Necrotizing Fasciitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Necrotizing Fasciitis Treatment Market Analysis by Mordor Intelligence

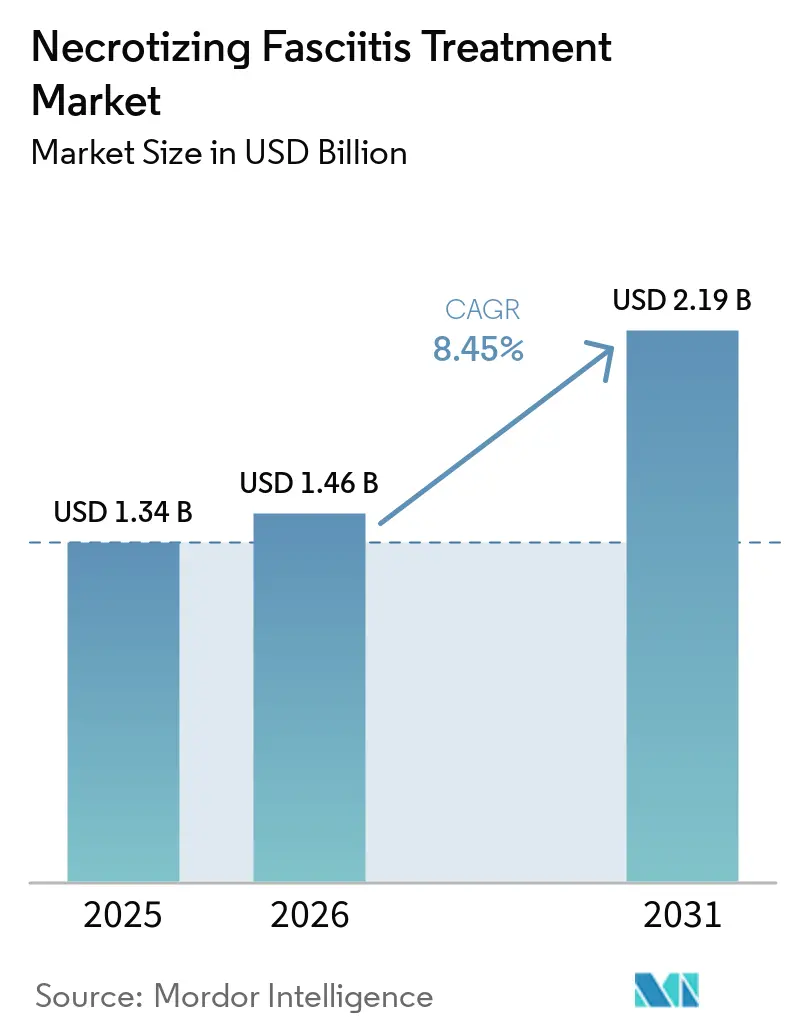

The Necrotizing Fasciitis Treatment Market size is projected to be USD 1.34 billion in 2025, USD 1.46 billion in 2026, and reach USD 2.19 billion by 2031, growing at a CAGR of 8.45% from 2026 to 2031.

The market is advancing faster than many infection care niches because the highest-risk patient pool now includes more people with diabetes, severe obesity, transplant-related immunosuppression, cancer treatment exposure, and chronic steroid use across major healthcare systems. Diabetes remained the most visible comorbidity in published cohorts, appearing in 47% to 62% of cases across Asia, North America, and Europe, and that pattern matters because these patients often need more debridements, longer ICU care, and broader use of adjunctive wound management after surgery. The result is that growth comes from both case incidence and a larger treatment bundle per admission, which supports spending across surgery, antibiotics, wound care, and supportive critical care. Competition still remains spread across product niches rather than integrated disease platforms, which leaves room for companies that can build stronger positions in NPWT, toxin-suppressive anti-infectives, biologic debridement, or NF-specific development programs. At the same time, the market still faces limits from referral delays outside tertiary centers and from cautious reimbursement for IVIG and HBOT, which keeps part of the addressable opportunity tied to evidence generation and better access pathways.

Key Report Takeaways

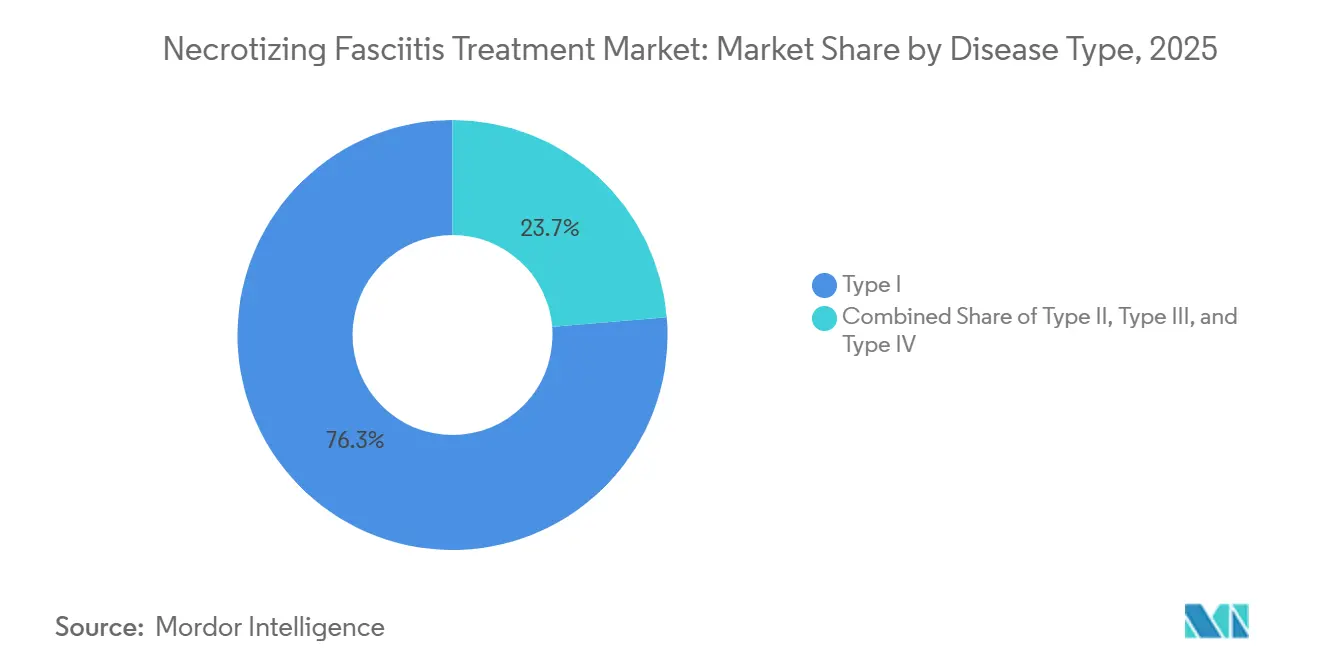

- By disease type, Type I polymicrobial NF held 76.3% of the necrotizing fasciitis treatment market share in 2025, while Type II monomicrobial NF is forecast to grow at a 9.4% CAGR through 2031.

- By treatment modality, surgical intervention accounted for 22.2% of the necrotizing fasciitis treatment market size in 2025, while antibiotic therapy is projected to expand at a 9.5% CAGR through 2031.

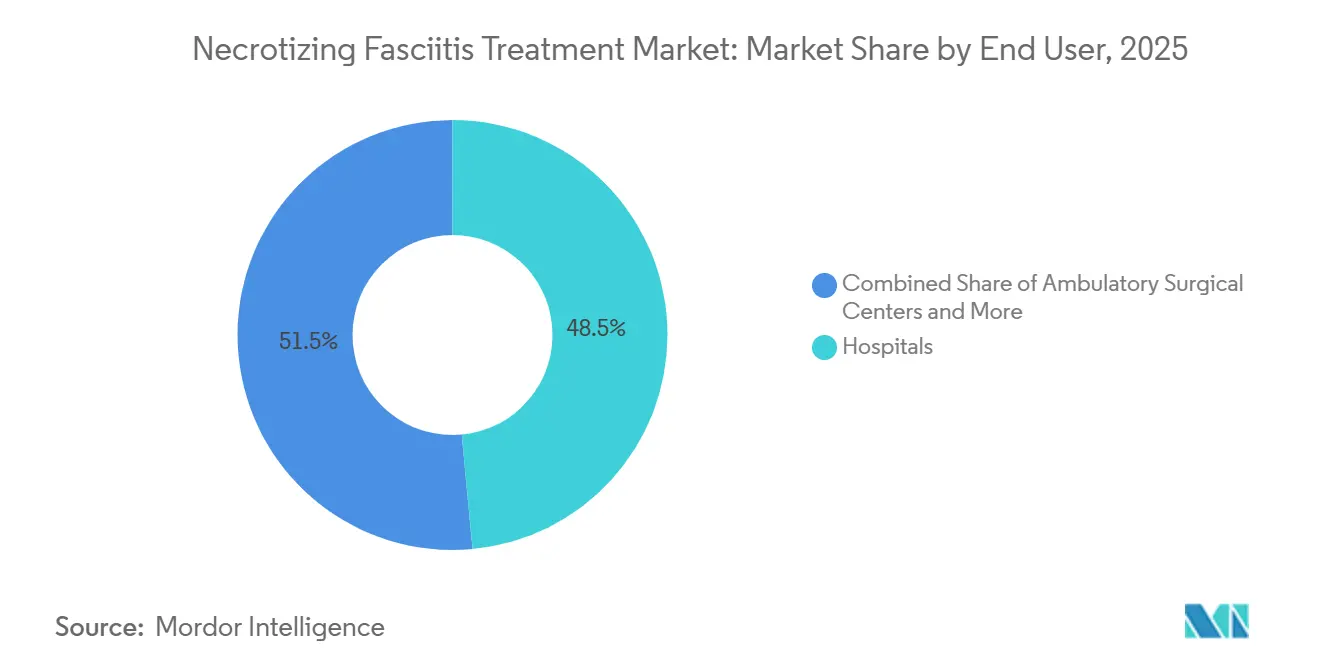

- By end user, hospitals held 48.5% of the market in 2025, while ambulatory surgical centers are forecast to record the highest CAGR at 9.3% through 2031.

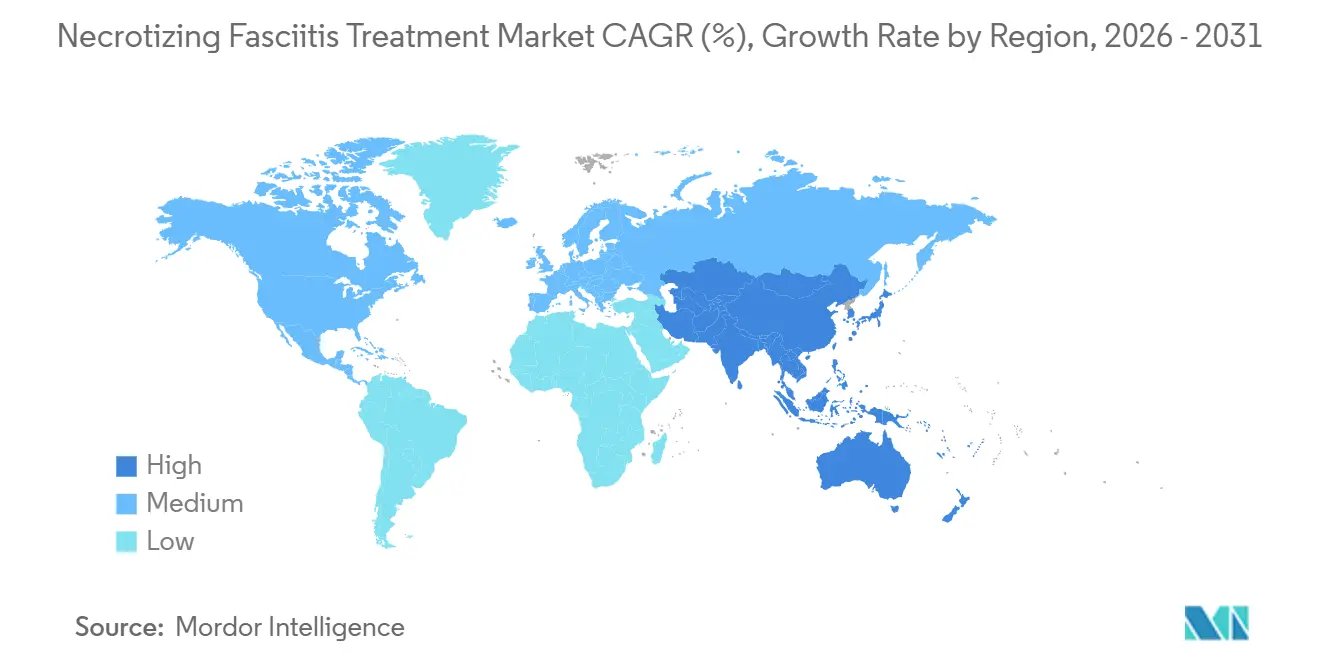

- By geography, North America represented 39.2% of the necrotizing fasciitis treatment market share in 2025, while Asia-Pacific is expected to grow at a 9.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Necrotizing Fasciitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes, Obesity, And Immunocompromised Patient Pool | +2.2% | Global, strongest in North America, South Asia, and East Asia | Long term (≥ 4 years) |

| Faster Emergency Recognition And CT-Supported Triage | +1.3% | North America, Western Europe, high-income APAC | Medium term (2-4 years) |

| Wider Use Of NPWT And Advanced Wound Closure Workflows | +1.5% | Global, with fastest uptake in North America and Europe | Medium term (2-4 years) |

| Stronger Hospital Access To Broad-Spectrum Anti-Infectives | +0.9% | Global, especially emerging markets expanding formularies | Medium term (2-4 years) |

| Rising Gram-Negative NF Burden In Asia And Africa | +0.8% | APAC core, spill-over to sub-Saharan Africa and MEA | Long term (≥ 4 years) |

| Post-Pandemic Invasive Group A Strep Rebound | +0.7% | High-income countries globally, pediatric centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes, Obesity, and Immunocompromised Patient Pool

The necrotizing fasciitis treatment market is most strongly supported by the rising number of patients whose metabolic or immune deficits make NF more likely and more difficult to control. Diabetes remained the leading comorbidity across major published cohorts, appearing in 47% to 62% of cases, and poor glycemic control was linked with deeper tissue involvement, greater need for repeat debridement, and longer ICU stays. This pattern affects revenue because diabetic NF cases usually consume more antibiotics, more wound care, and more critical care resources per admission rather than only adding case volume. Immunosuppressive regimens for autoimmune disease, transplant care, and oncology are also enlarging a second high-risk cohort that sits outside the diabetes pool and still needs aggressive infection surveillance and treatment support. As these comorbidities rise in parallel, hospitals are dealing with a patient mix that is older, sicker, and more expensive to manage, which keeps demand broad across the care pathway.

Faster Emergency Recognition and CT-Supported Triage

The necrotizing fasciitis treatment market also benefits from faster diagnosis because speed to surgery changes both survival and downstream treatment use. A Dutch multicenter study reported that direct CT use identified clinically occult gas in 52% of gas-positive cases and reduced diagnostic ambiguity in 31% of imaged patients, while still stressing that imaging should never delay surgery when suspicion is already high. The 2025 Chinese consensus moved CT into the first-choice emergency screening role and placed point-of-care ultrasound alongside it as a rapid triage tool for tertiary centers. Better recognition means more true NF patients reach operative management inside the critical early window, which increases use of operating room consumables, wound devices, and post-operative care rather than losing those cases before definitive treatment. That change supports higher realized revenue per confirmed case across the necrotizing fasciitis treatment market.

Wider Use of NPWT and Advanced Wound Closure Workflows

The necrotizing fasciitis treatment market is also being lifted by the wider use of negative pressure wound therapy after debridement. A 2025 review on upper-limb NF reported that controlled subatmospheric pressure at negative 125 mmHg after proper surgical clearance was associated with a 30% reduction in healing time versus conventional dressings, and it described the growing relevance of NPWT systems with instillation and dwell time for antibacterial wound-bed management. This matters because NPWT is no longer treated as an optional add-on in many advanced centers and is now part of the routine wound workflow after source control. Smith+Nephew stated that its Advanced Wound Devices segment recorded 20.6% underlying growth in Q4 2024, with the PICO single-use NPWT platform acting as a major commercial driver[1]Smith+Nephew, “Investor Presentation February–April 2025,” Smith+Nephew, smith-nephew.stylelabs.cloud. A randomized trial comparing irrigating and traditional NPWT in necrotizing soft tissue infections is actively enrolling and is expected to report in 2026, which could further strengthen evidence-backed adoption across the necrotizing fasciitis treatment market.

Stronger Hospital Access to Broad-Spectrum Anti-Infectives

The necrotizing fasciitis treatment market is gaining from broader hospital access to anti-infectives because empiric therapy has become more complex and more drug intensive. The SURFAST review from greater Paris noted that more than 50% of NF patients present in septic shock, and that state can expand the volume of distribution for hydrophilic antibiotics by up to 3-fold, which pushes clinicians toward high loading doses, prolonged infusions, and therapeutic monitoring to achieve adequate tissue exposure. That treatment reality is expanding formularies beyond older monotherapy patterns and supporting routine stocking of carbapenems, beta-lactam and beta-lactamase inhibitor combinations, linezolid, vancomycin, and other broader-spectrum options. In resource-limited settings, piperacillin-tazobactam plus levofloxacin is emerging as a lower-cost regimen that can still support adequate empiric coverage where carbapenem access remains constrained. The result is a higher-value antibiotic bundle per hospitalization, which keeps this part of the necrotizing fasciitis treatment market on a strong growth path even when population incidence remains low in absolute terms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ICU, Surgery, And Prolonged-Stay Costs | -1.8% | Global, most acute in uninsured and underinsured populations | Long term (≥ 4 years) |

| Limited Randomized Evidence For IVIG And HBOT | -0.9% | Global, with payer scrutiny highest in North America and Europe | Medium term (2-4 years) |

| Referral Delays Outside Tertiary Surgical Centers | -0.7% | APAC, Sub-Saharan Africa, rural North America, MEA | Long term (≥ 4 years) |

| HBOT Chamber Access And Transfer Logistics | -0.5% | Global except high-income concentrated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ICU, Surgery, and Prolonged-Stay Costs

The necrotizing fasciitis treatment market faces a direct brake from the high cost of hospitalization because NF requires surgery, intensive care, repeated wound management, and long recovery periods. A U.S. National Inpatient Sample analysis found that Fournier gangrene cases carried USD 37,809 higher hospital costs per admission than non-perineal necrotizing soft tissue infections and were associated with a longer average stay by nearly 2 days. In a resource-limited Chinese cohort, median treatment cost reached CNY 70,230 (USD 10,325), alongside a median stay of 30 days. These costs matter because they make late presentation, treatment discontinuity, and lower uptake of multi-session NPWT or adjunctive therapies more likely in financially constrained settings. As the patient mix shifts toward older and more comorbid cases, cost pressure remains a material restraint on the necrotizing fasciitis treatment market.

Limited Randomized Evidence for IVIG and HBOT

The necrotizing fasciitis treatment market also runs into payer resistance because IVIG and HBOT still lack the depth of randomized evidence that usually supports broad reimbursement. A prospective randomized HBOT trial targeting 160 NF patients is enrolling and expects primary results in 2026, but the need for this study already reflects how limited current evidence remains. Existing observational HBOT data are hard to interpret because more stable patients are often the ones selected for transfer and treatment, which can make outcomes appear better than they would in an evenly randomized population. IVIG faces a similar issue because many supportive datasets are retrospective, and clinicians still reserve it mainly for severe GAS toxic shock or closely selected cases. Until stronger trials close that evidence gap, the necrotizing fasciitis treatment market will keep seeing narrower utilization of these adjunctive therapies than the biology alone might suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Polymicrobial Prevalence Anchors the Market, Strep Rebound Accelerates Type II

Type I polymicrobial NF held 76.3% of the necrotizing fasciitis treatment market size in 2025. That position reflects the fact that Type I disease accounts for 70% to 90% of confirmed cases in most published cohorts and usually requires multi-agent empiric antibiotics, serial debridements every 12 to 24 hours, and prolonged ICU management[2]Silvia Tedesco, “Necrotizing Soft Tissue Infections, A Surgical Narrative Review,” Updates in Surgery, doi.org. In the necrotizing fasciitis treatment industry, this segment generates demand across nearly every treatment layer because a typical polymicrobial admission uses surgery, antibiotics, wound devices, dressings, and later reconstruction support. Type III and Type IV disease remain much smaller by revenue because Gram-negative marine infections and fungal NF are still concentrated in narrower clinical settings.

Type II NF is projected to expand at a 9.4% CAGR from 2026 to 2031, making it the fastest-growing disease subtype. The rise is linked with the post-pandemic increase in invasive GAS infections and the spread of M1UK-linked virulence, which has kept toxin-suppression therapy and critical care clinically important. This part of the necrotizing fasciitis treatment market is still smaller in absolute value than Type I, but its growth rate shows that procurement is starting to reflect toxin-driven disease patterns more clearly. In the necrotizing fasciitis treatment industry, that trend favors clindamycin, IVIG in selected toxic shock cases, and ICU-level supportive care rather than simple volume growth alone.

By Treatment Modality: Surgery Anchors Revenue While Antibiotic Complexity Drives Growth

Surgical intervention represented 22.2% of the necrotizing fasciitis treatment market size in 2025, making it the largest treatment modality. Surgery remains the core of care because published reviews continue to show that very early operative intervention changes survival, with one 2025 surgical review reporting a mortality odds ratio of 0.43 when surgery occurred within 6 hours of admission versus later intervention. In practical terms, each patient often needs 3 to 4 operations, followed by skin grafting, flap coverage, or even amputation in some extremity cases, which keeps the surgical cost base high. That clinical structure ensures surgery remains the revenue anchor of the necrotizing fasciitis treatment market even as other modalities grow.

Antibiotic therapy is forecast to rise at a 9.5% CAGR from 2026 to 2031, which makes it the fastest-growing modality. This growth is tied less to case volume and more to regimen intensity because hospitals now use structured combinations such as carbapenem or piperacillin-tazobactam, plus vancomycin or another resistant Gram-positive agent, plus clindamycin for toxin suppression. The 2025 Chinese national consensus also formalized parallel empiric backbones built around meropenem, imipenem-cilastatin, piperacillin-tazobactam, or ceftriaxone, each paired with vancomycin and clindamycin. That treatment complexity pushes drug spend per admission upward and gives this part of the necrotizing fasciitis treatment market a clear growth edge over more mature modalities.

By End User: Hospitals Dominate, ASCs Gain Ground Through Post-Stabilization Migration

Hospitals held 48.5% of revenue in 2025 and remained the leading end-user channel in the necrotizing fasciitis treatment market. That share follows the biology of the disease because patients need immediate resuscitation, ICU beds, emergency operating access, CT imaging, microbiology support, and pathology review during the first phase of care. Tertiary and teaching hospitals take a disproportionate share of complex NF volume because they can move faster from diagnosis to surgery and can continue serial debridement without referral delays. Specialty wound centers and clinics still matter because they absorb dressing changes, graft surveillance, and NPWT follow-up that would otherwise extend inpatient length of stay.

Ambulatory surgical centers are forecast to grow at a 9.3% CAGR from 2026 to 2031. The shift does not reflect a move away from hospitals for acute NF treatment, but it does show that wound revision, graft procedures, flap modification, and device changes are gradually moving into lower-acuity settings once sepsis is controlled. Single-use NPWT devices make that transition more practical because they support outpatient wound management after stabilization. As survival improves and more patients proceed to staged reconstruction, this channel should keep taking a larger role within the necrotizing fasciitis treatment market.

Geography Analysis

North America accounted for 39.2% of the necrotizing fasciitis treatment market size in 2025. The region leads because it combines relatively high NF incidence, strong reimbursement for complex surgical care, and broad use of advanced wound management and adjunctive therapies. The United States sets the tone for the necrotizing fasciitis treatment market in this region because guideline-backed diagnosis, high ICU utilization, and broad hospital formulary access support higher treatment intensity per case[3]“Clinical Guidance for Type II Necrotizing Fasciitis,” Centers for Disease Control and Prevention, cdc.gov. Canada contributes steady procurement through a hospital-centered care model, while Mexico adds growth exposure through rising diabetes and obesity-linked risk. Regional performance is still held back by uneven access outside advanced centers, especially when patients first present to smaller hospitals and lose time before definitive surgery.

Europe remained the second-largest geography in the necrotizing fasciitis treatment market. Germany, the United Kingdom, France, Italy, and Spain anchor regional demand because they combine high tertiary-care capability with stronger referral systems and organized specialty networks. French SURFAST work on antibiotic pharmacokinetics in septic-shock NF is influencing dosing and infusion practices across the region, which supports more structured anti-infective procurement in hospital settings. Scandinavia also stands out because multicenter observational work on HBOT came from hospitals operating within a coordinated referral structure, which helps Europe maintain a clinically advanced profile in the necrotizing fasciitis treatment market.

Asia-Pacific is expected to grow at a 9.8% CAGR from 2026 to 2031 and is the fastest-growing regional block in the necrotizing fasciitis treatment market. China is central to that rise because the 2025 national consensus standardized empiric antibiotics, CT-based triage, and NPWT application criteria across tertiary hospitals, which creates a much clearer procurement framework. The Guangxi cohort also showed a structurally Gram-negative case mix, led by E. coli and Klebsiella pneumoniae, which supports stronger demand for carbapenems and piperacillin-tazobactam than in many Western settings. India remains important because hospital-level practice still leans on piperacillin-tazobactam plus clindamycin as a practical empiric backbone, while Japan continues to support specialized diagnostic and surgical pathways through updated clinical guidance. South America, the Middle East, and Africa are smaller in value, but the necrotizing fasciitis treatment market in those regions is still expanding as diabetes, HIV co-infection, and tertiary hospital development change the case mix and treatment pathway.

Competitive Landscape

The necrotizing fasciitis treatment market is moderately fragmented because no company controls the full care pathway from diagnosis through surgery, antibiotics, wound closure, and immune support. Competition is instead organized by product specialization, with antibiotic suppliers, IVIG producers, and wound management companies each holding influence over separate pieces of treatment demand. In antibiotics, companies such as Pfizer, Merck & Co., Astellas Pharma, GSK, Hikma, and Teva compete mainly on hospital formulary placement, supply continuity, and pricing discipline rather than on disease-specific branding. In NPWT and advanced wound care, Solventum, Smith+Nephew, Mölnlycke, and Convatec are more differentiated because device evidence, contract positioning, and ease of outpatient use can shift account-level preference. This structure keeps the necrotizing fasciitis treatment market active but dispersed, and it limits the chance that one supplier can set the pace across all modalities.

Smith+Nephew offers one of the clearest recent strategic examples in the necrotizing fasciitis treatment market because it reported 20.6% underlying growth in Advanced Wound Devices in Q4 2024 and identified NPWT expansion as a 2025 priority, supported by the PICO single-use platform. That matters because portable NPWT directly supports the shift of wound care and device management into ambulatory and post-acute settings. CSL Behring, Grifols, Octapharma, and Takeda remain relevant in IVIG, but this remains a narrower segment because utilization still depends on severe GAS toxic shock presentations and cautious payer coverage. The competitive balance therefore still favors companies that can align with hospital protocols rather than firms waiting for a large standalone adjunctive therapy opportunity.

Pipeline white space is the main strategic opening in the necrotizing fasciitis treatment market because no therapy is currently approved specifically for NF and most treatment still relies on off-label use within surgical-first protocols. That absence leaves room for companies pursuing better debridement tools, new anti-infectives, or stronger evidence packages around adjunctive care. It also means that a company able to secure a true NF-specific label would likely gain outsized formulary visibility and market access compared with current suppliers that depend on broader anti-infective or wound-care portfolios. Until that happens, the necrotizing fasciitis treatment market should remain a multi-supplier arena where value is created through niche leadership rather than through end-to-end platform control.

Necrotizing Fasciitis Treatment Industry Leaders

Pfizer Inc.

Merck & Co., Inc.

GSK plc

CSL Behring

Grifols, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: EurekAlert shared insights from a December 2025 article published in Impact Journals LLC, discussing Necrotizing fasciitis (NF) of the head and neck. Although rare, this infection progresses rapidly and can be life-threatening, making it a critical surgical emergency.

- January 2025: Recce Pharmaceuticals completed dosing all 30 patients in its Phase II ABSSSI trial for RECCE 327 Topical Gel. The trial showed a 93% primary efficacy rate with no serious adverse events reported. The company is preparing for a Phase III registrational trial in Australia in the first half of 2025, along with a separate Phase III study for diabetic foot infections in Indonesia. These efforts aim to position R327G for future FDA and TGA submissions, including coverage for NF.

Global Necrotizing Fasciitis Treatment Market Report Scope

As per the scope of the report, necrotizing fasciitis is a severe bacterial infection that rapidly destroys the fascia, the connective tissue surrounding muscles, blood vessels, and nerves. It is often referred to as "flesh-eating disease" because of the extensive tissue damage it causes. The condition requires prompt medical treatment, including antibiotics and often surgical removal of dead tissue, to prevent widespread tissue death and systemic complications.

The necrotizing fasciitis treatment market is segmented by disease type into type I, type II, type III, and type IV. By treatment modality, the market is categorized into antibiotic therapy, surgical intervention, adjunctive therapies, and supportive critical care. Based on end user, the market is divided into hospitals, specialty clinics and wound care centers, ambulatory surgical centers, and home and rehabilitation settings. Geographically, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Type I |

| Type II |

| Type III |

| Type IV |

| Antibiotic Therapy |

| Surgical Intervention |

| Adjunctive Therapies |

| Supportive Critical Care |

| Hospitals |

| Specialty Clinics and Wound Care Centers |

| Ambulatory Surgical Centers |

| Home and Rehabilitation Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Type I | |

| Type II | ||

| Type III | ||

| Type IV | ||

| By Treatment Modality | Antibiotic Therapy | |

| Surgical Intervention | ||

| Adjunctive Therapies | ||

| Supportive Critical Care | ||

| By End User | Hospitals | |

| Specialty Clinics and Wound Care Centers | ||

| Ambulatory Surgical Centers | ||

| Home and Rehabilitation Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected growth outlook for the necrotizing fasciitis treatment market through 2031?

The necrotizing fasciitis treatment market is expected to move from USD 1.46 billion in 2026 to USD 2.19 billion by 2031 at a CAGR of 8.45%.

Which disease subtype generates the most revenue in necrotizing fasciitis care?

Type I polymicrobial NF led with 76.3% of revenue in 2025 because it is the most common presentation and usually needs multi-drug therapy, repeated surgery, and longer ICU care.

Why is antibiotic therapy growing faster than other treatment modalities?

Antibiotic therapy is projected to grow at a 9.5% CAGR because hospitals are using more complex empiric combinations to cover polymicrobial disease, resistant organisms, and toxin-producing pathogens.

Why do hospitals remain the main end-user setting for necrotizing fasciitis treatment?

Hospitals held 48.5% of revenue in 2025 because patients need emergency surgery, ICU support, imaging, microbiology, and serial debridement during the acute phase.

Which region is growing fastest in necrotizing fasciitis treatment?

Asia-Pacific is expanding at a 9.8% CAGR to 2031, supported by tertiary hospital expansion, standardized treatment protocols in China, and a rising Gram-negative case burden.

What is limiting wider use of adjunctive therapies such as IVIG and HBOT?

Broader uptake is restrained by limited randomized evidence, payer scrutiny, transport challenges, and the concentration of HBOT capacity in selected high-income centers.

Page last updated on: