Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

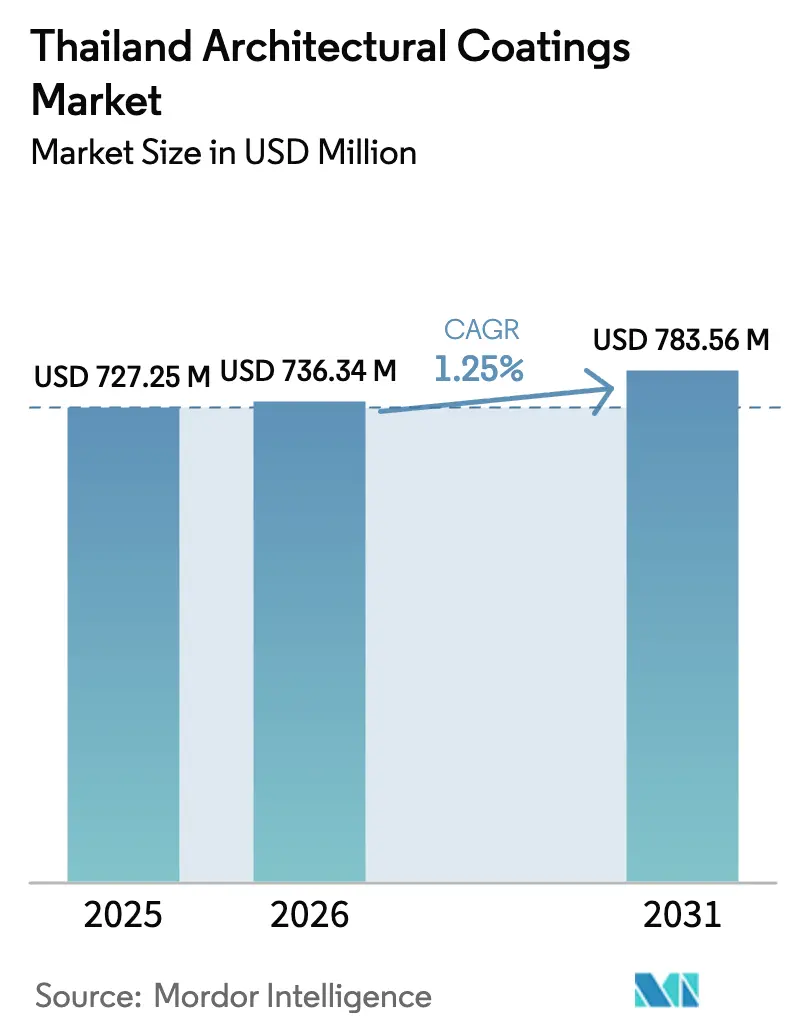

| Base Year Market Size (2025) | USD 727.25 Million |

| Market Size (2026) | USD 736.34 Million |

| Market Size (2031) | USD 783.56 Million |

| Growth Rate (2026 - 2031) | 1.25% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Architectural Coatings Market Analysis by Mordor Intelligence

Thailand Architectural Coatings Market size in 2026 is estimated at USD 736.34 million, growing from 2025 value of USD 727.25 million with 2031 projections showing USD 783.56 million, growing at 1.25% CAGR over 2026-2031. Muted volume growth reflects a mature demand base balanced by structural tailwinds—including construction spending linked to the Eastern Economic Corridor (EEC), rising repaint cycles for an aging building stock, and consumer preference for low-VOC products. Regulatory momentum toward safer chemistries reinforces the dominance of water-borne formulations, while raw-material volatility, especially titanium dioxide, keeps margin management at center stage.

Key Report Takeaways

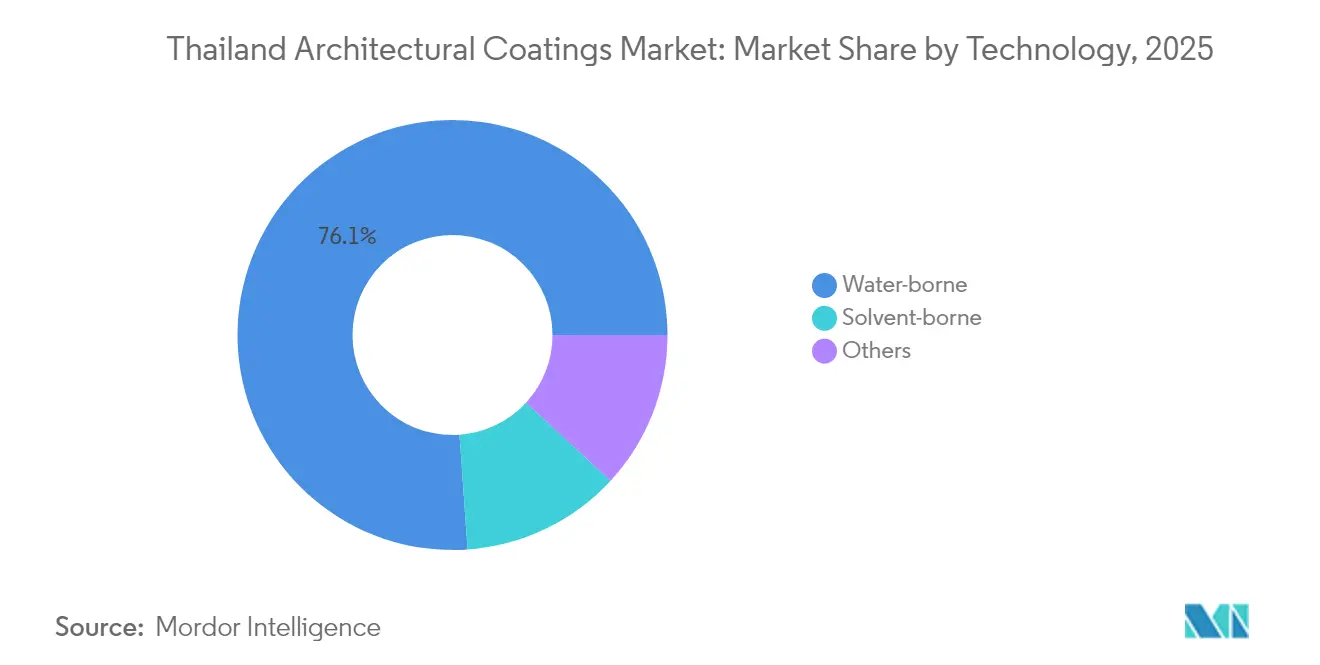

- By technology, water-borne coatings led with 76.12% revenue share in 2025; solvent-borne coatings are forecast to expand at a 1.39% CAGR through 2031.

- By resin type, acrylic resins accounted for 53.62% of the Thailand architectural coatings market size in 2025; polyurethane resins exhibit the highest projected CAGR at 1.47% to 2031.

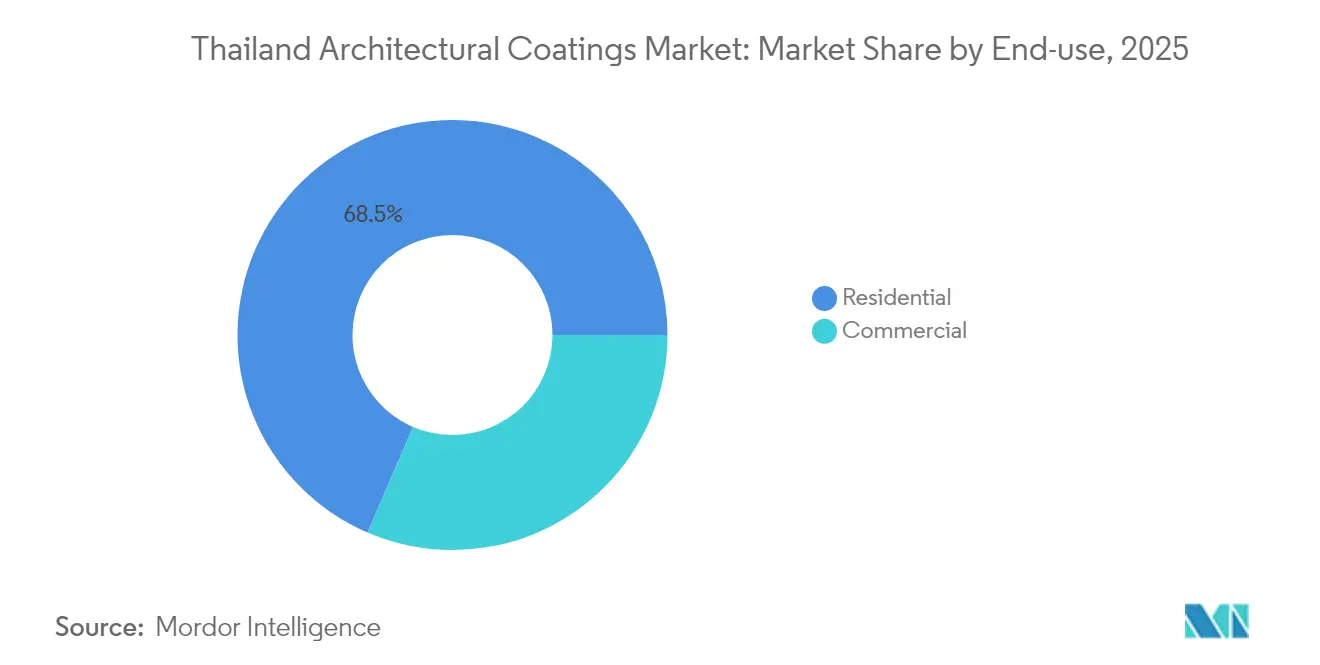

- By end-use, residential construction captured 68.54% share of the Thailand architectural coatings market size in 2025; commercial applications are advancing at a 1.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation and housing demand | +0.3% | National, concentrated in Bangkok Metropolitan Region | Medium term (2-4 years) |

| Government infrastructure and smart-city projects | +0.4% | National, with EEC focus in Eastern provinces | Long term (≥ 4 years) |

| Shift toward low-VOC water-borne systems | +0.2% | National, driven by regulatory compliance | Short term (≤ 2 years) |

| Ageing building stock driving repaint cycles | +0.3% | National, higher impact in urban centers | Medium term (2-4 years) |

| Modular construction and factory-applied finishes | +0.2% | National, concentrated in industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Housing Demand

Continued migration into metropolitan and secondary urban nodes sustains underlying demand for the Thailand architectural coatings market even as lending standards stay tight. Large mixed-use projects such as The Forestias, carrying a THB 125 billion (~USD 3.87 billion) budget across 398 rai, illustrate the pull for premium, environmentally aligned finishes that can endure tropical humidity while meeting green-building criteria[1]MQDC Communications, “The Forestias Mega Project,” mqdc.com. High-rise density demands façade systems with robust UV and moisture resistance, pushing formulators toward acrylic and polyurethane chemistries. Population inflows into secondary cities prompt regional warehouses and tinting centers to ensure color matching close to point of use. A positive correlation between new household formation and per-capita paint consumption signals a stable volume baseline, cushioning the modest headline CAGR expected for the Thailand architectural coatings market.

Government Infrastructure and Smart-City Projects

Double-track rail extensions, elevated mass-transit lines, and port upgrades require high-build solvent-borne epoxies and polyurethanes for corrosion control, while public-facing elements, stations, pedestrian bridges, urban furniture, consume color-stable water-borne acrylics. The Bangkok Metropolitan Administration’s repainting of 300+ bridges, executed with Nippon Paint materials valued at THB 10 million, underscores the scale of municipal maintenance cycles. Smart-city pilot zones integrate sensor housings and e-mobility infrastructure that demand specialty coatings for electromagnetic shielding and aesthetic integration. Regional logistics corridors linking Cambodia, Laos, and Myanmar expand export avenues for Thai manufacturers, giving the Thailand architectural coatings market a regional staging role. Sustainability clauses in public procurement feed adoption of low-VOC and recycled-content offerings, pushing suppliers to certify products under ecolabel schemes.

Shift Toward Low-VOC Water-Borne Systems

Thailand’s Hazardous Substance Act amendments, along with impending VOC caps modeled on South Korean and Chinese regimes, accelerate formulation shifts. Product stewardship costs for solvent lines, from permitting to stack-emission monitoring, are steering research and development budgets toward water-borne platforms with modified nano-acrylic or self-crosslinking polyurethane binders[2]“Global VOC Legislation,” International-marine, international-marine.com . TOA Paint’s Aqua Shield, promoted as Asia’s first multi-substrate water-based topcoat, claims triple the durability of solvent alternatives and a nine-fold VOC reduction, offering a benchmark for premium positioning. Consumer awareness of indoor air quality rises with the spread of ESG-certified office towers and green-label housing projects, closing the cost–value gap in favor of low-emission products. Multinationals mirror the trend: PPG opened a water-borne automotive-coatings facility in Chonburi in 2025, bringing transferable resin technologies and process know-how to the wider Thailand architectural coatings industry.

Aging Building Stock Driving Repaint Cycles

Buildings erected during Thailand’s 1990–2010 construction wave now approach critical maintenance milestones, creating predictable repaint windows that stabilize baseline demand. Commercial properties generally recoat every 5–7 years; residential structures cycle at 7–10 years, depending on exposure and initial film build. Hotel and resort operators, buoyed by occupancy rates inching toward pre-2019 levels, accelerate façade and interior refreshes ahead of the 2026 high-season, favoring washable low-sheen acrylics and anti-fungal formulations. Office tenants pivoting into ESG-compliant buildings specify low-VOC paints to secure LEED or WELL points, bolstering premium SKU velocity. Rising labor costs encourage longer-life choices, polyurethane clears for high-traffic lobbies or silicone-modified elastomerics for exterior walls, reducing total cost of ownership.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (TiO₂, solvents) | -0.2% | Global supply impact, affecting all Thai manufacturers | Short term (≤ 2 years) |

| Stricter solvent-emission regulations | -0.1% | National, with enforcement variations by province | Short term (≤ 2 years) |

| Skilled labour shortage for quality application | -0.1% | National, more severe in provincial markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Solvent-Emission Regulations

Proposed VOC caps and mandatory Pollutant Release and Transfer Register (PRTR) reporting elevate compliance costs, particularly for SMEs lacking in-house EHS expertise. Plant upgrades, incinerators, regenerative thermal oxidizers, closed-loop solvent recovery, require capital outlays that erode profitability during transition. Regulatory enforcement can vary by industrial estate, creating planning uncertainty. Market-wide, any delays in reformulation could cause SKU rationalization, temporarily reducing choice for repaint contractors and elongating approval cycles for new projects reliant on specific colors or textures.

Skilled Labor Shortage

Thailand’s construction sector competes with higher-wage logistics and electronics industries for labor, leaving a shortfall of trained applicators. Poor surface preparation or incorrect film build leads to premature coating failure, warranty claims, and brand damage for suppliers. The Thailand architectural coatings industry responds with applicator certification programs and mobile training labs that tour provincial hubs. Nevertheless, wage inflation raises installed-cost thresholds, potentially deferring discretionary projects, especially in budget-sensitive residential repainting segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Systems Maintain Commanding Lead

Water-borne coatings accounted for 76.12% of the Thailand architectural coatings market in 2025, reflecting a broad regulatory and consumer pivot toward low-VOC solutions. Product innovation centers on modified nano-acrylics that improve scrub resistance and quick-dry traits in humid climates. Retail chains such as HomePro and Thai Watsadu allocate the majority of shelf space to water-borne lines, reinforcing visibility. In parallel, government procurement guidelines increasingly mandate green-label paints, locking in institutional demand.

Despite a smaller revenue base, solvent-borne technologies remain indispensable for metal substrates, marine exposures, and industrial facilities that demand high chemical resistance. The segment is projected to grow at 1.39% CAGR to 2031 as infrastructure megaprojects consume heavy-duty alkyds, epoxies, and polyurethanes. Hybrid water-reducible alkyds are emerging as transition products, offering solvent-type flow with lower VOC levels. Powder and other niche technologies trail in the single digits but find pockets of expansion in factory-applied cladding and aluminum joinery.

By Resin Type: Acrylic Rules While Polyurethane Outperforms

Acrylic chemistry captured 53.62% of total revenue in 2025, translating to roughly USD 390 million of Thailand architectural coatings market size. Thermoplastic acrylics dominate economy interior grades, whereas self-crosslinking variants bolster premium exterior lines. Acrylic versatility extends to elastomeric roof coatings that tolerate thermal movement and resist standing water during monsoon seasons. Manufacturers mix acrylic with silicone additives to upgrade dirt pickup resistance, appealing to condo associations focused on long-cycle maintenance.

Polyurethane is the breakout performer, projected to climb at 1.47% CAGR through 2031 as wood-flooring trends shift to matte-look, high-durability finishes. Water-borne two-component PU systems meet rising indoor-air-quality expectations while delivering gym-floor hardness, positioning the chemistry for steady share gains. Epoxies occupy a specialized slice of the Thailand architectural coatings market, serving parking decks, hospitals, and commercial kitchens that value chemical tolerance. Alkyd and polyester resins survive in legacy products and powder lines but face share drift as environmental rules tighten.

By End-Use: Residential Still Commands But Commercial Gains Pace

Residential demand represented 68.54% of value in 2025 of the Thailand architectural coatings market size. Repaint cycles for detached houses, row homes, and condos drive recurring revenue even when new-build activity softens. Do-it-yourself channels thrive on color-matching kiosks and influencer-led décor campaigns. Consumers upgrade to wash-and-wear mattes and low-odor enamels as lifestyle aspirations rise. Premiumization offsets slower unit growth, sustaining value for retailers and brand owners.

Commercial applications, offices, hotels, malls, deliver the fastest growth at 1.52% CAGR. ESG-qualified office towers require paints contributing to LEED or WELL credits, tilting specifications to low-VOC water-borne epoxies and polyurethanes. The hospitality sector, approaching pre-pandemic occupancy, renovates lobbies and guestrooms with ultra-matt, stain-resistant finishes aimed at international tourists. Retail landlords modernize facades to compete with e-commerce, selecting graffiti-resistant clear coats and signature corporate palettes.

Geography Analysis

Bangkok Metropolitan Region remains the epicenter of the Thailand architectural coatings market. Dense vertical surfaces accelerate repaint turnover due to UV exposure and pollution buildup. Proximity to ports and central logistics hubs ensures rapid replenishment of dealer stocks and supports same-day tinting services.

Eastern provinces, Chonburi, Rayong, Chachoengsao, benefit from EEC incentives that spur industrial parks, airports, and seaports. Salt-laden air necessitates high-performance epoxy and polyurethane systems with certified corrosion-class ratings. Paint suppliers co-locate technical service centers near heavy-industry clusters to provide on-site inspection and coating failure diagnostics, deepening client loyalty.

Tourism-driven southern islands such as Phuket and Samui consume premium exterior alkali-resistant coatings that withstand coastal humidity. Resort operators lean on neutral color schemes that complement natural landscapes yet rely on durable topcoats to delay chalking. Northern cities, Chiang Mai, Khon Kaen, show steady urban expansion, but lower income profiles favor mid-tier brands and contractor-grade finishes, creating a two-speed pricing architecture across the Thailand architectural coatings market.

Competitive Landscape

The market is consolidated in nature. Jotun differentiates via corrosion-protection expertise and automated manufacturing that lifts plant productivity fivefold, compressing cost per liter. Multinationals tap regional research and development centers to introduce global platforms—AkzoNobel weighs a South Asia deco-portfolio review that could channel new investments to Thailand, while PPG’s Chonburi site scales water-borne know-how applicable to architectural lines. Smaller domestic brands compete on price but struggle with VOC-related capex and rising raw-material costs. E-commerce opens a niche for challenger brands offering niche shades shipped direct from micro-factories, though logistical costs limit scale for bulky 18-liter packs. Overall, strategic thrusts concentrate on greener chemistries, omni-channel retail, and tech-enabled color visualization tools, rapidly modernizing the Thailand architectural coatings industry.

Thailand Architectural Coatings Industry Leaders

AkzoNobel N.V.

Jotun

Nippon Paint Holdings Co., Ltd.

TOA Paint Public Company Limited

Kansai Paint Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Jotun launched Majestic Pure Color interior range and NUANCES Global Color Collection 2025 in Thailand, featuring a super-matt, anti-reflective finish across 30 curated shades.

- December 2024: TOA Paint unveiled 2025 Color Trends under the “Seamless Synchrony” concept developed with Thai architects to blend timeless neutrals and vibrant pop-culture hues.

Thailand Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By End-Use

| Residential |

| Commercial |

| By Technology | Water-borne |

| Solvent-borne | |

| Others | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms