Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

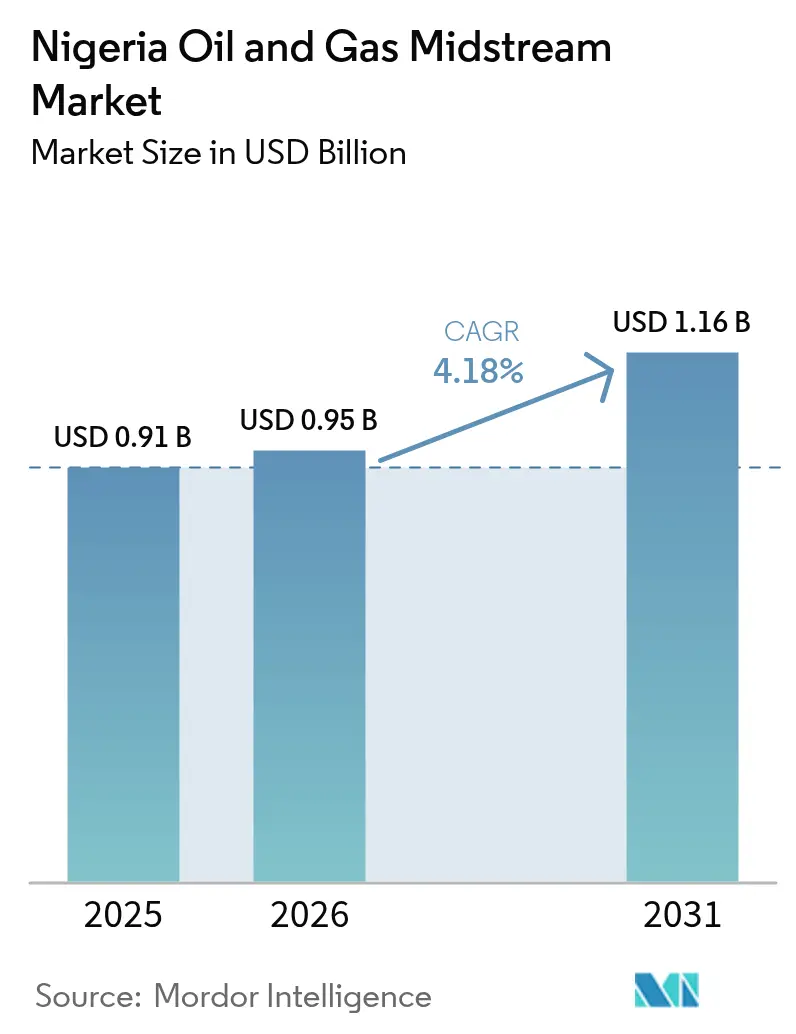

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Oil And Gas Midstream Market Analysis by Mordor Intelligence

Nigeria Oil And Gas Midstream Market size in 2026 is estimated at USD 0.95 billion, growing from 2025 value of USD 0.91 billion with 2031 projections showing USD 1.16 billion, growing at 4.18% CAGR over 2026-2031.

Regulatory certainty provided by the Petroleum Industry Act (PIA) accelerates private investment, yet pipeline vandalism and foreign-exchange volatility still erode capacity utilization. The commissioning of the USD 10 billion NLNG Train 7 project, which expands liquefaction capacity from 22 million to 30 million tonnes per annum (tpa) by 2027, underscores the shift toward gas-led diversification. Meanwhile, the 650,000-barrel-per-day Dangote Refinery reconfigures domestic product flows and spurs the construction of dedicated pipelines, which trim trucking costs and reduce import dependence.

Key Report Takeaways

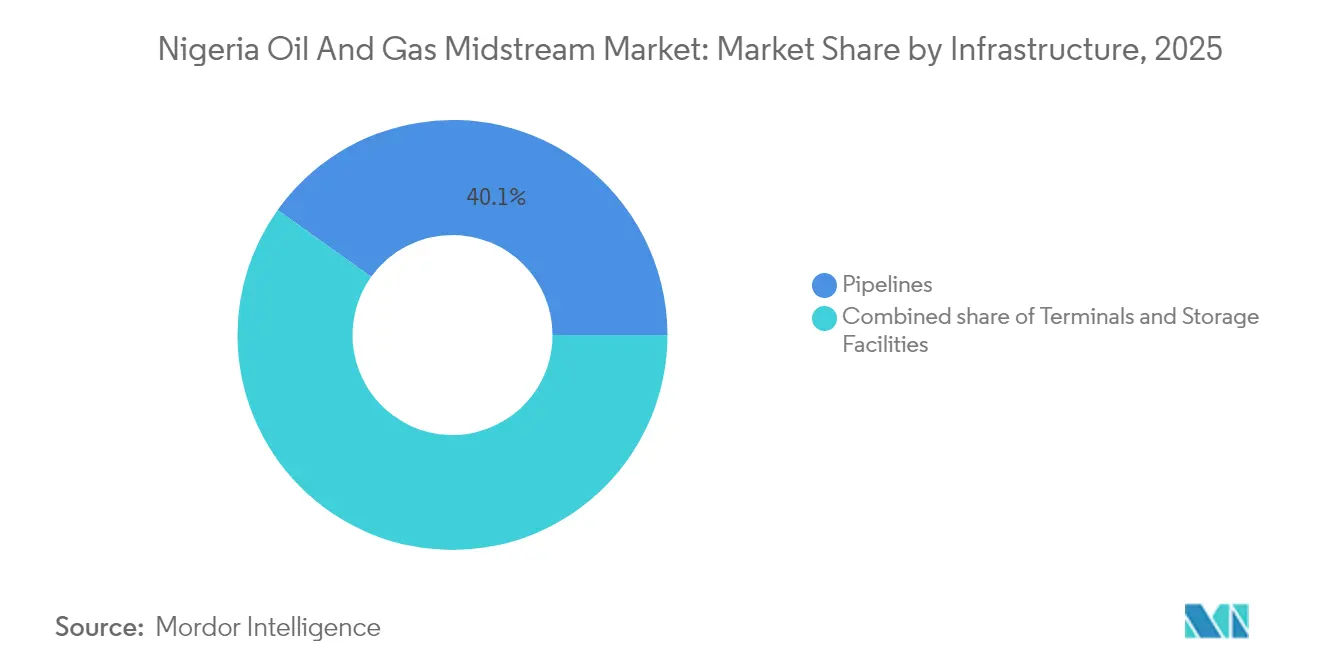

- By infrastructure, pipelines led with 40.12% of Nigeria's oil and gas midstream market share in 2025; storage facilities are projected to grow the fastest at a 5.34% CAGR through 2031.

- By product type, crude oil commanded a 44.72% share of the Nigeria oil and gas midstream market size in 2025, while LNG is expected to expand at a robust 7.18% CAGR to 2031.

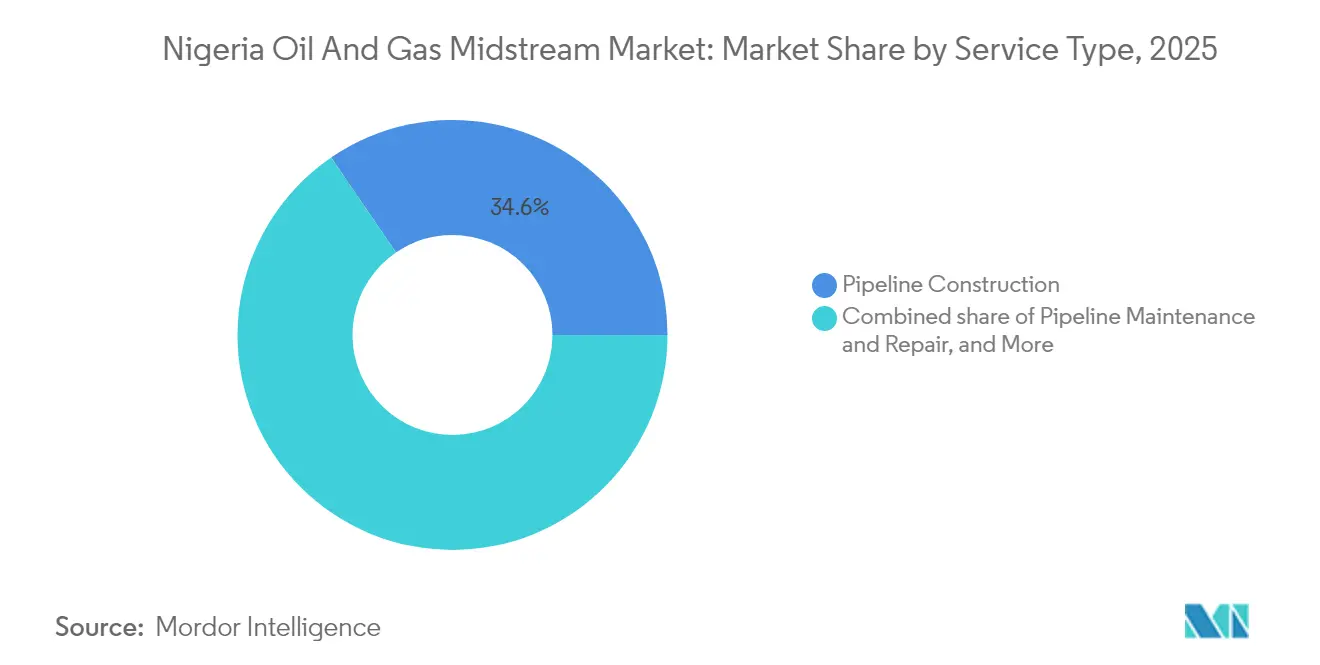

- By service type, pipeline construction accounted for 34.55% of the Nigerian oil and gas midstream market size in 2025, whereas pipeline maintenance and repair is poised for the highest growth at a 5.66% CAGR to 2031.

- Shell, TotalEnergies, Chevron, and Nigerian National Petroleum Company together controlled slightly above 54.25% of total midstream asset throughput in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Oil And Gas Midstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory clarity under PIA (2021) | +1.20% | National; early gains in Lagos, Rivers, Bayelsa | Medium term (2-4 years) |

| NLNG Train 7 and emerging FLNG projects | +0.80% | Niger Delta; coastal spillovers | Long term (≥ 4 years) |

| Dangote refinery-linked product pipelines | +0.60% | Southwest to northern corridors | Short term (≤ 2 years) |

| Domestic gas commercialization programs | +0.50% | Lagos, Kano, Kaduna clusters | Medium term (2-4 years) |

| BOT replacement of 5,000 km legacy pipelines | +0.40% | National high-traffic corridors | Long term (≥ 4 years) |

| Surge in coastal LPG storage terminals | +0.30% | Lagos to Akwa Ibom coastline | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Clarity Under the PIA (2021)

The PIA establishes the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) as a single rule-making body, ending decades of overlapping mandates that slowed project approvals. Transparent tariff-setting and guaranteed open-access provisions have slashed licensing timelines by 40% compared with pre-PIA procedures.(1)Nigerian Midstream and Downstream Petroleum Regulatory Authority, “PIA Implementation Update,” nmdpra.gov.ng Incentives such as accelerated depreciation and reduced tax rates for gas projects lower entry barriers for domestic investors and international lenders. Early adopters include private-equity-backed pipeline operators that secured build-operate-transfer concessions on high-traffic corridors. Execution challenges persist, however, because state-level agencies interpret the Act unevenly, creating compliance gaps that delay right-of-way acquisitions. NMDPRA’s capacity-building program for subnational regulators aims to harmonize enforcement and sustain investor confidence over the medium term.

NLNG Train 7 & Emerging FLNG Projects Boost Gas Export Capacity

Nigeria LNG Limited’s USD 10 billion Train 7 expansion increases export capacity by 8 million tonnes per annum (tpa) and introduces modular construction, which shortens onshore exposure to security risks.(2)Nigeria LNG Limited, “Train 7 Factsheet,” nigeria-lng.comComplementary initiatives such as UTM Offshore’s 2.8 million tpa floating LNG (FLNG) unit, backed by USD 2.1 billion in Afreximbank financing, highlight the industry’s tilt toward offshore processing that circumvents vandal-prone pipelines. Together, these projects align Nigeria with Asian spot-price dynamics, which averaged USD 12 per MMBtu in 2024, four times the domestic gas pricing. Extending the offtake windows into 2050 underpins lender confidence, while sovereign guarantees ease currency exposure for imported liquefaction modules. Successful delivery could raise gas exports by 30%, cushioning federal revenues against crude-price volatility.

Dangote Refinery-Linked Product Pipelines Cut Import Bottlenecks

The Dangote refinery rewires national supply chains by channeling diesel, gasoline, and jet fuel from the Lekki Free Trade Zone to northern depots via new product pipelines. Internal estimates indicate a 35% transportation cost savings compared to coastal imports delivered by road.(3)Dangote Group, “Refinery Project Overview,” dangote.com Reverse-flow engineering allows the network to move products southward when the plant undergoes maintenance, enhancing resilience. Although product pricing negotiations constrained the initial start-up, NMDPRA’s approval of a market-linked pricing template in mid-2025 unlocked higher run rates. Community engagement programs, including health centers and road rehabilitation, strengthen social license in host localities, mitigating the protest risk that historically plagued Niger Delta assets.

Domestic Gas Commercialization (NGFCP, Network Code Roll-out)

The Nigeria Gas Flare Commercialization Programme (NGFCP) awards 42 flare sites to private developers that must install gas gathering and processing infrastructure by 2027. By mandating third-party access through the Gas Transportation Network Code, the government dissolves vertically integrated grids that previously excluded independent power producers. Industrial gas demand is expected to rise to 4 bcf/d by 2030, driven by captive plants in the Lagos, Ogun, and Kaduna manufacturing hubs. Pricing remains the pivotal variable: producers seek USD 3-4 per MMBtu to meet bankability thresholds, while the power sector pushes for tariffs below USD 3 to contain electricity costs. Consensus mechanisms, including indexed tariffs tied to Henry Hub averages, are now under stakeholder review.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Endemic pipeline vandalism & oil theft | -1.80% | Rivers, Bayelsa, Delta | Short term (≤ 2 years) |

| Ageing infrastructure & maintenance backlog | -0.90% | National onshore systems | Medium term (2-4 years) |

| FX volatility inflates CAPEX & OPEX | -0.70% | All regions using imported inputs | Short term (≤ 2 years) |

| Political flashpoints disrupt assets | -0.40% | Rivers State & environs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Endemic Pipeline Vandalism & Oil Theft

Sophisticated criminal syndicates tap trunk lines, diverting up to 200,000 bpd of crude in 2024 and costing operators an estimated USD 2 billion in lost revenue. New techniques include welded bypasses buried several meters underground, complicating detection. The federal government responded by awarding a USD 130 million surveillance contract to a private security consortium that deploys drones, fiber-optic sensors, and community informants. Early evidence suggests a 20% reduction in theft incidents on monitored segments; however, the 5,000 km network still exceeds oversight capacity. Longer-term solutions—such as converting onshore pipelines to gas-powered underground lines that deter siphoning—remain capital-intensive.

Ageing Infrastructure & High Maintenance Backlog

More than half of Nigeria’s crude lines were installed before 1995, and corrosion now accounts for 60% of unplanned outages. NNPC pegs refurbishment requirements at USD 3.2 billion, competing with new-build budgets. Deferred maintenance exacerbates spill risks, which can lead to regulatory fines and community litigation. Operators are pivoting toward predictive maintenance by utilizing fiber-optic acoustic systems that pinpoint leak sounds in real-time. However, foreign-exchange shortages delay spare-part imports and raise local inflation on steel, valves, and coatings. To close the gap, NMDPRA encourages joint asset-management pools that allow smaller firms to share inventory and repair crews, thereby shortening downtime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Pipelines Retain Lead as Storage Accelerates

Pipelines carried 40.12% of the 2025 throughput, cementing their role at the core of Nigeria's oil and gas midstream market. The Warri-Kaduna system illustrates the operational complexity of handling multiple refined products across 600 km of restive terrain. Simultaneously, storage facilities expand at a 5.34% CAGR, buoyed by new coastal LPG terminals that cater to West African demand spikes. NMDPRA's 2024 technical code now mandates the installation of real-time overfill protection and vapor-recovery units, prompting legacy depots to upgrade. Underground caverns are gaining favor in the Niger Delta, where above-ground tanks are vulnerable to sabotage. Private investors secure 20-year concessions that bundle storage, jetty, and truck-loading racks, diversifying revenue streams.

The Nigeria oil and gas midstream market size for storage is expected to reach USD 0.23 billion by 2031, with coastal states contributing 70% of capacity additions. BOT financing reduces upfront state spending but requires transparent tariff indexing to U.S. Consumer Price Index benchmarks to offset naira depreciation. Synergies with nearby petrochemical parks shorten value chains and enhance offtake certainty. Nevertheless, slow customs clearance of cryogenic tanks prolongs construction schedules.

By Product Type: Crude Still Dominant, LNG Fastest Rising

Crude oil held a 44.72% share of the Nigerian oil and gas midstream market size in 2025, as legacy export pipelines, such as Trans-Niger and Nembe Creek, shifted volumes to offshore terminals. Yet LNG is advancing at a 7.18% CAGR, lifted by Train 7 and early-stage FLNG units that bypass vandal-prone onshore corridors. Natural gas infrastructure lags, causing 300 MMscf/d of shut-in associated gas in 2024. Dangote-driven refined-product output shifts the balance by reducing gasoline imports that once consumed USD 10 billion annually.

Emerging sulfur-removal and CO2-extraction technologies, installed at TotalEnergies’ Obite plant, enable higher-spec gas exports into European hubs starting in 2026.Downstream, low-pressure LPG lines supply micro-distribution centers that fill 6-kg cylinders for household cooking, supporting clean-energy goals. However, pipeline tariffs remain indexed to Brent prices, creating volatility for domestic users when crude markets spike.

By Service Type: Construction Leads, Maintenance Gains Momentum

Pipeline construction absorbed 34.55% of 2025 service revenues as BOT contractors replaced 5,000 km of obsolete lines. The Nigeria oil and gas midstream market share for maintenance is set to climb on a 5.66% CAGR, reflecting an overdue shift from capacity expansion to asset preservation. Advanced inline inspection tools now scan 300 km per deployment, cutting outage windows by 40%. Storage and handling services benefit from LPG terminal expansion and strategic petroleum reserve plans that require 90 days of coverage.

Transportation and logistics players deploy GPS-linked truck fleets and barge operations that integrate with new pipelines emanating from Lekki. Security-enhanced routing software reduces hijack incidents by 15% year-over-year on the Benin–Lokoja corridor. Nonetheless, the naira devaluation inflates diesel costs, which account for 25% of trucking expenses, eroding margins unless operators hedge their fuel purchases.

Geography Analysis

The Niger Delta remains the operational heartland, contributing over 75% of midstream throughput in 2025. Rivers State hosts the Port Harcourt refinery complex and serves as a major pipeline hub, transporting crude and products nationwide. However, recurrent community protests and political flashpoints require 24/7 surveillance and rapid-response maintenance teams. Lagos, Ogun, and Ondo anchor coastal infrastructure, including NLNG on Bonny Island and the Dangote refinery in Lekki. Coastal deepwater ports provide easier access to international shipping lanes, fostering export-oriented projects that mitigate onshore security challenges.

Northern states such as Kano and Kaduna underpin demand expansion as industrial estates seek steady gas supplies for captive power. The Ajaokuta–Kaduna–Kano line, designed to transport 2.2 billion cubic feet per day (bcf/d), will be the largest greenfield gas pipeline once completed in 2027, although insurgent threats in the Middle Belt are hampering construction progress. Central transit corridors spanning Benue and Nasarawa require joint military escorts for pipe-string convoys, adding 8% to logistics costs.

Geographic diversification accelerates through offshore processing, where FLNG units eliminate the need for long onshore gas lines. Meanwhile, Kaduna and Kano can receive product via rehabilitated narrow-gauge rail adapted with pressurized tank cars. Harmonized regulations across Nigeria's six geopolitical zones remain critical, as uneven enforcement undermines tariff predictability and revenue assurance. Collectively, these location-specific dynamics shaped the risk-reward calculus that guides capital allocation in Nigeria's oil and gas midstream market.

Competitive Landscape

The Nigeria oil and gas midstream industry is moderately concentrated, with the top five operators handling 55–60% of transported volumes in 2024. International majors maintain strategic stakes but continue to divest onshore assets; Shell sold its subsidiary SPDC to the Renaissance Consortium for USD 2.4 billion in early 2025. Deepwater assets appeal to TotalEnergies and Chevron, which doubled down on offshore gas hubs that face fewer sabotage incidents. Local independents, such as Seplat Energy and Oando, scale up by leveraging PIA incentives and 70% local content requirements enforced by the Nigerian Content Development and Monitoring Board.

Strategic partnerships dominate: UTM Offshore teams with SBM Offshore for FLNG hull fabrication, while NNPC partners with Dangote for pipeline interconnections that optimize refinery evacuation. Technology adoption focuses on fiber-optic sensing, satellite imagery, and AI-driven leak detection to boost uptime. Funding structures are evolving toward blended finance, which combines multilateral loans, export-credit guarantees, and naira-denominated bond issues that hedge currency risk.

Regulatory transparency, combined with rising domestic demand, entices service providers in welding, corrosion control, and EPC management. Still, entry barriers persist due to security premiums, insurance surcharges, and complex community-relations frameworks. The market concentration score stands at 6, reflecting a scenario where the top five firms control just over 55% of throughput, leaving meaningful room for niche players but requiring scale to absorb security and compliance costs.

Nigeria Oil And Gas Midstream Industry Leaders

Duport Midstream Company Limited (DMCL)

Nigerian National Petroleum Corporation

Chevron Nigeria Limited

Eni SPA

Shell PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nigerian National Petroleum Company announces enhanced security measures for critical pipeline infrastructure following recent disruptions to crude oil transportation systems.

- February 2025: UTM Offshore secures USD 2.1 billion financing from African Export-Import Bank for its 2.8 million tonnes per annum floating LNG project, targeting first production in Q1 2029.

- January 2025: TotalEnergies announces USD 550 million investment in gas processing facilities expansion in partnership with Nigerian National Petroleum Company Limited, targeting domestic market supply and export capacity enhancement.

- December 2024: TotalEnergies announces USD 550 million investment in gas processing facilities expansion in partnership with Nigerian National Petroleum Company Limited, targeting domestic market supply and export capacity enhancement.

- November 2024: The Nigerian Midstream and Downstream Petroleum Regulatory Authority has approved new technical standards for LPG storage terminals, mandating enhanced safety protocols and the implementation of environmental monitoring systems.

Nigeria Oil And Gas Midstream Market Report Scope

The midstream sector covers the transportation, storage, and trading of crude oil, natural gas, and refined products. In its unrefined state, crude oil is transported by two primary modes: tankers, which travel interregional water routes, and pipelines, through which most of the oil moves for at least part of the route.

The Nigerian oil and gas midstream market is segmented by type. By type, the market is segmented into transportation, storage, and LNG terminals. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

By Infrastructure

| Pipelines |

| Terminals |

| Storage Facilities (Underground and Above-ground) |

By Product Type

| Crude Oil |

| Natural Gas |

| Refined Products |

| LNG |

By Service Type

| Pipeline Construction |

| Pipeline Maintenance and Repair |

| Storage and Handling Services |

| Transportation and Logistics |

| By Infrastructure | Pipelines |

| Terminals | |

| Storage Facilities (Underground and Above-ground) | |

| By Product Type | Crude Oil |

| Natural Gas | |

| Refined Products | |

| LNG | |

| By Service Type | Pipeline Construction |

| Pipeline Maintenance and Repair | |

| Storage and Handling Services | |

| Transportation and Logistics |

Key Questions Answered in the Report

What is the current value of the Nigeria oil and gas midstream market?

The Nigeria oil and gas midstream market size stands at USD 0.95 billion in 2026.

How fast is the sector expected to grow?

It is projected to reach USD 1.16 billion by 2031, reflecting a 4.18% CAGR.

Which infrastructure segment is expanding the quickest?

Coastal storage facilities lead growth at a 5.34% CAGR through 2031.

Why is LNG gaining momentum?

NLNG Train 7 and planned FLNG units boost liquefaction capacity, driving a 7.18% CAGR for the LNG segment.

How does the PIA improve investment conditions?

The PIA centralizes regulation under NMDPRA, shortens license approval times by 40%, and offers tax incentives for gas projects.

What remains the biggest operational challenge?

Pipeline vandalism still causes yearly losses of around USD 2 billion despite upgraded surveillance efforts.

Page last updated on: