Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

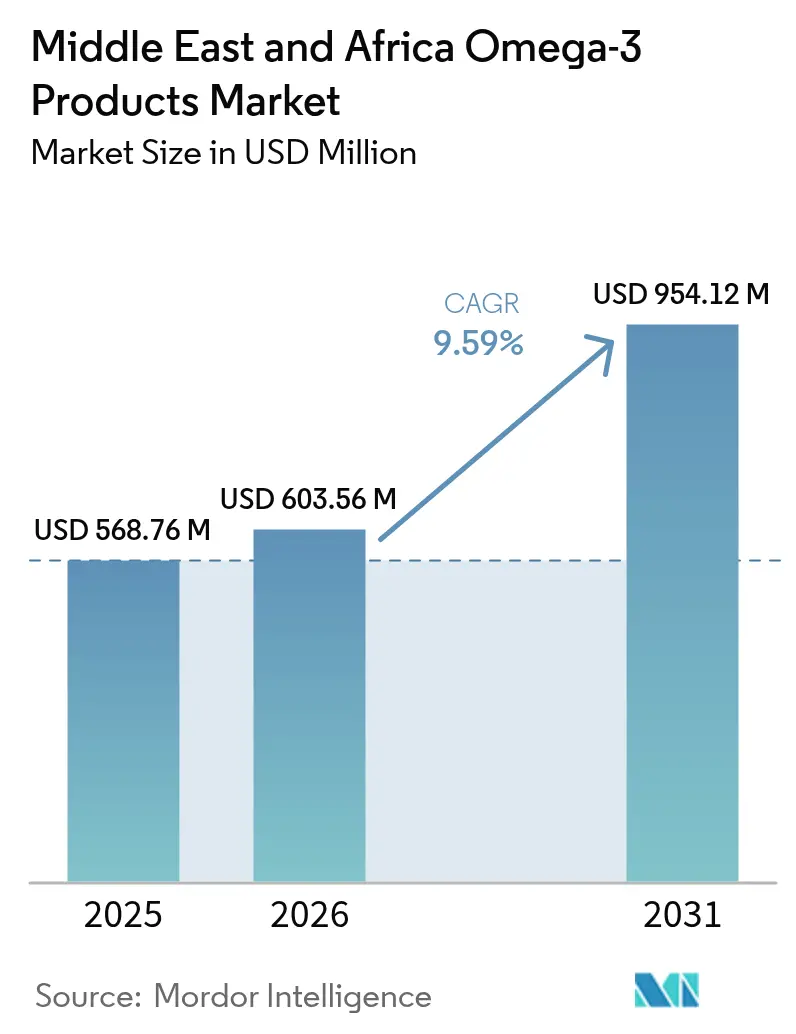

| Base Year Market Size (2025) | USD 568.76 Million |

| Market Size (2026) | USD 603.56 Million |

| Market Size (2031) | USD 954.12 Million |

| Growth Rate (2026 - 2031) | 9.59% CAGR |

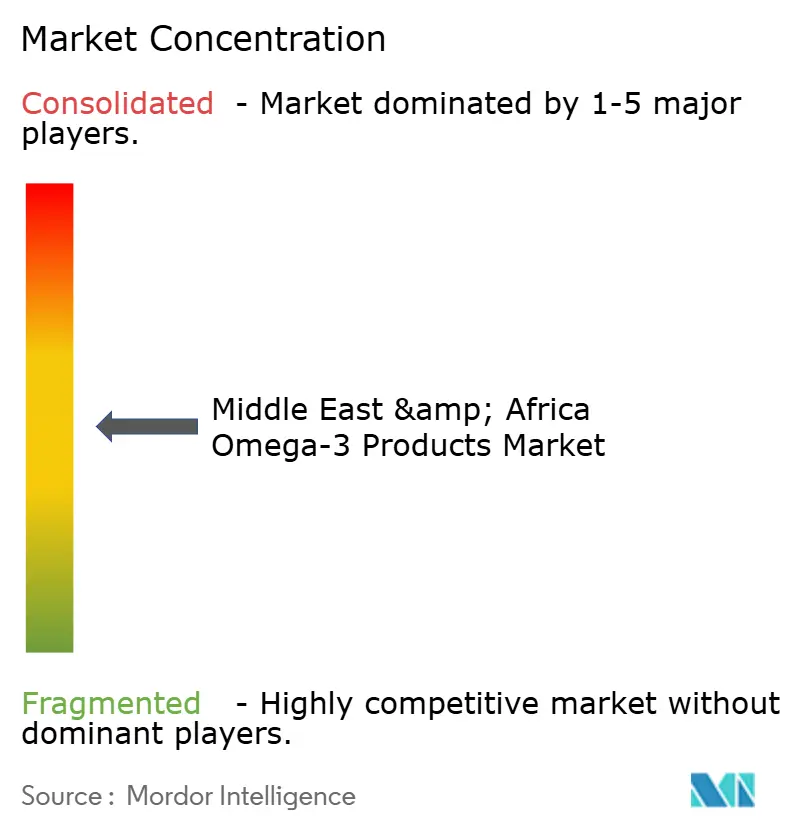

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Omega-3 Products Market Analysis by Mordor Intelligence

The Middle East and Africa Omega-3 products market size was valued at USD 568.76 million in 2025 and is estimated to grow from USD 603.56 million in 2026 to reach USD 954.12 million by 2031, registering a compound annual growth rate (CAGR) of 9.59% during 2026-2031. The Middle East and Africa omega-3 products market is driven by increasing awareness of preventive healthcare and the recognized benefits of fatty acids for heart, brain, and eye health. This has led to a shift toward regular supplement consumption instead of occasional use. The growing prevalence of lifestyle-related conditions, including cardiovascular diseases and metabolic disorders, has prompted healthcare professionals to recommend omega-3 capsules as part of daily nutritional support. According to data published by the United Nations Development Programme in February 2023, cardiovascular diseases account for 34% of all deaths in the United Arab Emirates[1]Source: United Nations Development Programme, “THE CASE FOR INVESTMENT IN PREVENTION AND CONTROL OF NON-COMMUNICABLE DISEASES IN THE UNITED ARAB EMIRATES ,” undp.org.

Key Report Takeaways

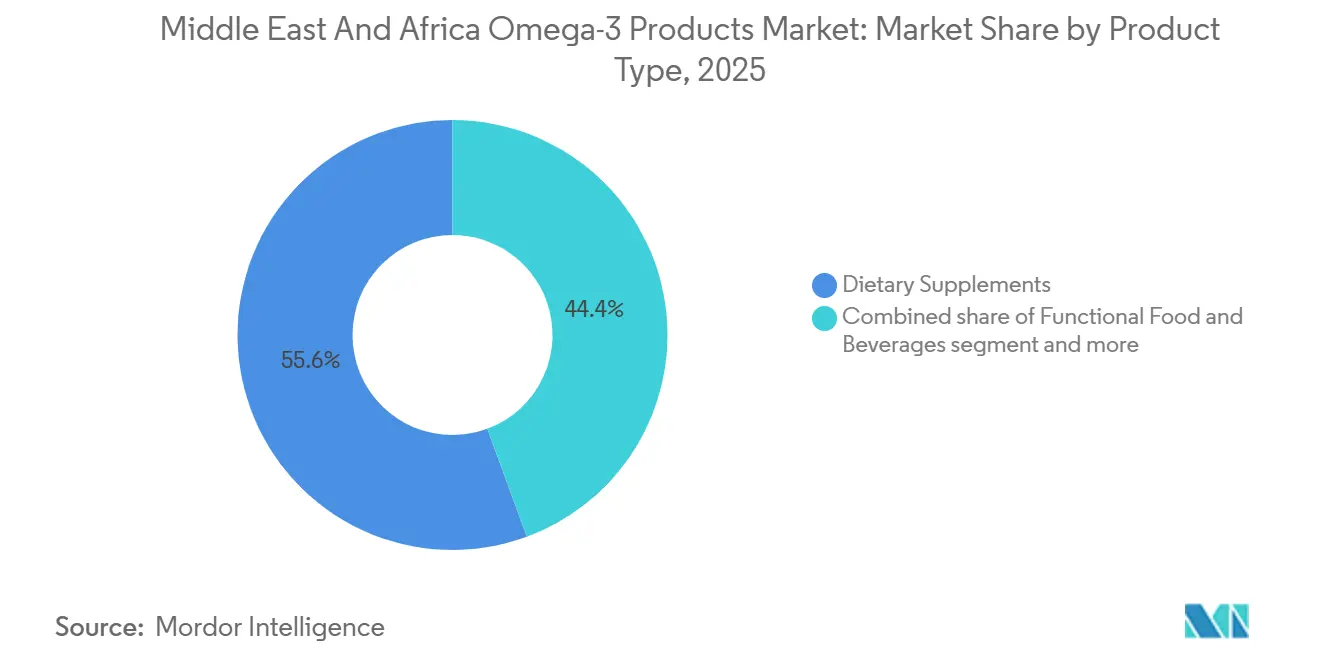

- By product type, dietary supplements led with 55.63% of the Middle East and Africa Omega-3 Products market share in 2025, while functional food and beverages are advancing at an 11.77% CAGR through 2031.

- By source, marine-based ingredients accounted for 88.12% of the Middle East and Africa Omega-3 Products market size in 2025, yet plant-based alternatives deliver the fastest growth at an 11.54% CAGR for 2026-2031.

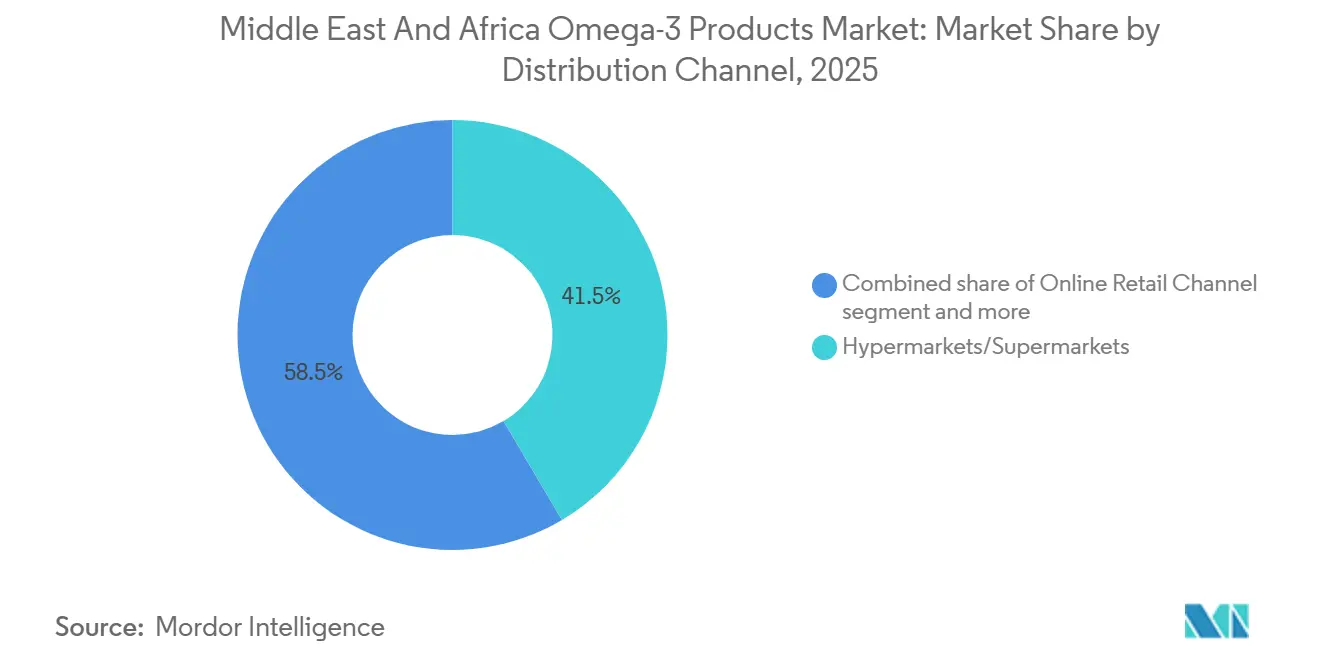

- By distribution channel, hypermarkets/supermarkets captured 41.49% of 2025 revenue; however, online retail is on track for a 12.21% CAGR through 2031.

- By geography, Saudi Arabia held 22.15% of 2025 revenue, whereas the United Arab Emirates posts the highest forecast growth at an 11.63% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Omega-3 Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in fortified food and beverage launches by global brands | +1.8% | Saudi Arabia, United Arab Emirates, Egypt (GCC core with spillover to North Africa) | Medium term (2-4 years) |

| Government-supported DHA fortification in prenatal and infant nutrition | +1.5% | Saudi Arabia, United Arab Emirates, Egypt, Morocco | Long term (≥ 4 years) |

| Expansion of algae-based fermentation for vegan omega-3 supply | +1.2% | Global, with early adoption in United Arab Emirates and Saudi Arabia | Medium term (2-4 years) |

| Growing incidence of cardiovascular and lipid disorders | +1.4% | Middle East and North Africa (region-wide) | Long term (≥ 4 years) |

| Premium supplement offerings using high-strength fish oils | +0.9% | GCC countries (Saudi Arabia, United Arab Emirates, Qatar) | Short term (≤ 2 years) |

| Aging population driving higher demand for omega-3 supplements | +1.0% | GCC countries, Turkey | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of algae-based fermentation for vegan omega-3 supply

The expansion of algae-based fermentation for vegan omega-3 production is becoming a significant driver in the Middle East and Africa omega-3 products market. This method offers a stable, non-marine source of DHA and EPA, aligning with regional dietary preferences and sustainability objectives. Cultivating microalgae in controlled fermentation tanks eliminates issues associated with fish-derived sources, such as odors, heavy-metal contamination, and dependence on marine resources. This makes algal-based omega-3 suitable for halal, vegetarian, and clean-label formulations, which are in high demand in Gulf countries and urban African markets. Local nutraceutical companies and contract manufacturers are increasingly utilizing algal oil to produce plant-based capsules, gummies, and fortified foods. Additionally, international suppliers are collaborating with regional distributors to reduce reliance on imported fish oil. The technology enables year-round production in arid climates, where aquaculture supply chains are limited, thereby improving product availability. This has encouraged brands to introduce vegan prenatal, pediatric, and lifestyle supplements, expanding the consumer base for omega-3 products in the region.

Growing incidence of cardiovascular and lipid disorders

The rising prevalence of cardiovascular and lipid disorders is a key driver of the Middle East and Africa omega-3 products market. Healthcare professionals are increasingly recommending EPA and DHA intake to aid in triglyceride management and support overall heart health. High incidences of hypertension, obesity, and dyslipidemia in Gulf countries and urban African populations have prompted physicians, cardiology clinics, and pharmacies to promote omega-3 capsules as part of long-term wellness strategies rather than short-term supplementation. Consequently, consumers are incorporating daily fish oil or algal oil products into preventive care routines, alongside dietary modifications and medical treatments. This medical endorsement has enhanced trust in the efficacy of omega-3 products, driving demand for both prescription-adjacent nutraceuticals and over-the-counter heart-health supplements across the region. According to the 2024 Health Determinants Statistics Publication by The General Authority for Statistics (GASTAT) for Saudi Arabia, the obesity rate among individuals aged 15 and above is 23.1%, while 45.1% of this age group are classified as overweight. Furthermore, the prevalence of obesity among children aged 2 to 14 years is 14.6%, with 33.3% of children in this age group being overweight[2]Source: General Authority for Statistics, “GASTAT publishes the results of Health Determinants Statistics Publication in Saudi Arabia 2024,” stats.gov.sa.

Premium supplement offerings using high-strength fish oils

Premium supplement offerings featuring high-strength fish oils are driving growth in the Middle East and Africa omega-3 products market. Consumers increasingly associate higher EPA and DHA concentrations with improved efficacy and quicker results. Brands are launching concentrated softgels, triglyceride-form oils, and purified formulations designed for specific benefits, such as heart rhythm support, cognitive performance, and joint health. These targeted products enable companies to differentiate themselves from basic nutrition supplements. Pharmacists and nutrition practitioners frequently recommend these high-potency variants to users who prefer fewer daily capsules, reinforcing their premium positioning. Additionally, the availability of internationally sourced, quality-tested products through pharmacies and e-commerce platforms enhances consumer confidence, promoting a shift from low-dose generic fish oil to higher-value, specialized omega-3 supplements in the region.

Aging population driving higher demand for omega-3 supplements

The aging population in the Middle East and Africa is driving increased demand for omega-3 supplements, as older adults seek nutritional support to enhance cognitive function, joint flexibility, and cardiovascular health. Healthcare practitioners frequently recommend EPA and DHA as part of healthy aging practices, prompting seniors to adopt daily supplementation instead of occasional use. This trend aligns with demographic changes; according to the General Authority for Statistics, approximately 3.89 million individuals aged over 50 reside in the region's key Gulf markets, expanding the target audience for preventive nutrition products[3]Source: General Authority for Statistics, “Population by detailed Age,” stats.gov.sa. In response, brands are launching age-specific formulations, such as memory-support and mobility-support omega-3 capsules, to encourage consistent use among middle-aged and elderly consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fish oil prices increasing raw material costs | -0.8% | Global, with acute impact on import-dependent Middle East and Africa markets | Short term (≤ 2 years) |

| Import and labeling inconsistencies across GCC markets | -0.6% | GCC countries (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman) | Medium term (2-4 years) |

| Consumer shift to lower-cost alpha-linolenic acid (ALA) alternatives | -0.5% | Egypt, Morocco, Nigeria (price-sensitive markets) | Medium term (2-4 years) |

| Strict regulations for health claims and approvals | -0.4% | Saudi Arabia, United Arab Emirates, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile fish oil prices increasing raw material costs

Volatile fish oil prices, which increase raw material costs, serve as a restraint on the Middle East and Africa omega-3 products market. This is primarily because most regional manufacturers depend heavily on imported marine oils. Fluctuations in global fish catches, climate conditions, and shipping expenses often drive up input costs, compelling supplement brands to either raise retail prices or accept reduced profit margins. Higher retail prices can deter regular consumption in price-sensitive markets, limiting market penetration beyond urban areas. Additionally, procurement uncertainties complicate long-term contracts for softgel and fortified food producers, delaying product launches and making companies hesitant to expand their omega-3 product portfolios.

Import and labeling inconsistencies across GCC markets

Import and labeling inconsistencies across GCC markets hinder the growth of the Middle East and Africa omega-3 products market. Manufacturers are required to customize packaging, health claims, and documentation for each country, as no unified regional standard exists. Variations in acceptable nutrient claims, Arabic labeling requirements, halal certifications, and registration processes lead to higher compliance costs and delays in product approvals. Consequently, brands often introduce products in one Gulf market at a time rather than launching region-wide, which limits economies of scale and slows product availability. These regulatory disparities particularly challenge smaller exporters and new entrants, reducing product diversity and constraining overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Foods Outpace Supplements

Dietary supplements accounted for 55.63% of the market share in 2025; however, functional foods and beverages are projected to grow at a CAGR of 11.77% through 2031. The demand for omega-3 supplements in the Middle East and Africa is driven by increasing preventive healthcare practices, with consumers regularly using capsules or syrups to support heart, brain, and joint health. Medical professionals, including doctors and pharmacists, often recommend EPA and DHA for managing triglyceride levels and maintaining cognitive function, enhancing product credibility and encouraging repeat purchases. The growth of sports nutrition and the active-aging population further promotes daily consumption for recovery and mobility support. Additionally, halal-certified, odor-controlled, and plant-based algal formulations have broadened the appeal of these products to a more diverse consumer base. Furthermore, the expansion of e-commerce pharmacies and cross-border supplement retail has improved access to international brands, facilitating adoption even in areas beyond major metropolitan centers.

Omega-3 functional foods and beverages are gaining traction in the region as consumers increasingly prefer incorporating nutrition into their daily diets rather than relying on separate supplements. Products such as dairy items, bakery goods, and ready-to-drink beverages enriched with DHA are becoming more popular due to their convenience and suitability for consumption by all age groups, particularly children and pregnant women. Government nutrition guidelines promoting early-life brain development have encouraged the fortification of milk and cereals. Additionally, clean-label trends are driving manufacturers to use algal oil as an alternative to marine-derived ingredients. Supermarkets and modern retail chains are dedicating more shelf space to fortified staples, making omega-3 intake a routine part of daily eating habits rather than a specialized or medicinal purchase.

By Source: Algae Erodes Marine Dominance

Marine-based sources are projected to account for 88.12% of the Middle East and Africa omega-3 products market in 2025, while plant-based alternatives are expected to grow at a CAGR of 11.54% through 2031. The demand for marine-derived omega-3 products in the Middle East and Africa is driven by the established clinical trust in fish-sourced EPA and DHA for heart health and lipid management. Consumers seeking quick and noticeable benefits often opt for concentrated fish oil softgels, which are widely regarded as more effective compared to other sources. The availability of purified, deodorized, and pharmaceutical-grade oils has enhanced consumer acceptance. Furthermore, the growth of pharmacy chains and online supplement platforms has ensured consistent access to imported premium brands. Additionally, sports nutrition users and aging populations increasingly use marine omega-3 products for joint health and recovery, supporting repeat purchases and sustaining market demand.

Plant-based omega-3 functional products are gaining popularity among vegetarian, halal-sensitive, and sustainability-conscious consumers seeking alternatives to fish oil in everyday foods. Algae-derived DHA allows manufacturers to fortify dairy alternatives, beverages, cereals, and children’s nutrition products without introducing marine taste or allergen concerns, making it suitable for family consumption. Preferences for clean-label products and growing environmental awareness are driving brands to emphasize renewable sourcing. Additionally, local food processors are opting for plant-based ingredients due to simpler regulatory approval for fortified foods. Consequently, omega-3 enrichment is increasingly integrated into daily diets rather than being limited to supplements, expanding its appeal among younger and lifestyle-oriented consumer groups.

By Distribution Channel: E-Commerce Disrupts Supermarket Hegemony

Hypermarkets/supermarkets accounted for 41.49% of the market share in 2021, while online retail channels are projected to grow at a CAGR of 12.21% through 2031. In the Middle East and Africa, hypermarkets and supermarkets play a significant role in driving the sales of omega-3 products. Consumers often prefer purchasing health and nutrition items alongside their routine groceries, integrating supplements and fortified foods into their regular shopping habits. Large retail chains enhance this trend by offering prominent shelf placement, in-store promotions, and advisory counters that provide pharmacist-style guidance, fostering trust in product quality, particularly for family health and children’s nutrition.

Omega-3 functional products are experiencing significant growth through online retail channels, driven by digital pharmacies and e-commerce platforms offering a wider range of products, detailed ingredient information, and subscription delivery options tailored to daily supplementation needs. Consumers rely on online reviews and educational content to evaluate EPA/DHA concentrations, plant-based alternatives, and specialized formulations, such as those for prenatal or cognitive support. Online availability enhances access in areas with limited specialty nutrition stores, while promotional pricing and doorstep delivery encourage bulk purchases. This convenience, coupled with increasing digital health awareness, positions online platforms as effective channels for repeat purchases of fortified foods and beverages that align with consumers' ongoing wellness routines.

Geography Analysis

Saudi Arabia held 22.15% market share in Omega-3 products in 2025, driven by strong clinical endorsements within private hospitals and pharmacy chains, where supplements are often incorporated into physician-guided wellness plans rather than being used for self-medication. Prenatal and pediatric nutrition programs emphasize DHA intake, leading to increased usage among mothers and infants. Additionally, gym culture and weight-management programs promote the use of fish oil for recovery and metabolic balance. Consumers in Saudi Arabia generally prefer high-purity imported brands with quality certifications, resulting in higher adoption of premium formulations sold through pharmacies and health stores compared to basic multivitamins.

The United Arab Emirates is projected to grow at a CAGR of 11.63% through 2031. In the United Arab Emirates, omega-3 functional products are experiencing increased demand, driven by the rapid expansion of the premium ready-to-eat and on-the-go meal segment. This growth is attributed to changing consumer preferences for convenient and health-focused food options. Consumers are increasingly opting for fortified juices, yogurt drinks, and snack bars, which provide essential nutrients like omega-3 fatty acids. These products align with workplace wellness initiatives and cater to time-pressed lifestyles, offering multiple health benefits in a single serving.

In Turkey, Egypt, Morocco, Nigeria, and South Africa, omega-3 functional products are gaining traction as local food manufacturers enhance mass staples with nutrient enrichment to stand out in competitive packaged food markets. The growth of urban retail formats, such as neighborhood convenience stores and informal modern trade, supports the demand for shelf-stable fortified foods that can withstand warm climates and extended distribution routes. Furthermore, collaborations between regional processors and international ingredient suppliers facilitate localized product development with familiar flavors, enabling omega-3 enrichment to blend seamlessly into traditional diets rather than being perceived as an unfamiliar health concept.

Competitive Landscape

The Middle East and Africa Omega-3 Products Market is moderately concentrated, with key players such as DSM-Firmenich, BASF, and Cargill holding a significant share due to vertical integration and extensive multi-country distribution networks. These companies leverage their established supply chains, research and development capabilities, and strong brand presence to maintain their market position. However, niche players have opportunities to capitalize on untapped areas, including algae-based infant nutrition, which caters to the growing demand for plant-based alternatives; high-strength EPA formulations, which address specific health concerns such as cardiovascular health; and Halal-certified products, which meet the dietary requirements of the region's population.

The Middle East and Africa omega-3 products market comprises global ingredient specialists, branded nutraceutical companies, and regional distributors. These players primarily compete based on purity perception, certification credibility, and formulation versatility. Large multinational suppliers prioritize providing high-grade concentrates to pharmaceutical and premium supplement brands. Mid-sized companies focus on differentiation through stability enhancements, sensory neutrality, and alternative biological sources tailored to local dietary preferences. Meanwhile, new entrants are disrupting the market by offering innovative plant-derived oils and technologically advanced concentrates, catering to consumers seeking cleaner labels and traceable sourcing.

Competition is influenced by how effectively companies engage with consumers and comply with regulations across various markets. Direct-selling wellness networks establish trust through personal interactions and education-focused marketing, while digital retail channels enable niche brands to target younger audiences without requiring extensive physical distribution networks. As regulatory authorities increase scrutiny on product claims and labeling standards, companies with robust scientific documentation, transparent testing processes, and a strong understanding of local compliance requirements are better equipped to expand internationally.

Middle East And Africa Omega-3 Products Industry Leaders

Windmill Health Products

Amway Corp

Nestlé SA

Unilever PLC

NOW Health Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Seven Seas, a specialist in cod liver oil, launched two new supplements in the United Arab Emirates: Seven Seas JointCare Max and Seven Seas MaxEPA Forte. These products aim to enhance overall wellness and provide joint support. Leveraging its extensive expertise in omega-3 nutrition, Seven Seas has crafted these formulations with premium ingredients, catering to consumers prioritizing daily health maintenance.

- May 2023: Golden Terra Soya Oil introduced a 1-liter Mega-Fill Pack in Nigeria, gaining widespread acceptance among budget-conscious families and foodservice professionals. The tamper-proof refill pouch provides a convenient, affordable option for weekly purchases, meeting consumer preferences for value and health. The oil, fortified with Vitamin A and essential Omega-3 and Omega-6 fatty acids, contains no cholesterol or trans fats and promotes heart health. Its neutral taste profile and low oil retention characteristics make it suitable for multiple cooking methods, including frying, sautéing, and baking, while preserving natural food flavors and ensuring optimal cooking results.

- April 2023: Humanativ partnered with Tanmiah Food Company to introduce the first omega-3 DHA-enriched chicken in Saudi Arabia, under the Tanmiah Life brand. The product is naturally fortified using Humanativ's plant-based OmegaPro, a sustainable omega-3 DHA source in poultry feed. The enriched chicken provides significant health benefits, including enhanced support for heart function, brain development, and eye health, aligning with Tanmiah's commitment to providing high-quality, halal, and nutritious food options. The product is available in various cuts, including whole chickens, breasts, and thighs, through major retailers and Tanmiah's e-commerce platform across Saudi Arabia.

- January 2023: AlgiSys BioSciences announced plans to establish a fermentation-based production facility in Saudi Arabia to produce EPA and DHA Omega-3s and plant proteins. The expansion aims to decrease dependence on traditional fish oil and fishmeal sources while supporting regional food security initiatives, sustainable aquaculture development, and human nutrition requirements. Through its focus on non-GMO, halal-certified omega-3s production methods, AlgiSys is strengthening its Middle East presence and advancing its position in sustainable nutrition and biotechnology. The facility will implement advanced fermentation technologies to ensure efficient and environmentally responsible production processes.

Middle East And Africa Omega-3 Products Market Report Scope

The Middle-East and Africa omega-3 products market is segmented by product type into functional food, dietary supplements, and infant nutrition. By distribution channel, the market is segmented into grocery retailers, pharmacies and drug stores, internet retailing, and other distribution channels. By geography, the market is segmented into South Africa, the United Arab Emirates, and the rest of Middle-East and Africa.

By Product Type

| Dietary Supplements |

| Functional Food and Beverages |

| Infant Nutrition |

| Pharmaceuticals |

| Others |

By Source

| Marine-Based | Fish |

| Krill | |

| Others | |

| Plant-Based | |

| Algae-Based |

By Distribution Channel

| Hypermarkets/Supermarkets |

| Health Stores |

| Online Retail Channel |

| Other Distribution Channels |

Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Dietary Supplements | |

| Functional Food and Beverages | ||

| Infant Nutrition | ||

| Pharmaceuticals | ||

| Others | ||

| By Source | Marine-Based | Fish |

| Krill | ||

| Others | ||

| Plant-Based | ||

| Algae-Based | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Health Stores | ||

| Online Retail Channel | ||

| Other Distribution Channels | ||

| Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa omega-3 products market in 2026?

The Middle East and Africa omega-3 products market size is expected to reach USD 603.56 million in 2026 with a 9.59% CAGR outlook to 2031.

Which product type segment grows the fastest to 2031?

Functional food and beverages record a 11.77% CAGR, outpacing supplements, infant nutrition, and pharmaceuticals.

How is e-commerce changing omega-3 distribution?

Online retail is expected to grow at a 12.21% CAGR, led by platforms such as Noon and Amazon that provide same-day delivery and subscription models in the GCC.

Which country leads regional growth?

The United Arab Emirates posts the fastest CAGR at 11.63%, benefiting from streamlined supplement registration and affluent consumer demographics.

Page last updated on: