Mexico Plastic Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

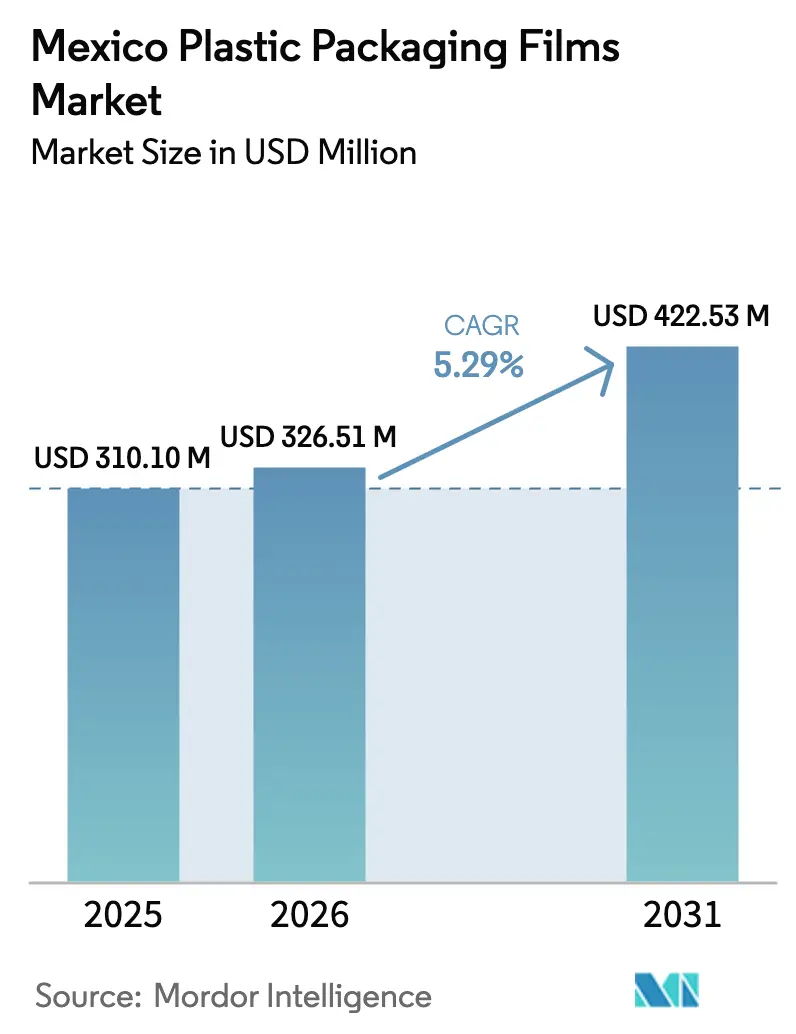

| Base Year Market Size (2025) | USD 310.10 Million |

| Market Size (2026) | USD 326.51 Million |

| Market Size (2031) | USD 422.53 Million |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Plastic Packaging Films Market Analysis by Mordor Intelligence

The Mexico plastic packaging films market size is expected to grow from USD 310.10 million in 2025 to USD 326.51 million in 2026 and is forecast to reach USD 422.53 million by 2031 at 5.29% CAGR over 2026-2031. This steady trajectory is anchored in near-shoring momentum that is drawing automotive, electronics, and consumer-goods assembly into northern states, thereby driving demand for local converting capacity. At the same time, new environmental regulations shrink the margin for low-value disposable formats and redirect investment toward lightweight, recycle-ready, and bio-based solutions. Producers that master downgauging, high-barrier coatings, and post-consumer-recycled (PCR) integration are winning long-term contracts from multinational brand owners that now treat Mexico as an export springboard to North America and Latin America. The resulting shift in specifications fuels a continuous technology cycle inside the Mexico plastic packaging films market, even as petrochemical feedstock volatility and electricity costs pressure margins.

Key retail and consumer indicators point to resilient consumption. ANTAD members plan USD 3 billion in retail investments by 2025, a 30.43% increase from 2024, which will expand shelf space and logistics hubs that need protective film formats for ambient, chilled, and frozen categories. E-commerce parcel volumes continue double-digit gains, pushing demand for puncture-resistant mailer films and cold-chain liners that limit temperature variability to ±2 °C over 48 hours. On the supply side, capacity additions center on three-layer blown extrusion lines equipped with gravimetric dosing and internal bubble cooling to hold thickness variation below ±2.5%. These investments, often financed by dollar-denominated loans, hedge against resin price swings and allow converters to deliver export-compliant jobs with shorter lead times. As a result, the Mexico plastic packaging films market maintains a balanced outlook, combining predictable end-market expansion with evolving product-mix upgrades toward higher value per kilogram.

Key Report Takeaways

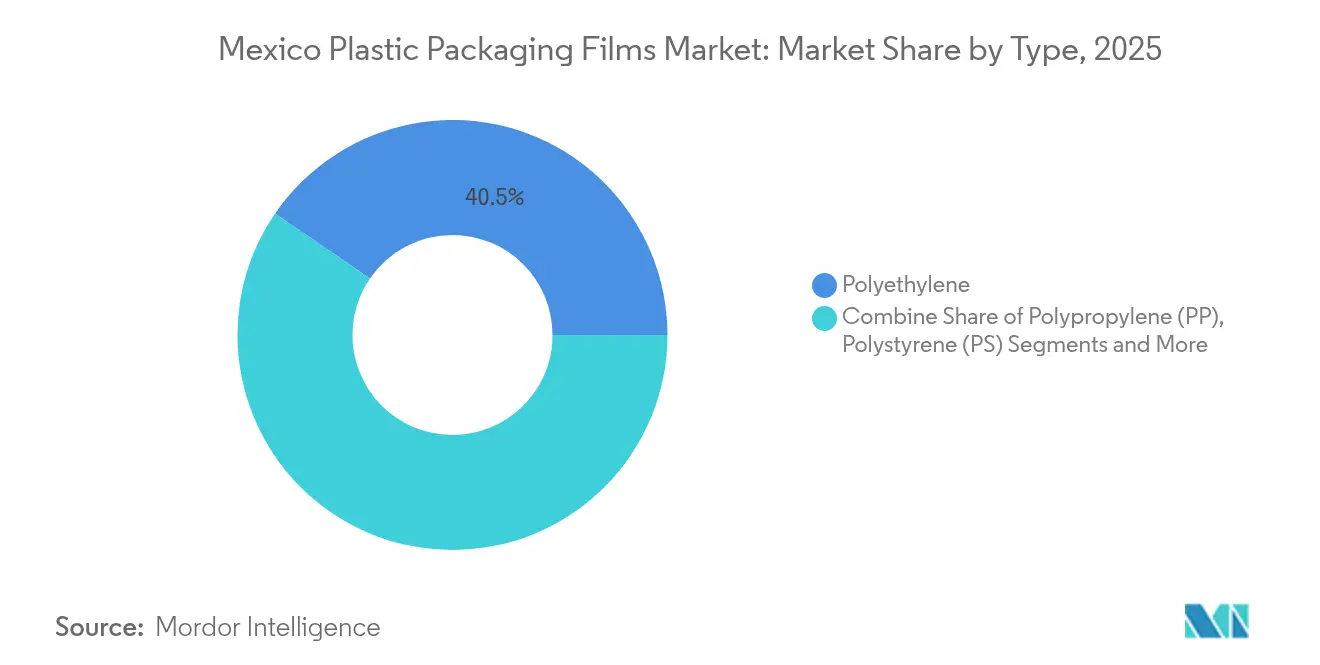

- By material, polyethylene led with 40.45% of Mexico plastic packaging films market share in 2025, while bio-based films are projected to register a 9.34% CAGR through 2031.

- By end-use industry, the food segment held 54.60% revenue share of the Mexico plastic packaging films market size in 2025; healthcare and pharmaceuticals post the fastest 8.52% CAGR to 2031.

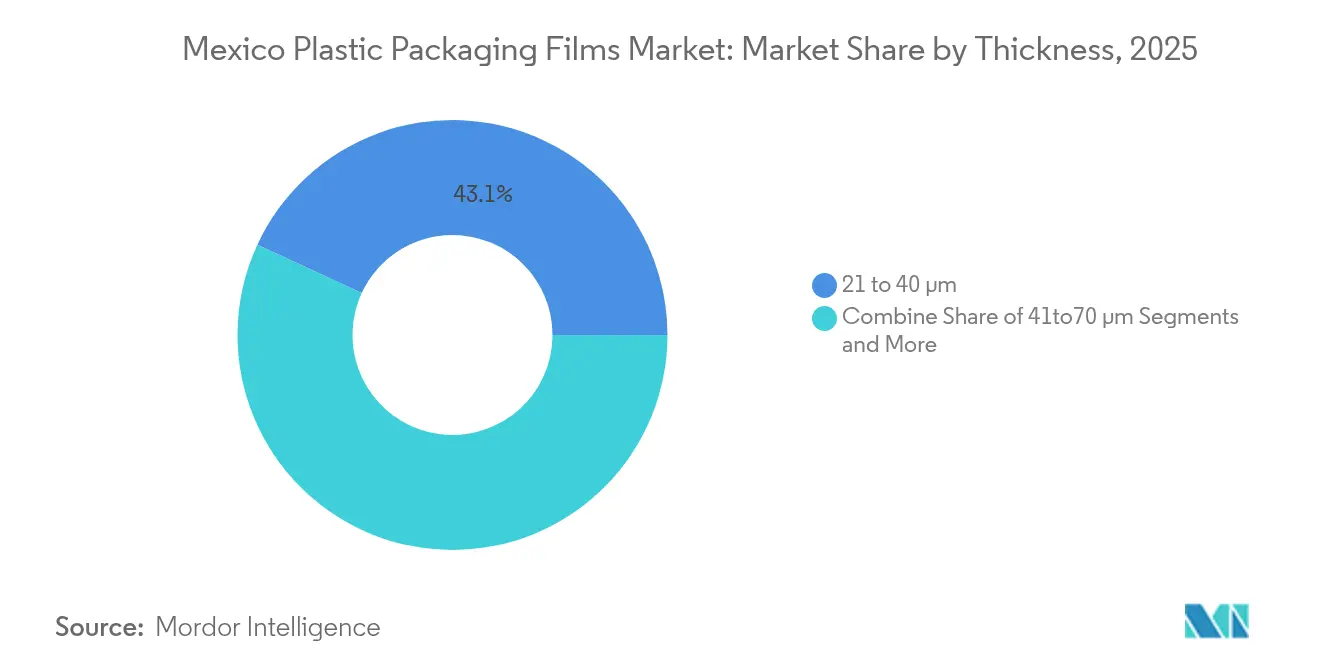

- By thickness, the 21–40 µm range captured 43.10% of Mexico plastic packaging films market share in 2025, whereas ultra-thin films (≤20 µm) are forecast to grow at 7.14% CAGR between 2026 and 2031.

- By functionality, barrier films accounted for 38.40% share of the Mexico plastic packaging films market size in 2025 and are advancing at a 5.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Plastic Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight packaging solutions | +1.2% | National, manufacturing corridors | Medium term (2–4 years) |

| Food and beverage shelf-life extension needs | +0.9% | National, export-focused regions | Short term (≤2 years) |

| Expansion of organized retail and e-commerce | +0.8% | Mexico City, Guadalajara, Monterrey | Medium term (2–4 years) |

| Advanced barrier coatings for export compliance | +0.7% | Border states, export zones | Short term (≤2 years) |

| Government incentives for recycling infrastructure | +0.5% | National, pilot programs in major cities | Long term (≥4 years) |

| Near-shoring spurs domestic film production capacity | +0.6% | Northern manufacturing clusters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight Packaging Solutions

Manufacturers across food, beverage, and durable-goods sectors prioritize weight reduction to curb freight costs and meet emissions targets. ANTAD’s USD 3 billion infrastructure program upgrades 1.4 million m² of distribution space, amplifying demand for stretch and shrink bundling that maximizes pallet density. Klöckner Pentaplast’s kp FlexiFlow flow-wrap, launched in October 2024, trims material weight by up to 75% while retaining equivalent oxygen barrier, proving that ultra-thin gauges can pass drop and compression tests.[1]Klöckner Pentaplast, “kp launches recyclable barrier flow-wrap films,” kpfilms.comAutomotive wire-harness suppliers use metallocene LLDPE at 17 µm to wrap parts for export without tearing, underscoring the growing competence of local converters in thin-film precision. As near-shoring accelerates, lightweighting becomes a purchasing criterion embedded in sourcing scorecards, guaranteeing recurring demand inside the Mexico plastic packaging films market.

Food and Beverage Shelf-Life Extension Needs

Mexico exported USD 55 billion in processed foods in 2024, much of it semi-perishable and shipped thousands of kilometers under USMCA rules. Brand owners rely on EVOH-based laminates that block oxygen ingress below 0.05 cc/m²-day for cheeses and deli meats. Tetra Pak reduced greenhouse-gas emissions by 20% in its Mexican operations and recycled 54,640 tons of packaging in 2023, showcasing how barrier innovation and carbon reduction co-evolve. A study in Food Chemistry Advances shows sensor-embedded PLA films detect total volatile basic nitrogen increases of 25 ppm, allowing exporters to flag spoilage before goods cross the border. Such paired shelf-life and transparency capabilities widen the gap between commodity and specialty supply within the Mexico plastic packaging films market.

Expansion of Organized Retail and E-Commerce

Retail e-commerce jumped 23% in 2024, boosting parcel film consumption for protective void-fill and ice-pack liners in last-mile grocery deliveries. The food-delivery boom generated 300,000 tons of plastic waste, prompting Mexico City and 27 municipalities to enforce extended producer responsibility fees. Converters answer with dual-use films that meet both curbside-recycling and optical-sortation criteria. Durable anti-puncture designs maintain dart impact above 180 g at −5 °C, ensuring frozen items survive 60-minute ride-hailing delivery loops. As omnichannel retailers merge store and online inventories, packaging must withstand pallet storage and courier handling, expanding the specification spectrum and cementing growth prospects for the Mexico plastic packaging films market.

Advanced Barrier Coatings for Export Compliance

March 2025 rules require pre-packaged foods bearing nutritional warnings to secure advertising permits, aligning Mexico with Codex Alimentarius principles. ExxonMobil and Hosokawa Alpine demonstrated a 95% polyethylene pouch with oxygen transmission below 0.5 cc/m²-day at 23 °C and 50% RH, clearing the threshold for fresh-meat exports. ORMOCER coatings on 25 µm BOPP cut oxygen permeation by 95%, offering mono-material solutions that meet curbside-recycling guidelines in the United States and Europe.[2]MDPI, “Alternative Oxygen Barrier Coatings for Flexible PP Films,” mdpi.com These combined advances keep barrier formats at the focal point of technology upgrades inside the Mexico plastic packaging films market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent single-use plastic regulations and taxes | -0.8% | Urban areas nationwide | Short term (≤2 years) |

| Petrochemical feedstock price volatility | -0.6% | Manufacturing-intensive regions | Medium term (2–4 years) |

| Shortage of high-quality recycled resin | -0.4% | Recycling-dependent clusters | Medium term (2–4 years) |

| Supply disruption of specialty additives | -0.3% | Import-dependent processors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Single-Use Plastic Regulations and Taxes

Plan México imposes a 20% single-use plastic reduction by 2030, while Mexico City’s ban triggered 70,000 fines since 2021 and expansion into the State of Mexico in 2024. The tax authority levies 5%–50% temporary tariffs on 544 HS codes that include polyethylene and BOPP, inflating landed costs for downgauged commodity film grades. Food-service chains such as Starbucks shifted 28 million units in 2024 from single-use plastics to fiber-based or reusable options, highlighting how regulation reshapes order books across the Mexico plastic packaging films industry.

Petrochemical Feedstock Price Volatility

Braskem Idesa operates at 78% capacity because domestic ethane output hovers near 50% of 2014 levels, forcing spot imports and exposing buyers to a USD 0.08/lb spread in Q1 2025. Plastics Technology recorded a 2.9 cents/lb resin uptick in March 2025 amid unscheduled cracker shutdowns. Forward-thinking converters hedge through recycled-content integration contracts such as Amcor’s offtake agreement for mechanically recycled PE from NOVA Chemicals’ Indiana facility starting H2 2025. These buffering strategies sustain service levels across the Mexico plastic packaging films market despite feedstock turbulence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyethylene Leads While Bio-Based Films Accelerate

Polyethylene held 40.45% of Mexico plastic packaging films market share in 2025 due to its adaptability from bread bags to heavy-duty shipping sacks. Low-density variants cater to bread and produce wrap, linear low-density grades serve stretch-hood and frozen-food pouches, and high-density grades fill detergent pods and agrochemical liners. Three-layer coextrusion with mLLDPE outer skins enables 18 µm collation shrink that resists 25 kg stacking loads, underscoring polyethylene’s role in down-gauged, high-strength formats.

Bio-based films, forecast to grow 9.34% CAGR, combine PLA or sugarcane-derived PE with high-barrier coatings to satisfy Plan México mandates. Accredo’s 100% bio-based stand-up pouch, displayed at Pack Expo 2024, offers ASTM D6400 compostability and passes 95-kPa hermetic seal tests. Royal Society of Chemistry research documents edible coatings’ 6.81% CAGR from 2017-2023, suggesting commercialization pathways for starch-based and chitosan films in single-serve produce packs. Polypropylene and PET remain staples for snack and beverage labels, yet their share edges down as brands trial mono-material PE laminates compatible with mechanical recycling. This diversification reinforces long-term resilience in the Mexico plastic packaging films market.

By End-Use Industry: Food Dominance Meets Healthcare Innovation

Food commanded 54.60% of the Mexico plastic packaging films market size in 2025. Confectionery makers leverage transparent BOPP with cold-seal coatings for high-speed wrapping at 500 packs/min, while meat processors adopt 15-layer coextruded barrier films yielding oxygen transmission below 0.3 cc/m²-day. Dairy processors measure shelf-life gains of seven days when integrating anti-fog additives in mozzarella cheese pouches, illustrating how incremental functionality elevates value per kilogram.

Healthcare and pharmaceuticals exhibit the fastest 8.52% CAGR as Mexico solidifies its role as North America’s secondary supply hub. Evertis’ Evercare PET films incorporate 50% PCR yet pass USP <661> extractables tests, making them viable for blister and syringe applications. TekniPlex Healthcare’s transparent recyclable mid-barrier blister runs on legacy thermoformers without slowing cycle times, reducing capital barriers for generic-drug packers. Personal-care brands demand glossy PE/PE laminates that accept high-definition digital print, while industrial users refurbish protective wrap formats with flame-retardant additives. This mosaic of specifications enlarges opportunity breadth across the Mexico plastic packaging films industry.

By Thickness: Mid-Range Optimization Drives Performance

Films in the 21–40 µm band captured 43.10% of Mexico plastic packaging films market share in 2025 as they deliver the best performance-to-cost ratio for foods, personal care, and household products. Flexible snack pouches at 25 µm withstand 1 m drop tests while cutting resin usage 12% relative to 30 µm predecessors. Three-layer shrink film at 35 µm secures beverage multipacks for cross-dock shipping over 2,000 km, a common route between Monterrey bottling plants and Mexico City warehouses.

Ultra-thin films (≤20 µm) advance at 7.14% CAGR propelled by metallocene catalyst adoption and online gauge-control systems that maintain ±0.5 µm accuracy. Oxygen barrier remains possible at these gauges when EVOH layers reach 3 µm in the core, keeping total thickness low while meeting export regulations. The 41-70 µm band addresses dry-bulk chemicals and pet-food bulk sacks, whereas films over 70 µm protect heavy machinery during marine transport. Thermochromic studies find that color-change response remains stable when film thickness exceeds 60 µm, implying specialized growth pockets at higher gauges. These nuanced thickness strategies sustain balanced demand distribution across the Mexico plastic packaging films market.

By Functionality: Barrier Films Lead Innovation

Barrier films controlled 38.40% of the Mexico plastic packaging films market size in 2025 due to stringent export-quality metrics. Metallized PET delivers light barriers below 0.1% transmittance for premium coffee, while ceramic SiOx coatings on 12 µm PET achieve water-vapor rates under 0.05 g/m²-day. ExxonMobil’s all-PE barrier pouch maintains 97% polyethylene content and still reaches oxygen transmission below 0.5 cc/m²-day, proving compatibility with domestic recycling streams.

Heat-shrink film serves beverage, tissue, and can multipacks, delivering holding strength with 3% post-shrink haze that still allows barcode readability. Twist-wrap film for confectionery introduces anti-static properties to prevent dust attraction on glossy surfaces. The “other functionality” bucket, growing 9.22% CAGR, captures antimicrobial, UV-blocking, and smart-indicator films. Mondi’s FlexStudios initiative shortens concept-to-market cycles to 90 days, helping converters embed these multifunctional properties before competitors replicate them. This continual layering of attributes fortifies value capture within the Mexico plastic packaging films market.

Geography Analysis

Northern states bordering the United States absorb nearly 47.60% of the Mexico plastic packaging films market thanks to maquiladora clusters in Tijuana, Ciudad Juárez, and Reynosa that assemble electronics, medical devices, and automotive parts. Under USMCA de-minimis provisions, these factories ship duty-free goods into the United States, provided packaging meets FDA and ASTM migration limits. Converters co-located in these corridors offer 72-hour turnaround on printed roll-stock, reducing inventory buffers and transit costs.

Central Mexico—anchored by Mexico City, Guadalajara, and Monterrey—accounts for roughly 38.10% of domestic demand due to dense population and rising middle-class purchasing power. ANTAD’s store count climbed to 68,500 in 2025, expanding shelf space that requires eye-catching, shelf-ready pouches and trays. Tetra Pak’s ISCC PLUS-certified operations in Querétaro supply cartons made from recycled polymers, establishing sustainability benchmarks that ripple into flexible packaging procurement. E-commerce warehouses across the Bajío capitalize on access to three tolled highways that cut delivery times to both coasts, underpinning robust film consumption.

Southern and southeastern states such as Chiapas, Oaxaca, and Yucatán represent 14.30% but grow above the national CAGR on the back of agro-export expansion. Tropical produce like mangoes and avocados travels 2,200 km to United States distribution centers, demanding breathable yet moisture-barrier films that sustain freshness beyond 12 days. Edible coatings derived from mango peel and Arabic gum extend grape shelf life by 40% during storage trials, indicating future adoption among local packers. Government-funded agrovoltaic initiatives power cold-storage hubs in indigenous communities, prompting demand for pre-formed produce bags that integrate humidity scavengers. These developments diversify growth drivers across the Mexico plastic packaging films market.

Competitive Landscape

The Mexico plastic packaging films market exhibits fragmented Market. Amcor’s USD 8.43 billion merger with Berry Global delivers 285 kilotons of regional flexible-film capacity and USD 650 million anticipated synergies by fiscal 2028. Novolex’s union with Pactiv Evergreen adds 39,000 SKUs ranging from wrap films to rigid lids, enabling cross-selling into food-service chains in Mexico’s 50 largest cities.

Collaborative R&D shapes competitive edge. ExxonMobil and Hosokawa Alpine co-developed a seven-layer all-PE barrier line that runs at 450 kg/h, yielding pouches that achieve recyclability without compromising optics. Mondi’s FlexStudios allows brand owners to prototype functional films inside 10 weeks, slashing conventional 26-week cycles. Givaudan doubled micro-encapsulation capacity in Querétaro, capturing fragrance film demand for personal care sachets

Circular-economy projects create new alliances. Arca Continental and Coca-Cola invested MXN 56.5 million to recover 380 million PET bottles per year, feeding PetStar-the world’s largest food-grade recycling plant-and ensuring local rPET supply. Amcor’s offtake agreement with NOVA Chemicals secures mechanically recycled PE, helping fulfill its 30% PCR target by 2030. Collectively, these moves reinforce technology depth and sustainability credentials, shaping future procurement choices across the Mexico plastic packaging films market.

Mexico Plastic Packaging Films Industry Leaders

-

FLEX AMERICAS S.A. de C.V.

-

Innovia Films (CCL Industries Inc.)

-

Evertis de México S.

-

Poly Rafia, S.A. De C.V.

-

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its all-stock combination with Berry Global, forming a global flexible-packaging leader with USD 3 billion annual cash-flow potential and USD 650 million synergy target.

- January 2025: Amcor signed a memorandum with NOVA Chemicals to secure mechanically recycled polyethylene from a new Indiana facility for use in its Mexico flexible-film operations.

- October 2024: Klöckner Pentaplast introduced kp FlexiFlow EH 155 R (PE) and kp FlexiFlow PH 255 R (PP) flow-wrap films, each containing more than 93% single-polymer content and cutting package weight by up to 75% .

- May 2024: UFlex commissioned a post-consumer recyclate (PCR) plant at its El Salto site, enabling in-house production of recycled PET and PE resins for flexible film extrusion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Mexico plastic packaging films market as the annual value of converted flexible polymer films, primarily PE, BOPP, CPP, BOPET, and select high-barrier laminates, sold to brand owners or co-packers for primary or secondary packaging of consumer and industrial goods. Converted output includes roll-stock, pre-made pouches, shrink over-wraps, and twist wraps measured at ex-converter prices.

Scope exclusion: bulk film sold for agricultural mulch, greenhouse, construction, geomembrane, or any rigid sheet application is kept outside the baseline.

Segmentation Overview

-

By Type

-

Polypropylene (PP)

- Biaxially Oriented PP (BOPP)

- Cast PP (CPP)

-

Polyethylene (PE)

- Low-Density PE (LDPE)

- Linear Low-Density PE (LLDPE)

- High-Density PE (HDPE)

- Biaxially Oriented PET (BOPET)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

- Ethylene-Vinyl Alcohol (EVOH)

- PETG

- Bio-based Films

- Multilayer Barrier Films

- Other Film Types

-

Polypropylene (PP)

-

By End-Use Industry

-

Food

- Candy and Confectionery

- Frozen Foods

- Fresh Produce

- Dairy Products

- Dry Foods

- Meat, Poultry and Seafood

- Pet Food

- Other Food Products

- Healthcare and Pharmaceuticals

- Personal Care and Home Care

- Industrial Packaging

- Agriculture

- Chemicals

- Other End-Use Industry

-

Food

-

By Thickness

- ≤20 µm

- 21–40 µm

- 41–70 µm

- More than 70 µm

-

By Functionality

- Barrier Films

- Heat-Shrink Films

- Twist-Wrap Films

- Anti-Fog and Anti-Static Films

- Other Functionality

Detailed Research Methodology and Data Validation

Primary Research

We interview senior packaging buyers at food processors in Jalisco, purchasing managers at northern maquiladoras, and executives from flexible-film plants clustered around Toluca. Conversations test resin yield factors, pass-through lags, typical scrap rates, and the practicality of mono-material rollouts, giving us on-ground guardrails that desktop sources cannot provide.

Desk Research

We first map the demand pool through import and domestic shipment series from sources such as INEGI trade statistics, Secretaria de Economia customs dashboards, and Banco de Mexico price bulletins; these reveal volume swings and resin inflation. Data from ANIPAC, CANIFARMA, and the National Retail & Self-Service Chain (ANTAD) help us calibrate food, pharma, and retail unit growth. Company 10-Ks, investor decks, and packaging converters' audited accounts add margin and average-selling-price clues. Select paid databases, D&B Hoovers for converter revenue splits and Dow Jones Factiva for deal pipelines, augment the public trail. The sources listed illustrate our approach; many additional datasets were tapped for validation and clarification.

A second layer extracts regulatory and environmental signals. Government Diario Oficial publications outline recycled-content mandates, while patent filings retrieved via Questel hint at upcoming barrier-film technologies. Press releases from logistics unions highlight e-commerce parcel flows that translate into mailer film demand. This broad sweep ensures that our desk work captures both structural and emerging variables.

Market-Sizing & Forecasting

A top-down build starts with reconstructed film demand by end use derived from production plus net trade, which is then aligned with household consumption, export output, and sachet penetration ratios. We next corroborate totals with selective bottom-up checks: sampled PE/PP film capacity utilization, average converter selling prices, and roll-stock to pouch conversion factors. Key drivers fed into the model include supermarket floor-space additions, frozen-food tonnage, e-commerce parcel counts, resin price indices, and recycled-content adoption curves. A multivariate regression, refreshed annually, links these drivers to film demand, while ARIMA smoothing handles near-term shocks. Where converter disclosures are sparse, we apportion volumes using interview-validated throughput norms.

Data Validation & Update Cycle

Analysts run variance scans against historical elasticities, benchmark outputs to customs line-item trends, and escalate anomalies for senior review. Reports refresh every twelve months; material events such as resin duty changes trigger interim model tweaks. Before publication, one analyst re-checks all live indicators so clients receive the freshest baseline.

Why Our Mexico Plastic Packaging Films Baseline Earns Trust

Published estimates often differ; currency timing, product scope, and conversion stages rarely align across firms. Buyers need to know which figure traces back to verifiable Mexican demand rather than global roll-ups.

Key gap drivers emerge when scopes drift. Some publishers lump non-packaging sheets with stretch film, others quote factory gate production values that overlook import-dependent converters, and a few project forward from 2022 without refreshing retail or maize-starch blend uptake assumptions. By selecting only converted flexible films, updating 2024-based drivers, and applying interview-tested ASPs, Mordor Intelligence minimizes those distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 310.10 million (2025) | Mordor Intelligence | - |

| USD 1,014.6 million (2022) | Regional Consultancy A | Combines non-packaging films and sheets and uses older base year production revenue |

| USD 1.97 billion (2024) | Industry Journal B | Broad "packaging films" tag without thickness or conversion filter; relies on import-value proxies |

Taken together, the comparison shows that our disciplined scope setting, yearly refresh cadence, and dual validation steps deliver a balanced, transparent baseline that decision-makers can reproduce and stress-test with modest data access.

Key Questions Answered in the Report

What is the current size of the Mexico plastic packaging films market?

The Mexico plastic packaging films market size is USD 326.51 million in 2026 and is projected to reach USD 422.53 million by 2031.

Which material holds the largest share in Mexico’s plastic packaging films?

Polyethylene leads with 40.45% of Mexico plastic packaging films market share due to its versatility across food, industrial, and agricultural uses.

Which end-use segment is growing fastest?

Healthcare and pharmaceuticals record the fastest 8.52% CAGR through 2031, driven by expanding domestic drug manufacturing and higher regulatory alignment.

How are regulations influencing film specifications?

Plan México’s 20% single-use plastic reduction target and city-level bans force brands to adopt recycle-ready, compostable, or bio-based films with reduced thickness and higher PCR content.

What role does near-shoring play in market growth?

Near-shoring relocates supply chains closer to U.S. consumers, boosting demand for locally produced high-performance films that meet export standards while cutting transit times.

Page last updated on: