Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

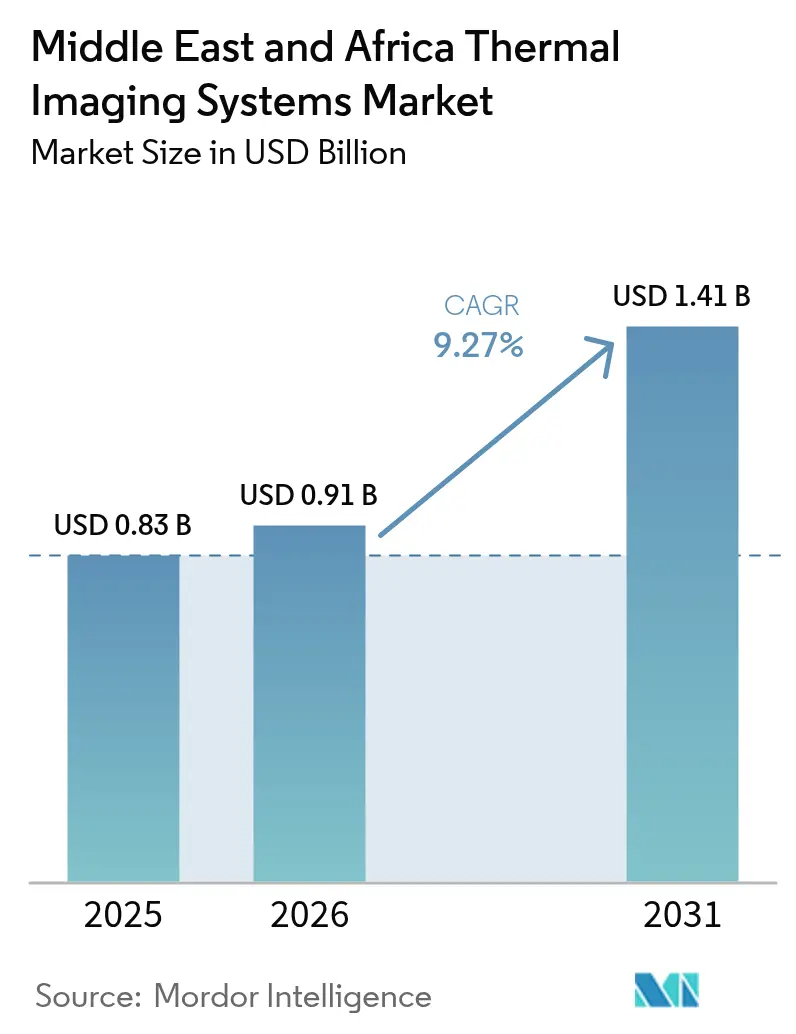

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 9.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Thermal Imaging Systems Market Analysis by Mordor Intelligence

The Middle East And Africa Thermal Imaging Systems Market size is projected to expand from USD 0.83 billion in 2025 and USD 0.91 billion in 2026 to USD 1.41 billion by 2031, registering a CAGR of 9.27% between 2026 to 2031.

Rising demand for predictive maintenance in oil and gas, smart-city surveillance, and Gulf Cooperation Council defense modernization is expanding the addressable base for both cooled and uncooled solutions. Hardware continues to anchor revenue thanks to large-scale fixed-camera deployments on borders, ports, and energy assets, while recurring calibration, training, and analytics subscriptions are steering spending toward services. Wider availability of low-cost microbolometers and edge-AI chipsets is moving the thermal imaging systems market beyond its military core into commercial building inspection, automotive driver-assistance, and logistics. U.S. and European primes dominate high-end cooled platforms, Chinese vendors are gaining share in commercial fixed cameras, and start-ups are democratizing handheld diagnostics for small contractors.

Key Report Takeaways

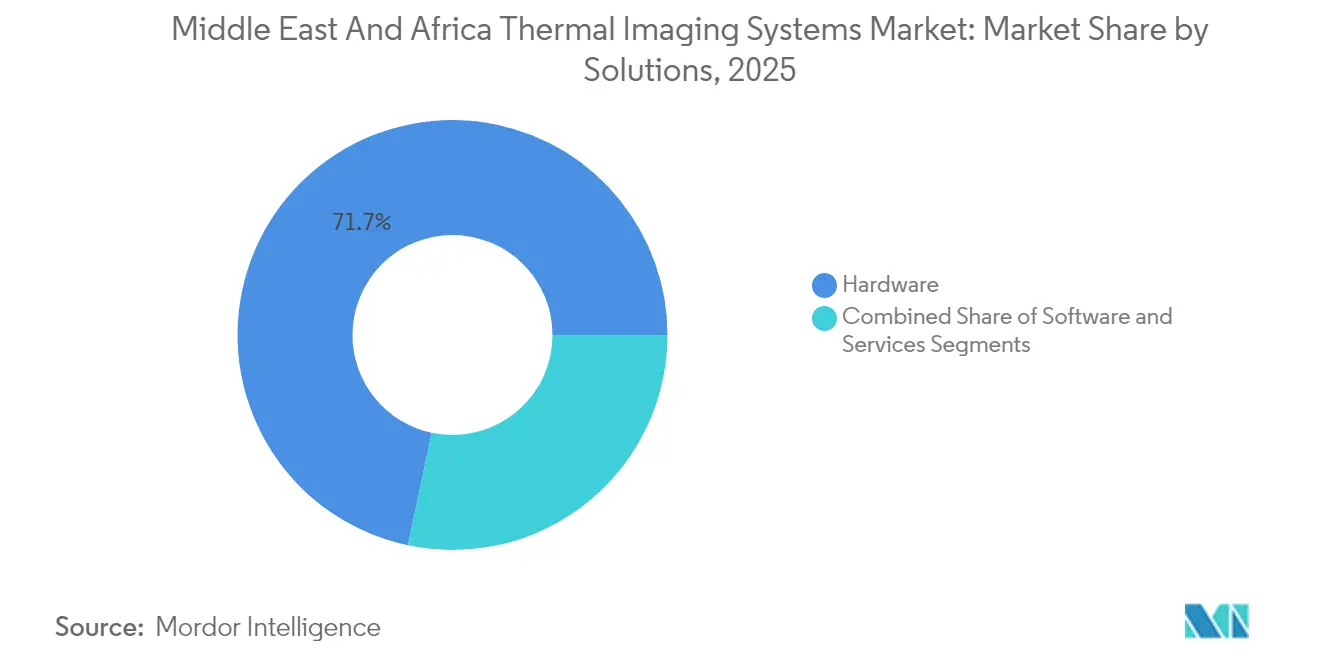

- By solutions, hardware led with 71.68% revenue share in 2025; services are projected to advance at a 10.39% CAGR through 2031.

- By product type, fixed thermal cameras accounted for 58.05% of the thermal imaging systems market share in 2025, whereas handheld units are expected to post a 9.64% CAGR to 2031.

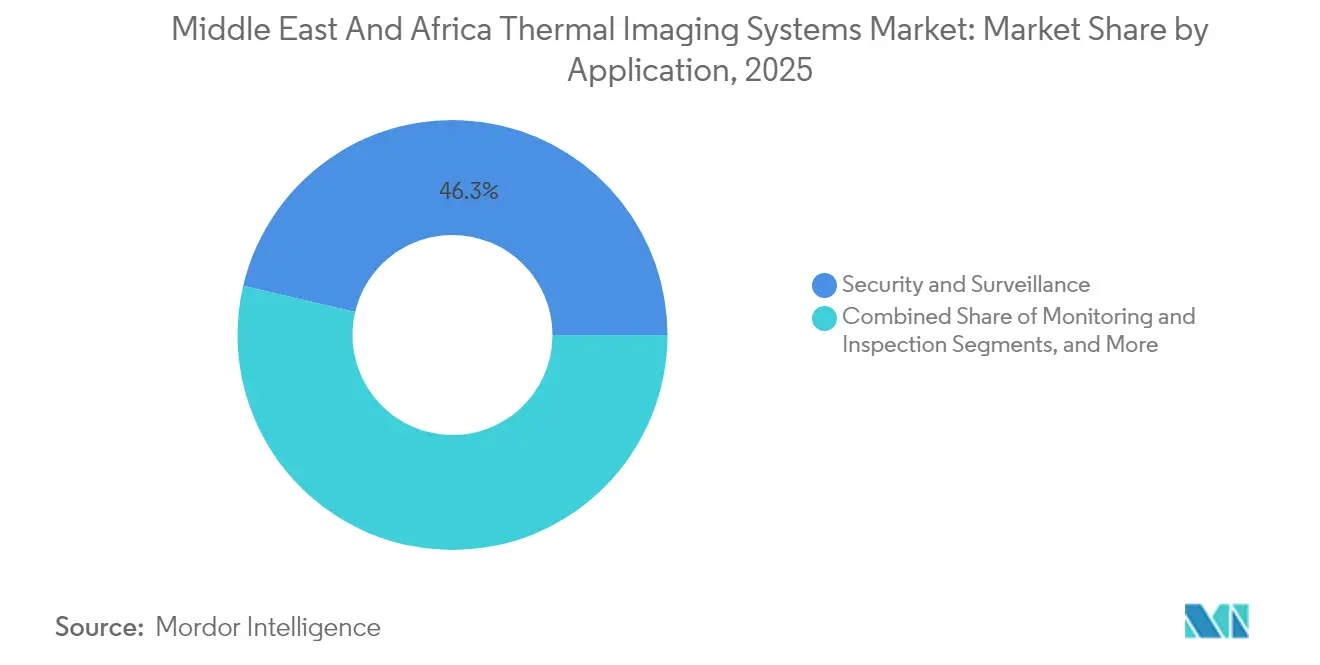

- By application, security and surveillance captured 46.32% revenue in 2025, while monitoring and inspection is set to grow at a 10.17% CAGR through 2031.

- By end-user, aerospace and defense occupied 54.06% spending in 2025; oil and gas is forecast to expand at an 11.54% CAGR over the same period.

- By Country, Saudi Arabia commanded 37.74% of regional revenue in 2025; Africa is positioned for a 10.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Thermal Imaging Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Defense modernization programs across GCC states | +2.3% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Expanding oil and gas predictive maintenance requirements | +2.1% | Saudi Arabia, UAE, Kuwait, South Africa | Long term (≥ 4 years) |

| Rapid urban security investments through smart-city initiatives | +1.8% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2-4 years) |

| Lower-cost uncooled sensors boosting commercial adoption | +1.5% | UAE, Saudi Arabia, South Africa | Short term (≤ 2 years) |

| AI-enabled thermal-vision analytics improving ROI | +1.2% | Saudi Arabia, UAE, South Africa | Medium term (2-4 years) |

| Advent of rugged, drone-mounted thermal payloads for desert operations | +1.0% | Saudi Arabia, UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Defense Modernization Programs Across GCC States

Regional militaries are refreshing legacy electro-optical suites with third-generation thermal imagers that extend detection ranges and enable multispectral fusion. Saudi Arabia’s State Authority for Military Industries signed a 2024 memorandum with Hensoldt to localize production, underscoring the push for indigenous capability. Parallel U.S. Army awards to Teledyne FLIR for vehicle sensor systems cascade into foreign military sales channels and guide GCC specifications toward cooled mid-wave infrared arrays. Export-license bottlenecks persist, yet bilateral agreements are trimming approval cycles for trusted Gulf partners. As a result, hardware revenue rises while automatic target-recognition algorithms open recurring software opportunities.

Expanding Oil and Gas Predictive Maintenance Requirements

National oil companies now fuse thermal data with vibration and historian feeds to predict failures weeks ahead. Abu Dhabi National Oil Company rolled out AIQ’s Neuron 5 platform across upstream assets in 2024. Saudi Aramco’s 2024 contract with Gecko Robotics highlights robotic ultrasonic and thermal inspections that displace scaffold-based surveys and avert costly shutdowns. Drone-mounted cameras scan flare stacks and subsea lines for hotspots that signal corrosion or leaks, embedding thermal vision into digital-twin workflows. Cost avoidance from averted outages, often exceeding USD 20 million per incident, validates multiyear inspection budgets.

Rapid Urban Security Investments Through Smart-City Initiatives

Gigaprojects such as NEOM in Saudi Arabia and Dubai’s expanding smart-traffic grid integrate fixed thermal cameras for perimeter security, crowd monitoring, and autonomous-vehicle navigation. Dubai’s Roads and Transport Authority added thermal vision to incident-detection loops in 2024, cutting response times on major arterials.[1]Dubai Roads and Transport Authority, “Smart Traffic Management System,” rta.ae Egypt’s New Administrative Capital mirrors this model across government buildings and transit hubs. Municipal buyers favor turnkey packages that couple cameras, cloud analytics, and cyber-secure data handling, converting one-off purchases into subscription revenue.

Lower-Cost Uncooled Sensors Boosting Commercial Adoption

Microbolometer prices below USD 100 and smartphone-compatible add-ons under USD 500 are moving the thermal imaging systems market into small construction firms and home inspectors. Magna International shipped over 1.2 million automotive thermal-sensing units by 2024 and will release its fifth-generation platform in 2025, anticipating a USD 500 million opportunity as advanced driver-assistance gains regulatory backing. Affordable handhelds priced under USD 1,000 now diagnose HVAC inefficiencies and electrical hotspots for small enterprises in the UAE and South Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and maintenance costs for cooled platforms | −1.4% | Saudi Arabia, UAE, South Africa | Long term (≥ 4 years) |

| Stringent export-control regimes limiting sensor availability | −1.1% | Africa (excl. South Africa), select Middle East | Long term (≥ 4 years) |

| Shortage of certified thermography professionals | −0.9% | South Africa, Kenya, Nigeria, Saudi Arabia, UAE | Medium term (2-4 years) |

| Performance degradation from dust, humidity, and extreme heat | −0.7% | Saudi Arabia, UAE, Qatar, Kuwait, North Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Maintenance Costs for Cooled Platforms

Cooled mid-wave detectors exceed USD 50,000 per unit and rely on cryogenic coolers that demand six-month service intervals in sandy environments. Budget-constrained agencies in Africa and minor Gulf states therefore default to uncooled alternatives or defer projects, slowing top-line growth. Leasing models that shift maintenance risk to vendors are emerging but hinge on creditworthy buyers and predictable regulatory frameworks.

Stringent Export-Control Regimes Limiting Sensor Availability

ITAR and Wassenaar rules cap frame rate and pixel counts for many African buyers, stretching approval cycles to a year.[2]U.S. Department of State, Directorate of Defense Trade Controls, “ITAR Regulations,” pmddtc.state.gov Western suppliers thus lean toward GCC markets while Chinese vendors ship lower-spec, license-free options into Africa, fragmenting the supply chain and limiting interoperability among regional forces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solutions: Hardware Remains Dominant, Services Accelerate

Hardware generated 71.68% of revenue in 2025, reflecting sustained procurement of cameras, lenses, and detector modules for defense borders, oil terminals, and smart-city grids. The thermal imaging systems market size for hardware is projected to expand steadily as governments fund perimeter upgrades. Services, however, will outpace all other categories at a 10.39% CAGR as operators lock in calibration, analytics, and training contracts that convert capital layouts into predictable operating expenses. Early adopters such as Advanced Energy Industries bundle annual service plans, fostering sticky client relationships.

The services trajectory also addresses the regional shortage of certified thermographers. Training providers in the UAE and South Africa charge up to USD 1,900 for Level II certification, and the 2024 launch of the Certified Thermographers Network – Africa aims to harmonize standards across 20-plus countries. Software revenue follows hardware penetration, as cloud-hosted dashboards and edge-AI engines monetize data streams over multiyear cycles.

By Product Type: Fixed Cameras Lead, Handhelds Gain Traction

Fixed installations commanded 58.05% revenue in 2025 owing to large-area surveillance of borders, airports, and petro-chemical hubs. These systems integrate with visible-light cameras and radars, enabling layered situational awareness. Handheld units will post a 9.64% CAGR through 2031 as price points fall below USD 5,000 and smartphone add-ons popularize point-and-shoot diagnostics for electricians and building inspectors.

Teledyne FLIR’s Hadron 640 and Gremsy’s Vio F1 illustrate how miniaturized modules blur delineations between fixed and mobile platforms. Demand also comes from utilities that now issue handheld cameras to line crews for real-time fault detection. Consequently, the thermal imaging systems market share for handhelds is set to widen as field diagnostics embed infrared checks into daily workflows.

By Application: Security Rules, Monitoring Surges

Security and surveillance absorbed 46.32% of total demand in 2025 as regional governments invested in border fences, port checkpoints, and airport aprons. GCC militaries specify 1280 × 1024 detectors for 5-kilometer human classification, underpinning hardware orders. Monitoring and inspection, however, will climb at a 10.17% CAGR to 2031 as oil and gas, utilities, and food plants shift toward condition-based maintenance regimes that rely on continuous infrared feeds to flag overheating assets.

Fever screening, gas-leak detection, and laboratory research constitute the detection-and-measurement subset. Post-pandemic public-health mandates sustain temperature-screening lanes at high-traffic sites, while petro-chemical plants deploy optical gas imaging to visualize methane plumes invisible to the naked eye.

By End-User: Defense Still Largest, Oil and Gas Fastest

Aerospace and defense captured 54.06% spending in 2025 on the back of armored-vehicle retrofits and night-vision upgrades integrated into combined-arms platforms. The thermal imaging systems market size for defense is set to expand, but oil and gas will surpass all others in momentum with an 11.54% CAGR as upstream operators embed thermal lenses into digital-twin dashboards that trigger predictive work orders. Automotive OEMs likewise prepare for regulatory mandates on automatic emergency braking, driving future volume orders for long-wave infrared cameras.

Healthcare adoption includes non-contact neonatal monitoring and vein visualization, while food processors verify cooking temperatures and seal integrity to meet export compliance. Such varied use cases broaden the revenue pyramid, reducing over-reliance on a single vertical.

Geography Analysis

Saudi Arabia retained 37.74% regional revenue in 2025, supported by Vision 2030 localization goals, Aramco’s refinery-inspection digitization, and NEOM’s smart-city build-out. The kingdom’s procurement scale yields favorable unit economics for cooled mid-wave arrays, and domestic assembly partnerships hint at future cost reductions. The United Arab Emirates ranks second, leveraging ADNOC’s predictive-maintenance rollouts and Dubai’s AI-driven traffic management to keep pipeline inspection and urban safety budgets buoyant.

Turkey’s defense programs, coupled with in-house detector fabrication at Aselsan, secure steady demand. Africa, forecast to grow 10.03% through 2031, is led by South African border-security upgrades and Kenyan wildlife-conservation initiatives that deploy drone-borne cameras. Fragmented regulations and service voids remain hurdles, yet Chinese suppliers tap this gap with bundled video-analytics packages priced well below Western offerings. Nigeria, Egypt, and Morocco emerge as mid-tier adopters in oil and gas and critical-infrastructure protection, albeit constrained by licensing delays and limited technician pools.

Across the rest of the Middle East-Qatar, Kuwait, Oman, Bahrain, Iraq, Jordan, and Lebanon smaller yet rising budgets target airport expansions, offshore-platform safety, and petro-chemical asset integrity. Public-private concession models spread capital costs across decades, making subscription-based thermal services attractive for municipalities. The thermal imaging systems market continues to normalize from a defense-heavy posture to a multipronged tool for operational safety, logistics, and urban governance.

Competitive Landscape

The thermal imaging systems market features moderate concentration. Six Western defense primes Teledyne FLIR, L3Harris, Lockheed Martin, BAE Systems, Leonardo DRS, and Elbit Systems command the majority of cooled-detector sales, leveraging proprietary fabrication, ruggedization know-how, and embedded relationships with defense ministries. Chinese manufacturers such as Hangzhou Hikvision, Guide Infrared, and Zhejiang Dali supply price-competitive 384 × 288 and 640 × 512 uncooled cameras bundled with video-management software, rapidly scaling commercial installations across seaports and industrial parks.

Thermoteknix, Testo, Optris, and Ametek-Land specialize in high-accuracy radiometric devices for process control and scientific research, differentiating on calibration traceability and ISO 9001 compliance. North American start-ups, notably Seek Thermal and Infrared Cameras Inc., democratize handheld imaging under USD 500, expanding the user base among facility managers and electricians.

Technology integration sets competitive boundaries. Vendors embedding edge-AI inference chips reduce latency and bandwidth costs, critical for remote oil platforms and desert outposts. Compliance with ITAR and Wassenaar export regimes further segments suppliers: Western primes emphasize license support for GCC allies, while Chinese firms address less-restricted African buyers. Emerging white-space lies in autonomous-vehicle perception stacks, drone payloads for offshore inspections, and transformer health analytics in power grids.

Middle East And Africa Thermal Imaging Systems Industry Leaders

Teledyne FLIR LLC

L3Harris Technologies Inc.

Lockheed Martin Corporation

BAE Systems plc

Leonardo DRS Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Teledyne FLIR won a USD 168 million U.S. Army contract for the Next-Generation Brigade Combat Team Reconnaissance Vehicle sensor suite, with options for Middle Eastern foreign military sales.

- November 2024: RTX’s Raytheon unit received USD 86.7 million for third-generation FLIR B-Kit upgrades, enhancing armored-vehicle thermal ranges.

- August 2024: Leonardo DRS secured a USD 117 million award for the Family of Weapon Sights-Individual, set to reach GCC allies via foreign military channels.

- July 2024: Teledyne FLIR booked USD 15 million for ThermoSight HISS-XLR long-range weapon sights tailored to desert operations.

Middle East And Africa Thermal Imaging Systems Market Report Scope

The Middle East and Africa industries are increasingly adopting thermal imaging technologies, which enhance visibility, safety, and operational efficiency. With thermal cameras becoming increasingly pivotal in security, surveillance, monitoring, and measurement, the study examines the demand drivers and technological advancements propelling the growth of this market.

The Middle East and Africa Thermal Imaging Systems Market Report is Segmented by Solutions (Hardware, Software, Services), product type (Fixed Thermal Cameras, Handheld Thermal Cameras), Application (Security and Surveillance, Monitoring and Inspection, Detection and Measurement), End-User (Aerospace and Defense, Automotive, Healthcare and Life Sciences, Oil and Gas, Food and Beverages, Other end-users), and Country (Middle East [Saudi Arabia, UAE, Turkey, Rest of Middle East], Africa [South Africa, Kenya, Rest of Africa]). The Market Forecasts are Provided in Terms of Value (USD).

By Solutions

| Hardware |

| Software |

| Services |

By Product Type

| Fixed Thermal Cameras |

| Handheld Thermal Cameras |

By Application

| Security and Surveillance |

| Monitoring and Inspection |

| Detection and Measurement |

By End-user

| Aerospace and Defense |

| Automotive |

| Healthcare and Life Sciences |

| Oil and Gas |

| Food and Beverages |

| Other End-users |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Solutions | Hardware | |

| Software | ||

| Services | ||

| By Product Type | Fixed Thermal Cameras | |

| Handheld Thermal Cameras | ||

| By Application | Security and Surveillance | |

| Monitoring and Inspection | ||

| Detection and Measurement | ||

| By End-user | Aerospace and Defense | |

| Automotive | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Food and Beverages | ||

| Other End-users | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East and Africa thermal imaging systems market in 2031?

The Middle East and Africa thermal imaging systems market is expected to reach USD 1.41 billion by 2031, supported by a 9.27% CAGR.

Which segment is growing fastest by solutions?

Services are forecast to post a 10.39% CAGR as buyers shift toward calibration, training, and analytics subscriptions.

How much of the market does Saudi Arabia currently hold?

Saudi Arabia accounted for 37.74% of regional revenue in 2025.

Why are handheld thermal cameras gaining popularity?

Falling prices below USD 5,000 and smartphone-compatible devices under USD 500 are enabling on-demand diagnostics for utilities, construction, and facility maintenance.

Which application is forecast to accelerate the most?

Monitoring and inspection is set to expand at a 10.17% CAGR as industries move toward condition-based maintenance.

What restrains adoption of cooled thermal platforms?

Acquisition costs above USD 50,000 and high maintenance demands limit uptake among budget-constrained agencies, especially in Africa and smaller Gulf nations.

Page last updated on: