Melt Blown Polypropylene Filters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

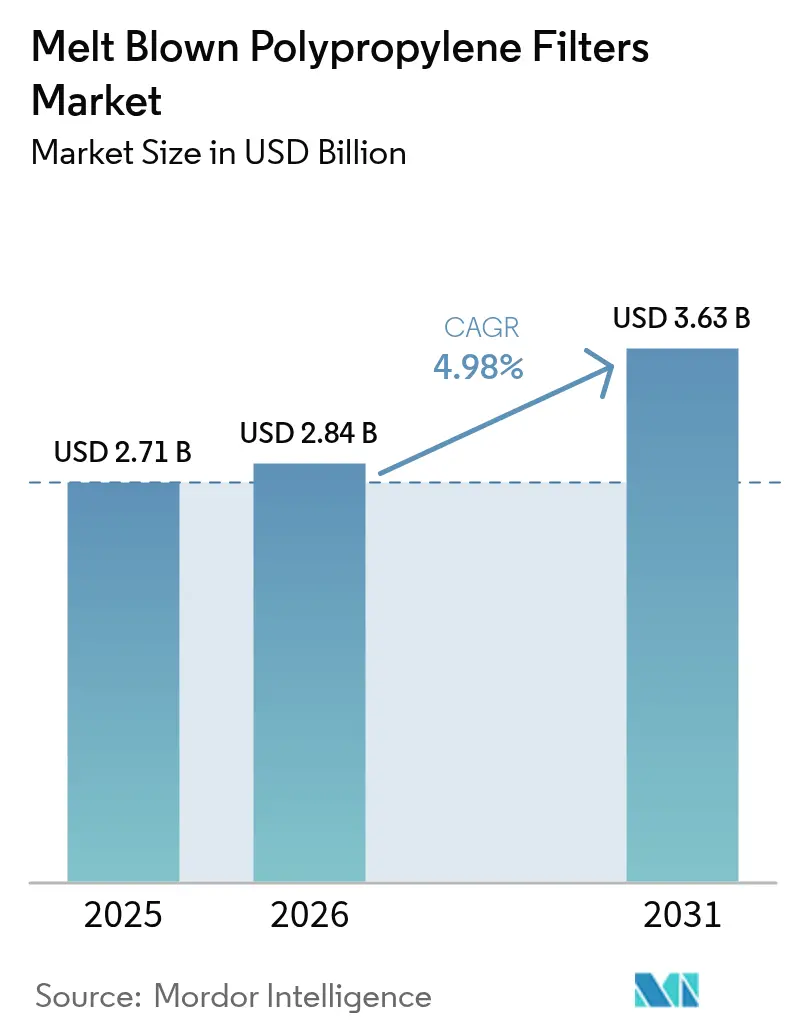

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Melt Blown Polypropylene Filters Market Analysis by Mordor Intelligence

Melt Blown Polypropylene Filters market size in 2026 is estimated at USD 2.84 billion, growing from 2025 value of USD 2.71 billion with 2031 projections showing USD 3.63 billion, growing at 4.98% CAGR over 2026-2031. Growth rests on rising demand for high-purity water, tougher food-grade rules, and accelerating investments in desalination and industrial wastewater reuse worldwide. Polypropylene’s chemical resistance, thermal stability, and cost advantage keep it the dominant media across critical liquid and air systems approved for food, beverage, pharmaceutical, and semiconductor processes[1]U.S. Food and Drug Administration, “Food Contact Substance Inventory,” fda.gov. Asia-Pacific anchors both demand and capacity expansion, underpinned by large municipal projects, rapid factory build-outs, and focused technology upgrades that drive uptake of advanced filtration cartridges and high-flow pleated elements.

Key Report Takeaways

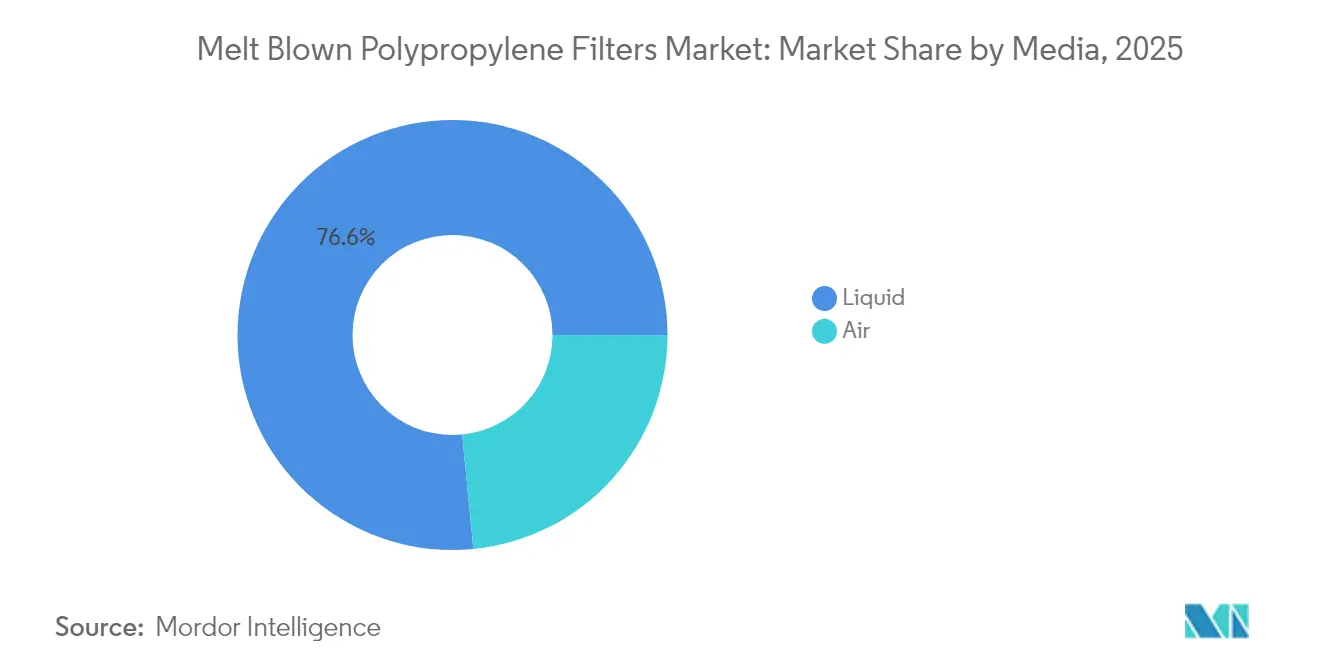

- By media, liquid filtration led with 76.55% revenue share in 2025; air filtration is projected to expand at a 6.85% CAGR through 2031.

- By product configuration, cartridge designs held 62.40% share of the melt-blown polypropylene filters market size in 2025, while high-flow pleated filters are forecast to grow at 6.31% CAGR to 2031.

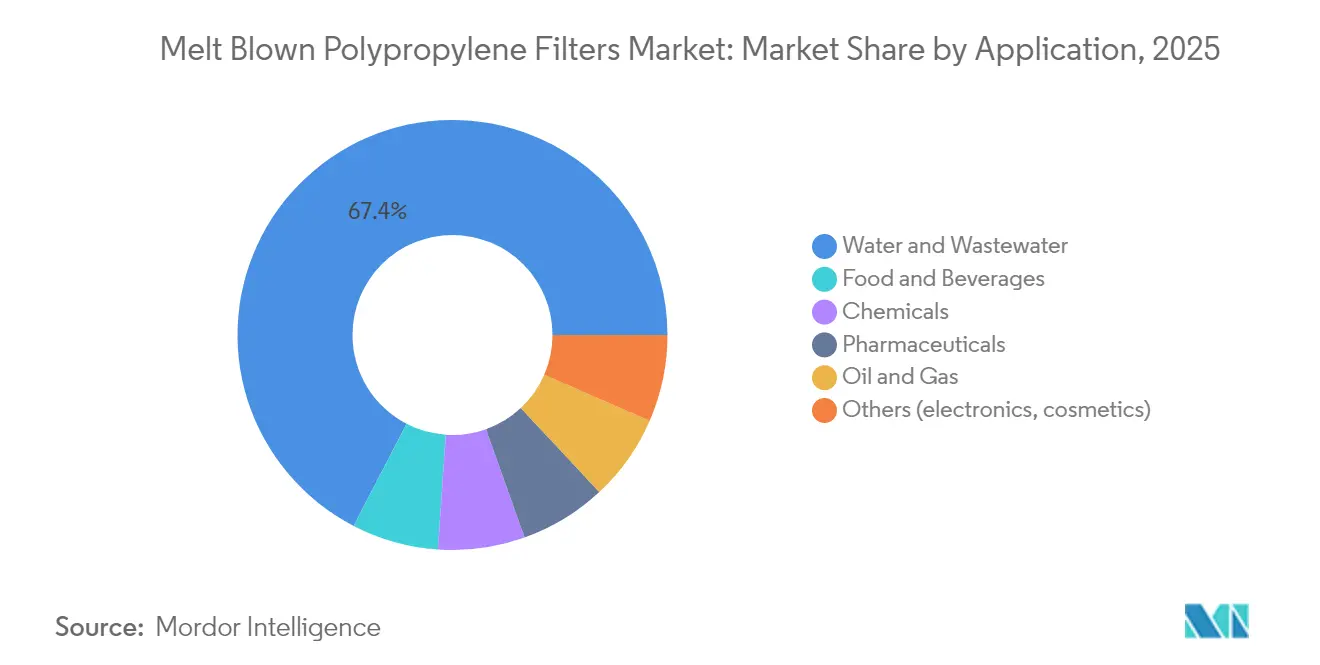

- By application, water and wastewater treatment accounted for 67.40% share of the melt-blown polypropylene filters market size in 2025; pharmaceuticals are expected to advance at a 5.99% CAGR through 2031.

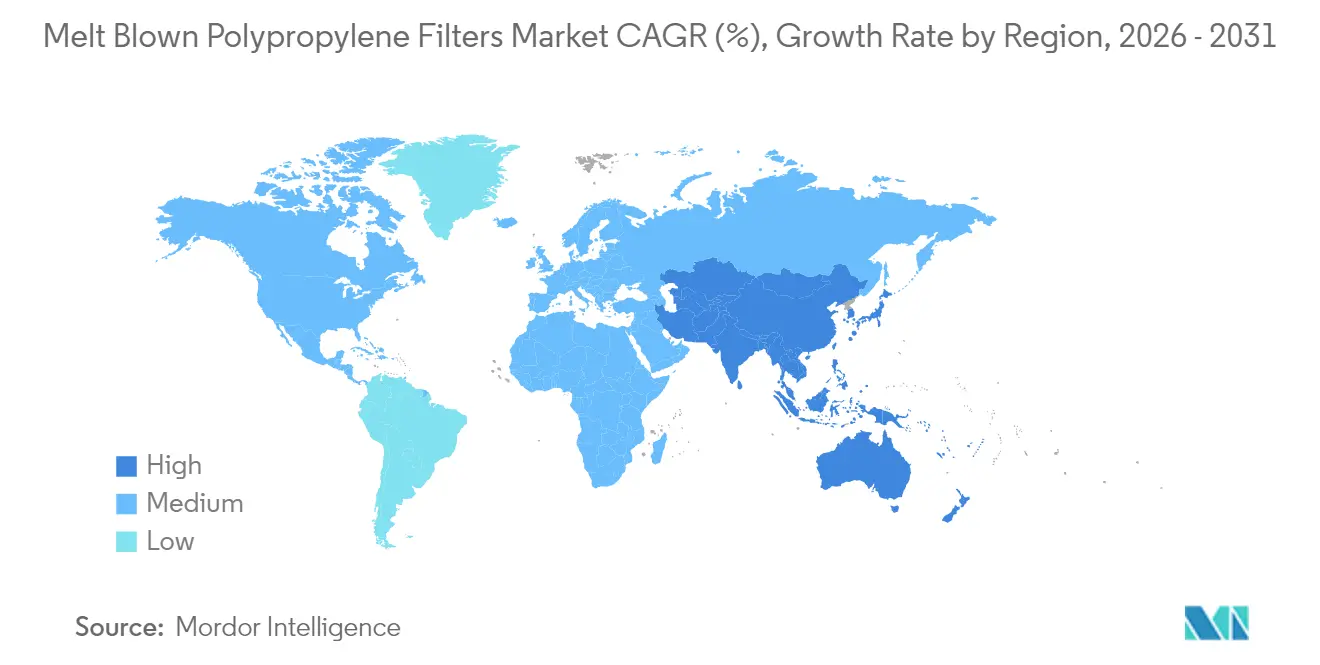

- By geography, Asia-Pacific commanded a 35.28% share in 2025 and is anticipated to deliver the fastest regional CAGR of 6.92% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Melt Blown Polypropylene Filters Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high-purity water treatment solutions | + 1.8% | Global, with a concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Stringent food-grade filtration regulations | + 1.2% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rapid capacity build-out of desalination plants | + 1.0% | Middle East and Africa, Asia-Pacific coastal regions | Medium term (2-4 years) |

| Increasing demand for food and beverage sector | + 0.8% | Global, with emphasis on developed markets | Short term (≤ 2 years) |

| Increasing usage in healthcare and pharmaceuticals | + 0.7% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Purity Water Treatment Solutions

Industrial and municipal operators are retrofitting plants with smart membrane trains that rely on melt-blown polypropylene prefilters to guard costly reverse-osmosis elements from particle overload. Artificial-intelligence-assisted membrane bioreactors extend service life and cut chemical cleaning cycles, prompting procurement teams to specify polypropylene media capable of withstanding repeated back-flush sequences. Bioinspired capillary filters, which imitate mucus-layer capture in nature, are being prototyped to boost efficiency in pretreatment skids[2]Nature, “Bioinspired Capillary Filtration,” nature.com. Ever-stricter discharge permits and corporate water-positive pledges keep demand robust in electronics, food, and chemicals plants, ensuring the melt-blown polypropylene filters market enjoys repeat sales for replacement cartridges. In regions facing water scarcity, polypropylene filters help utilities achieve potable-reuse targets by delivering consistent turbidity, SDI, and bacterial log-reduction performance.

Stringent Food-Grade Filtration Regulations

Europe’s Packaging and Packaging Waste Regulation requires proof of recycled content and non-migration for polypropylene filters used in filling lines, accelerating audits of melt-blown production facilities. Major beverage brands stipulate NSF/ANSI 61 clearance and BSE-TSE statements, narrowing the approved vendor list and favoring companies with robust compliance infrastructure. Pharmaceutical guidelines mandate 0.2-micron final filtration ahead of filling, expanding the addressable market for non-fiber-releasing polypropylene media tailored to withstand gamma sterilization. Sustainability goals pushing for food-grade recycled polypropylene create scope for advanced solvent-based purification processes, such as those pioneered by PureCycle, to supply virgin-like resin streams.

Rapid Capacity Build-Out of Desalination Plants

Coastal nations are scaling reverse-osmosis desalination by pairing photovoltaic arrays with modular plants, driving steady demand for polypropylene depth filters that pre-condition seawater laden with silt and biofouling agents. Pretreatment integrity safeguards thin-film composite membranes, whose replacement cost can be 30–40% of total plant capex, making melt-blown cartridges an economical insurance. Operators prioritizing energy efficiency deploy high-surface-area filters to cut differential pressure and pump load, extending membrane runs between chemical cleans. Advanced oxidation and constructed wetlands are now integrated upstream but still rely on polypropylene cartridges to screen colloidal carryover. As decentralised containerised units are shipped to remote islands, demand shifts toward compact, easy-to-dispose cartridges, further expanding the melt-blown polypropylene filters market in off-grid applications.

Increasing Usage in Healthcare and Pharmaceuticals

Asahi Kasei’s Planova FG1, whose upstream depth prefilters are melt-blown polypropylene chosen for low extractables. FDA reclassification of breathing-circuit bacterial filters as Class II devices compels respiratory manufacturers to procure certified polypropylene media tested for particle shedding and airflow resistance. Electrostatic-assist melt-blown technology now creates sub-micron fibers that raise bacterial retention without boosting pressure drop, delivering processing economies for vaccine plants. Continuous-processing bioreactors require single-use capsule filters with polypropylene depth layers that streamline changeouts, expanding aftermarket cartridge demand. Projected bioprocess capacity expansions across North America, Europe, and Singapore reinforce the melt-blown polypropylene filters market outlook in sterile applications.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in polypropylene resin prices | -1.5% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Competition from pleated high-flow cartridges | -0.8% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| End-of-life sustainability and recycling concerns | -0.5% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polypropylene Resin Prices

Petrochemical firms pursue renewable feedstocks and pyrolysis oil, yet scale-up risks keep quarterly pricing unstable. New propylene capacities, such as LyondellBasell’s 400 kilotonne Channelview project expected in 2028, promise longer-term supply certainty but not short-term relief. Asian oversupply from Chinese refineries further depresses spot prices, compelling cartridge makers to hedge futures and renegotiate annual supply contracts. Price swings impede accurate project costings for municipal bids, delaying procurement schedules and tempering near-term growth in the melt-blown polypropylene filters market.

Competition from Pleated High-Flow Cartridges

High-flow pleated filters, led by Pall’s Ultipleat® platform, deliver up to 115,443 lpm throughput, reducing housing count and changeout labor in large desalination and refinery services. Their coarse-to-fine pleat geometry guarantees collapse resistance at differential pressures where traditional melt-blown cartridges deform. Life-cycle assessments often show 30–50% lower total cost of ownership despite higher unit price, accelerating user conversion. Equipment OEMs design skids around pleated columns, making retrofits easier than before and chipping away at melt-blown polypropylene filters market share. Melt-blown suppliers respond with hybrid depth-pleat constructions, yet the performance gap in flow-rate-per-cartridge remains a competitive hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Media: Liquid Filtration Commands Market Dominance

Liquid applications generated 76.55% of the melt-blown polypropylene filters market share in 2025, reflecting their integral role in safeguarding industrial and municipal water circuits MDPI. Stringent discharge rules, heightened desalination investments, and the proliferation of zero-liquid-discharge plants anchor recurring demand for polypropylene cartridges that capture sand, rust, and organic debris before membrane or ion-exchange stages.

Air filtration, although representing a smaller base, outpaces liquid with a 6.85% CAGR through 2031. Hospitals, cleanrooms, and vaccine fill-finish suites adopt high-efficiency particulate air systems that increasingly deploy polypropylene depth layers as a sacrificial stage ahead of HEPA media. Regulatory calls for indoor-air-quality monitoring in schools and commercial buildings amplify cartridge and panel filter retrofits in ventilation systems.

By Product Configuration: Cartridges Lead Amid Pleated Innovation

Cartridges retained 62.40% of 2025 revenue, supported by decades of installed housings across water, food, and chemical plants worldwide. Procurement familiarity, low upfront cost, and simple disposal give traditional melt-blown designs staying power in skids where flow rates are moderate and changeout frequency is acceptable. The melt-blown polypropylene filters market size attributed to cartridge sales is projected to expand modestly, yet its share will erode as users migrate high-throughput lines toward pleated options that compress footprint and maintenance.

High-flow pleated elements, projected to grow at 6.31% CAGR, are rewriting OPEX models for refineries, offshore platforms, and mega-desalination complexes. Their ability to process six to ten times the flow of a 40-inch depth cartridge cuts housing count, floor space, and differential pressure losses.

By Application: Water Treatment Dominance with Pharmaceutical Upside

Water and wastewater systems delivered 67.40% of 2025 sales, anchored by expanding municipal networks, desalination retrofits, and stricter effluent discharge permits. The melt-blown polypropylene filters market remains fundamental to reverse-osmosis pretreatment, sand-media replacement, and tertiary reuse units. Operators adopt finer-grade polypropylene cartridges to improve silt density index scores and prolong membrane life, translating directly into lower energy consumption and chemical cleanings.

Pharmaceutical lines exhibit the highest CAGR at 5.99% through 2031 as biologics, cell therapies, and vaccine fill-finish operations expand capacity across the United States, Ireland, Germany, and Singapore. The melt-blown polypropylene filters market size serving aseptic processing is set to climb alongside new drug-substance facilities that emphasize closed, single-use bioreactors and rapid-change filtration trains. Food and beverage plants, chemical processors, and oil refineries contribute stable demand, while electronics and cosmetics producers purchase specialty grades that ensure ultrapure rinse and formula clarity.

Geography Analysis

Asia-Pacific contributed 35.28% of global revenue in 2025 and is on track for a 6.92% CAGR, supported by USD trillions in water-infrastructure financing across China, India, Indonesia, and Australia. Indian utilities increasing treatment capacity from USD 11 billion in 2024 to USD 18 billion in 2026 rely on melt-blown cartridges for sediment removal, chlorine de-chlorination, and tertiary reuse, reinforcing aftermarket volume. Chinese industrial parks install closed-loop reuse systems mandated by provincial eco-zones, embedding polypropylene depth filters as consumables. Japan’s WOTA BOX, reclaiming over 98% of wastewater, integrates multi-stage polypropylene filtration in its compact modules, supporting urban resilience during disasters.

North America remains a technology front-runner, led by federal PFAS remediation programs budgeting USD 13.5 billion for treatment retrofits that employ polypropylene prefilters ahead of granular activated carbon beds. Europe focuses on sustainability and circular-economy legislation, influencing both product design and end-of-life management. The EU Packaging and Packaging Waste Regulation pushes recycled-content thresholds, compelling filter manufacturers to qualify feedstock purity through advanced solvent-based regeneration technologies pioneered by PureCycle.

Competitive Landscape

The melt-blown polypropylene filters market shows moderate fragmentation. Technology differentiation has become the key competitive lever. Suppliers market hybrid depth-pleat designs promising 30% higher dirt holding than conventional melt-blown cartridges. Others commercialize low-differential-pressure variants for energy-constrained desalination islands. Innovations also extend to end-of-life services; certain vendors now collect spent cartridges, shred them, and feed the material into chemical-recycling reactors that regenerate polypropylene pellets fit for new filter production. The move aligns with EU eco-design directives and helps buyers meet Scope 3 emission targets.

Melt Blown Polypropylene Filters Industry Leaders

Eaton

Donaldson Company, Inc.

3M

Pall Corporation (Danaher)

Parker-Hannifin Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific announced the acquisition of Solventum's Purification and Filtration business, thus expanding its melt-blown polypropylene filters market.

- February 2024: Amazon Filters Ltd. introduced sustainable melt-blown filters using Borealis’ Bornewables polypropylene derived from renewable feedstocks, targeting water, oil and gas, food, chemical, and pharma applications.

Global Melt Blown Polypropylene Filters Market Report Scope

The Melt Blown Polypropylene Filters Market report includes:

| Air |

| Liquid |

| Cartridge |

| High-flow pleated |

| Capsule |

| Sheet and Roll Media |

| Water and Wastewater |

| Food and Beverages |

| Chemicals |

| Pharmaceuticals |

| Oil and Gas |

| Others (electronics, cosmetics) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Media | Air | |

| Liquid | ||

| By Product Configuration | Cartridge | |

| High-flow pleated | ||

| Capsule | ||

| Sheet and Roll Media | ||

| By Application | Water and Wastewater | |

| Food and Beverages | ||

| Chemicals | ||

| Pharmaceuticals | ||

| Oil and Gas | ||

| Others (electronics, cosmetics) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the melt-blown polypropylene filters market?

The global melt-blown polypropylene filters market is valued at USD 2.84 billion in 2026 and is projected to reach USD 3.63 billion by 2031.

Which region leads demand for melt-blown polypropylene filters?

Asia-Pacific holds the largest share at 35.28% in 2025 and is also the fastest-growing region with a forecast 6.92% CAGR through 2031.

What application segment generates the most revenue?

Water and wastewater treatment dominates, accounting for 67.40% of 2025 revenue, reflecting strict water-quality rules and rising desalination capacity.

Why are pleated high-flow cartridges a competitive threat?

They offer higher flow rates, longer service life, and lower total cost of ownership, capturing share in large-volume applications such as refineries and mega-desalination plants.

Page last updated on: