Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

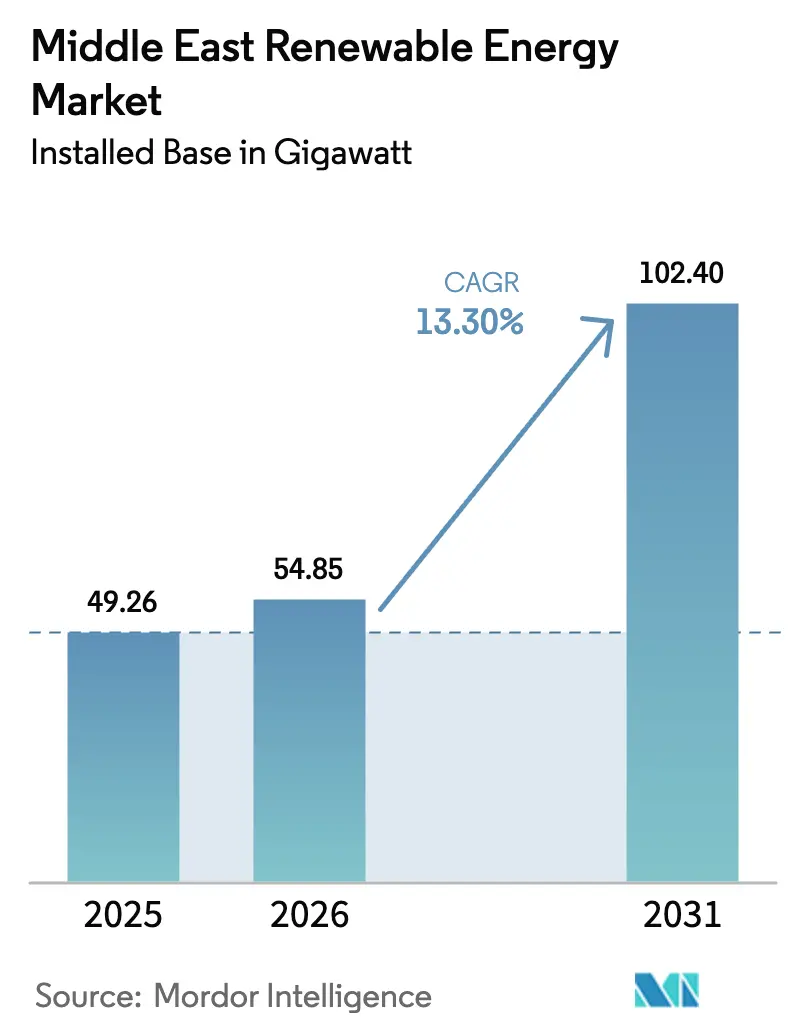

| Base Year Market Size (2025) | 49.26 gigawatt |

| Market Volume (2026) | 54.85 gigawatt |

| Market Volume (2031) | 102.40 gigawatt |

| Growth Rate (2026 - 2031) | 13.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Renewable Energy Market Analysis by Mordor Intelligence

The Middle East Renewable Energy Market size in terms of installed base is projected to expand from 49.26 gigawatt in 2025 and 54.85 gigawatt in 2026 to 102.40 gigawatt by 2031, registering a CAGR of 13.30% between 2026 to 2031.

Strong national decarbonization targets, steep solar-and-wind cost declines, and green-hydrogen export ambitions are steering capital away from hydrocarbons and toward utility-scale and distributed projects. Sovereign wealth funds are underwriting tender pipelines, while European majors and Chinese module makers are locking in multi-gigawatt supply agreements. Grid-modernization programs, the rollout of battery-energy-storage systems, and an expanding power-purchase-agreement market are further accelerating deployment. Execution risk persists, yet the investment case strengthens as technology learning curves compress levelized costs and policy frameworks tighten around net-zero deadlines.

Key Report Takeaways

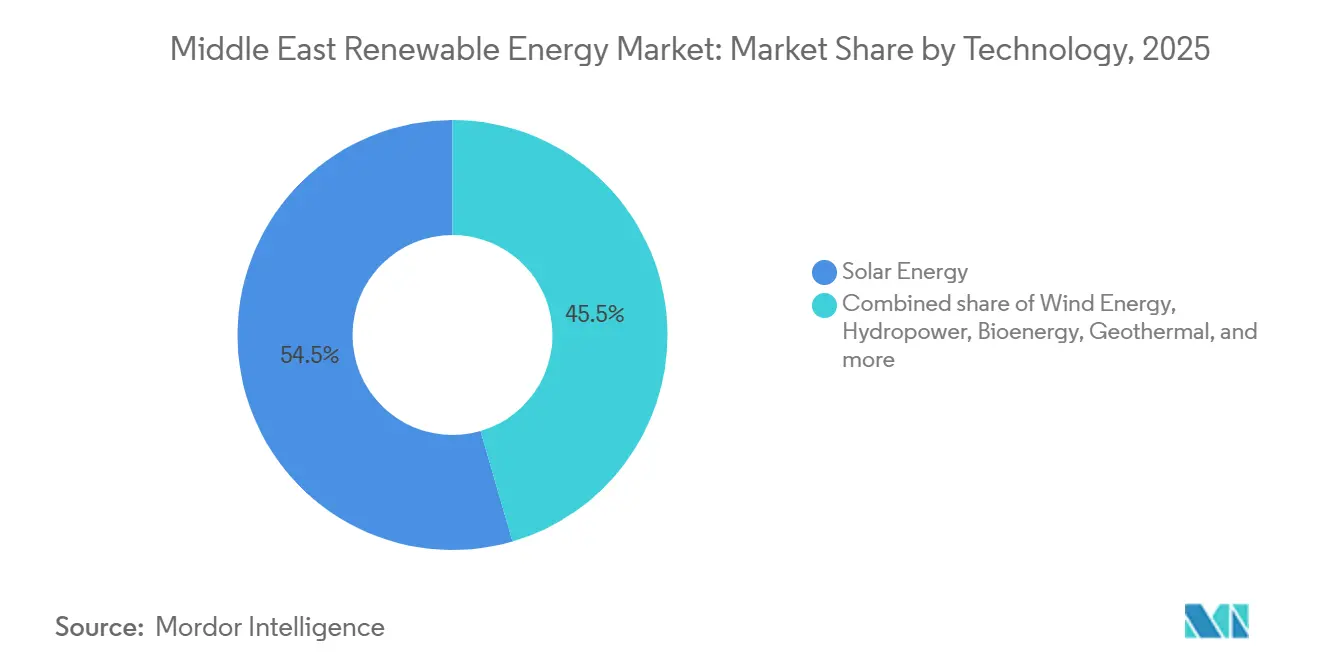

- By technology, Solar Energy led with a 54.51% Middle East renewable energy market share in 2025; Wind Energy is forecast to grow at an 18.56% CAGR to 2031.

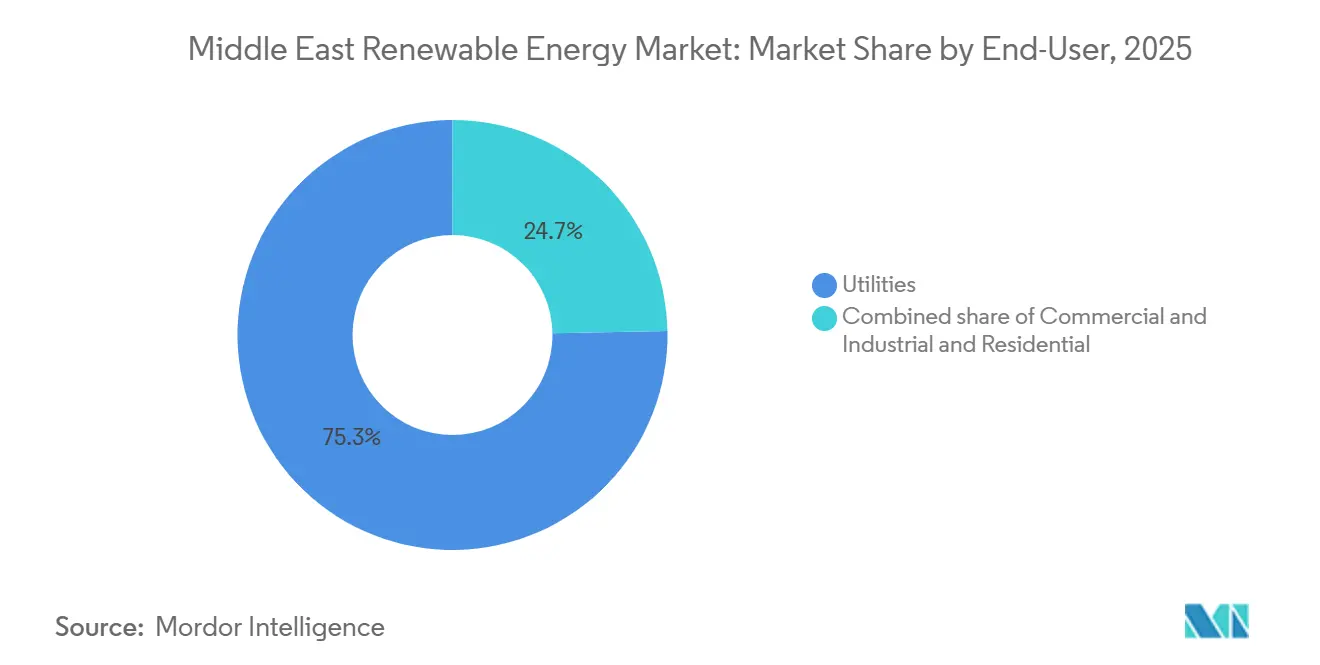

- By end-user, the Utilities segment accounted for 75.29% of the Middle East renewable energy market size in 2025, while Commercial and Industrial installations are advancing at a 25.63% CAGR through 2031.

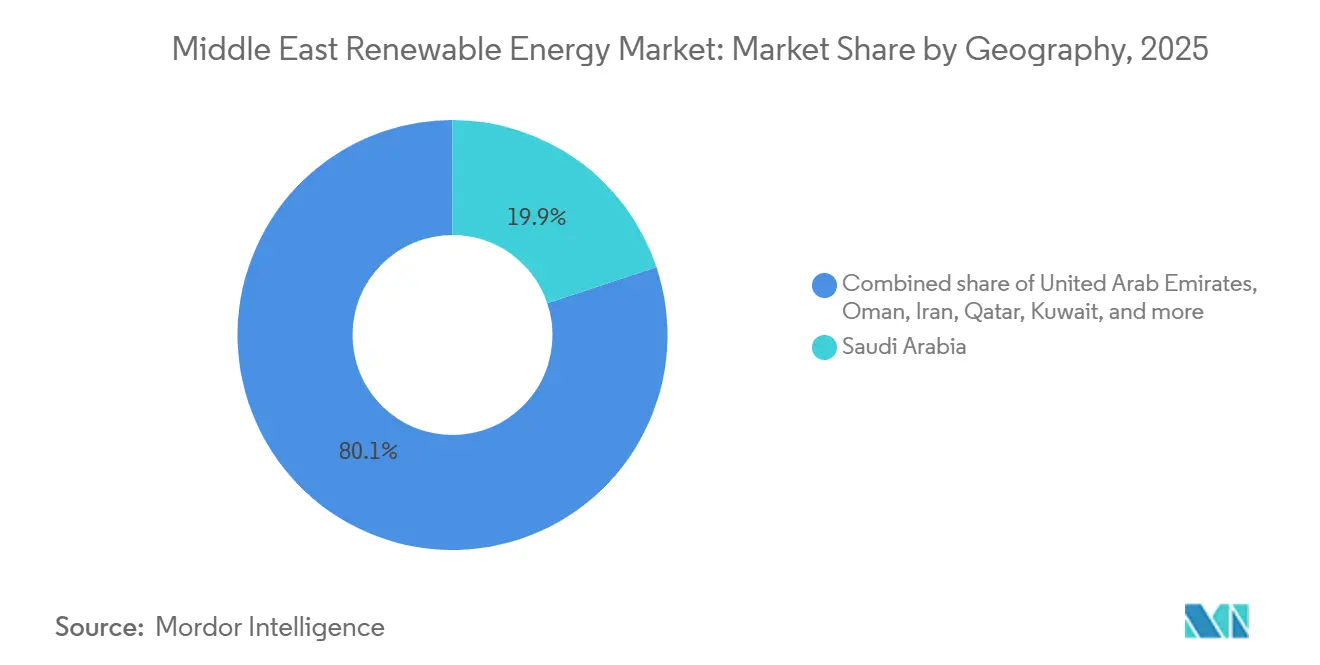

- By geography, Saudi Arabia held 19.87% of the Middle East renewable energy market share in 2025 and is expanding at a 34.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ambitious 2030–2050 national renewable-energy targets | 4.5% | Saudi Arabia, UAE, Oman, Qatar, Kuwait; spillover to Jordan and Bahrain | Long term (≥ 4 years) |

| Rapid solar-PV and wind LCOE decline | 3.2% | Global, with acute impact in Saudi Arabia, UAE, Jordan, and Oman | Medium term (2-4 years) |

| Green-hydrogen export mega-projects pipeline | 2.8% | Saudi Arabia (NEOM), UAE, Oman; export corridors to Europe and Asia | Long term (≥ 4 years) |

| Off-grid hybrid micro-grids for desert tourism & mining | 1.5% | Saudi Arabia (NEOM tourism), UAE remote facilities, Oman mining zones | Short term (≤ 2 years) |

| Abundant solar irradiance & wind corridors | 2.5% | Saudi Arabia, UAE, Oman, Jordan; highest impact in desert regions with >2,200 kWh/m² annual irradiance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ambitious 2030–2050 National Renewable-Energy Targets

Binding clean-energy objectives are redirecting public spending, fast-tracking tenders, and crowding out new thermal capacity. Saudi Arabia must add 18 GW annually to hit its 130 GW 2030 goal, a pace that dwarfs its 2024 base.[1]Saudi Ministry of Energy, “National Renewable Targets 2026 Update,” energy.gov.sa The UAE’s 50% clean-power mandate funnels sovereign capital into public-private partnerships that de-risk early-stage development. Qatar and Kuwait have set smaller but symbolic quotas that broaden the regional procurement funnel. Targets anchor pipeline visibility, yet slippage in grid upgrades or land acquisition can delay follow-on investments in hydrogen and desalination, exposing financiers to cascading project-timeline risk.

Rapid Solar-PV and Wind LCOE Decline

Photovoltaic and onshore-wind tariffs now undercut gas-fired generation, making renewables the default choice for greenfield capacity. Regional solar LCOE averaged USD 37 per MWh in 2025 and is on track to hit USD 17 by 2060.[2]UAE Ministry of Energy, “Energy Strategy 2050,” moenr.gov.ae Saudi Arabia’s Dawadmi wind bid at 1.34 cents per kWh erased the economic rationale for new thermal plants.[3]Saudi Power Procurement Company, “Dawadmi Wind Round 6 Results,” sppc.sa Module oversupply, bifacial-panel efficiency gains, and tracker optimization have sliced balance-of-system costs by 22% since 2024. While utilities secure 25-year PPAs at sub-2-cent tariffs, equipment makers face thinner margins, forcing a pivot toward next-generation technologies and service revenues.

Green-Hydrogen Export Mega-Projects Pipeline

Gigawatt-scale hydrogen ventures convert domestic solar and wind resources into export commodities that diversify hydrocarbon economies. The USD 8.4 billion NEOM plant combines 4 GW of renewables to produce 600 t/d of hydrogen for ammonia conversion bound for Europe.[4]NEOM Company, “Hydrogen Project Fact Sheet,” neom.com Masdar’s Abu Dhabi and Omani projects target 1 million t/y by 2030, demanding 15–20 GW of dedicated capacity. Long-dated offtake agreements de-risk renewable build-outs, but concentration in a handful of mega-facilities magnifies exposure to electrolyzer delays or construction overruns.

Off-Grid Hybrid Microgrids for Desert Tourism & Mining

Remote resorts, defense posts, and mineral sites are replacing diesel with solar-plus-storage systems that cut fuel use by up to 70%. NEOM’s hospitality zones deploy 500 kW–5 MW microgrids that align with luxury sustainability branding. High avoided-fuel costs, modular design, and quick permitting grant developers premium tariffs and faster paybacks. Standardizing microgrid controls under IEC 62898 is emerging as a priority to scale deployments across varied loads and harsh climates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent fossil-fuel power subsidies | -1.8% | Saudi Arabia, UAE, Kuwait, Qatar, Bahrain; limited impact in Jordan and Oman | Medium term (2-4 years) |

| Limited grid interconnection & storage capacity | -1.4% | Saudi Arabia, UAE, Oman; acute in Kuwait and Bahrain | Short term (≤ 2 years) |

| Desert soiling & water-usage challenges for PV | -1.2% | Saudi Arabia, UAE, Kuwait, Qatar; regions with high dust concentration and water scarcity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Fossil-Fuel Power Subsidies

Gulf retail tariffs as low as USD 0.048 / kWh undercut rooftop-solar economics and slow distributed adoption. A 1% subsidy rollback correlates with a 10.61% jump in renewable generation, yet political sensitivities push reforms to 2027 and beyond in Kuwait and Qatar. Two-tier markets emerge where subsidized households stick with grid power while utility-scale solar flourishes under competitive tenders. The gap limits addressable demand for residential installers and defers mass-market battery uptake.

Limited Grid Interconnection & Storage Capacity

Legacy networks, built for baseload thermal plants, strain under variable solar and wind influx. Saudi Arabia’s 7.8 GWh storage project adds only four hours of cover, leaving multi-day wind lulls unresolved. The GCC Interconnection Authority’s USD 3.5 billion upgrade aims to double cross-border transfer capacity by 2028, but right-of-way hurdles are already pushing milestones into 2027. Developers are forced to co-locate storage, accept curtailment, or rethink project sizing, all of which compress returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Dominance Anchors Transition

Solar Energy held 54.51% of the Middle East renewable energy market in 2025 and is advancing at an 18.56% CAGR through 2031. This outsized share reflects irradiance levels above 2,200 kWh/m² in Saudi Arabia and the UAE, rapid module cost declines, and supportive tender frameworks. Concentrated-solar-power plants such as Dubai’s 950 MW Noor Energy 1 add 5,907 MWh of molten-salt storage, providing evening dispatch that photovoltaics alone cannot match. Wind installations cluster along Saudi Arabia’s northern highlands and Oman’s coasts, where capacity factors top 40%. Hydropower and bioenergy remain marginal due to resource limitations, while geothermal and ocean technologies sit at the pilot stage.

Aggressive procurement favors high-performance hardware. First Solar shipped 1.8 GW of cadmium-telluride panels prized for high-temperature resilience, whereas JinkoSolar delivered 3.1 GW of bifacial Tiger Neo modules that capitalize on ground-albedo gains. Siemens Gamesa and Vestas are vying to supply 1.5 GW of turbines for Saudi Arabia’s Dawadmi project. The Middle East renewable energy market size for wind could swell if forthcoming Red Sea offshore studies confirm 45%-plus capacity factors, yet solar will remain the anchor technology through 2031.

By End-User: Commercial and Industrial Surge Reshapes Demand

Utilities controlled 75.29% of 2025 capacity, reflecting sovereign-backed gigawatt tenders and long-term PPAs. Commercial and Industrial customers, however, are expanding at a 25.63% CAGR, outpacing every other category as multinational firms pursue on-site generation to meet global net-zero targets. Yellow Door Energy’s solar-as-a-service model covers more than 500 MW across 100 sites, helping clients shave 20–30% off energy bills in unsubsidized zones. Saudi Arabia’s rooftop-solar initiative seeks 3 GW of corporate installs by 2030, while the UAE already hosts 1.5 GW on warehouse and logistics roofs.

Residential uptake lags due to subsidized tariffs and split-incentive hurdles. Jordan is the exception, posting 10% household penetration thanks to higher retail rates and 30-day permit cycles. As commercial fleets scale, demand grows for modular batteries sized at 100 kW–2 MW and energy-management software that optimizes load shifting. The Middle East renewable energy market will therefore see distributed systems erode the utility share but complement rather than cannibalize grid-scale additions.

Geography Analysis

Saudi Arabia’s procurement pipeline exceeds 50 GW, anchored by NEOM’s USD 8.4 billion hydrogen complex that absorbs 4 GW of solar and wind and guarantees long-term offtake. The UAE’s diversified pathway taps Masdar’s global 100 GW ambition and pairs 19 GW of domestic renewables with nuclear baseload to stabilize supply. Oman is positioning Duqm as a logistics bridge to European and Asian hydrogen markets, requiring dedicated transmission corridors and port retrofits.

Israel’s 7.5 GW renewables base meets 20% of power demand but faces land scarcity, steering growth to rooftops and agrivoltaics. Jordan’s streamlined permitting delivers 27% renewable penetration, the region’s highest, while Qatar’s Al Kharsaah and Siraj 1 plants push the emirate toward its 5 GW 2035 goal. Kuwait’s Shagaya park contends with land-use disputes that could delay its 15% 2030 target. Bahrain, with limited space, leans on distributed solar, initiating a 710 MW pipeline through 2035 to hedge reliance on imported gas.

Iran’s 1.2 GW capacity reflects sanctions-constrained finance, yet high irradiance in Yazd and Semnan offers latent potential. Iraq’s 1 GW Basra solar plant signals interest in diversifying export-dependent revenues. Conflict-affected Yemen and smaller territories add less than 5% capacity, showing that governance quality outweighs resource endowment when scaling the Middle East renewable energy market.

Competitive Landscape

Utility-scale development is moderately concentrated. ACWA Power operates 9.5 GW with another 10 GW under development, leveraging sovereign guarantees to bid sub-2-cent tariffs. Masdar, armed with Abu Dhabi backing, targets a 100 GW global portfolio by 2030, coupling regional assets with ventures in Africa and Central Asia. TotalEnergies and Engie blend utility solar with hydrogen offtake and rooftop plays, diversifying revenue streams.

In the distributed segment, fragmentation is rising. Yellow Door Energy finances and operates on-site arrays for commercial customers across the UAE and Saudi Arabia, a capital-light model that skirts grid bottlenecks. Technological rivalry between JinkoSolar’s high-efficiency bifacial modules and First Solar’s high-temperature cadmium-telluride panels drives procurement decisions in sandy, high-heat environments. Battery providers and microgrid-software startups are entering to supply storage-as-a-service, signaling a pivot from pure capacity addition to integrated energy solutions. Regulatory heterogeneity around wheeling charges, net metering, and foreign ownership still favors incumbents with deep local partnerships.

Middle East Renewable Energy Industry Leaders

Yellow Door Energy

ACWA Power

Masdar

EDF Renewables

JinkoSolar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ENGIE has successfully achieved financial closure on its most ambitious solar endeavor to date: the 1.5-gigawatt Khazna Solar Park located in Abu Dhabi.

- December 2025: Acwa Power, along with Water and Electricity Holding Company (Badeel) and Saudi Aramco Power Company, all based in Riyadh, have reached a financial milestone for five solar and two wind projects in Saudi Arabia. These seven projects, boasting a combined capacity of 15 GW, successfully obtained a senior debt facility of $5.9 billion, backed by a consortium of local, regional, and international banks.

- October 2025: Saudi Arabia has inked renewable energy contracts exceeding SAR 9 billion (USD 2.4 billion). The Saudi Power Procurement Company, overseeing the initiative, has distributed these contracts across five projects: four solar and one wind, collectively boasting a capacity of 4,500 megawatts.

- January 2025: Masdar, the Emirati state-owned renewable investment firm, has joined forces with EWEC to construct a massive solar and battery energy storage (BESS) facility. This ambitious project will integrate 5.2 GW of solar power with 19 GWh of battery storage, aiming to deliver a steady output of 1 GW of renewable energy.

Middle East Renewable Energy Market Report Scope

Renewable energy emanates from natural sources, or processes replenished naturally, including sources like wind, sunlight, etc. It creates lower emissions than non-renewable resources.

The Middle East renewable energy market is segmented by technology, end user, and geography. By technology, the market is segmented into solar energy, wind energy, hydropower, bioenergy, geothermal, and ocean energy. By end user, the market is segmented into utilities, commercial and industrial, and residential. By geography, the market is segmented into the United Arab Emirates, Saudi Arabia, Oman, Iran, Israel, Jordan, Qatar, Kuwait, Bahrain, and the rest of the Middle East. For each segment, the market sizing and forecasts have been provided on the basis of volume (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Oman |

| Iran |

| Israel |

| Jordan |

| Qatar |

| Kuwait |

| Bahrain |

| Rest of Middle East |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Oman | |

| Iran | |

| Israel | |

| Jordan | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current installed renewable capacity in the Middle East renewable energy market?

Installed capacity stands at 54.85 GW in 2026 and is projected to climb to 102.40 GW by 2031.

Which technology dominates new additions in the Middle East renewable landscape?

Solar Energy leads, accounting for 54.51% of 2025 capacity and growing at an 18.56% CAGR.

How fast is Saudi Arabia expanding clean-energy assets?

Saudi Arabia is adding renewables at a 34.22% CAGR, supported by Vision 2030 targets and record-low tender tariffs.

Why are Commercial and Industrial buyers accelerating procurement?

Corporate sustainability mandates and sub-grid-parity solar tariffs are driving a 25.63% CAGR for Commercial and Industrial installations.

What restrains rooftop-solar adoption despite strong irradiance?

Deep fossil-fuel subsidies keep retail electricity prices low, delaying parity for residential systems.

Page last updated on: