Next-Generation Customer Loyalty Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

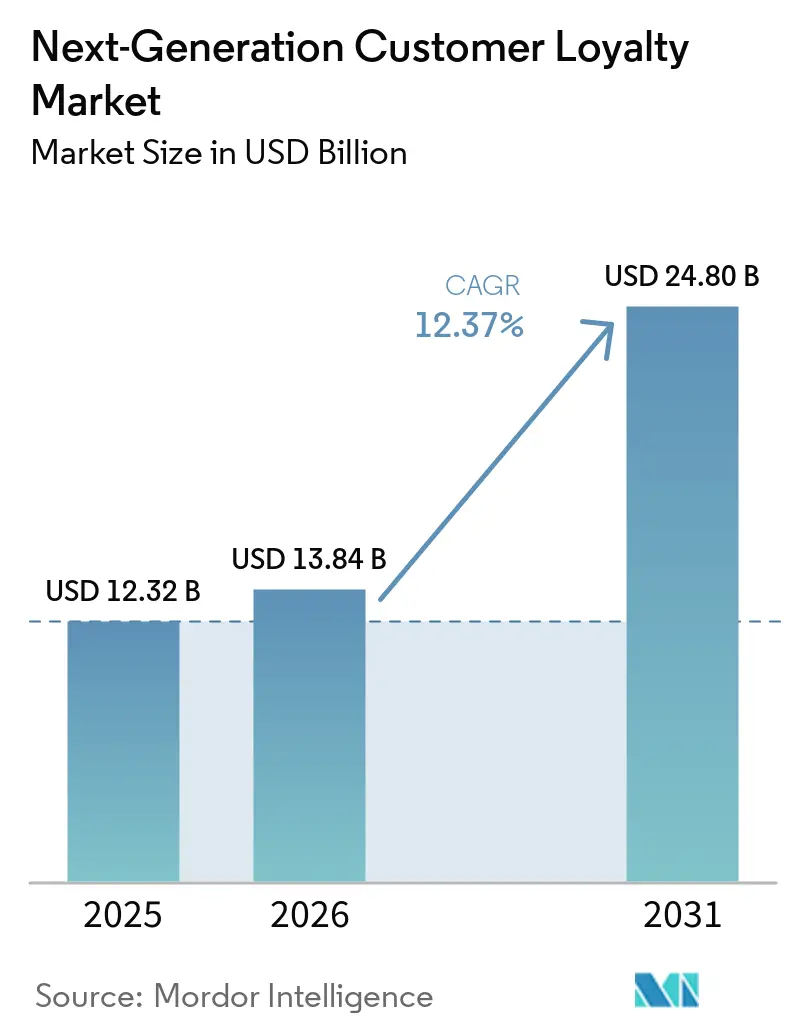

| Market Size (2026) | USD 13.84 Billion |

| Market Size (2031) | USD 24.80 Billion |

| Growth Rate (2026 - 2031) | 12.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next-Generation Customer Loyalty Market Analysis by Mordor Intelligence

The Next-Generation Customer Loyalty Market size is expected to grow from USD 12.32 billion in 2025 to USD 13.84 billion in 2026 and is forecast to reach USD 24.80 billion by 2031 at 12.37% CAGR over 2026-2031.

Real-time customer engagement is shifting from static, transaction-led schemes to AI-driven orchestration that learns and responds to first-party signals across channels, including mobile wallet passes and payment-linked journeys. Platform integrations and coalition structures are extending reach while lowering acquisition costs through shared identity and governed data exchange, as seen in new cross-brand alliances that combine travel, retail, and fuel benefits for everyday relevance. Wallet-native experiences are building app-free engagement through policy-governed notifications and rate-limited APIs, requiring robust design for reliability at scale. Mergers, product launches, and payments-rail adjacencies indicate a market race to unify loyalty, identity, offers, and analytics into composable stacks for omnichannel activation.

Key Report Takeaways

- By engagement channel, mobile applications led with a 43.44% revenue share of the next-generation customer loyalty market in 2025. Social/messaging channels are projected to post the fastest growth at a 16.33% CAGR through 2031.

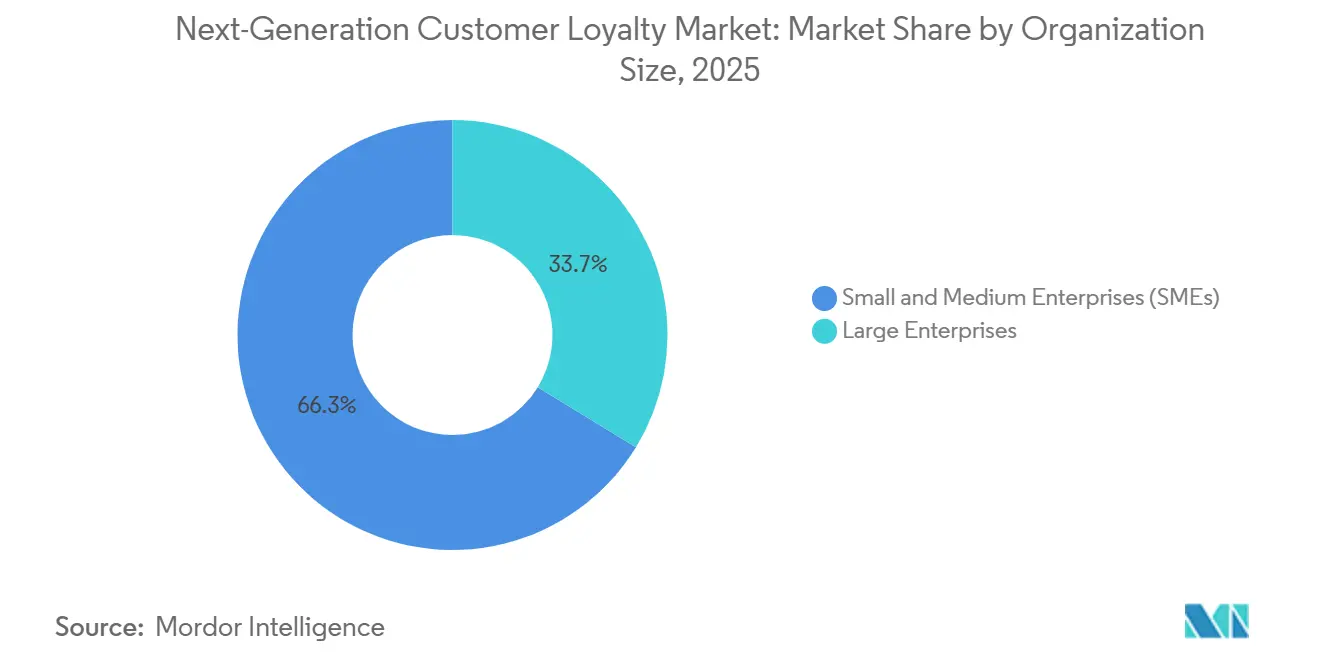

- By organization size, small & medium enterprises held 66.26% share of the next-generation customer loyalty market in 2025 and are projected to expand at a 21.24% CAGR through 2031.

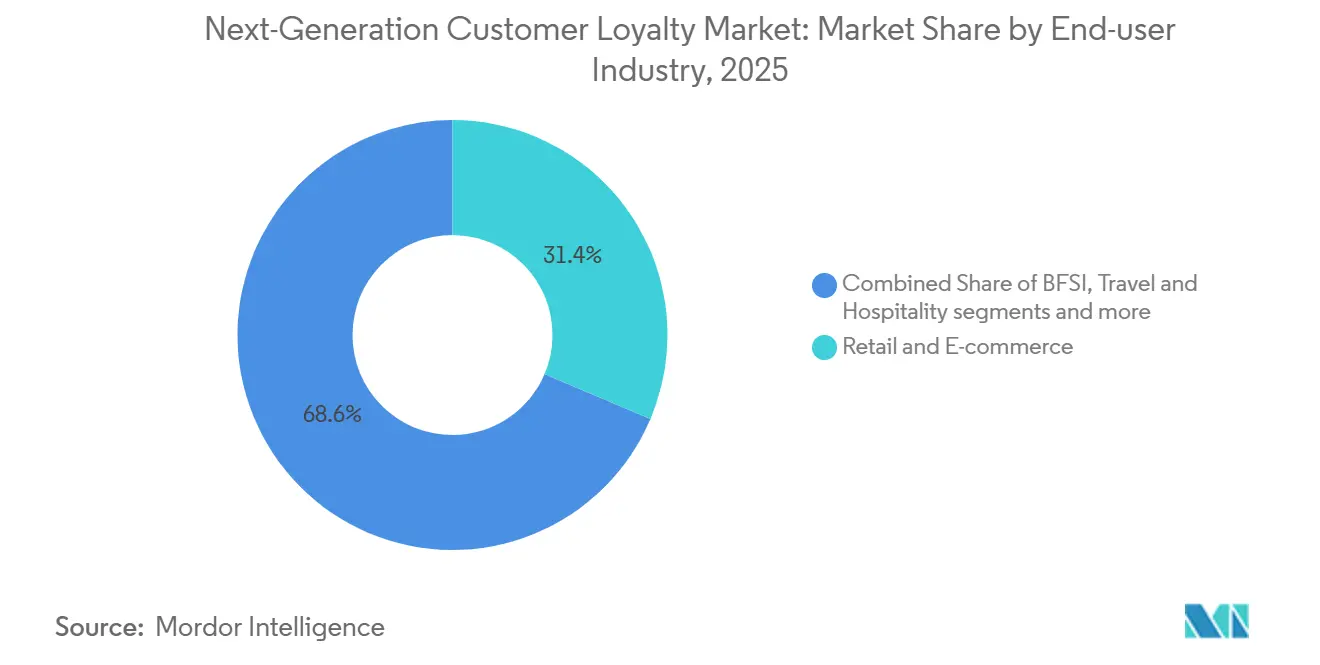

- By end-user industry, retail & e-commerce accounted for 31.38% share of the next-generation customer loyalty market in 2025. BFSI is projected to record the highest growth at a 22.35% CAGR through 2031.

- By geography, North America captured 37.35% share of the next-generation customer loyalty market in 2025. Asia-Pacific is projected to be the fastest-growing region, with a 11.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Next-Generation Customer Loyalty Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cookie-less shift boosts first-party loyalty | +3.2% | Global, with acute effect in North America & the European Union, where third-party cookie deprecation is most advanced | Medium term (2-4 years) |

| Real-time AI offer decisioning adoption | +2.8% | APAC core, spill-over to North America enterprise retail | Short term (≤ 2 years) |

| Wallet passes replacing plastic cards | +1.9% | North America, Europe, rapid uptake in urban APAC metros | Medium term (2-4 years) |

| Coalition partnerships rapidly expand reach | +2.1% | Canada, United Kingdom leadership, emerging in Latin America | Long term (≥ 4 years) |

| Gamified zero-party data capture accelerates | +1.7% | Global, strongest in Gen Z or Millennial dense urban markets | Short term (≤ 2 years) |

| Receipt data enables SKU-level rewards | +1.0% | National programs, early gains in United States, United Kingdom, Benelux | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cookieless Shift Drives First-Party Loyalty Infrastructure

Browser-level tracking restrictions and privacy-led changes are accelerating the pivot to consented, first-party data that loyalty programs are structurally positioned to capture and activate across channels. The next-generation customer loyalty market is shifting from rented audience visibility to owned identity graphs built from transactional histories, declared preferences, and verified engagement signals, under clear consent flows. As brands consolidate customer identity within loyalty-led ecosystems, activation quality improves, enabling precise offer decisioning tied to measurable outcomes rather than inferred browsing intent[1]Adobe, “Introducing Adobe Journey Optimizer Loyalty,” Adobe Business Blog, adobe.com. The same shift is elevating loyalty from a promotional lever to core data infrastructure, integrating profile, event, and journey data with real-time omnichannel orchestration. This structural reorientation is central to the next-generation customer loyalty market because it reduces dependency on third-party signals and builds defensibility through consent-based value exchange at scale.

AI-Powered Real-Time Offer Decisioning Scales Personalization

AI-first orchestration is moving loyalty from periodic campaigns to continuous, signal-driven decisions that adapt content, offers, and tiers in real time across channels. Platforms are embedding agentic capabilities that analyze loyalty signals, flag at-risk members, and propose targeted retention tactics that accelerate time to impact while reducing manual effort. Retail operators and multi-location brands are layering decisioning with insights, strategy, and activation tooling so teams can query performance in natural language, assemble offers, and test outcomes quickly. This approach supports the next-generation customer loyalty market by unifying identity, propensity, and budget logic to deliver one-to-one experiences with closed-loop attribution across web, app, and store. As decisioning becomes composable and API-first, brands can scale personalization without monolithic upgrades while maintaining governance across consumer touchpoints.

Digital Wallet Passes Create App-Free, Always-On Engagement

Apple Wallet and Google Pay are enabling app-free loyalty with passes that update in real time and surface on-device notifications, in line with clear platform policies[2]Google, “Google Wallet API, Loyalty Cards FAQ,” Google for Developers, developers.google.com. Program operators can provision enrollment, balances, and offers directly to mobile wallets and tap into NFC, QR, or barcode validation without requiring native app downloads or logins at the point of sale. Rate limits and content guidelines govern performance and branding, so high-volume deployments require an architecture that respects API thresholds and image-rendering rules for reliability and compliance. This engagement layer strengthens the next-generation customer loyalty market by reducing friction, increasing message visibility, and supporting omnichannel redemption with minimal staff training. As wallet-native experiences complement apps, SMS, and email, brands gain multi-channel optionality while insulating programs from shifts in any single platform policy.

Coalition Partnerships Extend Reach and Dilute Acquisition Costs

Unified or bilateral programs that link currencies across airlines, fuel, and retail are expanding earning and redemption options, building daily relevance and creating cross-journey data under governed agreements. Travel and fuel partnerships rolling out in 2026 show how members link accounts to earn more at the pump while converting points into travel value, gaining engagement benefits for both brands[3]WestJet, “WestJet and Petro-Canada Connect the Road to the Runway,” WestJet Media Room, westjet.mediaroom.com. Hospitality networks are adding bank and retail partners so members can use and accumulate points on everyday purchases, which positions loyalty as a lifestyle utility beyond core services. These partnerships support the next-generation customer loyalty market by extending frequency, lowering acquisition costs through shared identity, and enabling merchant-funded rewards with clearer attribution. Coalition execution also benefits from standardized data sharing and clear legal frameworks that protect privacy while permitting insight-driven personalization across participating brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent data privacy compliance burdens | -2.5% | Europe, North America, and emerging in APAC or MEA | Short term (≤ 2 years) |

| Legacy POS and IT fragmentation | -1.8% | Global, acute in mature markets with legacy stacks | Medium term (2-4 years) |

| Loyalty liability accounting pressures intensify | -1.2% | Markets with strict IFRS 15 or ASC 606 enforcement | Long term (≥ 4 years) |

| Wallet platform policy volatility risks | -0.8% | Global, with regional variation in enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Data Privacy Compliance Burdens Constrain Experimentation

Regulatory requirements across jurisdictions are tightening consent standards and limiting data reuse, increasing operational overhead for loyalty teams and requiring robust consent management and auditability at scale. Brands are adapting program design to ensure data minimization and clear disclosures, while engineering linkages between loyalty identities and customer data platforms to ensure consistent rights management across channels. The next generation customer loyalty market responds with privacy-by-design architectures that segregate sensitive attributes and log member choices for transparent reporting and enforcement readiness. Operators that align value exchange with transparent privacy controls see stronger trust and participation, especially when programs make redemption easy and explain how data powers relevant benefits. This environment prioritizes disciplined governance and documentation without sacrificing agility, so teams are emphasizing platform capabilities that unify preference, identity, and consent at the core.

Legacy POS and IT Fragmentation Delays Real-Time Personalization

Many retailers and multi-location brands operate legacy POS and middleware that are not built for event streaming, which complicates real-time balance updates and the execution of offers at checkout. The modernization path emphasizes phased rollouts and API-first loyalty engines that can coexist with current stacks while progressively enabling instant earn, burn, and eligibility checks. The next-generation customer loyalty market, therefore, favors composable architectures that cleanly integrate with payment, CRM, and e-commerce, enabling operators to avoid brittle batch jobs and reduce customer-facing latency. Loyalty teams also reinforce store execution with wallet-native experiences that require minimal cashier intervention and can operate even when app adoption is low. As integration quality improves, brands unlock reliable redemption, stronger satisfaction, and better attribution across online and offline journeys.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organisation Size: SMEs Gain Ground as Cloud Platforms Democratize Access

Large enterprises held a 33.74% share of the next-generation customer loyalty market in 2025, reflecting their ability to fund enterprise-wide platforms, unify identity, and scale AI-led personalization across channels. Banks are broadening eligibility and tiered benefits to drive primacy across checking, credit, lending, and investments, as seen in the launch of BofA Rewards that extends enrollment to any client with an active checking account and introduces benefits calibrated by tier[4]Bank of America, “New BofA Rewards Program to Reach Millions More Clients,” Bank of America Newsroom, newsroom.bankofamerica.com. This institutional model leverages embedded finance, identity protection, and lifestyle offers to deepen engagement through everyday needs that extend beyond single-product incentives. Enterprise operators are also adding channel breadth with wallet passes and agentic decisioning to orchestrate timely, personalized incentives at scale. As these capabilities converge, the next-generation customer loyalty market is reinforcing loyalty as part of financial planning, cross-sell strategy, and operating model discipline rather than treating it as a pure marketing expense.

SMEs, supported by cloud-native platforms and modular pricing, are expanding rapidly as barriers to real-time loyalty experience design continue to fall. The next-generation customer loyalty industry is delivering SME-ready integrations that connect storefronts, point of sale, and messaging into cohesive workflows, shortening time to value for smaller teams with limited engineering capacity. Wallet-native capabilities let SMEs deliver enrollment, balances, and offers without a full app build, while agentic tools reduce manual campaign work through on-platform guidance. As these SMEs scale, they are also adopting receipt-upload features to bridge online and in-store proof of purchase, enabling SKU-level validation without complex POS changes. Over time, this democratization supports competitive diversity inside the next-generation customer loyalty market, with a long tail of brands able to fund relevant benefits and governed personalization.

By End-User Industry: Retail Dominates Share; BFSI Leads Growth with Embedded Finance

Retail and e-commerce accounted for a 31.38% share in 2025 as loyalty became foundational to repeat purchasing, cross-basket upsell, and store-identified sales performance. Leading retailers integrate loyalty enrollment, member pricing, pay-with-points, and account management across web, app, and point-of-sale to reduce friction and deliver immediate value. Operators are also connecting program data to retail media to close the loop between exposure, conversion, and incrementality, which strengthens budget cases for one-to-one offers. Mobile wallet passes are amplifying member recognition and coupon-less redemption through notification delivery and at-register validation, helping staff serve members consistently in high-volume environments. As retail journeys bridge the store and digital, the next-generation customer loyalty market anchors identity, benefits, and offers as part of core retail operations rather than as sidecar marketing initiatives.

BFSI is the fastest-growing end-user segment and is projected to expand at a 22.35% CAGR through 2031 as banks embed loyalty across payments and everyday finance. New programs like BofA Rewards and PNC TotalRewards combine credit card reward bonuses, higher savings rates, and relationship-based benefits to create holistic value that reinforces primary account status. PNC’s tiered model, with a national rollout in 2026, demonstrates the scale of relationship-linked perks, where enrollment is automatic based on balances and benefits extend from lending to service tiers, thereby strengthening retention and cross-sell. Payments-linked loyalty is also extending into partner ecosystems as financial institutions power co-branded engagement and merchant-funded rewards across fitness, retail, and travel. This evolution reinforces the next-generation customer loyalty industry as payments, commerce media, and identity converge for omnichannel activation.

By Engagement Channel: Mobile Apps Dominate; Social/Messaging Channels Surge

Mobile Applications held a 43.44% share in 2025, reflecting customer preference for unified experiences that integrate earning, redemption, and help in a single interface across web-to-app journeys. Many programs use wallet-native passes as an auxiliary channel to reduce download friction, improve notification visibility, and deliver enrollment and balances to a broader audience. Since wallet APIs enforce rate limits per second, operators design event flows that queue or batch lower-priority updates to preserve responsiveness during peaks, which stabilizes member trust during high-traffic campaigns. Across the next-generation customer loyalty market, app and wallet strategies are complementing each other to widen reach and ensure real-time offer execution that meets customer expectations at checkout and in digital channels. This hybrid approach supports predictable redemption, stronger conversion, and durable member satisfaction.

Social or Messaging Channels are projected to grow fastest at a 16.33% CAGR through 2031, and the next-generation customer loyalty market size for this channel is projected to expand at that pace as conversational interfaces help members get balances, reminders, and incentives without switching contexts. Teams are embedding loyalty within messaging workflows to surface timely, location-aware perks and coordinate with email and push while respecting consent and frequency controls. At the store level, staff can recognize members via phone number, QR code, or wallet pass validation, reducing enrollment friction and supporting line-speed service during busy periods. As these channels mature, brands are closing the loop from conversation to conversion with real-time eligibility checks and automatic reward application that are easier to adopt for SMEs and enterprises alike. The cumulative impact strengthens the next-generation customer loyalty market by balancing channel diversity with consistent identity and rapid offer fulfillment.

Geography Analysis

North America held 37.35% of the next-generation customer loyalty market share in 2025, supported by high digital adoption, omni-channel maturity, and an expanding set of AI-first loyalty orchestration tools. Platforms in 2026 are launching embedded agents that analyze signals, surface risks, and recommend retention actions to improve the speed and precision of personalization. New bank programs broaden eligibility and unify benefits across cards, deposits, savings, and lending, strengthening customer primacy and underscoring loyalty’s role in financial relationship depth. PNC’s national rollout approach shows how relationship metrics trigger automatic tiering and service differentiation that scales across markets. North American operators are also leaning into wallet-native channels to deliver app-free enrollment and redemption with policy-governed notifications that reach members reliably at scale. Coalitions and linked programs are expanding in Canada, where industry associations highlight the advantages of cross-brand value exchange for frequency and spend consolidation.

Asia-Pacific is projected to be the fastest-growing region, with a 11.64% CAGR through 2031, reflecting mobile-first adoption and a strong foundation for super-app and wallet-linked loyalty. Financial services and travel alliances are connecting banks and hospitality to enable dual earning and redemption that fits frequent travel corridors across major cities. As bank partners expand program relevance into everyday spend, hospitality networks gain more top-of-funnel opportunities while card issuers deepen engagement through lifestyle rewards. Wallet passes and lightweight validation methods are well-suited to urban density and store network complexity, enabling consistent recognition and faster redemption without requiring app installs. This foundation supports the next-generation customer loyalty market as APAC brands balance growth with compliance and expand cross-merchant engagement models.

Europe pairs advanced analytics capabilities with high-standard consent governance, rewarding transparent value exchange and stronger member participation. Retail programs are partnering with AI-first orchestration tools to deepen personalization for tens of millions of households and to accelerate experimentation with content and offers at scale. Wallet-native technology continues to enhance the in-store experience by reducing friction and enabling rapid enrollment and balance updates. Still, it requires attention to platform limits and image guidelines to protect performance during peak usage. In the Middle East and Africa, new hospitality partnerships with leading banks enable point conversion and broaden redemption options that resonate with regional travel and retail patterns. As these regions expand digital payments and unify identity across channels, the next-generation customer loyalty market builds a diversified base for omnichannel programs that are flexible, compliant, and scalable.

Competitive Landscape

The next-generation customer loyalty market shows moderate concentration with intensifying rivalry across enterprise suites, specialist loyalty platforms, and SMB-focused SaaS providers. Enterprise CX suites now embed loyalty orchestration into journey platforms, equipping brands with agents that analyze signals and propose retention actions to accelerate measurable outcomes. Specialist providers continue to differentiate through composable, API-first architectures that plug into real-time CDPs and point of sale for instant incentives and granular governance. SMB-focused platforms emphasize speed to value with wallet-native passes, receipt validation, and message channel integrations that reduce engineering lift and speed deployment. This stratification underscores the strategic shift from one-off promotions to unified data assets that inform merchandising, finance, and operations.

Strategy patterns highlight three vectors. First, AI enablement is moving from analytics to orchestration, with embedded agents, insight surfacing, and real-time offer builders now shipping in production platforms to scale one-to-one experiences. Second, coalition and partner ecosystems are gaining momentum as cross-brand programs extend relevance into everyday categories and link currencies across airlines, fuel, retail, and hospitality. Third, wallet-native engagement is becoming a durable complement to apps and web, adding always-on surfaces with clear platform governance for speed and reliability at checkout. Together, these moves reinforce the next-generation customer loyalty market as a convergence point for identity, payments, and offer logic with closed-loop attribution.

Disruptors and incumbents alike are racing to operationalize composability. Real-time incentive engines are integrating directly with journey platforms and CDPs, enabling event-triggered rewards and omnichannel consistency with centralized governance. Receipt-scanning and upload features are democratizing SKU-level rewards for brands that do not own the point of sale, which broadens loyalty’s reach to sectors selling through third-party retailers. Specialist marketers are also connecting loyalty and merchant-funded rewards into unified intelligence layers that monetize off-platform spend and expand funded incentives without discounting margin. As these elements mature, the next generation customer loyalty market aligns technology investment with measurable outcomes and compliance-by-design operations.

Next-Generation Customer Loyalty Industry Leaders

Salesforce Inc.

Oracle Corp. (CrowdTwist)

Comarch SA

Capillary Technologies

Epsilon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Adobe launched Adobe Journey Optimizer Loyalty, an AI-first loyalty orchestration application that transforms static loyalty programs into living systems with agent-driven insights, unified data, and cross-channel activation.

- April 2026: Tesco and Adobe entered a strategic AI partnership to personalize experiences and reward loyalty for 24 million-plus Clubcard households, including an innovation lab for scaled experimentation.

- April 2026: WestJet and Petro-Canada announced a loyalty partnership enabling linked accounts for cross-program earning and redemption across travel and fuel categories.

- March 2026: PAR Technology launched PAR Retail Drive AI, an intelligence layer for convenience and fuel retailers that brings real-time insights, agentic automation, and multi-agent strategy planning.

Global Next-Generation Customer Loyalty Market Report Scope

Next-Generation Customer Loyalty Market refers to the industry of advanced loyalty solutions that use digital platforms, data analytics, AI, personalization, and omnichannel rewards programs to help businesses increase customer retention, engagement, and lifetime value.

The Next Generation Customer Loyalty Market Report is Segmented by Organisation Size (Large Enterprises, Small & Medium Enterprises), End-User Industry (Retail & E-commerce, BFSI, Travel & Hospitality, Telecommunications, Healthcare, Media & Entertainment, Energy & Utilities, FMCG & CPG), Engagement Channel (Mobile Application, Web & E-mail, Point-of-Sale, Social/Messaging), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). Market Forecasts are Provided in Terms of Value (USD).

| Large Enterprises |

| Small & Medium Enterprises (SMEs) |

| Retail & E-commerce |

| BFSI |

| Travel & Hospitality |

| Telecommunications |

| Healthcare |

| Media & Entertainment |

| Energy & Utilities |

| FMCG & CPG |

| Mobile Application |

| Web & E-mail |

| Point-of-Sale (POS) |

| Social / Messaging |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Organisation Size | Large Enterprises | |

| Small & Medium Enterprises (SMEs) | ||

| By End-user Industry | Retail & E-commerce | |

| BFSI | ||

| Travel & Hospitality | ||

| Telecommunications | ||

| Healthcare | ||

| Media & Entertainment | ||

| Energy & Utilities | ||

| FMCG & CPG | ||

| By Engagement Channel | Mobile Application | |

| Web & E-mail | ||

| Point-of-Sale (POS) | ||

| Social / Messaging | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the next-generation customer loyalty market?

The next-generation customer loyalty market size was USD 12.32 billion in 2025 and is projected to reach USD 24.80 billion by 2031 at a 12.37% CAGR during 2026-2031.

Which engagement channels are leading and growing fastest in this space?

Mobile Applications led with 43.44% share in 2025, while Social or Messaging Channels are projected to grow the fastest at a 16.33% CAGR through 2031.

Which customer segments are most influential by company size?

Retail and e-commerce held 31.38% share in 2025, while BFSI is projected to post the fastest growth at a 22.35% CAGR through 2031 on the back of relationship-led and payments-linked programs.

Which region leads and which is scaling the fastest?

North America led with 37.35% share in 2025, and Asia-Pacific is projected to be the fastest-growing region at an 11.64% CAGR through 2031.

What capabilities are differentiating platforms in 2026?

AI-first orchestration, wallet-native engagement, and composable integrations with CDPs and POS for real-time incentives are the clearest differentiators shipping in production platforms.

Page last updated on: