Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

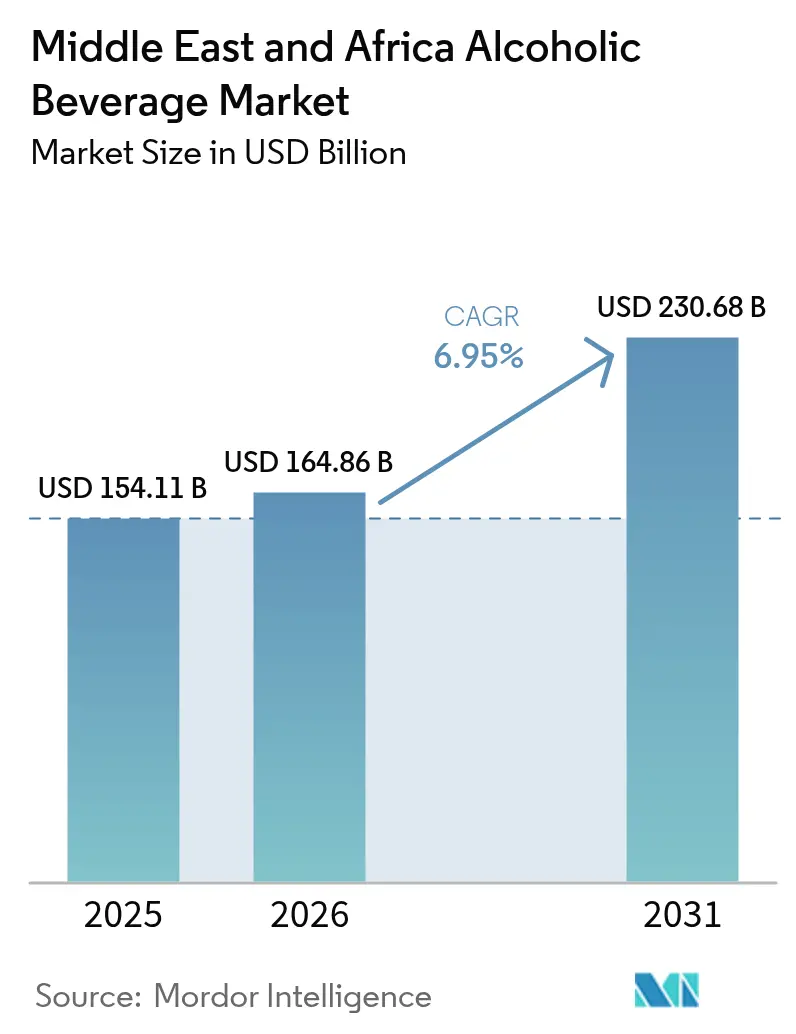

| Base Year Market Size (2025) | USD 154.11 Billion |

| Market Size (2026) | USD 164.86 Billion |

| Market Size (2031) | USD 230.68 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Alcoholic Beverage Market Analysis by Mordor Intelligence

The Middle East and Africa alcoholic beverage market size is projected to expand from USD 154.11 billion in 2025 and USD 164.86 billion in 2026 to USD 230.68 billion by 2031, registering a CAGR of 6.95% between 2026 to 2031. The market’s growth is primarily driven by strong macroeconomic developments, significant demographic shifts, and changing consumer behavior patterns. Rapid urbanization and rising disposable incomes are fueling consumption, particularly among young adults and affluent consumers who increasingly seek premium beverage options. Key growth markets include South Africa, the United Arab Emirates, and Nigeria, supported by advanced manufacturing capabilities, a growing expatriate population, and thriving tourism industries. The market is further strengthened by continuous product innovation, including flavored variants and ready-to-drink offerings, catering to modern consumer demands for variety, convenience, and accessibility.

Key Report Takeaways

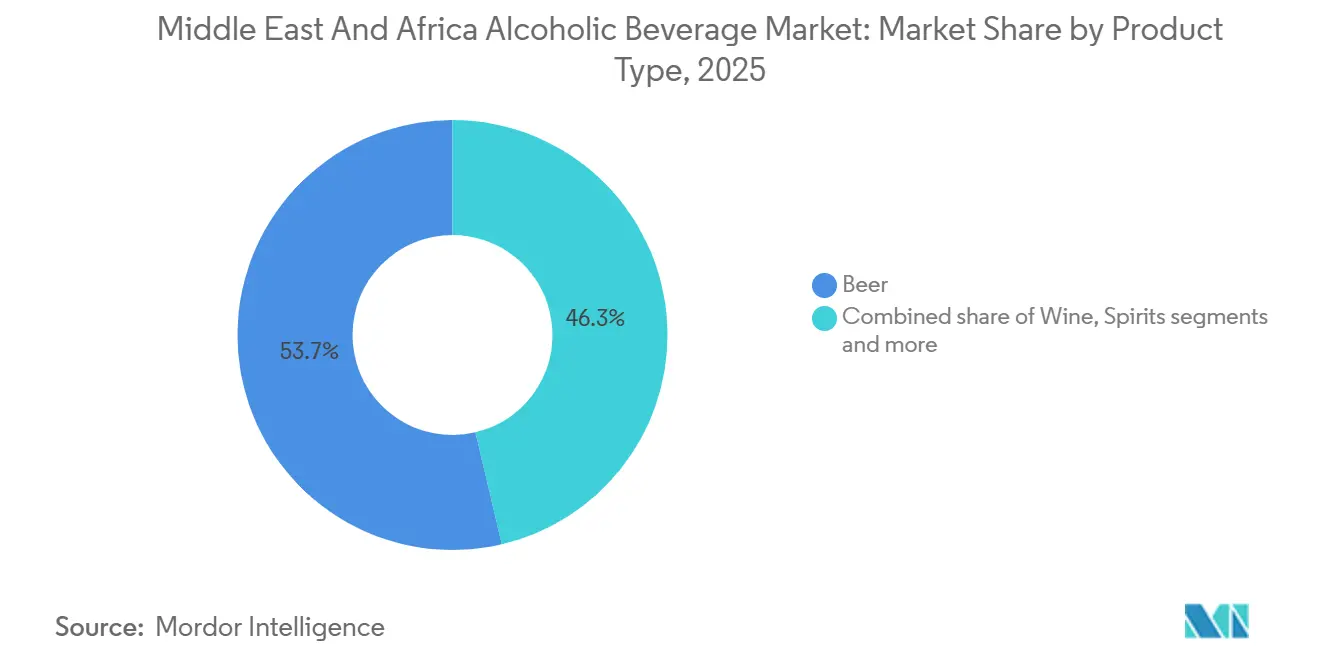

- By product type, beer held 53.68% of the Middle East and Africa alcoholic beverage market share in 2025; wine is forecast to grow at a 9.09% CAGR through 2031.

- By end user, the male segment accounted for 70.21% of 2025 revenue, whereas female demand is advancing at an 8.07% CAGR to 2031.

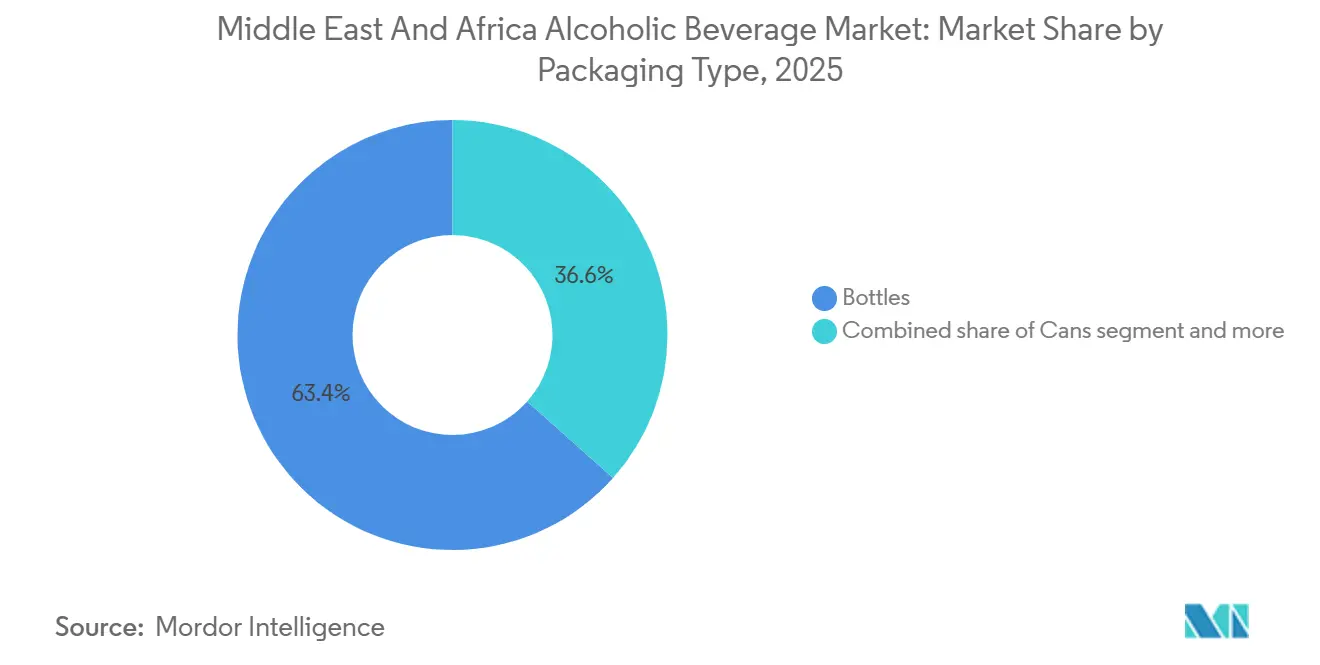

- By packaging type, bottles captured 63.42% of 2025 sales, while cans are expanding at an 8.38% CAGR between 2026 and 2031.

- By distribution channel, off-trade accounted for 66.17% of 2025 turnover, while on-trade is recovering at a 7.59% CAGR through 2031.

- By geography, South Africa led with 21.83% of 2025 revenue; the United Arab Emirates is the fastest-growing, with an 8.05% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Alcoholic Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and experience-led consumption | +1.4% | UAE, Saudi Arabia, South Africa (urban centers: Dubai, Riyadh, Cape Town, Johannesburg) | Medium term (2-4 years) |

| Expansion of travel retail and duty-free channels | +1.2% | UAE, Saudi Arabia, Qatar, with spillover to Egypt and Morocco transit hubs | Short term (≤ 2 years) |

| Growth of hospitality, entertainment, and mega-events | +1.1% | Saudi Arabia (NEOM, Red Sea Project), UAE (Dubai, Abu Dhabi), Qatar (FIFA legacy infrastructure) | Long term (≥ 4 years) |

| Rising popularity of low-alcohol and no-alcohol alternatives | +0.9% | Global, with accelerated adoption in UAE, Saudi Arabia, Egypt, South Africa | Medium term (2-4 years) |

| Convenient ready-to-drink (RTD) offerings | +0.8% | UAE, South Africa, Nigeria (urban youth segments in Lagos, Johannesburg, Dubai) | Short term (≤ 2 years) |

| Product innovation and flavor variety | +0.7% | Global, with premium launches concentrated in South Africa, UAE, Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and Experience-Led Consumption

Affluent consumers in Gulf states and South African metropolitan areas are trading up to ultra-premium spirits and limited-edition releases, a behavioral shift that is compressing volume growth while inflating revenue per transaction. Diageo reported that its Reserve portfolio, comprising brands priced above USD 50 per bottle, grew 18% in Middle Eastern markets during fiscal 2025, outpacing its mainstream spirits by a factor of three[1]. This premiumization wave is intertwined with experiential retail: Dubai Duty Free's liquor division generated USD 290.6 million in 2025, with single-malt whiskies and cognacs accounting for 41% of spirits revenue despite representing only 22% of unit sales[2]Source: Dubai Duty Free, “Record-Breaking Sales of USD 2.378 Billion in 2025,” dubaidutyfree.com. South Africa's wine estates are leveraging this trend by launching cellar-door experiences and pairing menus, converting casual buyers into high-margin direct-to-consumer customers. The dynamic is self-reinforcing: as disposable incomes rise and social media amplifies luxury signaling, brands can command higher price points without sacrificing share, effectively decoupling revenue growth from volume expansion.

Expansion of Travel Retail and Duty-Free Channels

Travel retail is emerging as a disproportionately influential channel, capturing 9% of regional revenue in 2025 but contributing 14% of incremental growth, according to data extrapolated from Dubai Duty Free's performance metrics. The UAE's position as a global aviation hub, handling over 140 million passengers in 2025, creates a captive, high-spending audience for duty-free alcohol, with average basket sizes 2.3 times higher than domestic off-trade purchases, according to the UAE Government[3]Source: UAE Government, “Tourism Statistics 2025,” u.ae. Saudi Arabia's planned Red Sea International Airport and NEOM Bay Airport will add 20 million annual passenger capacity by 2030, each featuring duty-free zones where alcohol sales will be permitted despite broader domestic prohibitions. This channel's appeal extends beyond price arbitrage: limited-edition releases and exclusive packaging drive impulse purchases among transit passengers, a behavior that brands exploit through airport-exclusive SKUs. Egypt and Morocco are upgrading terminal retail infrastructure to capture spillover demand from European and Asian travelers, though execution lags Gulf benchmarks due to regulatory inconsistencies and lower per-passenger spend.

Growth of Hospitality, Entertainment, and Mega-Events

Saudi Arabia's Vision 2030 blueprint is catalyzing a hospitality buildout that will fundamentally alter on-trade dynamics. The kingdom awarded licenses for 100 new hotels in 2025, many of which include licensed bars and restaurants within designated entertainment districts where alcohol service is permitted. FIFA's 2034 World Cup award to Saudi Arabia guarantees infrastructure investments exceeding USD 20 billion, including 15 stadiums and 185,000 hotel rooms, creating sustained on-premise demand through 2035[4]Source: FIFA, “World Cup 2034 Infrastructure Plans,” fifa.com. The UAE's post-Expo 2020 momentum continues, with Dubai's licensed venue count rising 12% year-on-year to 1,847 outlets in 2025, spanning rooftop bars, beach clubs, and Michelin-starred restaurants UAE Government. This expansion is not confined to Gulf states: South Africa's Cape Town and Johannesburg are attracting international hotel chains that anchor mixed-use developments around premium beverage programs. The strategic implication is clear, on-trade is transitioning from a margin-dilutive necessity to a brand-building and premiumization engine, particularly for spirits and craft beer portfolios that command 60-80% gross margins in hospitality settings.

Rising Popularity of Low-Alcohol and No-Alcohol Alternatives

Health-conscious consumption and regulatory accommodation are converging to legitimize zero-alcohol beverages in markets where traditional products face cultural headwinds. Heineken's 0.0 portfolio, spanning beer, cider, and malt beverages, achieved 23% volume growth across Middle Eastern markets in 2025, with Saudi Arabia and Egypt leading adoption. Diageo's non-alcoholic spirits range, including Gordon's 0.0% and Tanqueray 0.0%, launched in UAE retail channels in January 2025, targeting the 34% of surveyed consumers who seek social-drinking occasions without intoxication. AB InBev's Corona Cero entered Saudi Arabian supermarkets in March 2025, the first international beer brand to secure distribution under the kingdom's revised food-safety regulations that classify sub-0.5% ABV beverages as non-alcoholic. This segment's growth is asymmetric: it cannibalizes minimal share from full-strength products but expands total category penetration by recruiting abstainers and occasional drinkers. Pernod Ricard's acquisition of non-alcoholic aperitif brand Ceder's in 2024 underscores the strategic priority multinational players assign to this whitespace, particularly in geographies where demographic and religious factors constrain conventional alcohol marketing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty and policy volatility | -0.8% | Saudi Arabia, Egypt, Nigeria (policy reversals and enforcement inconsistency) | Medium term (2-4 years) |

| Cultural and religious sensitivities | -0.6% | Saudi Arabia, Egypt, Morocco, UAE (varying enforcement of Islamic principles) | Long term (≥ 4 years) |

| High pricing due to taxes and duties | -0.7% | South Africa, UAE, Turkey, Egypt (excise tax escalation) | Short term (≤ 2 years) |

| Illicit and unregulated alcohol trade | -0.5% | Nigeria, Egypt, Kenya, South Africa (counterfeit and smuggled products) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty and Policy Volatility

Abrupt policy shifts in key markets are compressing investment horizons and inflating risk premiums. Saudi Arabia's 2026 announcement permitting alcohol in tourist zones arrived without detailed licensing frameworks, leaving operators uncertain about eligibility criteria, fee structures, and enforcement protocols. Egypt reversed a planned excise-tax reduction in January 2025, instead imposing a 15% surcharge on imported spirits, a decision communicated with 48 hours' notice that stranded inventory and disrupted Q1 pricing strategies. Nigeria's multiple regulatory agencies, NAFDAC, Customs, and state-level boards, issue conflicting guidance on labeling, import permits, and distribution, forcing brands to maintain parallel compliance teams and inflating go-to-market costs by an estimated 18-22% relative to comparably sized African markets. This volatility deters long-term capital commitments: Heineken's Dubai brewery represents a rare greenfield investment, whereas most multinational expansions favor asset-light partnerships or third-party manufacturing to preserve exit optionality. The World Health Organization's 2025 alcohol taxation report highlights that MEA jurisdictions exhibit the highest year-over-year variance in excise rates globally, a pattern that penalizes supply-chain optimization and favors agile, locally embedded competitors.

Cultural and Religious Sensitivities

Islamic principles governing alcohol consumption create persistent demand headwinds that no amount of marketing can fully offset. Saudi Arabia's tourist-zone liberalization explicitly excludes Saudi nationals from purchasing or consuming alcohol, segmenting the addressable market to expatriates and visitors, a cohort that represented only 38% of the kingdom's 2025 population. Egypt's 2024 Ramadan alcohol-sales suspension, extended from the traditional month to 45 days, compressed Q1 revenue for on-trade operators by 19% year-on-year, a disruption that recurs annually with variable duration. Morocco permits alcohol sales but restricts advertising and imposes licensing quotas that cap outlet density at one per 5,000 residents in urban areas, effectively capping market penetration regardless of demand elasticity. These constraints are not static: grassroots movements in several North African states advocate for stricter controls, creating tail risk that liberalization trends could reverse. Brands navigate this terrain through euphemistic marketing, sponsorship of non-alcohol events, and portfolio diversification into zero-ABV products that comply with religious dietary laws while maintaining brand visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beer Anchors Revenue, Wine Accelerates

Beer's 53.68% share of 2025 revenue reflects entrenched consumption habits, distribution ubiquity, and price accessibility, yet wine's 9.09% forecast CAGR through 2031 signals a structural reallocation toward higher-margin, premiumized categories. Lager dominates beer volume, accounting for an estimated 78% of segment sales, driven by Heineken, AB InBev, and Carlsberg portfolios optimized for hot-climate refreshment and mass-market pricing. Low-alcohol beer is carving a niche in health-conscious and religiously observant demographics, with Heineken 0.0 achieving distribution in 12,400 Middle Eastern outlets by end-2025, up from 7,800 in 2024. Ale and craft styles remain subscale but are growing 16-19% annually in South Africa's urban centers, where microbreweries leverage local ingredients and experiential taprooms to command premium pricing.

Wine's acceleration is driven by South African exports, which reached 421 million liters in 2025, with Middle Eastern and African destinations accounting for 34% of the volume, up from 28% in 2023, according to Wines of South Africa (WoSA)[5]Source: Wines of South Africa, “Industry Statistics 2025,” wosa.co.za. Still wine accounts for 68% of category revenue, yet sparkling wine is expanding faster, with an estimated 11-13% CAGR, as celebratory occasions and hospitality venues drive prosecco and cava adoption. Fortified wines, including port and sherry, retain niche appeal in Gulf markets where sweeter profiles align with regional palate preferences. Spirits, encompassing whisky, rum, vodka, and cognac, benefit from premiumization tailwinds: Diageo's Reserve portfolio grew 18% in Middle Eastern markets during fiscal 2025, with single-malt Scotch and aged cognacs leading growth. Tequila and mezcal are emerging categories, with Pernod Ricard's Altos and Olmeca brands achieving 27% growth in UAE on-trade channels in 2025, driven by cocktail culture and bartender advocacy. Liqueurs and other spirits capture residual demand, often serving as mixers or ingredients in RTD formulations.

By End User: Male Dominance Persists, Female Segment Surges

Male consumers' 70.21% share of 2025 revenue underscores entrenched gender disparities in alcohol access and social acceptability, yet the female segment's 8.07% forecast CAGR, outpacing the overall market by 112 basis points, reflects urbanization, workforce participation, and targeted marketing. Diageo's 2025 consumer survey across the UAE, South Africa, and Egypt found that 41% of female respondents aged 25-40 consumed alcohol at least monthly, up from 34% in 2023, with wine and RTD cocktails preferred over beer and spirits.

Brands are responding with gender-neutral packaging, influencer partnerships, and occasion-based messaging that de-emphasizes traditional male-coded imagery. Pernod Ricard's Beefeater Pink Strawberry gin, launched in South African retail in April 2025, achieved 62% female purchase incidence, demonstrating the commercial viability of explicitly targeting this cohort. Male consumption patterns are bifurcating: premium spirits and craft beer attract affluent urban professionals, while value lagers and local spirits dominate rural and lower-income segments. The strategic implication is that female-segment growth is disproportionately concentrated in higher-margin categories, amplifying its revenue contribution beyond its volume share and justifying incremental marketing investment despite cultural and regulatory headwinds in several markets.

By Packaging Type: Bottles Dominate, Cans Gain Momentum

Bottles' 63.42% share of 2025 packaging revenue reflects legacy infrastructure, premium positioning, and regulatory requirements in certain jurisdictions that mandate glass for spirits above 20% ABV. Yet cans' 8.38% forecast CAGR, the fastest among packaging formats, is driven by portability, sustainability credentials, and single-serve convenience that aligns with RTD and low-alcohol product proliferation. Ball Corporation reported that beverage-can shipments to Middle Eastern and African markets rose 9.2% year-on-year in 2024, with alcoholic beverages representing 31% of incremental volume, up from 24% in 2023. Heineken is committed to achieving 100% recyclable packaging by 2025 and reducing packaging-related carbon emissions by 40% by 2030, targets that favor aluminum cans over glass due to lower transport weight and higher recycling rates. Cans are also penetrating wine: South African producers launched 18 canned wine SKUs in 2025, targeting outdoor recreation and festival channels where glass is prohibited, according to Wines of South Africa (WoSA).

Glass bottles retain dominance in spirits and premium wine due to perceived quality associations and closure technologies, such as cork and screw caps, that signal authenticity. Diageo's ultra-premium whisky releases exclusively use glass, often with embossed detailing and secondary packaging that enhances shelf presence and gifting appeal. PET and other plastic formats capture residual share, primarily in informal retail and low-income segments where breakage risk and deposit schemes favor lightweight alternatives. The packaging landscape is also shaped by anti-counterfeiting imperatives: tamper-evident closures, holographic labels, and QR-code authentication are becoming standard in markets like Nigeria and Egypt, where illicit trade erodes brand equity and consumer trust. These technologies add 2-4% to packaging costs but are increasingly non-negotiable in high-risk geographies, effectively raising barriers to entry for smaller producers while reinforcing incumbent advantages in supply-chain security and regulatory compliance.

By Distribution Channel: Off-Trade Leads, On-Trade Rebounds

Off-trade's 66.17% share of 2025 distribution revenue reflects the dominance of supermarkets, liquor stores, and e-commerce in markets where retail density and price transparency favor self-service formats. South Africa's Shoprite and Pick n Pay chains account for an estimated 38% of national alcohol sales, leveraging private-label portfolios and promotional pricing to capture price-sensitive shoppers. The UAE's e-commerce alcohol platforms, African + Eastern and MMI, reported 34% year-on-year GMV growth in 2025, driven by home delivery, subscription models, and digital-exclusive SKUs that bypass traditional retail intermediaries. Off-trade's margin structure, typically 18-25% gross margin for retailers, incentivizes aggressive ranging and promotional activity, compressing brand pricing power but expanding category accessibility.

The on-trade's 7.59% forecast CAGR through 2031 signals post-pandemic normalization and a structural upgrade in hospitality infrastructure. Dubai's licensed venue count reached 1,847 outlets in 2025, up 12% year-on-year, spanning rooftop bars, beach clubs, and Michelin-starred restaurants that command USD 18-30 per cocktail, margins unattainable in retail. Saudi Arabia's Vision 2030 hospitality buildout, targeting 100 million annual tourist visits by 2030, will add thousands of licensed on-premise outlets, creating sustained demand for premium spirits and craft beer portfolios. On-trade also serves as a brand-building channel: Pernod Ricard's bartender academies in UAE and South Africa trained 1,200 mixologists in 2025, seeding advocacy for its Absolut, Jameson, and Chivas portfolios in high-visibility venues. The channel's vulnerability lies in regulatory exposure, license revocations, operating-hour restrictions, and tax audits disproportionately impact on-trade operators, and macroeconomic sensitivity, as discretionary dining and nightlife spending contracts faster than at-home consumption during downturns. Brands navigate this by maintaining balanced channel exposure, though the strategic priority is shifting toward on-trade given its premiumization and experiential advantages.

Geography Analysis

South Africa's 21.83% share of 2025 revenue positions it as the region's anchor market, underpinned by a 300-year winemaking heritage, entrenched beer consumption, and a diversified spirits industry spanning local distilleries and multinational subsidiaries. The nation's wine exports reached 421 million liters in 2025, with intra-African and Middle Eastern shipments growing 19% year-on-year as producers diversify away from saturated European markets, according to WOSA. Yet domestic consumption faces headwinds from successive excise increases, 6.5% on spirits and 4.8% on wine in the 2025 budget, that are eroding affordability for middle-income households and fueling illicit trade estimated at 15-18% of total volume, according to the South African Revenue Service (SARS). The South African Revenue Service's enforcement crackdowns seized 8.4 million liters of contraband in 2024, yet officials acknowledge this represents a fraction of total illicit flows. The market's maturity limits organic growth, but premiumization and craft segments, particularly craft beer and artisanal gin, are expanding 16-19% annually, driven by urban millennials and experiential retail, according to the South African Breweries.

The United Arab Emirates' 8.05% forecast CAGR, the fastest among tracked geographies, reflects its position as a global tourism and aviation hub, with over 140 million passengers transiting its airports in 2025. Dubai Duty Free's liquor division generated USD 290.6 million in 2025, with single-malt whiskies and cognacs commanding 41% of spirits revenue despite representing only 22% of unit sales, underscoring the premiumization intensity. The emirate's 1,847 licensed on-trade venues, up 12% year-on-year, span rooftop bars, beach clubs, and Michelin-starred restaurants that anchor mixed-use developments and drive experiential consumption. Regulatory reforms in 2024 legalized e-commerce alcohol sales and relaxed licensing requirements for hotels, expanding addressable outlets by an estimated 18%. Heineken's USD 100 million Dubai brewery joint venture with Sirocco, targeting 2027 commissioning, will supply 250,000 hectoliters annually and reduce reliance on European imports subject to 50% excise duties. Saudi Arabia's market is undergoing a historic inflection: the kingdom's 2026 decision to permit alcohol sales in designated tourist zones, while maintaining prohibition for nationals, unlocks latent demand in a population of 36 million, though execution details remain opaque. Vision 2030's hospitality investments, including 100 new hotels licensed in 2025 and FIFA 2034 World Cup preparations, will create sustained on-premise demand through the next decade.

Nigeria, Egypt, Morocco, and Turkey present divergent dynamics shaped by regulatory volatility, cultural factors, and economic conditions. Nigeria's market is constrained by high import tariffs, NAFDAC's stringent labeling requirements, and illicit competition that captures an estimated 18-22% of volume, yet urbanization and a growing middle class sustain 5-6% annual growth in formal channels. Egypt's 2024 methanol-poisoning incidents, resulting in 194 deaths, prompted a government crackdown that closed 1,200 unlicensed outlets, temporarily disrupting supply but failing to address root causes of counterfeit proliferation. The nation's 185% effective tax rate on premium spirits limits formal-market penetration to affluent urban cohorts, while tourism recovery, Red Sea resorts hosted 8.2 million visitors in 2025 sustains on-trade demand, according to the Egypt Tourism Authority. Morocco's licensing quotas cap outlet density at one per 5,000 urban residents, constraining distribution despite growing tourism that reached 14.5 million arrivals in 2025. Turkey's market contracted 14% in volume during 2024-2025 following excise hikes that pushed spirit prices from TRY 850 to TRY 1,215 (USD 35 to USD 50), illustrating the demand elasticity risks inherent in punitive fiscal regimes. The Rest of Middle East and Africa, encompassing Kenya, Ghana, Angola, and Gulf states beyond UAE and Saudi Arabia, collectively represents 22% of regional revenue, characterized by fragmented regulation, nascent formal channels, and high growth volatility tied to commodity-price cycles and political stability.

Competitive Landscape

The Middle East and Africa alcoholic beverage industry exhibits a moderate concentration, reflecting a duopoly in beer, Anheuser-Busch InBev and Heineken command a majority combined share, coexisting with oligopolistic spirits competition among Diageo, Pernod Ricard, and Bacardi, and fragmented wine and artisanal segments where regional players retain defensible positions. Multinational incumbents are pivoting toward localization strategies to mitigate tariff exposure and regulatory risk: Heineken's USD 100 million Dubai brewery joint venture with Sirocco, slated for 2027 commissioning, will supply 250,000 hectoliters annually, reducing reliance on European imports subject to UAE's 50% excise levy. Diageo is evaluating local production in Gulf states to serve Saudi Arabia's nascent tourist-zone market, a move that would replicate its African playbook, where East African Breweries anchored regional expansion before its USD 2.3 billion divestiture to Asahi in 2025.

Competitive intensity is escalating in zero-alcohol and RTD segments, where portfolio breadth and speed-to-market determine share capture: Pernod Ricard's acquisition of non-alcoholic aperitif brand Ceder's in 2024 and Diageo's launch of Gordon's 0.0% and Tanqueray 0.0% in UAE retail channels in January 2025 illustrate the strategic priority assigned to these whitespace categories. Technology adoption is differentiating leaders from laggards, particularly in e-commerce enablement and anti-counterfeiting. The UAE's African + Eastern and MMI platforms reported 34% year-on-year GMV growth in 2025, leveraging AI-driven recommendation engines and subscription models that increase customer lifetime value by 40-55% relative to transactional buyers. Blockchain-enabled track-and-trace systems are becoming table stakes in Nigeria and Egypt, where counterfeit penetration exceeds 18%: Diageo's deployment of serialized QR codes on Johnnie Walker bottles in Nigeria reduced reported counterfeits by 31% within six months of rollout.

White-space opportunities concentrate in female-targeted products, low-alcohol innovations, and premiumized local spirits: South African gin brands like Inverroche and Musgrave are capturing share from international incumbents by emphasizing indigenous botanicals and craft narratives, achieving 19% growth in 2025 despite minimal marketing spend. Emerging disruptors include direct-to-consumer wine clubs in South Africa and subscription RTD services in UAE, both bypassing traditional retail intermediaries and capturing 25-35% gross margins versus 18-22% in conventional channels. The competitive landscape will likely consolidate further as regulatory complexity and capital intensity favor scale players, yet niche specialists with strong local ties and agile go-to-market models can sustain profitable growth in under-served segments and geographies.

Middle East And Africa Alcoholic Beverage Industry Leaders

Anheuser-Busch InBev SA/NV

Heineken Holdings N.V.

Diageo plc

Pernod Ricard SA

Molson Coors Beverage Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Compass Box Whisky entered the South African market, expanding its presence and introducing its distinctive whisky portfolio to South African consumers.

- August 2025: Don Julio introduced its Reposado and Blanco tequila variants in Nigeria through a launch event in Lagos. The products target affluent consumers and luxury lifestyle enthusiasts.

- May 2025: Salty Nerd, a premium grain vodka brand, launched in the United Arab Emirates. The charcoal-filtered vodka will be available in 750ml and 180ml bottles, with an alcohol content of 42.8% ABV.

- April 2025: Mack Brands introduced three spirits in South Africa: Conte Camillo Negroni, Tequila Rosaluz, and Finvara Irish Whiskey. These products target consumers seeking premium alcoholic beverages.

Middle East And Africa Alcoholic Beverage Market Report Scope

An alcoholic beverage is a drink that contains ethanol, a type of alcohol produced by the fermentation of grains, fruits, or other sources of sugar. The Middle East and Africa Alcoholic Beverage Market was segmented into product type, end-user, packaging type, distribution channel, and geography. By product type, the market is segmented into beer, wine, spirits, and others. The beer segment is further categorized into ale, lager, low-alcohol, and other beer types. The wine segment includes fortified wine, still wine, sparkling wine, and other wine types. The spirits segment covers brandy and cognac, liqueur, tequila and mezcal, rum, whisky, and other spirit types. This segmentation examines shifts in consumer preferences, premiumization trends, and innovation across alcoholic beverage categories. Based on end user, the market is analyzed across male and female consumers, highlighting variations in consumption behavior, product choices, and purchasing drivers. By packaging type, the report evaluates demand for bottles, cans, and other packaging formats, assessing the influence of convenience, sustainability, and brand positioning. In terms of distribution channel, the market is divided into on-trade and off-trade, capturing sales across hospitality venues and retail environments. Geographically, the report covers key countries including South Africa, Saudi Arabia, the United Arab Emirates, Nigeria, Egypt, Morocco, and Turkey, along with the rest of the Middle East and Africa. This report provides a comprehensive analysis of the Middle East and Africa alcoholic beverages market, with market size estimations and forecasts presented in both value (USD Million) and volume (Liters).

By Product Type

| Beer | Ale Beer |

| Lager | |

| Low-Alcohol Beer | |

| Other Beer Types | |

| Wine | Fortified Wine |

| Stilll Wine | |

| Sparkling Wine | |

| Other Wines Types | |

| Spirits | Brandy and Cognac |

| Liquer | |

| Tequilla and Mezcel | |

| Rum | |

| Whisky | |

| Other Spirit Types | |

| Others |

By End User

| Male |

| Female |

By Packaging Type

| Bottles |

| Cans |

| Others |

By Distribution Channel

| On-trade |

| Off-trade |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Beer | Ale Beer |

| Lager | ||

| Low-Alcohol Beer | ||

| Other Beer Types | ||

| Wine | Fortified Wine | |

| Stilll Wine | ||

| Sparkling Wine | ||

| Other Wines Types | ||

| Spirits | Brandy and Cognac | |

| Liquer | ||

| Tequilla and Mezcel | ||

| Rum | ||

| Whisky | ||

| Other Spirit Types | ||

| Others | ||

| By End User | Male | |

| Female | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is premium wine growing in the Middle East and Africa alcoholic beverage market?

Wine is projected to rise at a 9.09% CAGR through 2031, led by sparkling variants in hospitality venues.

Which packaging format is gaining the most traction across the region?

Cans are advancing at an 8.38% CAGR because of portability, recycling rates, and alignment with RTDs.

Why are duty-free shops important for alcoholic beverage suppliers?

They account for only 9% of sales but deliver 14% of incremental growth, buoyed by high-spending transit passengers.

How significant is illicit alcohol to overall consumption?

Counterfeit and smuggled liquor captures 15.1% of African demand, equal to about USD 2.8 billion in lost formal revenue.

What impact will Saudi Arabia’s tourist-zone policy have on market growth?

The 2026 liberalization opens a new channel for expatriate and visitor sales, adding upside to long-term on-trade forecasts, although licensing clarity is still pending.

Page last updated on: