Nigeria Air Freight Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.18 Billion |

| Market Size (2026) | USD 8.7 Billion |

| Market Size (2031) | USD 11.82 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

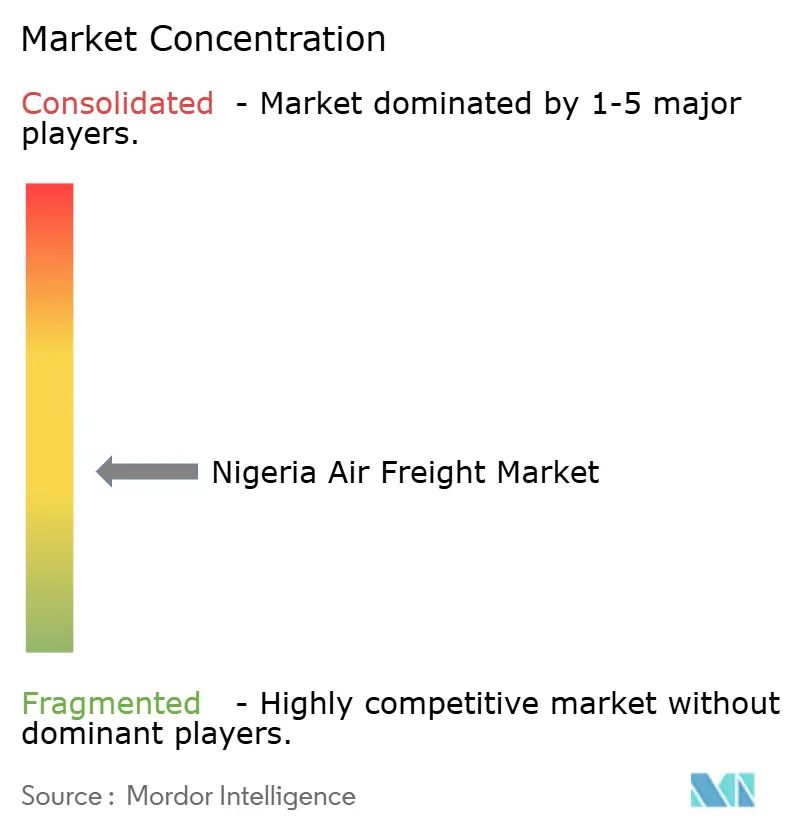

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Air Freight Market Analysis by Mordor Intelligence

The Nigeria Air Freight Market size was valued at USD 8.18 billion in 2025 and estimated to grow from USD 8.7 billion in 2026 to reach USD 11.82 billion by 2031, at a CAGR of 6.32% during the forecast period (2026-2031).

Growth is anchored by the country’s position as West Africa’s main economic hub, which pulls high-value, time-critical shipments toward air transit even as basic infrastructure struggles to keep pace. International routes still move the bulk of volume, yet domestic lanes—energised by fast-growing e-commerce networks and new cargo-friendly airports—are increasing more quickly and gradually reducing Nigeria’s dependency on cross-border flows. Ongoing customs digitisation is cutting clearance times and lowering transaction costs, encouraging exporters of perishables and pharmaceuticals to make greater use of air lift. Airlines are adding dedicated freighters and refining cold-chain services to match rising demand from healthcare shippers, while competitive fare cuts triggered by new entrants underscore how pricing pressure can swiftly reshape capacity decisions. Persistent jet-fuel price swings and currency volatility remain real headwinds, but operators are adapting through fleet upgrades and closer supplier partnerships, keeping overall growth on track.

Key Report Takeaways

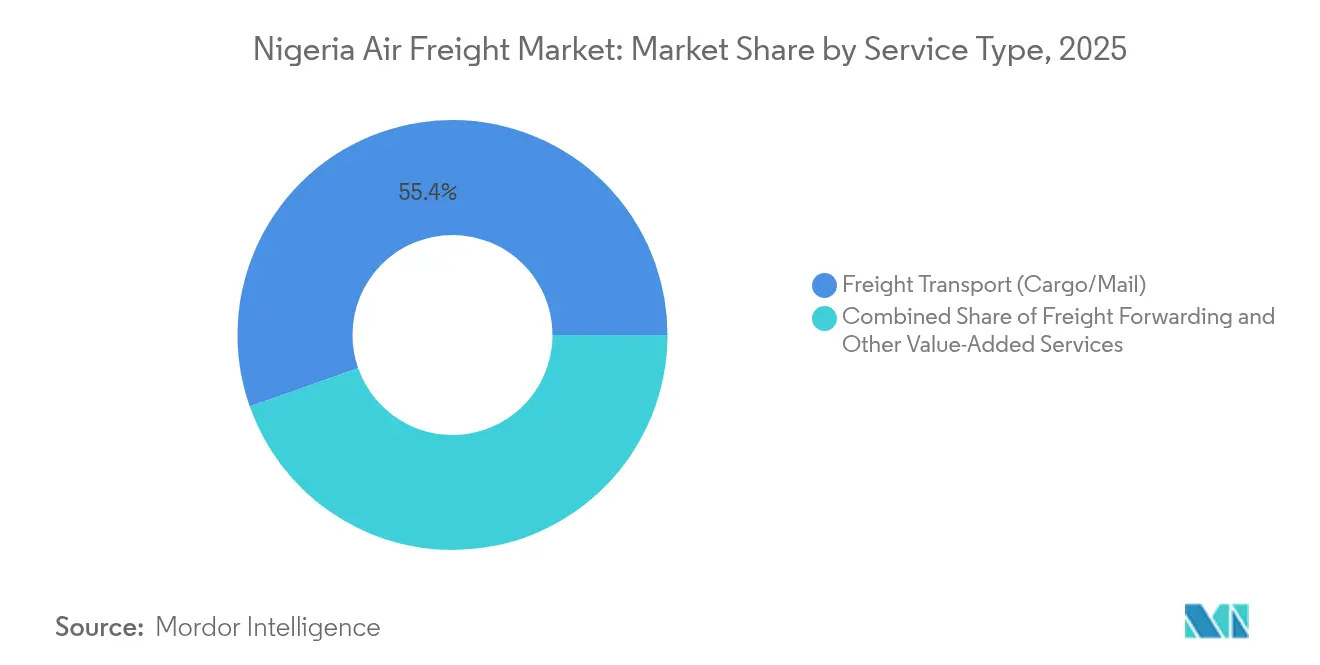

- By service type, freight transport commanded 55.40 % market share in 2025, while value-added services are set to grow the fastest at a 10.92 % CAGR through 2031.

- By destination, international routes held 80.20 % of market size in 2025; domestic air freight is forecast to expand at a 9.35 % CAGR to 2031.

- By carrier type, belly cargo accounted for 53.60 % of traffic in 2025, whereas dedicated freighters are expected to post the highest CAGR of 9.85 % during the forecast period.

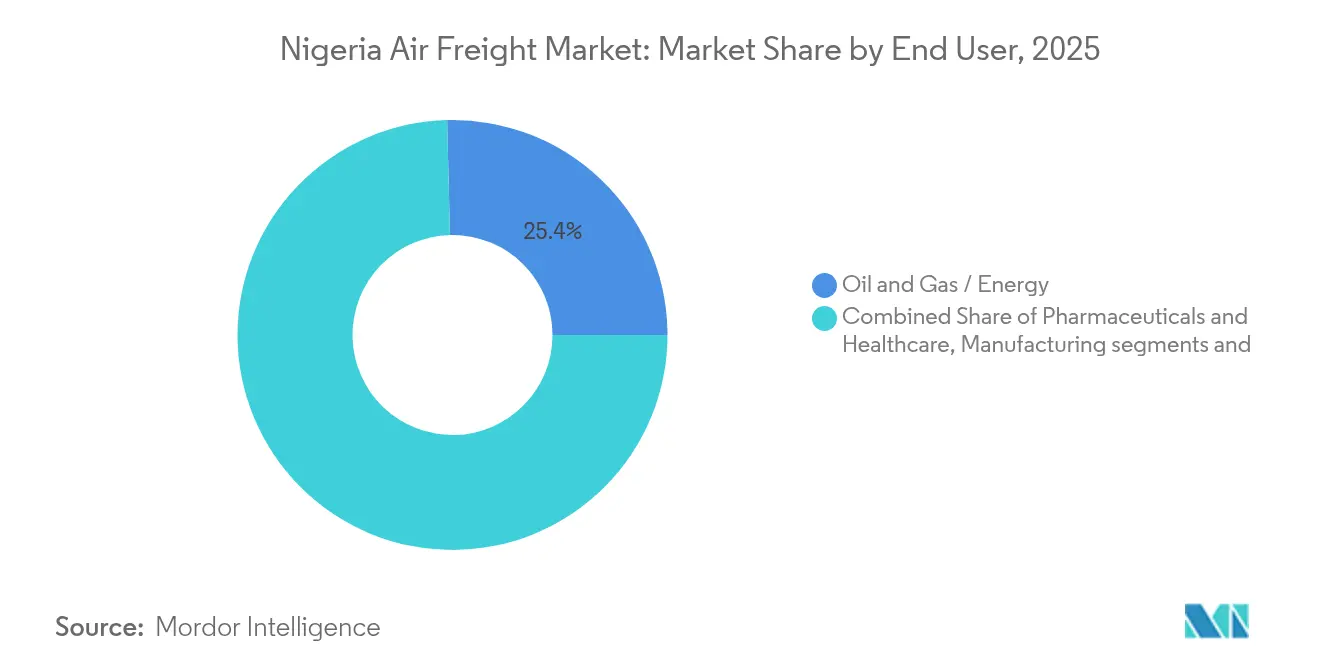

- By end-user industry, oil & gas dominated with a 25.40 % share in 2025, while pharmaceuticals and healthcare lead growth prospects at an 10.83 % CAGR to 2031.

- By cargo type, general cargo represented 72.20 % of the market size in 2025; special cargo is projected to rise fastest with a 10.42 % CAGR through 2031.

- By geography, the South West region captured 46.80 % of market share in 2025, and North Central is positioned for the strongest regional growth at a 11.40 % CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Air Freight Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing E-commerce Penetration Boosting B2C Air Cargo Volumes | +1.8% | National (Lagos-Abuja axis) | Medium term |

| Oil and Gas Project Time-Critical Logistics Demand | +1.5% | Delta region, Lagos | Short term |

| Pharma Cold-Chain Expansion Around Lagos-Abuja Corridor | +1.2% | Lagos-Abuja corridor | Medium term |

| Perishable Agri-Export Programs (Shea Butter, Flowers, Sea-Food) | +0.90% | Agricultural belts to Lagos | Medium term |

| Nigeria Customs Process Digitization (Trade Single Window) | +1.40% | National | Short term |

| Regional Hub-Spoke Connectivity via Ethiopian & Emirates Interline Agreements | +1.00% | Lagos outward | Medium term |

| Source: Mordor Intelligence | |||

Growing E-commerce Penetration Boosting B2C Air Cargo Volumes

Rapid adoption of online retail is driving a noticeable uptick in smaller, higher-frequency consignments that move best by air. Express operators say daily tonnage has begun to outstrip pre-pandemic highs, even though overall capacity additions remain modest. Because shoppers expect two-day delivery nationwide, merchants now embed air freight costs into product pricing as a standard rather than a premium service. This behavioural change is reshaping airline belly-hold planning, with carriers allocating more square metres to loose parcels instead of palletised freight.

Oil and Gas Project Time-Critical Logistics Demand

Large energy investments such as the multi-billion-dollar Ogidigben Gas Revolution Industrial Park and the recently commissioned Dangote refinery require precision equipment that cannot risk maritime delays. Charter brokers consequently report higher utilisation of nose-loader freighters capable of lifting out-of-gauge pieces into Niger Delta airstrips. By fulfilling maintenance-critical deliveries within hours, air freight is directly supporting project timelines, and in turn, the sector’s capital inflow reinforces Nigeria Air Freight industry revenue. The pattern underlines how a single mega-project can ripple across forwarding, ground handling, and regional airport development.

Pharma Cold-Chain Expansion Around the Lagos-Abuja Corridor

Investments in temperature-controlled warehouses at Lagos and Abuja airports have expanded available cold storage by thousands of pallet positions. Airlines are responding with dedicated cool-dolly fleets and real-time monitoring to meet stringent pharmaceutical handling protocols. As vaccines and biotechnological products move through these corridors, failure-rate data show a steady decline, encouraging even conservative shippers to choose air instead of costly refrigerated trucking. This virtuous cycle is positioning Nigeria as an emerging West-African distribution hub for temperature-sensitive medicine.

Perishable Agri-Export Programs (Shea Butter, Flowers, Sea Food)

Government-backed export corridors now link northern crop clusters directly with Lagos cargo terminals, reducing dwell times for produce such as shea butter and cut flowers. Exporters have started negotiating seasonal block-space agreements with carriers, a practice that was rare five years ago. Indications are that air-lifted perishables are achieving higher price realisations abroad than equivalent sea shipments, encouraging farmers to plant varieties suited for the air channel. This development also diversifies the Nigeria Air Freight market away from its historic dependence on inbound consumer goods.

Restraints Impact Analysis*

| Restraint | (~)% Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Jet-A1 Supply Disruptions Driving Cost Volatility | –1.2 % | National | Short term |

| Airport Cargo Infrastructure Congestion (Lagos MMIA) | –1.1 % | Lagos MMIA | Medium term |

| High Security Surcharges Due to Cargo Pilferage Risk | –0.8 % | National | Short term |

| Naira FX Liquidity Constraints Impacting Freight Payments | –1.3 % | National | Short term |

| Source: Mordor Intelligence | |||

Chronic Jet-A1 Supply Disruptions Driving Cost Volatility

Frequent spikes in aviation fuel prices force carriers to adopt dynamic surcharges that complicate budgeting for shippers. Although some airlines hedge, most Nigerian operators rely on spot purchases, making them vulnerable to exchange-rate swings. These pressures accelerate the search for fuel-efficient aircraft such as B737-800BCF conversions, which promise lower burn per tonne-kilometre. A trend toward strategically staging uplift in neighbouring states with steadier supply is also emerging, indirectly stimulating regional cooperation.

Airport Cargo Infrastructure Congestion (Lagos MMIA)

Lagos Murtala Muhammed International Airport is nearing its physical limits, with ramp congestion at peak hours causing delays and additional ground handling fees. Cargo handlers have begun implementing appointment-based truck docks to smooth gate arrivals, mimicking best practices at larger global hubs. As a result, airlines capable of operating off-peak schedules gain a competitive edge because they avoid ground queues. The congestion challenge is prompting renewed calls for a dedicated cargo airport or at least significant apron expansion to safeguard future Nigeria Air Freight market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Service Type: Value-Added Services Outpace Core Transport

Value-Added Services are forecast to expand their Nigeria Air Freight market share rapidly, with the segment’s market size expected to post a 10.92 % CAGR between 2026 and 2031. Customs brokerage, insurance, and specialised packaging now often bundle with transport in one invoice, and shippers increasingly regard these extras as indispensable rather than optional. Digital customer portals introduced by forwarders allow real-time milestone visibility, which strengthens loyalty and drives repeat business. A visible outcome is that freight operators now recruit compliance specialists almost as aggressively as they hire load-planners.

Freight Transport (Cargo and Mail), which holds 55.40 % of current revenue, remains indispensable because it underpins all other offerings. Yet its relative share is slowly eroding as logistics providers monetise ancillary activities with higher margins. Carriers that once sold only space are pivoting toward door-to-door solutions, capturing greater wallet share per shipment. This transition illustrates how the Nigeria Air Freight industry is moving up the value chain in response to client expectations.

Destination: Domestic Routes Gain Momentum

International services currently represent 80.20 % of Nigeria Air Freight market size, sustained by outbound crude-oil-linked spare parts and inbound consumer electronics. The segment benefits from extensive intercontinental belly capacity on routes to Europe and the Middle East, keeping unit rates comparatively competitive. Nevertheless, its CAGR is projected below the domestic segment because lanes are close to maturity on frequency and gauge. Continuous diversification into non-oil exports is expected to prevent stagnation, but growth will likely track global GDP more than local structural shifts.

Domestic air freight is forecast to grow at a 9.35 % CAGR through 2031, outpacing all other destination categories. E-commerce fulfilment and pharmaceutical resupply along the Lagos-Abuja spine are prime contributors. New cargo-friendly terminals in Maiduguri and Kano shorten distances to underserved northern markets, making next-day delivery economically viable. As shippers gain confidence in schedule reliability, modal substitution from road to air should continue, particularly during the rainy season.

Carrier Type: Freighters Gaining Market Share

Dedicated freighters are projected to lift their Nigeria Air Freight market share to parity with belly cargo by the end of the decade, supported by an 9.85 % CAGR. Growth is propelled by specialised needs such as temperature-controlled pharmaceuticals and outsized industrial parts that cannot fit in passenger holds. Nigerian operators adding converted narrow-body freighters gain flexibility to serve secondary airports with limited ground equipment. This fleet evolution also opens overnight express opportunities that belly-hold schedules cannot match.

Belly cargo retains advantages on high-density intercontinental routes, currently commanding a 53.60 % share of tonnage. Its competitiveness stems from marginal cost economics, where freight rates chiefly cover handling rather than airframe operation. The main risk is that any unforeseen passenger demand slump could remove lift, pushing shippers toward dedicated freighter contracts. Consequently, belly-heavy airlines are incentivised to maintain balanced passenger strategy to secure freight loyalty.

End-User Industry: Pharmaceuticals Lead Growth Trajectory

Oil and gas maintains the largest single Nigeria Air Freight market share at 25.40 %, yet its growth trajectory is modest compared with emerging verticals. The sector’s heavy-lift and urgent-part requirements generate consistent charter work, and value-added forwarders now deliver cradle-to-site solutions within the Niger Delta. Still, gradual energy transition policies worldwide signal that diversification will be prudent for carriers. As local refineries reach steady state, maintenance rather than construction will dominate future movements, slightly dampening volume escalation.

Pharmaceuticals and healthcare are forecast to register a 10.83 % CAGR between 2026 and 2031, the fastest in the market. Expansion of accredited cold rooms and real-time temperature mapping has reassured global manufacturers that Nigeria can meet Good Distribution Practice standards. As a result, vaccine distributors increasingly position regional stock in Lagos for re-export to neighbouring countries, amplifying throughput. This phenomenon showcases how infrastructure maturity can unlock entirely new revenue streams.

Cargo Type: Special Cargo Driving Innovation

General Cargo dominates the Nigeria Air Freight Market with a 72.20% share in 2025, encompassing the broad range of standardized shipments that form the backbone of air freight operations. This predominance reflects the versatility and cost-efficiency of general cargo handling for many commodity types. However, the market is witnessing a significant shift toward Special Cargo, which is projected to grow at a CAGR of 10.42% (2026-2031), nearly double the overall market growth rate of 6.32%.

This accelerated growth in Special Cargo is being driven by increasing demand for specialized handling of temperature-sensitive pharmaceuticals, perishable agricultural exports, and high-value oil and gas equipment. The trend is prompting investments in specialized facilities and equipment, with airlines enhancing their operations to include temperature-controlled environments for pharmaceuticals and other sensitive goods. The air cargo industry's adaptation to post-COVID requirements has further accelerated innovations in special cargo handling, particularly for cold chain logistics. This evolution is creating new competitive dynamics as carriers and handling agents differentiate through specialized capabilities, with collaborative approaches emerging to enhance cold chain infrastructure and improve the efficiency of special cargo operations.

Geography Analysis

The South West region commands 46.80 % market share of the Nigeria Air Freight market in 2025, giving it the largest regional market size and consolidating its long-standing status as the nation’s primary logistics gateway. Lagos’s Murtala Muhammed International Airport (MMIA) alone processes roughly 47,000 metric tons of freight each year, anchoring a dense network of ground handlers and express integrators that few other Nigerian airports can currently match . The presence of large-scale manufacturing zones, Nigeria’s biggest consumer base, and the USD 21 billion Dangote refinery complex keeps south-west outbound lifts steady throughout the year. These structural advantages allow airlines to schedule multiple daily wide-body rotations, which in turn creates attractive frequency for small-parcel e-commerce shipments. An important knock-on effect is that the region’s abundant belly capacity holds line-haul rates in check, indirectly lowering logistics costs for shippers elsewhere in the country who trans-ship through Lagos. Even so, rising congestion at MMIA is prompting some forwarders to pre-book off-peak slots, an operational workaround that underlines the value of dependable time windows for temperature-sensitive cargo.

North Central is forecast to post a 11.40 % CAGR between 2026 and 2031, meaning its market size is expanding almost twice as fast as the national average. Abuja’s steadily growing role as a consolidation hub for domestic distribution explains much of this momentum; the city’s more temperate climate supports cold-chain reliability, making it the logical midpoint on the Lagos–Abuja pharmaceutical corridor. Recent investments in GDP-compliant storage have reduced temperature excursions on biologics shipments, encouraging healthcare producers to base regional inventory in the capital. As volumes rise, forwarders are moving to daily narrow-body freighter services rather than ad-hoc road transfers, a shift that frees capacity at Lagos while improving product shelf life. The region’s growth also benefits from improved road and rail links that shorten trucking legs into the Middle Belt, where agricultural producers can now reach urban markets faster. The inference emerging from these developments is that Abuja’s hub function is transforming from political epicentre to indispensable logistics pivot for time-critical consignments nationwide.

Although North West and North East currently account for modest slices of Nigeria Air Freight market share, infrastructure upgrades point to accelerating expansion. The completion of the Maiduguri runway extension allows international wide-body operations from January 2025, positioning the city as a new entry point for humanitarian aid and seasonal crop exports . In parallel, the reopened Nigeria–Niger border at Jibiya-Maradi has revived land trade worth hundreds of millions of dollars annually, giving air-to-road routings fresh relevance for high-value goods moving into the Sahel . The planned Chinese-funded railway from Kano to Maradi will further stitch together air, rail and road legs, potentially lowering last-mile costs for exporters that fly produce out of Kano’s Mallam Aminu Kano International Airport. As dedicated freighters obtain traffic rights to these revamped gateways, local farmers and spare-parts suppliers gain access to time-definite services once obtainable only through Lagos. The likely outcome is a gradual narrowing of the regional share gap as northern airports capture niche, high-yield cargo streams that thrive on reduced ground transit times.

Competitive Landscape

International mega-carriers continue to dominate headline capacity, but local airlines are reshaping competition through nimble route choices and pricing. Ethiopian Airlines Cargo leverages Addis Ababa’s integrated hub to feed Nigerian traffic into intercontinental freighters, offering shippers reliable transit times that match European benchmarks. Emirates SkyCargo’s commitment to double overall capacity this decade, including new freighters earmarked for African lanes, signals long-run intent to defend share. These moves compel Nigerian operators to specialise in segments where local knowledge adds tangible value, such as inland trucking integration and regulatory navigation.

Domestic challenger Air Peace has proven that aggressive fare strategies on passenger services can shift cargo dynamics by injecting fresh belly capacity and stimulating rate competition. Its London launch quickly led to fare reductions by foreign rivals, demonstrating price elasticity in both passenger and freight markets. Although such tactics squeeze margins, they also raise utilisation, which can offset lower yields if managed carefully. The episode illustrates how a single local entrant can reprice entire corridors, forcing incumbents to reassess allocation of wide-body assets.

Specialisation is the new battleground. Handling agents at Lagos are pursuing Good Distribution Practice certification to court pharmaceutical traffic, while forwarders are investing in online booking portals that quote door-to-door rates in real time. Security accreditation has become another differentiator, with technology such as tamper-evident seals and GPS-tracked trucks extending protection beyond the airport perimeter. As shippers grow more discerning, carriers lacking either niche capability or credible alliances risk relegation to rate-taker status, underscoring the importance of continuous service innovation.

Nigeria Air Freight Industry Leaders

Ethiopian Airlines Cargo

Emirates SkyCargo

Turkish Cargo

DHL Aviation

Allied Air

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Air Peace detailed plans to add three Boeing 777s and open Lagos–New York and Lagos–Houston services before December 2025, positioning the carrier for direct U.S. freight and belly-cargo flows.

- December 2024: Emirates SkyCargo confirmed a USD 1 billion capacity-doubling program that will grow its fleet past 300 aircraft and add more than 20 destinations, a move that will lift lift options on Nigeria corridors.

- June 2024: Ethiopian Airlines Cargo partnered with MailAmericas to strengthen cross-border e-commerce flows through Addis Ababa, improving parcel connectivity into and out of Nigeria.

- January 2024: Air Peace added Lagos–Cotonou and Lagos–Abidjan, lifting its West-African network to 10 cities and widening intra-regional cargo options.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Nigeria air freight market as the total gross revenue earned inside the country from moving commercial cargo by fixed-wing or rotor-wing aircraft across domestic and international lanes, whether handled directly by airlines or through freight-forwarding and integrator services, and expressed in constant 2024 US dollars.

Scope Exclusions: Passenger charter belly-hold baggage, drone parcel flights, and government defense lifts are not sized within this assessment.

Segmentation Overview

- By Service Type

- Freight Transport (Cargo/Mail)

- Freight Forwarding

- Other Value-Added Services (Customs brokerage, insurance, etc.)

- By Destination

- Domestic

- International

- By Carrier Type

- Belly Cargo

- Freighter

- By End-User Industry

- Manufacturing

- Oil & Gas / Energy

- Pharmaceuticals & Healthcare

- Perishables & Food

- Retail & Consumer Goods

- Others

- By Cargo Type

- General Cargo

- Special Cargo

- By Region (Nigeria)

- South West

- South South

- South East

- North Central

- North West

- North East

Detailed Research Methodology and Data Validation

Primary Research

Several conversations with cargo airline station managers, ground-handling chiefs, customs brokers, and large online retailers across Lagos, Abuja, and Port Harcourt allowed our analysts to verify lane yields, seasonal capacity swings, and the realistic pace of customs digitization. Follow-up surveys with regional logistics associations helped close data gaps and stress-test headline growth drivers identified during desk work.

Desk Research

We began with wide desk work, pulling annual tonnage and chargeable weight statistics from the Federal Airports Authority of Nigeria, cargo throughput alerts from the Nigerian Civil Aviation Authority, bilateral trade values on UN Comtrade, and airport infrastructure updates from ICAO and IATA.

Macro markers came from the World Bank Logistics Performance Index, Central Bank of Nigeria exchange data, and e-commerce checkout volumes reported by the Nigeria Inter-Bank Settlement System.

Where company-level context was needed, D&B Hoovers and Dow Jones Factiva helped us validate carrier and forwarding revenue splits.

A variety of peer-reviewed journals and West African freight associations supplied additional context on perishables, oil and gas tools, and express parcels.

This list illustrates key inputs and is not exhaustive.

Market-Sizing & Forecasting

A top-down model starts with FAAN reported tonnes, multiplies by interview-validated average revenue per ton, and is re-expressed in USD after monthly naira conversions.

Selected bottom-up checkpoints, handler throughput roll-ups, and sampled airline financials calibrate the totals.

Key variables include cargo tonnage, blended yield, e-commerce parcel share, jet-fuel index, non-oil export GDP, and real effective exchange rate; each feeds a multivariate regression that projects demand through 2030.

Gaps in sampled forwarding invoices are bridged using historical yield curves and tonnage elasticity observed during COVID recovery.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review where anomalies against external trade data or prior editions trigger re-contact with experts.

Reports refresh annually, while material shocks such as subsidy removal or runway closures prompt interim updates so clients always receive our freshest view.

Why Mordor's Nigeria Air Freight Baseline Earns Trust

Published estimates often diverge because firms pick different service buckets, airport coverage, currencies, and refresh cadences.

Key gap drivers in this market include whether forwarding fees are counted, how Lagos re-routing distortions are smoothed, and if naira conversions use parallel or official windows. Mordor's model covers both freight transport and forwarding revenue, uses dual-window FX averaging, and is updated every twelve months, which explains the wider yet steadier baseline versus others.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.18 billion (2025) | Mordor Intelligence | |

| USD 3.08 billion (2024) | Global Consultancy A | Counts airline carriage only and omits forwarding fees and domestic legs |

| USD 3.01 billion (2025) | Regional Consultancy B | Uses two airports, fixes constant yield, and applies aggressive uniform CAGR |

In short, our disciplined scope selection, dual-source FX treatment, and yearly refresh give decision-makers a balanced, traceable baseline they can rely on when capacity, tariffs, or consumer demand shift without warning.

Key Questions Answered in the Report

What is the current Nigeria Air Freight market size?

The market is valued at roughly USD 8.7 billion in 2026, with steady growth anticipated through 2031.

Which segment is growing fastest in the Nigeria Air Freight industry?

Pharmaceuticals and healthcare show the highest projected CAGR because of expanding cold-chain infrastructure and rising healthcare demand.

Why is domestic air cargo growing faster than international cargo?

E-commerce expansion, improved regional airports, and dedicated corridors for perishables are accelerating internal flows, boosting domestic CAGR above international lanes.

How are fuel price fluctuations affecting air-freight operators in Nigeria?

Jet-A1 volatility raises operating costs and drives frequent surcharge adjustments, pushing airlines to seek more fuel-efficient fleets and alternate refuelling points.

Which airports are emerging as alternatives to Lagos for cargo traffic?

Upgraded facilities in Abuja, Maiduguri, and Kano are attracting pharmaceuticals, humanitarian aid, and regional trade consignments, gradually easing pressure on Lagos.

How is digital customs reform influencing the market?

The National Single Window system reduces paperwork and clearance lead times, making air freight more attractive for importers and exporters who value speed.

Page last updated on: