MENA Architectural Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

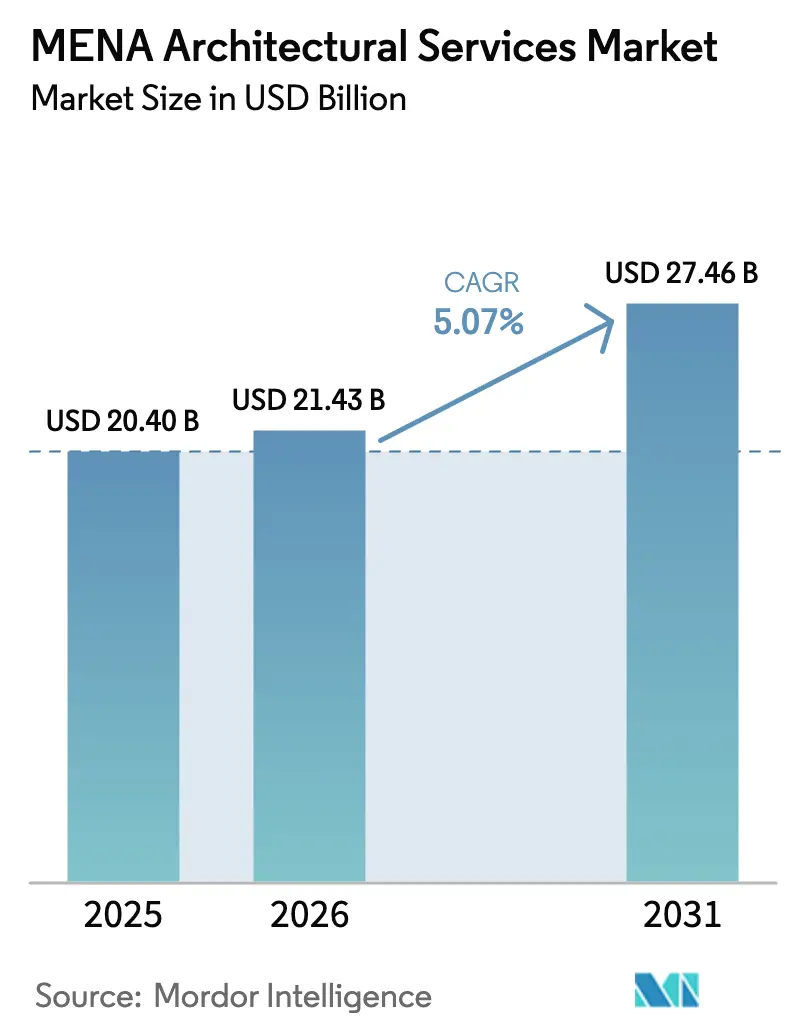

| Base Year Market Size (2025) | USD 20.40 Billion |

| Market Size (2026) | USD 21.43 Billion |

| Market Size (2031) | USD 27.46 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Architectural Services Market Analysis by Mordor Intelligence

MENA architectural services market size in 2026 is estimated at USD 21.43 billion, growing from 2025 value of USD 20.40 billion with 2031 projections showing USD 27.46 billion, growing at 5.07% CAGR over 2026-2031. Robust government spending on giga-projects, mandatory digital-design regulations, and rising demand for green buildings are sustaining this trajectory. Saudi Arabia, buoyed by Vision 2030 and a USD 55 billion annual contracts pipeline, anchors regional expansion, while the United Arab Emirates (UAE) and Qatar contribute scale and pace through aviation, mixed-use, and sports infrastructure programs. Specialized sub-segments such as heritage conservation and BIM consulting are outpacing the wider market as regulators impose digital-twin requirements on cultural assets and historic districts. Strong sovereign-wealth backing for design-build start-ups, plus greater private-sector participation through public-private partnerships, broadens the opportunity pool. Nevertheless, volatile oil prices and construction-cost inflation, especially in Saudi Arabia, where costs are among the world’s fastest rising in 2025, introduce funding and pricing risk.

Key Report Takeaways

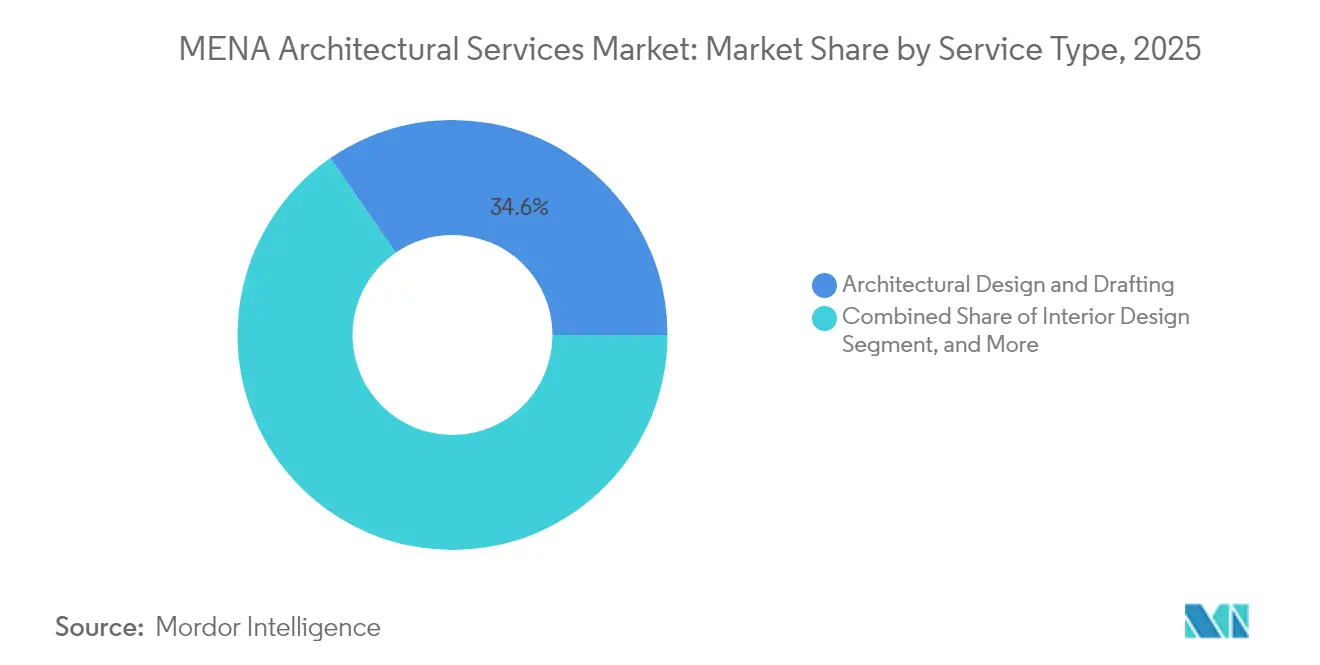

- By service type, architectural design and drafting led with 34.62% of the MENA architectural services market share in 2025; heritage conservation and BIM consulting are projected to expand at a 5.73% CAGR through 2031.

- By end-user sector, commercial projects accounted for 30.78% of the MENA architectural services market size in 2025, while healthcare is forecast to grow at a 5.42% CAGR through 2031.

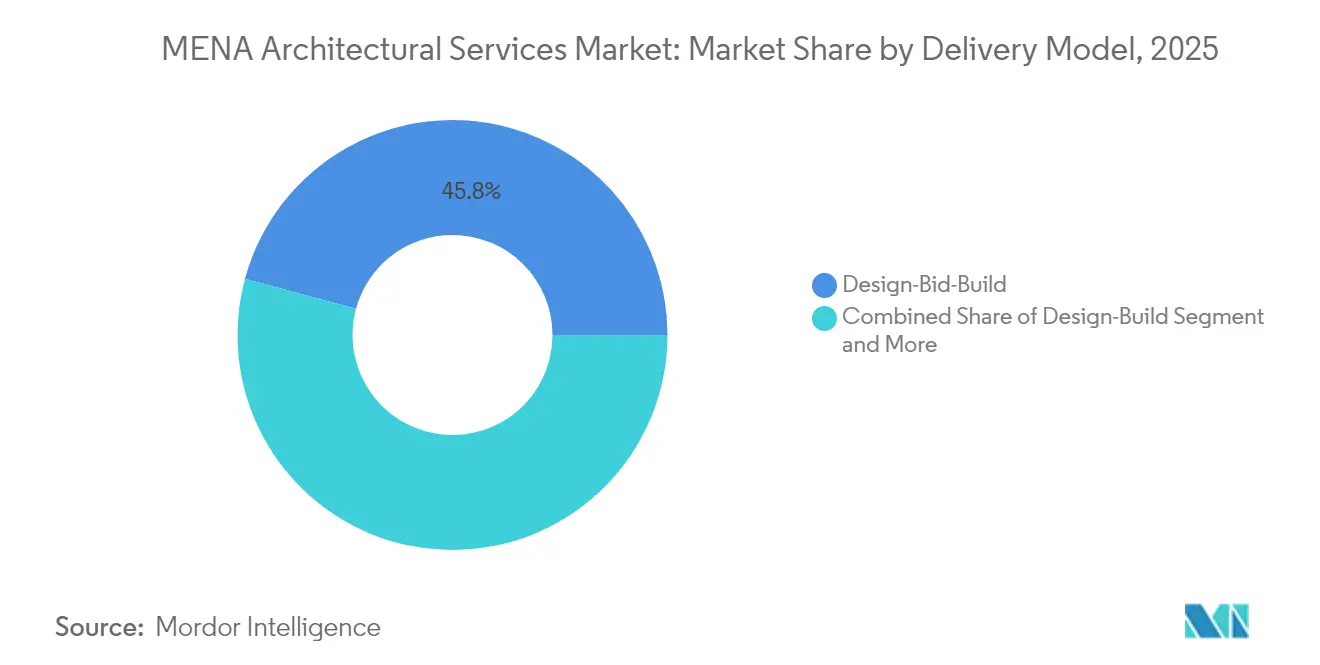

- By delivery model, Design-Bid-Build remained the dominant procurement route in 2025, accounting for 45.78% of the market share, while Integrated Project Delivery is projected to record the fastest growth rate of 5.49% through 2031.

- By geography, Saudi Arabia dominated the MENA architectural services market with a 67.35% share in 2025, whereas Qatar is expected to record the highest 5.32% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MENA Architectural Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led Giga Projects Pipeline | +2.1% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Rising Demand for Sustainable and Green Buildings | +1.8% | Global, with UAE and Saudi Arabia leading | Long term (≥ 4 years) |

| Rapid Urbanization and Population Growth | +1.5% | Egypt, Morocco, Algeria, Jordan | Long term (≥ 4 years) |

| Mandatory BIM Adoption Across GCC | +1.2% | GCC core, spill-over to Egypt and Jordan | Short term (≤ 2 years) |

| Cultural Heritage Restoration Investments | +0.9% | Saudi Arabia, Egypt, Morocco | Medium term (2-4 years) |

| Sovereign Wealth Funds Backing Design-Build Start-ups | +0.7% | GCC states, particularly UAE and Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Giga Projects Pipeline

The region’s USD 3.7 trillion construction pipeline is the single largest demand engine for the MENA architectural services market.[1]AECOM, “Middle East Property & Construction Handbook 2024,” aecom.com Saudi Arabia’s USD 500 billion NEOM program alone has reshaped service requirements, with Bechtel and Parsons managing the new King Salman International Airport that targets 120 million passengers a year.[2]Engineering News-Record staff, “Saudi Arabia Selects Bechtel, Parsons for Mega-Airport Project,” enr.com Project scope adjustments, such as reducing The Line’s initial scale to 2.4 kilometers by 2030, have not curbed the need for complex urban-planning, landscape, and integrated-delivery expertise. Parallel mega-airports in Dubai and Doha extend opportunities across aviation-terminal architecture. These multibillion-dollar undertakings elevate risk-management, digital-coordination, and sustainability skills from optional to essential as governments mandate transparent cost and schedule controls. International firms that embed local joint-venture structures and digital-twin workflows are best positioned to secure repeat commissions.

Rising Demand for Sustainable and Green Buildings

Green-building codes are maturing quickly, compelling the MENA architectural services market to integrate lifecycle energy modeling and low-carbon materials into the baseline scope. The UAE’s Estidama, Dubai Green Building Regulations, and LEED uptake, covering 5,255 regional projects totaling 1.5 billion ft², set a regional benchmark.[3]Green Business Certification Inc., “GBCI MENA,” gbci.org Saudi Arabia’s Mostadam rating system, optimized for local climate, is gaining traction as a culturally resonant alternative to LEED.[4]IOP Publishing, “Mostadam vs LEED: Market Transformation Toward Sustainability in Saudi Arabia,” iopscience.iop.org Market surveys show only 11% of firms currently deliver portfolios exceeding 60% green projects, yet that share is expected to rise to 26% by 2024 as clients seek demonstrable energy savings. Flagship projects such as Dubai’s LEED-Platinum DEWA Solar Innovation Centre highlight the commercial viability of high-performance architecture. Firms able to provide cradle-to-grave carbon accounting and secure third-party certifications command premium fees and deepen client stickiness.

Rapid Urbanization and Population Growth

North Africa’s youthful population is intensifying demand for housing, healthcare, and education, translating into a resilient backlog for the MENA architectural services market. Egypt is adding an entire New Administrative Capital, featuring what would become the world’s tallest 1,000-meter tower, reinforcing the need for skyscraper design, high-speed vertical transportation, and resilient infrastructure. Morocco’s 115,000-seat Grand Stade Hassan II and Algeria’s USD 3 billion desalination program illustrate the breadth of opportunities, from stadiums to industrial utilities. Egypt alone must add 38,000 hospital beds by 2030, worth USD 8-13 billion, stretching local design capacity. Governments are therefore commissioning mixed-use master plans that compress health, education, and residential functions into single districts, elevating demand for multidisciplinary architectural teams.

Mandatory BIM Adoption Across GCC

Dubai Municipality broadened its BIM mandate in 2024 to all public projects, towers exceeding 20 floors, and buildings larger than 200,000 ft², accelerating digital-delivery uptake in the MENA architectural services market. Yet only 25% of regional firms use BIM at scale, constrained by skills shortages and software costs. Saudi Arabia lacks a binding BIM decree, but large developers now embed BIM deliverables in tenders, nudging the market toward rapid adoption. Clients increasingly demand Level 2 BIM or higher, forcing consultancies to invest in training and platform interoperability. Firms offering turnkey BIM consulting and onsite upskilling secure a first-mover advantage as regulators and owners converge on digital-twin standards to cut rework and improve asset performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Talent Shortage in High-Performance Design | -1.4% | Global, acute in GCC and North Africa | Short term (≤ 2 years) |

| Volatile Oil Prices Impacting Public Construction Spend | -1.1% | GCC core, secondary effects in Egypt and Jordan | Medium term (2-4 years) |

| Localisation Quotas Limiting Foreign Firms | -0.8% | Saudi Arabia, UAE, with spillover effects | Long term (≥ 4 years) |

| IP Ownership Disputes in Integrated Contracts | -0.5% | Regional, particularly affecting international firms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Talent Shortage in High-Performance Design

A persistent scarcity of qualified architects, BIM coordinators, and sustainability specialists is constraining delivery schedules across the MENA architectural services market. In the UAE, 93% of engineering employers report hiring difficulties, with 58% of large firms stating that candidates lack the requisite technical depth. Saudi Arabia’s USD 1.68 trillion project pipeline intensifies competition; firms like KEO International doubled headcount to 2,600 in 2024 to keep pace with Vision 2030 demand. The skills gap widens as clients request AI-enabled design optimization and advanced computational workflows. International practices are therefore partnering with universities and running in-house academies focused on BIM, sustainability, and heritage digitization. Governments are bolstering localization programs, for example, the UAE Centennial Plan 2071, to cultivate domestic expertise, but these initiatives will take years to translate into an expanded talent pool.

Volatile Oil Prices Impacting Public Construction Spend

Oil-linked fiscal revenues continue to shape budgeting cycles across GCC states, creating funding unpredictability for the MENA architectural services market. Empirical research confirms positive long-run correlations between oil prices and GDP growth in Saudi Arabia, Kuwait, Qatar, and the UAE, translating into cyclical public tender volumes. Lower prices force governments to defer or phase projects, exemplified by NEOM’s population-target revision amid financing pressures. Diversified economies such as the UAE absorb shocks better through tourism, logistics, and finance, but regional contractors still face cash-flow stress when payments slow. To mitigate volatility, owners are employing cost-escalation clauses and mixed-financing models that share price risk between public and private stakeholders. Architectural firms with flexible staffing and geographically diverse portfolios are weathering commodity cycles more effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Transformation Reshapes Traditional Offerings

Architectural design and drafting retained 34.62% of the MENA architectural services market share in 2025, underpinned by a steady stream of mixed-use and infrastructure commissions. Mandatory BIM deliverables, however, are redefining core workflows, pushing firms to shift from 2D documentation toward data-rich digital twins. Engineering services contributed 27.65% revenue as projects like NEOM require multidisciplinary collaboration across civil, structural, and MEP packages. Interior design holds 14.72% fueled by high-end hospitality in Dubai and Riyadh, while urban-planning and landscape work is advancing at a 5.51% CAGR, driven by green corridor mandates within giga-projects.

Heritage conservation and BIM consulting, although niche, is projected to expand at a 5.73% CAGR through 2031, outpacing overall MENA architectural services market growth. Digitization of historic Cairo using HBIM exemplifies the emerging blend of laser scanning, point-cloud modeling, and virtual-reality storytelling. Firms offering AI-driven design optimization capture premium fees as clients pursue carbon-intensity reductions and accelerated approvals. The evolving regulatory landscape, including Saudi Arabia’s Mostadam and Dubai’s Emirates Green Building Council benchmarks, requires advisory expertise on certification pathways. Consequently, the MENA architectural services market size attributable to advisory and consultancy is poised to widen as owners seek end-to-end strategic guidance alongside traditional blueprints.

By End-User Sector: Healthcare Emerges as Growth Leader

Commercial real estate dominated demand with 30.78% of the MENA architectural services market size in 2025, led by office, retail, and hospitality investments designed to diversify economies beyond hydrocarbons. The residential segment remained resilient at 25.16% in 2025, buoyed by demographic and urbanization pressures, particularly in Egypt and Morocco. Institutional and public projects represented 28.22% in 2025, capturing education campuses, government headquarters, and cultural centers, including Saudi Arabia’s New Murabba district.

Healthcare is the fastest rising vertical, projected to grow at a 5.42% CAGR through 2031, elevating its contribution within the MENA architectural services market. Egypt’s mandate for 38,000 additional beds necessitates tertiary hospitals, outpatient clinics, and telemedicine hubs costing up to USD 13 billion. Flagships such as Dubai’s Hamdan Bin Rashid Cancer Hospital, designed to LEED Gold and WELL Building standards, illustrate the pivot toward patient-centric, technology-enabled care environments. Private operators like Burjeel Holdings posted AED 2.4 billion in revenue in H1 2024, underscoring private-sector appetite for specialized oncology, fertility, and rehabilitation centers. This momentum prompts architects to integrate AI diagnostics suites, sterile logistics robotics, and adaptable ICU pods, aligning design thinking with next-generation clinical workflows.

By Delivery Model: Integrated Approaches Gain Traction

Design-Bid-Build remains the workhorse procurement route across the MENA architectural services market, particularly for government ministries familiar with sequential tendering. Yet complex giga-projects are accelerating adoption of Integrated Project Delivery (IPD), which is forecast to post a 5.49% CAGR to 2031. IPD encourages concurrent engineering, risk-sharing contracts, and early contractor involvement, critical for compressed timelines set by Vision 2030 and Expo-driven milestones. Public-Private Partnerships (PPP) are gathering scale; GCC countries together have USD 2.5 trillion of planned PSP projects, with Saudi Arabia courting private capital through revamped concession laws.

Design-Build is gaining favor for rail and airport terminals because single-point accountability shortens delivery schedules, though regional familiarity remains nascent compared to EPC frameworks that are dominant in oil and gas. Jordan’s 42-project PPP pipeline, largely in water and energy, demonstrates how smaller economies leverage private equity to bridge fiscal gaps, though pandemic-induced traffic declines forced renegotiations at Queen Alia airport. The MENA architectural services industry, therefore, must master multi-contract governance, advanced cost-control algorithms, and integrated scheduling to thrive under diversified delivery models that reward collaboration and data transparency.

Geography Analysis

Saudi Arabia captured 67.35% of the MENA architectural services market in 2025 as Vision 2030 sustained aggressive capital outlays despite cost inflation pressures. The Kingdom’s portfolio spans the cuboid Mukaab landmark, multiple logistics zones, and airport expansions, reinforcing a pipeline that requires vast design resources but also faces rising material and labor costs among the fastest globally in 2025. Mandatory localization rules, including regional-headquarters incentives, are reshaping competition as foreign firms establish permanent Saudi entities to bid for public work.

The UAE, Dubai, offers cost-competitive construction compared to Riyadh and Doha, and Abu Dhabi is pursuing carbon-positive urbanism exemplified by Masdar City’s Innovation Hub that sources 60% renewable energy. Mandatory BIM, multi-certification green codes, and a pro-investment legal framework attract global studios that use the Emirates as a regional springboard. Qatar, though smaller, is projected to be the fastest-growing geography at 5.32% CAGR to 2031 on the back of post-World-Cup economic diversification and additional LNG infrastructure.

North Africa contributes diversity and scale. Egypt holds a 10.21% regional share in 2025, anchored by the New Administrative Capital and healthcare mega-projects. Morocco’s 2030 FIFA World Cup preparations, including the 115,000-seat Grand Stade Hassan II, keep sports architecture in focus, while Algeria’s desalination push demands industrial utility design. Oman shows 5.21% CAGR potential, but BIM adoption remains low, offering space for digital-first consultancies. Region-wide initiatives like BUILD ME, spanning six countries, are introducing climate-neutral building benchmarks and consistent energy-classification systems, widening the addressable sustainability market.

Competitive Landscape

The MENA architectural services market accommodates global giants and agile local specialists in roughly equal measure. AECOM reported USD 15.3 billion global revenue and a USD 55 billion backlog in fiscal 2024, attributing a record share to Middle East design and program-management wins. KEO International achieved 23% overall revenue growth and a remarkable 102% spike in Saudi Arabia by embedding technology centers and regional talent hubs. Digital differentiation shapes bid success: partnerships like AECOM’s alliance with One Click LCA embed embodied-carbon calculators directly into design workflows, a decisive factor as clients chase net-zero targets.

Localization policies are redrawing competitive boundaries. Saudi Arabia’s regional headquarters mandate forces foreign firms to establish substantive on-ground operations or forfeit public contracts, benefiting domestic practices that can scale quickly. Heritage digital-twin specialists are emerging as disruptive niche players; Middle East Architecture Network (MEAN) leverages computational design and 3D printing to merge contemporary forms with vernacular craft, winning museum and pavilion commissions. Meanwhile, multidisciplinary firms strengthen vertical integration: AECOM’s elevator-manufacture joint venture with TK Elevator signals a push into equipment supply chains aligned with Vision 2030 industrialization goals.

Sports, healthcare, and cultural mega-projects drive marquee opportunities. Populous’s Aracmo Stadium concept positions the company for Saudi Arabia’s 2034 World Cup bid, while HKS’s 20,000-seat Diriyah arena illustrates demand for immersive fan experiences grounded in Saudi geology. Contract sizes and durations reward firms that can lock multi-year framework agreements, but rising cost volatility elevates financial-risk thresholds. As a result, the overall market favors well-capitalized players that can absorb payment delays, invest in R&D, and sustain local recruitment programs.

MENA Architectural Services Industry Leaders

AECOM Technology Corporation

KEO International Consultants

AtkinsRéalis Limited

Omrania and Associates

Foster + Partners Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TK Elevator and Alat formed a EUR 160 million joint venture to localize elevator and escalator manufacturing in Saudi Arabia, supporting Vision 2030 industrial goals.

- February 2025: Dubai Municipality and Therme Group unveiled Therme Dubai – Islands in the Sky, a 100-meter-high thermal-wellness destination designed by Diller Scofidio + Renfro.

- November 2024: Burjeel Holdings reported H1 2024 revenue of AED 2.4 billion, citing expanded specialty facilities and Saudi JV primary-care roll-out.

- August 2024: Populous released the Aracmo Stadium concept for Saudi Arabia’s 2034 World Cup candidacy.

MENA Architectural Services Market Report Scope

Architectural services encompass feasibility studies, architectural programming, and project management, including design, preparation of construction documents, and construction administration.

The MENA Architectural Services Market Report is Segmented by Service Type (Architectural Design and Drafting, Interior Design, Engineering Services, Urban Planning and Landscape, Construction and Project Management, Architectural Advisory and Consultancy, Heritage Conservation and BIM Consulting), End-User Sector (Commercial, Institutional and Public, Residential, Healthcare, Industrial, Other Specialized Facilities), Delivery Model (Design-Bid-Build, Design-Build, Integrated Project Delivery, Public-Private Partnership), and Geography (UAE, Saudi Arabia, Qatar, Kuwait, Bahrain, Oman, Egypt, Morocco, Algeria, Jordan, Lebanon). The Market Forecasts are Provided in Terms of Value (USD).

| Architectural Design and Drafting |

| Interior Design |

| Engineering Services |

| Urban Planning and Landscape |

| Construction and Project Management |

| Architectural Advisory and Consultancy |

| Heritage Conservation and BIM Consulting |

| Commercial (Office, Retail, Hospitality) |

| Institutional and Public |

| Residential |

| Healthcare |

| Industrial |

| Other Specialized Facilities |

| Design-Bid-Build |

| Design-Build |

| Integrated Project Delivery (IPD) |

| Public-Private Partnership (PPP) |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| Egypt |

| Morocco |

| Algeria |

| Jordan |

| Lebanon |

| By Service Type | Architectural Design and Drafting |

| Interior Design | |

| Engineering Services | |

| Urban Planning and Landscape | |

| Construction and Project Management | |

| Architectural Advisory and Consultancy | |

| Heritage Conservation and BIM Consulting | |

| By End-User Sector | Commercial (Office, Retail, Hospitality) |

| Institutional and Public | |

| Residential | |

| Healthcare | |

| Industrial | |

| Other Specialized Facilities | |

| By Delivery Model | Design-Bid-Build |

| Design-Build | |

| Integrated Project Delivery (IPD) | |

| Public-Private Partnership (PPP) | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Egypt | |

| Morocco | |

| Algeria | |

| Jordan | |

| Lebanon |

Key Questions Answered in the Report

What is the current value of the MENA architectural services market in 2026?

The market is expected to reach USD 21.43 billion in 2026 and is forecast to reach USD 27.46 billion by 2031.

What are the key challenges facing architects in the region?

Skills shortages in BIM, sustainability, and heritage conservation, coupled with oil-price-linked funding volatility, are the primary headwinds.

Which end-user sector is expanding fastest in regional design demand through 2031?

Healthcare leads with an 5.42% CAGR outlook through 2031, fueled by hospital and clinic investments across Egypt, the UAE, and Saudi Arabia.

How is digital transformation influencing architectural practice in MENA?

Mandatory BIM mandates across the GCC and growing AI adoption are pushing firms toward data-rich digital-twin workflows and integrated project delivery.

Page last updated on: