Middle East Geospatial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

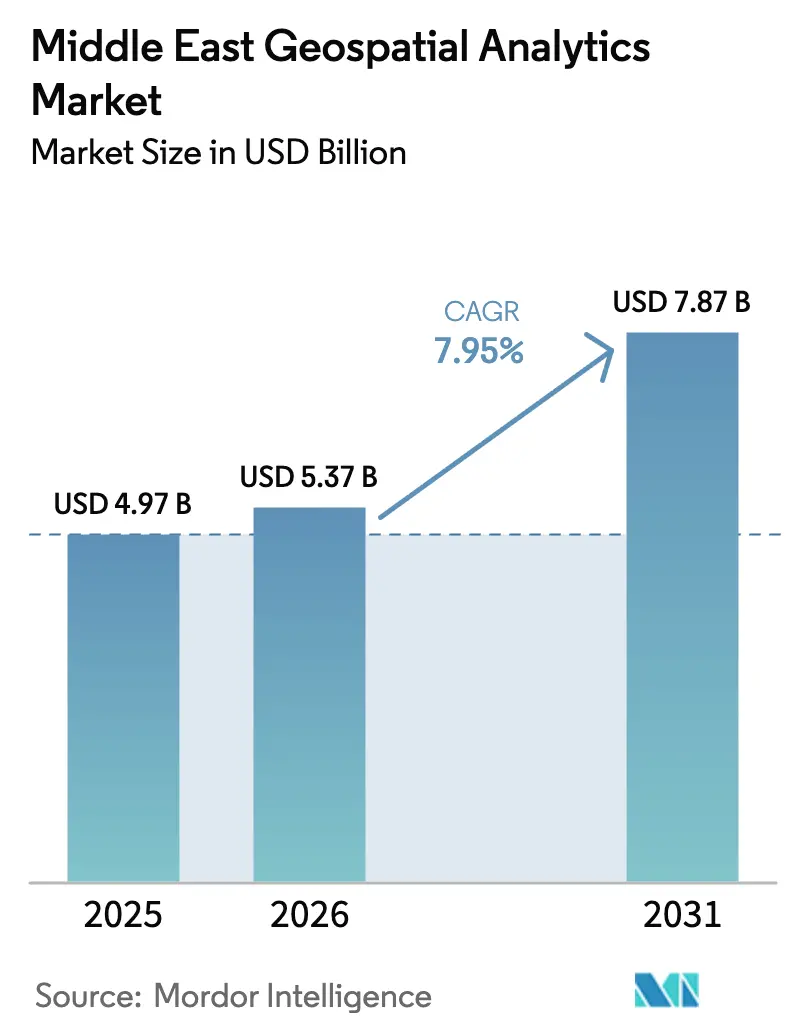

| Base Year Market Size (2025) | USD 4.97 Billion |

| Market Size (2026) | USD 5.37 Billion |

| Market Size (2031) | USD 7.87 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

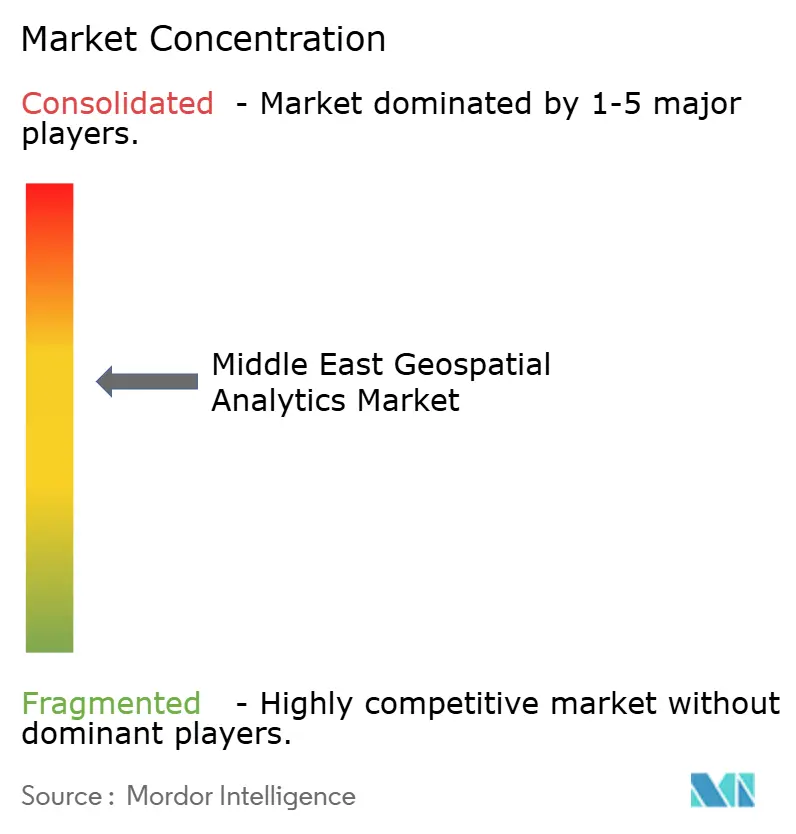

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Geospatial Analytics Market Analysis by Mordor Intelligence

The Middle East Geospatial Analytics Market size was valued at USD 4.97 billion in 2025 and estimated to grow from USD 5.37 billion in 2026 to reach USD 7.87 billion by 2031, at a CAGR of 7.95% during the forecast period (2026-2031). Accelerated smart-city programs, massive public-sector digital-twin projects, and sovereign data-center investments are reinforcing demand for spatial intelligence platforms. Government modernization agendas such as Saudi Arabia’s Vision 2030 and the UAE’s National AI Strategy 2031 are allocating multibillion-dollar budgets that anchor technology adoption in construction, utilities, mining, and defense. Rapid cloud build-outs, exemplified by a 36% annual increase in AI infrastructure spending in the UAE, are lowering entry barriers for smaller enterprises while creating scale for edge-enabled processing. [1]Gulf Construction Editorial, “Building for AI: A Race Against Time,” Gulf Construction, gulfconstructiononline.com Competitive intensity is heightening as global geospatial software vendors face cloud hyperscalers and a wave of UAE free-zone geo-AI start-ups. Persistent skills shortages in deep-learning GIS, plus the rising cost of LiDAR and synthetic-aperture-radar sensors, act as structural constraints that could temper project roll-outs.

Key Report Takeaways

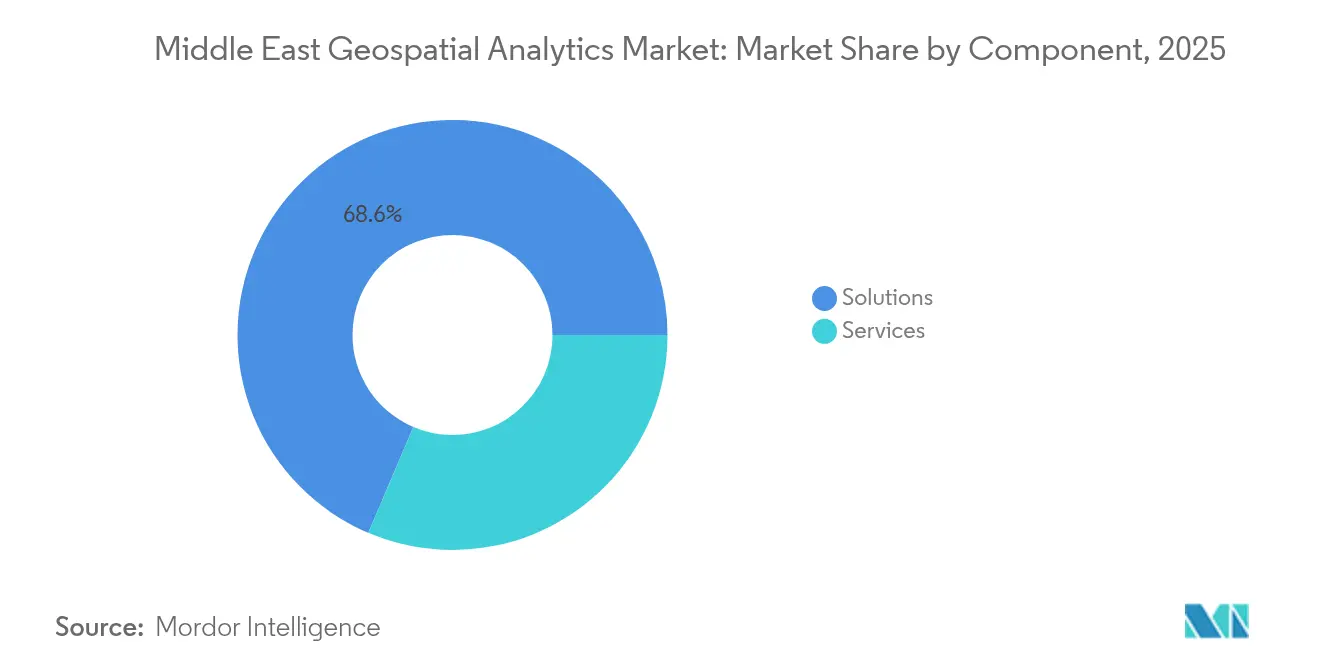

- By component, solutions led with 68.60% of the Middle East geospatial analytics market share in 2025, while services are expanding at an 11.05% CAGR through 2031.

- By analytics type, descriptive analytics accounted for 43.25% revenue share in 2025; prescriptive analytics is set to grow at a 10.28% CAGR to 2031.

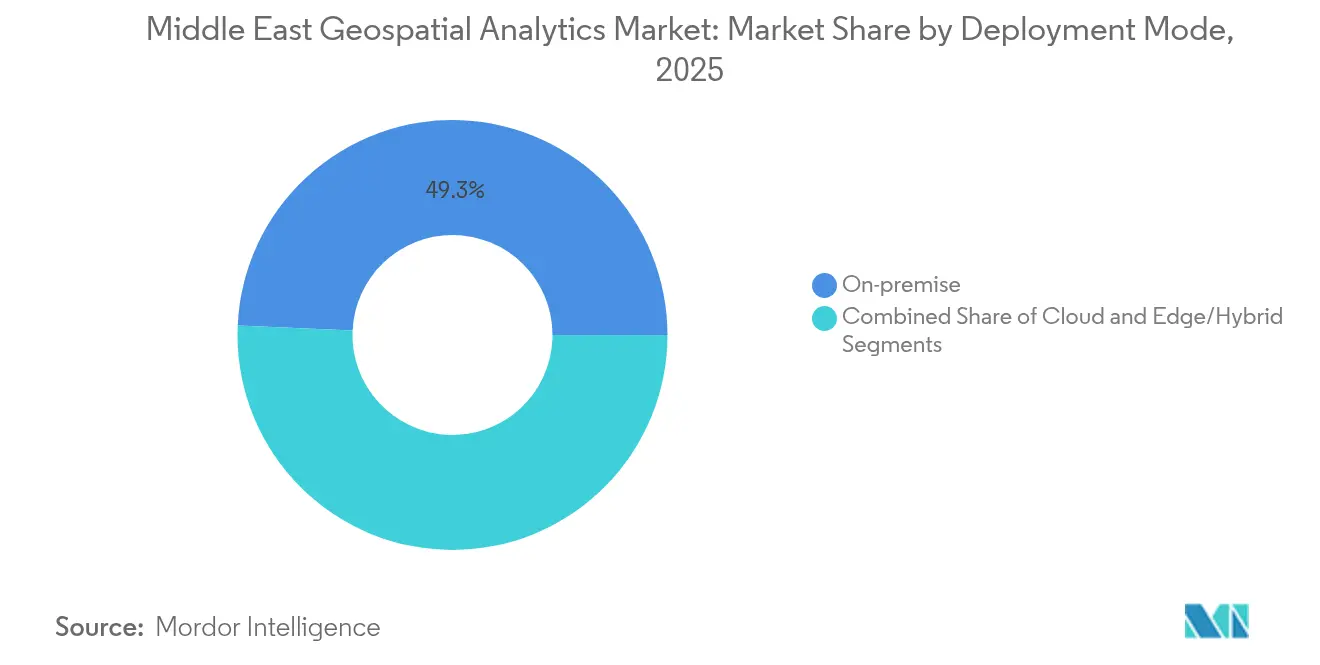

- By deployment mode, on-premise systems held 49.30% share of the Middle East geospatial analytics market size in 2025, whereas cloud deployments are projected to rise at an 11.18% CAGR over the forecast period.

- By application, imagery and remote-sensing analytics captured 33.55% revenue share in 2025, and geovisualization and 3-D modeling are forecast to expand at a 10.57% CAGR through 2031.

- By end-user industry, government and municipalities commanded a 28.65% share in 2025, while utilities and energy lead growth at a 10.33% CAGR.

- By country, Saudi Arabia held a 41.25% share in 2025, and Qatar is poised for the fastest 10.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Dynamics observed within Middle east present a holistic view when set against the broader international context. The geospatial analytics market analysis by Mordor Intelligence provides that expanded global perspective.

Middle East Geospatial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging smart-city programs across GCC | +2.1% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Mandated satellite-based cadastral modernization | +1.8% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Rapid cloud-GIS migration by utilities | +1.5% | GCC countries, Turkey | Short term (≤ 2 years) |

| 5G-enabled edge analytics roll-outs | +1.4% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Rise of geo-AI startups in UAE free zones | +0.9% | UAE (regional spill-over) | Short term (≤ 2 years) |

| Oil-to-non-oil economic diversification projects | +1.3% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Smart-City Programs Across GCC

Gulf megaprojects are hard-wiring geospatial analytics into urban-management architectures. Dubai’s 2040 Urban Master Plan doubles green areas while targeting a population of 7.8 million, demanding real-time spatial modelling for the “20-minute city” concept. [2]Arab Urban Development Institute Team, “Projects—Urban Master Plan 2040,” Arab Urban Development Institute, araburban.org Saudi Arabia’s partnership with Naver is delivering 10-cm resolution 3-D twins for Riyadh and four additional cities, enabling flood simulation and infrastructure optimisation. The USD 2.5 billion Aion Sentia platform in the UAE integrates AI-driven spatial data to orchestrate city services end-to-end. These projects create predictable, multi-year demand for high-volume imagery ingestion, advanced routing analytics, and predictive maintenance models inside the Middle East geospatial analytics market.

Mandated Satellite-Based Cadastral Modernization

New land-registration statutes require sub-meter accuracy and audit trails, pushing agencies toward cloud-enabled spatial data infrastructures. Saudi Arabia’s draft Global AI Hub Law outlines “Private,” “Extended,” and “Virtual” hubs, formalising sovereign hosting while enabling cross-border cadastral integration. The UAE’s MBZ-SAT will lift domestic earth-observation capacity, accelerating update cycles for parcel databases. Kuwait demonstrates downstream value: its utilities ministry cut service-connection times after embedding cadastral layers into a GIS workflow. Standardised cadastral basemaps unlock richer analytics in taxation, infrastructure planning, and environmental monitoring.

Rapid Cloud-GIS Migration by Utilities

Utilities adopt distributed clouds to process petabyte-scale sensor feeds without high on-premise capital outlays. Aramco’s partnership with Microsoft and Armada has deployed the world’s first industrial distributed cloud, combining edge nodes with regional hyperscale zones to automate safety monitoring of energy assets. Etisalat leverages 5G edge computing with Intel and Lenovo to serve low-latency utility IoT workloads. Similar projects across Kuwait’s Digital Integrated Field prove that private-cloud GIS trims data-ingestion delays and improves asset-lifecycle visibility. The Middle East geospatial analytics market benefits as utilities outsource complex model management to managed-service providers.

5G-Enabled Edge Analytics Roll-Outs

Coverage expansion and a dense micro-data-center footprint reduce round-trip latency to milliseconds, vital for autonomous systems and situational awareness. Qualcomm and e& inaugurated an Abu Dhabi engineering center to co-design 5G edge-AI gateways for smart mobility and industrial automation. Saudi Telecom Company’s 54.7% population coverage supports more than 25 tier-III data centers, delivering the backhaul critical for high-frequency geolocation updates. These infrastructures embed real-time geospatial processing into field operations, deepening market penetration in logistics, oil, and public safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geospatial-data sovereignty regulations | -1.2% | Saudi Arabia, UAE, regional spillover | Medium term (2-4 years) |

| Skilled-talent shortage for deep-learning GIS | -1.8% | Regional, acute in UAE and Saudi Arabia | Long term (≥ 4 years) |

| Fragmented legacy cadastral datasets | -1.1% | Saudi Arabia, UAE, Oman, Turkey | Long term (≥ 4 years) |

| High LiDAR and SAR acquisition costs | -0.9% | Global, particularly affecting smaller regional players | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Geospatial-Data Sovereignty Regulations

Fragmented localisation mandates elevate compliance overheads for multinational deployments. Saudi Arabia’s draft Global AI Hub Law prescribes three distinct hosting archetypes with divergent audit obligations, complicating regional data-lake architectures. The UAE’s localisation rules force foreign providers to build local points of presence or enter joint ventures, lengthening deployment timelines. Intensifying Chinese hyperscaler expansion in the Gulf introduces geopolitical scrutiny over platform selection and encryption standards. These dynamics squeeze smaller vendors and prolong procurement cycles within the Middle East geospatial analytics market.

Skilled-Talent Shortage for Deep-Learning GIS

The gap in AI-ready geospatial engineers drives salary inflation and project delays. CIO reports persistent ICT skill deficits that risk billions in unrealised regional output. Saudi Arabia’s plan to up-skill 1,000 engineers under Vision 2030 and the UAE’s “One Million Arab Coders” initiative illustrate long-term remediation, yet specialised geo-AI curricula remain scarce. AgFunder highlights shortages in climate-smart-agriculture technologists, signaling how niche verticals struggle even more acutely. A thinner talent pipeline slows adoption of advanced analytics modules and increases dependency on external service firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gaining Momentum

Solutions continued to dominate the Middle East geospatial analytics market with a 68.60% share in 2025, reflecting entrenched investments in software suites and sensor hardware. However, the services segment is expanding at an 11.05% CAGR as ministries and enterprises outsource integration, model training, and 24/7 managed analytics. Regional shortages in deep-learning GIS specialists make vendor-delivered professional services the pragmatic route for rapid roll-out. Governments favour turnkey frameworks that bundle data-ingestion pipelines, sovereign cloud hosting, and Arabic language interfaces.

Service providers leverage strategic alliances to deepen vertical intimacy. Bentley Systems integrated Google geospatial content to deliver richer context within digital-twin workflows, underpinning infrastructure-as-a-service offerings. Managed-service portfolios now include continuous satellite imagery updates, AI model retraining, and cyber-resilience audits. This evolution positions the services cohort to capture rising OPEX budgets as the Middle East geospatial analytics market prioritises speed over in-house capability building.

By Analytics Type: Prescriptive Analytics Advancing

Descriptive analytics retained 43.25% revenue share in 2025 by providing dashboards and historical pattern recognition across land, asset, and population datasets. Yet prescriptive analytics is growing 10.28% annually, propelled by demand for automated optimisation in traffic orchestration, energy load balancing, and emergency-response routing. Defence conglomerate EDGE unveiled an AI-enabled geospatial platform able to recommend and auto-execute mission-critical manoeuvres, underscoring momentum toward action-oriented engines.

Organisations move through a maturity curve starting with descriptive and evolving to predictive, diagnostic, and finally prescriptive; budget allocations increasingly prioritise the latter stages. Confidence in AI explainability, combined with 5G edge connectivity, allows decision loops to compress from minutes to seconds, boosting market penetration for higher-value analytics tiers within the Middle East geospatial analytics market.

By Deployment Mode: Cloud Transformation Accelerating

On-premise architectures accounted for 49.30% of the Middle East geospatial analytics market size in 2025, mirroring historical preferences for data-sovereign control. Cloud deployments, however, are scaling at an 11.18% CAGR as hyperscale build-outs across the GCC foster elastic compute economics. Saudi Arabia’s data-center pipeline—projected to reach USD 15.9 billion by 2030—offers low-latency colocation that meets stringent localisation rules while retaining hyperscale flexibility.

Edge and hybrid models combine in-country micro-DCs with regional cores, catering to latency-sensitive mining and oilfield scenarios. Utilities adopt distributed clouds to host geofenced digital twins, satisfying regulators yet enjoying consumption-based pricing. This convergence of compliance and cloud economics propels the Middle East geospatial analytics market toward an infrastructure-agnostic paradigm.

By Application: Geovisualization and 3-D Modeling Emerging

Imagery and remote-sensing analytics led with a 33.55% share in 2025, validating the primacy of multispectral and SAR data streams for asset monitoring and land-use mapping. Geovisualization and 3-D modeling are the fastest-growing applications at 10.57% CAGR, catalysed by mega-projects like NEOM and digital-twin mandates across transport corridors. Live, immersive models support construction sequencing, underground-utility clash detection, and urban-heat-island mitigation.

The Dubai Metro digital twin improves passenger-flow simulations, while Saudi projects achieve 10-cm positional accuracy for flood-risk analytics. Advancements in GPU-accelerated rendering and cloud-native scene services let planners manipulate terabyte-scale point clouds through browser interfaces. These capabilities expand addressable use cases and reinforce the trajectory of the Middle East geospatial analytics market.

By End-user Industry: Utilities and Energy Transformation

Public administrations remained the largest customers, securing 28.65% of 2025 revenue due to cadastral modernisation, smart surveillance, and emergency-response optimisation. Utilities and energy companies record the highest 10.33% CAGR as they retrofit networks for renewables integration and predictive maintenance. Aramco’s distributed cloud enables millisecond-level leak detection, while Kuwait’s utilities ministry shortened connection cycles after a GIS overhaul.

The Middle East geospatial analytics market benefits from decarbonisation agendas that require spatial optimisation of solar assets, hydrogen pipelines, and EV-charging nodes. Sector-specific modules now include corrosion-risk heatmaps and dynamic load-balancing algorithms, underpinning higher subscription renewals and multi-year managed-services contracts.

Geography Analysis

Saudi Arabia commanded 41.25% of the Middle East geospatial analytics market in 2025 as Vision 2030 funded smart-city, mining, and defence modernisation on an unprecedented scale. A dedicated USD 100 billion AI allocation and an additional USD 40 billion investment vehicle support satellite programs and sovereign cloud zones. NEOM’s adaptive-twin architecture and a mining roadmap chasing USD 75 billion GDP contribution by 2035 secure long-run project pipelines.

The UAE positions itself as an AI innovation nucleus through MBZ-SAT, Space42, and heavy 5G backhaul, accelerating adoption across defence, urban planning, and logistics. Dubai’s 2040 master plan underpins continuous demand for terrain deformation analysis and green-space optimisation. Abu Dhabi’s sovereign wealth fund backing of edge-AI start-ups fills white spaces in predictive geospatial intelligence offerings. Collectively, these initiatives deepen the UAE’s strategic share of the Middle East geospatial analytics market.

Qatar is forecast to log an 10.88% CAGR through 2031, buoyed by FIFA World Cup infrastructure repurposing and National Vision 2030 digitisation goals. Showcases such as “Qatar GIS of the Future” highlight the government's appetite for high-resolution satellite data integration. Turkey, Oman, and Bahrain promote complementary growth. Turkey’s industrial base generates sustained imagery demand, while Oman nurtures a space-accelerator programme that feeds regional supply chains. The evolving space economy across Asia and the Gulf broadens cross-border collaboration prospects, reinforcing the scale of the Middle East geospatial analytics market.

Coverage of the geospatial analytics market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Africa, alongside detailed country-level intelligence for United Arab Emirates, Saudi Arabia, Israel, Nigeria, Canada, South Korea, India, and Brazil, each shaped by local operating conditions.

Competitive Landscape

The competitive arena displays moderate fragmentation. Incumbents such as Esri, Hexagon, and Trimble leverage decades-old ecosystems, whereas cloud hyperscalers add geospatial capability through API portfolios and acquisitions. Microsoft’s Azure Orbital, Google’s Earth Engine, and Amazon Location Services embed spatial analytics into broader developer toolkits, pressuring traditional license models. Meanwhile, regional specialists like Bayanat commercialise sovereign datasets and AI pipelines tailored to Arabic semantics and local compliance contexts. [4]Bayanat Product Team, “AI-Powered Predictive Geospatial Intelligence,” Bayanat, bayanat.ai

Edge-computing differentiation is intensifying. Telecommunications carriers co-develop spatial SDKs with chipset firms to package low-latency analytics for drones, autonomous trucks, and critical-event monitoring. Qualcomm’s collaboration with e& illustrates hardware-software convergence that incumbents must match. In addition, procurement criteria increasingly reward adherence to sovereign-cloud statutes, pushing vendors to certify data-center residencies and encryption schemes.

Mergers and venture-backed alliances accelerate feature expansion: Maxar deepened 3-D city-mesh production via Blackshark.ai, and Bentley-Google integration streamed point-cloud context into engineering workflows. As talent remains scarce, vendors bundle training academies and low-code modelling to lock in customer bases. Collectively, these dynamics sustain a vibrant yet contested Middle East geospatial analytics market.

Middle East Geospatial Analytics Industry Leaders

Esri Inc.

Hexagon AB

Trimble Inc.

Bentley Systems Inc.

Maxar Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Qualcomm and e& formed a strategic alliance to advance 5G edge-AI solutions, opening an Abu Dhabi engineering center for energy, manufacturing, and logistics use cases.

- May 2025: The Mohammed bin Rashid Space Centre announced Geo-Spatial Week 2025 to showcase regional spatial analytics innovation.

- February 2025: EDGE launched an AI-powered geospatial intelligence platform at IDEX 2025, targeting defence and security clients.

- February 2025: Bold Technologies confirmed a USD 2.5 billion budget for the Aion Sentia cognitive city platform, scheduled for 2027 completion.

- February 2025: NSG detailed satellite expansion plans to reinforce Saudi Arabia’s space economy and spatial analytics capacity.

- January 2025: NSG and Esri announced a partnership to accelerate geospatial innovation within Saudi Arabia.

- January 2025: Maxar expanded 3-D geospatial capabilities through collaboration with Blackshark.ai.

- October 2024: Bentley Systems partnered with Google to inject advanced geospatial context into infrastructure engineering software.

Middle East Geospatial Analytics Market Report Scope

Geospatial analytics is acquiring, manipulating, and displaying imagery and data from the geographic information system (GIS), such as satellite photos and GPS data. The specific identifiers of a street address and a zip code are used in geospatial data analytics. They are used to create geographic models and data visualizations for more accurate trends modeling and forecasting.

The Middle East geospatial analytics market is segmented by type (surface analysis, network analysis, geovisualization), by end user vertical (agriculture, utility and communication, defence and intelligence, government, mining and natural resources, automotive and transportation, healthcare, real estate, and construction), by country (United Arab Emirates, Turkey, Saudi Arabia). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Solutions |

| Services |

| Descriptive Analytics |

| Diagnostic Analytics |

| Predictive Analytics |

| Prescriptive Analytics |

| On-premise |

| Cloud |

| Edge/Hybrid |

| Surface and Terrain Analysis |

| Network and Route Analysis |

| Geovisualization and 3-D Modelling |

| Imagery and Remote-Sensing Analytics |

| Defense and Intelligence |

| Government and Municipalities |

| Utilities and Energy |

| Agriculture and Environment |

| Transportation and Logistics |

| Real Estate and Construction |

| Mining and Natural Resources |

| Healthcare and Public Health |

| Other End-user Industries |

| United Arab Emirates |

| Saudi Arabia |

| Turkey |

| Qatar |

| Oman |

| Rest of Middle East |

| By Component | Solutions |

| Services | |

| By Analytics Type | Descriptive Analytics |

| Diagnostic Analytics | |

| Predictive Analytics | |

| Prescriptive Analytics | |

| By Deployment Mode | On-premise |

| Cloud | |

| Edge/Hybrid | |

| By Application | Surface and Terrain Analysis |

| Network and Route Analysis | |

| Geovisualization and 3-D Modelling | |

| Imagery and Remote-Sensing Analytics | |

| By End-user Industry | Defense and Intelligence |

| Government and Municipalities | |

| Utilities and Energy | |

| Agriculture and Environment | |

| Transportation and Logistics | |

| Real Estate and Construction | |

| Mining and Natural Resources | |

| Healthcare and Public Health | |

| Other End-user Industries | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Qatar | |

| Oman | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current value of the Middle East geospatial analytics market?

The market stands at USD 5.37 billion in 2026 and is forecast to reach USD 7.87 billion by 2031.

Which country leads regional demand?

Saudi Arabia accounts for 41.25% of revenue, buoyed by Vision 2030 and large-scale digital-twin investments.

Which segment is growing the fastest?

Cloud deployment shows the highest 11.18% CAGR because sovereign data-center build-outs are easing localisation concerns.

Why are services expanding rapidly?

Acute shortages in deep-learning GIS skills push organisations to outsource integration and model management, driving an 11.05% CAGR in services revenue.

How are smart-city projects influencing the market?

Megaprojects like Dubai’s Urban Master Plan and Saudi digital-twin initiatives demand continuous geovisualisation, accelerating platform subscriptions and 3-D modelling adoption.

What is the primary restraint on market growth?

Fragmented data-sovereignty regulations raise compliance costs and elongate deployment timelines, reducing the overall market CAGR by an estimated 1.2%.

Page last updated on: