Natural Food Colorants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

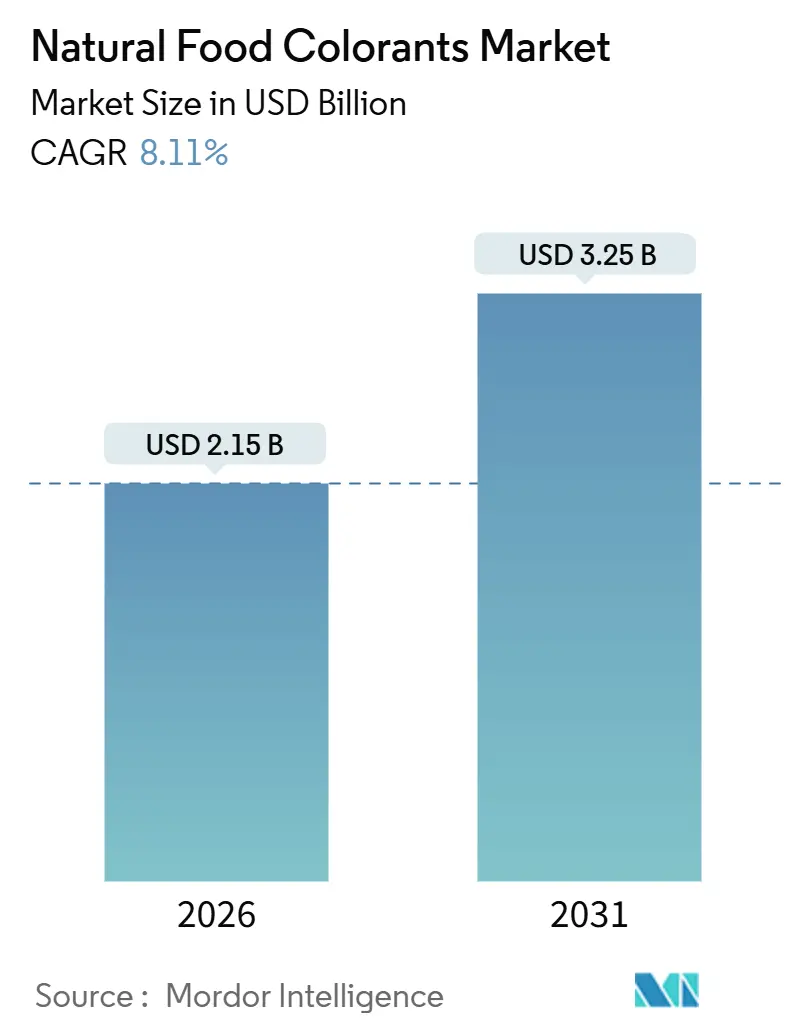

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 3.25 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

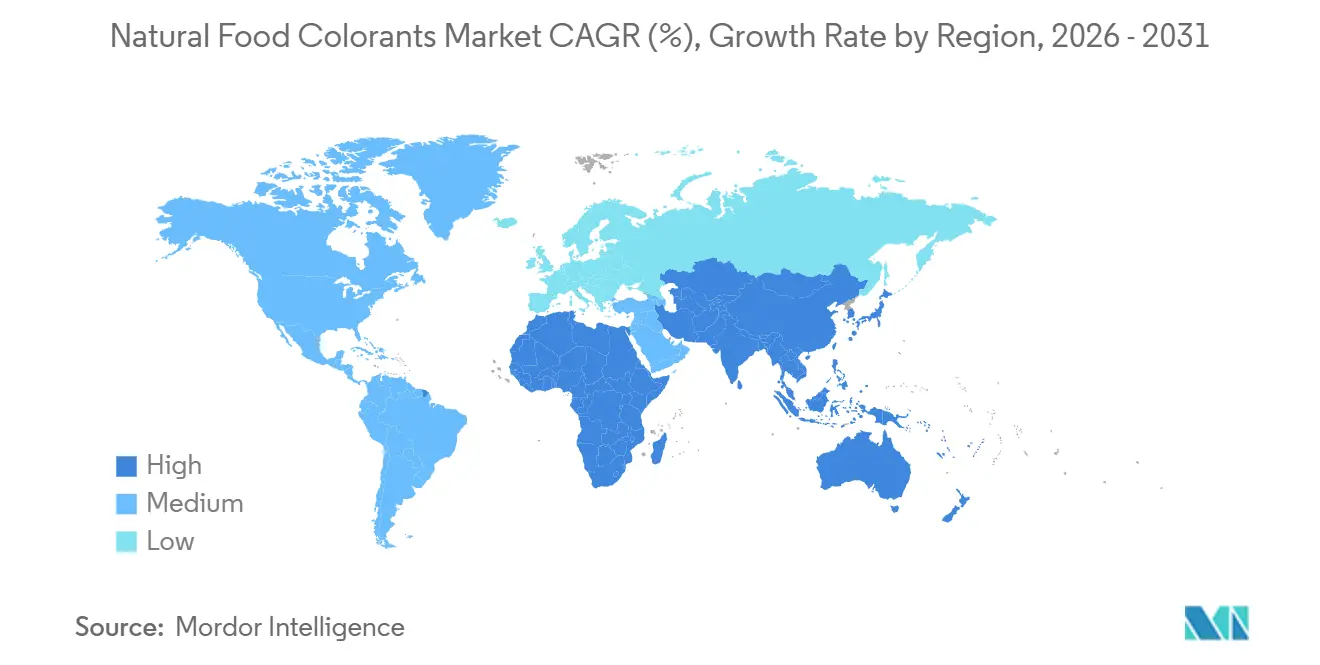

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

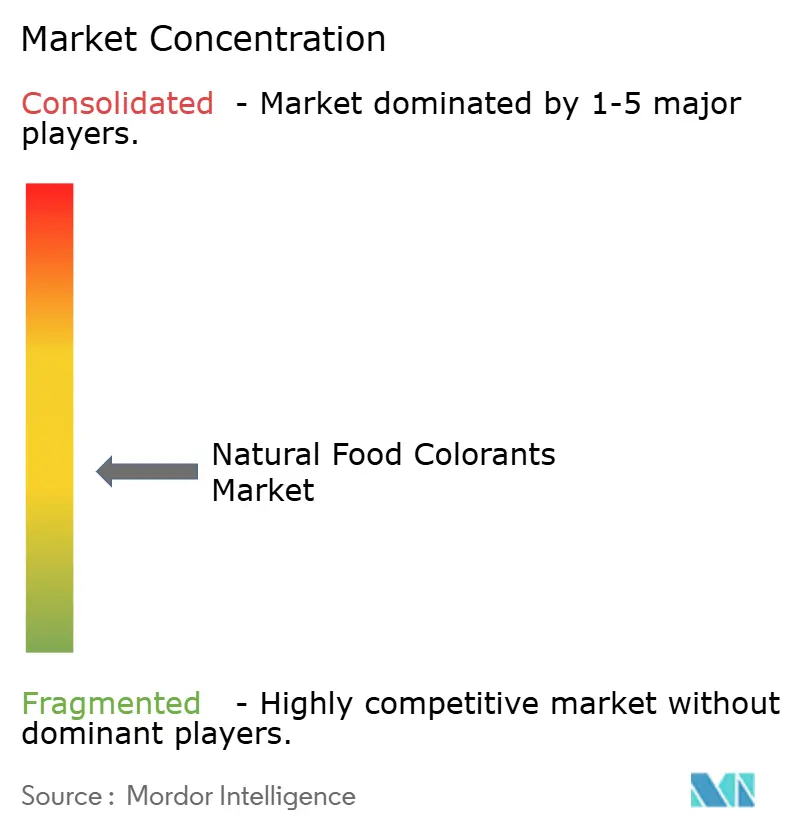

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Natural Food Colorants Market Analysis by Mordor Intelligence

The natural food colorants market reached a market size of USD 2.15 billion in 2026 and is projected to advance to USD 3.25 billion by 2031, translating into an 8.11% CAGR across the forecast horizon. Momentum stems from a tight interplay of stricter regulations, consumer hostility toward synthetic azo dyes, and extraction and fermentation breakthroughs that protect margins even as raw-material volatility persists. Europe set the regulatory tone early, Asia-Pacific now posts the fastest uptake, and North America rides fresh U.S. Food and Drug Administration approvals that unlocked long-sought natural blue solutions. Market participants defend share through mergers, fermentation scale-ups, and technology that stabilizes pigments in heat- and pH-stressed foods. Retailer scorecards that penalize artificial colors, especially in beverages, have become near-mandatory gates to shelf space. Precision biology simultaneously compresses production cycles and eliminates weather-linked variability, elevating entry barriers for commodity extractors and widening the gap between innovation leaders and smaller regional processors.

Key Report Takeaways

- By product type, carotenoids led with 45.12% revenue share in 2025; anthocyanins are projected to expand at a 9.15% CAGR through 2031.

- By color, red pigments captured 31.28% share of the natural food colorants market size in 2025, while blue hues are moving ahead at a 10.02% CAGR to 2031.

- By form, powder formats dominated with 58.25% share in 2025; liquid concentrates are forecast to post a 9.58% CAGR through 2031.

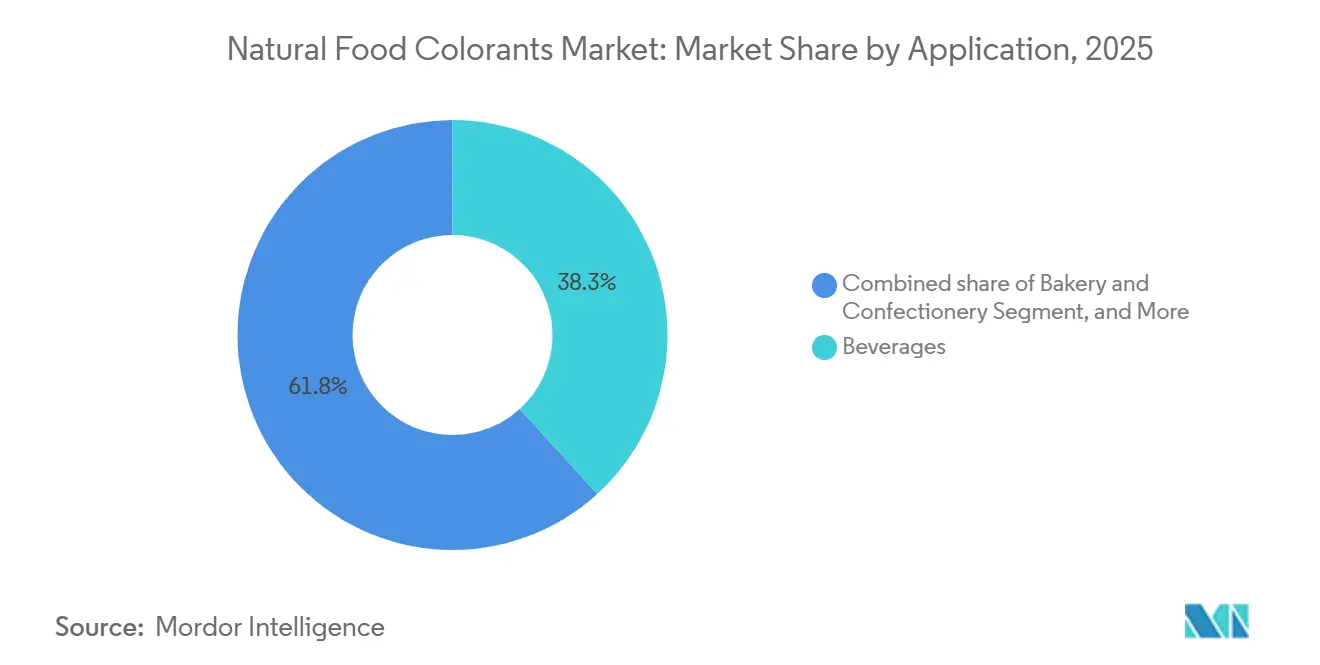

- By application, beverages accounted for 38.25% of the natural food colorants market size in 2025, and dietary supplements are rising at a 10.58% CAGR over 2026-2031.

- By geography, Europe held 35.46% natural food colorants market share in 2025, whereas the Asia-Pacific is on track for a 9.78% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Natural Food Colorants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Preference for Clean-Label and Natural Ingredients Over Synthetic Dyes | +2.1% | Global, with early gains in Western Europe, North America, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising Demand in Beverages, Bakery, and Confectionery for Plant-Based Pigments | +1.8% | Global, strongest in North America and Europe for beverages; Asia-Pacific for bakery | Short term (≤ 2 years) |

| Health Benefits from Antioxidants in Carotenoids and Phycocyanin Sources | +1.3% | Global, with premium positioning in North America and Western Europe dietary supplements | Medium term (2-4 years) |

| Technological Advancements in Natural Color Extraction Driving the Market | +1.2% | Global, concentrated in research and development hubs in Netherlands, Denmark, United States | Long term (≥ 4 years) |

| Regulatory Approvals from Government Organizations | +1.0% | North America (FDA), Europe (EFSA), Asia-Pacific (FSSAI, CFDA) | Short term (≤ 2 years) |

| Microbial and Oil-Soluble Innovations for Scalable, Cost-Effective Production | +0.7% | Global, early commercial adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for Clean-Label and Natural Ingredients Over Synthetic Dyes

A 2025 survey by the International Food Information Council reveals that 83% of global consumers consider ingredient transparency important when purchasing packaged foods[1]Source: International Food Information Council, “2025 Food & Health Survey,” foodinsight.org. Additionally, 86% of consumers can now differentiate between natural and synthetic colors. This growing awareness is largely attributed to advocacy campaigns that associated certain azo dyes, such as Tartrazine and Allura Red, with hyperactivity in children. In response, the European Union introduced a 2010 mandate requiring warning labels on products containing six specific synthetic colorants, driving voluntary reformulations and emphasizing the importance of European Commission Regulation 1333/2008. Major retailers have responded to this shift: In 2024, Tesco and Carrefour eliminated artificial color products from their private-label lines, while Walmart's "Great For You" label excluded synthetic dyes. This has created a two-tiered shelf system, where products with natural colors command a 20 to 30% price premium but maintain similar sales velocity. As production methods like microbial fermentation and supercritical CO₂ extraction reduce natural color costs by 15% annually, the willingness-to-pay gap is narrowing. This trend enables brands to adopt clean-label positioning without relying solely on premium pricing. On the regulatory side, companies must comply with the FDA's Color Additive Petitions and the EFSA's re-evaluation protocols. While these processes require detailed toxicological dossiers, achieving approval offers a significant competitive edge.

Rising Demand in Beverages, Bakery, and Confectionery for Plant-Based Pigments

In 2025, beverage applications represented 38.25% of the natural-color volume. This growth was primarily driven by leading carbonated soft-drink companies reformulating their products to meet retailer scorecards that penalize synthetic additives. PepsiCo, for example, removed artificial colors from Gatorade in 2024, replacing them with beta-carotene and fruit-and-vegetable concentrates. This reformulation extended across PepsiCo's global portfolio and was mirrored by Coca-Cola's reformulation of Fanta in European markets, as detailed in PepsiCo's 2024 Annual Report. The bakery and confectionery sectors face specific challenges. Anthocyanins derived from red cabbage and elderberry degrade in alkaline pH environments, such as cake batters. To address this, manufacturers encapsulate these colorants in maltodextrin matrices or co-formulate them with citric acid buffers, ensuring color stability during baking at temperatures exceeding 180 °C. Confectionery leader Mars transitioned M&M's to spirulina-derived blue and turmeric yellow in select markets. While this change resulted in a 10 percent cost increase, it aligned with clean-label mandates and eliminated the use of synthetic Brilliant Blue FCF. This shift also created export opportunities, as regulators in the Middle East and Southeast Asia increasingly adopt EU standards. According to the GCC Standardization Organization, products with natural colors face fewer import restrictions compared to those using synthetic dyes. Compliance with standards such as ISO 22000 food-safety certification and Halal/Kosher endorsements is essential, and natural plant-based pigments are better positioned to meet these requirements than insect-derived carmine.

Health Benefits from Antioxidants in Carotenoids and Phycocyanin Sources

Fortified beverages and gummies now provide 10 to 20 milligrams of lutein and zeaxanthin, xanthophyll carotenoids derived from marigold petals. These dosages are clinically associated with improving macular pigment optical density and protecting against blue light exposure for digital device users. Astaxanthin, sourced from Haematococcus pluvialis microalgae, exhibits singlet-oxygen quenching capabilities that are 550 times more potent than vitamin E. This makes astaxanthin a valuable ingredient in sports-nutrition bars, offering both coral-pink coloration and oxidative-stress reduction. Phycocyanin, obtained from Arthrospira platensis (commonly known as spirulina), demonstrates in vitro COX-2 inhibition. This supports joint-health claims in dietary supplements while also providing a turquoise hue to protein powders and functional shots. The combination of color and bioactivity allows brands to optimize their ingredient lists. For example, they can replace synthetic Blue 1 and a separate antioxidant with a single spirulina extract. This approach simplifies product labels and reduces formulation costs by 12 percent per SKU. Regulatory authorities play a significant role, with the FDA granting Generally Recognized as Safe (GRAS) status to specific carotenoid sources. Additionally, the EFSA establishes acceptable daily intake (ADI) guidelines, which natural extracts typically meet at functional dosages[2]Source: U.S. Food and Drug Administration. "Color Additives." fda.gov..

Technological Advancements in Natural Color Extraction Driving the Market

Pulsed electric field (PEF) technology uses short bursts of high voltage to rupture plant-cell membranes. This technique increases anthocyanin yields from blackcurrants by 40% compared to conventional solvent maceration and reduces processing time from 8 hours to just 45 minutes. Supercritical CO₂ extraction, conducted at 31°C and 74 bar, selectively extracts lipophilic carotenoids from paprika and annatto. This method prevents thermal degradation and hexane residues, ensuring compliance with organic certification standards and achieving a 25% price premium in European markets. Natural deep eutectic solvents (NADES), composed of choline chloride and organic acids, dissolve polyphenolic pigments at ambient temperature. This eliminates the need for energy-intensive heating and aligns with green-chemistry principles, appealing to procurement teams focused on sustainability. Microencapsulation using alginate or gum-arabic shells protects anthocyanins from pH and light exposure. This extends the shelf life of beverages in clear-PET bottles from 3 to 12 months, enabling ambient distribution in tropical regions with limited cold-chain infrastructure. Compliance requirements include adherence to EU Regulation 1333/2008 on food additives, which restricts processing aids, and ISO 9001 quality-management certification, a standard for Tier-1 suppliers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Processing Cost and Low Yield of Natural Food Colorants | -1.4% | Global, most acute in price-sensitive markets in South Asia, Africa, and Latin America | Short term (≤ 2 years) |

| Supply chain variability from seasonal plant and algal sources | -0.9% | Global, concentrated in regions dependent on single-origin crops (Peru for annatto, India for turmeric) | Medium term (2-4 years) |

| Color instability in high-heat or acidic food applications | -0.6% | Global, particularly impacting bakery and acidic beverage segments | Medium term (2-4 years) |

| Stringent Regulatory Compliance Requirements | -0.4% | North America (FDA), Europe (EFSA), Asia-Pacific (FSSAI, CFDA) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Processing Cost and Low Yield of Natural Food Colorants

The global natural food colorants market faces significant economic challenges, despite advancements in technology. Processing costs and yield limitations create price premiums that restrict market penetration worldwide. Natural colorants command higher prices than synthetic alternatives, which presents formulation challenges, particularly in mass-market products with strict margin requirements across different regions. Multiple factors contribute to this cost differential, including raw material inconsistency, complex extraction processes, lower pigment concentrations in natural sources, and varying regional production capabilities. These economic constraints have prompted innovation in biotechnology solutions globally. Companies such as Phytolon are developing fermentation-based production methods to potentially reduce natural colorant costs. The Food and Drug Administration (FDA) has received color additive petitions from Phytolon for beetroot red and prickly pear yellow, signaling advancement in commercializing these innovative approaches. Although processing costs remain a significant market restraint worldwide, increasing regulatory pressure to eliminate synthetic dyes is creating market conditions where the price premium for natural alternatives becomes more acceptable. The high production costs continue to hamper market growth, particularly in price-sensitive developing markets where manufacturers struggle to maintain competitive pricing.

Supply Chain Variability from Seasonal Plant and Algal Sources

In Andhra Pradesh and Tamil Nadu, India's primary turmeric cultivation zones, curcumin content ranges from 2.5% to 6.5%, depending on monsoon rainfall and soil sulfur levels. This variability forces buyers to over-contract by 30% to ensure sufficient pigment supply, driving up inventory-carrying costs. Carmine, extracted from cochineal insects (Dactylopius coccus) raised on Peruvian Opuntia cacti, is affected by biennial pest cycles and climate-related cactus die-offs. These issues caused a 40% supply shortfall in 2024, with spot prices escalating from USD 80 to USD 135 per kilogram within eight weeks. Spirulina, grown in open raceways, is susceptible to contamination by Anabaena and Microcystis cyanobacteria, which produce hepatotoxic microcystins. A single contamination event can destroy an entire 10-hectare pond, delaying deliveries by 90 days. Annatto seed (Bixa orellana) harvests in Peru and Kenya occur annually, requiring processors to finance 12 months of working capital to maintain a consistent supply. This ties up USD 2 million to USD 5 million per facility and increases financing costs by 180 basis points compared to synthetic-dye distributors using just-in-time inventory. Compliance requirements, including traceability under EU Regulation 178/2002 and FSMA Preventive Controls, mandate supplier audits and lot-level documentation, adding USD 12,000 to USD 20,000 in annual administrative expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirulina Challenges Carotenoid Dominance

In 2025, carotenoids accounted for 45.12% of the revenue, emphasizing their significant role in dairy, bakery, and beverage sectors. As fermentation secures a growing 22% share of the market, the natural food colorants market for carotenoids is expected to grow steadily, reducing the cost gap with synthetic alternatives. Anthocyanins, driven by vegan candy lines that have effectively replaced carmine while maintaining signature reds and purples, are the fastest-growing product group, with a 9.15% CAGR.

Beta-carotene produced via precision fermentation has already reached cost parity with synthetic options, signaling a turning point that could impact other carotenoids. Despite challenges with pH and heat, curcumin continues to maintain its niche in curry sauces and dietary supplements. While carmine's use in food is declining, its demand in cosmetics provides partial support. However, as berry-derived reds gain momentum, carmine's share in the natural food colorants market is expected to decrease. Spirulina, the leader in the blue colorant segment, now faces competition from emerging players like butterfly pea and Galdieria. Nevertheless, spirulina's established sensory profile and scale advantages provide incumbents with an opportunity to optimize cost efficiencies.

By Color: Red Dominance Continues, Blue Emerges as Eye-Catching Star

In 2025, red accounted for a 31.28% share of the market, a position the natural food colorants market is unlikely to lose soon due to red's extensive application in fruits, desserts, and sauces. However, the blue subsegment, growing at a 10.02% CAGR, is attracting considerable attention from beverage, ice-cream, and sports-nutrition brands aiming to create visually appealing content for social media. The FDA's 2025 approval of butterfly pea extract, along with EFSA's authorization of Galdieria blue, has expanded the options available to formulators, encouraging spirulina to improve its flavor-masking technologies.

Yellows (such as curcumin and beta-carotene) and oranges (including annatto and paprika) remain essential, while greens often rely on pigment combinations, which restricts their growth. Meanwhile, purple and pink shades are gaining traction in premium segments like yogurts and frozen desserts, aligning with the consumer interest in “unicorn” color palettes. Although red will maintain its dominance in absolute revenue, the blue segment is expected to surpass other colors in terms of relative growth.

By Form: Powder Dominance Persists, Yet Liquid Concentrates Gain popularity

In 2025, powder formats accounted for 58.25% of the segment's revenue, valued for their shelf stability, precise dosing in bakery mixes, and compatibility with dry-blending equipment commonly used in snack and cereal production. Spray-drying and freeze-drying technologies encapsulate natural pigments within maltodextrin or gum-arabic matrices, providing a shelf life of 24 months under ambient conditions. This advancement not only extends product longevity but also reduces cold-chain logistics costs by 35% compared to liquid concentrates, as reported in the Journal of Food Engineering. Liquid concentrates, comprising aqueous and oil-based dispersions, are projected to grow at a 9.58% CAGR through 2031. This growth is driven by beverage co-packers increasingly adopting inline injection systems, which reduce batch-to-batch color variation to below 1 Delta E and eliminate dust exposure risks for production workers.

Additionally, liquid formats support micro-dosing in functional shots and ready-to-drink teas. In these cases, powders would require high-shear mixing for dissolution, increasing processing time by 8 to 12 minutes per batch. Emulsion technologies stabilize lipophilic carotenoids in aqueous beverages by achieving droplet sizes below 200 nanometers, preventing creaming and enhancing color intensity threefold. This innovation enables formulators to reduce dosage rates by 64%, significantly lowering raw-material costs. However, powder formats face limitations in acidic beverage applications, where anthocyanin powders exhibit 20% lower color intensity than liquid concentrates due to incomplete rehydration and particle agglomeration. Regulatory compliance remains critical, with the FDA's good manufacturing practices for color additives mandating particle-size specifications and microbial limits. Similarly, the EU's Regulation 1333/2008 imposes restrictions on processing aids in liquid formulations.

By Application: Nutraceuticals Drive Future Growth

In 2025, beverages represented 38.25% of application revenue, driven by carbonated soft drinks, sports drinks, and ready-to-drink teas reformulated to meet retailer clean-label scorecards penalizing synthetic additives. Non-alcoholic beverages dominated with 82% of the beverage-application volume, while alcoholic segments, such as craft beer, flavored malt beverages, and ready-to-drink cocktails, embraced natural colors to align with premiumization and health-conscious trends. Dietary supplements experienced the fastest application growth, with a 10.58% CAGR projected through 2031. This growth is supported by products like lutein and zeaxanthin softgels for eye health, astaxanthin capsules for sports recovery, and spirulina tablets marketed for immune support. The dietary supplement segment benefits from the dual functionality of natural colors, which enhance visual appeal and deliver bioactive compounds that support label claims. This functionality enables brands to simplify ingredient lists and streamline regulatory filings. Bakery and confectionery applications face formulation challenges. For example, anthocyanins degrade in alkaline pH cake batters, requiring encapsulation or co-formulation with acidulants, while curcumin loses 60% of its intensity during retort sterilization.

Dairy products, including yogurt, ice cream, and cheese, utilize annatto, beta-carotene, and carmine. Oil-soluble formats are preferred in high-fat matrices to prevent halo effects. Snacks and cereals use turmeric, paprika, and beetroot powders to create trendy "rainbow" varieties targeting young consumers. However, to prevent color migration between adjacent pieces, barrier coatings are applied, adding an extra cost of USD 0.02 per unit. Regulatory bodies significantly influence the market, with the FDA issuing GRAS notices for specific applications and the EFSA imposing use-level restrictions, such as capping curcumin at a daily intake of 0.1 milligrams per kilogram of body weight.

Geography Analysis

In 2025, Europe accounted for 35.46% of global revenue, driven by strict clean-label regulations and the early elimination of synthetic azo dyes. The European Commission's 2010 directive, which required warning labels on six synthetic colorants, prompted voluntary reformulations. By 2024, major retailers such as Tesco and Carrefour had removed artificial-color products from their private-label lines, adhering to European Commission Regulation 1333/2008. In January 2025, EFSA approved Galdieria sulphuraria-derived phycocyanin, enabling the production of blue plant-based yogurts and ice creams. These products, which previously relied on spirulina with seaweed off-notes, triggered reformulation projects across 22 European dairy brands within six months, as noted in the EFSA Journal 2025. Spain and the Netherlands, home to GNT Group's Exberry facility in Mierlo and Roha Dyechem's Catalonia plant, serve as key natural-color production hubs, benefiting from proximity to end-users and access to raw materials from North Africa and South America. Poland and Belgium are emerging as growth markets, with their confectionery and bakery sectors adopting natural colors to meet EU export standards and achieve premium positioning in Western European markets.

Asia-Pacific leads with a strong 9.78% CAGR through 2031, fueled by urbanization, rising incomes, and increased packaged-food consumption in China, India, and Southeast Asia, as per World Bank Development Indicators. In 2024, China's National Health Commission expanded its list of approved natural colors, aligning with Codex Alimentarius standards and enhancing export competitiveness for local food processors. India's FSSAI, in 2024, approved red cabbage extract and safflower yellow, enabling manufacturers to reformulate traditional sweets (mithai) and beverages (lassi, flavored milk) with natural colors, targeting premium urban markets, as highlighted in the FSSAI Notification[3]Source: Food and Safety Standards Authority of India, "Natural Food Colorants Notification 2024." fssai.gov.in.. Japan and South Korea are experiencing high adoption of natural colors, particularly in confectionery and dairy, driven by health-conscious consumers and regulations that favor plant-based additives. Japan's Ministry of Health, Labor and Welfare maintains a more extensive positive list of 158 natural colors compared to its synthetic-dye approvals. Australia's food sector is following Europe's clean-label trend, with major retailers Woolworths and Coles prioritizing natural colors in their private labels, prompting supplier reformulations. In Indonesia, Thailand, and Singapore, the ready-to-drink beverage and snack sectors are growing rapidly, with natural colors aligning with Halal certification and Islamic dietary laws, accounting for 68% of the regional beverage volume, as per the GCC Standardization Organization.

North America represented 28% of global revenue in 2025, with the U.S. contributing 74% of that volume. This growth was driven by the FDA's May 2025 approvals of butterfly pea flower and Galdieria blue, along with clean-label initiatives from retailers like Walmart, which introduced the "Great For You" icon to identify products free from synthetic dyes. Canada's food sector closely aligns with U.S. regulations, and Health Canada's 2024 discussions on synthetic-dye restrictions suggest potential phase-outs, mirroring European trends. Chile, Colombia, and Peru are leveraging local raw materials, such as Peru's annatto and Colombia's turmeric to supply both regional and export markets, though seasonal supply variability remains a challenge. In the Middle East and Africa, demand for Halal-certified foods in Saudi Arabia, the UAE, and Egypt is driving the market. Here, natural plant-based colors are more compliant with Islamic dietary laws than insect-derived alternatives like carmine. South Africa and Nigeria are emerging as key production hubs for spirulina and annatto, focusing on intra-African trade and European export opportunities.

Competitive Landscape

The natural food colorants market is moderately concentrated, with regional and global players dominating the market. Leading companies such as Sensient Technologies, GNT Group B.V., Givaudan S.A., Döhler Group SE, and DIC Corporation play a significant role in shaping the natural food colorants market. These companies capitalize on their extensive product portfolios, advanced technical expertise, and well-established global distribution networks to maintain their market dominance. Their substantial investments in research and development further strengthen their competitive positioning and drive innovation in the industry.

These key players are actively expanding their product offerings by focusing on sustainable sourcing practices, clean-label product innovations, and strategic mergers and acquisitions. For instance, Givaudan's acquisition of Naturex has significantly enhanced its capabilities in botanical and natural color solutions, enabling it to cater to the growing demand for natural ingredients. Similarly, Sensient is heavily investing in research and development to create natural pigments with improved heat and light stability, specifically designed for applications in the dairy and beverage industries, addressing critical industry needs.

In addition to the efforts of major players, regional companies are increasingly expanding their footprint, particularly in emerging markets, by forming strategic partnerships. The market is also experiencing a notable rise in biotechnology firms that employ advanced techniques such as fermentation and precision breeding to develop natural colorants with superior stability and cost-effectiveness. Furthermore, many companies are adopting vertical integration strategies to secure a consistent supply of raw materials and ensure stringent quality control throughout the production process, thereby enhancing their operational efficiency and product reliability.

Natural Food Colorants Industry Leaders

-

Sensient Technologies Corporation

-

Doehler Group SE

-

Givaudan S.A.

-

GNT Group B.V.

-

DIC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Oterra has opened a new color blending and application center in Kerala, India, to support customers in the Indian, Asia-Pacific, and Middle East markets. The facility focuses on natural colors for food and beverage applications.

- December 2024: Kalsec Inc. expanded its partnership with Connell Caldic, a distributor of ingredients. The agreement utilizes Caldic's operations, sales, and marketing teams in China to expand Kalsec's presence in the Asia-Pacific market.

- July 2024: Givaudan Sense Colour launched Amaize orange-red at IFT 2024. This addition to the Amaize line of corn-based anthocyanin colors offers a bright orange-red shade that matches Red 40 in acidic applications.

- May 2024: Brenntag expanded its distribution agreement with Oterra to include Sweden, building upon their existing partnership in the Nordic region and globally. Oterra supplies natural food colors to the food and beverage, dietary supplements, and pet food industries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study, according to Mordor Intelligence, values the natural food colorants market as the sales of pigments extracted from plant, microbial, mineral, or animal sources that are incorporated into finished foods and beverages for visual appeal or added functionality.

Covered families include carotenoids, anthocyanins, curcumin, chlorophyll, spirulina phycocyanin, and related blends in powder or liquid form.

Scope Exclusion: We exclude any petroleum-derived or nature-identical dyes and all cosmetic or feed applications.

Segmentation Overview

-

Product Type

- Anthocyanins

- Carotenoids (Includes Beta-Carotenes)

- Curcumin

- Carmine

- Spirulina

- Other Types

-

Color

- Blue

- Green

- Red

- Yellow

- Purple

- Orange

- Pink

- Others

-

Form

- Powder

- Liquid

-

Applications

- Bakery and Confctionery

- Dairy Products

-

Beverages

- Non-alcoholic

- Alcoholic

- Dietary Supplements

- Snacks and cereals

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed pigment processors, beverage technologists, retail buyers, and regulatory advisors across North America, Europe, and Asia-Pacific.

Their inputs refined adoption rates, costing norms, and seasonality assumptions that underpin the model.

Desk Research

We start with FAO crop output, UN Comtrade HS codes for paprika, turmeric, and spirulina, USDA price decks, EFSA additive approvals, and Questel patent filings to frame pigment supply and regulatory context.

Public 10-Ks, investor presentations, Innova clean-label launch dashboards, plus insights from D&B Hoovers and Dow Jones Factiva let us map company footprints and demand pulses.

The sources cited are illustrative; many additional documents informed verification.

Market-Sizing & Forecasting

A top-down share-of-ingredients model reconstructs demand from agricultural output, trade flows, and typical extraction yields. We then cross-check totals with selective supplier roll-ups of volume multiplied by blended selling price.

Key variables include spirulina pond acreage, beetroot concentrate yields, synthetic-to-natural price spreads, clean-label SKU launches, and regional calorie-intake shifts.

Multivariate regression plus scenario analysis projects each driver, while median ratios bridge data gaps flagged by bottom-up tests.

Data Validation & Update Cycle

Outputs clear variance alerts, senior review, and peer audit.

We refresh the model every year and trigger interim updates whenever regulation or raw-material costs shift materially.

Why Our Natural Food Colorants Baseline Commands Reliability

We recognize that published market values often differ because firms vary pigment scope, application mix, and update cadence.

Our review shows the largest gaps arise when niche blues are skipped, single-region pricing is used, or straight-line growth ignores imminent bans on synthetic dyes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.03 B (2025) | Mordor Intelligence | n/a |

| USD 1.69 B (2025) | Global Consultancy A | Omits food-service volumes and fermentation pigments |

| USD 1.42 B (2023) | Trade Journal B | Covers only beverages and bakery; relies on limited survey data |

These contrasts show that Mordor's driver-based model, strict scope selection, and annual review deliver a balanced, transparent baseline clients can trust.

Key Questions Answered in the Report

What is the projected value of the natural food colorants market by 2031?

It is set to reach USD 3.25 billion, reflecting an 8.11% CAGR from 2026-2031.

Which region is growing fastest for natural food colorants?

Asia Pacific is advancing at a 9.78% CAGR on the back of regulatory harmonization and rising packaged-food penetration.

Which application segment shows the highest growth?

Dietary supplements lead with a 10.58% CAGR thanks to carotenoid and phycocyanin health claims.

How dominant are powder formats today?

Powders account for 58.25% of segment revenue due to long shelf life and compatibility with dry-blend processes.

Page last updated on: