Saudi Arabia Geospatial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

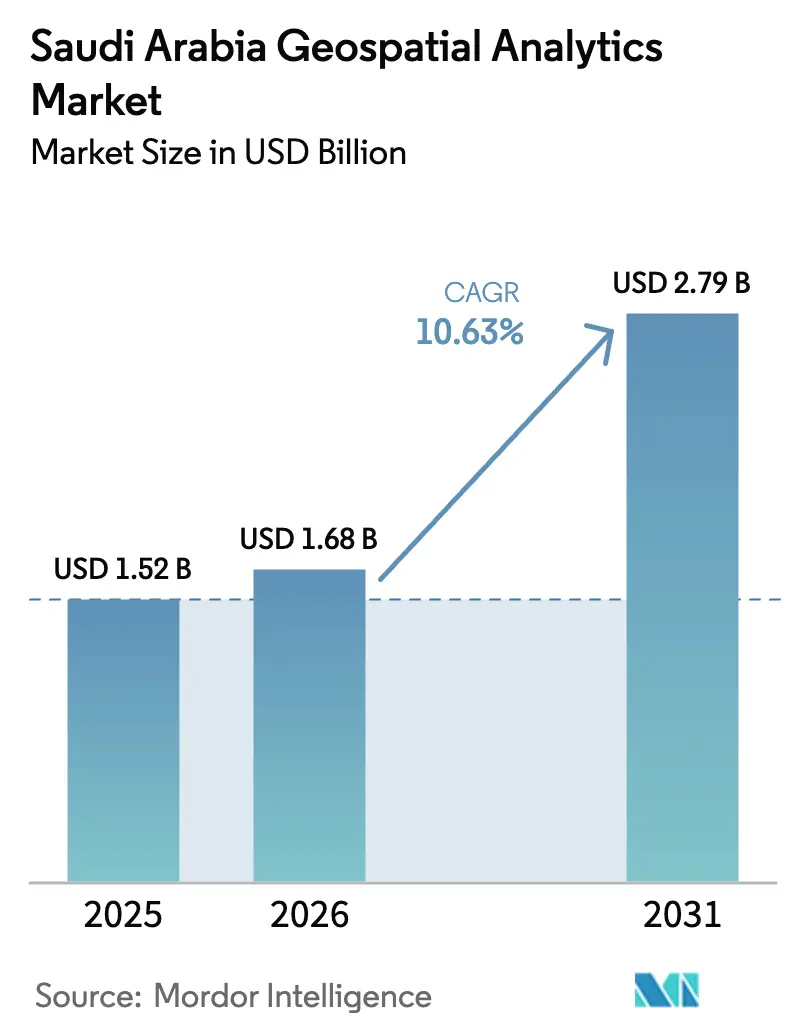

| Base Year Market Size (2025) | USD 1.52 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 10.63% CAGR |

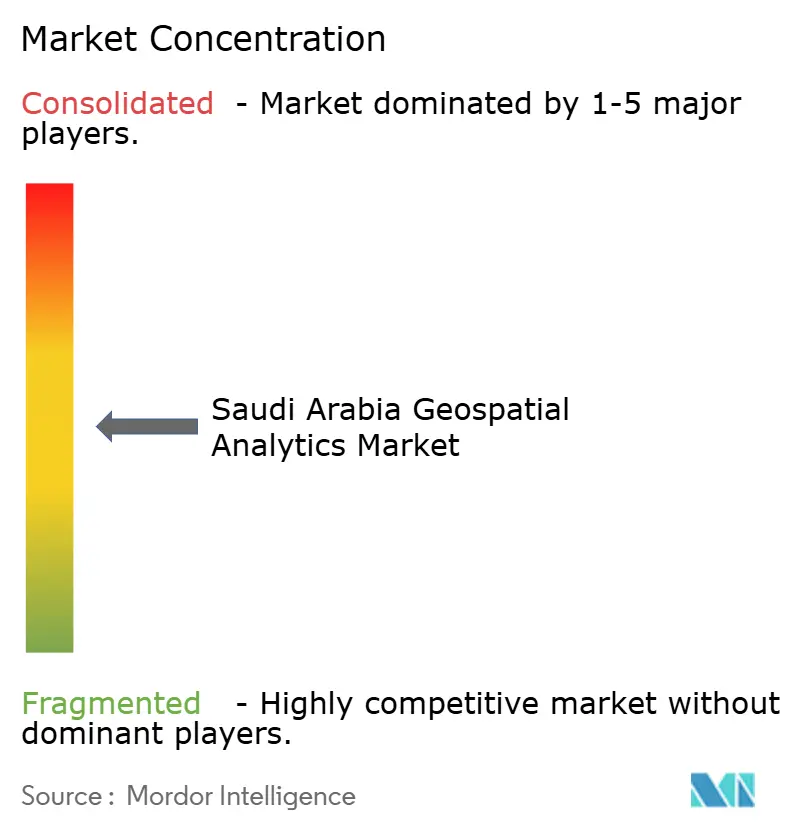

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Geospatial Analytics Market Analysis by Mordor Intelligence

The Saudi Arabia geospatial analytics market size in 2026 is estimated at USD 1.68 billion, growing from 2025 value of USD 1.52 billion with 2031 projections showing USD 2.79 billion, growing at 10.63% CAGR over 2026-2031. Momentum stems from Vision 2030 smart-city mandates, public-sector digitization, and a nationwide shift toward cloud-first spatial infrastructures. The Saudi Arabia geospatial analytics market continues to benefit from hyperscale data-center roll-outs that lower the total cost of ownership and from abundant Earth-observation data that unlock real-time monitoring use cases. Rising commercial demand, especially in retail and logistics, signals diversification beyond governmental projects. Moderate market concentration encourages technology partnerships, while the Personal Data Protection Law sets a strict compliance baseline that shapes deployment choices.[1]Ministry of Finance KSA, “Saudi Ministry of Finance Announces Budget Statement for FY 2025,” mof.gov.sa

Key Report Takeaways

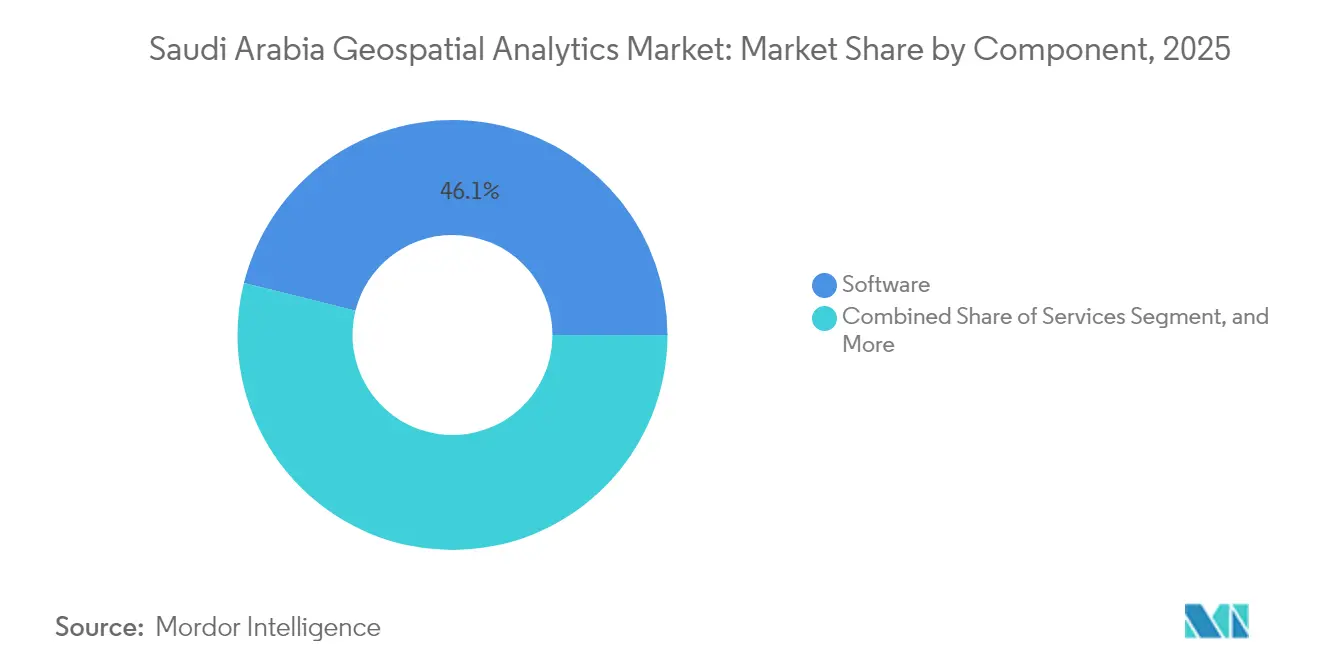

- By component, software led with 46.12% revenue share of the Saudi Arabia geospatial analytics market in 2025; data and content are projected to expand at a 11.78% CAGR through 2031.

- By type, surface analysis accounted for 45.15% of the Saudi Arabia geospatial analytics market share in 2025, while spatial data mining and predictive modeling are advancing at a 12.18% CAGR through 2031.

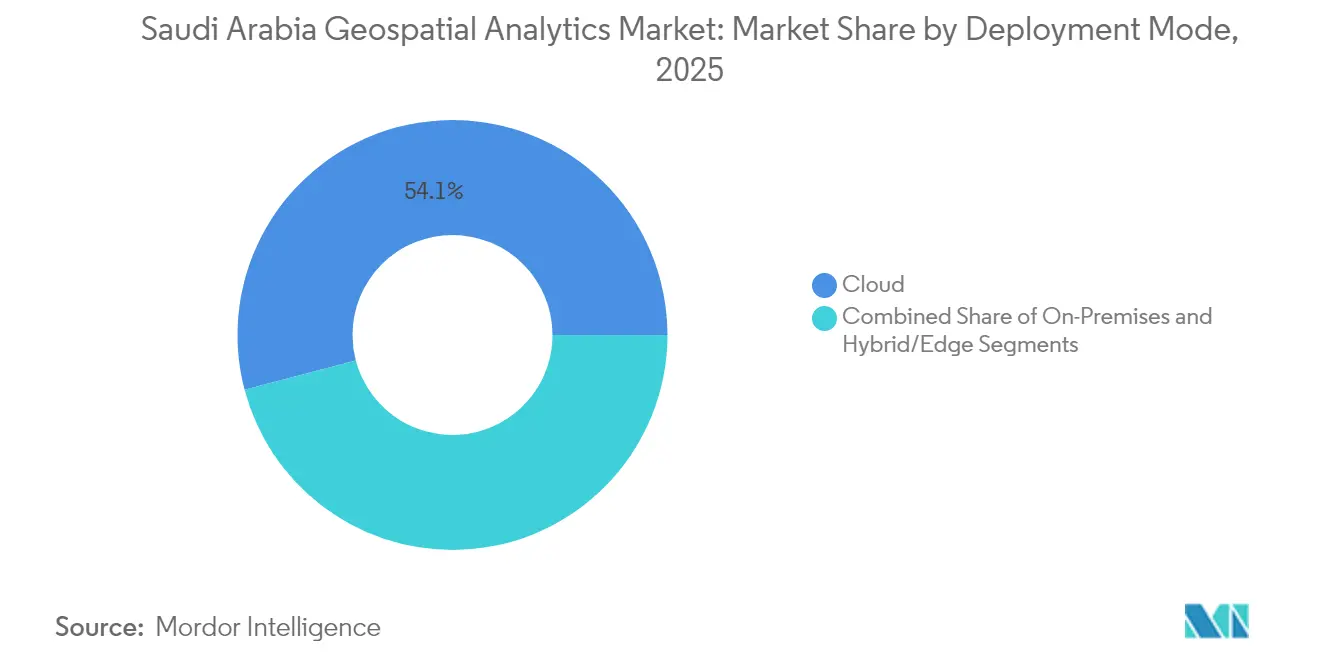

- By deployment mode, cloud captured 54.10% of the 2025 revenue of the Saudi Arabia geospatial analytics market and is growing at an 11.55% CAGR through 2031.

- By data source, satellite and aerial imagery commanded 44.62% of demand in 2025 of the Saudi Arabia geospatial analytics market; mobile and social-media geo-data is set to rise at a 12.09% CAGR.

- By end-user vertical, government and smart-city authorities held 27.84% of the 2025 spending of the Saudi Arabia geospatial analytics market, whereas retail and location-based services are poised for a 12.52% CAGR.

- By region, the central region dominated with a 42.96% share of the Saudi Arabia geospatial analytics market in 2025, while the eastern region is projected to register the fastest 11.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Saudi arabia includes both locally based firms and those operating across multiple regions. The market landscape in the global geospatial analytics industry research shows how these players are arranged internationally.

Saudi Arabia Geospatial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 smart-city mandates | +2.8% | Central and Western | Long term (≥ 4 years) |

| Rapid cloud build-out | +2.1% | Central and Eastern | Medium term (2-4 years) |

| GIS adoption in megaprojects | +1.9% | Western and Central | Long term (≥ 4 years) |

| High-resolution EO and SAR access | +1.4% | National | Medium term (2-4 years) |

| National Geospatial Platform APIs | +1.2% | Central | Short term (≤ 2 years) |

| NSG–Esri GeoAI alliance | +0.9% | Central expanding national | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Smart-City Mandates Accelerating Demand for Location Intelligence

Vision 2030 allocates SAR 1.285 trillion in 2025 spending to development programs, driving large-scale adoption of geospatial analytics across NEOM, the Red Sea Project, and Qiddiya. NEOM’s linear urban design depends on continuous spatial modeling for infrastructure routing, environmental monitoring, and visitor services.[2]NEOM, “NEOM Official Website,” neom.com Ninety-seven percent of government services are now digitized, generating datasets that require location-based analysis. Utilities integrate geospatial analytics to manage smart grids, while the Saudi Green Initiative’s pledge to plant 10 billion trees by 2030 relies on spatial suitability modeling. These programs collectively embed geospatial thinking into national development, firmly anchoring the Saudi Arabian geospatial analytics market.

Rapid Cloud and Hyperscale Data-Center Build-Out Lowering TCO

Cloud providers have invested USD 2.5 billion in local data centers, establishing sovereign infrastructure that removes cross-border data-transfer bottlenecks.[3]fDi Intelligence, “Silicon Kingdom: Opening Doors for Global Business?” fdiintelligence.com The 2023 Cloud Computing Special Economic Zone offers tax incentives and localization clarity, encouraging organizations to migrate spatial workloads. Elastic compute capacity enables resource-intensive processes such as digital twins and AI-driven image analytics. Neo Space Group’s UP42 acquisition exemplifies how local firms leverage cloud platforms to scale on-demand analytics. Lower capital expenditure accelerates cloud adoption, reinforcing the leadership of cloud within the Saudi Arabian geospatial analytics market.

Widespread GIS Adoption in Utilities and Infrastructure Megaprojects

Utilities responsible for a USD 1.5 trillion construction pipeline use geospatial tools for asset siting, predictive maintenance, and route optimization. NEOM’s 100% renewable grid depends on spatial resource assessments; Saudi Aramco integrates geospatial analytics for pipeline integrity and environmental compliance. Water and Electricity Company projects employ location intelligence to shorten outage response times. Each deployment expands the installed base of spatial platforms, stimulating demand for services and high-resolution datasets across the Saudi Arabian geospatial analytics market.

Commercial Availability of High-Resolution EO Constellations and SAR Data

Local access to sub-meter imagery and SAR data improves coverage over dust-prone deserts and coastal areas. Ministries responsible for agriculture and environment now procure continuous monitoring datasets to support food security and land-rehabilitation programs. High revisit rates enable progress tracking for giga-projects, fueling the data-and-content segment’s double-digit growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front licensing and imagery costs for SMEs | -1.8% | Northern and Southern | Short term (≤ 2 years) |

| Geoprivacy and data-sovereignty constraints | -1.2% | National | Medium term (2-4 years) |

| GASGI permit cycles for UAV/LiDAR | -0.9% | National | Short term (≤ 2 years) |

| Scarcity of bilingual spatial-data scientists | -0.7% | Central and Eastern | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Licensing and Data-Acquisition Costs for SMEs

Enterprise GIS suites often require initial payments above USD 50,000, and premium satellite imagery packages add further expense. Cost burdens hinder smaller firms, especially in regions dominated by SMEs. SDAIA’s regulatory sandbox provides experimentation space, yet budget realities delay full-scale deployments. This capex hurdle slows broader ecosystem growth within the Saudi Arabia geospatial analytics market.

Geoprivacy and Data-Sovereignty Concerns

Personal Data Protection Law enforcement, since September 2024, imposes strict rules for geospatial datasets that can identify individuals. Cross-border transfers now need SDAIA contracts, and National Cybersecurity Authority controls add security overhead. International vendors must localize processing pipelines, extending project lead times and costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Anchor Market Growth

The Saudi Arabia geospatial analytics market size shows software solutions at a 46.12% share in 2025. Cloud-native GIS suites integrate seamlessly with national e-government backbones, allowing ministries to visualize assets and model growth scenarios. Vendors embed AI modules for automated feature extraction, aligning with the National Strategy for Data and AI. Data and content, growing at a 11.78% CAGR, benefit from expanded access to EO constellations and SAR feeds that address desert climate challenges.

Professional services flourish as agencies request customized dashboards and predictive models for megaproject oversight. Local providers such as Neo Space Group package imagery with analytics toolkits, reducing foreign-data dependency. Hardware and sensor demand remain steady, driven by IoT devices in smart grids and environmental monitoring stations. Together, these dynamics reinforce software leadership while showcasing the evolving component mix of the Saudi Arabia geospatial analytics market.

By Type: Surface Analysis Leads, Predictive Modeling Surges

Surface analysis held 45.15% Saudi Arabia geospatial analytics market share in 2025, reflecting heavy use in terrain modelling for construction and renewable-energy siting. Civil works teams overlay topography with engineering plans to reduce earth-moving costs. Spatial data mining and predictive modeling register a 12.18% CAGR as agencies apply machine learning to traffic flows, climate forecasts, and public-health surveillance.

Network and location analysis support logistics corridors that link Gulf ports with inland hubs. Geovisualization tools enable immersive 3D city twins used by NEOM planners to engage stakeholders. Government funding for AI research accelerates algorithm development, ensuring predictive modeling will capture a larger slice of the Saudi Arabia geospatial analytics market size over the forecast horizon.

By Deployment Mode: Cloud Extends Its Lead

Cloud captured 54.10% revenue in 2025 and is expanding at an 11.55% CAGR, making it the primary delivery model for the Saudi Arabia geospatial analytics market. Organizations deploy spatial workloads on Saudi-hosted instances of Azure, Google Cloud, and Oracle to meet localization mandates. Pay-as-you-go pricing lowers entry barriers and supports surge processing for remote-sensing imagery.

On-premises systems linger in defense and critical-infrastructure settings where air-gapped environments are mandatory. Hybrid and edge setups address real-time needs such as smart intersections that demand millisecond latency. As 5G coverage widens, edge nodes will process video analytics and LiDAR in situ, complementing rather than replacing centralized cloud pipelines.

By Data Source: Satellites Dominate, Mobile Data Gains Pace

Satellite and aerial imagery accounted for 44.62% of 2025 demand, underscoring reliance on overhead monitoring for gigaproject oversight. SAR sensors supply cloud-penetrating views essential for sandstorm-prone locales. The Saudi Arabia geospatial analytics market size linked to mobile and social-media geo-data is growing fastest at a 12.09% CAGR as anonymization frameworks permit retail and mobility analytics.

UAV-based LiDAR unlocks sub-centimeter mapping for heritage preservation and volumetric stockpile auditing, but GASGI permit timelines remain a bottleneck. Continuous feeds from IoT sensors in utilities, pipelines, and agriculture provide high-frequency updates that, when fused with satellite imagery, enable multi-scale decision workflows.

By End-User Vertical: Government Stronghold Meets Retail Upswing

Government and smart-city authorities generated 27.84% of 2025 spending, driven by Vision 2030 digital-service targets. Ministries depend on enterprise GIS to track infrastructure spend and environmental metrics. Retail and location-based services are projected to lead growth at a 12.52% CAGR as malls, quick-service restaurants, and e-commerce firms harness footfall analytics for site selection.

Utilities and energy enterprises employ geospatial analytics for grid optimization, while defense agencies demand high-security platforms. Agriculture programs use remote sensing to optimize irrigation in water-scarce zones, aligning with FAO-backed efficiency pilots. These diverse use cases broaden the Saudi Arabia geospatial analytics market beyond its public-sector foundation.

Geography Analysis

The central region, including Riyadh, held 42.96% 2025 share, cementing its status as the administrative and technological hub of the Saudi Arabia geospatial analytics market. The central region’s leadership in the Saudi Arabia geospatial analytics market derives from Riyadh’s concentration of ministries responsible for digital governance, procurement, and regulatory oversight. Budget allocations recorded in the 2025 fiscal plan earmark extensive capital for smart-city projects, stimulating continuous spatial-data procurement and platform roll-outs. Educational institutions in the capital add a pipeline of GIS graduates, partially easing the talent shortage.

The eastern region shows the highest 11.78% CAGR, propelled by energy-sector modernization and port-logistics upgrades. The eastern region grows rapidly on the back of Saudi Aramco’s digital oilfield initiatives, petrochemical facility upgrades, and port automation in Dammam and Jubail. These industries embed location intelligence to reduce downtime, manage pipelines, and ensure environmental compliance. Mining concessions mapped through the Ta’adeen Platform expand the Saudi Arabia geospatial analytics market size for mineral exploration and operations monitoring.

The western corridor benefits from giga-projects such as NEOM’s linear city, the Red Sea luxury tourism zone, and the entertainment city of Qiddiya. Each project requires multi-disciplinary spatial solutions covering environmental impact assessments, construction progress tracking, and visitor-flow optimization. Religious-tourism centers in Makkah and Madinah deploy crowd-management analytics to ensure pilgrim safety. Northern and southern provinces leverage precision farming and border-security applications, highlighting how diverse geography shapes demand patterns.

Mordor Intelligence tracks the geospatial analytics market across other major regions such as Africa and Middle East, with additional country-level coverage spanning Israel, Russia, Italy, Germany, France, Spain, and Nigeria, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Saudi Arabia geospatial analytics market hosts a balanced mix of international platform providers and fast-emerging domestic firms. Esri’s long-standing government relationships anchor large-scale GIS deployments, while Hexagon and Trimble offer specialized survey and asset-management modules. Neo Space Group accelerates vertical integration by acquiring UP42 to secure local control over satellite imagery provisioning.[4]Space Watch Africa, “Saudi-Based Agri-Climate Start-Up iyris Poised to Scale,” spacewatchafrica.com

Global cloud vendors cultivate regional presence to satisfy data-residency laws and deliver turnkey spatial-services stacks. The NSG–Esri GeoAI alliance trains algorithms on Arabic-language datasets, building localized feature catalogs that raise performance benchmarks. Start-ups leverage the National Geospatial Platform’s open APIs to offer sector-specific dashboards in retail analytics and logistics routing.

Competitive dynamics center on data-localization compliance, AI integration, and development of bilingual interfaces. Firms that bundle imagery, software, and domain consulting gain traction among agencies tasked with tight Vision 2030 deadlines. Moderate consolidation coexists with ample room for niche specialists, keeping the Saudi Arabia geospatial analytics market vibrant yet disciplined.

Saudi Arabia Geospatial Analytics Industry Leaders

Environmental Systems Research Institute, Inc.

Neo Space Group JSC

Saudi Company for Artificial Intelligence

TechButtons IT Solutions LLC

xMap Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Esri Saudi Arabia showcased localized GIS solutions at LEAP 2025, signaling sustained investment in market-specific innovation.

- January 2025: The National Center for Vegetation Cover completed an FAO study tour on geospatial tools for sustainable food systems.

- December 2024: The Ministry of Finance released the 2025 SAR 1.285 trillion budget, prioritizing developmental projects that intensify spatial analytics demand.

- November 2024: The Saudi Irrigation Organization and FAO launched a geospatially enabled irrigation-efficiency project across 21 farms.

Saudi Arabia Geospatial Analytics Market Report Scope

Geospatial analytics is the process of acquiring, manipulating, and displaying imagery and data from the geographic information system (GIS), such as satellite photos and GPS data. The specific identifiers of a street address and a zip code are used in geospatial data analytics. They are used to create geographic models and data visualizations for more accurate trends modeling and forecasting.

The Saudi Arabia geospatial analytics market is segmented by type (surface analysis, network analysis, and geovisualization), by end-user vertical (agriculture, utility and communication, defense and intelligence, government, mining and natural resources, automotive and transportation, healthcare, real estate and construction, and other end-user verticals).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Software |

| Services |

| Data and Content |

| Hardware and Sensors |

| Surface Analysis |

| Network and Location Analysis |

| Geovisualization |

| Spatial Data Mining and Predictive Modeling |

| Cloud |

| On-Premises |

| Hybrid/Edge |

| Satellite and Aerial Imagery |

| UAV/Drone |

| GIS and IoT Sensor Feeds |

| Mobile and Social Media Geo-data |

| Government and Smart-City Authorities |

| Defense and Intelligence |

| Utilities and Energy |

| Agriculture and Natural Resources |

| Transportation and Logistics |

| Real Estate and Construction |

| Healthcare and Public Health |

| Retail and Location-Based Services |

| Other End-User Verticals (Banking, Insurance, Tourism) |

| Central (Riyadh, Qassim) |

| Western (Makkah, Madinah) |

| Eastern (Ash-Sharqiyah) |

| Northern (Tabuk, Hail, Northern Borders, Al-Jouf) |

| Southern (Asir, Jazan, Najran, Al-Bahah) |

| By Component | Software |

| Services | |

| Data and Content | |

| Hardware and Sensors | |

| By Type | Surface Analysis |

| Network and Location Analysis | |

| Geovisualization | |

| Spatial Data Mining and Predictive Modeling | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid/Edge | |

| By Data Source | Satellite and Aerial Imagery |

| UAV/Drone | |

| GIS and IoT Sensor Feeds | |

| Mobile and Social Media Geo-data | |

| By End-User Vertical | Government and Smart-City Authorities |

| Defense and Intelligence | |

| Utilities and Energy | |

| Agriculture and Natural Resources | |

| Transportation and Logistics | |

| Real Estate and Construction | |

| Healthcare and Public Health | |

| Retail and Location-Based Services | |

| Other End-User Verticals (Banking, Insurance, Tourism) | |

| By Region | Central (Riyadh, Qassim) |

| Western (Makkah, Madinah) | |

| Eastern (Ash-Sharqiyah) | |

| Northern (Tabuk, Hail, Northern Borders, Al-Jouf) | |

| Southern (Asir, Jazan, Najran, Al-Bahah) |

Key Questions Answered in the Report

What is the expected value of the Saudi Arabia geospatial analytics market by 2031?

It is projected to reach USD 2.79 billion, reflecting sustained double-digit growth.

Which component currently leads spending in Saudi geospatial solutions?

Software platforms hold 46.12% of 2025 revenue due to their integration with government digital services.

Why is cloud deployment growing faster than on-premises setups?

Local hyperscale data centers lower costs and satisfy data-localization rules, pushing cloud deployments to an 11.55% CAGR.

Which data source is expanding the fastest?

Mobile and social-media geo-data is growing at a 12.09% CAGR as privacy-compliant analytics frameworks mature.

Which region will post the highest growth rate through 2031?

The eastern region is projected to grow at a 11.78% CAGR, fueled by energy-sector modernization and port-logistics projects.

What major regulation influences data processing choices?

The Personal Data Protection Law, fully enforceable since September 2024, governs geoprivacy and cross-border transfers.

Page last updated on: