Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

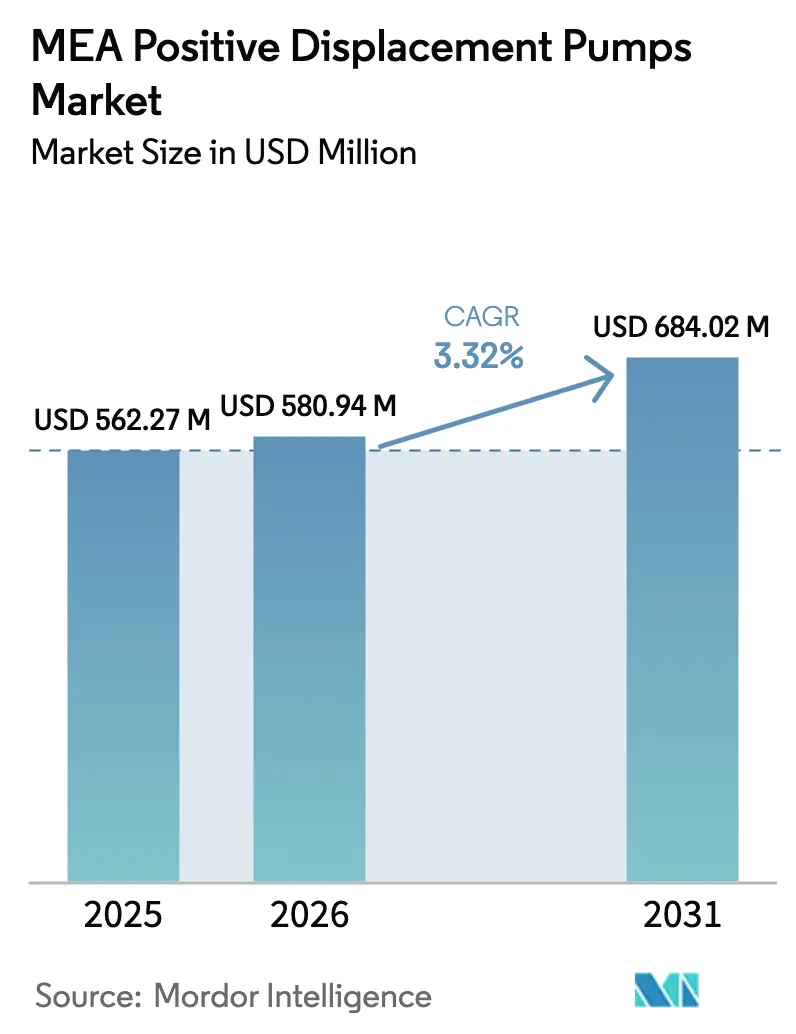

| Base Year Market Size (2025) | USD 562.27 Million |

| Market Size (2026) | USD 580.94 Million |

| Market Size (2031) | USD 684.02 Million |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

MEA Positive Displacement Pumps Market Analysis by Mordor Intelligence

The Middle East and Africa positive displacement pump market size in 2026 is estimated at USD 580.94 million, growing from 2025 value of USD 562.27 million with 2031 projections showing USD 684.02 million, growing at 3.32% CAGR over 2026-2031. This moderate headline figure masks contrasting regional dynamics: heavy upstream spending in the Gulf Cooperation Council is supporting large‐capacity rotary screw installations, while African mining expansion is lifting demand for abrasion-resistant dewatering solutions. Oil price stability, stricter industrial water-reuse mandates and rising food-safety certifications are jointly underpinning fresh capital outlays. At the same time, localized manufacturing investments in Egypt and South Africa are shortening lead times and partially insulating buyers from currency swings. Collectively, these factors position the Middle East and Africa positive displacement pump market for steady, if unspectacular, growth despite cyclical risks.

Key Report Takeaways

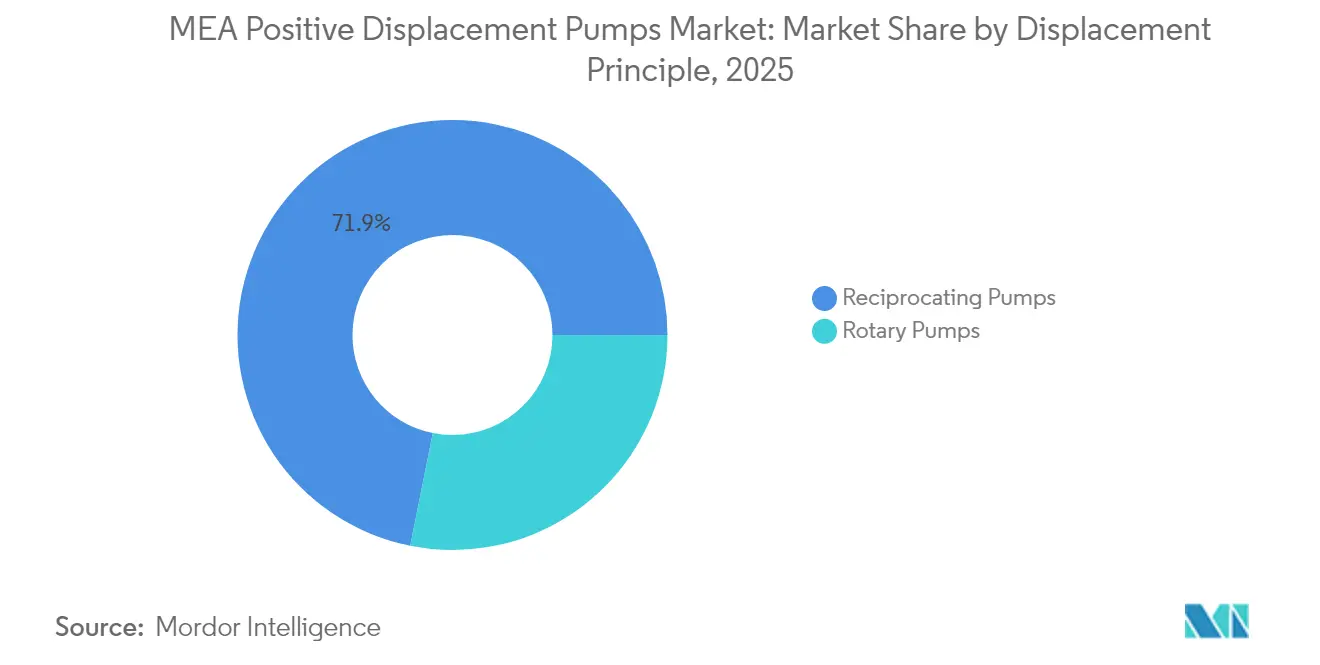

- By displacement principle, rotary screw units captured 28.15% revenue share in 2025; peristaltic pumps are projected to expand at a 3.67% CAGR through 2031.

- By end-user industry, oil and gas applications held 30.85% of the Middle East and Africa positive displacement pump market share in 2025, while pharmaceuticals recorded the highest projected CAGR at 3.74% to 2031.

- By material, cast-iron constructions accounted for 46.12% of the Middle East and Africa positive displacement pump market size in 2025; alloy and specialty metals are on track for an 4.12% CAGR between 2026-2031.

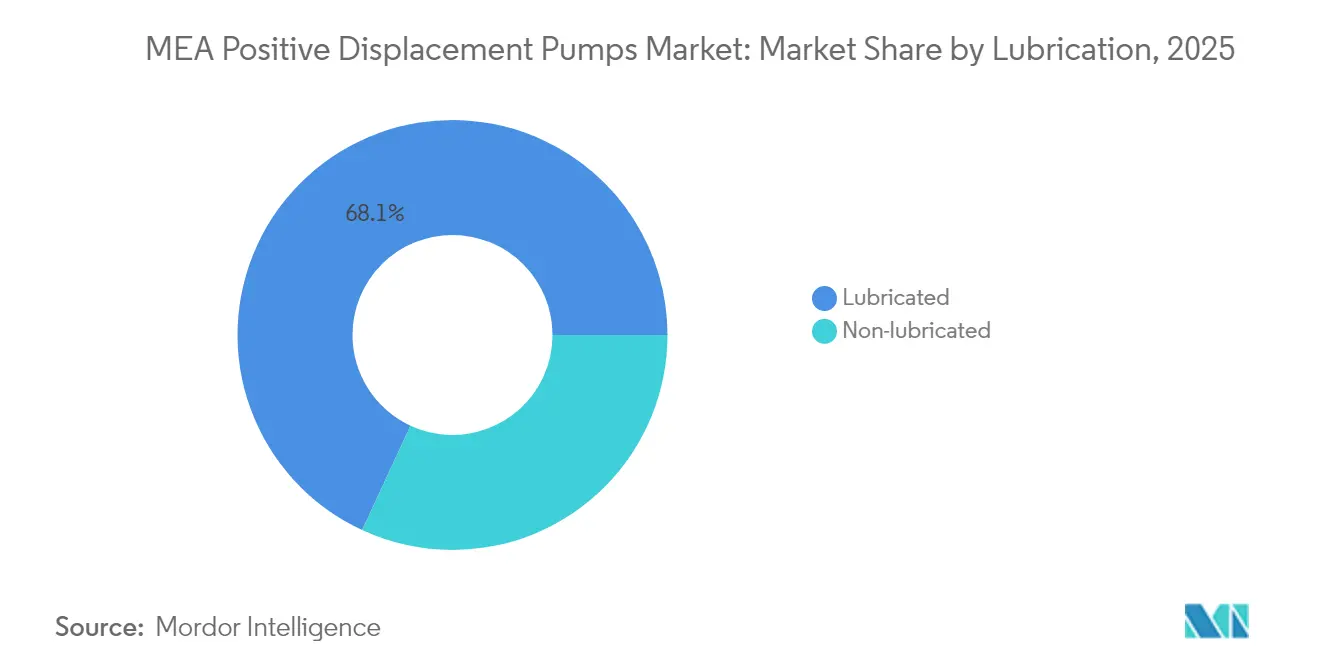

- By lubrication, conventional lubricated designs commanded 68.10% share in 2025; non-lubricated variants lead growth at 3.76% CAGR on contamination-free operation advantages.

- By flow-rate, <10 m³/h models controlled 36.20% of 2025 sales, whereas >200 m³/h pumps represent the fastest growing category with a 4.85% CAGR through 2031.

- By geography, the Middle East generated 69.40% of 2025 revenue; Africa is the fastest progressing region, advancing at a 4.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MEA Positive Displacement Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrial water-reuse mandates | +0.8% | Middle East core, expanding to North Africa | Medium term (2–4 years) |

| Upstream oil and gas project pipeline revival | +1.2% | GCC states, Algeria, Nigeria | Short term (≤ 2 years) |

| Rising CAPEX in African mining and metals | +0.6% | Sub-Saharan Africa, South Africa core | Long term (≥ 4 years) |

| Food-grade pump demand under FSSC 22000 | +0.4% | Regional, with concentration in UAE, South Africa | Medium term (2–4 years) |

| Precision dosing for regional green-hydrogen electrolyzers | +0.3% | Egypt, Saudi Arabia, Morocco | Long term (≥ 4 years) |

| Off-grid solar powered wellhead pumping in arid zones | +0.2% | Nigeria, Algeria, remote Middle East locations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Upstream oil and gas project pipeline revival

Thirty upstream projects passing final investment decision in 2024 unlocked USD 125 billion in spending, with national oil companies eager to capitalize on breakeven costs near USD 47 per barrel.[1]Upstream Online, “Top contractors compete for strategic Middle East gas facility expansion deals for USD 5 billion-plus project,” upstreamonline.com ADNOC Gas alone earmarked USD 5 billion for three gas-processing facility expansions, each requiring high-pressure plunger and diaphragm pumps. Saudi Aramco’s initiative to raise gas output by 60% before 2030 further enlarges the addressable installed base. These developments translate into recurrent demand spikes for rugged rotary screw and reciprocating units able to handle sour gas and multiphase flow, lifting short-cycle orders in the Middle East and Africa positive displacement pump market.

Rapid industrial water-reuse mandates

Severe water scarcity has pushed Saudi Arabia to target 100% wastewater reuse against an 18% baseline, with the National Water Company committing USD 23 billion to sewage upgrades.[2]WaterWorld, “Middle East Gears Up for Water Reuse Technologies,” waterworld.com Industrial facilities are now obliged to install chemical dosing and sludge-handling systems that operate reliably in corrosive environments. Ceramic membrane pilots at Saudi Aramco have already achieved 85–90% recovery rates, cutting fresh-water draws by 22 million gallons annually.[3]Water Tech Online, “Recovering Filter Backwash to Reduce Groundwater Consumption,” watertechonline.com These initiatives favor diaphragm, peristaltic and progressive-cavity pumps configured in duplex stainless steel, sustaining medium-term tailwinds for the Middle East and Africa positive displacement pump market.

Rising CAPEX in African mining and metals

Underground expansion of Botswana’s Karowe diamond mine and Guinea’s Bankan gold project exemplify the USD-intensive pipeline sweeping Sub-Saharan Africa.[4]Modern Mining, “Modern Mining September 2024,” modernmining.com Hard-rock shafts now descend deeper, elevating hydrostatic head and solids loading that outstrip centrifugal capabilities. Positive displacement designs, such as Becker Mining’s PVS 80, delivering 20 l/s at 57 m head, are specified to handle slurry and entrained gas. With critical-mineral exploration ramping up for energy transition supply, the Middle East and Africa positive displacement pump market benefits from a longer-dated order book tied to mine dewatering and reagent dosing.

Food-grade pump demand under FSSC 22000

Regional processors must obtain FSSC 22000 certification to access export chains, prompting upgrades to hygienic lobe, peristaltic and twin-screw pumps capable of clean-in-place routines. UAE beverage plants, South African dairy lines and emerging Nigerian confectionery facilities are shifting toward polished stainless steel constructions with elastomers compliant to FDA and EU regulations. The resulting price premium offsets currency depreciation risks and underpins supplier margins in the Middle East and Africa positive displacement pump market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and TCO versus centrifugal alternatives | -0.7% | Regional, particularly price-sensitive African markets | Short term (≤ 2 years) |

| Skilled-labor scarcity for complex maintenance | -0.5% | Sub-Saharan Africa, remote Middle East locations | Medium term (2-4 years) |

| Proliferation of counterfeit spares eroding reliability | -0.3% | UAE, Nigeria, Egypt | Short term (≤ 2 years) |

| Currency volatility inflating imported component costs | -0.4% | Africa core, Turkey, Egypt | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and TCO versus centrifugal alternatives

Procurement teams frequently judge equipment on upfront cost, a metric where centrifugal pumps offer savings of 20–30% for high-volume, low-viscosity duties. In commodity-linked African economies, cash-constrained operators select single-stage volutes even when duty conditions favor positive displacement geometry. Vendors respond with energy-efficient upgrades: Wear Reduction Technology embedded in Weir’s WARMAN AH line cuts power draw by up to 5%, narrowing lifetime-cost differentials.

Proliferation of counterfeit spares eroding reliability

Authorities in the UAE confiscated 4 000 fake water pumps retailing at one-third the authentic price. Substandard wear parts cause unplanned shutdowns, tarnish equipment reputations and inflate warranty claims. The threat is especially acute in hazardous-duty oil and gas installations where gasket failure can trigger environmental penalties. Manufacturers are expanding QR-code traceability and authorized service networks to restore confidence and safeguard growth in the Middle East and Africa positive displacement pump market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Displacement Principle: Rotary dominance continues while peristaltic gains

Rotary pumps generated 28.15% of 2025 revenue, underlining their entrenched role in viscous-fluid transfer across upstream oil and gas and asphalt blending. Diaphragm and piston reciprocating models together carved out a sizable niche on the strength of leak-free operation when handling aggressive chemicals. The Middle East and Africa positive displacement pump market size for peristaltic designs is projected to climb at a 3.67% CAGR as pharmaceutical formulators shift to single-use tubing for sterility assurance.

Technology roadmaps show gear pumps retaining cost leadership for moderate-pressure duties below 10 bar, while progressive-cavity machines penetrate slurry handling owing to resilient stator materials. Vogelsang’s EP series one-piece housing rated to 260 psi and 392 °F demonstrates the innovation thrust toward higher pressure envelopes. Providers are also hybridizing rotary and reciprocating architectures to optimize efficiency at variable flow demands, a trend poised to broaden solution palettes and defend pricing in the Middle East and Africa positive displacement pump market.

By End-user Industry: Oil and gas holds leadership as healthcare drives growth

Oil and gas accounted for 30.85% of 2025 sales thanks to multiphase transfer, chemical injection and blowout-preventer circuits that demand rugged plunger and twin-screw units able to manage gas entrainment. Water and wastewater followed at 26.52% on the back of desalination and sewage-network upgrades. Chemicals and petrochemicals benefiting from regional downstream integration strategies. Pharmaceuticals, while occupying a smaller base, will pace the market with a 3.74% CAGR through 2031 as sterile processing lines proliferate across UAE, Egypt and Saudi greenfield plants.

Food and beverage manufacturers energized by Gulf food-security programs favoring local production. In mining and metals, a 9.65% share hinged on abrasion-resistant pumping during dewatering and concentrate transfer. Diversifying end-markets distributes risk and cushions revenue swings, reinforcing the resilient outlook for the Middle East and Africa positive displacement pump market.

By Material: Cast-iron ubiquity coexists with specialty alloy surge

Cast-iron casings delivered 46.12% of 2025 turnover, reflecting affordability and sufficient corrosion resistance in non-aggressive water duties. Stainless steel reached 34.58% as sanitary and chemical services broadened. Specialty alloys, including duplex stainless, Hastelloy and chrome iron, register an 4.12% CAGR to 2031, propelled by high-temperature hydrocarbon processing and acidic leach circuits.

Investment in localized alloy machining, notably at Johannesburg tooling clusters, is cutting lead times for replacement stators and rotors. Becker Mining’s adoption of 28% chrome iron for hard-rock pumps demonstrates the performance dividend of metallurgical upgrades. As end-users weigh lifecycle costs, demand for premium alloys will steadily expand the Middle East and Africa positive displacement pump market size.

By Lubrication: Maintenance culture steers adoption patterns

Lubricated assemblies captured 68.10% of 2025 revenue because they align with entrenched maintenance protocols in refineries and power stations. Nevertheless, contamination-sensitive industries embrace non-lubricated magnetic-drive and canned-motor designs that eliminate oil leakage risk.

Vendors emphasize extended-life bearings and dry-run tolerant elastomers to bridge the reliability perception gap, enhancing competitive footing. Momentum toward predictive maintenance via cloud-enabled vibration sensors further differentiates premium offers in the Middle East and Africa positive displacement pump market.

By Flow-rate: Precision segment still leads while large-volume units accelerate

Pumps rated below 10 m³/h maintained a 36.20% share in 2025, underpinning chemical dosing and laboratory synthesis tasks requiring ±1% flow accuracy. Units between 10–50 m³/h followed at 34.10%. Although >200 m³/h pumps form a smaller slice, their 4.85% CAGR underscores rising infrastructure megaprojects such as Egypt’s government-led irrigation schemes that specified Torishima multi-plunger trains.

Atlas Copco’s expansion of the WEDA submersible range with Wear Deflector Technology evidences engineering focus on high-volume pit and tunnel dewatering. This polarization between micro-dosing and bulk transfer reinforces the need for diverse product portfolios to secure wallet share in the Middle East and Africa positive displacement pump market.

Geography Analysis

The Middle East delivered 69.40% of 2025 revenue owing to energy-sector intensity and robust public-works outlays. Saudi Arabia’s wastewater-reuse vision and Qatar’s LNG expansion assure recurring project streams, keeping distributors’ order books healthy. The UAE’s diversified economy adds pharmaceutical, food and semiconductor capacity that requires hygienic pumping solutions. Turkish demand remains stable although lira depreciation poses import hurdles. The regional installed base is increasingly monitored via digital twins, improving mean-time-between-service and favoring value-added service contracts.

Africa supplied 30.60% of 2025 sales yet is growing faster at 4.05% CAGR. South Africa anchors the installed base through mature deep-level mining where chrome-iron casings extend pump life. Nigeria invests in wellhead remediation and modular refineries, triggering calls for chemical-injection skids. Egypt’s emergence as a production hub, illustrated by Xylem’s pump plant in 10th of Ramadan City, encourages supply-chain localization and price competitiveness.

Currency volatility remains a cross-cutting risk; rand depreciation has inflated imported spare-part costs by double digits, narrowing OEM market reach. Governments and multilaterals are responding by funding turnkey water and power assets, cushioning procurement budgets. As infrastructure densifies and mining CAPEX accelerates, Africa’s contribution to the Middle East and Africa positive displacement pump market size will keep edging higher through the decade.

Competitive Landscape

The playing field is moderately fragmented: global majors such as Atlas Copco, Xylem, Grundfos and Flowserve coexist with regional specialists and rental firms. Top-five suppliers collectively control an estimated 60–65% of revenue, leaving room for niche entrants focused on hygienic, solar-ready or high-pressure applications. Atlas Copco’s EUR 5 million (USD 5.88 Million) acquisition of Integrated Pump Rental strengthens its footprint in Sub-Saharan Africa’s mining and construction segments. Xylem’s Egyptian factory highlights strategic localization that cuts delivery cycles from 16 weeks to 6 weeks and lowers landed costs.

Differentiation levers center on energy efficiency, wear-life, and digital monitoring. Vendors introducing duplex-steel rotors and low-shear screw geometries justify 10–15% price premiums. Service models are shifting toward outcome-based contracts guaranteeing uptime, aligning incentives with end-user productivity goals. Counterfeit mitigation through blockchain provenance tags and QR-code spare-part authentication is gaining traction, enhancing brand integrity in the Middle East and Africa positive displacement pump market.

Emergent challengers target solar-powered wellhead lifting where remote Nigerian operations lack grid access. Others focus on FSSC 22000-certified designs for regional food exporters pursuing zero-recall reputations. These white-space plays ensure competitive intensity stays balanced, sustaining innovation velocity across materials science, sealing solutions and IIoT integration.

MEA Positive Displacement Pumps Industry Leaders

-

Dover Corporation

-

Ingersoll Rand Inc.

-

Alfa Laval AB

-

Gorman-Rupp Company

-

Watson-Marlow Fluid Technology Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Roto Pumps unveiled advanced manufacturing infrastructure and launched P Range compact pumps targeting USD 100 million revenue by 2028, with an emphasis on oil and gas, mining, and wastewater applications.

- August 2024: Atlas Copco acquired South-African pump rental specialist Integrated Pump Rental for EUR 5 million, bolstering dewatering services in Sub-Saharan mines.

- July 2024: Xylem Egypt plant celebrated its first operational year, producing split-case and end-suction models for regional markets under a joint venture with Tiba Manzalawi Group.

- June 2024: Torishima secured large pump orders for an Egyptian irrigation project, reflecting agricultural infrastructure investment momentum.

MEA Positive Displacement Pumps Market Report Scope

The market is defined by the revenue generated from the sale of positive displacement pumps offered by different market players for a diverse range of end-user applications across the Middle East and Africa. Market trends are evaluated by analyzing investments made in product innovation, diversification, and expansion. Advancements in the oil and gas, chemicals, food and beverage, water and wastewater, pharmaceuticals, power generation, and other industries are also crucial in determining the market's growth.

The Middle East and Africa Positive Displacement Pump Market Report is Segmented by Displacement Principle (Rotary Pumps, Reciprocating Pumps), End-user Industry (Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Food and Beverage, Power Generation, Pharmaceuticals and Life-Sciences, Mining and Metals, Other Industries), Material (Cast Iron, Stainless Steel, Alloy and Specialty Metals), Lubrication (Lubricated, Non-lubricated), Flow-rate (<10, 10–50, 50–200, >200 m³/h), and Geography (Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Displacement Principle

| Rotary Pumps | Gear |

| Lobe | |

| Screw (Single, Twin, Triple) | |

| Vane | |

| Reciprocating Pumps | Diaphragm |

| Piston/Plunger | |

| Peristaltic |

By End-user Industry

| Oil and Gas |

| Chemicals and Petrochemicals |

| Water and Wastewater |

| Food and Beverage |

| Power Generation |

| Pharmaceuticals and Life-Sciences |

| Mining and Metals |

| Other Industries |

By Material

| Cast Iron |

| Stainless Steel |

| Alloy and Specialty Metals |

By Lubrication

| Lubricated |

| Non-lubricated |

By Flow-rate (cubic meter/hour)

| Less than 10 |

| 10-50 |

| 50-200 |

| More than 200 |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Turkey | |

| Rest of Middle East | |

| Africa | Nigeria |

| Egypt | |

| Algeria | |

| South Africa | |

| Kenya | |

| Rest of Africa |

| By Displacement Principle | Rotary Pumps | Gear |

| Lobe | ||

| Screw (Single, Twin, Triple) | ||

| Vane | ||

| Reciprocating Pumps | Diaphragm | |

| Piston/Plunger | ||

| Peristaltic | ||

| By End-user Industry | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Water and Wastewater | ||

| Food and Beverage | ||

| Power Generation | ||

| Pharmaceuticals and Life-Sciences | ||

| Mining and Metals | ||

| Other Industries | ||

| By Material | Cast Iron | |

| Stainless Steel | ||

| Alloy and Specialty Metals | ||

| By Lubrication | Lubricated | |

| Non-lubricated | ||

| By Flow-rate (cubic meter/hour) | Less than 10 | |

| 10-50 | ||

| 50-200 | ||

| More than 200 | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| Egypt | ||

| Algeria | ||

| South Africa | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Middle East and Africa positive displacement pump market in 2031?

The market is projected to reach USD 684.02 million by 2031, growing at a 3.32% CAGR from 2026.

Which displacement principle is expected to grow fastest in the region?

Peristaltic pumps are poised for a 3.67% CAGR through 2031 on strong demand in pharmaceutical and food applications.

Why are non-lubricated pumps gaining popularity?

They eliminate oil contamination risk and reduce maintenance, making them attractive for pharmaceuticals, food processing and remote solar-powered installations.

What major risk could slow market growth?

The spread of counterfeit spare parts undermines equipment reliability and erodes user trust, particularly in price-sensitive markets.

Page last updated on: