Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

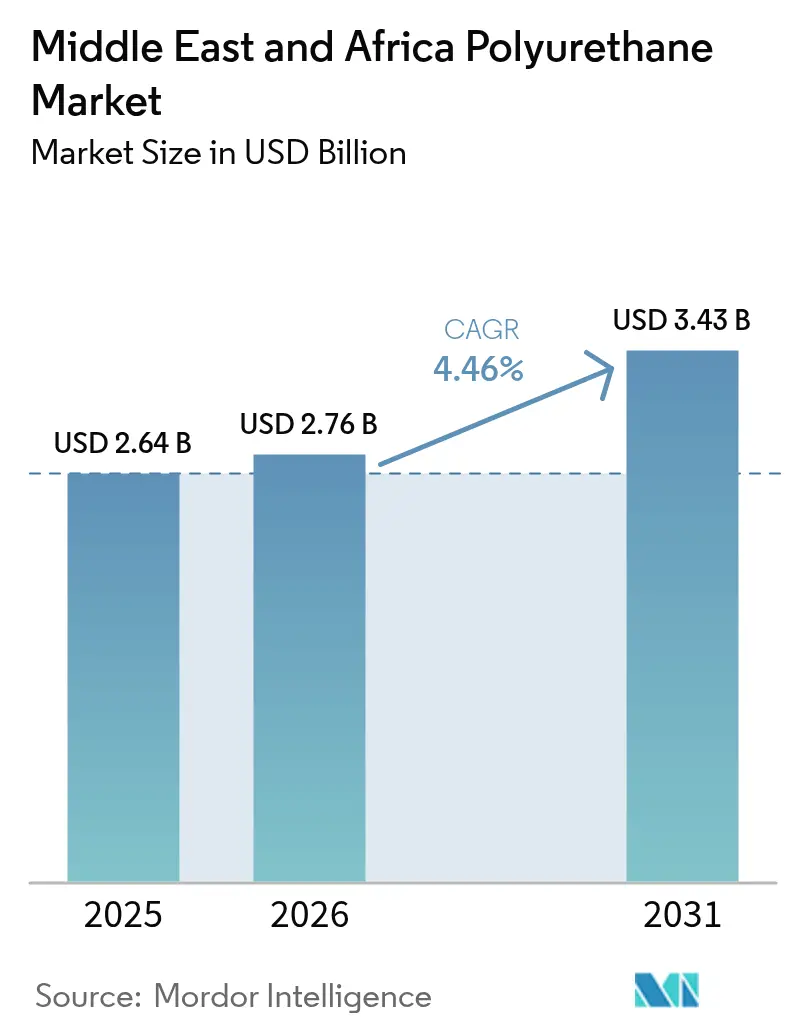

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Polyurethane Market Analysis by Mordor Intelligence

The Middle East And Africa Polyurethane Market size was valued at USD 2.64 billion in 2025 and estimated to grow from USD 2.76 billion in 2026 to reach USD 3.43 billion by 2031, at a CAGR of 4.46% during the forecast period (2026-2031). Rapid infrastructure expansion, sovereign-backed industrial localization, and stricter energy-efficiency norms are intensifying demand for rigid and flexible polyurethane solutions across construction, mobility, and cold-chain applications. The acquisition of Covestro by ADNOC has reinforced regional feedstock security, while synchronized price increases by major suppliers signal tighter supply–demand balances. Bio-based polyols are gaining momentum as regulators tighten carbon-reduction targets and end users pursue circularity strategies. At the same time, volatile isocyanate pricing and tougher worker-safety limits are pressuring margins and accelerating investment in process automation and exposure-control technologies.

Key Report Takeaways

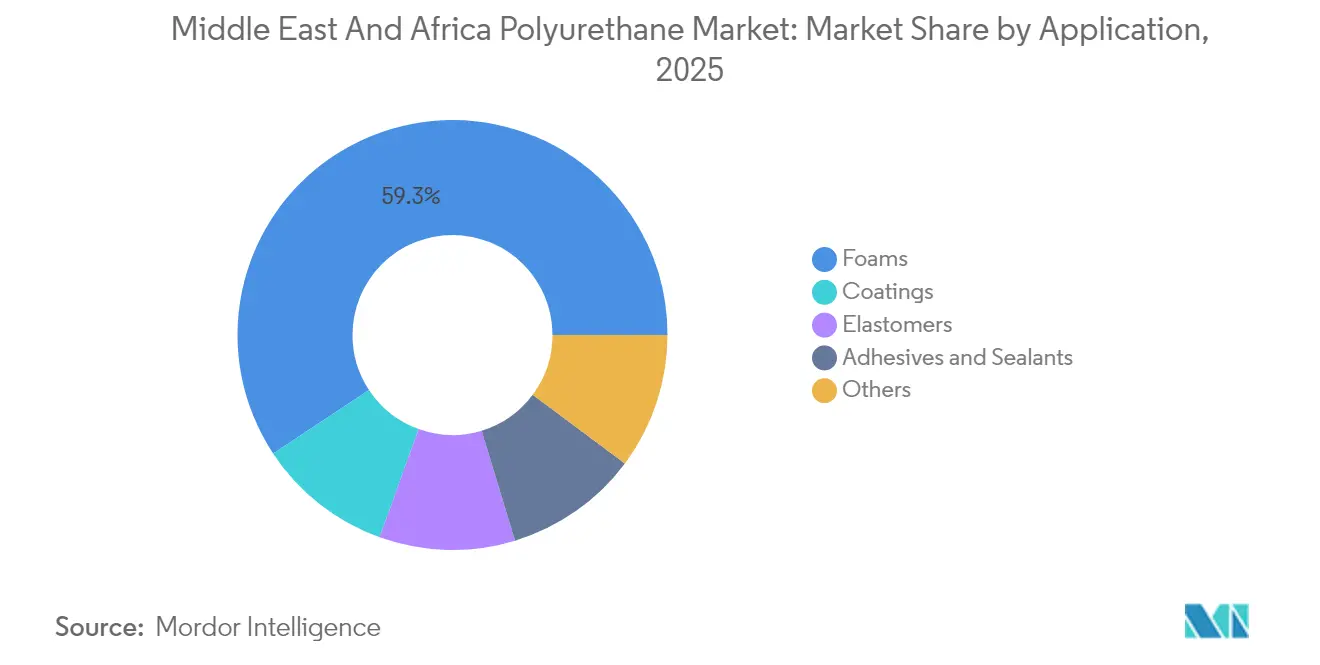

- By application, foams accounted for 59.28% of the Middle East and Africa polyurethane market share in 2025; coatings are projected to expand at a 5.19% CAGR through 2031.

- By end-user industry, the building and construction sector held 38.05% of the Middle East and Africa polyurethane market size in 2025, while the automotive sector is forecast to grow at a 5.38% CAGR between 2026 and 2031.

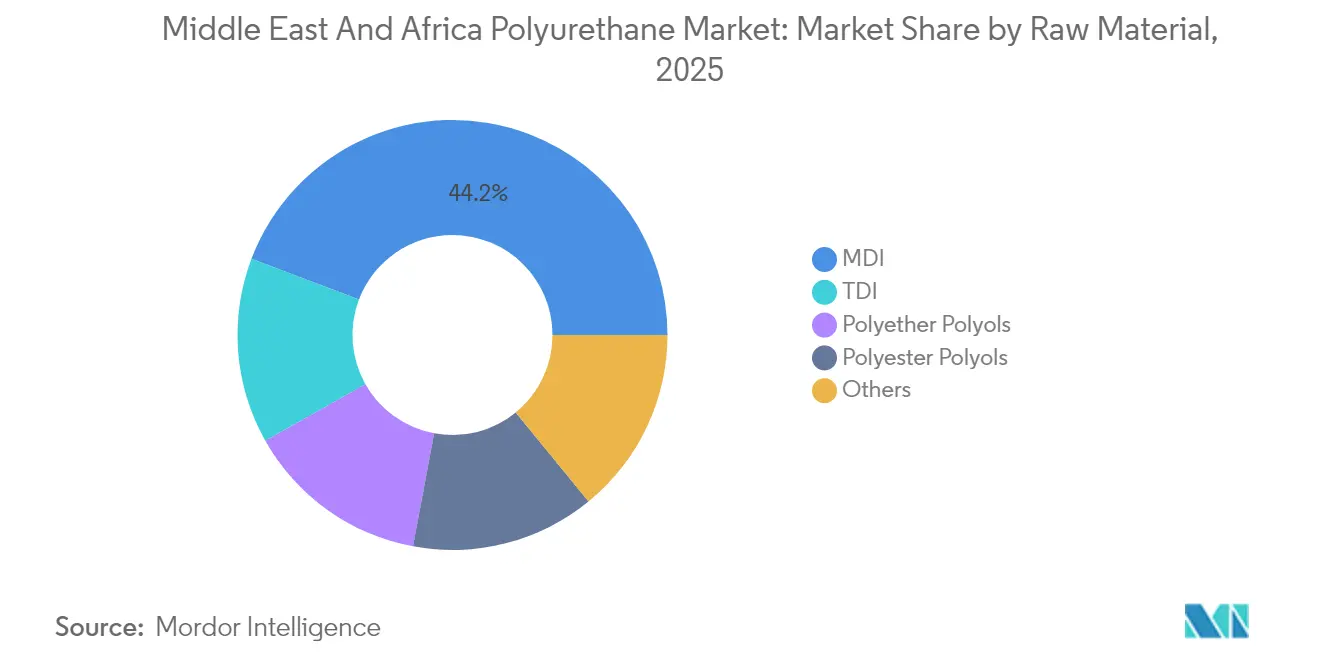

- By raw material, MDI led with 44.23% revenue share in 2025; bio-based polyols are expected to post the fastest 5.71% CAGR during the outlook period.

- By geography, Saudi Arabia commanded 24.05% market share in 2025, whereas the United Arab Emirates is projected to record a 4.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Polyurethane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-led construction boom in GCC | +1.20% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Expansion of cold-chain logistics | +0.80% | Sub-Saharan Africa, GCC | Long term (≥ 4 years) |

| Automotive and EV production localization | +0.60% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Growth in regional furniture & mattress output | +0.40% | Saudi Arabia, Egypt, Morocco | Short term (≤ 2 years) |

| District-cooling mandates | +0.30% | UAE, Qatar, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Construction Boom in GCC

The Gulf’s multibillion-dollar project pipeline is the single largest demand catalyst for rigid foams, sealants, and spray-applied insulation. Mega-developments such as NEOM, the Red Sea tourism corridor, and Dubai 2040 urban upgrades specify building-envelope solutions that cut operational emissions by at least 50%. Polyurethane panels and spray systems deliver the required thermal resistance and moisture control under prolonged desert exposure. Modular on-site worker housing and temporary logistics facilities add year-round volume for prefabricated panels containing rigid polyurethane cores. Mandatory local-content thresholds are already encouraging international formulators to build blending plants inside Saudi Arabia and the UAE, shortening lead times and lowering import tariffs. The Middle East and Africa polyurethane market therefore benefits directly from the region’s determination to diversify beyond hydrocarbons.

Expansion of Cold-Chain Logistics and Insulation Demand

Rising food-security priorities and vaccine-distribution programs are accelerating investment in temperature-controlled warehouses, solar-powered refrigeration kiosks, and insulated shipping containers. Roughly half of produce losses in sub-Saharan Africa are linked to inadequate cooling infrastructure. Distributed cold rooms equipped with polyurethane-insulated panels and phase-change storage modules cut spoilage, enhance farmer incomes, and meet climate-adaptation funding criteria. African start-ups have deployed thousands of solar refrigeration units since 2020, illustrating the scalable addressable volume for rigid foams. International development banks routinely stipulate high-R-value insulation to maximize energy savings, locking polyurethane into project specifications. These trends reinforce long-run demand visibility for the Middle East and Africa polyurethane market.

Automotive and EV Production Localization

Saudi Arabia targets 500,000 electric vehicles per year by 2030 and has allocated multi-billion-dollar incentives to lure global OEMs. Vehicle production in ambient temperatures exceeding 40 °C requires advanced battery potting compounds, lightweight interior foams, and weather-resistant coatings. Polyurethane systems offer the necessary dielectric stability and mechanical cushioning, reducing thermal stress on battery cells and occupants alike. Local-content mandates are prompting Tier-1 suppliers to co-locate molding and compounding lines, cutting lead times and import duties. Charging-station rollouts across six Gulf states add demand for polyurethane-coated cables, encapsulated electronic modules, and corrosion-resistant enclosure seals. As a result, automotive is the fastest-growing consumer segment in the Middle East and Africa polyurethane market.

Growth in Regional Furniture and Mattress Manufacturing

Residential completions, e-commerce adoption, and hospitality investments are stimulating regional furniture output. Flexible polyurethane foam dominates seating, bedding, and ergonomic office products due to its exceptional comfort-to-weight ratio and flame-retardant properties. Local producers save logistics costs and gain formulation flexibility by sourcing foam blocks regionally rather than importing finished goods. The relocation of value chains supports job creation and dovetails with government diversification agendas. Short product cycles in online retail further favor local suppliers capable of fast prototyping and customized density grades. In turn, these dynamics lift flexible-foam consumption inside the Middle East and Africa polyurethane market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate & polyol prices | -0.90% | Import-dependent MEA | Short term (≤ 2 years) |

| Stricter VOC & worker-safety limits on TDI/MDI | -0.40% | GCC industrial zones, South Africa | Medium term (2-4 years) |

| Reduced energy subsidies | -0.30% | Saudi Arabia, UAE, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and Worker-Safety Limits on TDI/MDI

The American Conference of Governmental Industrial Hygienists has cut the 8-hour exposure limit for TDI to 1 ppb. Regional factories will need real-time monitoring, specialized ventilation, and biomonitoring programs to remain compliant. Capital upgrades weigh heaviest on small and mid-sized converters that lack scale economies, potentially accelerating consolidation. Multinationals are revising SDS documentation and offering lower-monomer alternatives, but pricing uplifts are unavoidable. Compliance spending is expected to temper near-term margins inside the Middle East and Africa polyurethane market[1]Covestro "New toluene diisocyanate TDI occupational exposure limits adopted by the ACGIH," solutions.covestro.com.

Reduced Energy Subsidies Inflating Processing Costs

Fiscal reforms across Saudi Arabia, Egypt, and the UAE are phasing out preferential energy tariffs. Polyurethane reactors and continuous-panel lines are electricity-intensive, and higher utility bills erode the historical cost advantage of Gulf producers. The issue is compounded by elevated shipping rates, pushing converters to optimize batch sizes and adopt energy-saving catalysts. Although subsidy removal supports long-term budget stability, it introduces near-term cost pass-through challenges for the Middle East and Africa polyurethane market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Foams Sustain Leadership as Coating Demand Intensifies

Foams generated 59.28% of revenue in 2025, cementing their role as the backbone of insulation, seating, and packaging. Rigid foams benefit most from district-cooling lines and energy-efficient building codes, while flexible foams ride the wave of automotive and furniture expansion. Spray foam usage is climbing in roof retrofits where seamless coverage outperforms board products under thermal-cycling stress. The coatings subsector, though smaller, is growing at a robust 5.19% CAGR on the back of marine anti-corrosion contracts and industrial floor refurbishments. Formulators are introducing zero-VOC polyurethane dispersion technologies to meet tighter emission caps. Collectively, these dynamics reinforce the revenue resilience of the Middle East and Africa polyurethane market.

Advances in elastomer chemistry are opening niches in oil-field pipeline pigs, mining screens, and conveyor belts that demand abrasion resistance. Adhesives and sealants profit from modular construction practices, with moisture-cured grades enabling rapid on-site assembly. Vertical integration by ADNOC after acquiring Covestro is expected to yield cost-optimized foam systems for local converters, enhancing supply-chain agility inside the Middle East and Africa polyurethane market.

By End-User Industry: Construction Dominates, Automotive Races Ahead

Building and construction consumed 38.05% of polyurethane output in 2025. Government-backed housing schemes, smart-city districts, and rail corridors specify high-R-value insulation and low-VOC coatings that align with green-building standards. The automotive sector is recording the quickest gains at a 5.38% CAGR, propelled by large-scale EV assembly plants and charging-infrastructure programs. Polyurethane’s light weight and vibration-damping qualities meet vehicle range and passenger-comfort targets, while thermal-interface foams safeguard battery modules. Electronics and appliances leverage rigid foams for refrigerator liners and HVAC ducting, aided by rising middle-class spending. Hospitality-driven mattress replacement cycles lift demand for flame-retardant flexible foams, sustaining volume across diverse uses within the Middle East and Africa polyurethane market.

Oil and gas, although a modest consumer, purchases premium elastomers and pipeline coatings that tolerate sour-gas exposure and desert temperatures. Packaging volumes are up as food-delivery apps and pharmaceutical distributors adopt insulated containers lined with polyurethane. North-African footwear clusters continue to source microcellular soling systems, capitalizing on duty-free access to European buyers. SABIC’s post-turnaround earnings are financing additional system-house capacity to target these value-added niches.

By Raw Material: MDI Retains Prime Position Amid Bio-Based Upswing

MDI accounted for 44.23% of total feedstock in 2025 thanks to its versatility in rigid insulation boards, structural panels, and molded auto parts. TDI remains key for flexible furniture and bedding foams, though occupational-exposure scrutiny is encouraging formulators to adopt low-monomer grades. Polyether polyols supply mass-market applications, while polyester polyols serve coatings that require chemical resilience. Bio-based polyols—sourced from plant oils and captured CO₂—are the most dynamic sub-category, expanding at 5.71% CAGR as brand owners set Scope 3 emission targets. A portfolio of carbon-negative polyols, commercialized by Aether Industries and deployed by HB Fuller, exemplifies emerging circular models inside the Middle East and Africa polyurethane market.

ADNOC’s integration with Covestro brings cutting-edge phosgene-free MDI technology and positions Abu Dhabi as a global export base. Meanwhile, Saudi Aramco’s research into CO₂-based polyols signals a long-run shift toward lower-carbon chemistries. Supply-chain resilience is moving up the agenda as Red Sea shipping routes face geopolitical disruptions, pushing converters to diversify sourcing for critical isocyanates and polyols.

Geography Analysis

Saudi Arabia contributed 24.05% of 2025 sales, anchored by NEOM’s giga-projects, a 500,000-unit EV target, and a robust housing program. Rigid insulation boards, spray foams, and specialty elastomers dominate local specifications, reflecting performance demands under extreme heat. The United Arab Emirates is the fastest-growing geography with a projected 4.84% CAGR thanks to district-cooling build-outs, free-zone logistics hubs, and Expo-legacy expansion projects. Dubai’s enforcement of certified insulation values has made polyurethane sandwich panels the default choice for new commercial towers.

South Africa remains the largest African buyer, leveraging its diversified manufacturing base and state-funded infrastructure upgrades. Local extrusion plants blend imported isocyanates with domestic polyols to serve refrigeration, automotive trim, and mining belts. Egypt’s construction recovery, buoyed by currency stabilization and multilateral financing, is spurring greenfield foam plants near Cairo’s industrial zones. Morocco benefits from proximity to European export markets and incentives for automotive wire-harness and seat-cushion production, keeping flexible-foam lines running near capacity. Collectively, these dynamics support geographically balanced growth for the Middle East and Africa polyurethane market. Regional integration initiatives, including the GCC single-market and the African Continental Free Trade Area, are streamlining customs regimes and accelerating cross-border raw-material flows. Logistics investments such as Saudi Arabia’s land-bridge rail and Kenya’s Lamu port strengthen supply-chain resilience against maritime disruptions. Climate-driven demand bifurcates by latitude: Gulf states mandate heat-reflective coatings, whereas sub-Saharan economies prioritize cold-chain infrastructure, diversifying application mixes inside the Middle East and Africa polyurethane market.

Competitive Landscape

The Middle East and Africa polyurethane market is consolidated. ADNOC’s USD 16.4 billion purchase of Covestro delivers upstream-to-specialty integration, promising competitive feedstock pricing and R&D spillovers. Parallel price rises by Huntsman, BASF, and Wanhua signal disciplined supply management and reinforce oligopolistic tendencies. Regional champions such as SABIC are investing in low-carbon methanol and circularity platforms to secure customer loyalty under tightening ESG audits.

Technology differentiation is winning contracts: digital twin process controls reduce scrap rates, while novel catalysts cut curing times by 20% in high-throughput panel lines. Service-based business models, such as on-site foam cutting and cold-chain maintenance packages, deepen customer lock-in. Emerging start-ups focus on bio-based feedstocks and chemical-recycling pilots for mattress foam, attracting venture funds aligned with climate mandates. The competitive field is therefore a blend of integrated majors, agile regional specialists, and sustainability-driven disruptors, all seeking share in the Middle East and Africa polyurethane market.

Middle East And Africa Polyurethane Industry Leaders

-

BASF

-

BCI Holding SA

-

Covestro AG

-

Dow

-

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Huntsman raised the prices of MDI and polyurethane system products by EUR 125/ton across Europe, Africa, the Middle East, and India, citing rising costs of raw materials, energy, and logistics. This price increase is likely to drive up costs in the Middle East and Africa polyurethane market, potentially influencing pricing strategies and market competitiveness in the region.

- October 2024: ADNOC completed its USD 16.4 billion acquisition of Covestro, achieving vertical integration from petrochemical feedstocks to specialty polyurethanes. This development strengthens Abu Dhabi's position as a key global chemicals hub while enhancing regional supply capabilities and access to advanced technologies.

Middle East And Africa Polyurethane Market Report Scope

Polyurethane is a plastic polymer material used to produce modern, versatile, and safe consumer and industrial products that are environmentally friendly. Polyurethane is formed by reacting a polyol (an alcohol with more than two reactive hydroxyl groups per molecule) with a diisocyanate or a polymeric isocyanate in the presence of suitable catalysts and additives.

The Middle East and Africa polyurethane market is segmented by application, end-user, and geography. By application, the market is segmented into foams, coatings, adhesives and sealants, elastomers, and other applications. By end-user, the market is segmented into furniture and interiors, building and construction, electronics and appliances, automotive, footwear, packaging, and other End-user industries. The report also covers the market size and forecasts for the market in seven major countries across the Middle East and Africa region.

For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Application

| Foams | Rigid Foam |

| Flexible Foam | |

| Spray Foam | |

| Coatings | |

| Adhesives and Sealants | |

| Elastomers | |

| Others |

By End-user Industry

| Building and Construction |

| Furniture and Bedding |

| Automotive |

| Electronics and Appliances |

| Footwear |

| Packaging |

| Oil and Gas and Mining |

| Others |

By Raw Material

| MDI |

| TDI |

| Polyether Polyols |

| Polyester Polyols |

| Others (Bio-based Polyols) |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| South Africa |

| Egypt |

| Kuwait |

| Qatar |

| Morocco |

| Rest of Middle-East and Africa |

| By Application | Foams | Rigid Foam |

| Flexible Foam | ||

| Spray Foam | ||

| Coatings | ||

| Adhesives and Sealants | ||

| Elastomers | ||

| Others | ||

| By End-user Industry | Building and Construction | |

| Furniture and Bedding | ||

| Automotive | ||

| Electronics and Appliances | ||

| Footwear | ||

| Packaging | ||

| Oil and Gas and Mining | ||

| Others | ||

| By Raw Material | MDI | |

| TDI | ||

| Polyether Polyols | ||

| Polyester Polyols | ||

| Others (Bio-based Polyols) | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Kuwait | ||

| Qatar | ||

| Morocco | ||

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

How large is the Middle East and Africa polyurethane sector in 2026?

The Middle East and Africa polyurethane market size is USD 2.76 billion in 2026, with a 4.46% CAGR outlook to 2031.

Which application generates the most polyurethane demand across the region?

Foams lead, capturing 59.28% revenue in 2025 thanks to construction insulation, furniture cushions, and automotive seating.

What is driving polyurethane usage in Gulf construction?

Mega-projects and district-cooling mandates require high-R-value rigid foams and coatings to meet stringent energy-efficiency targets.

Why are bio-based polyols gaining traction?

Corporate carbon-reduction commitments and new low-carbon procurement policies support a 5.71% CAGR for bio-based polyols through 2031.

How will ADNOC’s acquisition of Covestro affect regional supply?

The deal secures local isocyanate production, improves feedstock availability, and is expected to lower costs for downstream converters.

Which country offers the fastest growth opportunity?

The United Arab Emirates is projected to expand at a 4.84% CAGR to 2031, driven by logistics-hub expansion and stringent building codes.

Page last updated on: