Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

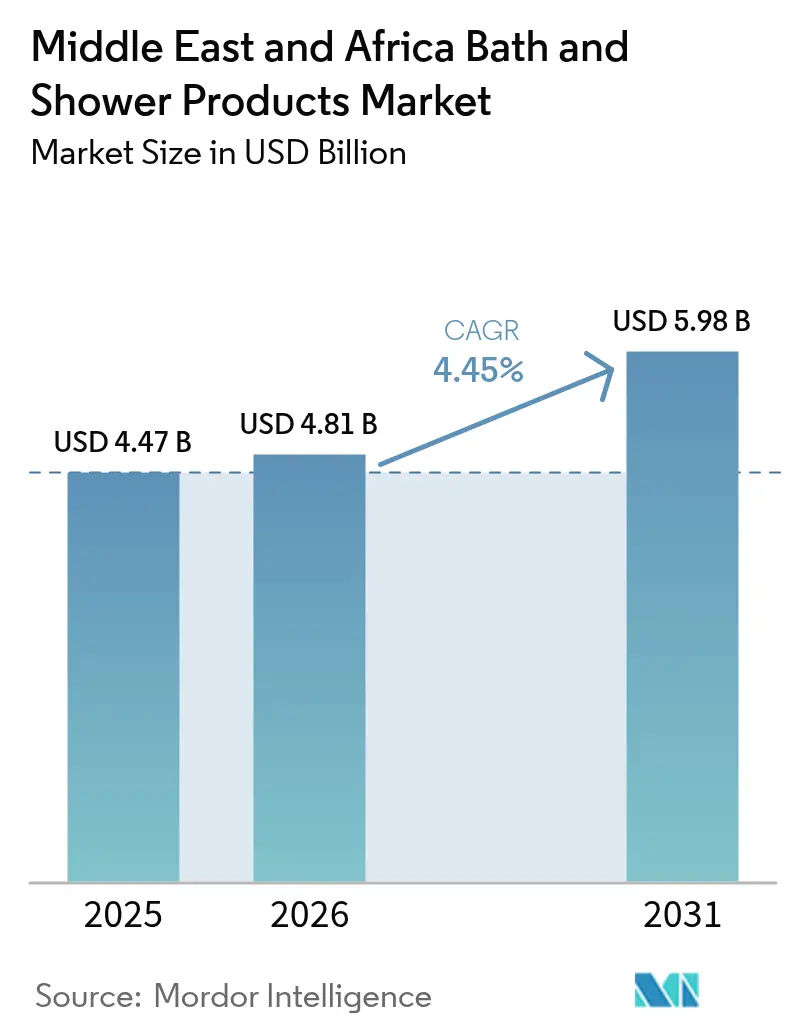

| Base Year Market Size (2025) | USD 4.47 Billion |

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 5.98 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Bath And Shower Products Market Analysis by Mordor Intelligence

The Middle East and Africa bath and shower products market size is expected to grow from USD 4.47 billion in 2025 to around USD 4.81 billion in 2026, with projections showing it could reach USD 5.98 billion by 2031. This reflects a CAGR of 4.45% during the 2026-2031 period. The market’s growth is being driven by rapid urbanization, increasing hygiene awareness among the middle class, and a strong shift toward online shopping. Body wash and shower gel are currently the most popular product types, but bar soap is growing the fastest. This trend highlights two key dynamics, including affordability driving demand in sub-Saharan Africa and premiumization gaining traction in the Gulf states. Organic products are also becoming more popular as consumers pay closer attention to ingredient lists and look for halal and clean label options. E-commerce platforms are benefiting from higher average order values and the growing influence of social media marketing, which is speeding up digital adoption across the region.

Key Report Takeaways

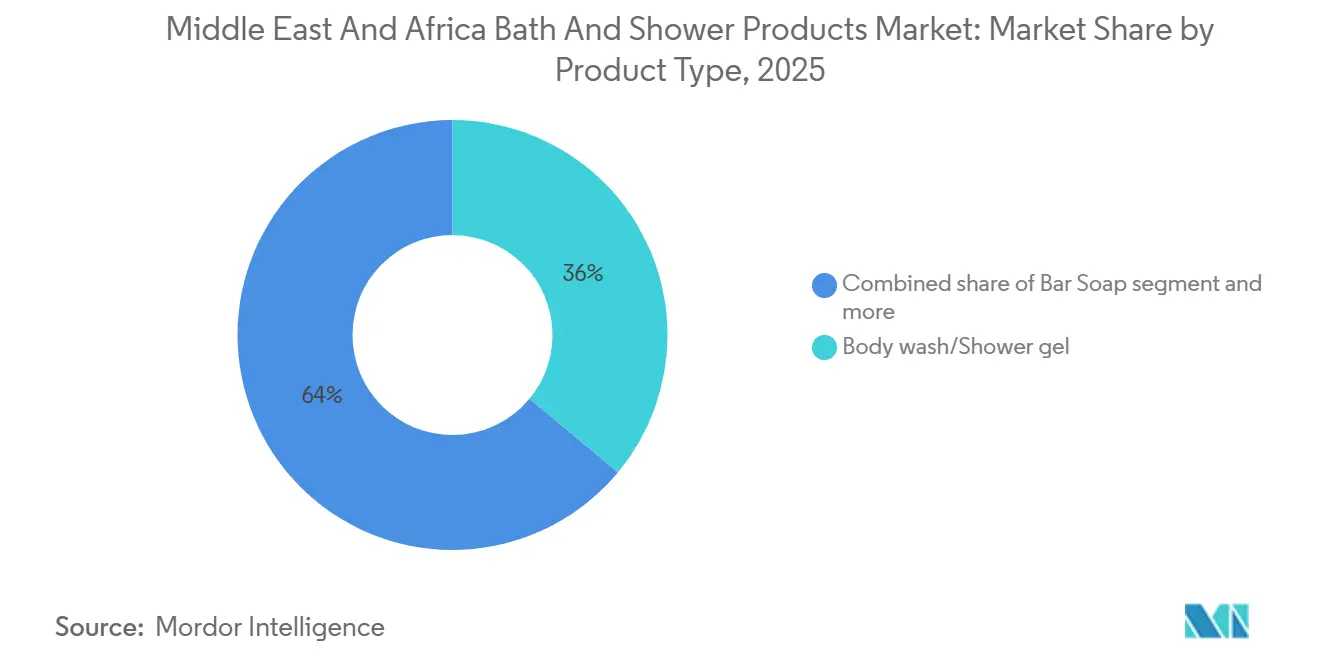

- By product type, body wash/shower gel led with 36.02% share in 2025, while bar soap is forecast to post the fastest 5.18% CAGR through 2031.

- By category, conventional products held the largest revenue share at 65.12% in 2025, while organic offerings are projected to grow at a 5.78% CAGR through 2031, driven by the convergence of clean-label and halal standards.

- By end-user, adults accounted for the largest revenue share at 87.25% in 2025, whereas the kids segment is expected to grow at a 6.06% CAGR, supported by the demand for hypoallergenic and pH-balanced formulations.

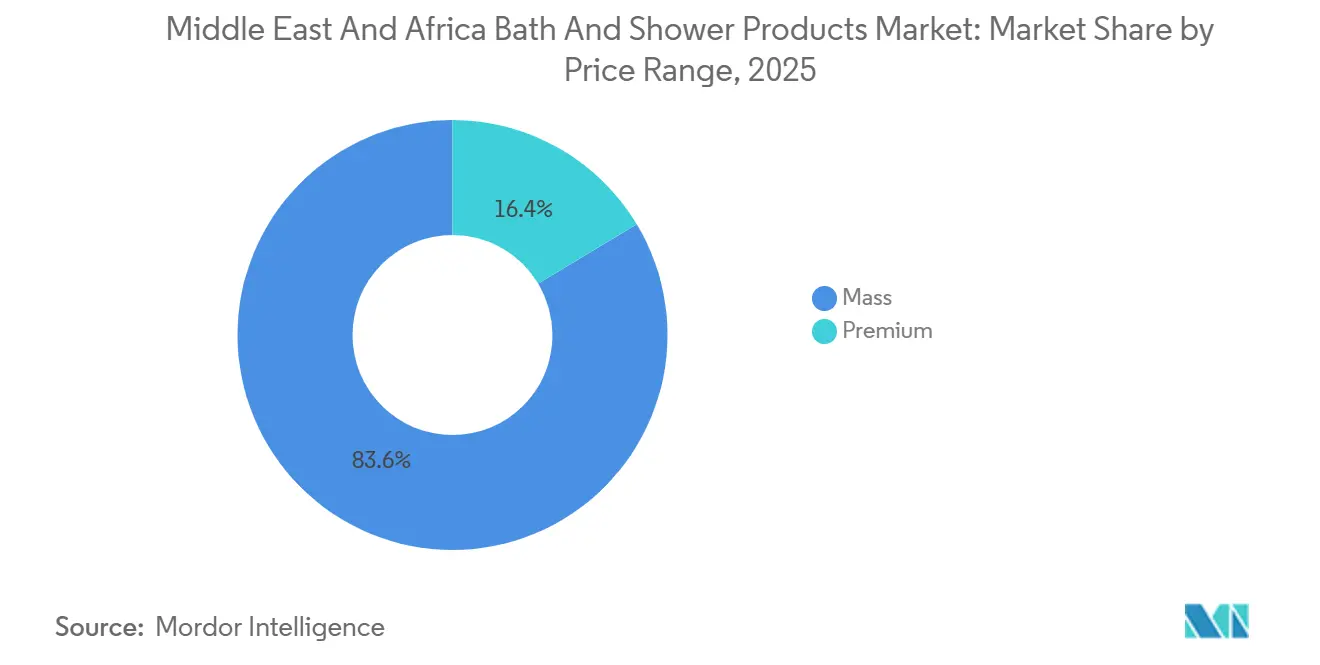

- By price range, mass products dominated with 83.62% in value share as the largest segment in 2025, while the premium tier accounted for 6.89% and is forecast to grow at high single-digit rates, driven by affluent Gulf consumers and duty-free retail hubs.

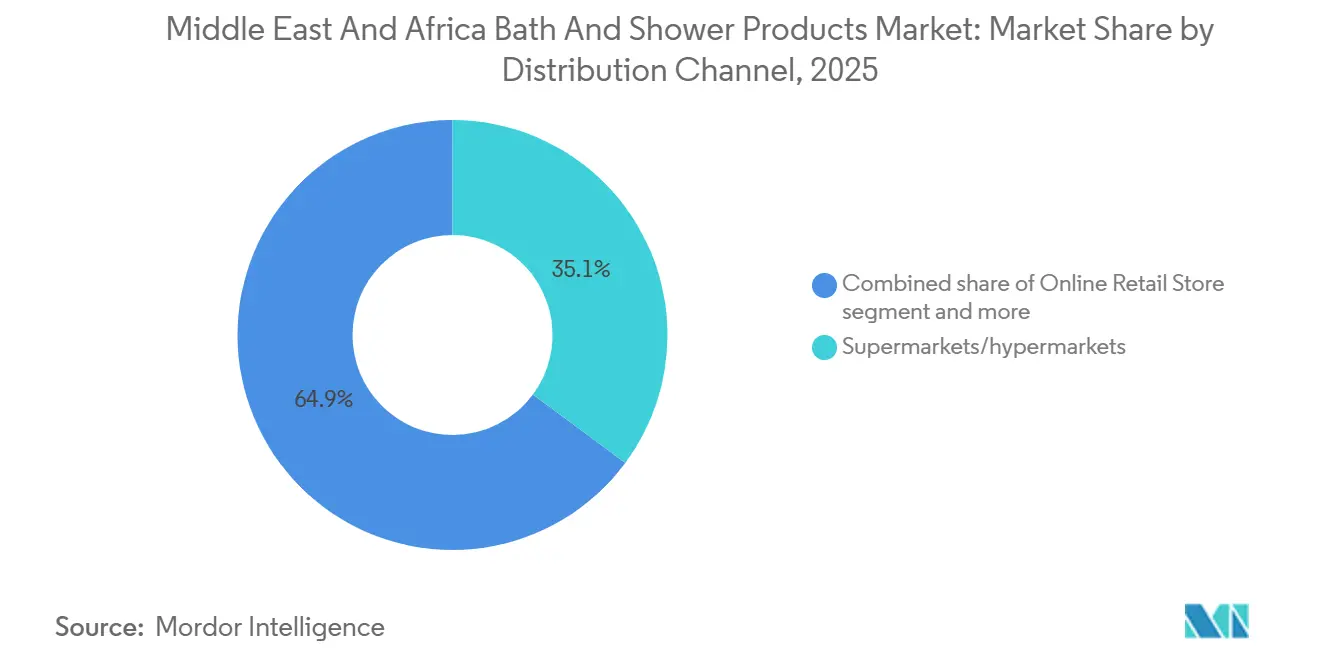

- By distribution channel, supermarkets/hypermarkets held the largest revenue share at 35.14% in 2025, while online retail is expected to grow at a 5.81% CAGR, supported by improvements in last-mile infrastructure.

- By geography, Saudi Arabia contributed the largest revenue share at 25.50% in 2025, while South Africa is projected to grow at a 6.31% CAGR, driven by investments in modern retail and supply-chain efficiency.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Bath And Shower Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hygiene awareness among the middle-class population | +0.8% | Global, with pronounced gains in Nigeria, Egypt, South Africa | Medium term (2-4 years) |

| Increasing preference for sulfate-free and pH-balanced products | + 0.6% | The United Arab Emirates, Saudi Arabia, South Africa core, spillover to Turkey | Short term (≤ 2 years) |

| Impact of social media and celebrity endorsements on market growth | + 0.7% | Gulf Cooperation Council states, urban Turkey | Short term (≤ 2 years) |

| Growing demand for natural and organic ingredients | +0.9% | Global, early adoption in the United Arab Emirates, Saudi Arabia, and South Africa | Medium term (2-4 years) |

| Increasing preference for premium and luxury bath products | +0.5% | Saudi Arabia, the United Arab Emirates, Qatar, Kuwait | Long term (≥ 4 years) |

| Product innovation and multifunctionality driving market growth | +0.7% | Global, technology hubs in the United Arab Emirates, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising hygiene awareness among the middle-class population

The economic report on Africa highlights that the continent is set to remain the world's second-fastest-growing region, with more than half of its nations now classified as middle-income[1]Source: United Nations Economic Commission for Africa, "ECONOMIC REPORT ON AFRICA", africarenewal.un.org. This economic transformation has led to a notable increase in the adoption of antibacterial cleansers, which were previously considered non-essential. In December 2025, Unilever introduced Lifebuoy Skin Solutions, priced above standard bar soaps, and achieved sales volumes that exceeded expectations within nine months. The post-COVID-19 period has entrenched handwashing as a daily routine, supported by public health campaigns in countries like Egypt and South Africa. This established habit continues to drive market growth, even as the initial surge in pandemic-related panic buying has subsided. Urban areas with dense populations remain pivotal, as the message of infection prevention strongly resonates within these communities.

Increasing preference for sulfate-free and pH-balanced products

The personal care market is undergoing a significant transformation as consumers grow more aware of the link between sulfates and skin irritation. The Saudi Food and Drug Authority (SFDA) has highlighted the harmful effects of sunlight exposure, including premature skin aging, burns, and eye damage, recommending sunscreen with at least SPF 30, limiting sun exposure during peak hours, and using protective accessories like hats and sunglasses[2]Source: Saudi Food and Drug Authority "SFDA: Using Sunscreens Reduces Tanning Risks", sfda.gov.sa. In response to the demand for gentler products, brands are reformulating offerings, such as Dove’s pH-balanced body wash with a pH of 6.9, launched in early 2025 and gaining popularity in UAE supermarkets. Social media further drives this trend, with dermatologists and influencers advocating sulfate free products, increasing consumer awareness, and encouraging brands to expand their portfolios with milder solutions.

Impact of social media and celebrity endorsements on market growth

In South Africa, social media usage is projected to reach 29.1 million users in 2025, accounting for 44.9% of the total population[3]Source: World Population Review, "Social Media Users by Country 2026", worldpopulationreview.com. This extensive engagement highlights the significant impact of social media and celebrity endorsements on market growth. Gulf residents, for instance, spend an average of nearly three hours daily on social media, making it a powerful channel for influencing consumer purchasing decisions, with influencers playing a pivotal role in shaping preferences. While this channel enhances brand visibility, it also introduces challenges such as demand volatility due to the rapid evolution of viral trends. Market participants are increasingly adopting agile product development pipelines and flexible manufacturing systems to address these challenges. These approaches allow companies to respond swiftly to shifting consumer demands and leverage emerging trends effectively, while also mitigating risks associated with inventory mismanagement.

Product innovation and multifunctionality driving market growth

Water scarcity in regions like the Gulf states and sub Saharan Africa is driving demand for sustainable, waterless, and multifunctional products. P&G's Sustainability Report highlights that these products reduce shipping weight and eliminate cold chain logistics. In 2024, L'Oréal committed to increasing waterless product launches by the decade's end, starting with Garnier Ultimate Blends solid shampoo bars in the UAE and Saudi Arabia. Multifunctional products like Nivea Men's 3-in-1 body wash, combining cleansing, moisturizing, and deodorizing, appeal to busy consumers, as noted by Beiersdorf. CeraVe's AM Facial Moisturizing Lotion with SPF 30, initially for facial use, is now popular in the Gulf for body application due to high sun exposure, prompting the brand to explore bodyspecific SPF products. Unilever's patent for timerelease vitamin E microcapsules in body wash highlights innovations in encapsulation technology, enabling gradual release of active ingredients and fragrances, as detailed in Unilever's Patent Filing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of counterfeit products | -0.5% | Nigeria, Egypt, Morocco, with transit routes through the United Arab Emirates | Short term (≤ 2 years) |

| Regulatory barriers and delays | -0.4% | Saudi Arabia, Egypt, Nigeria, with harmonization gaps across Middle East and Africa | Medium term (2-4 years) |

| Supply chain disruptions caused by poor transportation infrastructure | -0.6% | Sub-Saharan Africa, North Africa inland regions | Long term (≥ 4 years) |

| High costs associated with cold chain storage operations | -0.3% | Nigeria, Egypt, Saudi Arabia, the United Arab Emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of counterfeit products

Counterfeit personal care products harm brand reputation and pose health risks to consumers. According to the Organisation for Economic Co-operation and Development (OECD), counterfeit cosmetics and personal care items make up a notable share of the global trade in fake goods. Morocco, the UAE, and Nigeria are identified as key transit and source points for these counterfeit products, as highlighted in an OECD report. In September 2025, Nigeria's National Agency for Food and Drug Administration and Control (NAFDAC) seized counterfeit personal care items. These included fake creams and soaps, which were found to contain dangerous levels of mercury and lead. To address this issue, multinational companies are increasing their investments in anti counterfeiting technologies. For example, in 2024, Under resourced regulatory agencies and weak border controls make enforcement challenging. The mass market segment is particularly affected by counterfeit products, as pricesensitive consumers often turn to informal channels. These channels attract buyers with discounts ranging from 30 to 50%, unintentionally driving demand for counterfeit goods.

Regulatory barriers and delays

The Middle East and Africa often face overlapping testing and registration requirements, delaying market entry and increasing compliance costs. In Saudi Arabia, the SFDA takes months to approve cosmetic products, requiring stability tests, microbial challenge tests, and halal certifications. Dubai Municipality's SFDA in the UAE processes approvals faster, within 3 to 6 months. In 2024, Egypt's National Organization for Safety and Cleanliness of Aquatic Environment mandated local clinical trials for claims like skin lightening or anti aging. Nigeria's NAFDAC, despite stricter enforcement, struggles with capacity issues, causing delays in product registrations. Efforts to harmonize regulations, led by the African Continental Free Trade Area's cosmetic standards working group, are still in early stages with minimal progress on mutual recognition agreements. Multinational corporations leverage regulatory teams and established authority relationships, while smaller brands and local manufacturers face greater challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bar Soap Gains Ground Through Affordability and Premiumization

By 2025, urban consumers favored body wash/shower gel, capturing 36.02% of the market. This trend highlights a growing preference for convenient pump dispensers and a belief that these products offer superior moisturization compared to traditional bar soaps. Urban areas, with their emphasis on convenience and hygiene, are driving the robust demand for body wash and shower gel.

Bar soap is projected to grow at a CAGR of 5.18% through 2031, driven by its affordability and regional demand. In sub-Saharan Africa, bar soap dominates the mass market due to its lower price, while premium variants with ingredients like oud and argan oil are gaining traction in Gulf markets. Additionally, niche wellness products, such as body scrubs and bath salts, are witnessing growth, with Bath & Body Works' aromatherapy range performing well in the UAE and Saudi Arabia.

By Category: Organic Products Surge Amid Clean Label Consciousness

Conventional products accounted for 65.12% of the market share in 2025. This strong position is supported by established distribution networks, cost advantages from economies of scale, and consumer trust in well-known brands like Dove, Nivea, and Lux. These products also benefit from longer shelf life, with synthetic preservatives extending their usability to 24 to 36 months, compared to 12 to 18 months for organic alternatives. Additionally, the reliance on imported raw materials, such as shea butter and aloe vera extracts from West Africa and Europe, increases the production costs of organic products, making conventional options more accessible and cost-effective.

Organic products are expected to grow at a compound annual growth rate (CAGR) of 5.78% through 2031, making them the fastest-growing segment. This growth is driven by rising consumer interest in ingredient transparency and halal-certified products, particularly in the Middle East and Africa. According to NSF International, a large group of consumers in the region actively seek "natural" or "organic" labels, with many willing to pay a premium of 20 to 35% for certified products. Regulatory initiatives, such as Egypt's introduction of organic cosmetic certification standards in 2024 and the GCC's halal certification frameworks, further support this trend.

By End User: Kids Segment Accelerates on Parental Safety Concerns

In 2025, adults dominated 87.25% of market demand, driven by a larger population and higher per capita use of body wash, bar soap, and specialty products. Anti-aging and skin brightening innovations, such as Olay's Regenerist Retinol 24 body lotion and Neutrogena's Hydro Boost body gel cream, are thriving in Gulf and South African markets. Gender specific products like Nivea Men's 3-in-1 body wash and Dove Men+Care are also boosting growth, supported by a 12% rise in male grooming demand in the Middle East in 2024.

The kids' segment, projected to grow at a 6.06% CAGR through 2031, is gaining momentum due to rising demand for hypoallergenic, tear-free, and dermatologist-tested products. Johnson & Johnson's Vita Rich Cocoa Butter body wash, launched in the UAE in May 2025, caters to mothers in dry Gulf climates. CeraVe's Baby line, introduced in South Africa in 2024, addresses pediatric skin issues like eczema. Regulatory measures, including Saudi Arabia's SFDA safety testing and allergen disclosure requirements, are shaping the market. Parents increasingly prefer pharmacy and specialty retail channels for certified products, with Halal certification remaining vital in Gulf markets.

By Price Range: Mass Segment Dominates While Premium Gains Momentum

The Middle East and Africa bath and shower products market is predominantly led by the mass price segment, which accounted for 83.62% of the total market share in 2025. This segment's dominance is attributed to the strong demand for affordable, everyday hygiene products among a price-sensitive and diverse consumer base. Factors such as rising urbanization, population growth, and improved access to modern retail formats, including supermarkets and hypermarkets, are driving high-volume sales of competitively priced soaps, shower gels, and body washes across the region.

Conversely, the premium segment, while smaller in market share, is anticipated to grow at a CAGR of 6.89% through 2031. This growth reflects shifting consumer preferences and increasing disposable incomes in key markets. Enhanced exposure to global beauty trends, heightened awareness of personal grooming, and a preference for high-quality, skin-beneficial formulations are encouraging consumers to opt for premium bath and shower products. This segment is distinguished by features such as natural ingredients, dermatologically tested formulations, sulfate-free and paraben-free claims, luxury fragrances, and visually appealing packaging.

By Distribution Channel: Digital Commerce Rises

By 2025, supermarkets/hypermarkets held a 35.14% share of the distribution market, driven by their one-stop shopping convenience, impulse purchase opportunities, and promotional visibility through loyalty programs and displays. Specialty stores, such as Clicks in South Africa and Nahdi in Saudi Arabia, focus on dermatologist-recommended products, supported by expert consultations and certifications.

Online retail channels are projected to grow at a CAGR of 5.81% through 2031, fueled by investments in e-commerce infrastructure and last-mile delivery in Gulf and South African markets. Platforms like Noon.com and Amazon.ae lead in the UAE, while Jumia and Takealot dominate in Nigeria and South Africa. Social commerce is rising, with L'Oréal's 2024 partnership with ArabyAds leveraging influencer content. Omnichannel strategies, such as Clicks Group's in-store pickups and Boots UAE's same-day delivery, are bridging online and offline channels.

Geography Analysis

In 2025, driven by high disposable incomes, strong halal governance, and a digitally adept youth population, Saudi Arabia represented 25.50% of the regional market value. The high disposable incomes have enabled consumers to spend more on premium and niche products, while robust halal governance ensures compliance with religious and ethical standards, fostering trust among consumers. Additionally, the digitally savvy youth have accelerated the adoption of online platforms, influencing purchasing behaviors and market dynamics.

South Africa, with a CAGR of 6.31%, benefits from an efficient logistics network and the growth of Clicks Group, which now operates over 800 stores. The country's well-developed logistics infrastructure supports the seamless distribution of goods, ensuring product availability across various regions. Pharmacy chains are strategically promoting dermatologist-recommended products, increasing the value per customer visit by catering to specific consumer needs and preferences. Additionally, incentives for domestic manufacturing are helping South Africa reduce its dependence on imports, fostering local production capabilities, and ensuring timely restocking to minimize stockouts and enhance supply chain efficiency.

The United Arab Emirates, leveraging Dubai’s expedited customs clearance in its free-zone infrastructure, has cemented its status as a re-export hub. The influx of tourists and their duty-free spending further bolsters its prominence in premium distribution. Turkey, merging European production standards with Middle Eastern demand, serves as both a substantial domestic market and a launchpad for exports to North Africa. While Egypt and Nigeria boast scale advantages, they grapple with infrastructure challenges and counterfeit threats, leading to heightened compliance and monitoring expenses. Morocco, alongside the wider MEA markets, remains fragmented, offering first movers a chance to introduce localized fragrances and pricing strategies tailored to informal retail practices.

Competitive Landscape

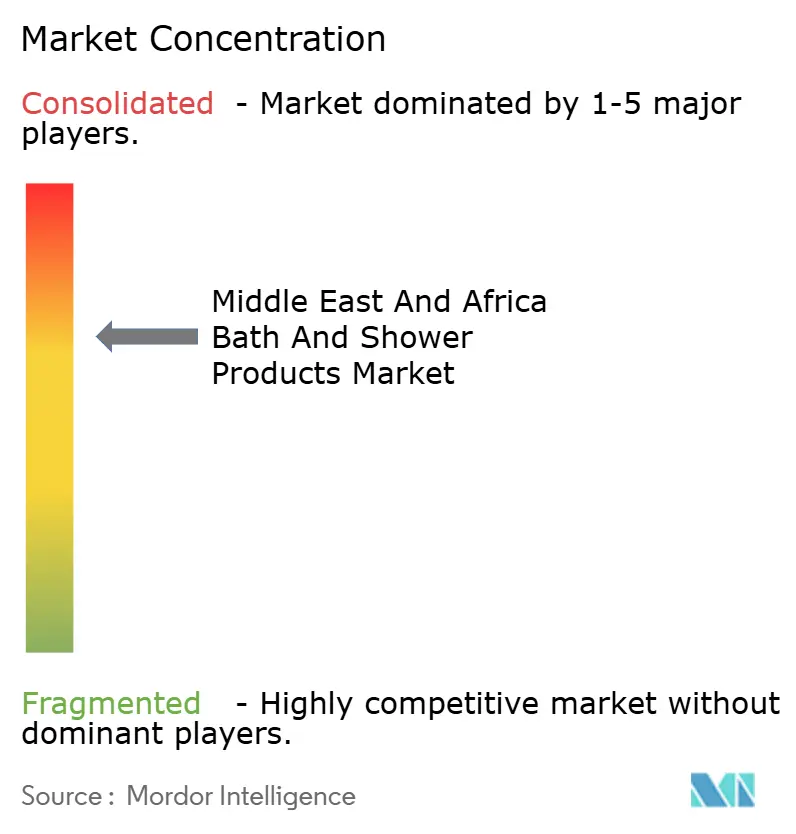

In the Middle East and Africa, the bath and shower products market is moderately consolidated. Major players like Unilever, Procter & Gamble, L’Oréal, Beiersdorf, and Johnson & Johnson dominate the mass market segment, leveraging advantages in procurement, research and development, and omnichannel distribution. Unilever showcases its strategic breadth, while its Lifebuoy brand focuses on hygiene growth in Nigeria, a new USD 150 million plant in the UAE caters to premium shoppers with organic products.

Regional players, including National Detergent Company and Savanna Laboratories, leverage cultural insights and nimble operations to carve out their niche. By emphasizing local fragrances, smaller pack sizes, and adaptable sourcing, they resonate with mid-tier consumers. Moreover, partnerships in contract manufacturing with global giants not only diversify their revenue streams but also bolster their technical expertise.

Digital prowess distinguishes the market leaders from the rest. For instance, P&G's introduction of a waterless shampoo in Gulf markets not only cuts down on freight costs but also aligns with sustainability goals. Similarly, L’Oréal's collaboration with a data centric influencer platform has led to notable conversion boosts, underscoring the value of performance driven marketing. Unilever's deployment of anti counterfeit blockchain technology in Nigeria not only bolsters consumer trust but also provides insights into purchasing behaviors. While mid sized players are tapping into direct-to-consumer strategies, they face challenges like escalating digital ad expenses and the intricacies of compliance as they grow.

Middle East And Africa Bath And Shower Products Industry Leaders

-

The Procter & Gamble Company

-

Unilever PLC

-

L'Oréal S.A.

-

Beiersdorf AG

-

L'Occitane International SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tork, a leading name in professional hygiene, introduced a new soap line designed for the climate challenges of the Middle East, India, and Africa (MEIA). The range, including liquid and foam soaps, was developed to perform in high temperatures and humidity, highlighting Tork's focus on regional needs and sustainability.

- February 2025: Stada introduced nine new Oilatum products in Saudi Arabia, which included "rich moisturizing creams for deep hydration, gentle body washes for everyday cleansing, and baby-focused items such as soothing bath bubbles and a comprehensive head-to-toe wash.

- January 2025: Cosmo Cosmetics, a leading and innovative beauty brand in the UAE, announces the opening of its cutting-edge manufacturing facility located in Dubai Investment Park 2.

Middle East And Africa Bath And Shower Products Market Report Scope

The bath and shower products market in Middle East and Africa is segmented in terms of liquid bath products (segmented into bath foam/gel and bath oil/pearls), shower products (segmented into body wash/shower gel and other shower products), other bath products (segmented into bath salts/powder and other bath additives), soaps (segmented into bar soaps and liquid soaps), and distribution channel (segmented into convenience stores, department stores, online retail, pharmacies, specialist retailers, supermarkets and hypermarkets, and other distribution channels. By geography, the market is segmented into South Africa, Saudi Arabia, the United Arab Emirates, and the Rest of Middle East and Africa.

By Product Type

| Bar Soap |

| Body Wash/Shower Gel |

| Other Product Type |

By Category

| Conventional |

| Organic |

By End-User

| Adult |

| Kids |

By Price Range

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Others Distribution Channel |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Bar Soap |

| Body Wash/Shower Gel | |

| Other Product Type | |

| By Category | Conventional |

| Organic | |

| By End-User | Adult |

| Kids | |

| By Price Range | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Others Distribution Channel | |

| By Geography | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the bath and shower products market in Middle East and Africa?

The market stood at USD 4.47 billion in 2025 and is projected to reach USD 4.81 billion in 2026.

How fast is the bath and shower products market expected to grow?

The market is forecast to expand at a 4.45% CAGR between 2026 and 2031, reaching USD 5.98 billion by the end of the period.

Which product type is growing fastest in the region?

Bar soap is the fastest-growing product type, set to rise at a 5.18% CAGR through 2031 owing to affordability in Africa and premium artisanal bars in Gulf markets.

Why are organic bath and shower products becoming popular?

Consumers increasingly demand ingredient transparency and halal-compliant formulations, driving organic lines to a 5.78% CAGR forecast.

Page last updated on: