Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

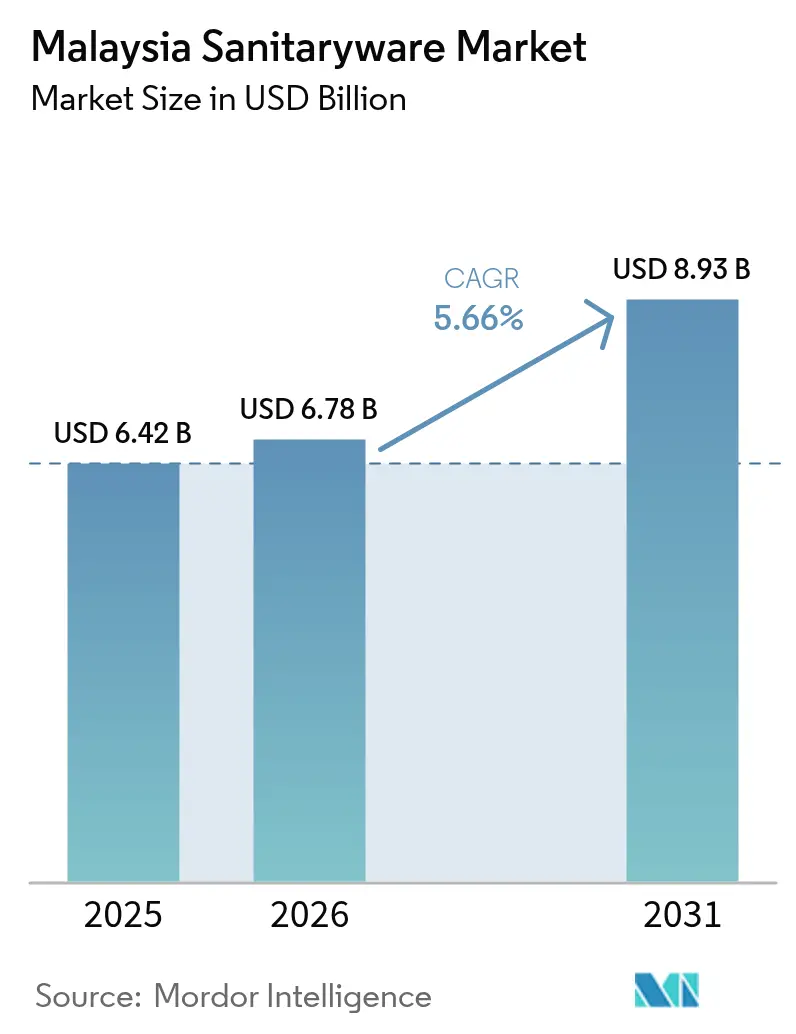

| Base Year Market Size (2025) | USD 6.42 Billion |

| Market Size (2026) | USD 6.78 Billion |

| Market Size (2031) | USD 8.93 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Sanitaryware Market Analysis by Mordor Intelligence

The Malaysia sanitaryware market size was valued at USD 6.42 billion in 2025 and estimated to grow from USD 6.78 billion in 2026 to reach USD 8.93 billion by 2031, at a CAGR of 5.66% during the forecast period (2026-2031). Growth rests on steady residential construction, accelerating infrastructure modernization, and the government’s sustained housing allocations that channel predictable, large-volume orders into the supplier base. The ongoing rise in urban migration, which has significantly increased the national urbanization rate, is driving a heightened demand for compact, water-efficient fixtures. These products are particularly suited to the spatial constraints and resource efficiency requirements of densely populated apartment settings. The increasing penetration of e-commerce is transforming traditional distribution frameworks, allowing manufacturers to directly reach consumers while minimizing reliance on costly physical retail networks. This shift is driving efficiency and reducing operational expenses in the supply chain. Green-building certification tied to the Water Sector Transformation 2040 agenda is nudging all builders toward dual-flush cisterns and low-flow faucets[1]PR1MA, “PR1MA Affordable Housing Programs,” pr1ma.my . Finally, the rebound in hospitality projects following border reopenings is lifting commercial refurbishment demand and exposing domestic consumers to touchless technologies, accelerating mainstream adoption.

Key Report Takeaways

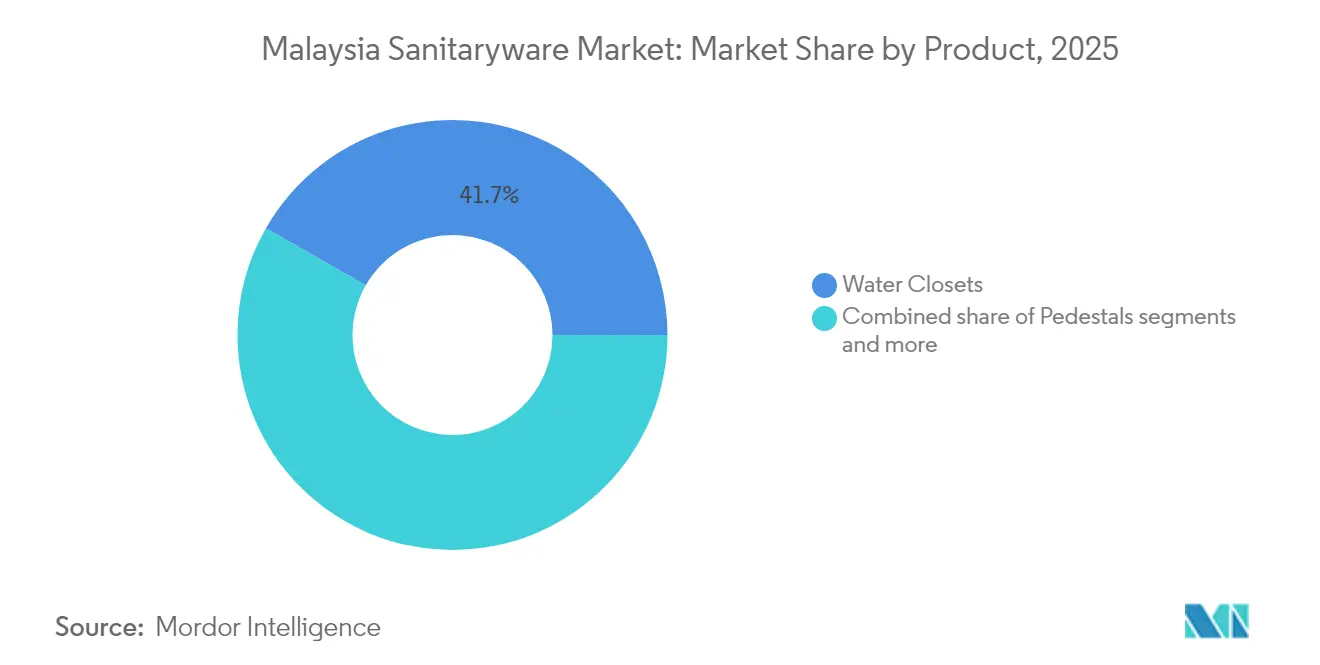

- By product category, water closets led with 41.73% of the Malaysia sanitaryware market share in 2025; cisterns are projected to grow at a 10.02% CAGR through 2031.

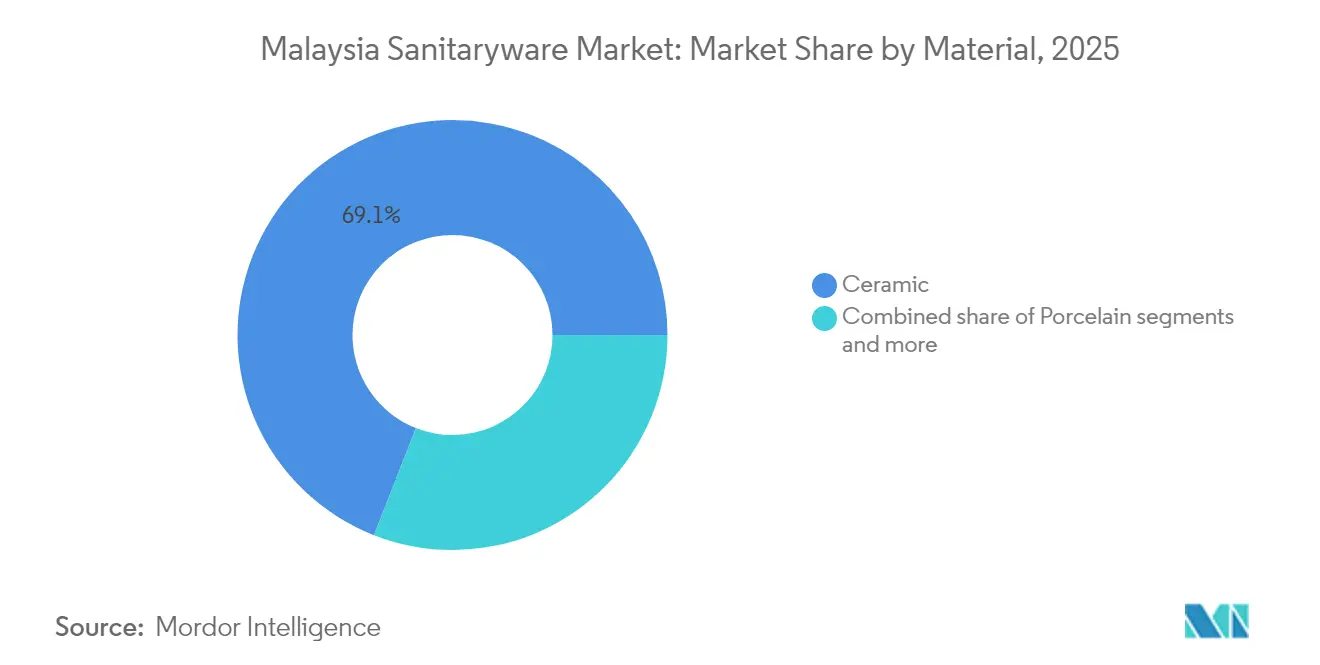

- By material, ceramic accounted for 69.05% of the Malaysia sanitaryware market size in 2025, while natural stone and mosaic combined are pacing at a 9.21% CAGR to 2031.

- By application, bathroom installations captured 77.68% of the Malaysia sanitaryware market share in 2025; kitchen installations are advancing at a 7.74% CAGR during the forecast.

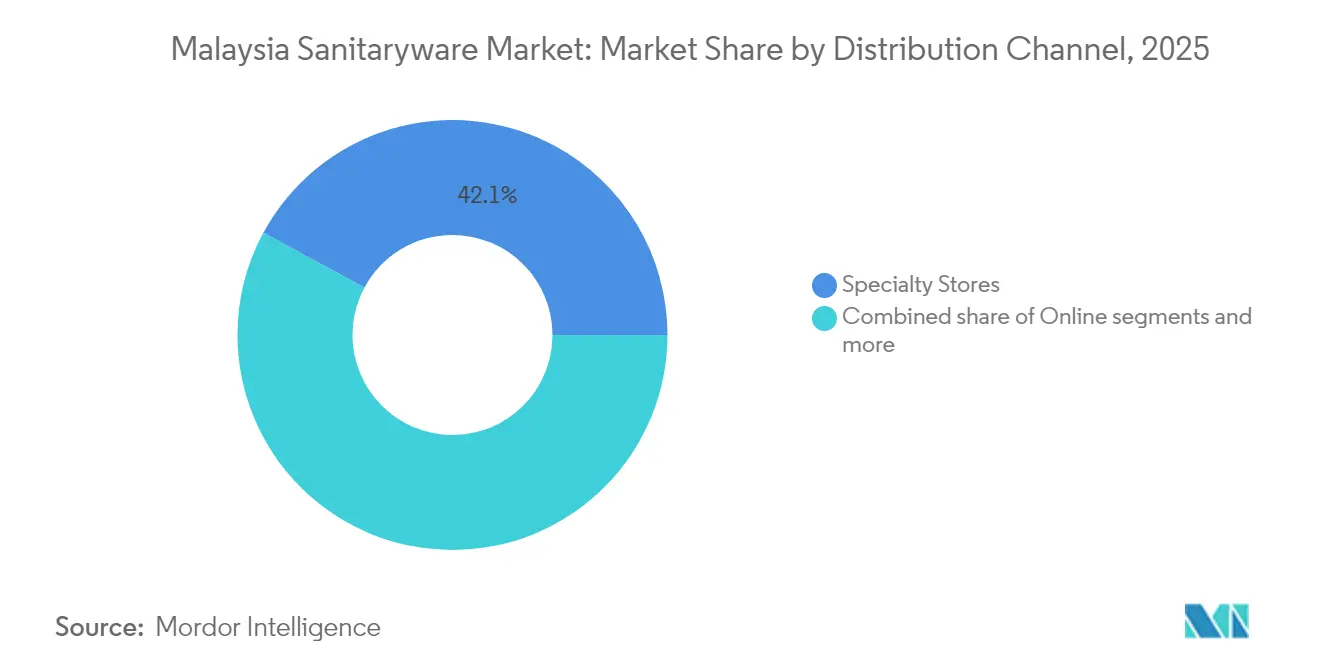

- By distribution channel, specialty stores held 42.12% of the Malaysia sanitaryware market share in 2025; online platforms are forecast to rise at a 12.48% CAGR to 2031.

- By end-user, residential projects commanded 65.71% of the Malaysia sanitaryware market size in 2025, whereas commercial projects exhibit the fastest 8.02% CAGR through 2031.

- By geography, the Central Region maintained a 46.83% of the Malaysia sanitaryware market share in 2025; East Malaysia is expanding at a 9.54% CAGR due to federal rural-infrastructure outlays.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Sanitaryware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization and Government Housing Initiatives | +1.8% | National, concentrated in the Central and Southern Regions | Medium term (2-4 years) |

| Rising Disposable Incomes and Middle-Class Renovation Demand | +1.2% | Central Region, Northern Region urban centres | Long term (≥ 4 years) |

| Growth of E-commerce Home-Improvement Platforms | +0.9% | National, with higher penetration in the Central Region | Short term (≤ 2 years) |

| Hotel & Tourism Boom Accelerating Hospitality Restroom Upgrades | +0.7% | Central Region, East Coast tourism corridors | Medium term (2-4 years) |

| Water-Efficient Green-Building Certification Push | +0.5% | Central Region, expanding to Northern and Southern Regions | Long term (≥ 4 years) |

| Modular Prefabricated Bathroom Pods Adoption in High-Rise Projects | +0.4% | Central Region, Southern Region industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Government Housing Initiatives

Malaysia’s urban population will move past 80% by 2030, locking in multi-year demand for affordable, standardized sanitaryware that meets procurement rules in programs such as PR1MA and Rumah Mesra Rakyat [2]: Nova School of Business and Economics, “E-commerce Expansion Strategy,” run.unl.pt . Productivity targets under the Construction Industry Transformation Programme are steering contractors toward bulk ordering from local factories able to guarantee on-time volume. Housing tenders now include explicit low-flow and dual-flush specifications, which create a technology minimum that lifts overall product quality. Because each state-backed project carries firm delivery milestones, suppliers can plan capacity with greater certainty and spread fixed costs over predictable production runs. That stability has encouraged domestic players to invest in new kilns and glazing lines, raising the Malaysia sanitaryware market’s technical baseline.

Rising Disposable Incomes and Middle-Class Renovation Demand

Urban middle-income households increasingly treat bathroom upgrades as value-enhancement projects that parallel rising apartment resale prices in Kuala Lumpur and Penang. In 2024, retail chains such as MR DIY expanded their operations, driving the mainstream adoption of mid-tier bathroom products, including faucets, wash basins, and soft-close seats. The increasing purchasing power of dual-income households, coupled with higher discretionary budgets, has positioned these consumers as key drivers of demand for complete bathroom renovations. Many of these households are utilizing in-store credit plans to finance such upgrades, reflecting a growing trend toward convenience and affordability in home improvement spending. This segment cares about aesthetics and longevity, raising pull-through for porcelain and natural-stone finishes. The cycle supports higher average selling prices and smooths seasonal demand fluctuations, reinforcing the Malaysia sanitaryware market’s revenue resilience.

Growth of E-commerce Home-Improvement Platforms

Shopee and Lazada jointly command over 70% of Malaysia’s online retail traffic, giving sanitaryware brands national reach without sizeable showroom footprints[3]Academy of Sciences Malaysia, “Water Sector Transformation 2040,” wst2040.my. The increasing penetration of smartphones allows consumers to efficiently compare product SKUs, access instructional installation videos, and seamlessly schedule services within a single session, streamlining the overall shopping experience. Government programs like the Digital Free Trade Zone have shortened last-mile delivery times for bulky goods and lowered freight costs. Platform partnerships now bundle certified installers, neutralizing the historical deterrent of self-installation risk. As a result, online volume is expanding faster than any other channel, pushing legacy specialty outlets to adopt click-and-collect or virtual-tour models to retain share in the Malaysia sanitaryware market.

Hotel & Tourism Boom Accelerating Hospitality Restroom Upgrades

Tourist arrivals rebounded strongly in 2024, and the East Coast Rail Link is opening second-tier destinations to hotel developers. International chains standardize bathroom specs across properties, which means large, recurring orders for touchless faucets, sensor urinals, and antimicrobial surfaces. Local suppliers that achieve the required ISO quality marks win stable contracts and export-grade reputational benefits. The guest experience focus on hygiene translates to higher demand for rimless bowls, concealed cisterns, and easy-clean glazes throughout the Malaysia sanitaryware market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Ceramic Raw-Material Prices | -0.8% | National, affecting all manufacturing regions | Short term (≤ 2 years) |

| Sluggish Completion of Public Infrastructure Projects | -0.6% | East Malaysia, Northern Region, rural areas | Medium term (2-4 years) |

| Rising Competition from Low-Cost Imports (e.g., Vietnam, China) | -0.5% | National, concentrated in price-sensitive segments | Long term (≥ 4 years) |

| Limited Awareness of Hygienic Touchless Sanitaryware | -0.3% | East Malaysia, rural areas across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Ceramic Raw-Material Prices

Energy-linked clay and glaze inputs have witnessed abrupt price spikes, crimping gross margins for domestic kilns. Local producers such as Claytan Group must juggle spot purchases with longer-term contracts to secure supply continuity[4]Claytan Group, “Company Milestones & Achievements,” claytangroup.com . Smaller firms with limited hedging capabilities face significant challenges in submitting fixed-price tenders, which restricts their ability to compete for inclusion in large-scale housing projects. This inability to mitigate cost fluctuations exposes these firms to financial risks, thereby reducing their competitiveness in the market. The persistent uncertainty surrounding input costs is expected to constrain capacity expansion efforts, which, in turn, could moderate the short-term growth trajectory of Malaysia's sanitaryware market.

Sluggish Completion of Public Infrastructure Projects

The Malaysia sanitaryware market faces challenges in maintaining consistent demand visibility due to timing discrepancies in project execution. Delays in rural water and sewerage infrastructure projects, caused by prolonged multi-agency approval processes, disrupt the timeline for downstream fixture installations. These delays place financial strain on suppliers, as they are compelled to hold finished inventory for extended periods, impacting their working capital. Furthermore, the federal government's transition to a 'build-then-sell' housing model has lengthened funding cycles for developers, creating additional uncertainty. This shift has also deferred the initiation of certain private projects, further complicating market dynamics and demand forecasting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Water Closets Anchor Volume While Cisterns Lead Innovation

Water Closets generated 41.73% of 2025 revenue, confirming their status as the essential fixture in every new build and renovation within the Malaysia sanitaryware market. Steady population growth and rising household formation guarantee basal demand, whereas design refreshes such as rimless bowls lift replacement cycles. Cisterns, however, claim the fastest 10.02% CAGR between 2026-2031 as dual-flush technology becomes mandatory in municipal tender books and green-building checklists. Vendors able to certify 4.5-liter flush performance under SIRIM standards secure priority placement on government supplier rosters.

Claytan’s Water Saver cistern exemplifies local innovation that meets both price and efficiency goals, reinforcing domestic share. International premium brands compete by bundling concealed tanks and electronic bidet controls, appealing to luxury condos. Combined, these dynamics push average transaction values upwards and help the Malaysia sanitaryware market capture higher specification tiers without sacrificing baseline affordability.

By Material: Ceramic Dominance Faces Natural-Stone Disruption

Ceramic constitutes 69.05% of 2025 sales thanks to mature kiln infrastructure, abundant local clay, and predictable cost curves in the Malaysia sanitaryware market. Mass-market apartments and budget hotels continue to default to white-glazed ceramic for durability and price. Nevertheless, Natural Stone and Mosaic variants are climbing at 9.21% CAGR on the back of premium hotel refurbishments and upscale landed homes. Developers position stone basins and textured mosaics as visual differentiators that justify premium selling prices.

The Malaysian Green Technology Corporation has issued guidelines emphasizing the use of recycled materials and energy-efficient firing techniques in green manufacturing processes. Companies adopting these practices, particularly those experimenting with composite blends and fireclay, are strategically positioning themselves to earn GBI points, thereby broadening their material portfolios. This strategic shift is fostering diversification in supplier revenue streams while mitigating the risks associated with raw material price fluctuations in the traditional ceramics segment of the Malaysian sanitaryware market.

By Application: Bathrooms Dominate yet Kitchens Accelerate

Bathroom installations accounted for 77.68% of 2025 turnover, anchoring predictable replacement cycles tied to tile rehabs and leak-prevention upgrades across the Malaysia sanitaryware market. Packages often include a wash basin, a closet, a cistern, a faucet, and accessories, presenting cross-selling opportunities. Kitchens, while smaller at present, are posting a 7.74% CAGR as open-plan layouts convert sinks and faucets into focal design elements. Property listings increasingly spotlight premium kitchen hardware to attract urban professionals, prompting developers to budget for higher-end stainless or granite composite sinks.

Builders striving to achieve GBI compliance are increasingly adopting a comprehensive approach by monitoring water consumption across entire residential units, rather than limiting the focus to bathrooms. This strategic shift is driving the growing demand for aerated kitchen faucets, which are recognized for their water-saving capabilities. These developments are contributing to the diversification of the product portfolio within Malaysia's sanitaryware market, while simultaneously creating opportunities for value addition and up-selling throughout the various stages of project lifecycles.

By Distribution Channel: Online Platforms Transform Market Access

Specialty stores retained 42.12% of 2025 sales by offering showroom touch-and-feel experiences, installer referrals, and post-sale service bundles that are vital for high-ticket items. Yet online platforms are expanding at a 12.48% CAGR as friction points, the chief being installation, are alleviated through vetted service add-ons. E-logistics improvements sponsored by the Digital Free Trade Zone shorten delivery windows even for fragile ceramic pieces, eroding one of brick-and-mortar’s traditional advantages.

Manufacturers now list full SKU catalogues online, from entry-level closets to designer basins, democratizing access for rural buyers. Hybrid models blending physical display with QR-code ordering prevent channel conflict and preserve specialty-store margins. The overall shift signals a long-run rebalancing of the Malaysia sanitaryware market toward more data-driven, customer-centric distribution.

By End-User: Commercial Acceleration Outpaces Residential Base

Residential demand made up 65.71% of 2025 expenditure, sustained by steady handovers of PR1MA units and private condos. However, Commercial orders are growing quicker at 8.02% CAGR, thanks to tourism, retail, and co-working space builds. Multi-property hotel operators are increasingly centralizing their procurement processes to standardize guest experiences across their portfolios. This approach often results in large-scale bulk orders that frequently exceed the quantities outlined in standard contracts. Concurrently, corporate office towers are integrating touchless fixtures as part of their efforts to achieve WELL and ESG certifications. This trend is compelling mid-tier suppliers to invest in skill development and technological advancements to meet evolving market demands. The strong correlation between commercial fit-out activities and overall GDP growth underscores the segment's sensitivity to fiscal policies and investment inflows. This relationship introduces an element of cyclicality to the Malaysian sanitaryware market while simultaneously enabling diversification beyond the residential construction cycle. Such diversification positions the market to better withstand fluctuations in specific sectors and leverage opportunities across broader economic developments

Geography Analysis

Central Region delivered 46.83% of 2025 turnover, propelled by Greater Kuala Lumpur’s role as a command hub for finance, government, and high-density housing. Luxury condominiums in Mont Kiara and Bangsar lifted per-unit fixture budgets, while public projects such as school toilet upgrades broadened volume requirements. Johor’s Iskandar corridor reinforced Southern Region demand by attracting Singaporean capital into mixed-use precincts that mandate internationally branded sanitaryware.

The Northern Region leveraged tourism in Penang and Kedah, where heritage hotel restorations require aesthetic, often natural-stone fixtures to match colonial architecture. East Coast states benefited from federal stimulus tied to the East Coast Rail Link, opening secondary cities to chain hotels and branded service apartments. Each new node seeds downstream maintenance and refurbishment business, supporting steady cash flows within the Malaysia sanitaryware market.

East Malaysia demonstrated the highest CAGR of 9.54%, primarily attributed to Sarawak's water-grid program. This initiative has significantly facilitated the development of sanitation infrastructure across rural districts, addressing critical needs and driving regional growth. Suppliers catering to this geography must navigate longer lead times and higher logistics costs, making lightweight, modular products attractive. Compliance oversight by Standards Malaysia and SIRIM ensures uniform quality regardless of region yet also erects entry hurdles for low-spec imports. Together, regional nuances compel producers to field differentiated price-points, installation kits, and after-sales networks, deepening the Malaysia sanitaryware market’s competitive sophistication.

Competitive Landscape

The top players, Claytan Group, Johnson Suisse, TOTO, American Standard, and Roca, controlled a significant share of 2024 sales, forming a moderately consolidated but still contestable oligopoly. Domestic firms lean on proximity advantages, integration with government tender processes, and familiarity with SIRIM standards. Claytan’s first-in-ASEAN fireclay suite and low-flush cisterns exemplify cost-plus-innovation positioning that keeps importers at bay.

International brands leverage R&D scale to roll out rimless bowls, smart bidets, and antimicrobial glazes ahead of local rivals. Yet their higher price band leaves room for niche specialists like Rigel Technology to serve design-build contractors with project-specific customizations. Gamuda IBS’s pod factory lines now pre-install fixtures, locking in preferred suppliers and potentially shifting market power toward those offering pod-compatible SKUs.

Startup activity endures: TMJ Ceramics registered a sanitaryware trademark in 2024, signalling fresh capacity coming online. While import competition from Vietnam and China pressures entry-level price tiers, domestic content policies, especially on public projects, continue to shield a portion of demand. Collectively, strategic thrusts point toward higher technology content, environmental compliance, and digital service integration across the Malaysia sanitaryware market.

Malaysia Sanitaryware Industry Leaders

Roca Malaysia

American Standard (LIXIL)

TOTO Malaysia

Johnson Suisse

Kohler (Malaysia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Malaysian Investment Development Authority confirmed a record RM378.5 billion investment inflow for 2024; a significant share is allocated to greenfield construction projects that will require large-volume procurement of next-generation, water-efficient sanitary fixtures.

- January 2025: TOTO outlined a major expansion program that will triple its overseas showroom count to 300 locations across 63 U.S. cities, reallocating resources from a slowed China real-estate market to faster-growing segments.

- September 2024: Malaysia’s Energy Transition and Water Transformation Ministry (PETRA) launched a digital-innovation roadmap for the water sector that earmarks grants for smart-sensor sanitaryware R&D and pilot deployments.

- April 2024: Topmix Bhd. Initiated an IPO to fund capacity growth in decorative surface products, broadening upstream supply options for premium bathroom and kitchen fit-outs.

Malaysia Sanitaryware Market Report Scope

Sanitaryware, also known as plumbing fixtures or plumbing appliances, refers to any plumbing product that is installed and maintained by a licensed plumber in a bathroom, kitchen, or toilet. The Malaysia Sanitaryware is segmented by product, material, application, end-user, and distribution channel. By product, the market is segmented into water closets, wash basins, pedestals, cisterns, and others. By material, the market is segmented into ceramics, metal, plastics, and others. By application, the market is segmented into kitchen and bathroom. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online, and other distribution channels, and by the end-user, the market is segmented into residential and commercial. The report offers market size and forecasts in value (USD) for all the above segments.

By Product

| Water Closets |

| Wash Basins |

| Pedestals |

| Cisterns |

| Others |

By Material

| Ceramic |

| Porcelain |

| Natural Stone |

| Mosaic |

| Others |

By Application

| Kitchen |

| Bathroom |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online |

| Other Distribution Channels |

By End-User

| Residential |

| Commercial |

By Geography

| Northern Region |

| Central Region |

| Southern Region |

| East Coast |

| East Malaysia |

| By Product | Water Closets |

| Wash Basins | |

| Pedestals | |

| Cisterns | |

| Others | |

| By Material | Ceramic |

| Porcelain | |

| Natural Stone | |

| Mosaic | |

| Others | |

| By Application | Kitchen |

| Bathroom | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| By End-User | Residential |

| Commercial | |

| By Geography | Northern Region |

| Central Region | |

| Southern Region | |

| East Coast | |

| East Malaysia |

Key Questions Answered in the Report

What is the current value of the Malaysia sanitaryware market?

The market is valued at USD 6.78 billion in 2026 and is projected to reach USD 8.93 billion by 2031.

Which product category holds the largest share?

Water Closets lead with 41.73% of 2025 revenue, underscoring their core role in all residential and commercial projects.

Which region is growing the fastest?

East Malaysia shows the highest 9.54% CAGR, driven by rural water-grid expansion and federal infrastructure spending.

How quickly are online channels expanding?

Online sales are growing at a 12.48% CAGR as logistics improvements and bundled installation services boost customer confidence.

Which material segment is disrupting ceramics?

Natural Stone and Mosaic products are rising at 9.21% CAGR, fueled by premium hotel refurbishments and upscale home projects.

What is the outlook for commercial demand?

Commercial applications, propelled by hospitality and office projects, are forecast to expand at an 8.02% CAGR through 2031.

Page last updated on: