Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

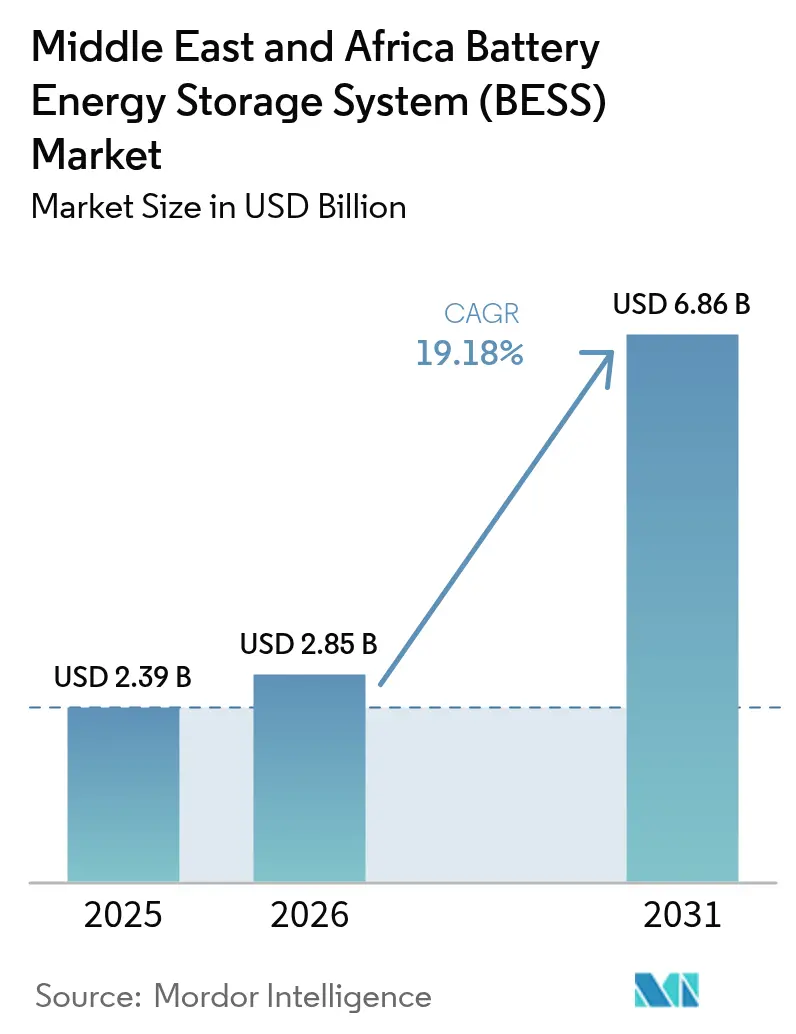

| Base Year Market Size (2025) | USD 2.39 Billion |

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 6.86 Billion |

| Growth Rate (2026 - 2031) | 19.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Battery Energy Storage System (BESS) Market Analysis by Mordor Intelligence

The Middle East And Africa Battery Energy Storage System Market size in 2026 is estimated at USD 2.85 billion, growing from 2025 value of USD 2.39 billion with 2031 projections showing USD 6.86 billion, growing at 19.18% CAGR over 2026-2031.

Accelerated sovereign-fund spending, mandatory storage, and renewables co-tenders, as well as sub-Saharan mining hybrids, are reshaping capacity additions. Lithium-ion price falls below USD 100/kWh have removed subsidy dependence, while flow-battery pilots demonstrate superior long-duration economics. Multi-year framework agreements, such as Saudi Electricity Company’s 2.5 GW deal, are lowering financing spreads, enabling developers to capture the upside of ancillary services. Heightened competition between Chinese cell suppliers and European integrators compresses hardware margins, redirecting value toward software, services, and local assembly.

Key Report Takeaways

- By battery type, lithium-ion chemistries held 79.82% of the Middle East and Africa battery energy storage system market share in 2025, while flow batteries are expected to expand at a 28.25% CAGR through 2031.

- By connection type, on-grid systems led with 73.65% revenue share in 2025; off-grid deployments are advancing at a 26.1% CAGR to 2031.

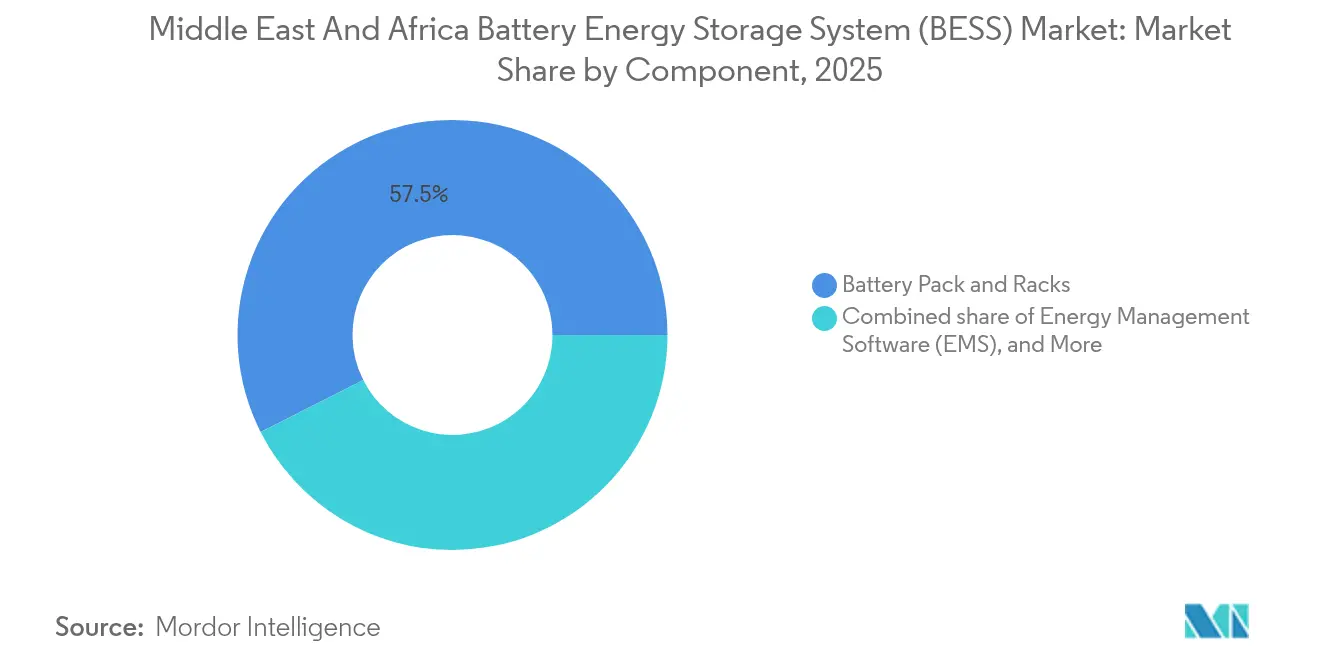

- By component, battery packs and racks captured a 57.45% share of the Middle East and Africa battery energy storage system market size in 2025; energy-management software is projected to rise at a 26.8% CAGR through 2031.

- By energy capacity range, the 10-100 MWh band accounted for 33.12% of the Middle East and Africa battery energy storage system market size in 2025, while the 100-500 MWh segment recorded the fastest growth at a 29.1% CAGR.

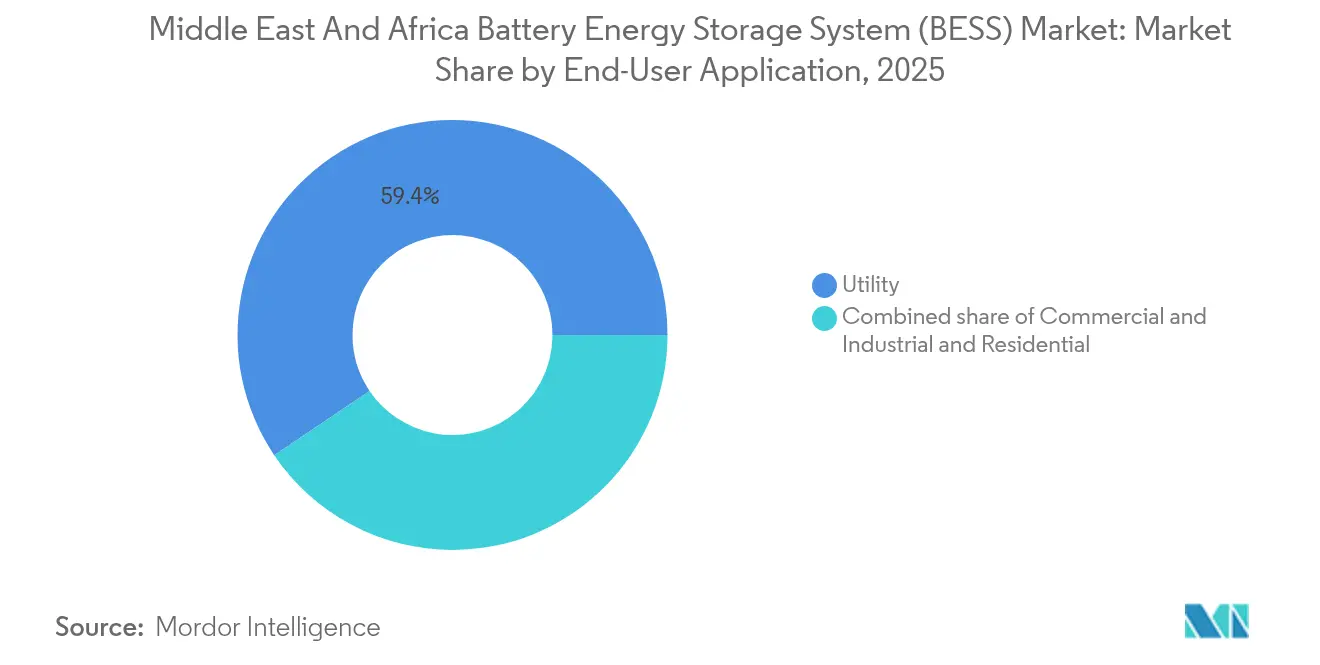

- By end-user, utility applications held a 59.44% share in 2025 and are projected to progress at a 21.9% CAGR to 2031.

- By geography, Saudi Arabia commanded a 23.08% share in 2025 and is forecast to grow at a 22.95% CAGR through 2031.

- The five largest suppliers collectively held roughly 55% of contracted capacity in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Battery Energy Storage System (BESS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid utility-scale solar and wind build-outs | 4.20% | Saudi Arabia, UAE, Egypt, South Africa | Medium term (2-4 years) |

| National grid-stability mandates | 3.80% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Falling LFP battery prices below USD 100/kWh | 3.50% | GCC and South Africa | Short term (≤ 2 years) |

| Oil-exporting nations’ decarbonization funds | 2.90% | Saudi Arabia, UAE, Qatar, Kuwait | Long term (≥ 4 years) |

| Mining-site hybrid-power economics | 2.40% | South Africa, DRC, Zambia, Namibia | Medium term (2-4 years) |

| Data-center power-quality requirements | 1.70% | UAE, Saudi Arabia, South Africa, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Utility-Scale Solar and Wind Build-Outs

Saudi Arabia, the United Arab Emirates, Egypt, and South Africa are embedding four-hour storage into every new solar tender and two-hour storage into all wind solicitations, making batteries a mandatory cost of entry.[1]PV Magazine, “Saudi Tenders Demand Four-Hour Storage,” pv-magazine.com Developers such as ACWA Power and Masdar have pre-ordered more than 12 GWh of lithium-iron-phosphate cells for projects scheduled before 2027. Egypt’s 1 GW solar pipeline pairs 200 MWh of storage to avoid curtailment in the Suez Canal Economic Zone. South Africa’s latest IPP round allocated 1.2 GW of battery capacity at tariffs that undercut Eskom’s coal fleet, demonstrating competitive parity. Because grid studies now evaluate generation and storage together, average project lead times have fallen by nearly two years, accelerating revenue realization.

National Grid-Stability Mandates

Regulators in Saudi Arabia and the UAE now treat storage as essential infrastructure, issuing directives that require the grid operator to procure fixed volumes or face financial penalties.[2]Energy Storage News, “ACWA Power Integrates 12 GWh of LFP,” energystoragenews.com Saudi Arabia mandated 26 GWh by 2027, while the UAE agreed to a 19 GWh framework that earns capacity payments independent of energy dispatch. Multi-year contracts reduce transaction costs and provide lenders with predictable cash flows, resulting in spreads of 200-250 basis points over the SOFR rate. Qatar has launched the Gulf’s first standalone 400 MWh tender, signaling a shift toward merchant storage models that monetize ancillary services. Strict IEC 62933 compliance rules filter out smaller suppliers that lack certified hardware, raising entry barriers and consolidating market share among tier-one integrators.

Falling LFP Battery Prices Below USD 100/kWh

Lithium-iron-phosphate cell prices dropped to USD 89/kWh in early 2025 as Chinese manufacturers reduced their margins to maintain plant operations at 60% utilization. Saudi Arabia secured an eight-year supply at USD 85/kWh, allowing for levelized storage costs of under USD 0.05/kWh, even without subsidies. South Africa’s Industrial Development Corporation has funded three local assembly lines that aim to achieve 40% local content by 2027, thereby reducing import duties and shipping costs. As LFP replaces nickel-rich chemistries, fire risk falls and cycle life exceeds 6,000 cycles, making daily arbitrage viable for more utilities. The price plunge is unlocking smaller commercial and industrial projects that previously failed to meet hurdle rates, broadening the addressable market.

Oil-Exporting Nations’ Decarbonization Funds

Sovereign wealth vehicles in Saudi Arabia, the UAE, and Qatar have earmarked USD 180 billion for renewables and storage through 2030, dwarfing private capital pools elsewhere in the region. The Public Investment Fund alone set aside USD 50 billion for 30 GWh of domestic storage and 20 GWh abroad, compressing the cost of capital to 4-6%. Masdar committed USD 30 billion across Egypt, Morocco, and Kenya, structuring 25-year PPAs that de-risk revenue for lenders. Qatar Investment Authority partnered with TotalEnergies on a 5 GWh project aimed at mining and telecom clients with diesel displacement goals. Ready access to equity shortens development cycles and enables lower tariff bids that still meet return thresholds, crowding in additional private financiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lagging distribution-network digitalization | -2.80% | Nigeria, Kenya, Tanzania | Long term (≥ 4 years) |

| Policy uncertainty in several African states | -2.30% | Nigeria, Kenya, Egypt, Zimbabwe | Medium term (2-4 years) |

| High sovereign-risk financing costs | -1.90% | Nigeria, Kenya, Egypt, Zambia | Medium term (2-4 years) |

| Limited local battery-grade raw-material refining | -1.60% | Region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lagging Distribution-Network Digitalization

Only 38% of Nigeria’s distribution feeders and 12% of Tanzanian substations have supervisory control and data acquisition links, preventing batteries from delivering frequency and voltage services. Kenya Power relies on manual dispatch instructions, creating latency that forces storage operators to oversize systems by up to 30% to capture revenue. Eskom initiated a USD 1.2 billion grid modernization project in 2024, but legal disputes have slowed the rollout of four million smart meters. Without real-time data, utilities cannot fully value fast-ramping capacity, resulting in shallow ancillary-service markets. The digital gap deters investors who discount projected cash flows when dispatch certainty is low.

Policy Uncertainty in Several African States

Nigeria’s suspension of feed-in tariffs in 2024 froze 2.5 GW of solar-plus-storage projects, triggering USD 800 million in arbitration claims.[3]Reuters, “Nigerian Feed-In Tariff Suspension Puts 2.5 GW in Limbo,” reuters.com Kenya’s regulator revised PPA templates three times in one year, stretching approval cycles from six to 18 months and inflating holding costs. Egypt delayed a 1.5 GWh tender as budget talks stalled, prompting developers to redeploy capital to the Gulf, where frameworks are predictable. Zimbabwe’s foreign-exchange restrictions prevent dividend repatriation, deterring international sponsors. Each reversal raises perceived risk and widens the spread investors demand over risk-free rates, slowing deployment relative to announced targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Flow Batteries Challenge Lithium Dominance

Lithium-ion chemistries remained dominant with an 79.82% share of the Middle East and Africa battery energy storage system market in 2025, thanks to rapid cost decline and mature supply chains. Flow batteries, however, are racing ahead at 28.25% CAGR through 2031 as utilities seek 8- to 12-hour discharge durations for daily arbitrage and seasonal shifting. Eskom’s 200 MWh vanadium redox contract highlights the appeal of 20,000-cycle lifetimes, which reduce levelized storage costs.

Cost spreads are narrowing: Saudi tenders priced LFP at USD 89/kWh, only 30% below flow bids, prompting developers to reconsider chemistry diversification. Lead-acid retains a foothold in telecom backup, while sodium-ion pilots in Morocco and Egypt signal a future low-cost alternative. Thermal-runaway concerns continue to erode nickel-rich chemistries, and hybrid supercapacitors are being trialed for sub-second response in microgrids.

By Connection Type: Off-Grid Gains on Mining Economics

On-grid installations accounted for 73.65% of 2025 deployments, primarily driven by large contracts in Saudi Arabia and the UAE, which supply frequency regulation and capacity firming. Yet, off-grid systems are forecast to expand at a 26.1% CAGR, driven by African mining firms replacing diesel with solar-plus-storage hybrids that achieve a levelized cost of less than USD 0.10/kWh.

Sibanye-Stillwater’s 50 MWh roll-out saves 18 million liters of diesel annually, illustrating the operational upside. Zambia’s Kansanshi copper project will pair 100 MW of solar power with 40 MWh of storage to achieve full energy autonomy by 2026. Rural microgrids in Kenya and hybrid commercial and industrial (C&I) systems in South Africa enhance resilience in areas where grid outages are prevalent.

By Component: Software Captures Value-Chain Margins

Battery packs and racks represented 57.45% of 2025 spending, yet pricing pressure from Chinese suppliers is eroding margins. Energy-management software, advancing at 26.8% CAGR, is where value is migrating: Fluence’s Mosaic raised project IRRs by up to 18% on Saudi fleets through predictive congestion bidding.

Huawei’s AI-enabled FusionSolar cut degradation by 20% by optimizing depth-of-discharge cycles. Regulatory fire-testing, such as UL 9540A compliance in South Africa, strengthens demand for proven thermal management and container designs, protecting incumbents from low-cost competitors. Services contracts worth 8-12% of capex over 10 years further enrich recurring-revenue models.

By Energy Capacity Range: Gigawatt-Hour Projects Reshape Scale

The 100-500 MWh band is the fastest-growing, charting a 29.1% CAGR as utilities choose stand-alone blocks that rival gas peakers on levelized cost. Saudi Arabia’s 1.3 GWh Red Sea project showcases merchant-storage profitability under time-of-use tariffs.

Systems below 10 MWh remain critical for residential, telecom, and small-C&I resilience, but gigawatt-hour ambitions signal consolidation among balance-sheet-strong developers able to manage multi-billion-dollar EPC scopes. African caps at 100 MWh constrain scale-economy gains, maintaining fragmentation in those markets.

By End-User Application: Utility Segment Dominates Growth

Utilities held a 59.44% market share in 2025 and are expected to grow at a 21.9% CAGR as grid stability mandates proliferate. The Saudi Electricity Company alone procured 10 GWh of capacity for black-start and spinning reserve duties.

Commercial and industrial users are adopting behind-the-meter storage for demand-charge management and outage protection, as exemplified by the 200 MWh installed at South African factories during the 2024 rolling blackouts. Data-center backup standards of 15-minute duration are another growth vector across GCC digital campuses. Residential uptake lags until financing models mature.

Geography Analysis

Saudi Arabia’s 23.08% 2025 share of the Middle East and Africa battery energy storage system market leads the region, and a 22.95% CAGR through 2031 is supported by its 48 GWh storage mandate, multi-year framework contracts, and 4-6% cost of capital. The Red Sea standalone facility validated merchant economics under dynamic tariffs.

The United Arab Emirates and Qatar follow, adopting capacity-payment models that uncouple revenue from dispatch. Masdar’s 19 GWh agreement demonstrates national-scale procurement, while Qatar’s standalone 400 MWh tender pioneers merchant storage in the Gulf. Sub-Saharan Africa holds upside: South Africa commissioned 1.2 GWh in 2024 to defer grid upgrades, Kenya’s 120 minigrids illustrate rural viability, and Egypt’s 200 MWh hybrid for Suez industries signals industrial appetite. Yet Nigeria’s tariff reversals and high sovereign spreads stall pipelines, underscoring the Gulf between regulatory certainty in GCC states and policy volatility elsewhere.

Competitive Landscape

The market is moderately concentrated, with the top five vendors controlling approximately 55% of the 2024 contracted volume. Chinese giants CATL and BYD leverage regional hubs and local-currency terms to undercut Western OEMs by 15-20% on a net-present-value basis. Fluence’s 2.5 GW deal with Saudi Electricity Company demonstrates that long-duration framework contracts can reduce transaction costs, a template that Tesla and Sungrow are replicating in the UAE and Egypt.

Technology differentiation shifts from cells to software; Huawei’s FusionSolar and Schneider’s EcoStruxure deliver AI-based bidding that raises asset returns 10-20%. Modular specialists such as AlphaESS exploit C&I niches where speed trumps scale. Patent activity in solid-state and grid-forming inverters, led by Siemens Energy and ABB, foreshadows the next wave of competitiveness.

Expect further consolidation as developers capable of financing projects exceeding 500 MWh crowd out smaller EPCs. Nonetheless, whitespace persists in off-grid mining and telecom microgrids, segments that demand flexible form factors and rapid deployment.

Middle East And Africa Battery Energy Storage System (BESS) Industry Leaders

NGK INSULATORS, LTD.

Tesla Inc

Huawei Digital Power

BYD Co. Ltd.

Fluence Energy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kuwait is moving forward with plans to construct one of the Middle East's largest battery energy storage systems, targeting a discharge capacity of 1.5 GW and a total storage range of 4–6 GWh.

- September 2025: Saudi Electricity Company (SEC), the state-owned utility of Saudi Arabia, has secured contracts for two significant battery energy storage systems (BESS) boasting a total capacity of 4.9 GWh.

- April 2025: Cummins unveiled its next-generation Battery Energy Storage Systems (BESS) at an event in Dubai, UAE.

- June 2025: In the third bid window, Scatec ASA clinched the preferred bidder status for the Haru BESS Battery Energy Storage Project, boasting a capacity of 123 MW/492 MWh.

Middle East And Africa Battery Energy Storage System (BESS) Market Report Scope

Battery energy storage is considered a critical technology in transitioning to a sustainable energy system. Battery energy storage systems store the generated energy and release it as needed by the end-user. They regulate voltage and frequency, reduce peak demand charges, integrate renewable sources, and provide a backup power supply. Batteries are crucial in energy storage systems, accounting for approximately 60% of the system's total cost.

The Middle East and Africa Battery Energy Storage System Market is segmented by battery type, connection type, component, energy capacity, end-user, and geography. By battery type, the market is segmented into lithium-ion, lead-acid, flow battery, sodium-ion, and other technologies. By connection type, the market is segmented into on-grid and off-grid. By component, the market is segmented into battery packs, racks, PCS, EMS, and Balance of Plant. By energy capacity, the market is segmented into below 10 MWh, 10 to 100 MWh, 100 to 500 MWh, and above 500 MWh. By end user, the market is segmented into Utility-scale, commercial and industrial (C&I), and residential. The report also covers the market size and forecasts for the Middle East and Africa Battery Energy Storage System Market across the major countries. The market sizing and forecasts for each segment are based on the revenue (USD Billion).

By Battery Type

| Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO)) |

| Lead-acid |

| Flow Battery (Vanadium Redox, Zinc-Bromine) |

| Sodium-ion |

| Other Battery Technologies (NiCd, Hybrid Super-capacitors) |

By Connection Type

| On-Grid (Utility Interconnected) |

| Off-Grid (Micro-Grid, Hybrid) |

By Component

| Battery Pack and Racks |

| Power Conversion System (PCS) |

| Energy Management Software (EMS) |

| Balance-of-Plant and Services |

By Energy Capacity Range

| Below 10 MWh |

| 10 to 100 MWh |

| 100 to 500 MWh |

| Above 500 MWh |

By End-user Application

| Utility |

| Commercial and Industrial |

| Residential |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| South Africa |

| Egypt |

| Kenya |

| Rest of Middle East and Africa |

| By Battery Type | Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO)) |

| Lead-acid | |

| Flow Battery (Vanadium Redox, Zinc-Bromine) | |

| Sodium-ion | |

| Other Battery Technologies (NiCd, Hybrid Super-capacitors) | |

| By Connection Type | On-Grid (Utility Interconnected) |

| Off-Grid (Micro-Grid, Hybrid) | |

| By Component | Battery Pack and Racks |

| Power Conversion System (PCS) | |

| Energy Management Software (EMS) | |

| Balance-of-Plant and Services | |

| By Energy Capacity Range | Below 10 MWh |

| 10 to 100 MWh | |

| 100 to 500 MWh | |

| Above 500 MWh | |

| By End-user Application | Utility |

| Commercial and Industrial | |

| Residential | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Kenya | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the Middle East and Africa battery energy storage system market?

The market was valued at USD 2.85 billion in 2026.

How fast is the sector expected to grow?

A 19.18% CAGR is projected between 2026 and 2031, lifting revenues to USD 6.86 billion.

Which country is the fastest-growing contributor?

Saudi Arabia is set to expand at a 22.95% CAGR through 2031 on the back of its 48 GWh mandate.

Which battery chemistry is gaining traction for long-duration storage?

Flow batteries are accelerating at a 28.25% CAGR due to superior multi-hour economics.

Why are off-grid systems important in sub-Saharan Africa?

They help mines and rural communities bypass unreliable grids while cutting diesel costs below USD 0.10/kWh.

What drives falling storage costs in the region?

Lithium-iron-phosphate prices dipping under USD 100/kWh and sovereign-fund financed mega-tenders.

Page last updated on: