Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

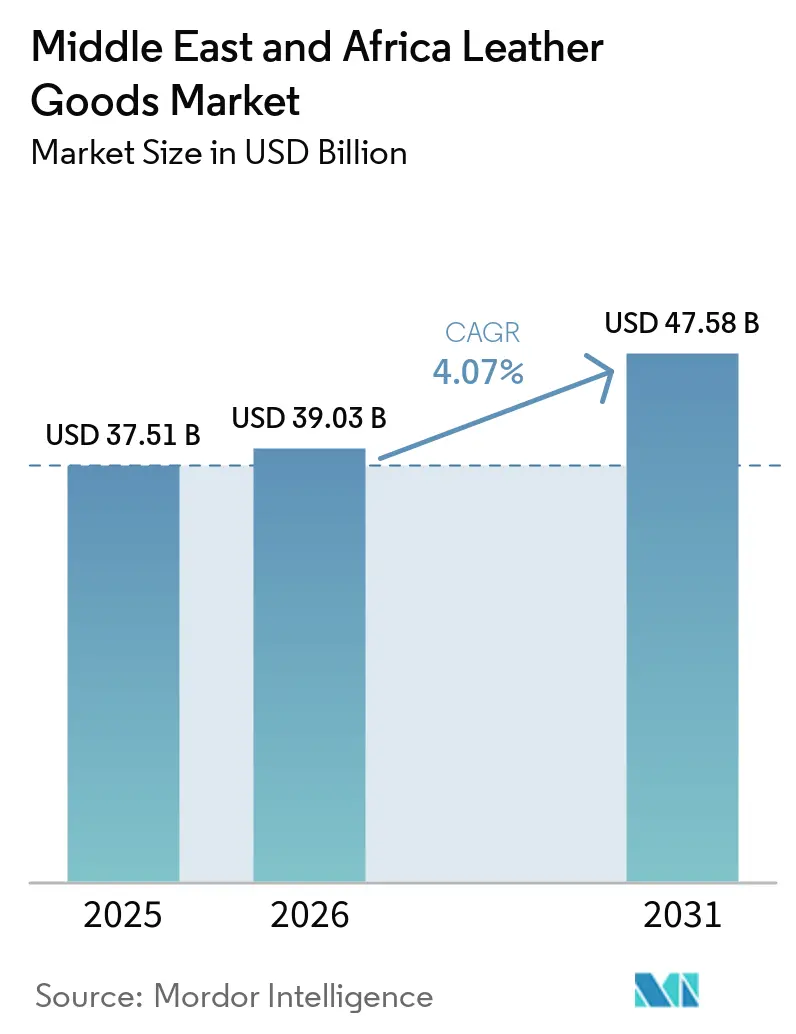

| Base Year Market Size (2025) | USD 37.51 Billion |

| Market Size (2026) | USD 39.03 Billion |

| Market Size (2031) | USD 47.58 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Leather Goods Market Analysis by Mordor Intelligence

The Middle East and Africa leather goods market size was valued at USD 37.51 billion in 2025 and estimated to grow from USD 39.03 billion in 2026 to reach USD 47.58 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031). The market's expansion is primarily attributed to the region's strategic economic diversification initiatives and increasing consumer purchasing power, particularly evident in Gulf Cooperation Council nations, where evolving luxury consumption behaviors are fundamentally restructuring traditional retail frameworks. Furthermore, the implementation of progressive regulatory reforms has facilitated enhanced foreign investment opportunities, establishing a robust foundation for sustained premium goods consumption across both mature and emerging consumer demographics. This market evolution reflects the region's broader economic transformation and increasing integration into global luxury retail networks, positioning it as a significant participant in the international leather goods trade.

Key Report Takeaways

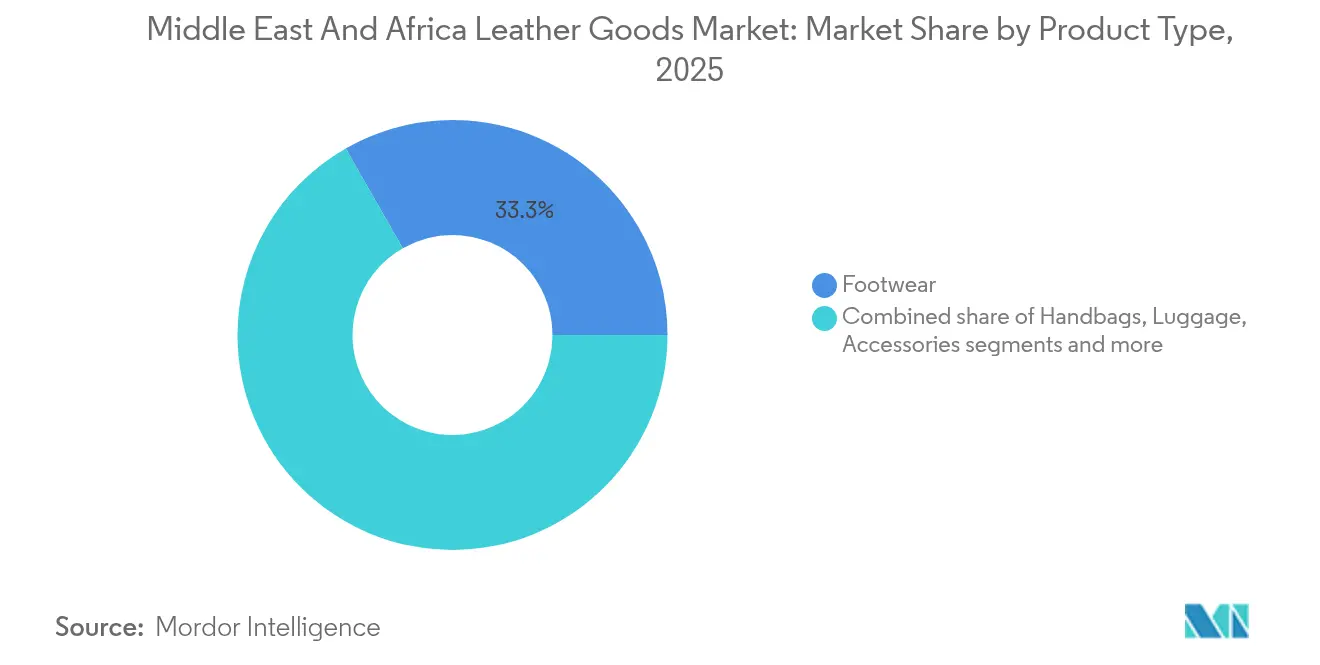

- By product type, footwear led with 33.27% of the Middle East and Africa leather goods market share in 2025, whereas accessories are projected to grow at a 4.32% CAGR from 2026 to 2031.

- By end user, men captured 55.08% share of the Middle East and Africa leather goods market size in 2025, while the women segment is set to advance at 4.44% CAGR through 2031.

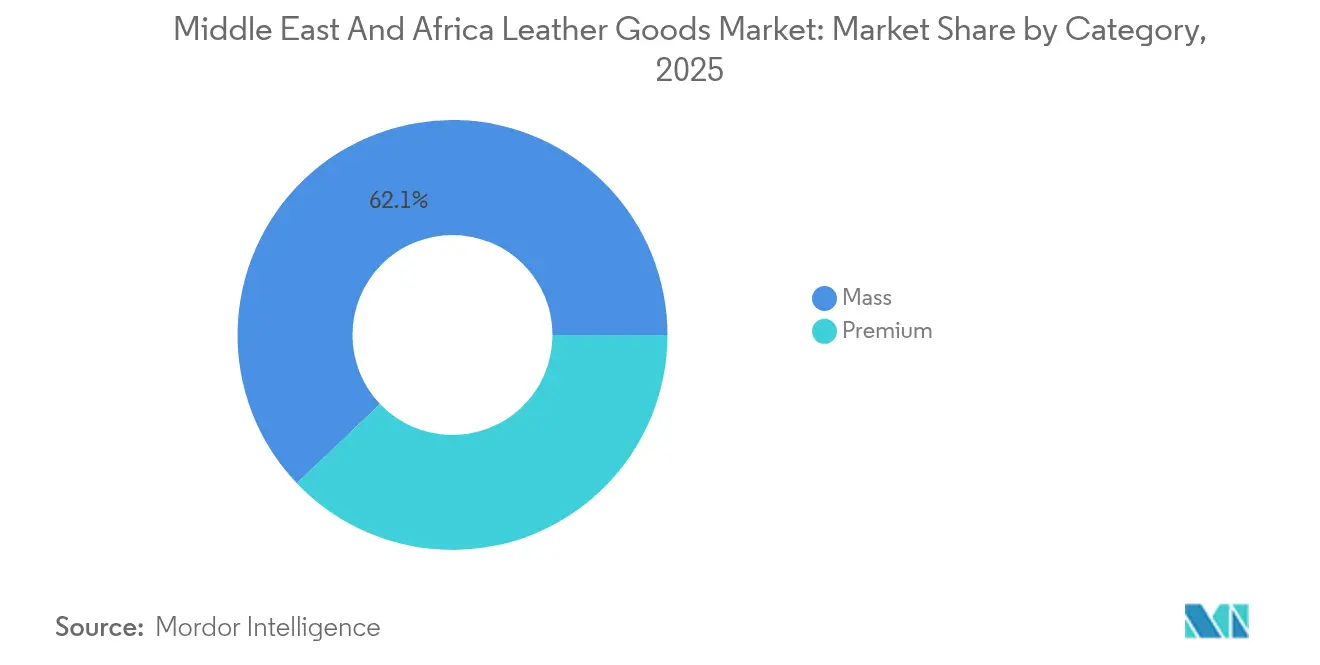

- By category, the mass segment dominated with 62.11% revenue share in 2025; the premium segment is forecast to expand at 4.66% CAGR to 2031.

- By distribution channel, offline stores accounted for 71.12% of revenue in 2025, but online stores are expected to post a 4.88% CAGR between 2026 and 2031.

- By geography, Turkey captured 28.41% of regional revenue in 2025, and South Africa is the fastest-growing market at 5.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Leather Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for luxury goods | +1.2% | United Arab Emirates, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Increasing popularity of synthetic (vegan) leather | +0.8% | United Arab Emirates, Turkey, Saudi Arabia | Long term (≥ 4 years) |

| Technological advancements in manufacturing | +0.6% | Turkey, Egypt, South Africa | Short term (≤ 2 years) |

| Fashion trends and consumer preferences | +0.9% | United Arab Emirates, Saudi Arabia, Nigeria | Medium term (2-4 years) |

| Influence of brand awareness and celebrity endorsements | +0.4% | Nigeria, United Arab Emirates, South Africa | Short term (≤ 2 years) |

| Focus on craftsmanship and premium quality | +0.7% | Morocco, Turkey, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Luxury Goods

The Middle East and Africa (MEA) leather goods market is experiencing significant growth, driven by increasing demand for luxury products. Economic prosperity, particularly in Gulf Cooperation Council (GCC) countries, has increased consumer disposable income, enabling purchases of premium leather products. The average monthly household disposable income in Saudi Arabia amounted to SAR 11,839, based on the 2023 Household Income and Consumption Expenditure Statistics published by the General Authority for Statistics (GASTAT) [1]Source: General Authority for Statistics, "Household Income and Consumption Expenditure Survey Publication 2023", stats.gov.sa . The region's young, fashion-conscious population actively seeks global luxury brands. The cultural significance of luxury goods in the Middle East and Africa (MEA) region, where leather products are viewed as symbols of status and achievement, further strengthens market demand. Consumers are drawn to leather goods for their durability, craftsmanship, and ability to convey social status.

Increasing Popularity of Synthetic (Vegan) Leather

The Middle East and Africa (MEA) leather goods market is experiencing significant growth driven by the rising demand for synthetic or vegan leather. This trend stems from increased environmental awareness, animal welfare concerns, and consumer preference for sustainable alternatives to traditional leather. Synthetic leather, including polyurethane (PU), bio-based, and plant-derived materials, offers reduced environmental impact compared to conventional leather production methods. Technological advancements have improved synthetic leather's quality, making it comparable to genuine leather in appearance, texture, and durability. This material serves in various applications across the fashion, footwear, and other industries. The region's ongoing urbanization and expanding middle-class population have increased the demand for affordable and durable goods, positioning synthetic leather as a practical choice that meets both economic and ethical considerations.

Technological Advancements in Manufacturing

Manufacturing technology advancements are transforming the Middle East and Africa (MEA) leather goods market across footwear, handbags, luggage, accessories, and clothing segments. The integration of modern technologies, including advanced tanning processes, precision cutting and stitching machinery, digital design tools, and automation, has improved production efficiency, product quality, and customization capabilities. Automated cutting systems and laser engraving technologies allow manufacturers to create intricate patterns and custom designs with minimal waste, meeting the growing demand for unique, high-quality products in the luxury and premium segments. The implementation of sustainable tanning techniques, such as vegetable tanning and water-based treatments, addresses environmental concerns and meets international standards while appealing to environmentally conscious consumers. For instance, in June 2023, Apparel Group's ALDO launched an Eid-Adha Collection featuring footwear styles with ALDO's Pillow Walk and Flex technology. The Pillow Walk technology provides soft, plush insoles for comfort, while Flex technology offers additional support and flexibility.

Fashion Trends and Consumer Preferences

Regional fashion trends reflect a balance between preserving cultural identity and adopting global styles, creating distinct opportunities for leather goods manufacturers. For instance, Nigerian luxury brand Marté Egele has gained international recognition, with its leather bags being carried by celebrities like Beyoncé, demonstrating how regional craftsmanship can achieve global appeal. Middle Eastern consumers show a preference for high-quality fashion that incorporates cultural elements, presenting opportunities for leather goods manufacturers to develop region-specific designs at premium price points. The growing emphasis on cultural authenticity in luxury consumption indicates that manufacturers need to combine global design standards with local cultural elements to gain market share in evolving consumer segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns and pollution | -0.9% | Turkey, Morocco, Egypt | Long term (≥ 4 years) |

| Counterfeit products and brand dilution | -0.6% | Nigeria, Egypt, United Arab Emirates | Medium term (2-4 years) |

| Animal welfare issues | -0.4% | Ethiopia, Kenya, South Africa | Short term (≤ 2 years) |

| Supply chain disruptions | -0.7% | Turkey, Egypt, Nigeria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Pollution

Environmental regulations increasingly restrict traditional leather production methods, requiring manufacturers to adopt cleaner technologies or risk losing market access. The Chouara tannery industry in Morocco exemplifies the challenge of balancing traditional methods with regulatory compliance. Water scarcity in the Middle East and North Africa region emphasizes the need for effluent reduction technologies, as conventional tanning processes require substantial water resources and generate ecosystem-impacting pollutants. The European Union's Ecodesign Regulation (ESPR), Regulation 2024/1781, imposes additional compliance requirements on manufacturers from the Middle East and African countries exporting to European markets, potentially constraining growth for companies that do not implement sustainable production practices. While these environmental requirements stimulate innovation in synthetic leather alternatives and cleaner production methods, they also increase operational costs, affecting price competitiveness in cost-sensitive market segments.

Counterfeit Products and Brand Dilution

Counterfeit leather goods undermine legitimate market growth by eroding consumer trust and reducing revenue for authentic manufacturers. The United Arab Emirates' (UAE) implementation of Federal Decree-Law No. 14 of 2023 on Electronic Transactions and enhanced intellectual property protection measures through customs engagement demonstrates the government's commitment to combat counterfeiting, though enforcement challenges persist across the region. Brand dilution from counterfeit products particularly affects premium leather goods manufacturers that depend on exclusivity and craftsmanship reputation to maintain premium pricing. The relationship between counterfeiting rates and factors like consumer behavior and perceived corruption indicates that market education and enforcement coordination are essential for protecting legitimate manufacturers' market share and profitability. Dubai Customs conducted 285 intellectual property enforcement operations in 2024, resulting in seizures valued at AED 92.695 million. The confiscated counterfeit merchandise encompassed watches, eyewear, electronics, apparel, textiles, handbags, and footwear. The organization processed registrations for 439 trademarks, 205 commercial agencies, and 6 intellectual property assets during this period [2]Source: Government of Dubai, “Dubai Customs Celebrates World Intellectual Property Day with Focus on Creativity and Protection”, dubaicustoms.gov.ae . These actions strengthen Dubai's investment environment by helping producers avoid losses from brand counterfeiting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Footwear Dominance Drives Market Foundation

Footwear holds a 33.27% market share in 2025, dominating the leather goods market due to its fundamental role in consumer wardrobes. The segment's strength comes from widespread demand for athletic footwear in mass markets and luxury leather shoes, particularly in Gulf countries where Italian and European premium brands maintain a significant presence. Additionally, accessories are projected to grow at 4.32% CAGR during 2026-2031, making it the fastest-growing segment. This growth reflects consumer preference for versatile luxury items that enhance multiple outfits without substantial wardrobe investments. Handbags contribute significantly to this expansion, notably in Nigeria, where domestic luxury brands gain international recognition through celebrity endorsements and cultural authenticity.

Luggage and clothing segments exhibit distinct growth patterns. The luggage segment benefits from increased business travel and tourism recovery across the region. According to UN Tourism, the Middle East recorded 95 million arrivals, performing 32% above pre-pandemic levels in 2024, with a 1% increase from 2023. Africa received 74 million arrivals, 7% higher than 2019 and 12% more than 2023 . The clothing segment faces competition from fast fashion alternatives that impact traditional leather garment categories.

By End User: Men Lead While Women Accelerate

Men account for 55.08% of the luxury leather goods market in 2025, primarily due to their established purchasing patterns in business and formal wear categories. This market share reflects the cultural emphasis on men's fashion and accessories across Middle Eastern and African markets. The women's segment is projected to grow at a 4.44% CAGR during 2026-2031, outpacing the men's category as female workforce participation and disposable income levels increase across the region.

The growth in women's consumption stems from fundamental socioeconomic changes, including higher education levels, career advancement, and evolving social norms. The United Arab Emirates (UAE) has implemented legal reforms permitting 100% foreign ownership in retail, enabling luxury brands to establish direct market operations and develop women-focused collections independently. This regulatory framework supports increased investment in female-oriented retail experiences and product development. The distinct growth rates between gender segments present opportunities for manufacturers to adjust their product portfolios while maintaining their existing customer base across both demographics.

By Category: Mass Market Foundation Supports Premium Growth

Mass category leather goods maintain a 62.11% market share in 2025, serving as the market foundation across diverse consumer income levels and usage requirements. This dominance reflects the region's economic composition, where middle-income consumers represent the largest purchasing demographic for leather goods across footwear, handbags, and accessories. The mass segment's stability provides manufacturers with volume-based revenue that supports operational scale and investment in premium product development.

The premium segment's growth rate of 4.66% CAGR correlates with regional wealth expansion, particularly in Gulf countries, where government diversification programs generate high-income employment positions. This trend is exemplified by Italian luxury leather goods manufacturer Valextra's strategic expansion in November 2024, with the opening of its flagship store in Dubai Mall's Fashion Avenue. This expansion represents a calculated response to the increasing demand for premium leather goods in the region, characterized by superior craftsmanship and exclusive designs. The market structure necessitates manufacturers to implement dual-focused strategies: maintaining competitiveness in mass markets while developing premium capabilities to capitalize on higher-margin opportunities within affluent consumer segments.

By Distribution Channel: Digital Transformation Reshapes Retail

The leather goods market in the Middle East and Africa (MEA) is experiencing significant changes in consumer purchasing patterns. In 2025, offline retail stores hold a dominant 71.12% market share, reflecting the region's preference for in-person shopping experiences. This preference stems from cultural practices where consumers prioritize physical examination of product quality, craftsmanship, and fit. Traditional retail outlets, including high-end boutiques and local artisan shops, remain successful by offering personalized service and building customer relationships essential to luxury purchases.

The market is transforming with increasing digital adoption. Online retail stores are expected to grow at a 4.88% CAGR from 2026 to 2031, indicating evolving consumer preferences. This expansion is driven by wider e-commerce adoption, better digital payment systems, and enhanced online product visualization. Younger, tech-savvy consumers particularly value the convenience of online shopping. E-commerce platforms are implementing augmented reality (AR) and artificial intelligence (AI) technologies to create interactive shopping experiences, enabling virtual product trials and customized recommendations.

Geography Analysis

Turkey holds a 28.41% market share in 2025, establishing itself as a manufacturing and export hub serving European and regional markets. The country's collaboration with Egypt to serve United States brands showcases how regional partnerships enhance competitiveness in global supply chains, particularly as companies diversify sourcing away from Asian markets. Turkey's focus on sustainable manufacturing practices and eco-friendly technologies aligns with increasing market demands for environmental compliance. Its established textile and leather expertise, combined with proximity to European markets, enables quick responses to fashion trends and seasonal demand fluctuations.

South Africa shows the highest growth potential with a projected 5.38% CAGR during 2026-2031. This growth stems from luxury brand expansion into secondary cities and a growing high-net-worth individual population. International brands such as Ferragamo, Louis Vuitton, Dior, and Gucci have established retail presence in the past decade, expanding into second and third-tier cities. The country's participation in the African Growth and Opportunity Act (AGOA) provides duty-free access to United States markets, benefiting local manufacturers who meet quality standards.

The United Arab Emirates and Saudi Arabia represent significant markets driven by luxury consumption patterns and supported by government policies that encourage foreign investment and retail expansion. Nigeria gains market recognition through local luxury brands achieving international visibility, as shown by Marté Egele's celebrity endorsements. Egypt attracts manufacturing investment from international brands seeking cost-effective production with European market access. Morocco's traditional tannery industry in Chouara, while facing modernization challenges, maintains cultural significance and export potential. Smaller regional markets benefit from tourism growth and economic diversification initiatives that expand their consumer base for leather goods.

Competitive Landscape

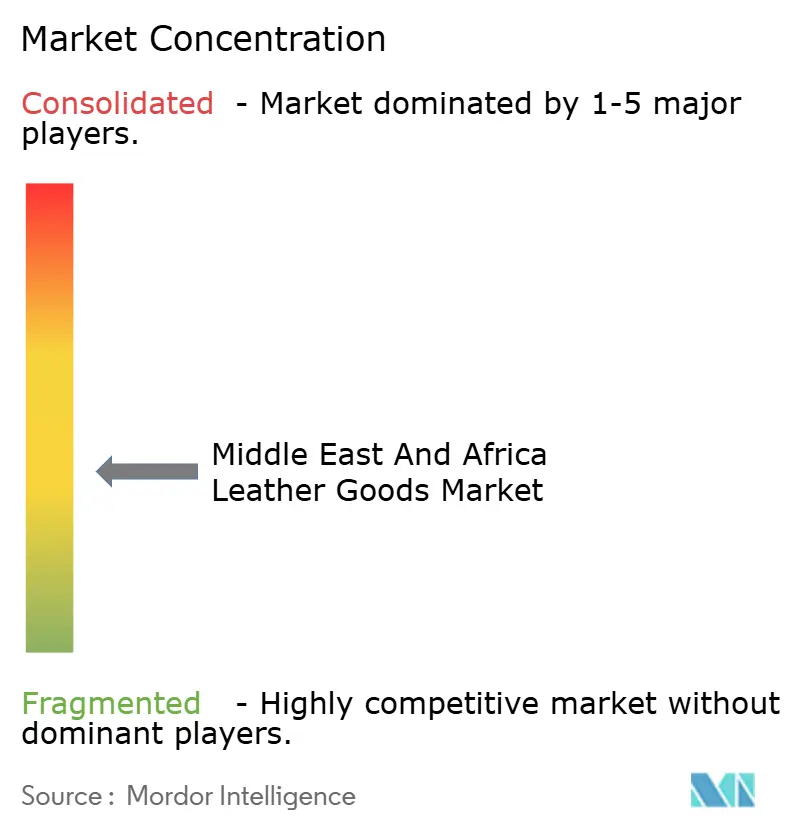

The Middle East and Africa leather goods market demonstrates moderate fragmentation among market participants. This fragmented competitive landscape enables both established luxury companies and regional players to gain market share through distinct approaches. Major companies like LVMH Moët Hennessy Louis Vuitton SE, Kering SA, and Hermès International S.A. pursue geographic expansion and premium positioning. Athletic brands such as Nike, Adidas, and Puma strengthen their footwear and accessories presence through manufacturing efficiencies and regional partnerships. The market structure allows smaller regional brands to compete effectively in niche segments by leveraging cultural authenticity and local craftsmanship.

Companies increasingly focus on vertical integration and supply chain control to gain competitive advantages. Technology adoption creates opportunities for differentiation, as demonstrated by Bentley's implementation of AI-powered hide inspection systems that enhance material quality and reduce waste while allowing artisans to concentrate on finishing work. The market presents opportunities in sustainable leather alternatives and digital commerce platforms. Companies that combine environmental responsibility with traditional craftsmanship can attract consumers who value both quality and sustainability in their purchases.

Moreover, luxury leather goods retail operations in the Middle East and Africa maintain significant dependence on physical stores, specifically high-end boutiques and flagship locations in commercial centers like Dubai and Johannesburg. These retail establishments deliver customized customer service and premium in-store experiences. Regional growth in internet accessibility and consumer adoption of e-commerce transactions has increased digital sales channels. Premium brands are developing their digital infrastructure through proprietary websites and strategic partnerships with established luxury e-commerce platforms, facilitating market penetration among younger demographics and expansion beyond traditional retail locations.

Middle East And Africa Leather Goods Industry Leaders

-

Nike Inc.

-

Puma SE

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

Hermès International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Loro Piana expanded its Middle East presence by establishing its first boutique in Riyadh, Saudi Arabia. The single-floor retail space incorporated an accessories section with leather goods at the entrance, followed by designated areas for footwear and men's and women's ready-to-wear collections.

- August 2024: Prada expanded its retail presence by establishing a boutique in Riyadh's Kingdom Centre, which occupied 420 square meters. The location offered women's ready-to-wear collections, leather goods, footwear, and accessories.

- June 2024: Minimalist, a Dubai-based luxury accessories company offering watches, jewelry, sunglasses, leather goods, and perfumes, established a new retail location at Yas Mall, Abu Dhabi. The store incorporated a VIP room for private shopping sessions and a traditional gahwa service area that implemented regional hospitality customs.

- February 2024: Saint Laurent released a collection of luxury handbags through an exclusive pre-release in select Middle Eastern markets. The collection comprised handcrafted leather designs.

Middle East And Africa Leather Goods Market Report Scope

Middle East leather goods market has been segmented by type, distribution channel, and geography. By type, the market can be segmented into footwear, luggage, and accessories, and by distribution channel, the market can be segmented into offline and online retail stores.

By Product Type

| Footwear |

| Handbags |

| Luggage |

| Accessories |

| Clothing |

| Other Product Types |

By End User

| Men |

| Women |

By Category

| Mass |

| Premium |

By Distribution Channel

| Offline Stores |

| Online Stores |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Footwear |

| Handbags | |

| Luggage | |

| Accessories | |

| Clothing | |

| Other Product Types | |

| By End User | Men |

| Women | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Offline Stores |

| Online Stores | |

| By Geography | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the Middle East Africa leather goods market?

The market is valued at USD 39.03 billion in 2026 and is projected to reach USD 47.58 billion by 2031.

Which product type holds the largest share in the region?

Footwear leads with 33.27% of the Middle East and Africa leather goods market share in 2025, driven by sustained demand across casual, athletic, and formal categories.

How important is online retail for future sales?

Online stores are expected to achieve a 4.88% CAGR, the fastest among distribution channels, owing to improved logistics and digital payment adoption.

Which country will be the fastest-growing market in the region?

South Africa is forecast to grow at 5.38% CAGR from 2026 to 2031, propelled by tourism recovery and export expansion under AGOA.

Page last updated on: