Cosmetic Implants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

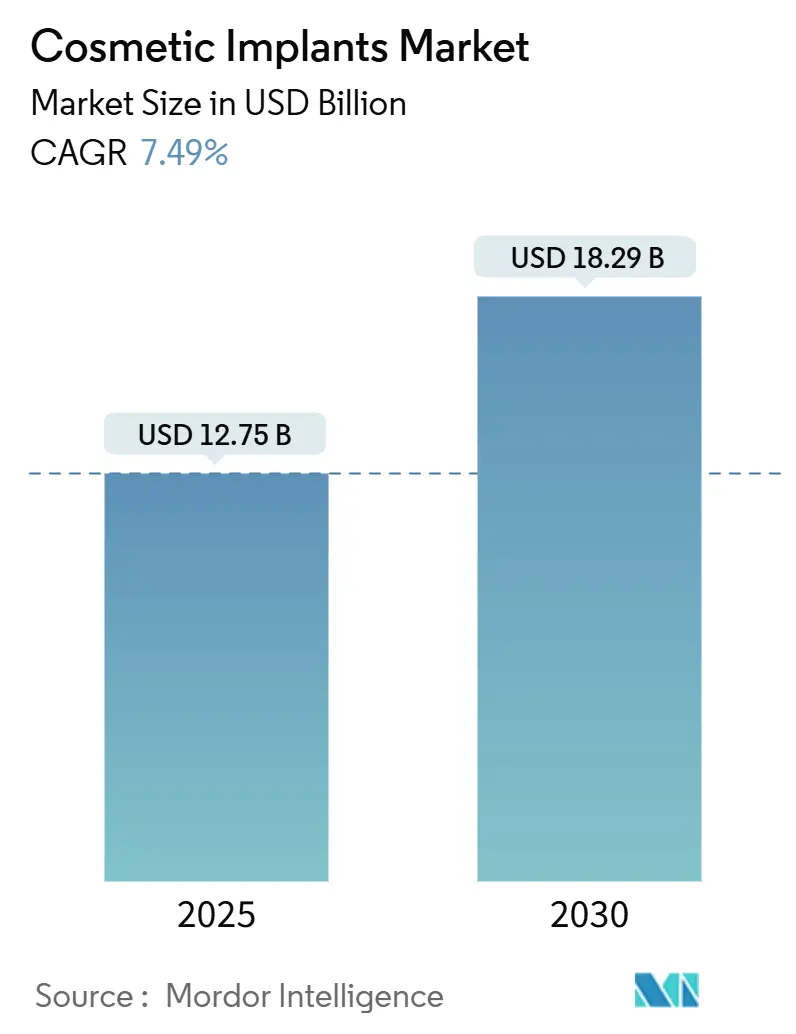

| Market Size (2025) | USD 12.75 Billion |

| Market Size (2030) | USD 18.29 Billion |

| Growth Rate (2025 - 2030) | 7.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cosmetic Implants Market Analysis by Mordor Intelligence

The Cosmetic Implants Market size is estimated at USD 12.75 billion in 2025, and is expected to reach USD 18.29 billion by 2030, at a CAGR of 7.49% during the forecast period (2025-2030).

Consistent demand stems from rapid material science breakthroughs, wider acceptance of aesthetic procedures among diverse age groups, and a steady preference for treatments that combine functional restoration with cosmetic appeal. Manufacturers continue to secure regulatory approvals that emphasize clinical safety, while advances in 3D printing, artificial intelligence, and regenerative medicine create opportunities for highly personalized solutions. Rising disposable income levels in emerging economies and expanding access through digital platforms have broadened the addressable patient pool. At the same time, premium pricing, heightened regulatory scrutiny, and competition from minimally invasive alternatives temper absolute growth but encourage differentiation based on safety, efficacy, and sustainability.

Key Report Takeaways

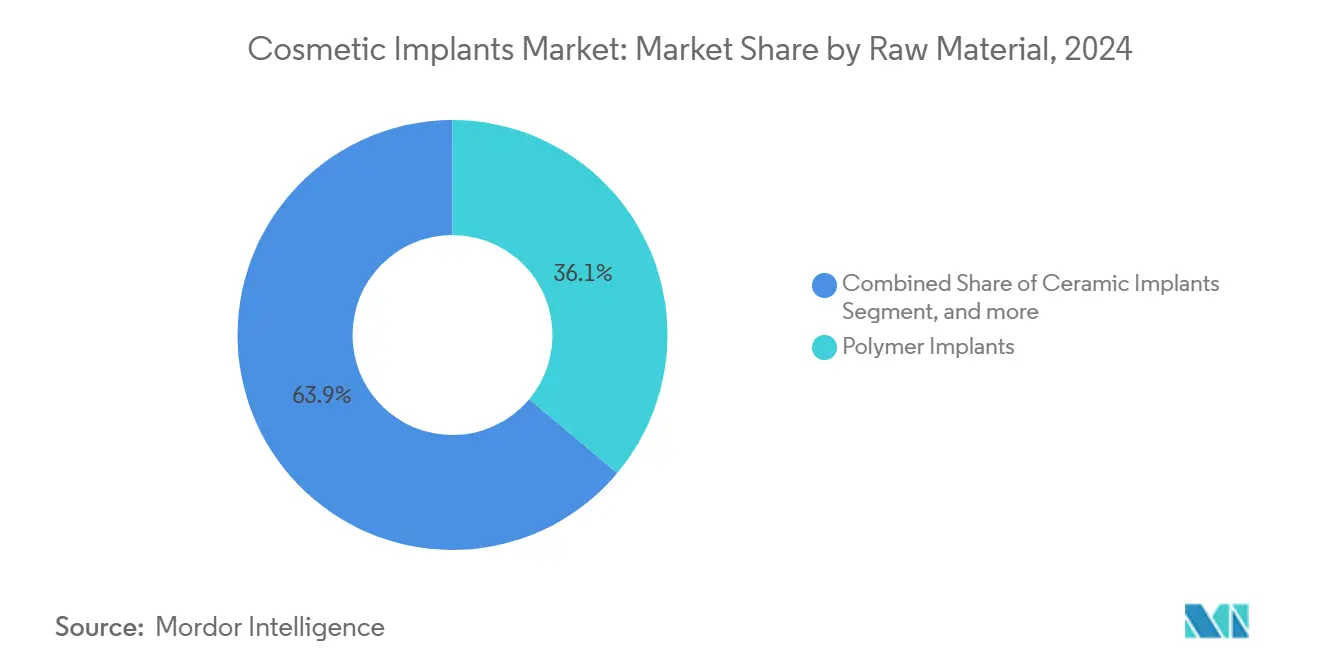

- By raw material, polymer implants captured 36.07% of cosmetic implants market share in 2024, while biological material implants are forecast to expand at a 9.44% CAGR to 2030.

- By application, dental procedures led with 46.14% of the cosmetic implants market size in 2024 and continue to anchor overall revenue momentum, while body contouring are forecast to expand at a 10.52% CAGR to 2030.

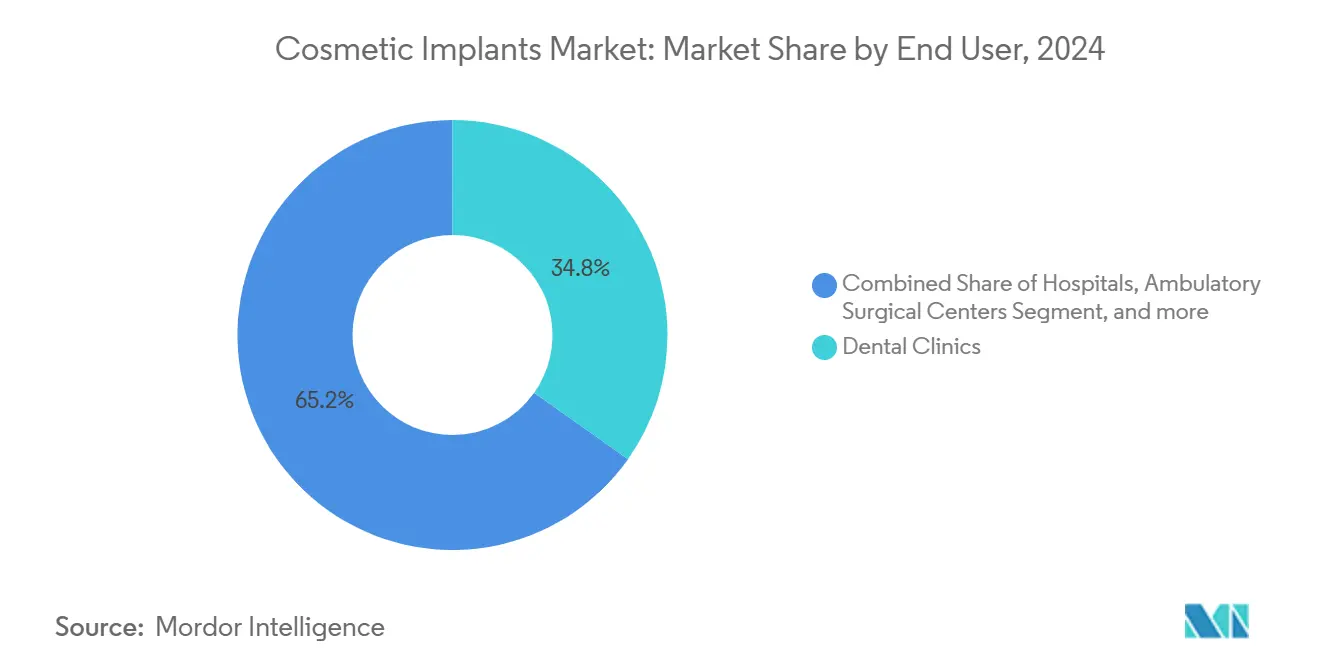

- By end-user setting, dental clinics led with 34.82% of the cosmetic implants market size in 2024 and ambulatory surgical centers represent the fastest-growing venue, advancing at an 11.08% CAGR between 2025 and 2030 as payers and patients shift toward cost-effective outpatient care.

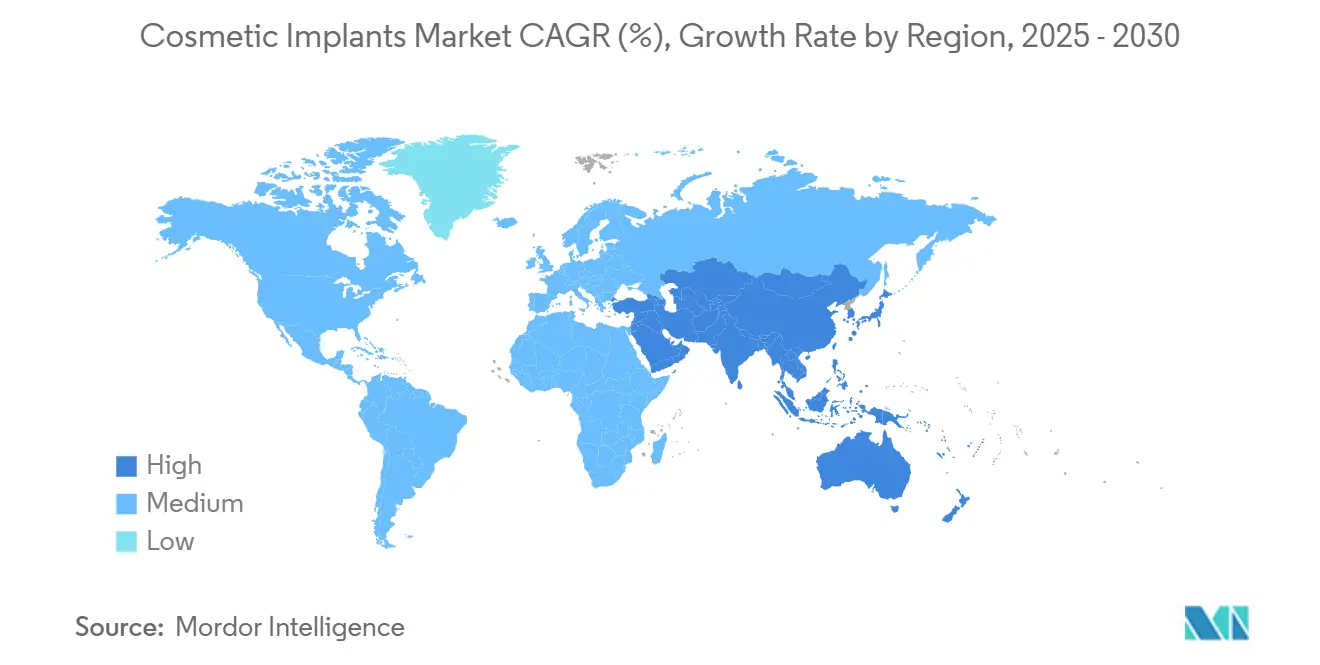

- By geography, North America held 42.34% of cosmetic implants market share in 2024, whereas Asia-Pacific is projected to record the highest regional CAGR at 9.96% through 2030.

Global Cosmetic Implants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating interest in aesthetic procedures for personal and social confidence | +1.8% | Global, strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Breakthroughs in biomaterials and 3D printing enabling precision and innovation | +2.1% | North America & Europe lead, APAC adoption rising | Long term (≥ 4 years) |

| Rising influx of medical tourists into cost-effective treatment hubs | +1.2% | Asia-Pacific core, spill-over to MEA & South America | Short term (≤ 2 years) |

| Increasing disposable income among middle-class consumers worldwide | +1.4% | Global, notably emerging APAC & South America | Medium term (2-4 years) |

| AR beauty filters driving aspirational standards and reshaping self-image norms | +0.8% | Global, pronounced in North America & developed APAC | Short term (≤ 2 years) |

| Growing demand for gender-affirming surgeries creating specialized segments | +0.6% | North America & Europe, expanding in progressive APAC | Long term (≥ 4 years) |

Source: Mordor Intelligence

Escalating Interest in Aesthetic Procedures for Personal and Social Confidence

The shift from corrective to enhancement-focused motivations has positioned the cosmetic implants market as a routine component of self-care for many consumers. Survey data show that 85% of medical aesthetic clients intend to sustain or increase spending on procedures, a sentiment now spanning multiple age cohorts. Gender dynamics are also evolving, with a marked rise in male participation and a growing emphasis on gender-affirming implant surgeries.[1]Cigna Healthcare, “Dental Implant Care: Trends and AI Adoption,” cigna.com Social-media exposure normalizes aesthetic treatments, eroding stigma and reinforcing aspirational standards. Younger demographics increasingly pursue “preventive” implants to delay visible aging, suggesting a structural expansion of lifetime demand. Clinics that tailor messaging to confidence, career advancement, and wellness capture higher patient retention rates while fostering long-term growth.

Breakthroughs in Biomaterials and 3D Printing Enabling Precision and Innovation

Additive manufacturing and advanced biomaterials underpin the latest wave of patient-specific solutions. Researchers at the University of Sydney demonstrated nanoscale 3D printing for synthetic bone substitutes with 300 nm resolution that supports robust bone regeneration.[2]University of Sydney, “Researchers Produce Synthetic Bone Substitute Using Nanoscale 3D Printing,” sydney.edu.au Shape-memory scaffolds combining polylactic acid and polycaprolactone now deliver dual tumor-ablation and bone-regrowth functionality on near-infrared activation. CollPlant’s partnership with Stratasys targets 200 cc regenerative breast implants manufactured from plant-based collagen, aligning with biodegradability and biocompatibility priorities. These advances address longstanding concerns over capsular contracture, implant rupture, and revision surgeries. Personalized design shortens operative time and improves aesthetic outcomes, reinforcing premium-pricing potential and competitive differentiation within the cosmetic implants market.

Rising Influx of Medical Tourists into Cost-Effective Treatment Hubs

Cross-border travel for cosmetic implants surged as patients leverage cost differentials and specialized expertise. South Korea’s integrated medical tourism framework bundles travel, procedure, and recuperation services into seamless packages that appeal to Chinese and Southeast Asian clients.[3]MDPI, “Medical Tourism Ecosystem in Korea for Chinese Patients,” mdpi.com Nonetheless, safety incidents and regulatory gaps in some popular destinations prompt more affluent travelers to favor jurisdictions with transparent oversight. Emerging Asian economies respond by fortifying domestic quality standards to retain outbound demand. The balance between affordability and assurance will continue to shape country-level growth trajectories.

Increasing Disposable Income Among Middle-Class Consumers Worldwide

Expanding middle-class segments in China, India, Indonesia, and Brazil represent a sizable influx of first-time elective procedure candidates. Rising household earnings coincide with a cultural transition that frames appearance enhancement as an investment in professional and social capital. Premiumization trends indicate willingness to pay for differentiated implant technologies that promise natural feel, low complication rates, and shorter recovery periods. Digital platforms streamline discovery, financing, and after-care, further lowering adoption barriers and enlarging the cosmetic implants market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of surgical implants and associated medical services | -1.5% | Global, acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Ongoing safety issues, product recalls, and legal disputes | -0.9% | North America & Europe, regulatory spillover worldwide | Short term (≤ 2 years) |

| Sustainability concerns tied to silicone and polymer waste disposal | -0.7% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Rising preference for non-surgical alternatives like dermal fillers and thread lifts | -1.2% | Global, pronounced in developed markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Premium Pricing of Surgical Implants and Associated Medical Services

Full-cycle procedure costs frequently surpass USD 17,000 when anesthesia, facility fees, and post-operative care are included, creating affordability barriers for a broad segment of potential patients. Heightened price sensitivity drives consumers toward minimally invasive fillers and thread-lift procedures that promise visible improvements with lower financial outlays and minimal downtime. Providers respond by migrating suitable interventions to ambulatory surgical centers, which achieve lean operating structures through streamlined staffing and shorter patient turnover times. Widening adoption of in-house financing and subscription-based maintenance plans offers partial mitigation but does not fully offset cost-related attrition.

Ongoing Safety Issues, Product Recalls, and Legal Disputes

High-profile FDA Class I recalls, including Hologic’s BioZorb marker and Allergan’s textured breast implants, reinforce consumer vigilance about long-term implant safety. Litigation exposure elevates insurance premiums and imposes recalls, re-labeling, and patient-notification costs that compress margins. In response, Establishment Labs reported capsular contracture rates of only 0.5% and rupture rates of 0.6% in its Motiva clinical program, underscoring how superior safety data can become a compelling marketing advantage. Upcoming Quality System Regulation revisions, effective February 2026 will further align U.S. standards with ISO 13485, demanding tighter supplier controls and more extensive post-market surveillance.

Segment Analysis

By Raw Material: Polymer Leadership Meets Biological Momentum

Polymer implants accounted for 36.07% cosmetic implants market share in 2024, underpinned by decades of clinical familiarity with silicone elastomers. These materials support a spectrum of breast, facial, and body contouring procedures, making them indispensable within current surgical workflows. However, concerns over long-term degradation and environmental impact motivate research into next-generation polymers with enhanced durability and recyclability. Biodegradable polydioxanone meshes and bioresorbable polycaprolactone screws exemplify the transition to eco-friendly options that lessen revision risk.

Biological material implants, although representing a smaller revenue base, advance at a 9.44% CAGR through 2030 and embody the frontier of regenerative aesthetics. Collagen-based scaffolds sourced from tobacco plants bypass zoonotic contamination worries while facilitating tissue ingrowth. Early trials report accelerated healing, lower inflammatory profiles, and improved tactile sensation. As 3D bioprinting platforms mature, patient-specific constructs can integrate vasculature and cellular components, potentially eliminating conventional prostheses for select indications over the long term. Ceramic and metal solutions maintain niche relevance in dental and craniofacial reconstruction thanks to compressive strength and osseointegration, yet their share is expected to recede as hybrid polymer-ceramic composites reach clinical readiness.

Note: Segment shares of all individual segments available upon report purchase

By Application: Dental Dominance and Body Contouring Upsurge

Dental implants secured 46.14% of cosmetic implants market revenue in 2024, reflecting the dual imperative of functional restoration and aesthetic integrity. Surgeons now employ AI-assisted treatment planning that overlays CBCT scans with intraoral optical impressions, producing precise drilling templates and reducing chair time by up to 30%. Zirconia and titanium alloy fixtures continue as mainstays, yet hybrid polymer-ceramic abutments gain popularity for patients requiring higher translucency in the esthetic zone.

Body contouring leads the growth trajectory, progressing at a 10.52% CAGR as patients demand comprehensive silhouette refinement. Customizable gluteal and pectoral implants produced via additive manufacturing address anatomical diversity while minimizing implant migration. Post-bariatric patients represent a growing cohort pursuing contouring solutions to manage redundant tissue once weight targets are met. Facial implants capture steady demand for mandibular angle, malar, and nasal augmentation, with 3D-printed porous polyethylene enabling long-lasting integration. Breast augmentation remains a stable contributor but faces incremental substitution by fat-grafting techniques augmented with platelet-rich plasma, a trend that may redirect volume toward combination procedures.

By End User: Ambulatory Settings Redefine Procedure Economics

Dental clinics held 34.82% of cosmetic implants market revenue in 2024, leveraging specialized workflow efficiencies and high patient throughput. Cloud-based practice management platforms integrate imaging, billing, and patient engagement, permitting real-time surgical simulation that enhances consent quality. Hospitals preserve a vital role in complex reconstructive cases requiring multidisciplinary teams, yet they face reimbursement pressure to move suitable interventions offsite.

Ambulatory surgical centers record an 11.08% CAGR, benefiting from lower fixed-cost structures, optimized staffing ratios, and streamlined regulatory requirements. These facilities often partner with device manufacturers on inventory consignment models that reduce capital outlays. Aesthetic clinics focus on integrated service lines that bundle injectables, laser resurfacing, and implant procedures, thereby maximizing lifetime patient value. Telehealth pre-consultations and AI-driven outcome visualization improve conversion rates, while post-operative remote monitoring apps cut readmission risk. As minimally invasive innovations proliferate, end-user competition will hinge on personalized care, flexible financing, and seamless digital engagement.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained a dominant 42.34% share of cosmetic implants market revenue in 2024, supported by advanced procedural expertise, robust payer coverage for reconstructive indications, and a high-income consumer base willing to pay premiums for novel solutions. Market expansion is also visible in Canada, where streamlined import pathways and favorable exchange rates attract inbound medical tourists. Mexico’s private clinics increasingly serve cross-border patients from the southern United States, driving upgrades in facility accreditation and infection-control protocols.

Europe positions safety as a competitive advantage, channeling stringent MDR compliance to reinforce patient trust. GC Aesthetics received the first MDR-certified breast implant, setting a benchmark for rivals. Germany and France lead regional procedure volumes, while Italy and Spain show pronounced growth in dental and body contouring applications. Sustainability directives accelerate investment in recyclable silicone supply chains, with New Dawn Silicones pioneering solvent-based depolymerization that achieves virgin-grade recovery. Post-Brexit regulatory divergence prompts multinational firms to establish separate conformity assessment strategies for the United Kingdom, raising costs but preserving market continuity.

Asia-Pacific ranks as the fastest-growing zone, expanding at 9.96% CAGR through 2030, and is projected to contribute more than 35% of incremental global revenue over the period. Japan spearheads high-tech implant research, including titanium lattice structures fabricated via electron-beam melting for craniofacial reconstruction. South Korea’s government-supported tourism clusters combine medical, hospitality, and cultural experiences that appeal to intra-regional travelers. China’s large urban middle class fuels demand for premium dental implants, and continued e-commerce penetration lifts awareness in Tier 2 and Tier 3 cities. India advances domestic manufacturing under its “Make in India” initiative, focusing on cost-effective polymer implants that target domestic patients and neighboring markets. Australia maintains rigorous Therapeutic Goods Administration evaluations, often acting as an early-adopter test bed before broader Asia-Pacific rollouts. Collectively, these trends underscore the region’s transition from volume-driven imports to innovation-led, locally adapted product development.

Competitive Landscape

Moderate fragmentation characterizes the cosmetic implants industry, with a blend of multinational conglomerates and agile innovators vying for technological leadership. Johnson & Johnson, through its Mentor division, leverages longitudinal data from more than 200,000 breast implant recipients to substantiate reliability claims. Establishment Labs’ 2025 guidance of USD 205–210 million underscores its successful U.S. market debut, propelled by low complication metrics and proprietary surface micro-textures. Straumann Group, Zimmer Biomet, and Dentsply Sirona concentrate on influence in the dental implant sub-segment, aided by vertically integrated workflows that encompass scanning, planning, and restoration.

Strategic acquisitions accelerate portfolio expansion and cross-selling opportunities. Zimmer Biomet’s 2024 purchase of Paragon 28 broadened its foot-and-ankle portfolio and extended its reach into adjacent elective markets. Sientra’s 2024 bankruptcy and sale to Tiger Aesthetics for USD 42.5 million signal consolidation pressures for single-line players lacking the scale to absorb prolonged litigation expenses and R&D investment. Investors direct capital toward additive manufacturing startups able to customize implants at surgical sites, potentially compressing lead times from weeks to hours.

R&D emphases gravitate toward biocompatible coatings that curb bacterial colonization, AI-enabled robotic placement systems, and environmentally sustainable manufacturing. Companies allocate double-digit revenue percentages to digital workflow integration, reasoning that superior visualization and prediction tools will reduce revision surgeries and secure surgeon loyalty. As regulatory bodies intensify post-market surveillance, market entrants must pair rapid innovation with rigorous clinical validation to maintain competitive parity. Overall, winning strategies center on data-backed safety, ecosystem partnerships, and geographic agility suited to divergent regional regulatory landscapes.

Cosmetic Implants Industry Leaders

-

3M

-

Allergan (AbbVie)

-

Cochlear Ltd

-

Dentsply Sirona

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Establishment Labs reported Q4 2024 revenue of USD 44.5 million with USD 3.3 million from U.S. Motiva implant launch, reaffirming 2025 guidance of USD 205-210 million representing 23-26% growth. The company's successful U.S. market entry following FDA approval demonstrates the commercial potential of technologically superior implant solutions.

- February 2025: Zimmer Biomet announced Q4 2024 net sales of USD 2.023 billion, up 4.3% year-over-year, and completed acquisition of Paragon 28 to expand foot and ankle orthopedic capabilities. The company received FDA approval for Oxford Cementless Partial Knee, the only FDA-approved cementless partial knee implant in the U.S.

- November 2024: Establishment Labs completed USD 50 million registered direct offering to support sales, marketing, and R&D activities for Motiva devices and femtech solutions. The funding strengthens the company's position for U.S. market expansion following FDA approval.

- October 2024: FDA issued updated guidance on biocompatibility assessment for medical devices, emphasizing adherence to ISO 10993-1 standards and improving consistency in premarket submissions. The guidance affects all implant manufacturers seeking U.S. market approval.

Global Cosmetic Implants Market Report Scope

As per the scope, cosmetic implants are devices or tissues placed inside or on the body's surface. Many implants are prosthetics intended to replace missing body parts. Other implants deliver medication, monitor body functions, or support organs and tissues. Some implants are made from skin, bone, or other body tissues. The Cosmetic Implants Market is segmented by Raw Material (Polymer Implants, Ceramic Implants, Metal Implants, and Biological Material Implants), Application (Dental Implants, Breast Implants, Facial Implants, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Raw Material | Polymer Implants | ||

| Ceramic Implants | |||

| Metal Implants | |||

| Biological Material Implants | |||

| By Application | Dental | ||

| Breast | |||

| Facial | |||

| Body Contouring | |||

| By End User | Hospitals | ||

| Specialty & Aesthetic Clinics | |||

| Ambulatory Surgical Centers | |||

| Dental Clinics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Polymer Implants |

| Ceramic Implants |

| Metal Implants |

| Biological Material Implants |

| Dental |

| Breast |

| Facial |

| Body Contouring |

| Hospitals |

| Specialty & Aesthetic Clinics |

| Ambulatory Surgical Centers |

| Dental Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the cosmetic implants market?

The cosmetic implants market size reached USD 12.75 billion in 2025 and is forecast to reach USD 18.29 billion by 2030.

Which raw-material segment leads the market?

Polymer implants command 36.07% cosmetic implants market share due to versatile applications and longstanding clinical familiarity.

Which application generates the highest revenue?

Dental procedures account for 46.14% of the cosmetic implants market, combining functional restoration with aesthetic benefits.

Which end-user segment is expanding the fastest?

Ambulatory surgical centers are growing at an 11.08% CAGR as payers and patients embrace cost-efficient outpatient settings.

Which region will register the highest growth through 2030?

Asia-Pacific is projected to record a 9.96% CAGR, driven by rising disposable incomes and supportive medical tourism frameworks.

How are safety concerns influencing competitive dynamics?

Manufacturers with strong clinical evidence and low complication rates, such as Establishment Labs’ 0.5% capsular contracture gain share, are expected to benefit as regulators heighten post-market surveillance.

Page last updated on: July 3, 2025