Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

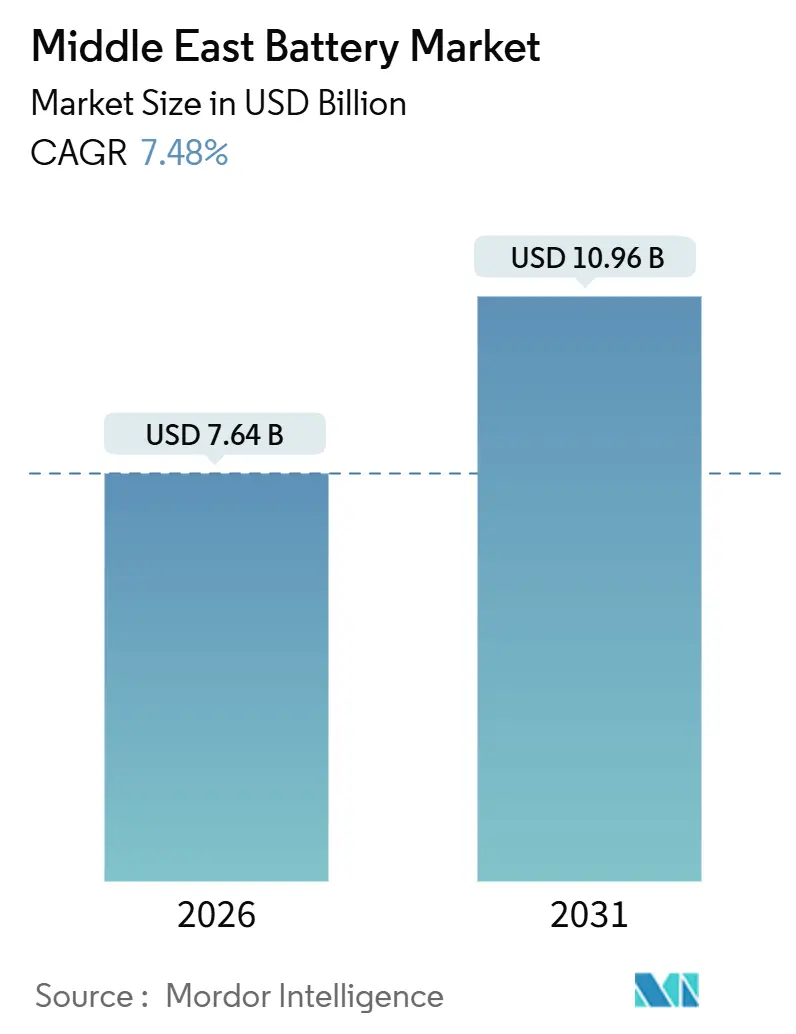

| Market Size (2026) | USD 7.64 Billion |

| Market Size (2031) | USD 10.96 Billion |

| Growth Rate (2026 - 2031) | 7.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Battery Market Analysis by Mordor Intelligence

The Middle East Battery Market size is estimated at USD 7.64 billion in 2026, and is expected to reach USD 10.96 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031).

Intensifying national Vision agendas are accelerating electrification, and utility-scale solar projects paired with storage are moving from pilots to multi-gigawatt procurements. Mandatory domestic-content rules are prompting global suppliers to form joint ventures, while falling lithium-ion costs are narrowing the price gap with diesel backup systems. Local recycling capacity, although nascent, is beginning to address end-of-life management. Raw-material import dependence and water scarcity remain structural headwinds, yet policy clarity and record-size tenders signal a durable demand runway for the Middle East battery market.

Key Report Takeaways

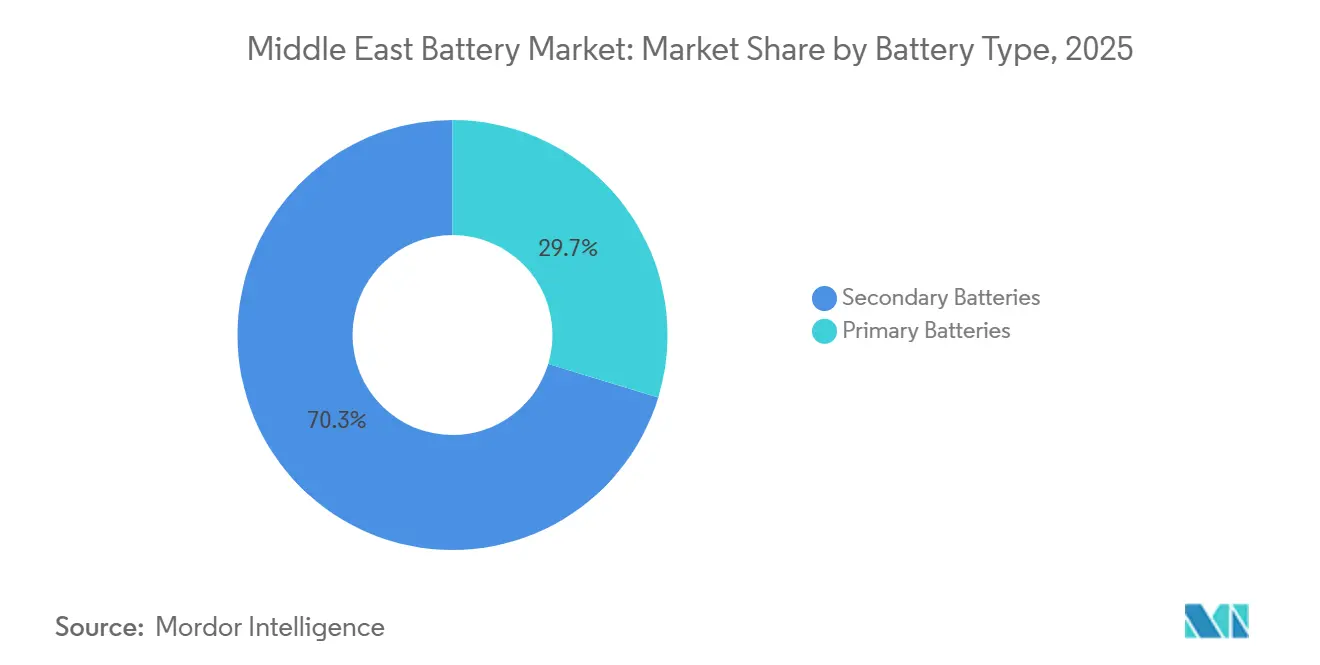

- By battery type, secondary batteries held 70.3% of the Middle East battery market share in 2025, and their revenue is forecast to grow at a 10.8% CAGR through 2031.

- By technology, lead-acid led with 39.8% share of the Middle East battery market size in 2025, while solid-state batteries are projected to expand at 30.9% CAGR during 2026-2031.

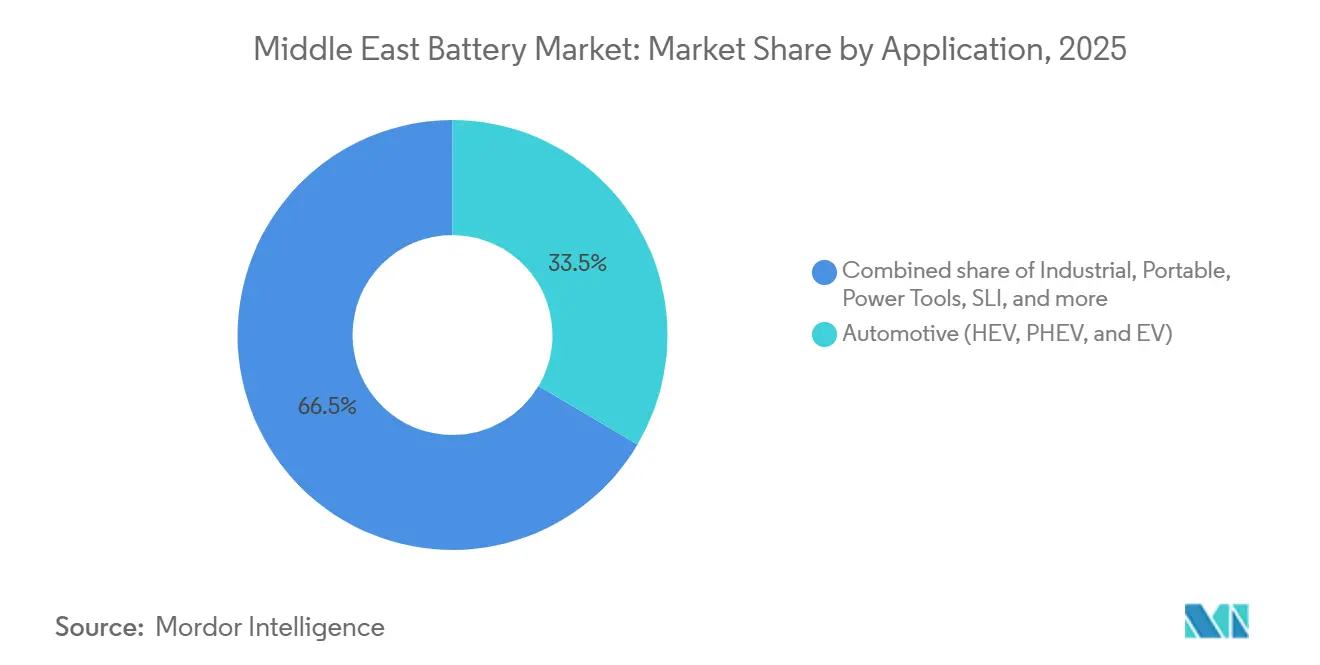

- By application, automotive batteries accounted for 33.5% of the Middle East battery market size in 2025 and are advancing at a 9.5% CAGR through 2031.

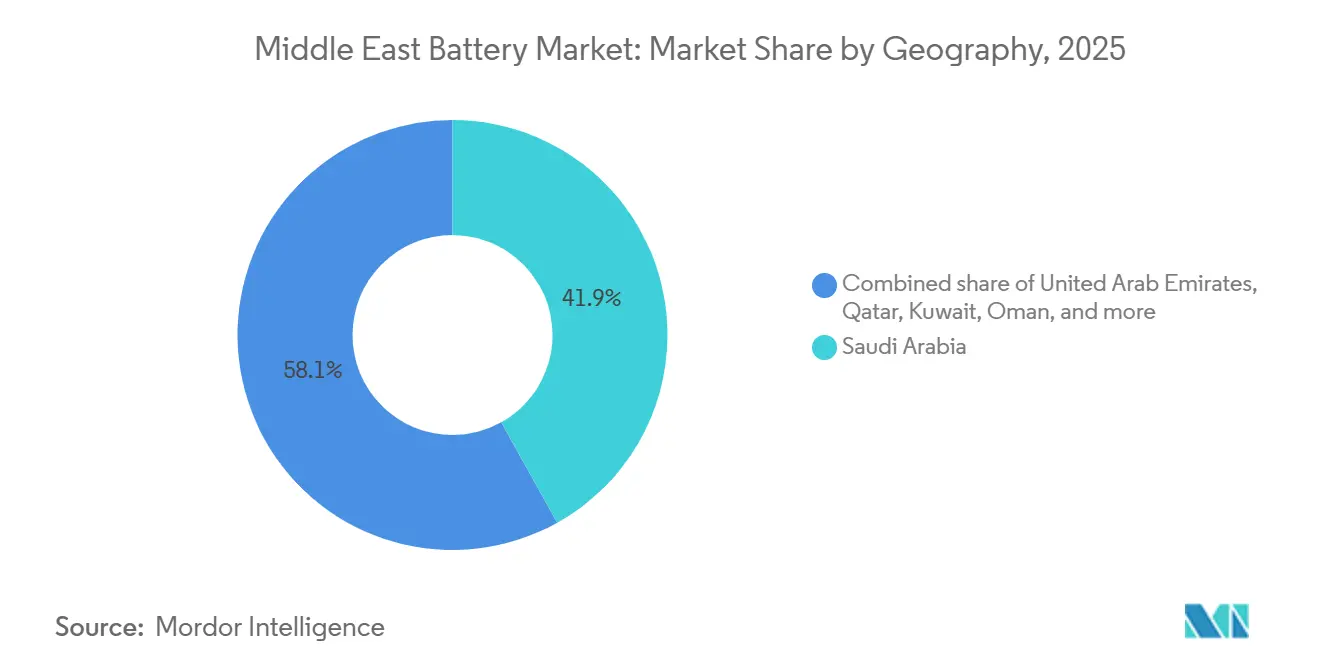

- By geography, Saudi Arabia captured 41.9% revenue share in 2025, whereas Oman is set to deliver the fastest 14.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV adoption push under Vision agendas | +2.1% | Saudi Arabia, UAE, Qatar, Oman, Kuwait | Medium term (2-4 years) |

| Utility-scale renewables driving ESS demand | +2.8% | Saudi Arabia, UAE, Oman, Qatar | Long term (≥ 4 years) |

| Incentives for local battery manufacturing | +1.2% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Expanding telecom and data-center backup need | +0.9% | GCC-wide with UAE, Saudi Arabia, Qatar focus | Short term (≤ 2 years) |

| Electrification of upstream O&G operations | +0.7% | Saudi Arabia, UAE, Kuwait, Oman | Medium term (2-4 years) |

| Off-grid desalination projects with storage | +0.5% | Oman, Saudi Arabia, UAE coastal areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Adoption Push Under National Vision Agendas

Saudi Arabia’s 2026 decision to nurture an electric-vehicle manufacturing sector is reshaping regional battery demand. Vision 2030 targets 30% electric-vehicle penetration in Riyadh by 2030, backed by an order to install 5,000 public chargers, and all new government fleet cars ordered after 2027 must be zero-emission.[1]Saudi Energy Ministry, “Vision 2030 Electric Vehicle Targets,” energy.gov.sa Qatar’s plan for 2,000 charging points by 2030 adds a secondary demand node. Lucid Motors began vehicle assembly in 2024 and signals local capability expansion. Actual electric-vehicle registrations were below 5,000 units in 2025, which indicates that incentives and consumer engagement must accelerate. Diverse charging standards across the Gulf fragment supplier strategies.

Utility-Scale Renewables Driving ESS Demand

Solar curtailment has already reached 1.2 TWh in Saudi Arabia during 2025, or 8% of total renewable output, and similar patterns are emerging in the UAE.[2]Saudi Power Procurement Company, “Battery Energy Storage System Tenders,” sppc.com.sa Battery energy storage systems are the preferred remedy, typified by Saudi Arabia’s 8 GWh phase-one tender awarded in 2025 and the UAE’s 19 GWh CATL–Masdar project that will supply 1 GW of round-the-clock power by 2027.[3]Reuters Staff, “CATL, Masdar Partner on USD 6 Billion UAE Battery Storage Project,” reuters.com Oman’s 100 MWh Ibri III storage plant shows that smaller states are embedding batteries at procurement launch. IRENA estimates that every new gigawatt of intermittent renewable capacity now requires 0.3-0.5 GWh of batteries to preserve grid stability.

Incentives for Local Battery Manufacturing

Saudi Arabia’s IKTVA rule mandating 30-50% in-kingdom value addition for awarded renewable and storage contracts, and the UAE’s “Make it in the Emirates” incentives, have brought cell makers to set up assembly lines. NEOM has earmarked USD 8.4 billion for hydrogen infrastructure that includes large batteries, creating further pull for local manufacturing. Tdafoq and Delectrik Power Systems agreed in 2025 to establish a flow-battery plant, exemplifying the shift from imports to joint ventures.

Expanding Telecom & Data-Center Backup Demand

The UAE hosts more than 50 active data centers in 2026, together exceeding 600 MW of IT load; each site relies on batteries for uninterruptible power supply. Saft’s lithium-ion rollout for Saudi telecom towers cut diesel use by 92% and truck rolls by 70%. EnerSys expanded a regional distribution network for PowerSafe batteries in 2024. Tesla’s Megapack has been adopted at off-grid sites where grid outages threaten connectivity. ITU guidelines standardize battery performance, so suppliers must guarantee sufficient cycle life under desert temperatures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -1.4% | GCC-wide | Short term (≤ 2 years) |

| Limited indigenous mineral supply | -0.9% | GCC-wide | Long term (≥ 4 years) |

| High capital cost versus diesel gensets | -0.7% | Saudi Arabia, Kuwait, Oman | Medium term (2-4 years) |

| Water-scarcity constraints on cooling and production | -0.6% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Lithium carbonate prices fluctuated between USD 12,000 and USD 18,000 per ton in 2025, unsettling budgetary planning for assemblers working on fixed-price contracts. With zero domestic lithium, cobalt, or nickel, every Middle East battery plant depends on imports. Cobalt supply disruptions in the Democratic Republic of Congo drove a 35% spot-price rise in early 2025, pushing suppliers toward cobalt-reduced chemistries. Saudi Arabia’s Public Investment Fund has acquired minority stakes in Australian and Chilean lithium ventures to hedge the exposure, yet end-product pricing inside the Middle East battery market still tracks global spot swings.

Limited Indigenous Mineral Supply

Regional geological surveys confirm negligible reserves of lithium, cobalt, or nickel, so refinery investment cannot offset upstream scarcity. The UAE signed a nickel hydroxide sourcing memorandum with Indonesia in 2025, but the material must still transit through third-party refiners. Recycling is immature: Dubatt’s 25,000 tpa lead-acid plant recovers only lead and cannot yet process lithium-ion scrap. Until closed-loop capacity scales are achieved, mineral dependence will restrain localized cost control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeables Dominate Fleet and Grid Segments

Secondary batteries led revenue with 70.3% in 2025, and the segment is projected to advance at a 10.8% CAGR through 2031. The figure reflects the rising share of electric vehicles, data-center backups, and grid-scale energy storage systems that demand thousands of deep cycles. The primary battery niche stays relevant in low-drain instrumentation and defense electronics but faces policy and cost headwinds as recycling mandates tighten.

Rechargeable uptake hinges on the total cost of ownership. BYD’s 6,000-cycle lithium iron phosphate pack for Saudi Electricity Company exemplifies economics that trump lower upfront prices of single-use chemistries.[4]BYD Company, “Saudi Arabia Battery Energy Storage Contracts,” byd.com Primary batteries supply under 30% of regional revenue, mainly in oilfield sensors where replacement intervals align with scheduled maintenance trips. Expanded enforcement of IEC 61960 standards in the UAE further cements safety requirements that favor reputable secondary suppliers.

By Technology: Solid-State Pilots Challenge Lead-Acid Incumbency

Lead-acid held 39.8% revenue in 2025, protected by cost leadership, robust recycling, and entrenched use in starter-lighting-ignition systems. Solid-state batteries, though still below 2% revenue, carry the highest 30.9% CAGR to 2031 as pilot lines migrate toward commercial runs in premium electric vehicles and high-reliability grid nodes.

Lithium-ion chemistries accounted for around 45% in 2025 and retained the default status for utility-scale storage. Flow batteries have broken into industrial slots after Aramco’s iron-vanadium unit demonstrated high-temperature tolerance. Enpower Greentech’s relocation under the UAE NextGenFDI program shows Gulf policymakers are courting solid-state pioneers with R&D incentives. Lead-acid prices remain 60-70% below lithium-ion on a per-kilowatt-hour basis but carry shorter cycle life, which narrows the advantage in long-run calculations.

By Application: Automotive Batteries Outpace Industrial and Portable Segments

Automotive batteries held a 33.5% share in 2025 and are expected to grow at a 9.5% CAGR through 2031, reflecting aggressive domestic-manufacturing targets in Saudi Arabia and new charging corridors in the UAE. Industrial stationary storage, particularly utility-scale energy storage systems, emerged as the fastest-growing subset inside industrial applications, underpinned by multi-gigawatt tenders meant to reduce solar curtailment.

Automotive demand is being institutionalized. Saudi government fleets shift to zero-emission models from 2027, creating a guaranteed procurement channel. Lucid’s plant secured in-kingdom assembly lines and will add cell assembly by 2027 to comply with IKTVA requirements. Forklifts and automated guided vehicles in Gulf warehouses migrate from lead-acid to lithium-ion to support continuous multi-shift duty cycles. Portable batteries are mature and tied to consumer electronics replacement cycles, which are lengthening and thus producing modest growth.

Geography Analysis

Saudi Arabia generated 41.9% of the Middle East battery market revenue in 2025. The two-phase 18 GWh storage tender and a 15.1 GWh BYD project pipeline define the most assertive grid-modernization drive. Upstream electrification and NEOM’s hydrogen plans add industrial and long-duration niches. Domestic value-addition rules force suppliers into joint ventures, anchoring manufacturing footprints that should deepen over the forecast frame.

The United Arab Emirates contributed roughly 28% revenue in 2025. The USD 6 billion CATL–Masdar 19 GWh storage complex illustrates the scale of solar-plus-storage programs. Data-center construction in Abu Dhabi and Dubai sustains telecom-grade lithium-ion shipments. The UAE recycling ecosystem, headed by Dubatt, is the first to tackle circularity but lacks lithium-ion processing scale.

Oman is on track for the fastest 14.7% CAGR to 2031, steered by Vision 2040 mandates and green-hydrogen export strategies. The 100 MWh Ibri III storage unit pioneers integrated solar-plus-storage procurement. Qatar targets 4 GW of renewable capacity by 2030 and hosts an emerging 1.675 GW solar-plus-storage pipeline. Kuwait’s Al Dibdibah project and Bahrain’s modest Noor 1 solar farm indicate earlier-stage renewable integration but create distributed opportunities for commercial storage systems.

Competitive Landscape

The five largest suppliers, BYD, CATL, LG Energy Solution, Tesla, and Samsung SDI, held an estimated 55-60% of 2025 revenue in the Middle East battery market. Regional players such as Middle East Battery Company, Saft, EnerSys, and Exide maintain leadership in lead-acid and specialized industrial niches. Chinese and South Korean cell makers, benefiting from gigawatt-scale capacity and cost advantages, capture most utility-scale storage awards. BYD’s 2025 joint development pact with Aramco aligns with the kingdom’s industrial strategy and embeds value transfer to satisfy IKTVA rules.

Technology diversification offers alternative differentiation. Aramco’s first commercial iron-vanadium flow battery validated long-duration storage outside lithium-ion’s four-hour window. Flow battery maker Tdafoq plans a Saudi plant, while Enpower Greentech is negotiating UAE incentives for solid-state trials. Recycling capability is the most conspicuous gap; Dubatt’s lead-acid plant recovers only a fraction of total end-of-life volume, offering a USD 200-300 million annual opportunity for lithium-ion recycling when consumer electric-vehicle fleets mature.

Smaller contenders position modular containerized batteries for telecom and microgrid deployments, betting on standardized architectures to shrink lead times. All suppliers must comply with IEC 62619 safety rules, which protect clients from thermal runaway and harmonize cell-qualification processes across Gulf markets.

Middle East Battery Industry Leaders

Exide Industries Ltd

Middle East Battery Company (MEBCO)

Tesla, Inc.

Saft Groupe SA

LG Energy Solution

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Saudi Power Procurement Company awarded phase-two storage capacity of 2.5 GW and 10 GWh, bringing the national contracted total to 4.5 GW and 18 GWh.

- May 2025: Saudi Aramco installed a 1 MWh iron-vanadium flow battery for gas compression, the first worldwide deployment of this chemistry in upstream oil and gas.

- April 2025: BYD and Saudi Aramco agreed to collaborate on new-energy-vehicle technologies, including provisions for in-kingdom cell production.

- January 2025: CATL and Masdar began construction of the 5.2 GW solar array with 19 GWh of batteries in the UAE, targeting 1 GW of round-the-clock power by 2027, the region’s largest solar-plus-storage venture.

- July 2024: Emirates Water and Electricity Company let a 400 MW battery contract to support the 2 GW Al Dhafra solar park evening ramp.

Middle East Battery Market Report Scope

A battery is an electrochemical device with one or more electrochemical cells that can be charged with an electric current and discharged when needed. Batteries are usually devices that are made up of multiple electrochemical cells that are connected to external inputs and outputs.

The Middle East battery market is segmented by type, technology, application, and geography. By type, the market is segmented into primary batteries and secondary batteries. By technology, the market is segmented into lead-acid, Li-ion, nickel-metal hydride, nickel-cadmium, sodium-sulfur, solid-state, flow batteryand emerging chemistries. By application, the market is segmented into automotive batteries, industrial batteries, portable batteries, power tools, SLI, and other applications. The report also covers the market size and forecasts for the battery market across the major countries in the region. For each segment, market sizing and forecasts have been done based on revenue (USD billion).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Rest of Middle East |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the forecast value of the Middle East battery market by 2031?

The market is expected to reach USD 10.96 billion by 2031, reflecting a 7.48% CAGR during 2026-2031.

Which battery type leads revenue in the Middle East?

Secondary (rechargeable) batteries held 70.3% of revenue in 2025 and are growing faster than primary batteries.

Which country contributes the largest share to regional demand?

Saudi Arabia generated 41.9% of revenue in 2025, driven by large grid-scale storage tenders and local manufacturing mandates.

What technology is growing the fastest?

Solid-state batteries show the highest growth outlook at 30.9% CAGR through 2031, although they remain in pilot phases today.

What is the main supply-chain risk for battery makers in the Gulf?

Complete reliance on imported lithium, cobalt, and nickel exposes manufacturers to raw-material price volatility and logistics disruptions.

Page last updated on: