Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

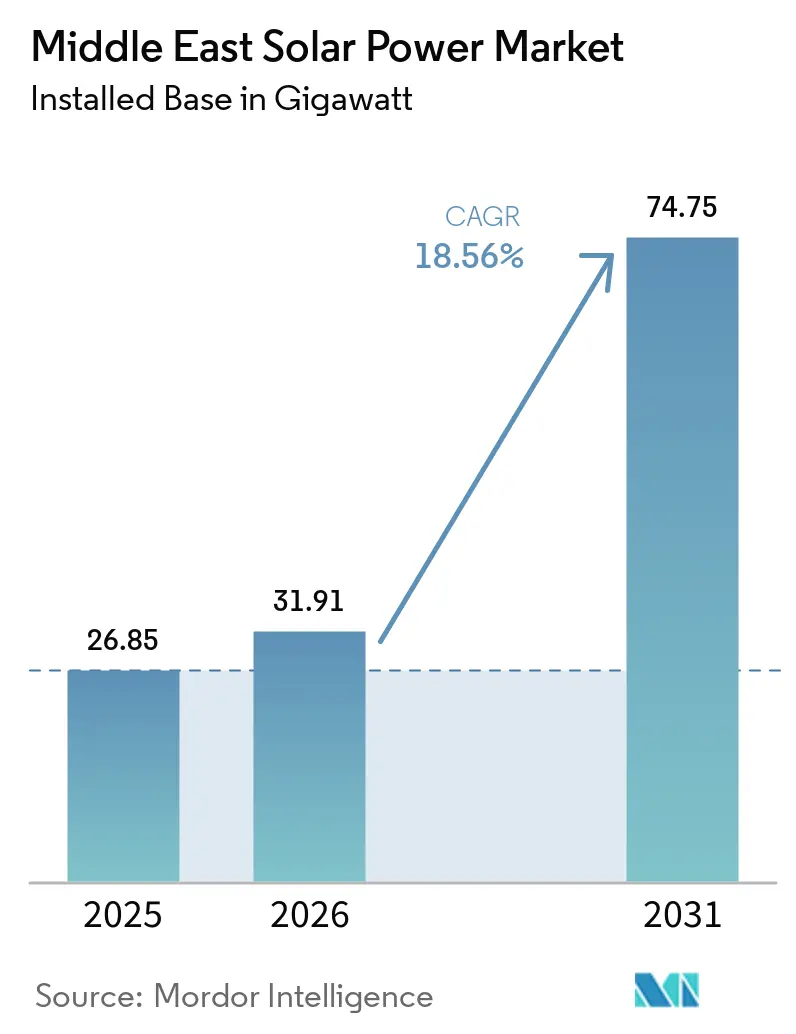

| Base Year Market Size (2025) | 26.85 gigawatt |

| Market Volume (2026) | 31.91 gigawatt |

| Market Volume (2031) | 74.75 gigawatt |

| Growth Rate (2026 - 2031) | 18.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Solar Power Market Analysis by Mordor Intelligence

The Middle East Solar Power Market size in terms of installed base is expected to grow from 26.85 gigawatt in 2025 to 31.91 gigawatt in 2026 and is forecast to reach 74.75 gigawatt by 2031 at 18.56% CAGR over 2026-2031.

The strong trajectory mirrors a policy-driven pivot away from hydrocarbons as governments embed solar build-outs into national infrastructure plans. Record-low tariffs below 1.1 US cents/kWh in Saudi Arabia’s Round 6 tender, accelerating corporate power-purchase agreements, and the region’s world-leading solar irradiation above 2,000 kWh/m²/yr together anchor cost-competitiveness. Rising localization of TOPCon cell production, large-scale storage procurements, and green-hydrogen links such as NEOM are widening project pipelines while compressing procurement cycles. Execution risks stem from grid congestion, desert operating conditions, and supply-chain exposure to Chinese equipment, yet mitigation strategies, battery tenders, robotic cleaning, and domestic manufacturing are reducing downside volatility. Overall, the Middle East solar power market is moving from the opportunity phase to the infrastructure phase, with sovereign backing cushioning financing costs even in higher-risk jurisdictions.

Key Report Takeaways

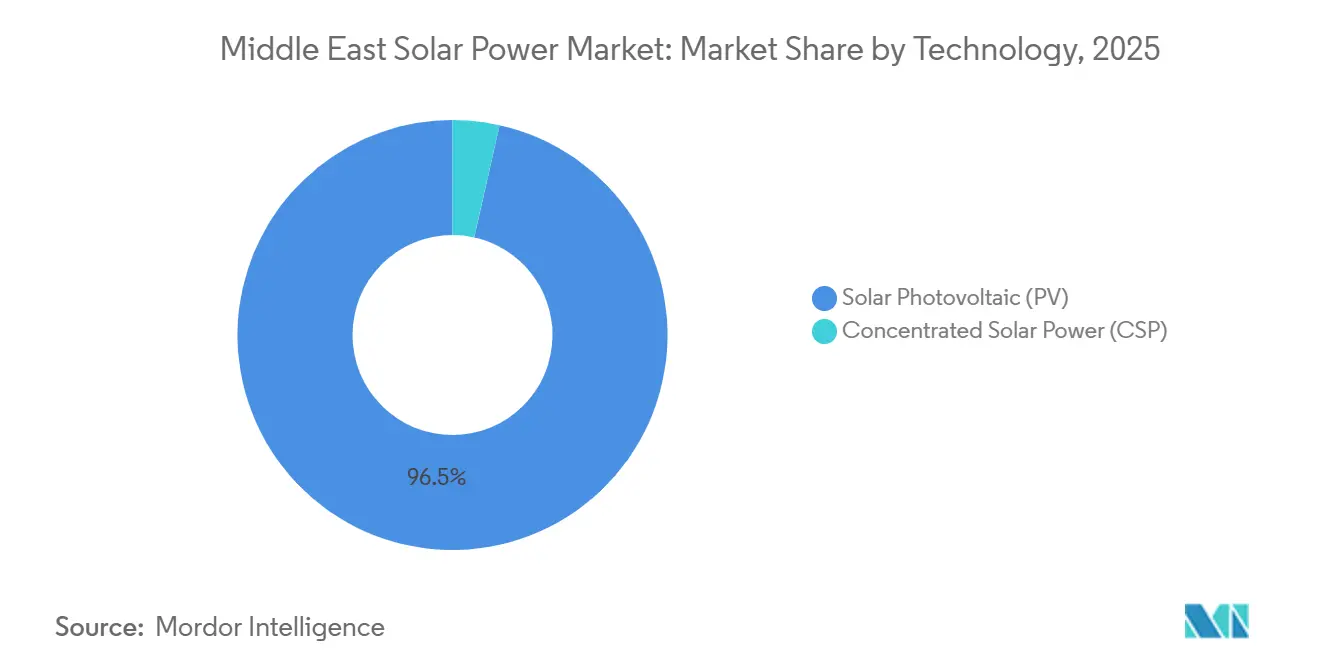

- By technology, photovoltaic systems captured 96.5% share of the Middle East solar power market size in 2025, while concentrated solar power will expand at a 30.44% CAGR to 2031, limited to hybrid projects pairing molten-salt storage with PV.

- By grid type, on-grid plants held 90.2% of the Middle East solar power market share in 2025, while off-grid sites will post the fastest 24.3% CAGR through 2031.

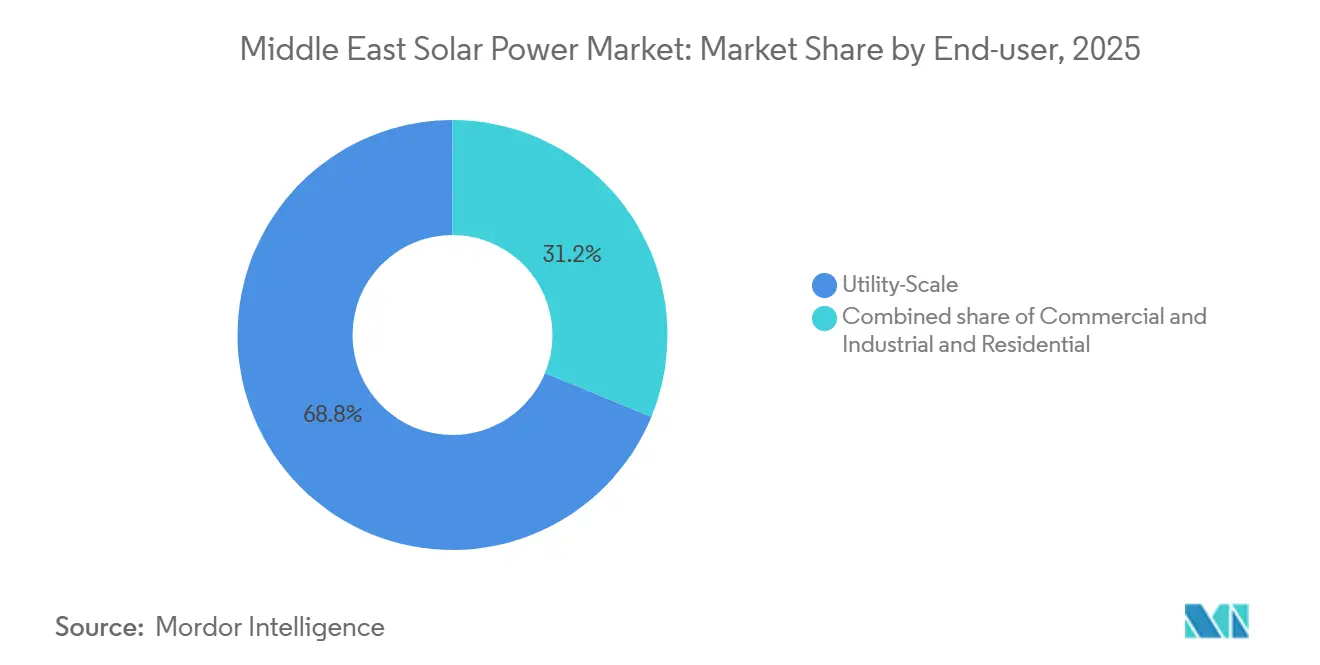

- By end-user, utility-scale projects led with 68.8% revenue share in 2025; residential arrays are projected to expand at a 22.5% CAGR through 2031.

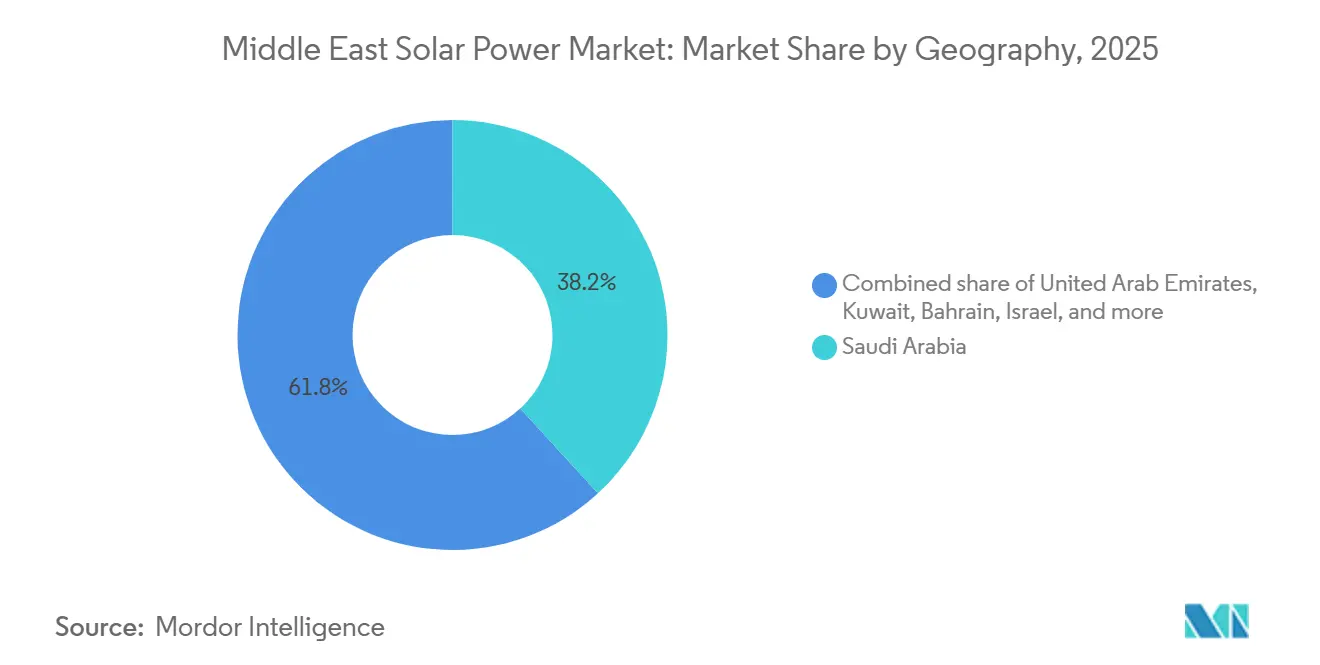

- By geography, Saudi Arabia, at 38.17% of regional capacity in 2025, is set to pace geography growth with a 30.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Solar Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National renewable-energy targets and mega-tenders | 5.2% | Saudi Arabia, UAE, Oman, Qatar, Kuwait | Medium term (2-4 years) |

| Falling LCOE of mono-PERC and TOPCon PV modules | 4.1% | Global, with strongest uptake in Saudi Arabia and UAE | Short term (≤ 2 years) |

| High solar irradiation exceeding 2,000 kWh/m²/yr | 3.8% | Saudi Arabia, UAE, Oman, Jordan, Israel | Long term (≥ 4 years) |

| GCC cross-border grid trade initiatives | 2.3% | Saudi Arabia, UAE, Kuwait, Bahrain, Qatar, Oman | Medium term (2-4 years) |

| Surge in corporate PPAs from data-center and industrial clusters | 3.6% | UAE, Saudi Arabia, with spillover to Qatar and Bahrain | Short term (≤ 2 years) |

| Utility-scale green-hydrogen developments needing solar feedstock | 4.7% | Saudi Arabia (NEOM, Oxagon), UAE, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Renewable-Energy Targets And Mega-Tenders

Nationwide programs are scaling from pilot auctions to multi-gigawatt blocks, creating a stable offtake pipeline for the Middle East solar power market. Saudi Arabia’s Round 6 tender in October 2025 awarded 4.5 GW across eight sites at a record 1.09682 US cents/kWh, underscoring sovereign resolve to treat solar as a baseload asset. The UAE’s utility EWEC followed with a 1 GW solar plus 400 MW battery RFP that required firm power delivery, signaling a shift to dispatchable renewables.[1]EWEC Communications, “Request for Proposals—1 GW Solar Plus Storage,” ewec.ae Oman’s Ibri III shortlist and Kuwait’s Al Dibdibah tender round out a region-wide queue topping 15 GW. Tender rules now mandate IEC-61215 and IEC-61730 certification, lifting quality standards and reducing warranty risk. Compressed bid-to-financial-close milestones of 15 months are forcing suppliers to hold inventory regionally, shortening historical procurement cycles by almost 40%.

Falling LCOE Of Mono-PERC And TOPCon PV Modules

Rapid diffusion of TOPCon has pushed module conversion efficiencies beyond 25% while narrowing price premiums to under 5% relative to PERC.[2]PV Magazine Staff, “TOPCon Modules Break 25% Conversion Barrier,” pvmagazine.com JinkoSolar’s USD 1 billion TOPCon joint venture with Saudi Arabia’s Public Investment Fund will deliver 10 GW/year from early 2026, cutting landed costs by up to 12%. A 5 GW plant inaugurated by Desert Technologies in Jeddah in 2024 further broadens local supply. Bifacial TOPCon modules yield an additional 10% to 15% in the desert’s high-albedo terrain, pushing the Middle East solar power market toward near-universal PV adoption as localized output scales and tender frameworks grant bid discounts for domestic content, lowering tariffs and deepening the cost gap with gas generation.

High Solar Irradiation Exceeding 2,000 kWh/m²/yr

Annual irradiation surpassing 2,400 kWh/m² in parts of Saudi Arabia enables single-axis trackers to reach 28%–32% capacity factors, levels once exclusive to gas turbines. Jordan’s 24 MW Disi array posts a 37.6% factor, compressing paybacks below seven years without subsidies. The Jordan–Israel Project Prosperity barter exchanges 600 MW of solar power for desalinated water, monetizing surplus irradiation while tackling water stress. Masdar’s 5.2 GW UAE project pairs 19 GWh of batteries with PV to supply 1 GW firm output by 2027, proving that high resource quality plus storage can displace spinning reserves. These metrics cement the Middle East solar power market as one of the world’s best-in-class resource plays.

GCC Cross-Border Grid Trade Initiatives

Regional interconnection is unlocking arbitrage across peak-load mismatches. The GCC Interconnection Authority has earmarked USD 3.5 billion through 2035 to expand 500 kV links, with the Saudi-Iraq tie-line due in April 2026. Enhanced transfer capacity lets Saudi Arabia export midday solar surplus to Kuwait and Bahrain, smoothing load curves and trimming ancillary-service costs by up to 20%. Egypt’s link through Saudi Arabia opens a renewable corridor to Europe via subsea cables, creating a natural price floor for utility-scale projects. Settlement friction persists because wheeling fees and balancing charges differ by jurisdiction, keeping traded volumes below 10% of installed capacity. Even so, grid trade remains a structural growth lever for the Middle East solar power market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion and intermittency management costs | -2.8% | Saudi Arabia (Eastern Province), UAE (Northern Emirates), Kuwait | Short term (≤ 2 years) |

| High soiling and water-intensive O&M in desert climates | -1.9% | Saudi Arabia, UAE, Oman, Kuwait, Qatar | Medium term (2-4 years) |

| Political-risk premium elevating project finance costs | -2.1% | Iraq, Lebanon, Yemen, with spillover to Jordan | Long term (≥ 4 years) |

| Import-dependency exposure to trade restrictions | -1.6% | Global, with acute impact on Saudi Arabia, UAE, Oman | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Congestion And Intermittency Management Costs

Transmission upgrades lag utility-scale rollouts, forcing developers to fund substations that add as much as 12% to capex. Curtailment in Saudi Arabia’s Eastern Province averages 8%–15% at midday, eroding internal rates of return. A 7.8 GWh battery tender awarded to Sungrow in 2024 aims for 10 GW of storage by 2030, yet lithium-iron-phosphate systems cost USD 250–350/kWh and trim IRR by 150-200 bps. The UAE’s Northern Emirates mirror the challenge, with EWEC seeking 400 MW/800 MWh of storage capacity. Kuwait’s Al Dibdibah timeline doubled to seven years due to the need for a dedicated 400 kV line, adding USD 180 million in grid spend. Reactive-power mandates and synchronous condensers further inflate balance-of-system budgets, tempering short-term expansion in the Middle East solar power market.

High Soiling And Water-Intensive O&M In Desert Climates

Desert dust can slash output by up to 40% between cleanings, and scarce water makes manual washing costly. KAUST measured 35%–40% soiling loss after 30 days in the Rubʽ al Khali, with performance restored to 92% after water-jet washing.[3]KAUST Energy Lab, “Soiling Loss Measurements in Rubʽ al Khali,” kaust.edu.sa NOMADD’s 61% local-content dry-cleaning robot costs USD 1.2 million per 100 MW, 30% above manual crews, but eliminates water use and cuts labor by 40%. Ecoppia’s waterless units are also being deployed, though capex remains high for small C&I arrays. Aramco unveiled a sub-USD 1,000 prototype in 2024, targeting mass rollout. Module output derates 0.4%–0.6% per °C above 25 °C, compressing yearly yield by up to 12%, which elevates temperature coefficient rankings in tender evaluations. Collectively, O&M challenges shave points off the Middle East solar power market’s headline returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: TOPCon Traction Accelerates Photovoltaic Supremacy

Photovoltaic installations represented 96.5% of the Middle East solar power market in 2025. The Middle East solar power market size for PV surpassed 30 GW in 2026, outpacing every other generation source on new-build economics. TOPCon efficiencies above 25% and bifacial gains around 12% are lowering land-use intensity and capex per watt. JinkoSolar’s 10 GW Saudi venture has already pre-sold production to ACWA Power’s Haden and Al-Khushaybi projects, locking in offtake through the decade.

Concentrated solar power clings to a 3.5% niche share but is projected to expand at a 30.44% CAGR to 2031. Dubai’s 950 MW MBR Phase 4 remains the flagship, combining 700 MW of CSP with 250 MW of PV and 5,907 MWh molten-salt storage. CSP’s USD 4,500–5,500/kW price tag confines replication to hybrid projects or mandates for local heliostat manufacturing. Battery-paired PV now beats CSP on levelized cost in almost every scenario, steering future capacity toward photovoltaics inside the Middle East solar power market.

By Grid Type: Distributed Microgrids Expand Beyond the Utility Perimeter

On-grid assets held 90.2% of installed capacity in 2025, kept dominant by multi-GW tenders that secure 20–25-year PPAs denominated in U.S. dollars. Yet the off-grid slice shows a 24.3% CAGR through 2031. Mining operations in Oman and telecom towers in Saudi Arabia deploy containerized solar-plus-storage systems that shave diesel use by up to 80%. Data-center developers in UAE free zones adopt 50–100 MW microgrids to bypass lengthy interconnection queues, illustrating how reliability needs override grid dependence.

The Middle East solar power market size for off-grid applications is projected to eclipse 7 GW by 2031 as corporate PPAs proliferate. Qatar’s BeSolar program rewards rooftop exports at QAR 0.237/kWh, spurring oversizing for excess generation. Household arrays in Dubai now connect within 30 days and zero upfront fees under the revamped Shams Dubai process.[4]DEWA Media Center, “Shams Dubai Connection Guidelines 2024,” dewa.gov.ae These design-to-export models reposition the grid as virtual storage and embed new growth lanes for distributed solar.

By End-User: Residential Uptake Quickens Amid Policy Tailwinds

Utility-scale plants accounted for 68.8% of the Middle East solar power market share in 2025, a dominance linked to economies of scale and low tariffs. ACWA Power’s twin 3 GW projects highlight how bulk procurement locks in module supply at preferential rates. However, residential volume is rising 22.5% annually as net-metering simplifications offset low retail tariffs. Dubai’s streamlined application, Qatar’s feed-in tariff, and Jordan’s increasing self-consumption caps expand addressable rooftops.

Commercial and industrial customers occupy a sweet spot between scale and autonomy. Yellow Door Energy’s 350 MW regional book demonstrates how third-party ownership eliminates capex barriers. EMSTEEL’s 31.5 MW rooftop in Sharjah delivers a 20% tariff discount, while district-cooling operator Emicool integrates 1.2 MW to shave afternoon peaks. Such examples reinforce the structural shift from utility mediation to direct bilateral models inside the Middle East solar power market.

Geography Analysis

Saudi Arabia commanded 38.17% of installed capacity in 2025 and is forecast to grow at a 30.6% CAGR through 2031, underpinned by a 130 GW renewable target and ongoing Saudi Arabia solar energy expansion. Round 6’s 4.5 GW award at sub-1.1 US cents/kWh cemented tariff leadership and validated the kingdom’s domestic-content strategy. Localized cell output from JinkoSolar and Desert Technologies reduces supply risk, while NEOM’s hydrogen hub locks in 4 GW captive demand. Grid congestion in the Eastern Province persists, but SEC’s 7.8 GWh storage order signals remediation.

The United Arab Emirates ranks second in cumulative capacity and accelerates dispatchable solar through Masdar’s 5.2 GW PV-plus-19 GWh battery complex, targeting 1 GW firm output by 2027. Dubai’s 950 MW MBR Phase 4 hybrid and Engie–Masdar’s 1.5 GW Khazna project broaden the asset mix. Rooftop uptake benefits from Shams Dubai’s faster approvals, while C&I PPAs add over 30 MW yearly, led by Yellow Door Energy. The UAE’s balanced portfolio and proactive storage procurement keep penetration rates above 25% of daytime demand.

Oman, Kuwait, Qatar, Bahrain, Jordan, and Israel round out the market. Oman’s Ibri III and Al Kamil Wal Wafi tenders aim at 4 GW by 2030; Kuwait’s Al Dibdibah faces a protracted grid build-out; Qatar’s 875 MW Industrial Cities array feeds both local clusters and UAE exports; Bahrain leverages public institutions for distributed solar; Jordan’s Project Prosperity hinges on sovereign guarantees; Israel secures 600 MW from Jordan in exchange for desalinated water. Rest-of-region states such as Iraq, Lebanon, and Yemen remain small due to political risk, yet grid interconnection plans hold latent upside for the Middle East solar power market.

Competitive Landscape

The Middle East solar power market exhibits moderate fragmentation. ACWA Power and Masdar dominate utility-scale tenders, yet the combined share of the top five IPPs sits near 40%. ACWA Power’s 1.2 GW Haden and 1.8 GW Al-Khushaybi projects illustrate advantages from early module offtake agreements with JinkoSolar. Masdar scales regionally with the 5.2 GW battery-backed complex in Abu Dhabi and partnerships in Oman and Bahrain.

Chinese OEMs supply over 70% of modules. JinkoSolar’s 10 GW Saudi factory and Trina Solar’s 3 GW tracker plant deepen localization, cutting landed costs by 8%–12% and satisfying domestic-content rules. Desert Technologies complements capacity with a 5 GW TOPCon line. Inverters are led by Sungrow, whose 7.8 GWh Saudi storage win and SG150CX launch position the firm for the high-growth C&I niche.

White-space opportunities lie in distributed generation and O&M automation. Yellow Door Energy showcases third-party ownership models that bridge the financing gap for C&I customers. Robotic cleaning suppliers NOMADD and Ecoppia tackle soiling, while Aramco prototypes aim for mass affordability. Tracker specialists Nextracker, Arctech, and Array Technologies jostle for market share through joint ventures with local fabricators. Overall, supply polarization between state-backed IPPs and agile distributed players shapes competitive dynamics inside the Middle East solar power market.

Middle East Solar Power Industry Leaders

ACWA Power

Masdar

JinkoSolar

First Solar

Longi Solar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ENGIE has successfully achieved financial closure on its most ambitious solar endeavor to date: the 1.5-gigawatt Khazna Solar Park located in Abu Dhabi.

- December 2025: Acwa Power, along with Water and Electricity Holding Company (Badeel) and Saudi Aramco Power Company, all based in Riyadh, have reached a financial milestone for five solar and two wind projects in Saudi Arabia. These seven projects, boasting a combined capacity of 15 GW, successfully obtained a senior debt facility of USD 5.9 billion, backed by a consortium of local, regional, and international banks.

- October 2025: Saudi Arabia has inked renewable energy contracts exceeding SAR 9 billion (USD 2.4 billion). The Saudi Power Procurement Company, overseeing the initiative, has distributed these contracts across five projects: four solar and one wind, collectively boasting a capacity of 4,500 megawatts.

- January 2025: Masdar, the Emirati state-owned renewable investment firm, has joined forces with EWEC to construct a massive solar and battery energy storage (BESS) facility. This ambitious project will integrate 5.2 GW of solar power with 19 GWh of battery storage, aiming to deliver a steady output of 1 GW of renewable energy.

Middle East Solar Power Market Report Scope

Solar power means using the sun's energy to produce electricity, either directly as thermal energy (heat) or indirectly through photovoltaic cells in solar panels and clear photovoltaic glass.

The Middle East solar power market is segmented by technology, grid type, end-user, and geography. By technology, the market is segmented into solar photovoltaic and concentrated solar power. By grid type, the market is segmented into on-grid and off-grid systems. By end-user, the market is segmented into utility-scale, commercial and industrial, and residential installations. The report also covers the market sizes and forecasts for the Middle East solar power market across key countries in the region, including Saudi Arabia, the United Arab Emirates, Oman, Kuwait, Qatar, Bahrain, Jordan, Israel, and the rest of the Middle East. For each segment, the market sizing and forecasts have been carried out on the basis of installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Oman |

| Kuwait |

| Qatar |

| Bahrain |

| Jordan |

| Israel |

| Rest of Middle East |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Oman | |

| Kuwait | |

| Qatar | |

| Bahrain | |

| Jordan | |

| Israel | |

| Rest of Middle East |

Key Questions Answered in the Report

How large is the Middle East solar power market in 2026?

Installed capacity reaches 31.91 GW in 2026 with an 18.56% CAGR expected to lift it to 74.75 GW by 2031.

Which country leads current regional capacity?

Saudi Arabia holds 38.17% of installed capacity and targets 130 GW of renewables before 2030.

What technology dominates new installations?

Photovoltaic systems account for 96.5% of capacity and benefit from TOPCon cells exceeding 25% efficiency.

How fast are off-grid systems growing?

Off-grid deployments show a 24.3% CAGR through 2031 as industrial clusters and data centers adopt solar-plus-storage microgrids.

What is the outlook for green-hydrogen projects?

Facilities like NEOM’s 600 t/day plant pair multi-GW solar arrays with electrolyzers, creating long-term captive demand for regional solar.

Page last updated on: