Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

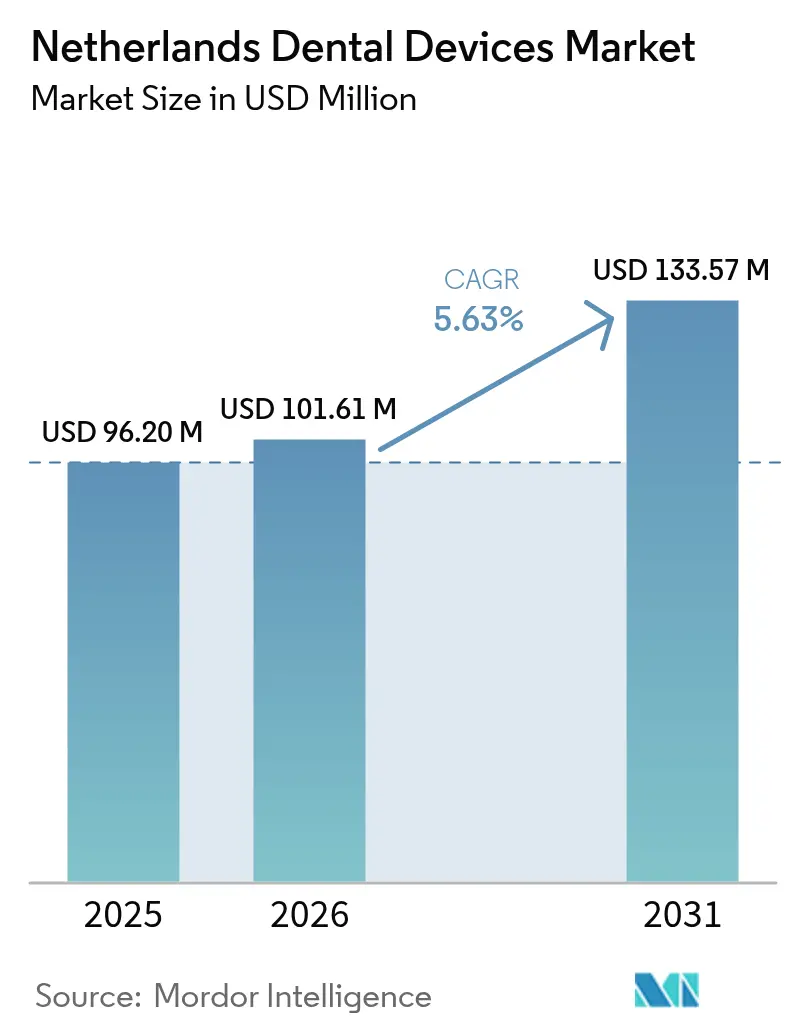

| Base Year Market Size (2025) | USD 96.20 Million |

| Market Size (2026) | USD 101.61 Million |

| Market Size (2031) | USD 133.57 Million |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Dental Devices Market Analysis by Mordor Intelligence

The Netherlands Dental Devices Market size was valued at USD 96.20 million in 2025 and estimated to grow from USD 101.61 million in 2026 to reach USD 133.57 million by 2031, at a CAGR of 5.63% during the forecast period (2026-2031).

The Netherlands dental devices market size stands at USD 96.20 million in 2025 and is projected to reach USD 129.47 million by 2030, recording a CAGR of 6.12% during the forecast period. Sustained public funding for basic dental insurance guarantees broad treatment access, while 84% of residents purchase supplementary coverage that reimburses higher-value procedures, thereby anchoring predictable demand across product categories. A steadily ageing population, low unmet-need ratios, and policy reforms that reward preventive care are translating into higher procedure volumes and faster turnover of consumables. Private-equity-backed corporate chains have begun buying solo practices and introducing standardised procurement, accelerating adoption of CAD/CAM systems, CBCT scanners, and chairside 3-D printers that cut chair-time and lift clinic throughput. Parallel growth in inbound cosmetic tourism centred on Amsterdam and Rotterdam is fostering specialist niches in orthodontics and aesthetic prosthodontics that favour premium clear aligners and zirconia-based restorations.

Key Report Takeaways

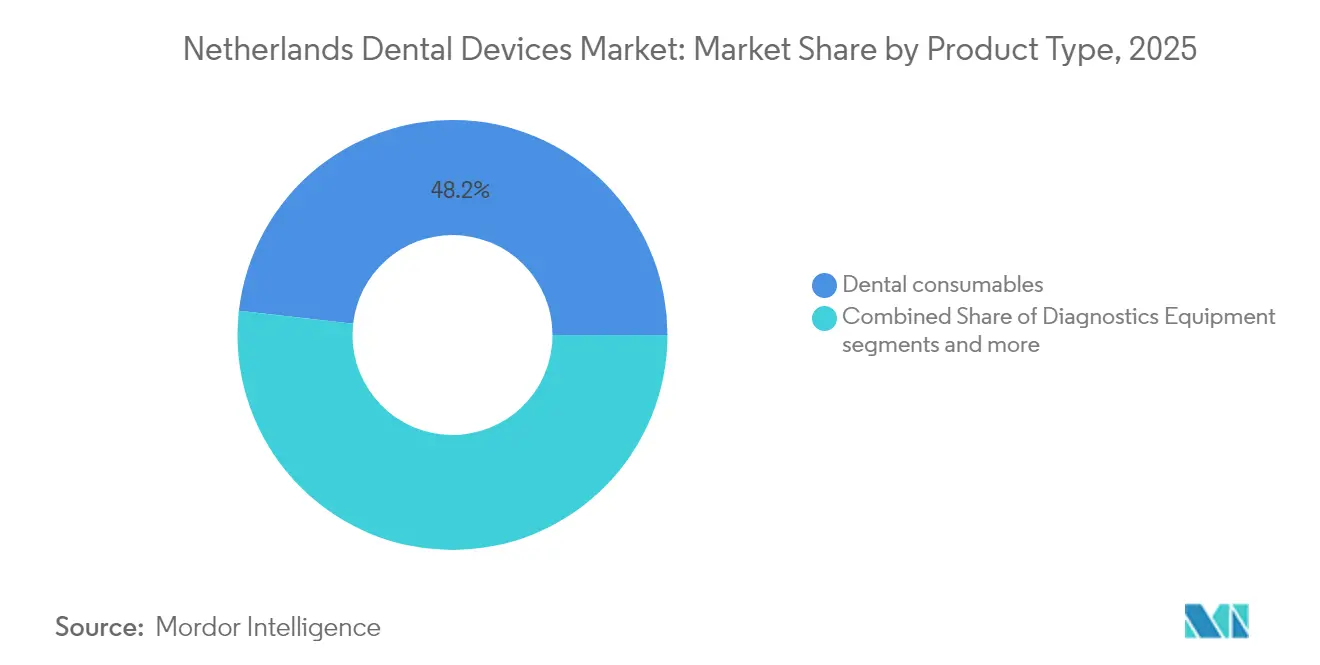

- By product type, dental consumables led with 48.21% of the Netherlands dental devices market share in 2025, while dental equipment is forecast to expand at a 6.31% CAGR to 2031.

- By treatment, prosthodontics accounted for 33.12% of the Netherlands dental devices market size in 2025 and is advancing at a 6.84% CAGR through 2031.

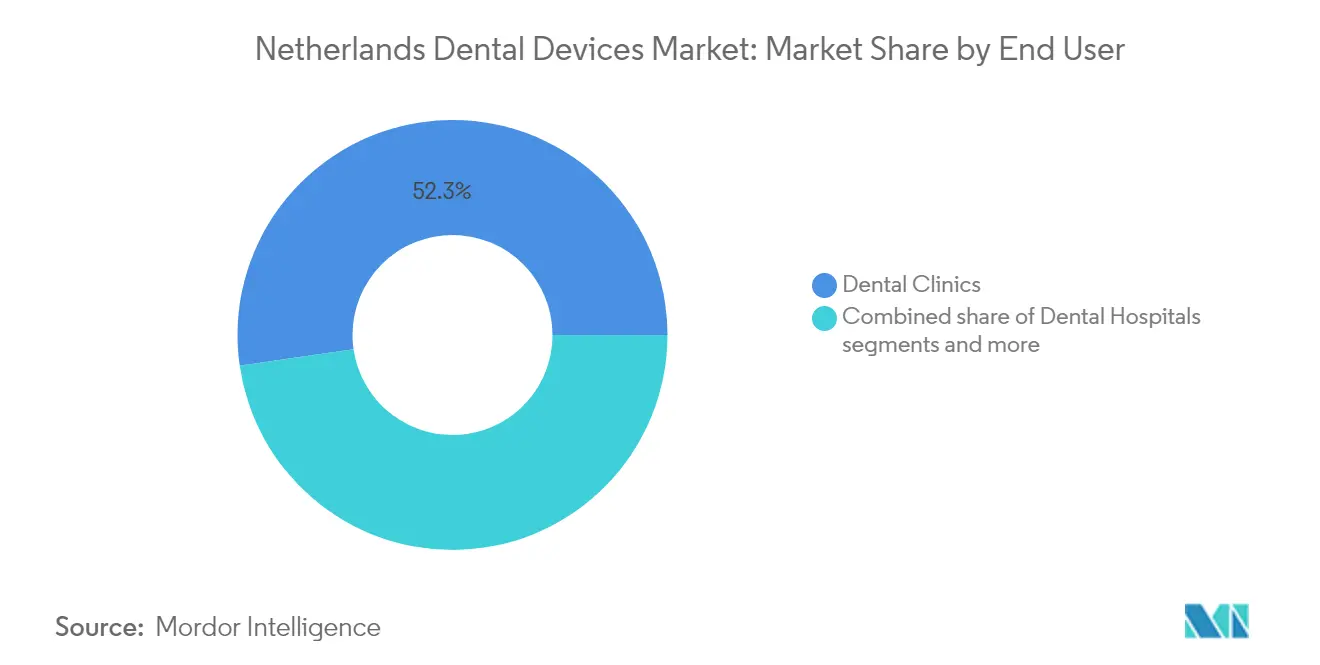

- By end user, dental clinics captured 52.29% revenue share in 2025; the segment is projected to grow at a 7.03% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Dental Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Government‐funded Basic Dental Insurance Coverage | +1.8% | National, with stronger impact in urban centers | Medium term (2-4 years) |

| Ageing Population Driving Implant Demand | +1.5% | National, with concentration in provinces with higher elderly populations | Long term (≥ 4 years) |

| Expansion of Corporate Dental Chains Standardising Procurement | +1.2% | National, with early concentration in Amsterdam, Rotterdam, Utrecht | Medium term (2-4 years) |

| Cosmetic-Tourism Surge in Amsterdam & Rotterdam | +0.9% | Amsterdam & Rotterdam, with spillover to Utrecht | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Government-funded Basic Dental Insurance Coverage

Comprehensive statutory insurance covers routine care for every resident, while supplementary policies reimburse advanced treatments, driving procedure frequency above the EU mean[1]Source: European Commission, “Eurostat—Unmet Dental Needs,” europa.euSource: European Commission, “Eurostat—Unmet Dental Needs,” europa.eu . The model incentivises annual check-ups, resulting in higher per-capita use of prophylactic consumables, radiology films, and disposable infection-control products. Reimbursement of digital impressions for crowns has spurred clinics to invest in intra-oral scanners that slash appointment times. Stable premium inflows give DSOs predictable cash-flows, encouraging bulk tenders for handpieces, bonding agents, and single-visit endodontic systems. Policy pilots that now refund guided implant surgery are set to widen the addressable base for high-margin surgical kits over the next three years.

Ageing Population Driving Implant Demand

People aged 65 and above will constitute 24% of Dutch residents by 2030, up from 20% in 2024, and they retain more natural teeth, necessitating complex restorations rather than full dentures[2]Source: Statistics Netherlands (CBS), “Population Forecast 2025-2030,” cbs.nl . Clinical guidelines increasingly recommend implant-supported overdentures for edentulous arches, boosting unit sales of titanium fixtures and biomimetic abutments. Manufacturers are rolling out shorter implants and surface-treated screws that osseointegrate in denser cortical bone often found in seniors. Public health surveys show 73.5% of citizens aged 65-74 visited a dentist in 2024, far above the EU average, signalling a robust pipeline for high-value regenerative materials. Geriatric demand is also lifting intra-surgical imaging uptake; CBCT scans help visualise pneumatized sinuses, reducing implant failures and supporting bundling of imaging-plus-surgery service packages.

Expansion of Corporate Dental Chains Standardising Procurement

Private-equity funds have poured capital into buy-and-build platforms such as Curaeos and Colosseum Dental, which together manage more than 350 chairs nationwide. These DSOs consolidate ordering through central warehouses, preferring vendors that supply full portfolios—from prophylaxis cups to chairside mills—under long-term agreements. Standardisation reduces SKU complexity by up to 30%, pushing clinics toward unified software ecosystems such as cloud-based practice-management tools that integrate digital radiography and billing. Vendors respond with turnkey service contracts covering installation, training, and predictive maintenance, a shift that is enlarging recurring revenue streams. Central oversight also accelerates roll-outs of new tech: Curaeos outfitted 60 locations with intra-oral scanners in 2024 within six months, a scale unattainable for solo practitioners.

Cosmetic-Tourism Surge in Amsterdam & Rotterdam

Direct flights, English-speaking clinicians, and price gaps versus UK clinics are attracting inbound patients seeking veneers, whitening, and clear aligners. Clinics advertise chairside CAD/CAM veneer delivery in one visit, leveraging 5-axis mills paired with AI smile-design software. Procedure bundles command 2-3 times domestic case values, lifting revenue per chair and stimulating procurement of zirconia blocks, high-resolution scanners, and 3-D printers for provisional crowns. Hotspot clustering boosts competitive pressure, prompting continuous equipment upgrades to differentiate on turnaround speed and digital preview quality. Spill-over benefits suppliers selling whitening gels, thermal forming units, and aligner thermoplastics, albeit within a limited geographic corridor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated Dentist-to-Population Ratio | -0.7% | National, with higher impact in urban areas | Medium term (2-4 years) |

| Adult Orthodontic Reimbursement Caps | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saturated Dentist-to-Population Ratio

Netherlands counts roughly 5.2 dentists per 10,000 inhabitants, ranking among the highest in Europe. Intense local competition compresses margins, curbing equipment refresh cycles, particularly for solo practitioners in major cities. Younger graduates favour part-time schedules, and 23% of the workforce will retire by 2030, creating asymmetry between current oversupply and future gaps. For manufacturers, the dynamic shifts the value proposition toward devices that deliver measurable productivity gains—such as rapid-cycle sterilizers and dual-use lasers—rather than incremental feature upgrades. Financing packages that spread payments over five years are increasingly pivotal to close sales.

Adult Orthodontic Reimbursement Caps

Basic insurance excludes adult braces, and most voluntary plans cap annual orthodontic benefits at EUR 500 (USD 544), covering only a fraction of EUR 3,000-5,000 comprehensive treatments. Out-of-pocket cost sensitivities pull demand toward mid-priced metal brackets or shortened aligner courses, restraining premium clear aligner uptake. Some clinics counter with subscription plans, yet conversion remains limited outside affluent cohorts. Vendors have responded by introducing tiered aligner lines featuring fewer stages, but overall unit ASPs remain under pressure. Because aligner workflows drive ancillary sales of intra-oral scanners, bonded attachments, and finishing kits, the reimbursement ceiling dampens linked revenue across multiple device categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Transformation Reshaping Equipment Segment

Dental consumables led demand in 2025, commanding 48.21% revenue as routine prophylaxis, restorations, and endodontic interventions require constant restocking. High visit rates—80.5% of citizens attend yearly check-ups—ensure stable throughput of composites, etchants, and single-use handpiece sleeves, a trend amplified by strict infection-control regulations. The segment also captures rising volumes of bone grafts and resorbable membranes linked to implant surgeries for elderly patients. Procurement centralisation by DSOs is steering orders toward house-brand consumables sourced under private-label contracts, disrupting legacy distributor margins yet widening price-conscious clinic adoption.

The Netherlands dental devices market size for dental equipment is projected to expand at a 6.31% CAGR, outpacing consumables as clinics digitise workflows. Adoption of chairside CAD/CAM units rose 18% in 2024 alone, driven by same-day inlay delivery that eliminates temporaries and second visits. Unified software suites now link scanners, mills, and CBCT images, enabling data-driven treatment plans that differentiate clinics competing on patient experience. Diagnostic equipment growth mirrors heightened demand for low-dose CBCT units that visualise airway dimensions for sleep-apnoea screening, adding incremental clinical services without new chair investments.

By Treatment: Demographic Shifts Elevating Implant Procedures

Prosthodontics dominated treatments with 33.12% of revenue in 2025, sustained by the implant boom among seniors retaining partial dentition. Implant-supported crowns, overdentures, and full-arch bridges utilise higher-priced components plus surgical kits, lifting average spend per case. Clinical guidelines increasingly endorse immediate-load protocols, intensifying demand for torque-controlled handpieces and high-stability biomaterials. The Netherlands dental devices market size for implant surgery kits is forecast to post high-single-digit gains, supported by insurer pilots that fund digital surgical guides.

Orthodontics is the fastest-growing treatment line, advancing at a 6.87% CAGR through 2031 despite reimbursement caps. The surge is fuelled by teen aligner demand, growing adult aesthetic awareness, and inbound cosmetic tourists. Clear aligner platforms integrate AI-driven treatment simulations that shorten chair-side consultations, enabling clinics to scale case volumes. The Netherlands dental devices market share for intra-oral scanners climbed to 65% of new orthodontic records in 2025, underscoring tight equipment-procedure linkage. Cloud portals that let patients track progress boost adherence, a selling point that DSOs include in marketing campaigns aimed at affluent urban consumers.

By End User: Consolidation Driving Clinic Segment Growth

Dental clinics captured 52.29% of 2025 revenue and post the fastest projected CAGR at 7.03% as consolidation fuels capital spending. DSOs own about 10-15% of chairs but make disproportionate equipment purchases, standardising on multi-function treatment centres that integrate imaging, suction, and digital displays. Clinic operators negotiate multi-year frame agreements bundling service contracts, which underpins predictable aftermarket revenue for manufacturers.

Dental hospitals, though smaller in number, handle complex maxillofacial surgeries and paediatric special-needs cases. They adopt advanced operating microscopes, piezosurgery units, and regenerative biomaterials earlier than clinics, acting as regional reference sites that influence procurement trends. Academic institutes remain early adopters of AI-enabled diagnostic software, publishing validation studies that accelerate broader market acceptance. Collaborative R&D projects between universities and start-ups such as Lake3D are generating multi-material 3-D printing applications for personalised prostheses, indicating a pipeline of disruptive products slated for commercial rollout by 2027.

Geography Analysis

Geography Analysis

Amsterdam, Rotterdam, and Utrecht dominate sales are the key regions, driven by dense clinic networks and cosmetic tourism traffic. DSOs cluster in these metros, enabling vendor field teams to service multiple locations within short travel radii, which lowers service-hour costs and speeds installation cycles.

Northern and eastern provinces such as Groningen, Drenthe, and Overijssel feature higher ratios of residents aged 65 plus, lifting per-capita implant and overdenture procedures. However, dentist supply gaps loom as older practitioners retire, prompting grant programmes that subsidise digital equipment for clinics willing to open satellite branches in underserved towns. Vendors offering remote training and cloud-based maintenance tools gain an edge where on-site support is less feasible.

The southern cross-border provinces North Brabant and Limburg benefit from Belgian and German patient flows seeking lower wait times or specific aesthetic treatments, creating a micro-cluster of multilingual practices. These regions adopt CE-certified equipment rapidly due to familiarity with EU regulatory updates and enjoy logistical advantages from distribution hubs in Eindhoven and Venlo. Overall, geographic disparities steer manufacturer go-to-market strategies toward metropolitan key-account teams complemented by regional partners that can navigate local insurance formularies and practice cultures.

Competitive Landscape

Global majors—Dentsply Sirona, Straumann, Nobel Biocare, and Envista—anchor the premium tier with expansive portfolios and bundled training. Mid-tier European suppliers such as Planmeca and W&H leverage niche leadership in imaging and rotary instruments, respectively, while local innovators like Lake3D target additive-manufacturing niches. Market concentration is edging upward as DSOs channel purchases through preferred-supplier contracts that can account for 60% of their annual spend. Vendors able to provide integrated digital workflows, financing, and continuous education strengthen lock-in effects.

In 2024 Dentsply Sirona booked a USD 910 million net loss linked to goodwill write-downs but raised R&D outlays to accelerate software-hardware integration, unveiling DS Core cloud services that synchronise imaging, milling, and patient data. Straumann opened a new Benelux training centre in Utrecht, offering implantology masterclasses that double as live product demonstrations.

Disruptive entrants focus on clear aligners, AI diagnostics, and chairside 3-D printing. Swiss-Dutch start-up Relu has partnered with several Dutch DSOs to pilot machine-learning caries-detection software, reporting 15% diagnostic-time cuts. Procurement simplification by DSOs is spurring OEM-to-OEM alliances—Planmeca and Align Technology now co-market scanner-aligner bundles targeted at consolidated groups. Vendors lacking full digital ecosystems risk displacement as chains rationalise supplier lists.

Netherlands Dental Devices Industry Leaders

Zimmer Biomet

3M

Henry Schein Inc.

Ultradent Products Inc.

Dentsply Sirona

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Axcel-backed Oral Care agreed to acquire De Tandartsengroep, adding 31 clinics and eight labs, creating an 80-site Dutch network.

- March 2025: The Netherlands Authority for Consumers and Markets launched an inquiry into private-equity roll-ups in dental care under proposed Wibz legislation.

Netherlands Dental Devices Market Report Scope

As per the scope of the report, dental devices are the tools that dental professionals use to provide dental treatment. They include tools to examine, manipulate, treat, restore, and remove teeth and surrounding oral structures. Standard instruments are the instruments used to examine, restore, and extract teeth and manipulate tissues. The Netherlands Dental Devices Market is Segmented by Product (General and Diagnostics Equipment, Dental Consumables, and Other Dental Devices), Treatment (Orthodontic, Endodontic, Periodontic, Prosthodontic), and End User (Hospitals, Clinics, and Other End Users). The report offers the value (in USD million) for the above segments.

By Product

| Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra Oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair and Equipment | ||

| Therapeutic Equipment | Dental Hand Pieces | |

| Electrosurgical Systems | ||

| CAD/CAM Systems | ||

| Milling Equipment | ||

| Casting Machine | ||

| Other Therapeutic Equipments | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns and Bridges | ||

| Other Dental Consumables | ||

| Other Dental Devices | ||

By Treatment

| Orthodontic |

| Endodontic |

| Peridontic |

| Prosthodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| By Product | Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra Oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair and Equipment | |||

| Therapeutic Equipment | Dental Hand Pieces | ||

| Electrosurgical Systems | |||

| CAD/CAM Systems | |||

| Milling Equipment | |||

| Casting Machine | |||

| Other Therapeutic Equipments | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns and Bridges | |||

| Other Dental Consumables | |||

| Other Dental Devices | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Peridontic | |||

| Prosthodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current size of the Netherlands dental devices market?

The Netherlands Dental Devices Market is valued at USD 101.61 million in 2026 and is forecast to reach USD 133.57 million by 2031.

Which product segment is growing fastest?

Dental equipment, driven by CAD/CAM systems and CBCT scanners, is projected to register a 6.31% CAGR through 2031.

How large is the corporate DSO footprint in the country?

Dental Service Organizations control roughly 10-15% of Dutch chairs, a share that is expected to climb as private equity funds continue roll-ups.

Why is implant demand rising?

An ageing population retains more natural teeth, leading to complex restorative needs and increased preference for implant-supported overdentures.

Page last updated on: