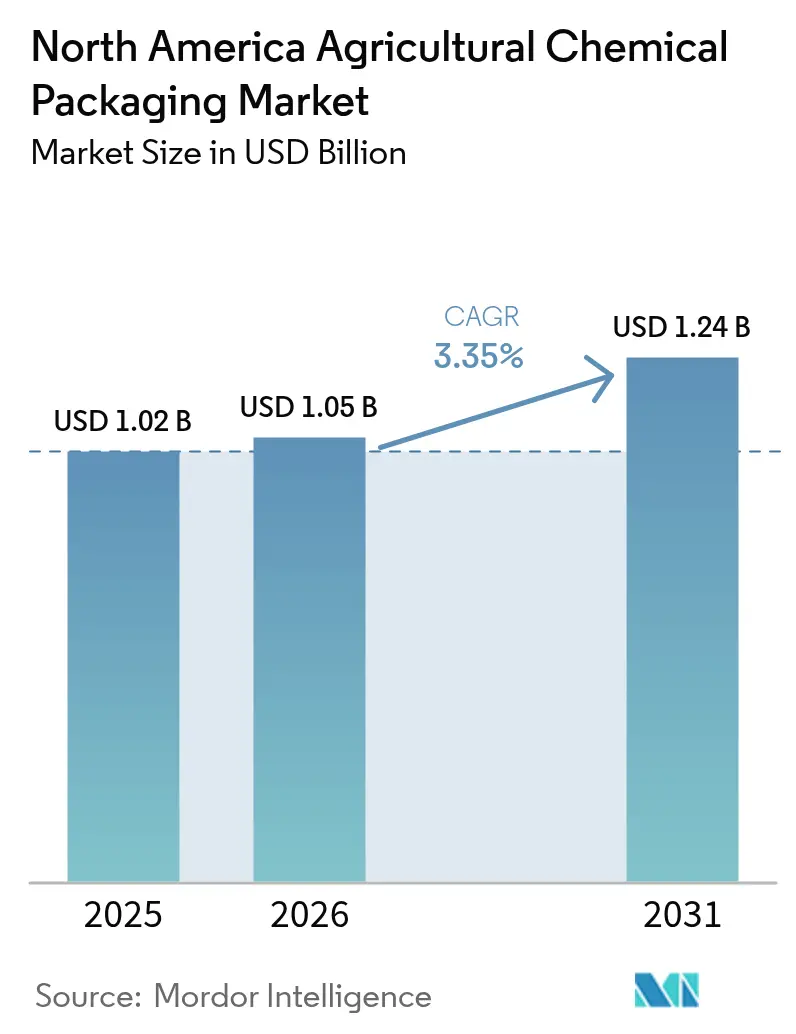

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

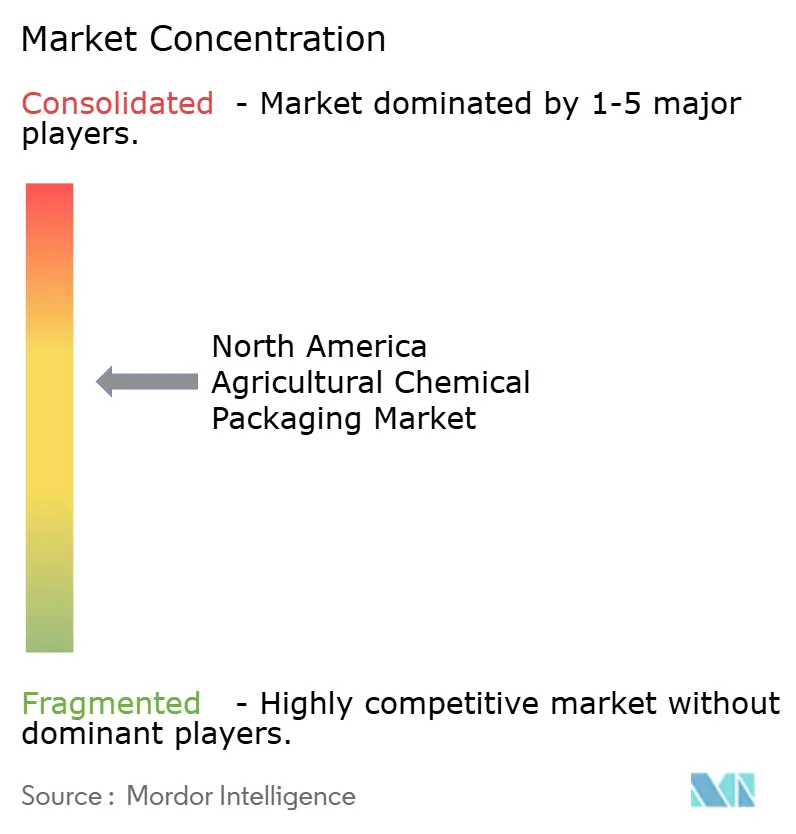

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Agricultural Chemical Packaging Market Analysis by Mordor Intelligence

The North America agricultural chemical packaging market size is expected to grow from USD 1.02 billion in 2025 to USD 1.05 billion in 2026 and is forecast to reach USD 1.24 billion by 2031 at 3.35% CAGR over 2026-2031. This steady expansion shows the market’s shift from volume-driven growth toward value-added formats that function as precision-application enablers rather than simple containers. Precision farming, sustainability mandates, and tighter stewardship rules are prompting suppliers to redesign pack sizes, barrier properties, and traceability features to protect active ingredients and support data-driven application. Plastic remains the dominant material, but bio-based and composite options record the fastest gains as extended producer responsibility (EPR) fees reward recyclable formats. Capacity investments in domestic resin and conversion lines further stabilize supply while enabling specialty grades that meet regulated performance thresholds.

Key Report Takeaways

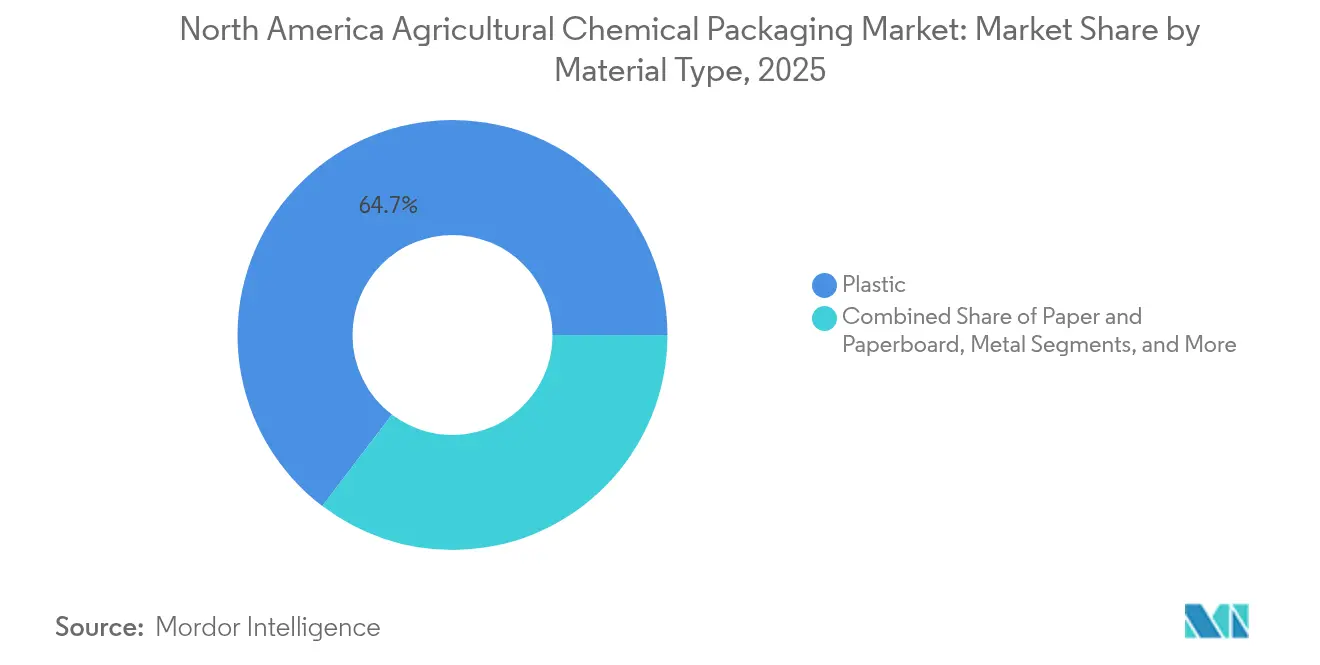

- By material type, plastic retained 64.65% of the North America agricultural chemical packaging market share in 2025, whereas composite and bio-based materials are projected to grow at a 4.35% CAGR through 2031.

- By product type, bags and pouches accounted for 43.92% of the North America agricultural chemical packaging market size in 2025, while intermediate bulk containers (IBCs) are expected to advance at a 4.67% CAGR to 2031.

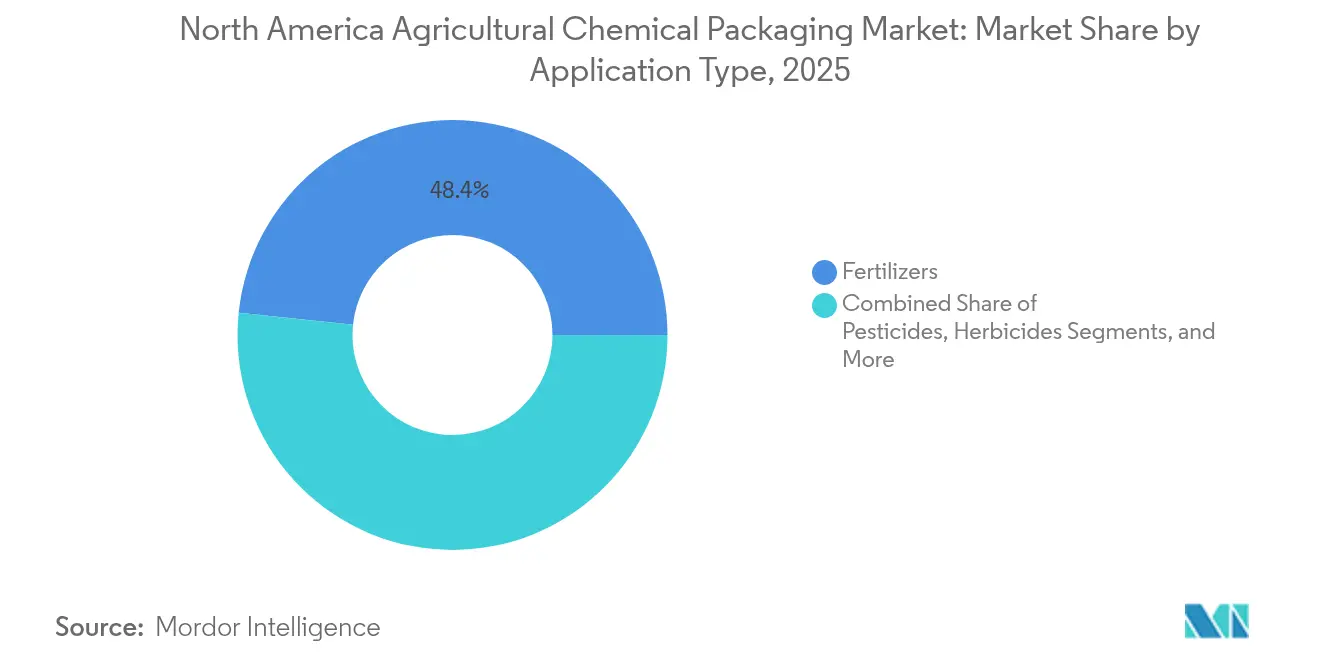

- By application, fertilizers led with 48.35% of the North America agricultural chemical packaging market share in 2025 and biologicals and plant growth regulators are expanding at a 5.11% CAGR through 2031.

- By capacity range, containers under 20 liters contributed 51.02% of the North America agricultural chemical packaging market size in 2025, whereas units over 200 liters are set to post the quickest 4.89% CAGR to 2031.

- By geography, the United States held 70.85% of regional revenue in 2025 while Mexico is poised for the highest 4.92% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on agriculture chemical packaging market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Agricultural Chemical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Controlled-release and water-soluble films | +0.8% | United States Midwest and wider region | Medium term (2-4 years) |

| Recyclable and bio-based packaging shift | +0.6% | United States and Canada, Mexico catching up | Long term (≥ 4 years) |

| Smaller-dose high-barrier precision packs | +0.5% | Great Plains and Prairie provinces | Short term (≤ 2 years) |

| Bulk-container reusability programs | +0.4% | United States and Canada | Medium term (2-4 years) |

| Digitally traceable stewardship solutions | +0.3% | United States, moderate Canada uptake | Medium term (2-4 years) |

| Domestic resin and conversion investments | +0.2% | United States Gulf Coast and Canadian hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Controlled-Release and Water-Soluble Film Adoption

Controlled-release packaging extends active ingredient efficacy and lowers labor inputs, answering the operational efficiency needs of large North American farms. Water-soluble films dissolve entirely in spray tanks and remove container-disposal headaches, improving safety and field productivity. Herbicide and fungicide applications benefit most because dosing precision directly affects yields and regulatory compliance. Precision-farming software accelerates uptake, as farmers favor packs that align with GPS-guided systems and variable-rate maps. As a result, packaging shifts from passive containment to a digitally integrated delivery component embedded in farm management workflows.

Sustainability-Driven Shift to Recyclable and Bio-Based Formats

EPR rules in five U.S. states impose eco-modulated fees that reward materials with recycled or renewable content, nudging converters toward polylactic acid (PLA), polyhydroxyalkanoate (PHA), and other bio-based resins. Cost premiums are narrowing as commercial-scale plants, such as Citroniq’s USD 12 million polypropylene line in Nebraska, increase supply. Brand sustainability pledges add downstream pressure, making carbon-footprint disclosure and recyclability critical purchase criteria for growers and input distributors. R&D now focuses on matching the moisture, oxygen, and UV barriers of conventional resins so that sensitive herbicides and biologicals remain stable throughout multi-season storage.

Precision-Farming Demand for Smaller-Dose, High-Barrier Packs

Variable-rate technologies boost demand for 250-milliliter to 5-liter containers that support precise titration across heterogeneous fields. Multi-layer films using nanocomposites deliver the oxygen and moisture barriers required to keep biological actives potent, while RFID tags tie container identifiers to agronomic software for automated compliance logs. Suppliers view these premium formats as revenue-enhancement opportunities that justify higher unit prices through dosage accuracy and shelf-life extension.

Bulk-Container Re-usability Programs by Large Distributors

Rental models operated by service providers such as CHEP illustrate how pooled IBC fleets lower capital outlays, standardize handling, and cut waste streams. Seasonal distributors appreciate on-demand capacity that scales with harvest cycles, while digital tracking enables real-time inventory optimization and predictive maintenance. Regulatory discussions around deposit systems further strengthen the economic case for multi-trip containers over single-use drums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening UN and DOT hazardous-goods rules | -0.4% | United States and Canada | Short term (≤ 2 years) |

| Volatile polymer and metal feedstock prices | -0.6% | North America-wide, Gulf Coast exposure | Short term (≤ 2 years) |

| Farmer push-back on packaging waste fees | -0.2% | U.S. EPR states | Medium term (2-4 years) |

| Distributor destocking cycles post-2023 | -0.3% | United States and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening UN and DOT Hazardous-Goods Regulations

Enhanced performance tests for drums and IBCs raise certification expenses by USD 50,000-100,000 per product line, a burden that smaller converters struggle to absorb. Inventory phase-outs of non-compliant stock disrupt supply chains and accelerate consolidation as niche suppliers seek acquisition by firms with established compliance laboratories and testing budgets.

Volatile Polymer and Metal Feedstock Prices

Polypropylene and polyethylene spot prices climbed 15% in March 2025, mirroring energy-market swings that feed directly into resin costs.[1]U.S. Energy Information Administration, “Petrochemical Feedstock Price Trends,” eia.gov Steel volatility likewise reshapes drum pricing. Large converters hedge or diversify sourcing, whereas small-scale players endure margin compression and delay capex decisions amid uncertain payback windows. The unpredictability complicates pricing agreements with distributors who demand stable year-ahead budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Dominance Faces Bio-Based Disruption

Plastic captured 64.65% of the North America agricultural chemical packaging market in 2025 owing to its high chemical resistance and favorable cost-to-performance ratio. The segment’s CAGR remains modest as bio-based and composite substrates outpace at 4.35%, propelled by EPR incentives and farm-level sustainability pledges. Composite laminates marry mechanical strength with downgauging potential, cutting polymer mass by up to 15% without forfeiting puncture resistance. Bio-based polypropylene sourced from non-food biomass increasingly meets moisture and oxygen protection criteria, positioning it for premium-priced specialty herbicide and biological packs.

Demand heterogeneity is widening: fertilizers rely on rugged HDPE jugs for cost efficiency, whereas living microbial products require oxygen-scavenging multilayers. Consequently, converters diversify material portfolios to hedge against policy changes and customer mix volatility. The North America agricultural chemical packaging market size devoted to bio-based formats is still niche, but early movers gain specification lock-ins as sustainability scorecards become standard in procurement.

By Product Type: IBCs Accelerate on Efficiency Demands

Bags and pouches delivered 43.92% revenue in 2025 because they fit existing filling lines, ship flat, and support water-soluble or controlled-release films. Yet IBCs register the highest 4.67% CAGR through 2031 as bulk intermediaries consolidate volumes to trim freight and labor. Digital-ready IBCs, fitted with QR plates or low-power sensors, shift containers from static storage to active visibility nodes in distributor networks.

Flexible intermediate bulk containers (FIBCs) and rigid combo totes broaden applications, especially for granular fertilizers where pallet-layer stability matters. Conversely, pouches evolve toward multilayer formats with built-in surfactants that improve spray-tank dispersion. The North America agricultural chemical packaging market share of pouches stays meaningful due to their role in precision dosing, yet the service-based economics of pooled IBC programs attract large retailers seeking waste-reduction credits and cost predictability.

By Application Type: Biologicals Drive Innovation Beyond Traditional Chemicals

Fertilizers maintained 48.35% market share in 2025, anchored by predictable bulk demand cycles and mature moisture-barrier needs. However, biologicals and plant growth regulators carve a 5.11% CAGR niche as integrated pest-management adoption expands. Live microbial inoculants necessitate refrigerated storage and high-barrier vials, prompting converters to adapt pharmaceutical-grade laminates for farm distribution.

Pesticide and herbicide packs push controlled-release and child-resistant closures to satisfy safety rules while aligning with labor-saving spray regimes. Segment diversity forces suppliers to maintain broad technical capabilities across moisture, oxygen, and UV protection. Thus, the North America agricultural chemical packaging market size devoted to specialty biologicals, though still small, commands superior margins and drives multilayer film R&D.

By Capacity Range: Precision Agriculture Reshapes Size Preferences

Containers below 20 liters held 51.02% share in 2025 as variable-rate seed and nutrient maps require small batches matched to field zones. Near-term growth persists, yet packages above 200 liters deliver the quickest 4.89% CAGR as national distributors routinize centralized blending and refill stations. Intermediate 21-200 liter drums cater to mid-scale horticulture and specialty-crop users demanding ergonomic handling without sacrificing throughput.

Smaller packs integrate RFID chips or near-field-communication tags that automate spray-record uploads into compliance databases. Large-capacity formats embed steel-frame reinforcements for rack safety and leverage HDPE liners for chemical integrity. Consequently, converters design modular lines capable of switching from 10-liter multilayer jugs to 1,000-liter composite IBCs within one shift to capture the full capacity spectrum of the North America agricultural chemical packaging market.

Geography Analysis

The United States controlled 70.85% of the North America agricultural chemical packaging market in 2025 thanks to its vast crop acreage, sophisticated distribution, and robust regulatory infrastructure. Precision-ag adoption is highest, creating demand for digitally traceable packs, controlled-release films, and high-barrier laminates that keep biologicals viable. EPR legislation in five states adds tiered fees favoring recycled content, accelerating material shifts toward multilayer composite grades that separate easily at recycling plants.

Canada represents a mature but weather-challenged landscape where packaging must withstand cold-chain disruptions and compressed application windows. Carbon tax expenses of USD 8,000-15,000 per grain farm encourage logistics optimization, prompting uptake of pooled IBC systems and downgauged multilayer films that lower outbound weight. Provincial alignment with U.S. hazardous-goods codes eases cross-border flows yet requires bilingual labeling and specific metric/imperial markings, adding complexity for converters.

Mexico is the fastest-growing sub-region at 4.92% CAGR, driven by near-shoring of ag-chemical formulation plants and irrigation-led acreage expansion. Modernization efforts spur demand for packaging that meets stricter labeling norms and potentially higher excise taxes on agrochem inputs. Water scarcity concerns raise interest in controlled-dose pouches and drip-fertigation soluble films tailored to reduce runoff. Mexico thus offers early-stage opportunities for suppliers able to transfer U.S. technology at cost points suited to local purchasing power.

Competitive Landscape

Industry consolidation shapes supplier dynamics as mega-mergers enlarge purchasing clout and R&D scale. Amcor’s proposed USD 8.4 billion purchase of Berry Global would create a USD 27.2 billion resin-buying powerhouse, streamlining raw-material negotiation and industrial footprint. [3]Amcor plc, “Investor Presentation Q2 FY2025,” amcor.com Smurfit Kappa’s USD 12.7 billion deal for WestRock strengthens corrugated offerings for secondary farm-input shipments. ProAmpac targets USD 5 billion revenue by 2028 by acquiring niche converters that possess precision-ag film know-how, illustrating a roll-up strategy that tilts the North America agricultural chemical packaging market toward a handful of diversified groups.

Technology differentiation, not just scale, is emerging as the key moat. CHEP’s tracking-enabled IBC rental service embeds logistics data feeds into customer ERPs, raising switching costs. Greif’s ModCan modular drum blends square-footage optimization with UN-certified performance to recapture share in concentrated-chemical transport. Smaller converters survive by specializing in bio-based resins or narrow-gauge blown-film lines that larger firms find uneconomical to tool.

Compliance investment is another barrier. The capital needed for UN 4G/11H testing rigs and in-house labs reinforces consolidation because only larger groups can amortize costs across high-volume SKU portfolios. Consequently, the North America agricultural chemical packaging industry shows a gradual but unmistakable tilt toward vertically integrated multinationals capable of spanning resin production through distribution-ready container fleets.

North America Agricultural Chemical Packaging Industry Leaders

Amcor plc

Greif Inc.

Mondi plc

Sonoco Products Company

ProAmpac LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Amcor reported mixed Q2 FY2025 North American results: low single-digit growth in flexibles but mid single-digit decline in rigid beverage packs.

- January 2025: ProAmpac outlined a USD 5 billion revenue ambition by 2028, anchored in acquisitions and vertical integration across specialty films and pouches.

- January 2025: Greif unveiled ModCan modular packaging at Pack-Expo Chicago, promising better load efficiency for agrochemical drums.

- December 2024: Sonoco completed a USD 3.9 billion purchase of Eviosys, expanding metal aerosol and closure capabilities.

North America Agricultural Chemical Packaging Market Report Scope

The study on the North American agricultural chemical packaging market tracks the vendors' revenue based on the market demand for the end-packaging-based products across key segments, as captured in the segmentation. The key product types considered for the study include bags & pouches, IBCs, cans & containers, and other product types. The breakdown based on material type is provided for plastic, paper & paperboard, metal, and other materials.

| Plastic |

| Paper and Paperboard |

| Metal |

| Composite and Bio-Based Materials |

| Bags and Pouches |

| Containers and Cans |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Other Product Types |

| Fertilizers |

| Pesticides |

| Herbicides |

| Biologicals and Plant Growth Regulators |

| ≤ 20 L |

| 21 – 200 L |

| > 200 L |

| United States |

| Canada |

| Mexico |

| By Material Type | Plastic |

| Paper and Paperboard | |

| Metal | |

| Composite and Bio-Based Materials | |

| By Product Type | Bags and Pouches |

| Containers and Cans | |

| Intermediate Bulk Containers (IBCs) | |

| Drums | |

| Other Product Types | |

| By Application Type | Fertilizers |

| Pesticides | |

| Herbicides | |

| Biologicals and Plant Growth Regulators | |

| By Capacity Range | ≤ 20 L |

| 21 – 200 L | |

| > 200 L | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America agricultural chemical packaging market in 2026?

It is valued at USD 1.05 billion in 2026 and is forecast to reach USD 1.24 billion by 2031.

Which material holds the biggest share of agricultural chemical packaging in North America?

Plastic commands 64.65% of regional revenue due to cost efficiency and chemical resistance.

What is driving the fastest growth in product types?

Intermediate bulk containers show a 4.67% CAGR as distributors prioritize reusability and logistics savings.

Why are smaller pack sizes gaining popularity?

Precision-agriculture equipment relies on smaller-dose, high-barrier containers that enable accurate variable-rate applications.

Which country is the fastest-growing market within North America?

Mexico is projected to grow at a 4.92% CAGR, aided by near-shoring and farm-modernization trends.

How are EPR regulations influencing packaging choices?

Eco-modulated fees in five U.S. states incentivize recyclable and bio-based formats, accelerating material shifts toward high-PCR and renewable resins.

Page last updated on: