Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

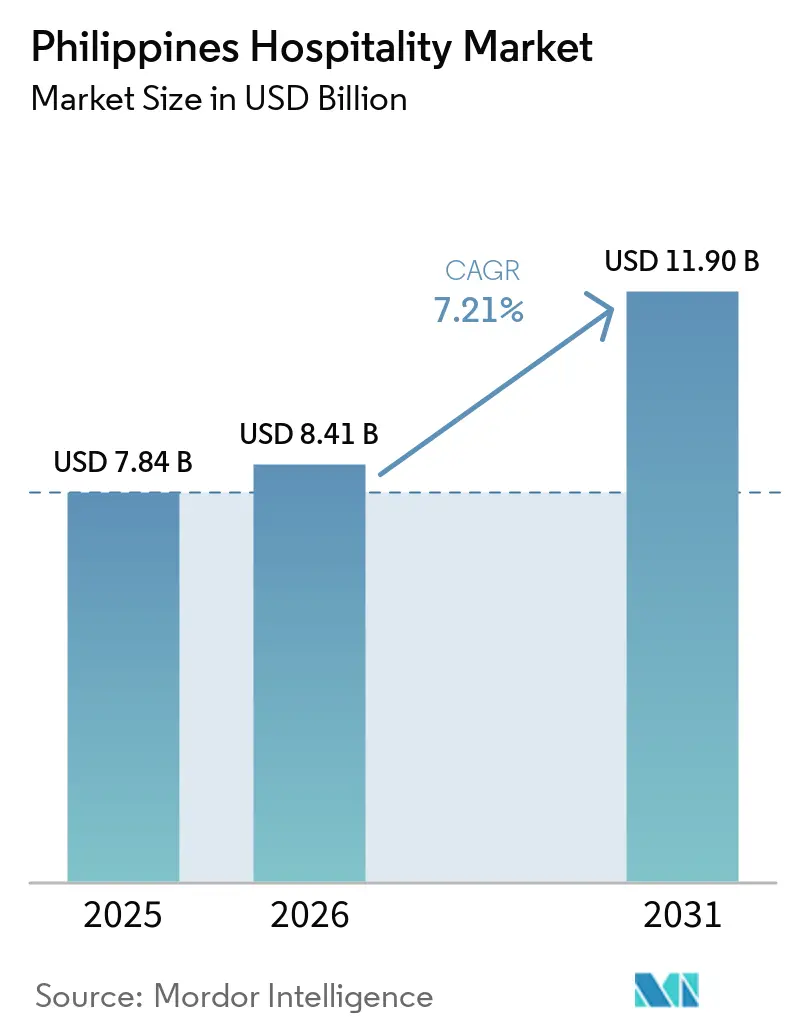

| Base Year Market Size (2025) | USD 7.84 Billion |

| Market Size (2026) | USD 8.41 Billion |

| Market Size (2031) | USD 11.90 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

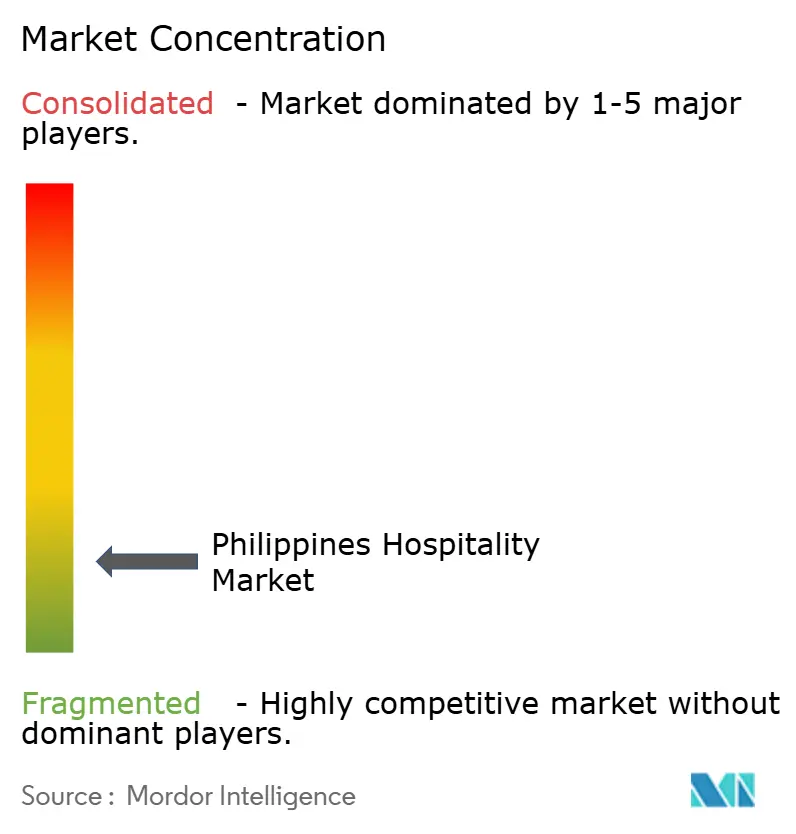

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Hospitality Market Analysis by Mordor Intelligence

The Philippines Hospitality Market size was valued at USD 7.84 billion in 2025 and is estimated to grow from USD 8.41 billion in 2026 to reach USD 11.90 billion by 2031, at a CAGR of 7.21% during the forecast period (2026-2031).

Domestic tourism outlays and international arrivals reinforce this outlook, with internal tourism expenditure surpassing pre-pandemic levels, while tourism direct gross value-added contributed 8.9% to GDP and supported 6.75 million jobs as of Q1 2024. Large-scale infrastructure spending, led by aviation and last-mile road projects, and the record throughput at Manila’s main gateway create new supply and demand corridors that lift occupancy and rate power for both branded and independent operators. Room supply remains short in fast-growing beach and eco-tourism clusters, which supports pricing even as digital direct booking channels rise and reshape distribution costs for operators. The demand mix diversifies as MICE, corporate travel, and eco-adventure segments deepen in regional hubs, though operational risks from natural hazards and labor scarcity require stronger resilience and workforce pipelines to maintain service standards.

Key Report Takeaways

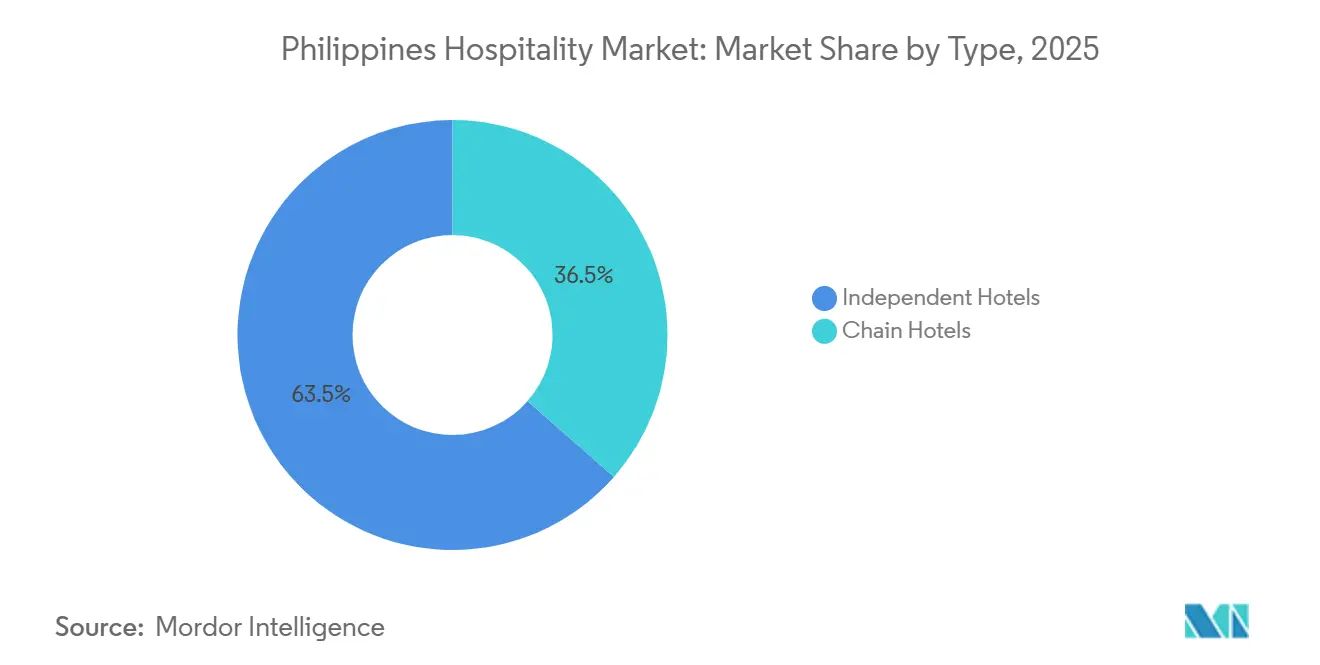

- By type, independent hotels led with 63.52% share of the Philippines hospitality market in 2025, while chain hotels are projected to grow at a 10.12% CAGR through 2031.

- By accommodation type, mid and upper-midscale properties accounted for the largest share at 36.25% of the Philippines hospitality market in 2025, while luxury hotels are forecast to record the fastest growth at a 9.52% CAGR through 2031.

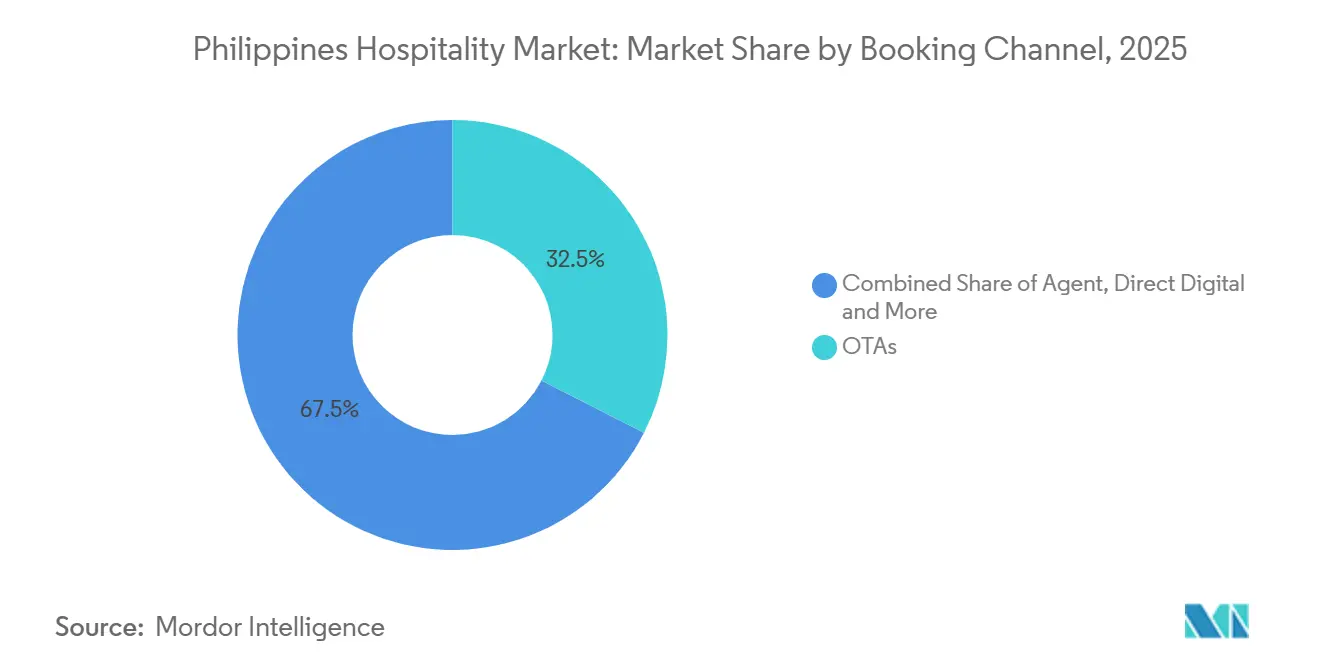

- By booking channel, OTAs held a 32.52% share of the Philippines hospitality market in 2025, while direct digital channels are projected to expand at a 9.31% CAGR through 2031.

- By geography, Western Visayas led with a 38.25% share of the Philippines hospitality market in 2025, while MIMAROPA is expected to register the fastest growth at an 8.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government tourism campaigns & infrastructure investments | +2.3% | National, with concentration in Manila, Cebu, Bohol-Panglao, Palawan, and Siargao | Medium term (2-4 years) |

| Expanded international air connectivity | +1.8% | National gateway, spill-over to Western Visayas, Central Visayas, MIMAROPA | Short term (≤ 2 years) |

| Growth in domestic travel demand | +1.5% | National, early gains in Western Visayas, Central Visayas, MIMAROPA | Short term (≤ 2 years) |

| Surge in MICE and business travel | +0.9% | NCR core, secondary hubs in Clark and Cebu | Medium term (2-4 years) |

| Rising interest in eco- and adventure tourism | +0.5% | MIMAROPA, Caraga, Western Visayas, Central Visayas | Long term (≥ 4 years) |

| Visa facilitation and tax-refund programs | +0.2% | National, immediate effects in Manila, Cebu, and Clark | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Tourism Campaigns and Infrastructure Investments

The government’s USD 26.5 billion (PHP 1.56 trillion) infrastructure outlay in 2026, including USD 3.35 billion (PHP 197.3 billion) for the transport department, strengthens aviation gateways and regional links that directly support hotel demand in tier-1 and tier-2 destinations[1]Source: Development Budget Coordination Committee, “2026 Budget Parameters and Infrastructure Allocations,” DBCC, dbm.gov.ph. The New NAIA Infra Corp concession, valued at USD 2.9 billion (PHP 170.6 billion), grows capacity for Manila’s main gateway to 62 million passengers annually and processed a record 52.02 million passengers in 2025, improving throughput for inbound and domestic travelers. Flagship projects like the Panay-Guimaras-Negros Bridge at USD 3.32 billion, and the Samal Island-Davao City Connector Bridge at USD 0.41 billion, cut inter-island travel times and unlock resort zones for development and scaling. Road works under the Tourism Road Infrastructure Program reached 882.281 km by mid-2024, improving last-mile access to eco and heritage attractions with measurable benefits for provincial hotel occupancy[2]Source: Department of Tourism, “Tourism Road Infrastructure Program Updates,” Department of Tourism, tourism.gov.ph. Navigation and air-traffic upgrades at NAIA, Kalibo, and Laoag further improve reliability, which supports itinerary planning and enhances traveler confidence during peak seasons. These coordinated investments lower friction in an archipelago setting, which drives higher average length of stay and broader dispersion of visitors beyond Metro Manila.

Expanded International Air Connectivity

Passenger volumes rose at both gateway and regional airports due to operational improvements and private capital in aviation assets that widen the funnel to leisure islands and business hubs. Manila’s concession program generated USD 1 billion in remittances in its first year and backed terminal upgrades that improve on-time performance and throughput during peak holidays. Arrivals data show 15.6 million total arrivals in 2025, including 6.7 million foreign travelers, which reinforces long-haul and regional connectivity across core markets[3]Bureau of Immigration, “Arrivals and E-gates Updates,” Bureau of Immigration, immigration.gov.ph. Capacity builds include the expansion of Bohol-Panglao International Airport, which improves access to prime dive and beach circuits in Central Visayas. The Bulacan greenfield gateway backed by long-term financing will decongest Manila’s airspace and provide redundancy that benefits airlines and hotel operators as routes scale. Parallel airport projects in Palawan and Siargao under the flagship pipeline position eco destinations to absorb demand, which helps diversify the hospitality industry in the Philippines across islands.

Growth in Domestic Travel Demand

Domestic tourism expenditure reached USD 53.7 billion (PHP 3.16 trillion) in 2024, signaling a complete recovery relative to 2019 and supporting higher base occupancy across city and resort markets. Regional performance confirms the structural rebound, as Western Visayas and Central Visayas recorded strong arrivals and receipts with Cebu and Panglao as anchors for urban and beach itineraries. MIMAROPA’s 2024 arrival and room-capacity gains reflect the appeal of Palawan’s eco attractions, while uneven infrastructure creates opportunities for targeted investment that can extend average stay and spend. Caraga’s acceleration highlights the rising importance of surf, dive, and adventure segments that align with Filipino travel preferences and multi-stop domestic trips. Operators adjust pricing and packages to longer booking windows and family groups, while digital payments improve conversion and last-minute travel execution. These factors broaden the hospitality industry in the Philippines by stabilizing shoulder-season demand and raising utilization outside international peak periods.

Surge in MICE and Business Travel

MICE revenue targets point to stepped-up promotion and venue capacity, with the sector aiming to grow its base through a pipeline of upgraded convention centers and integrated resorts. Business travel’s gradual normalization is evident in official arrival statistics, though large group movements depend on consistent visa processing and airline schedules. The planned Clark convention complex and SM Prime’s expansion of SMX venues add floor space and modern facilities that support recurring events and corporate bookings. Convention hotels in NCR and Cebu capture occupancy premiums during peak corporate quarters due to room-blocked events and spillover demand from adjacent trade and entertainment precincts. Provincial cities such as Iloilo and Bacolod also benefit from upgraded hotel stock and regional road links, which help spread the MICE calendar beyond Metro Manila. These developments raise midweek utilization and stabilize average daily rates for participants in the Philippines hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High vulnerability to natural disasters | -0.5% | National, severe in Eastern Visayas, Bicol, Northern Luzon, and Caraga | Long term (≥ 4 years) |

| Insufficient infrastructure in secondary destinations | -0.3% | MIMAROPA, Caraga, Northern Mindanao, and smaller islands | Medium term (2-4 years) |

| Skilled labor shortages in hospitality | -0.2% | National, acute in MIMAROPA, Caraga, Central Visayas | Medium term (2-4 years) |

| Overcrowding and environmental degradation at hotspots | -0.1% | Boracay, El Nido, Coron | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Vulnerability to Natural Disasters

The country experiences frequent tropical cyclones that peak in the July to October window, which creates systemic disruption risks for travel planning and hotel operations in coastal areas. Official damage statistics underscore the economic costs of these events and the need for resilient design in hospitality assets across high-risk provinces. Disaster mitigation and recovery outlays are embedded in national planning, yet event severity and uneven enforcement of building codes can leave property-level vulnerabilities. Operators in island destinations reinforce roofs, foundations, and power systems to protect continuity during adverse weather, which increases development and operating costs relative to inland peers. Temperature and sea-level trends add medium-term risks that factor into site selection and insurance policies for coastal resorts. These conditions require contingency plans and diversified demand bases to stabilize performance in the Philippines hospitality market.

Insufficient Infrastructure in Secondary Destinations

MIMAROPA’s sharp rise in arrivals and room stock has not been matched by uniform development across provinces, which constrains capacity and service quality outside leading municipalities. Select towns lack centralized wastewater systems and reliable utilities, requiring hotels to invest in on-site solutions that increase unit operating expenses. While Puerto Princesa benefits from more frequent flights and visitor services, adjacent municipalities show utility gaps that stall resort pipelines and limit dispersal benefits. The Tourism Road Infrastructure Program continues to add last-mile roads, but emerging destinations expand faster than the pace of enabling infrastructure. Caraga’s arrivals growth tests available rooms and trained staff, highlighting the need for coordinated investment to match demand with adequate supply. New airports in Palawan aim to reduce travel time and spur integrated resort zones, but commissioning timelines extend into the outer years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Hotels Capture Growth While Independents Hold Market

Independent hotels command 63.52% of the Philippines hospitality market share in 2025, while chain hotels are projected to grow at a 10.12% CAGR through 2031 as brand penetration and institutional capital increase. The consolidation strategy of large groups accelerates momentum, with SM Hotels forming a multi-property partnership with Radisson for new flags as part of its expansion cycle. Robinsons Hotels’ opening of the ultra-luxury NUSTAR Hotel in Cebu in 2025 adds 223 rooms and scales a portfolio that already spans dozens of properties in key cities[4]Source: Robinsons Land Corporation, “H1 2025 Report,” Robinsons Land, robinsonsland.com. Centralized revenue management and loyalty platforms allow chains to outperform on distribution and repeat stays, creating advantages in corporate and high-season leisure segments in the Philippines hospitality market. Independents remain competitive where authentic experiences and bespoke service differentiate, including eco and heritage assets that are less suited to standardized brand norms.

Chain operators leverage asset-light growth via management and franchise models that speed entry into provincial capitals and resort corridors without heavy balance-sheet risk. Megaworld’s 8,500-room footprint and the 1,530-room Grand Westside Hotel demonstrate scale at a time when large properties capture MICE and integrated-resort demand. Sustainability certifications such as IFC EDGE Zero Carbon at Ayala Land Hotels lower utility costs and align with corporate procurement criteria for business travel. Independent hotels often face succession and professionalization challenges that create selective acquisition opportunities for chains and investors attentive to culture and property DNA in the Philippines hospitality industry. The interplay between brand scale and local authenticity will define competitive positioning as supply grows against improving connectivity.

By Accommodation Type: Luxury Surges as Midscale Anchors Demand

Mid and upper-midscale hotels held the largest segment at 36.25% in 2025, while luxury properties are projected to grow fastest at a 9.52% CAGR as high-net-worth travelers and MICE delegates increase their share of nights and spend. Integrated-resort operators report strong occupancy from premium gaming and entertainment patrons, which raises pricing power for adjacent luxury and upper-upscale inventory in the Philippines hospitality market. The Mandarin at Ayala Triangle Gardens, set for a 2026 opening, targets embassy and corporate accounts with premium rates that match location and service positioning. Midscale hotels anchor domestic business trips and family travel in regional centers, with steady occupancy that diversifies cash flows during seasonal lulls. Utility cost inflation and OTA commissions pressure budget and economy margins, which push operators toward direct channels and cost-efficiency measures.

Service apartments benefit from corporate relocations and project-based stays with multinational accounts, which support long-stay ADR and reduce distribution costs through direct contracts. Rate differentials across tiers persist, with luxury ADRs in Metro Manila materially above midscale averages, which yields higher RevPAR despite lower average occupancy. The mid and upper-midscale cluster continues to dominate in provincial capitals, where location and reliable service are more important than tier upgrades for core demand segments in the Philippines hospitality industry. Luxury resorts in Palawan and similar destinations will rely on utility and transport upgrades to reach full potential as flight times shorten and power and fiber networks improve. Across tiers, sustainability standards and efficiency retrofits will improve margins and appeal to corporate buyers with ESG mandates.

By Booking Channel: Direct Digital Disrupts OTA Dominance

OTAs held 32.52% of bookings in 2025, while direct digital channels are projected to expand at a 9.31% CAGR through 2031 as hotel groups invest in owned platforms and loyalty programs to recapture margin in the Philippines hospitality market. SM Hotels increased the direct share of room nights through promotions and member rates, while Ayala Land’s app-based bookings continue to rise with a streamlined user experience and ancillary F&B ordering. Corporate and MICE bookings rely on direct sales and preferred agreements, which provide predictable base occupancy at negotiated net rates during event blocks. Traditional agents maintain relevance in select source markets with group itineraries and bundled services that simplify travel for first-time or older travelers. Operators continue to balance OTA visibility with cost control, with many pushing loyalty offers and value-adds to shift repeat guests to direct digital channels.

Mobile-led booking behavior strengthens direct channel strategies, as hotels invest in CRM and first-party data to personalize offers and improve conversion. Independent resorts in island destinations still depend on OTAs for discovery and international reach, especially where brand recognition and paid media budgets are limited. Analytics and dynamic pricing flatten historic distribution advantages of global chains, which narrows ADR gaps and directs investment toward owned digital experiences in the Philippines hospitality industry. Partnerships with airlines and wallets are used to stimulate off-peak travel and reduce cancellation risk, which improves yield management. Over time, higher direct shares can stabilize profit margins while OTAs continue to feed incremental demand in shoulder periods.

By Region: Western Visayas Leads While MIMAROPA Accelerates

Western Visayas leads with 38.25% of the Philippines hospitality market share in 2025, supported by Boracay’s strong arrivals and receipts alongside emerging city breaks in Iloilo and Bacolod. Boracay’s managed capacity safeguards the destination while supporting stable rate structures that benefit resort operators through peak seasons. MIMAROPA is projected to grow fastest at an 8.97% CAGR through 2031, with Palawan’s eco-tourism brand and airport pipeline reshaping accessibility and length of stay. The region logged higher receipts and room stock in 2024, signaling readiness for upscale and luxury entries that can scale with planned gateways. El Nido and Coron are anchors for international guests, while San Vicente is poised to expand with new airport capacity and destination planning.

Central Visayas posted broad-based arrivals growth and strong receipts, anchored by Cebu City and Lapu-Lapu City, with a mix of domestic and foreign travelers. Enhanced airport capacity and continuing route development funnel more visitors to dive and leisure spots in Bohol and Cebu’s coastal towns. Caraga shows sustained growth led by Siargao’s surf and eco offerings, with staffing and utilities planning required to maintain service quality as volumes rise. The Others cluster, including NCR and Calabarzon, will continue to function as gateways and short-stay destinations that feed island itineraries, supported by convention and corporate demand. As airport projects are commissioned, inter-island trip chaining will lift regional dispersal and broaden the Philippines hospitality market footprint.

Geography Analysis

Western Visayas, MIMAROPA, Central Visayas, and Caraga set the tone for regional performance, each supported by distinct demand drivers and infrastructure paths that influence hotel mix and rate strategies. Western Visayas balances managed volume in Boracay with expanding urban attractions, which allows sustained rate integrity for upscale beachfront properties and rising occupancy for city hotels. MIMAROPA’s growth is led by Palawan’s international appeal and incoming airport capacity that will compress travel time from Manila, which supports a move upmarket in select municipalities. Central Visayas benefits from Cebu’s connectivity and Bohol’s dive circuits, while significant domestic volumes provide base demand for midscale inventory. Caraga’s acceleration continues around Siargao’s eco and adventure proposition, and planned airport works will further stabilize flight schedules and lift high-season capacity.

The hospitality industry in the Philippines gains from strong domestic travel patterns that boost weekend and holiday stays in regions close to NCR, including Calabarzon, while also fueling longer itineraries in Visayas and Mindanao. Road additions from the Tourism Road Infrastructure Program improve last-mile access and encourage private investment in areas once considered operationally complex for resorts. Visitor receipts rise in regions that combine beaches, heritage sites, and culinary experiences, which drives mixed-use projects and co-located retail and F&B in urban centers. Environmental rules guide site planning in marine parks and protected areas, helping to protect corals and sensitive habitats and sustain premium dive and nature experiences. Expansion of e-gates and facilitation measures improves airport processing and enhances first and last impressions in gateway cities.

Airport expansion projects have a multiplier effect by drawing airlines and supporting year-round route economics, which increases the appeal of coastal destinations to both domestic and foreign travelers. As new capacity comes online, room supply must track demand to maintain rate stability, which encourages mixed portfolios of midscale and luxury hotels in high-growth municipalities. These dynamics help Western Visayas retain leadership while MIMAROPA closes the gap through airport-led gains and eco-tourism branding aligned to global preferences. Central Visayas remains a resilient pillar due to a balanced travel mix and consolidated hotel footprints in Cebu and Bohol. The Philippines hospitality market benefits as improved inter-island links expand trip chaining and average stay, raising utilization in both primary and secondary destinations.

Competitive Landscape

The market remains fragmented by property count even as large groups increase share through portfolio growth, partnerships, and conventional infrastructure that activates MICE calendars. SM Hotels, Robinsons Hotels, Ayala Land Hotels, and other leading platforms add rooms and event space to capture city and resort demand at scale in the Philippines hospitality market. Energy-efficiency investments and building certifications reduce operating costs and create procurement advantages for corporate accounts with ESG requirements. Integrated resorts led by major operators combine gaming, venues, and retail to drive occupancy and F&B spend across price points. TIEZA’s rehabilitation of heritage and eco properties demonstrates a viable model for sustainable assets that complement private developments in island chains.

Distribution strategies evolve as operators rebalance OTA presence with direct digital growth, aiming to recapture commission leakage while maintaining discoverability for international guests. Loyalty programs and owned apps improve repeat stay capture and cross-sell of F&B and events, which helps smooth seasonality in the Philippines hospitality market. Service apartments expand with corporate relocations and project-based stays, creating stable occupancy streams that offset leisure volatility. Utility cost dynamics push operators toward retrofits and renewable options to stabilize margins across portfolios. Airport-led projects increase the attractiveness of secondary destinations to institutional investors who require throughput, reliability, and multi-year room demand visibility.

Workforce availability is a strategic focus as groups coordinate with TESDA and universities to align curriculum to brand standards and multilingual needs. Overseas employment prospects continue to draw hospitality talent, which sustains wage pressure and skills gaps at home. Operators implement standardized training, flexible staffing, and career development programs to raise retention as new hotels open across regions in the Philippines hospitality market. Sustainability and resilience features are increasingly embedded into design and operations to mitigate climate and disaster risks that affect business continuity. These moves aim to enhance competitiveness while preserving local distinctiveness that remains core to the guest value proposition.

Philippines Hospitality Industry Leaders

SM Hotels and Conventions Corp.

Robinsons Hotels & Resorts

AyalaLand Hotels & Resorts Corp.

Megaworld Hotels & Resorts

DoubleDragon (HOTEL 101)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: New NAIA Infra Corp reported 52.02 million passengers for 2025 and the concession targets capacity expansion to 62 million annually, with USD 967 million (PHP 57 billion) remitted to the government in its first year

- May 2025: Robinsons Hotels & Resorts opened the ultra-luxury NUSTAR Hotel in Cebu with 223 rooms, expanding its national portfolio and high-end positioning

- February 2025: SM Hotels and Conventions Corp announced a USD 254.67 million (PHP 15 billion) expansion program through 2028 including eight new hotels and two convention centers, with SMX Convention Center Cebu scheduled to open in Q4 2026

- January 2025: NEDA confirmed progress on flagship airport projects including the New Siargao Airport, Busuanga Airport, and Southern Palawan Airport to support eco and island tourism

Philippines Hospitality Market Report Scope

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Type

| Luxury |

| Mid & Upper-Midscale Hotels |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate/MICE |

| Wholesale & Traditional Agents |

By Region (Philippines)

| Western Visayas |

| MIMAROPA |

| Central Visayas |

| Caraga |

| Others |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Type | Luxury |

| Mid & Upper-Midscale Hotels | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate/MICE | |

| Wholesale & Traditional Agents | |

| By Region (Philippines) | Western Visayas |

| MIMAROPA | |

| Central Visayas | |

| Caraga | |

| Others |

Key Questions Answered in the Report

What is the Philippines hospitality market size and growth outlook to 2031?

The Philippines hospitality market size is USD 8.41 billion in 2026 and is projected to reach USD 11.90 billion by 2031 at a 7.21% CAGR, supported by infrastructure upgrades and a sustained tourism rebound.

Which segments lead and grow fastest in the Philippines hospitality market?

Mid and upper-midscale hotels lead by share at 36.25% in 2025, while luxury hotels post the fastest growth at a 9.52% CAGR through 2031.

Which regions are most attractive for expansion in the Philippines hospitality market?

Western Visayas leads by share in 2025 with Boracay as anchor, while MIMAROPA is the fastest growing due to Palawan’s eco brand and new airport projects that will reduce travel time from Manila.

How is distribution changing for hotels in the Philippines?

OTAs held a 32.52% share in 2025, but direct digital is the fastest growing channel as hotel groups scale loyalty programs and owned apps to reduce commission costs and capture repeat guests.

What risks could slow the Philippines hospitality market?

Natural hazards, infrastructure gaps in secondary islands, and skilled labor shortages can constrain growth and raise operating costs, especially in coastal destinations.

What 2025–2026 developments matter most for investors?

What 2025-2026 developments matter most for investors?

Page last updated on: