Global Nerve Monitoring System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

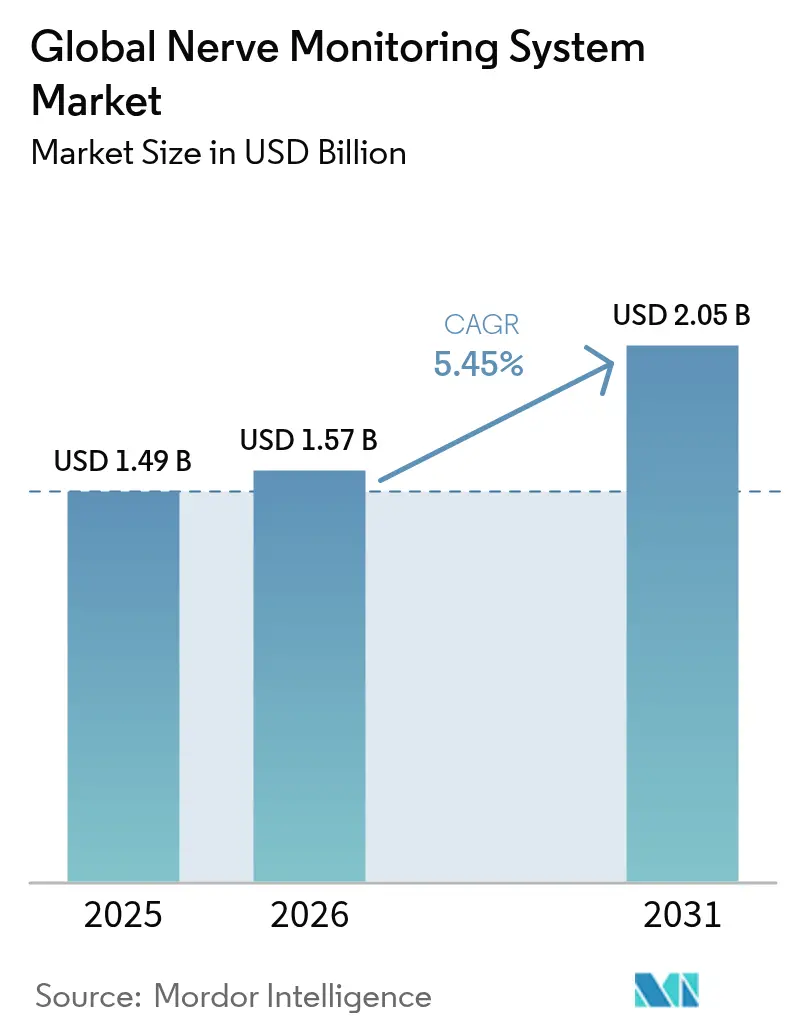

| Market Size (2026) | USD 1.57 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Nerve Monitoring System Market Analysis by Mordor Intelligence

The nerve monitoring systems market size is expected to grow from USD 1.49 billion in 2025 to USD 1.57 billion in 2026 and is forecast to reach USD 2.05 billion by 2031 at 5.45% CAGR over 2026-2031. Rising surgical complexity, mandatory patient-safety regulations, and the convergence of artificial intelligence with real-time neurophysiological monitoring are central to this expansion. Hospitals are embedding intraoperative nerve monitoring into spinal, neurosurgical, and ENT protocols to improve outcomes and limit liability exposure. Vendors are shifting toward consumable-driven revenue models that capitalize on electrodes and probes used in every procedure. Simultaneously, cloud-based remote monitoring services and AI-assisted analytics are widening access for facilities lacking full-time neurophysiologists. Consolidation among health systems is intensifying price negotiations but also unlocking large bundled contracts for suppliers able to provide end-to-end solutions.

Key Report Takeaways

- By product category, nerve monitors led with 45.32% of the nerve monitoring systems market share in 2025; nerve stimulation electrodes and probes are projected to expand at a 6.55% CAGR to 2031.

- By technology, electromyography commanded 38.92% share of the nerve monitoring systems market size in 2025 and is advancing at a 6.95% CAGR through 2031.

- By application, neurosurgery accounted for 30.74% share of the nerve monitoring systems market in 2025, while spine surgery is set to grow fastest at 7.29% CAGR through 2031.

- By end user, hospitals and surgical centers held 64.41% of the nerve monitoring systems market in 2025, yet ambulatory surgical centers are expanding at 7.63% CAGR to 2031.

- By geography, North America maintained 41.38% revenue in 2025; Asia-Pacific is the fastest-growing region at 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nerve Monitoring System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of intraoperative EMG in spinal & neurosurgery | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing reimbursed ENT nerve-monitoring procedures | +0.8% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Growth in complex oncology resections requiring IONM | +0.9% | Global, led by developed markets | Long term (≥ 4 years) |

| Hospital consolidation driving bundled device purchases | +0.7% | North America primarily, spreading to Europe | Medium term (2-4 years) |

| AI-assisted real-time signal-quality analytics | +0.6% | Global, early adoption in tech-forward markets | Long term (≥ 4 years) |

| Growth of cloud-based remote IONM service providers | +0.5% | North America & Europe, regulatory-dependent expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Intraoperative EMG in Spinal & Neurosurgery

Electromyography has become standard in complex spine and cranial procedures, driven by 2020 Korean guidelines that list EMG as essential for motor-pathway preservation and raise adoption above 85% in spinal deformity cases. Multimodal protocols that combine EMG with somatosensory and motor-evoked potentials have reduced false-negative rates below 2%, which lowers malpractice risk for surgeons and institutions. Robotic platforms increasingly rely on EMG data for autonomous trajectory correction, embedding the technology deeper into surgical workflows. Predictable demand for electrodes and probes stabilizes consumable revenue and encourages suppliers to refine single-use designs. Ongoing clinical studies continue to show better neurological outcomes when EMG is employed, reinforcing hospital purchasing decisions and strengthening the nerve monitoring systems market.

Increasing Reimbursed ENT Nerve-Monitoring Procedures

Enhanced CPT codes released by the American Academy of Otolaryngology simplified billing for intraoperative neurophysiology in endocrine and airway surgeries. Continuous monitoring now receives higher payment than intermittent approaches, allowing providers to upgrade equipment without eroding margins. Specialized endotracheal tubes embedded with electrodes shorten setup time and improve signal stability, expanding surgeon acceptance. Thyroid procedures adopting continuous monitoring have shown lower rates of recurrent laryngeal nerve injury, which translates into measurable cost savings for insurers. The reimbursement momentum is pulling new suppliers into the ENT segment and intensifying competition for procedure-specific consumables within the nerve monitoring systems market.

Growth in Complex Oncology Resections Requiring IONM

Pelvic intraoperative neuromonitoring lowered postoperative urinary dysfunction from 19% to 8% in the NEUROS multicenter trial. Evidence-based protocols are now mandated by top oncology centers for rectal, prostate, and head-and-neck cancers. Brachial plexus tumor resections using multimodal monitoring preserved neurological function in 94% of cases across 36-patient cohorts. These success metrics justify premium pricing for high-channel monitors and disposable electrodes. Integrating monitoring data with intraoperative navigation and fluorescence imaging enlarges procedural complexity and cements the nerve monitoring systems market as a cornerstone of modern oncologic surgery.

Hospital Consolidation Driving Bundled Device Purchases

Integrated delivery networks negotiate multiyear contracts covering capital systems, electrodes, and service agreements, creating volume commitments that favor full-portfolio vendors. USMON’s workflow platform manages more than 3 million patient records and USD 6 billion in claims annually, illustrating the scale that consolidated entities can command. Bundled purchasing lowers per-unit electrode pricing but locks suppliers into exclusive long-term relationships. Vendors able to demonstrate outcome gains and compliance support gain preferred-supplier status, reinforcing the competitiveness of the nerve monitoring systems market among the largest health systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost & disposable electrode pricing | -0.9% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Shortage of certified neurophysiologists | -1.1% | North America & Europe primarily | Medium term (2-4 years) |

| Signal-latency risks in remote monitoring | -0.4% | Global, concentrated in regions adopting telemedicine | Medium term (2-4 years) |

| Cyber-security vulnerabilities in connected OR suites | -0.6% | Global, with heightened concern in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Disposable Electrode Pricing

Comprehensive monitoring consoles range from USD 150,000 to USD 300,000, a hurdle that smaller ambulatory centers and emerging-market hospitals struggle to clear. Single-use electrodes add USD 200-500 for each surgery, pressuring margins in cost-sensitive settings. Although 2024 coding changes increased reimbursement for some neuromodulation procedures, gaps persist across many indications[1]Source: ASRA Pain Medicine, “Changes in Coding and Payment for Neuromodulation Procedures in 2024,” asra.com . Leasing models and pay-per-use contracts are gaining favor among budget-constrained providers, yet up-front costs remain a primary adoption barrier that tempers expansion of the nerve monitoring systems market, especially outside high-income economies.

Shortage of Certified Neurophysiologists

Training programs produce fewer than 200 certified neurophysiologists annually in North America, well below demand projections. Surveys show 70% of surgeons favor supervision by a neurologist or neurophysiologist over technologists, but staffing shortfalls push facilities to rely on less-qualified personnel. Universities are scaling certificate curricula and online modules that promise salaries of USD 70,000-99,000 for new entrants. Still, the specialty’s lengthy apprenticeship requirements delay workforce expansion. Staffing gaps restrict procedure volumes and slow the nerve monitoring systems market in regions where remote solutions or AI decision support are not yet fully deployed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monitors Lead While Consumables Accelerate

The nerve monitoring systems market recorded 45.32% revenue from nerve monitors in 2025, underscoring their role as foundational capital investments for hospitals. However, nerve stimulation electrodes and probes are growing at 6.55% CAGR, a signal that recurring consumable sales will contribute an increasing share of overall profit pools. Accessories and other consumables show the fastest velocity as single-use policies help eliminate sterilization costs and cross-contamination risk. The product mix is evolving toward a razor-and-blade model that stabilizes vendor cash flow and incentivizes continuous innovation in electrode design.

Consumable-centric strategies also mitigate the liability exposure associated with capital devices, highlighted by the 2024 recall of a major monitoring system linked to patient injuries. Premium electrodes that deliver higher signal-to-noise ratios and integrate RFID tracking command prices above USD 500 per case, offsetting lower device margins. As health systems centralize purchasing, suppliers offering flexible service contracts and automatic replenishment gain an advantage. These developments reinforce the position of consumables as critical growth drivers within the nerve monitoring systems market.

By Technology: EMG Dominance Drives Innovation

Electromyography contributed 38.92% revenue in 2025 and is expanding at 6.95% CAGR, reflecting its versatility across spine, cranial, and ENT applications. EMG’s compatibility with AI platforms accelerates its adoption further because machine learning improves artifact rejection and speeds alerting. Electroencephalography and evoked-potential monitoring remain essential in awake craniotomies and complex scoliosis corrections, though they occupy smaller revenue brackets. Electrocorticography persists as a niche used mainly in epilepsy surgery but commands premium pricing due to highly specialized demand.

Integration of multimodal monitoring is rising among Japanese spine surgeons who combine EMG, SSEPs, and MEPs to enhance surgical confidence. Vendors now position their consoles as open platforms that accept multiple signal modalities and third-party software, future-proofing customer investment. Robotic surgery solutions require millisecond-level feedback loops, pushing technology providers to refine latency and data-fusion capabilities. These requirements sustain high R&D spending and keep the nerve monitoring systems market on a steady trajectory of incremental technical improvement.

By Application: Spine Surgery Momentum Challenges Neurosurgery Leadership

Neurosurgery held 30.74% of revenue in 2025, yet spine surgery is on track for the fastest expansion at 7.29% CAGR as aging populations increase demand for deformity and fusion procedures acn.kr. Standardized guidelines have made spinal monitoring routine, which in turn elevates electrode consumption volume. ENT procedures benefit from favorable reimbursement, particularly for thyroid and parathyroid operations where continuous monitoring prevents recurrent laryngeal nerve injury. Oncology resections in the pelvis and brachial plexus continue to stimulate usage of high-channel systems that support nuanced functional mapping.

Application diversification spreads revenue risk and creates multiple entry points for new suppliers specializing in procedure-specific accessories. Robotic-assisted surgeries across spine, orthopedics, and soft-tissue fields require plug-and-play monitoring integration, further entwining monitoring with next-generation surgical platforms. As evidence linking IONM to reduced complication rates grows, payers and hospitals incorporate monitoring into quality metrics, increasing the baseline demand across every surgical vertical of the nerve monitoring systems market.

By End User: Ambulatory Centers Challenge Hospital Dominance

Hospitals and large surgical centers commanded 64.41% revenue in 2025 thanks to their infrastructure readiness and ability to manage complex surgeries. Ambulatory surgical centers are expanding at 7.63% CAGR as outpatient spine and ENT procedures migrate to lower-cost settings. Specialty clinics focused on pain management and minimally invasive surgery are also adopting compact monitoring systems that fit procedure-specific rooms.

Remote neurophysiology oversight levels the playing field by giving smaller facilities access to expert interpretation without hiring full-time staff. Portable consoles designed for quick setup and touchscreen workflows cater to teams with limited technical training. Group purchasing organizations extend hospital standards into affiliated ambulatory sites, driving uniformity in equipment choice. These shifts create fresh demand pockets while balancing the customer base within the nerve monitoring systems market.

Geography Analysis

North America retained 41.38% revenue in 2025, propelled by robust reimbursement and the presence of leading equipment makers. High surgical volumes in spine and ENT specialties underpin stable electrode consumption. Regulatory scrutiny of cybersecurity in operating-room devices spurred some hospitals to pivot toward domestic suppliers, a trend that reshapes vendor share. Workforce shortages encourage rapid uptake of remote monitoring networks and AI decision support, sustaining technology churn across the region’s nerve monitoring systems market.

Asia-Pacific is projected to post an 8.02% CAGR through 2031, the fastest globally, as countries invest in surgical infrastructure and adopt Western procedural protocols. China’s National Medical Products Administration streamlined device approvals in 2024, facilitating quicker import of monitoring platforms english.nmpa.gov.cn. India’s medical device sector, forecast to hit USD 50 billion by 2030, remains largely import-dependent, offering multinational vendors substantial runway Japan demonstrates sophisticated multimodal monitoring adoption, integrating AI analytics and robotics into routine spine surgery.

Europe shows steady expansion anchored by harmonized safety regulations and cross-border care initiatives. Hospital consolidation encourages bundled equipment contracts similar to North America. Meanwhile, South America and the Middle East register rising but uneven adoption as cost constraints persist. Tele-monitoring mitigates local staffing shortages, allowing smaller hospitals to participate in advanced procedures. Each of these regional dynamics contributes to the diversified growth profile of the nerve monitoring systems market worldwide.

Competitive Landscape

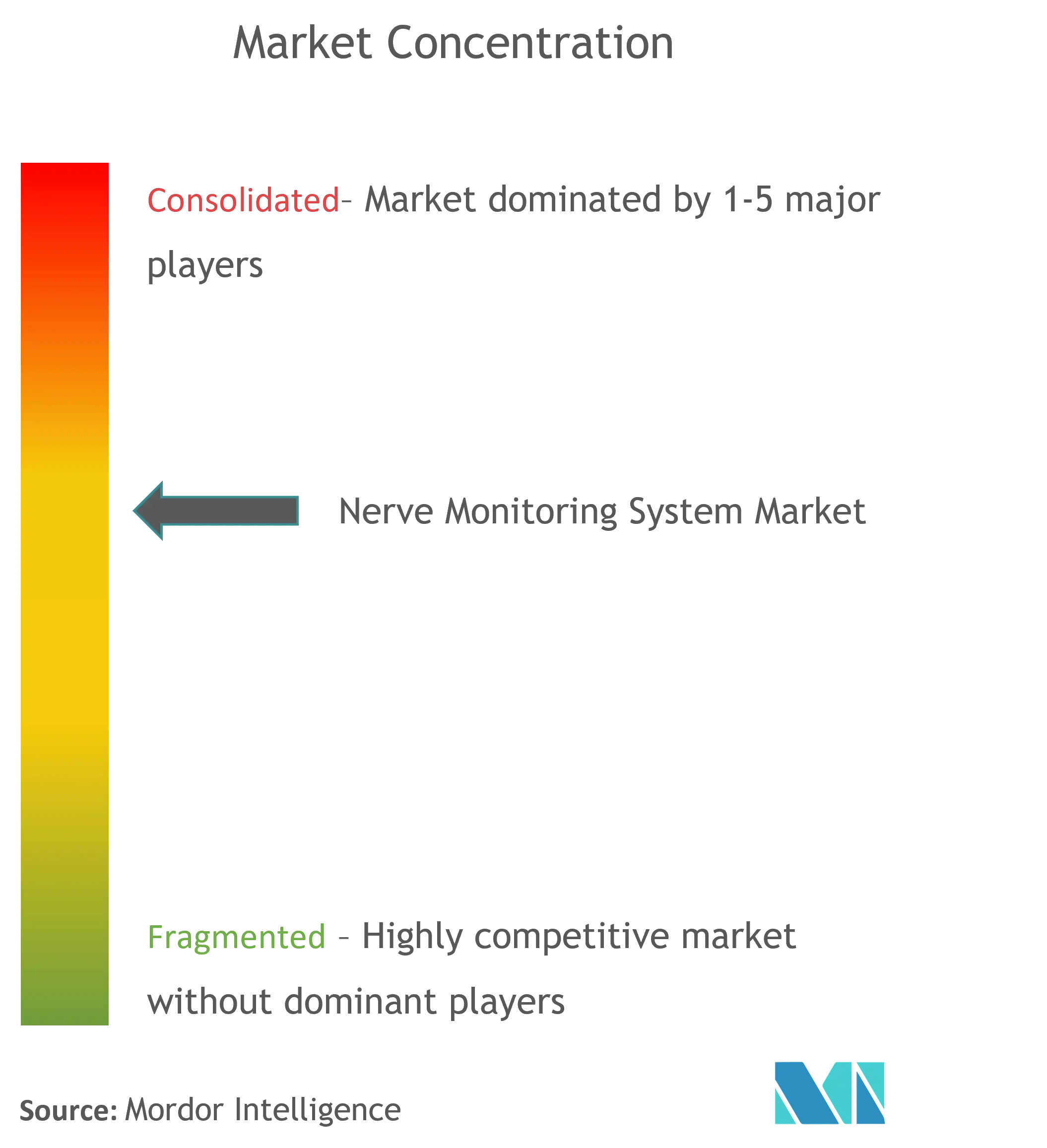

The nerve monitoring systems market is moderately concentrated, with leading manufacturers leveraging broad patent portfolios, regulatory experience, and clinical-evidence pipelines to protect share. Established companies such as Medtronic and Nihon Kohden pair equipment with proprietary electrodes and long-term service contracts that bind customers. Mid-tier suppliers compete through specialization, focusing on niche applications like intracranial electrodes or pediatric spine systems. Service providers that offer remote neurophysiology already partner with hardware vendors to deliver bundled outcomes guarantees, satisfying health-system demands for accountability and cost control.

Scale advantages are prompting mergers and acquisitions. Globus Medical’s USD 250 million purchase of Nevro in February 2025 broadened its neuromodulation footprint and offered cross-selling potential into monitoring customers. Nihon Kohden acquired a majority stake in NeuroAdvanced to deepen its electrode portfolio and solidify North American distribution[2]Source: Nihon Kohden Corporation, “Notice Regarding Acquisition of NeuroAdvanced,” nihonkohden.com . Such deals reflect a race to own differentiated consumables and advanced signal-analysis software, both critical to sustaining margin in an environment where basic hardware is increasingly commoditized.

Technology leadership now hinges on integrating AI algorithms, cybersecurity safeguards, and interoperability with robotic surgery platforms. Vendors unable to demonstrate measurable outcome gains risk contract exclusion by group purchasing organizations seeking standardized, data-driven value. Conversely, companies that embed cloud analytics and remote service capabilities position themselves at the forefront of the nerve monitoring systems market’s evolution toward connected, outcome-based healthcare delivery.

Global Nerve Monitoring System Industry Leaders

Medtronic

NuVasive, Inc.

Nihon Koden

Natus Medical

Checkpoint Surgical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Globus Medical announced acquisition of Nevro Corp for USD 250 million, expanding its neuromodulation portfolio.

- February 2025: Medtronic launched CD Horizon ModuLeX spinal system within the AiBLE ecosystem.

Global Nerve Monitoring System Market Report Scope

Per the report's scope, nerve monitoring systems enable surgeons to identify, confirm, and monitor motor nerve function to help reduce the risk of nerve damage during various procedures. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Nerve Monitors |

| Nerve Stimulation Electrodes & Probes |

| Accessories & Consumables |

| Electromyography (EMG) |

| Electroencephalography (EEG) |

| Evoked Potentials (EP) |

| Electrocorticography (ECoG) |

| Neurosurgery |

| Spine Surgery |

| ENT Surgery |

| Cardiovascular & Other Surgeries |

| Hospitals & Surgical Centers |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Nerve Monitors | |

| Nerve Stimulation Electrodes & Probes | ||

| Accessories & Consumables | ||

| By Technology | Electromyography (EMG) | |

| Electroencephalography (EEG) | ||

| Evoked Potentials (EP) | ||

| Electrocorticography (ECoG) | ||

| By Application | Neurosurgery | |

| Spine Surgery | ||

| ENT Surgery | ||

| Cardiovascular & Other Surgeries | ||

| By End User | Hospitals & Surgical Centers | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Global Nerve Monitoring System Market?

The Global Nerve Monitoring System Market size is expected to reach USD 1.57 billion in 2026 and grow at a CAGR of 5.45% to reach USD 2.05 billion by 2031.

Which product segment generates the highest revenue?

Nerve monitors hold 45.32% revenue, making them the leading product category.

Why is Asia-Pacific the fastest-growing region?

Expanded surgical infrastructure, streamlined regulatory pathways, and rising procedure volumes drive an 8.02% CAGR in the region.

How are AI technologies influencing intraoperative monitoring?

AI platforms improve signal-quality analytics with over 95% accuracy, reduce false alerts, and enable cloud-based predictive maintenance.

What limits the wider adoption of nerve monitoring systems?

High capital costs, expensive disposable electrodes, and a shortage of certified neurophysiologists remain the primary barriers.

Page last updated on: