Market Overview

| Study Period | 2021 - 2031 |

|---|---|

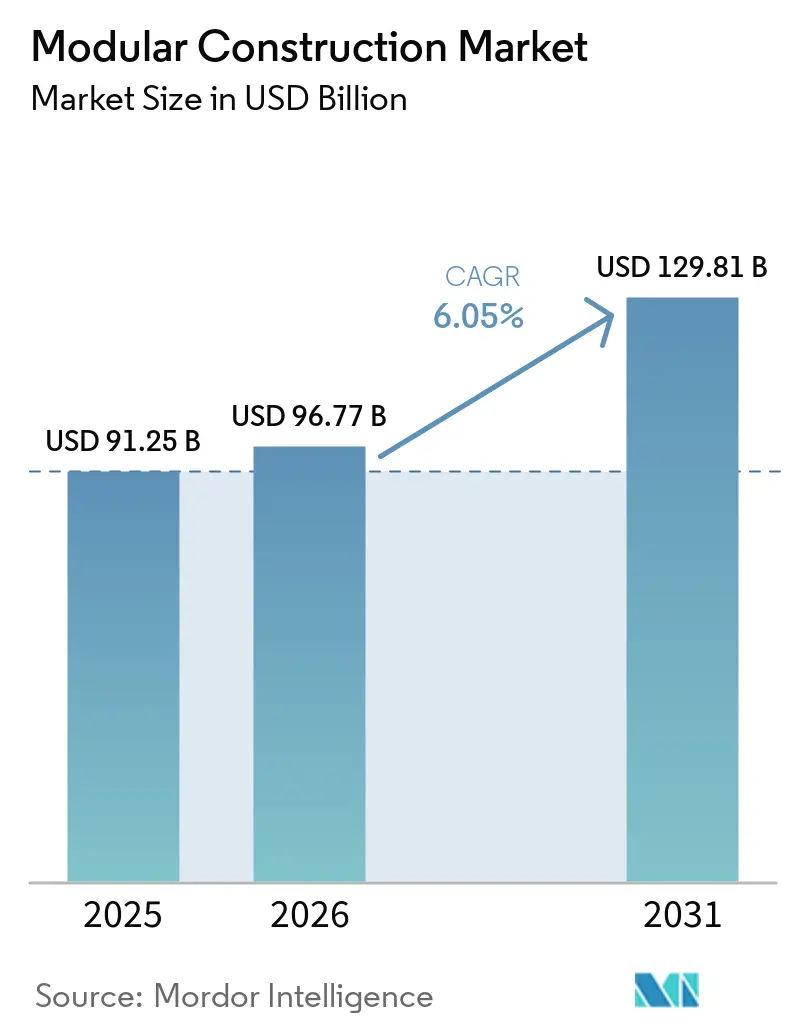

| Market Size (2026) | USD 96.77 Billion |

| Market Size (2031) | USD 129.81 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

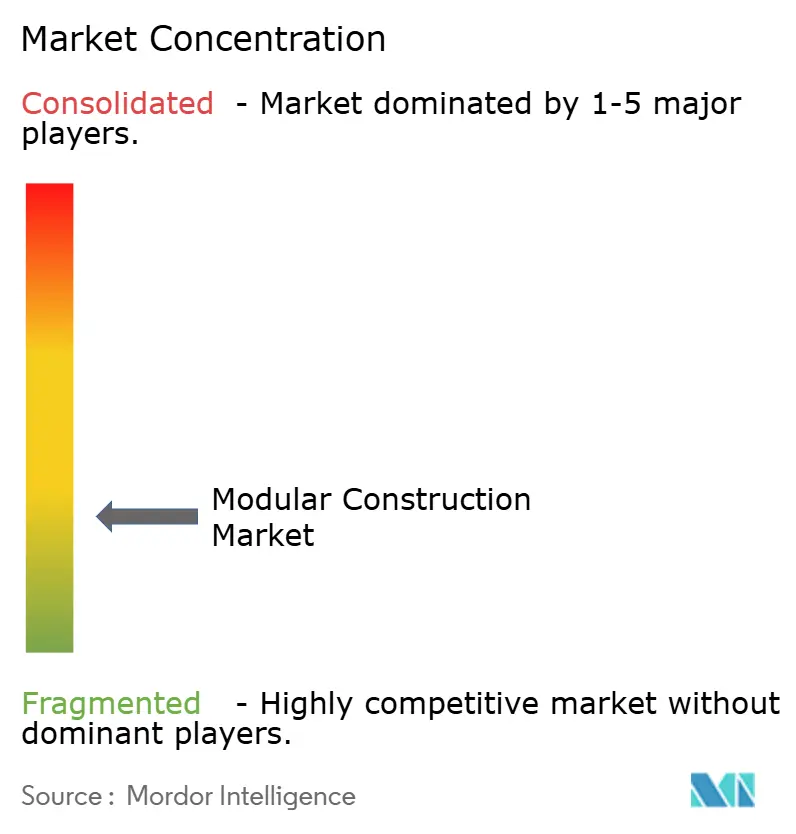

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modular Construction Market Analysis by Mordor Intelligence

The Modular Construction Market size is expected to increase from USD 91.25 billion in 2025 to USD 96.77 billion in 2026 and reach USD 129.81 billion by 2031, growing at a CAGR of 6.05% over 2026-2031. Factory-controlled fabrication is gaining ground as labor shortages, carbon-reduction targets, and government quotas make site-intensive building less viable. Steel modules dominate new orders because automated welding improves throughput and quality, while permanent configurations now underpin airports, schools, data centers, and multifamily housing. Public procurement policies in China, India, and several U.S. states enforce prefab quotas that accelerate volume growth. Capital markets have also tilted in favor of off-site projects, as lenders reward low-carbon delivery models with preferential rates.

Key Report Takeaways

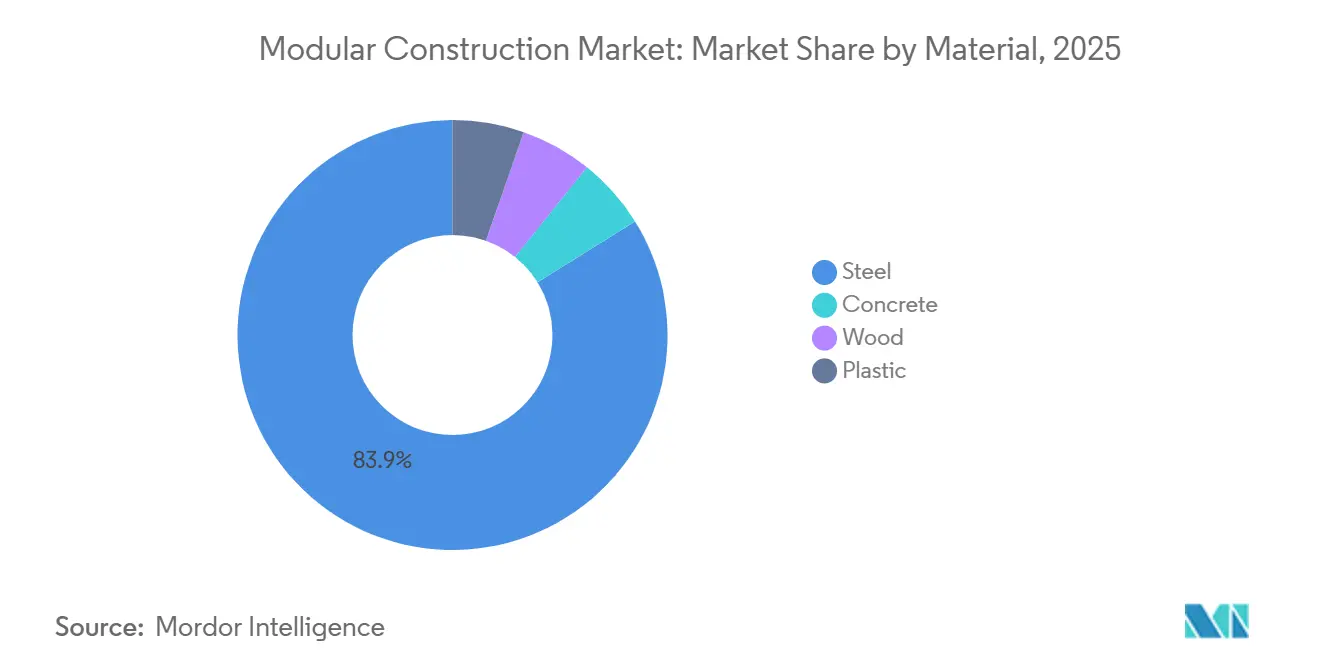

- By material, steel led with 83.87% of modular construction market share in 2025 and is forecast to advance at a 6.15% CAGR to 2031.

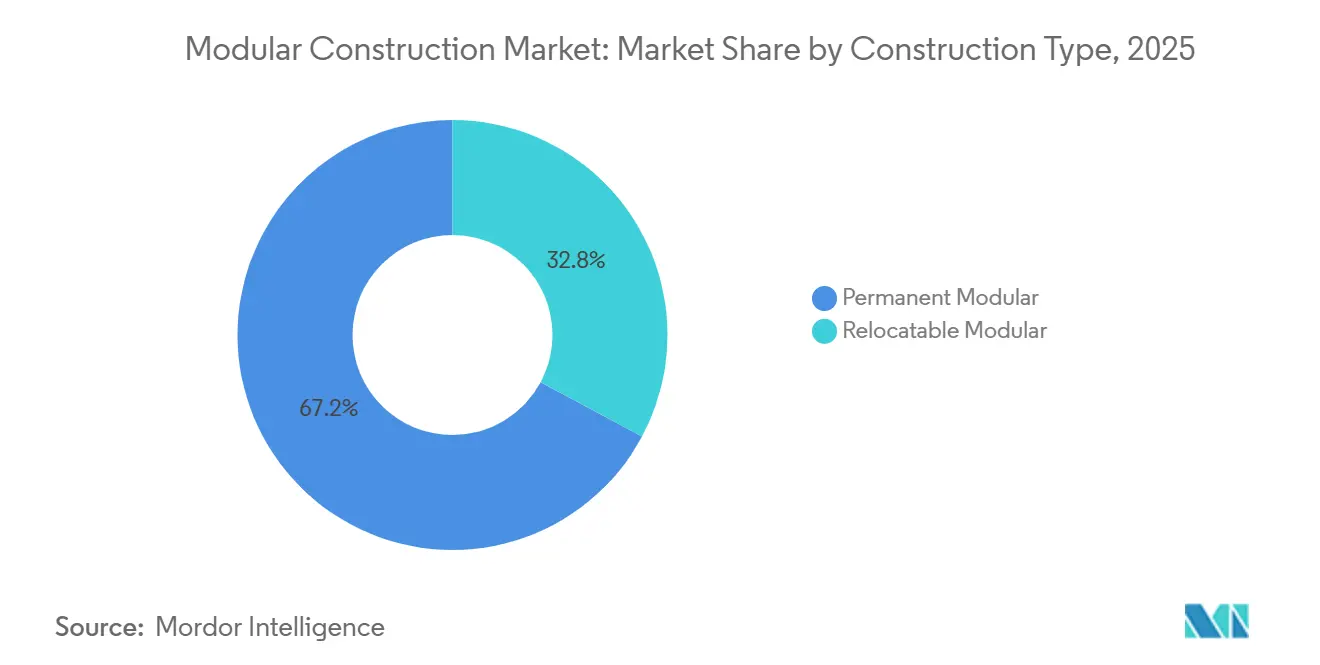

- By construction type, permanent modular accounted for 67.18% of modular construction market size in 2025, whereas relocatable modular is advancing at a 7.35% CAGR through 2031.

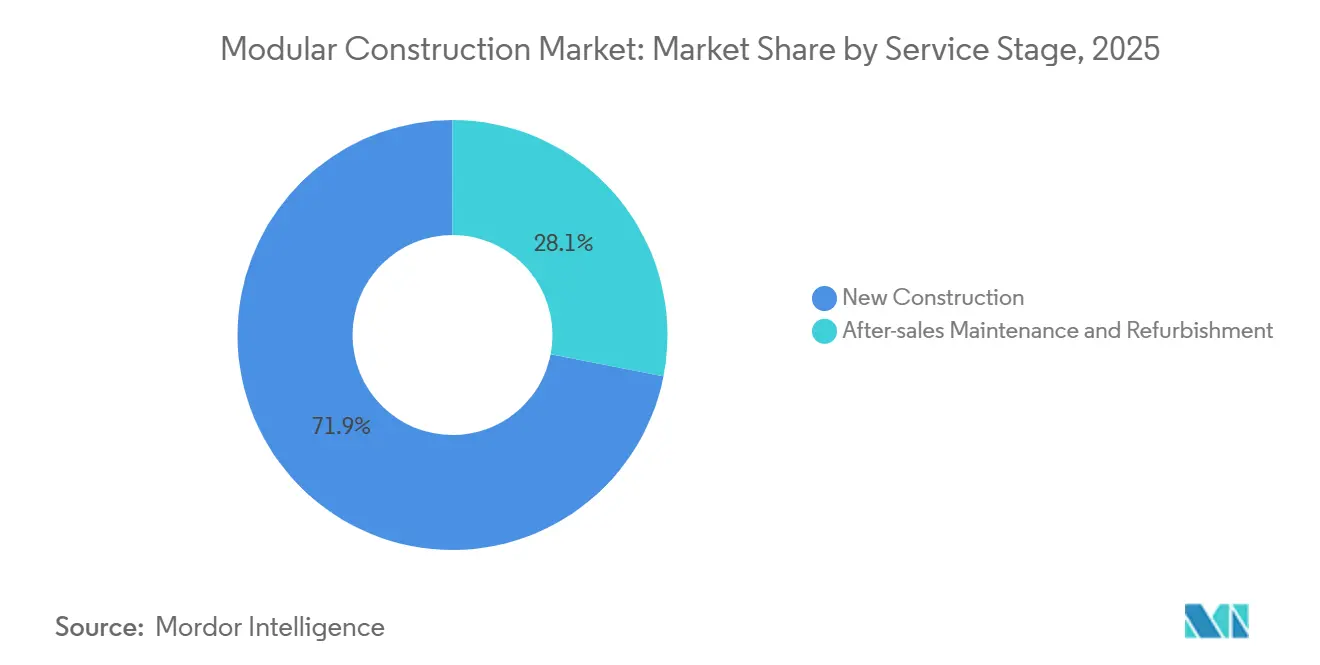

- By service stage, new construction accounted for 71.92% of modular construction market size in 2025, whereas after-sales maintenance and refurbishment is advancing at a 6.58% CAGR through 2031.

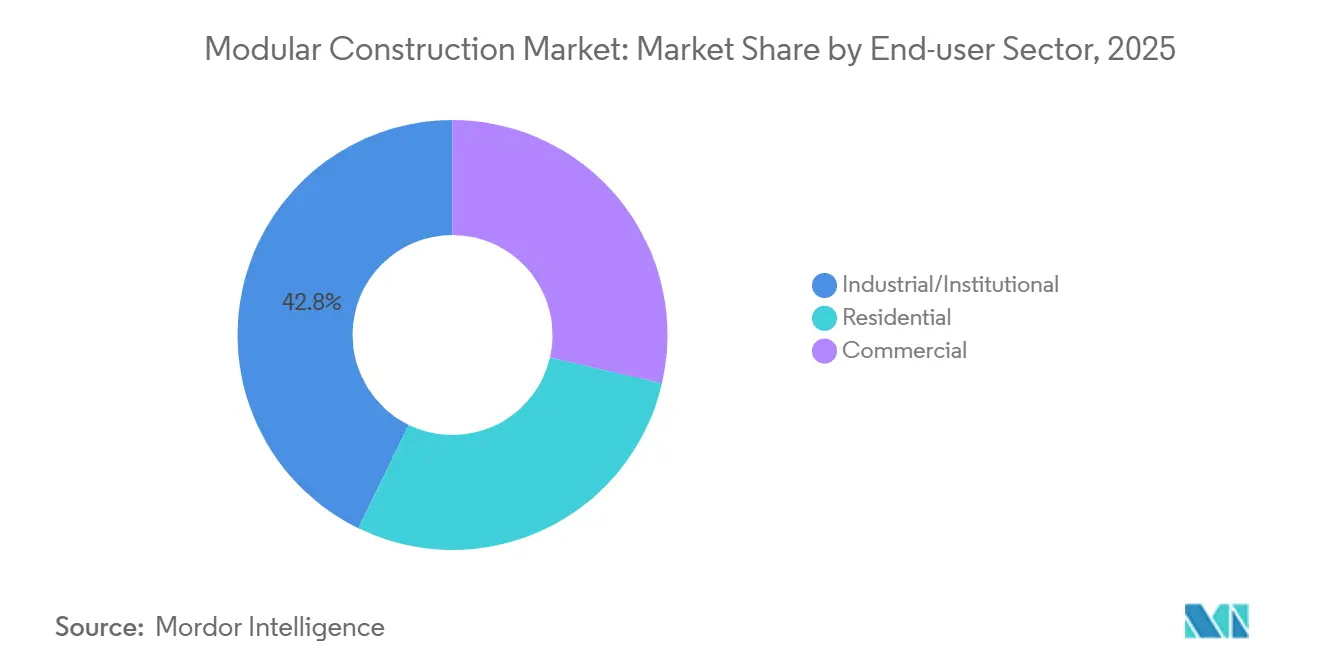

- By end-user sector, industrial/institutional captured 42.78% revenue in 2025; residential is projected to expand at a 7.86% CAGR to 2031.

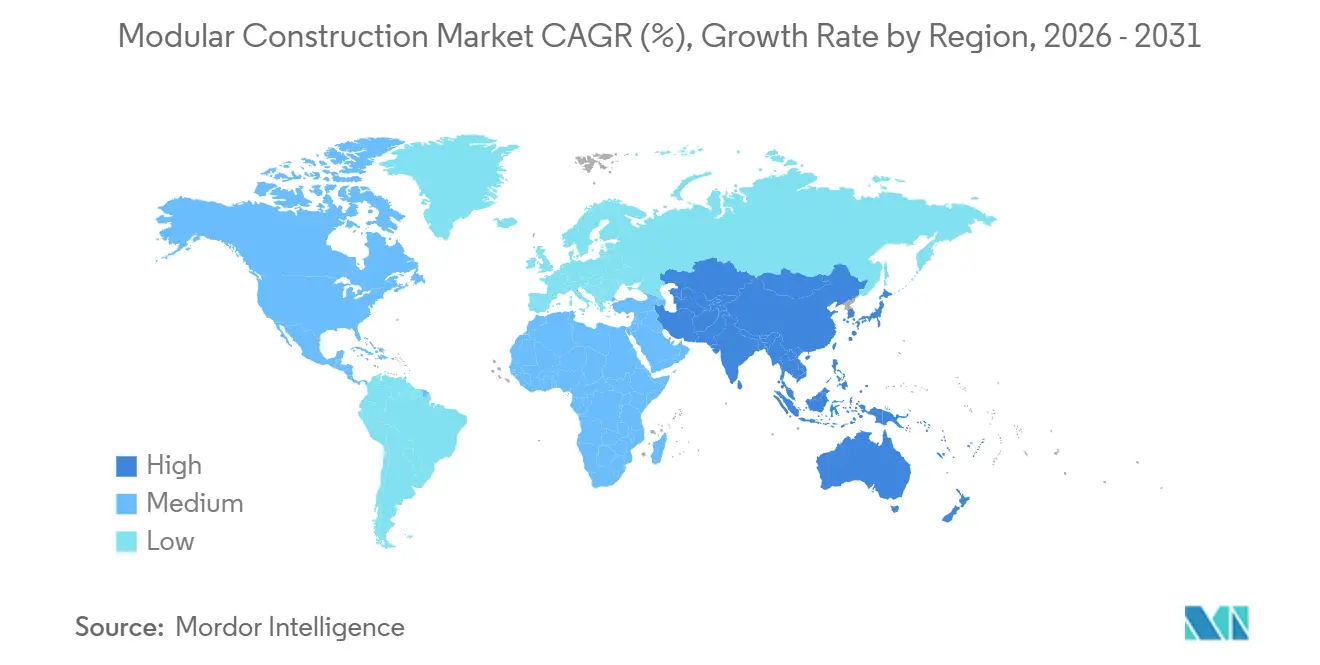

- By geography, Asia-Pacific commanded 47.16% revenue in 2025 and is forecast to grow at 7.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Modular Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanisation-Driven Housing Gap | +1.8% | APAC core (China, India, ASEAN), spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Supportive Government Incentives and Mandates | +1.5% | North America (California, federal programs), Europe (EU Timber Regulation), China (prefab mandates) | Short term (≤ 2 years) |

| Faster Project Timelines and Lifecycle Cost Savings | +1.3% | Global, with early gains in industrial/institutional sectors | Short term (≤ 2 years) |

| Labour-Shortage Mitigation Via Off-Site Fabrication | +1.2% | North America, Europe, Australia | Medium term (2-4 years) |

| ESG-Linked Financing and Carbon-Pricing Tailwinds | +0.9% | Europe, North America, select APAC markets (Singapore, Japan) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanisation-Driven Housing Gap

Asia-Pacific’s pace of city growth is stretching conventional building capacity. China’s urbanization rate reached 65% in 2024 and is guided to 70% by 2030, a shift that adds 300 million residents and intensifies demand for faster delivery models. Shenzhen, Beijing, and Shanghai require that 30% of public projects use prefab systems, and India’s Pradhan Mantri Awas Yojana has cleared 1.12 crore urban units, of which 88.62 lakh were completed by 2025[1]Press Information Bureau of India, “PMAY Progress Update,” pib.gov.in . Vietnam expects 40% urban population by 2030 and is piloting industrialized building in Hanoi and Ho Chi Minh City. Even the United Kingdom faces a 4.3 million-home shortfall, which prompted a target of 15,000 modular units each year, although factory capacity constrains current output. These conditions collectively lift baseline demand for the modular construction market.

Supportive Government Incentives and Mandates

Regulators have moved from voluntary guidelines to binding quotas and direct subsidies. California’s Factory-Built Housing program cut permitting cycles from 18 months to 6 months in areas that accepted USD 12 million of state technical aid in 2024. A federal bill, H.R. 10171, proposes USD 30 billion in grants and USD 3 billion in tax credits to accelerate adoption, while Europe’s revised Energy Performance of Buildings Directive requires all new structures to be zero-emission by 2030. Saudi Arabia’s Vision 2030 program targets 300,000 units per year and ranks modular delivery high for speed assurance. These tools improve project economics, favoring the modular construction market over conventional methods.

Faster Project Timelines and Lifecycle Cost Savings

Factory fabrication allows foundations and modules to progress in parallel, compressing schedules by 20-40%. Dallas Fort Worth International Airport’s Terminal F, a USD 4 billion build, is slated for completion 12 months sooner than stick-built peers, cutting USD 150 million in interest expense. A 2024 contractor survey found that 78% of firms using prefab recorded similar schedule gains. Modular designs also enable disassembly, lowering end-of-life disposal costs by up to 50% compared with demolition. These time and cost savings reinforce the appeal of the modular construction market for industrial operators that prize early revenue capture.

Labour-Shortage Mitigation Via Off-Site Fabrication

The U.S. industry must recruit 500,000 workers every year, yet participation rates have slipped since 2024. Factories equipped with automated welding and robotic material handling now deliver the output of 10-15 field crews with reduced error rates. Germany listed 200,000 unfilled construction posts in 2024, prompting HOCHTIEF and Züblin to scale prefab capacity. Japan faces similar pressure as 35% of its building workforce is older than 55. These deficits motivate contractors worldwide to shift toward factory assembly, supporting sustained growth for the modular construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Factory and Module-Handling CAPEX | -0.9% | Global, most acute in emerging markets with limited access to project finance | Medium term (2-4 years) |

| Architectural and Aesthetic Design Constraints | -0.6% | North America, Europe (luxury residential and landmark commercial segments) | Short term (≤ 2 years) |

| Fragmented Global Building Codes and Permits | -0.7% | Global, with acute friction in federal systems (U.S., Canada, Australia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Factory and Module-Handling CAPEX

Establishing a mid-scale plant that delivers 500–1,000 housing units each year demands USD 15–25 million for land, cranes, automated welders, and climate-controlled bays. Specialized trailers and escort vehicles add several million more for firms that serve multi-state corridors. Factories must operate at 60-70% utilization to meet breakeven, yet limited access to project finance in emerging markets keeps borrowing costs high. These economics funnel activity toward well-capitalized, vertically integrated players and restrain smaller contractors from entering the modular construction market.

Architectural and Aesthetic Design Constraints

Transport limits module dimensions to roughly 12–16 feet in width, a ceiling that narrows design freedom for bespoke homes or iconic commercial towers. A 2024 American Institute of Architects survey found that 62% of designers cited aesthetic rigidity as the primary obstacle to specifying modular systems. High-rise stacks above 20 stories require reinforced beams that erode weight and cost benefits. Luxury buyers often equate modular with utilitarian finishes, so adoption in top-tier residential and landmark projects remains muted, slowing penetration of the modular construction market in premium niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Retains Structural Primacy

Steel captured 83.87% of modular construction market share in 2025 thanks to its favorable strength-to-weight profile and compatibility with automated factory tools. That dominance is expected to persist as high-strength grades such as ASTM A992 allow longer spans while staying within transport weight limits. Automated welding drops labor hours and improves joint quality, further anchoring steel in industrial and multi-story projects.

Wood—mainly cross-laminated timber—has emerged as a low-carbon alternative in Europe and North America, enjoying double-digit growth under the EU Timber Regulation. CLT stores about 0.8 tons of CO₂ per cubic meter and now meets fire-safety codes up to 18 stories. Concrete modules remain niche due to heavy panel weights that raise logistics costs, while plastic composites are carving out roles in disaster relief where corrosion resistance and airlift ability outweigh structural limits. Continuous material innovation broadens supplier options, yet steel is expected to hold a clear lead in the modular construction market through 2031.

By Construction Type: Permanent Systems Drive Core Infrastructure

Permanent modular accounted for 67.18% of modular construction market size in 2025 and will stay ahead as airports, schools, data centers, and hospitals seek long-life assets. Integrated mechanical and electrical systems arrive pre-tested, cutting commissioning time and minimizing punch-list items.

Relocatable modular, growing at a 7.35% CAGR, appeals to mining, disaster relief, and temporary healthcare operators that value rapid deployment and reuse. WillScot Mobile Mini manages a fleet of more than 200,000 units under lease contracts that wrap in maintenance, showing how flexible asset models add depth to the modular construction market. The coexistence of long-life and relocatable designs enables suppliers to serve divergent risk profiles and funding cycles.

By Service Stage: New-Build Dominates but Lifecycle Services Expand

New construction represented 71.92% of revenue in 2025 as governments prioritized rapid unit delivery. China’s 30% prefab quota for public projects and India’s urban housing mission underscore demand for first-installation modules.

After-sales maintenance and refurbishment is growing at a 6.58% rate, signaling a pivot toward recurring revenue. Fleet owners now offer HVAC retrofits, roof replacements, and insulation upgrades that extend useful life by 10–20 years, a model that appeals to pension funds seeking steady income streams. The shift from one-off sales to service contracts strengthens customer ties and enlarges the modular construction market footprint.

By End-user Sector: Industrial/Institutional Hold Lead, Residential Accelerates

Industrial/institutional generated 42.78% of revenue in 2025, led by data centers and pharmaceutical plants that require controlled environments and stringent quality checks. Prefab electrical and cooling blocks cut build cycles in half and help operators meet surging AI workload demand.

Residential is forecast to rise at a 7.86% CAGR because median U.S. new-home prices touched USD 420,600 in 2024, making the 10–20% cost edge of modular units increasingly attractive. City authorities in Los Angeles and San Francisco now issue occupancy permits in as little as nine months for factory-built apartments, a timeline reduction that broadens the modular construction market among first-time buyers.

Geography Analysis

Asia-Pacific contributed 47.16% of global revenue in 2025 and is expected to expand at 7.21% through 2031. China’s plan to raise its urbanization ratio to 70% by 2030, India’s sizable housing missions, and prefab mandates across Singapore and Malaysia all steer capital toward off-site production. Japanese leaders Sekisui House and Daiwa House export factory know-how into Australia and the United States, strengthening regional value chains.

North America is characterized by labor shortages and large-scale incentives. The proposed USD 30 billion federal grant package and state-level programs shorten approval windows, while mega-projects such as Terminal F at Dallas Fort Worth showcase scale efficiencies[2]California Department of Housing and Community Development, “Factory-Built Housing Program Update,” hcd.ca.gov . Regulatory fragmentation between states, however, still inflates compliance costs and slows shipment across borders, tempering the pace of modular construction market growth.

Europe’s path is defined by decarbonization rules and timber uptake. The Energy Performance of Buildings Directive enforces zero-emission targets, positioning factory-made envelopes as a compliance shortcut. Labor deficits in Germany and the United Kingdom amplify the shift toward prefab methods. Emerging regions, including Saudi Arabia and Brazil, register strong demand but must overcome financing constraints and limited local plant capacity to unlock full contributions to the modular construction market.

Competitive Landscape

Global EPC firms such as Bechtel, Fluor, and Skanska have internalized modular capabilities to deliver energy and infrastructure mega-projects. Fluor’s work on 215 prefabricated process modules for the USD 30.3 billion LNG Canada plant underscores the logistical know-how required for transoceanic module shipping. Vertical integration is even deeper in Japan, where Sekisui House controls land sourcing, production, and after-sales maintenance, allowing margin capture across the entire value chain.

Technology adoption is a key differentiator. Firms that deploy Building Information Modeling cut design errors by 40%, while automated welding trims factory labor content by nearly one-third, lifting throughput without sacrificing quality. Patent filings focus on quick-connect systems that eliminate field welding and reduce on-site labor by up to 70%.

Competition is most intense in relocatable leasing, where WillScot, Algeco, and ATCO vie on fleet size and service responsiveness. In contrast, permanent modular contracts resemble traditional EPC bidding, with schedule guarantees and lifecycle cost commitments serving as primary selection criteria. This structure results in moderate overall concentration for the modular construction market.

Modular Construction Industry Leaders

Algeco UK Limited (Modulaire Group)

WillScot

DAIWA HOUSE INDUSTRY CO., LTD.

Bouygues Construction

ATCO Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: China International Marine Containers (CIMC) dispatched the Office Building Project in Bastos District, Yaoundé, Cameroon. This marked the first modular building project in the Central Africa region. The initial shipment of modules departed from CIMC Modular Building Systems' flagship production base in Xinhui, Jiangmen.

- September 2025: Mulk International, a division of UAE-based Mulk Holdings International, partnered with Marses to establish a joint venture (JV) named Mulk Marses Robotics. This new entity focuses on transitioning construction practices from traditional manual methods to automated modular construction.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global modular construction market as the revenues generated from factory-built volumetric or hybrid building modules that are transported to site and permanently or semi-permanently installed to deliver residential, commercial, or institutional facilities. The definition captures value added across design, module fabrication, onsite assembly, and commissioning.

Scope Exclusion: Simple panelized wall, roof, or floor systems shipped as flat packs without an integrated three-dimensional structural frame are excluded from the sizing.

Segmentation Overview

- By Material

- Steel

- Concrete

- Wood

- Plastic

- By Construction Type

- Permanent Modular

- Relocatable Modular

- By Service Stage

- New Construction

- After-sales Maintenance and Refurbishment

- By End-user Sector

- Industrial/Institutional

- Residential

- Commercial

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with prefab plant managers, project developers, construction consultants, and code officials across Asia-Pacific, North America, and Europe. These discussions validated realistic module throughput, installation yields, and expected ASP progression, and they filled data gaps that desk research alone could not bridge.

Desk Research

We began with authoritative open data, national construction-start statistics, building permit databases, and trade flows from UN Comtrade, Eurostat, and the U.S. Census to benchmark the total addressable construction pool. Trade association publications, such as those from the Modular Building Institute and Construction Industry Institute, then helped us isolate modular adoption rates by end use. Environmental codes, labor-cost indices from the International Labor Organization, and patent trends extracted through Questel provided early signals on technology shifts and price dynamics. Financial filings, investor decks, and reputable business press supplemented production capacity and average selling price (ASP) ranges for leading manufacturers. The sources cited above are illustrative; many additional secondary references were reviewed to validate trends and numeric inputs.

Market-Sizing & Forecasting

A top-down reconstruction of demand was executed by mapping regional construction spending to modular penetration rates, followed by selective bottom-up cross-checks using sampled factory output and ASP × volume estimates. Key variables driving the model include yearly modular share of new starts, average module size in square feet, factory utilization, regional labor cost differentials, and government housing targets. Multivariate regression linked these drivers to historical market value; forecast coefficients were stress-tested with scenario analysis before finalizing the 2025-2030 outlook. Where bottom-up samples under-represented certain geographies, calibrated uplift factors were applied and revalidated with interview feedback.

Data Validation & Update Cycle

Every draft run is peer-reviewed, variance-checked against independent metrics, and escalated when deviations exceed preset thresholds. The market model is refreshed annually, with interim revisions triggered by material policy shifts or merger activity. Before publication, an analyst performs a fresh validation pass so clients receive the latest view.

Why Mordor's Modular Construction Baseline Earns Global Confidence

Published estimates often diverge because firms mix prefab panels with volumetric units, anchor on different ASP assumptions, or refresh models at uneven intervals, and these choices naturally widen headline figures.

Key gap drivers for modular construction sizes include scope creep into panelized kits, unadjusted manufacturer revenue roll-ups, and currency conversions frozen at outdated exchange rates, which Mordor's continuous update cadence avoids.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 91.25 B (2025E) | Mordor Intelligence | - |

| USD 104.10 B (2024) | Global Consultancy A | Includes panelized systems and counts site labor savings as market value |

| USD 103.55 B (2024) | Industry Research Firm B | Uses manufacturer sales without regional ASP adjustment |

| USD 94.84 B (2025) | Trade Journal C | Excludes institutional buildings and applies single global growth factor |

In sum, our disciplined scope, continuously refreshed inputs, and transparent variable selection give decision-makers a dependable baseline that is neither overly conservative nor inflated, and one that can be readily traced back to verifiable data points.

Key Questions Answered in the Report

What is volume of the modular construction market?

What is the size of the modular construction market?

Which material dominates current modular builds?

Steel led with an 83.87% share in 2025 and is set to maintain primacy through 2031.

Which region is growing the fastest in modular adoption?

Asia-Pacific is forecast to advance at a 7.21% CAGR during 2026-2031 thanks to housing mandates and rapid urbanization.

How do permanent and relocatable modules differ in growth outlook?

Permanent systems hold two-thirds of revenue in 2025, while relocatable units are climbing faster at 7.35% through 2031.

Page last updated on: